36

IOBOA PROMOTION MATERIAL ON Government Sponsored Schemes By Jeetendra Kumar Panda VIDEO CLASS LINK: Click Here

IOBOA PROMOTION MATERIALON

Government Sponsored Schemes

By Jeetendra Kumar Panda

VIDEO CLASS LINK: Click Here

Topics covered

1. PMMY2. PMEGP I3. PMEGP II4. Stand-up India Scheme5. NRLM6. NULM7. SRMS8. DRI9. NEFS10.Laghu Udyami Credit Card Scheme (LUCC)

Government Sponsored Schemes

PMMY (Prime Minister’s Mudra Yojana)• MUDRA stands for Micro Units Development Refinance Agency

• Mudra loans can be given bya. Commercial Banks

b. Regional Rural Banks

c. Small Finance Banks

d. Micro Finance Institutions

e. Non-banking Finance Companies

• Funding support from MUDRA are two types :

Micro Credit Scheme for loans up to Rs. 1 lakh through MFI.

Refinance scheme for Commercial Banks, RRBs, SFBs & NBFCs .

• Loan can be applied though Udyami Mitra portal orPSBloansin59minutes.com portal

PMMY (Prime Minister’s Mudra Yojana)

• MUDRA eligibility norm for refinance for PSBsNet NPA – Should not exceed 15%

CRAR – As stipulated by RBI

Net worth - Above Rs. 250 Cr

• Interest rate cap for Mudra Loan for availing Refinance:

Banks – Max at Base rate / MCLR rate

RRBs – 3.50% over and above refinance rate

NBFCs- 6% over and above refinance rate

MFIs – margin cap of 10% for MFIs having portfolio >100 cr

margin cap of 12% for MFIs having portfolio <100 cr

or 2.75 times average base rate of 5 major

commercial banks (whichever is less)

PMMY (Prime Minister’s Mudra Yojana)

• Loans up to Rs. 50000 – Sishu

• Loans above Rs. 50000 and up to Rs. 500000 – Kishore

• Loans above Rs. 500000 and up to Rs. 1000000 - Tarun

• Mudra Debit Card can be given @20% of the limit.Mudra loan max Max limit

@20%ATM ECOM POS

50000 (Sishu) 10000 2000 1500 1500

500000 (Kishore) 100000 20000 10000 10000

1000000 (Tarun) 200000 20000 40000 40000

Per Day limit

Interest Subvention of 2% is available for Non NPA MUDRA Sishu Loans as follows :1. For Mudra loans who availed Moratorium, Interest subvention available for 12 months

period i.e. 1st September 2020 to 31st Aug 2021.2. For other borrowers from 1st June 2020 till 31st May 2021.

PMEGP I• Prime Ministers Employment Generation Programme

introduced by merging 2 schemes PMRY & REGP.

• Scheme is implemented by KVIC at National Level and at statelevel it is implemented by state KVIC Directorates, KVIBs & DICs.

• Maximum Project Cost :

Manufacturing Services

25 lakhs 10 lakhs

VIII Pass Required > 10 lakhs > 5 lakhs

• No Educational Qualification Required

• No Family Income Criteria

• Min Age 18 Years

• One person from Family (Family means only Husband and Wife)

PMEGP I

Particulars Margin Rate Of Subsidy

Location of Project Urban Rural

General Category 10% 15% 25%

Special Category 5% 25% 35%

• Project cost will include One cycle of Working Capital.• Working Capital component should be utilized not less than

75% of sanctioned limit and at least once 100% within 3 year ofthe lock-in period. If not then proportionate amount has to bereturned to KVIC.

• District level task Force Committee has been discontinued.• KVIC, KVIB or DICs has to forward the application to banks not

later than 3 weeks of receipt of application.

PMEGP I

• EDP Training is compulsory before release of the facilities.

• Collateral security can be taken for the loans above 10 lakhshowever for loan amount up to 10 lakhs no collateralsecurity to be taken.

• Margin Money received should be kept in the form of TDRfor 3 Years, No interest will be charged on loan disbursed tothe corresponding amount of TDR. No interest also to bepaid on TDR.

• If loan becomes bad before 3 years, due to the reasonbeyond the control of beneficiary, the margin money will bereturned to KVIC along with interest.

• As per PMEGP Scheme, any Town if the population doesn’texceed 20000 persons will be classified as Rural Area.

PMEGP I

• Negative list of activities:1. Any industry/business connected with Meat(slaughtered),i.e. processing, canningand/or serving items made of it as food, production/manufacturing or sale ofintoxicant items like Beedi/Pan/ Cigar/Cigarette etc., any Hotel or Dhaba or salesoutlet serving liquor, preparation/producing tobacco as raw materials, tapping oftoddy for sale.

2. Any industry/business connected with cultivation of crops/ plantation like Tea,Coffee, Rubber etc. sericulture (Cocoon rearing), Horticulture, Floriculture, AnimalHusbandry like Pisciculture, Piggery, Poultry, Harvester machines etc.

3. Manufacturing of Polythene carry bags of less than 20 microns thickness andmanufacture of carry bags or containers made of recycled plastic for storing,carrying, dispensing or packaging of food stuff and any other item which causesenvironmental problems.

4. Industries such as processing of Pashmina Wool and such other products likehand spinning and hand weaving, taking advantage of Khadi Programme under thepurview of Certification Rules and availing sales rebate.

5. Rural Transport (Except Auto Rickshaw in Andaman & Nicobar Islands, HouseBoat, Shikara & Tourist Boats in J&K and Cycle Rickshaw).

PMEGP -II

• All existing units financed under PMEGP/MUDRA Schemewhose margin money claim has been adjusted and the first loanavailed should have been repaid in stipulated time are eligibleto avail the benefits.

• The unit should have been making profit for the last three years.

• Beneficiary may apply to the same financing bank, whichprovided first loan, or to any other bank, which is willing toextend credit facility for second loan.

• Registration of Udyog Aadhaar Memorandum (UAM) ismandatory.

• The 2nd loan should lead to additional employment generation.

PMEGP -II

• Maximum cost of the project/unit admissible undermanufacturing sector for up-gradation is Rs.1.00 Crore, and themaximum subsidy would be Rs.15 lakhs (Rs.20 lakhs for NERand Hill States).

• The maximum cost of the project/unit admissible underService/Trading sector for up-gradation is Rs.25 lakhs, and themaximum subsidy would be Rs. 3.75 lakhs (Rs. 5 lakhs for NERand Hill States).

PMEGP -II

• Under the term loan component (construction ofbuilding/industrial shed, machinery & equipment etc.),the construction of own building may be included andceiling of construction should not usually exceed 25% ofthe total sanctioned project cost.

• The capital expenditure component including cost ofconstruction should be up to 60% of the total projectcost. The working capital cost would be up to40%.However, the financing bank can decide thecriteria at the time of sanction of loan based on thenature of the project.

PMEGP -II

• The Margin Money Subsidy will be kept as Term DepositReceipt (TDR) for 18 months.

• No interest will be paid on the TDR and no interest willbe charged on the corresponding amount of the loandisbursed.

• The TDR amount will be adjusted in the loan accountafter installation of the machinery and on the basis ofpositive report of a joint physical verification of theimplementing agency and the Bank.

Stand-up India Scheme

Target Group:

• At least 1 SC or ST borrower and at least one women borrower per

bank branch. In case of non-individual enterprise at least 51% of the

share holding and controlling stake should be held by either SC/ST

or women entrepreneur.

Purpose:

• For setting up a green field enterprise ( new enterprise)

Eligible activity :

• The enterprise may be in manufacturing , service including trading.

Recently Activities allied to agriculture, Food and Agro processing

and services supporting are included in the eligible activity.

Stand-up India Scheme

Quantum

• Above Rs. 10 lakhs – up to Rs. 100 Lakhs.

Margin

• Minimum margin of 15% out of which minimum 10% should befrom promoters own contribution. Remaining margin moneycan be provided in convergence with eligible central / stateschemes.

Repayment

• Term Loan – Repayment up to 7 years with a holiday period of18 months. CC payable on Demand . Limits are subject toannual review.

Security

• Collateral Security / third part guarantee can be obtained as perthe policy.

DAY- NRLM

Deendayal Antyodaya Yojana-National Rural Livelihood Mission.

• Beneficiary - Women SHG consists of 10 to 20 persons.

• In case of Special SHGs i.e. groups in difficult areas, groups withdisabled persons and group form tribal areas This number maybe min 5.

• Both Men and Women allowed in the SHG only when the groupis formed with persons with Disabilities, Elders, transgenders .

• SHG is a informal group, so registration is not mandatory,however federation of SHGs formed in village, panchayats,cluster or higher levels may be registered under appropriateacts prevailing in their respective states.

DAY-NRLM

Revolving Fund :

• Minimum 10000 and maximum up to 15000 per SHG

• SHG should have min 3/6 months existence and followPanchasutra.

a) Regular Meeting

b) Regular Saving

c) Regular internal Lending

d) Regular recovery

e) Maintenance of proper books of accounting.

• Only those SHGs with more than 70% BPL members are eligiblefor RF.

• No capital subsidy available as per the scheme.

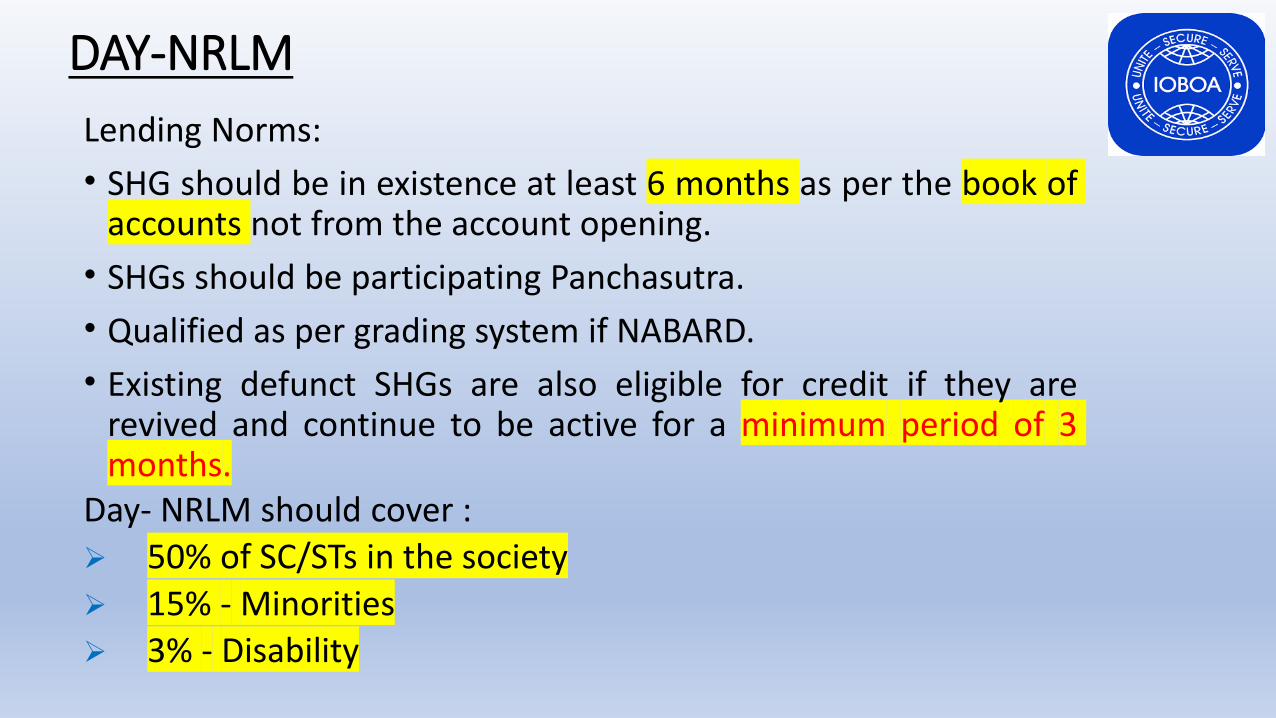

DAY-NRLM

Lending Norms:

• SHG should be in existence at least 6 months as per the book ofaccounts not from the account opening.

• SHGs should be participating Panchasutra.

• Qualified as per grading system if NABARD.

• Existing defunct SHGs are also eligible for credit if they arerevived and continue to be active for a minimum period of 3months.

Day- NRLM should cover :

➢ 50% of SC/STs in the society

➢ 15% - Minorities

➢ 3% - Disability

DAY-NRLM

Loan amount :

Type of loan 1st year/1st linkage

2nd year/2nd linkage

(whichever is later)

3rd year/3rd linkage

(whichever is later)

4th year / 4th linkage

(whichever is later)

Cash Credit 6 times/ Min 1 Lakh

8 times/ Min 2 lakhs

Min 6 Lakhs/ according to Micro Credit Plan

> 6 lakhs / according too Micro Credit Plan

Term Loan 6 times/ Min 1 Lakh

8 times/ Min 2 lakhs

Min 6 Lakhs/ according to Micro Credit Plan

> 6 lakhs / according too Micro Credit Plan

1st Dose to be repaid in 24 to 36months

2nd Dose to be repaid in 36 to 48months

3rd Dose to be repaid in 48 to 60 months

4th Dose to be repaid in 60 to 84months

DAY-NRLM

Above 2 lakhs – 50%

Above 4 lakhs – 75%

Above 6 lakhs – 85%

To be used primarily for income generating/ Productive purpose.

Security and Margin :

No Collateral Security up to loan amount Rs. 10 lakhs.

No lien on SB account of SHG and No deposit to be insisted forsanctioning loans.

NIL Margin for loan amount up to 10 lakhs.

DAY-NRLM

Interest Subvention :

• Interest subvention is available in 2 ways :

Identified 250 Districts :

• All women SHGs will be eligible for a regular interest subventionon a credit limit up to Rs.3 lakhs. The interest subvention isdifference between lending rate of the banks and 7% which iscapped at 5.50%

• Additional interest subvention of 3% is also available on promptrepayment by SHG. Reducing the effective rate of interest to4%.

• Both regular and additional interest subvention claim is donequarterly by banks.

DAY-NRLM

Other Districts :

• All women SHGs will be eligible for a regular interestsubvention on a credit limit up to Rs.3 lakhs. Theinterest subvention is difference between lending rateof the banks and 7% which is capped at 5.50%

• No additional interest subvention available with promptrepayment.

Prompt Repayment :

Term Loan :

All interest/ instalment payment should be paid within30 days of the due date

DAY-NRLM

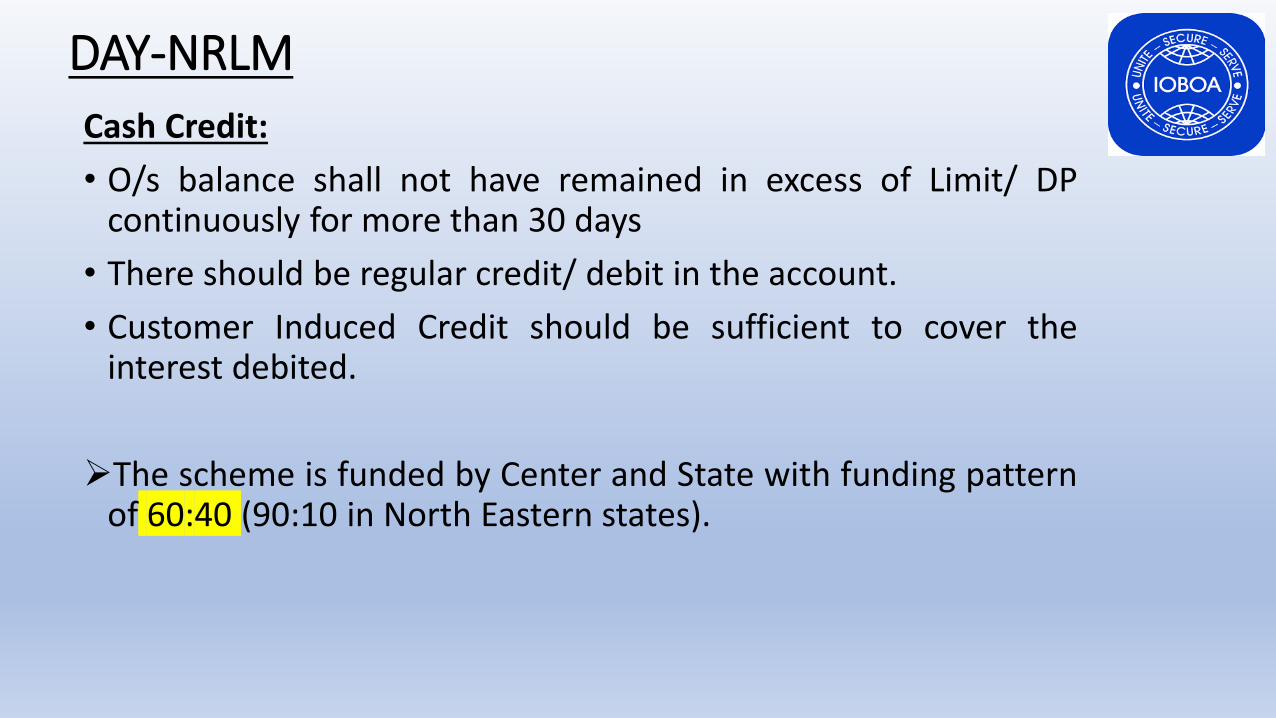

Cash Credit:

• O/s balance shall not have remained in excess of Limit/ DPcontinuously for more than 30 days

• There should be regular credit/ debit in the account.

• Customer Induced Credit should be sufficient to cover theinterest debited.

➢The scheme is funded by Center and State with funding patternof 60:40 (90:10 in North Eastern states).

DAY-NRLM

Dealing with Defaulters:

➢Banks should not deny the loan due to defaulter of members in

the group

➢In case of willful defaulters, benefit of thrift deposit, revolving

fund and Income from Credit activities available

➢No benefits from bank loans till the bank dues are paid off

➢Non-willful defaulters should not be barred from loan and can

be considered on case to case basis.

DAY-NULM

Deendayal Antyodaya Yojana – National Urban LivelihoodMission.• Launched by Ministry of Housing and Urban poverty

Alleviation.• The Scheme Covers loans to Individuals (SEP-I) and

loans to group enterprises (SEP-G) and SHG Groups.• The project is implemented by Urban Local Bodies,

Municipality Committee and hence selection ofbeneficiaries done by them.

• No educational qualification required• EDP is arranged by ULBs.

DAY-NULM

SEP-I (Self Employment Programme for Individuals):

Eligibility : Any Urban poor for setting up a microenterprises for self employment.

Age- Min 18

Project Cost- Max 2 lakhs

Collateral – Nil

Margin – Up to 50000 – Nil and above it 5 to 10%.

Repayment – 5 to 7 years after initial holiday period of 6to 18 months.

DAY-NULM

SEP-G (Self Employment Programme for Groups):

Eligibility : The Group Enterprise should have minimum 3members with a min 70% from Urban poor families.

Age- all members should be more than 18 years age.

Project Cost- 2 lakhs per member or 10 lakh whichever islower.

Collateral – Nil

Margin – Up to 50000 – Nil and above it 5 to 10%.

Repayment – 5 to 7 years after initial holiday period of 6to 18 months.

DAY-NULM Target under the scheme :• Minimum women beneficiary – 30%• SC/ST should be benefited at least to the extent of the

proportion of their strength in the city/ town population ofpoor.

• 3% for differently-able (PWDs)• 15% for minority communityInterest Subvention :• Interest subvention available for the difference amount

between the interest rate charged by bank and 7%.• Additional interest subvention of 3% available for Women

SHGs who repay their loan on time.

SRMS

Self Employment Scheme for Rehabilitation of ManualScavengers :

Manual Scavenger means a person who is locallyengaged for manually cleaning and disposing the wastes.

Cash Assistance: The identified manual scavengers, onefrom each family would be receiving cash assistance of40000 immediately after identification which can beallowed to withdraw in monthly instalment of Rs. 7000.

Project Cost- Rs. 10 lakhs- for any activities

Rs. 15 lakhs – for sanitation related activity

SRMS

Range of Project Cost Rate of Subsidy

Up to 2 lakhs 50% of the Project Cost

>2 lakh to 5 lakhs 1 lakh + 33.3% of PC

>5 lakhs to 10 lakhs 2 lakhs + 25% of PC

> 10 lakhs to 15 lakhs 3.25 lakhs

• Interest Subsidy : Gap between the interest charged bybank and interest rate as per the scheme.

• For Project Cost up to 25000 – 5% (For women-4%)

• For Project Cost above 25000 – 6%

SRMS

Moratorium Period : up to 2 years

Repayment period including the moratorium period :

For project cost up to 5 lakhs – 5 year

For project cost more than 5 lakhs – 7 years.

Maximum period of Training – 2 Years

Stipend during the training – 3000/ pm

DRI

Differential Rate of Interest Scheme:

Purpose : To assist the poorest of poor and bring themabove the poverty line.

Eligibility : individuals whose family income does notexceed 18000 pa in Rural and 24000 in Urban and SemiUrban areas.

Applicable : All over India

Quantum : 15000 for productive purpose

20000 for housing (only for SC/ST)

Additional 5000 for Disabled persons.

DRI

Target – Minimum 40% to SC/ST

2/3rd

to be routed through Rural and Semi

Urban branches.

No target for Women Entrepreneurs.

Subsidy : NIL

Margin- NIL

Security – No Collateral

Rate of Interest – 4% Simple

Repayment – Max 5 Yrs including 2 yrs HP.

Classified under Weaker Section category of PSL.

NEFS

National Equity Fund Scheme:

Purpose – To provide equity support to entrepreneurs forsetting up tiny/ small units, or expansion of existingunits.

Project Cost- Up to 50 lakhs

Margin – 10% of Project Cost

Equity assistance – 25% of PC or 10 lakhs whichever islower.

Security – Nil

Repayment – 7 yrs including moratorium 3 yrs.

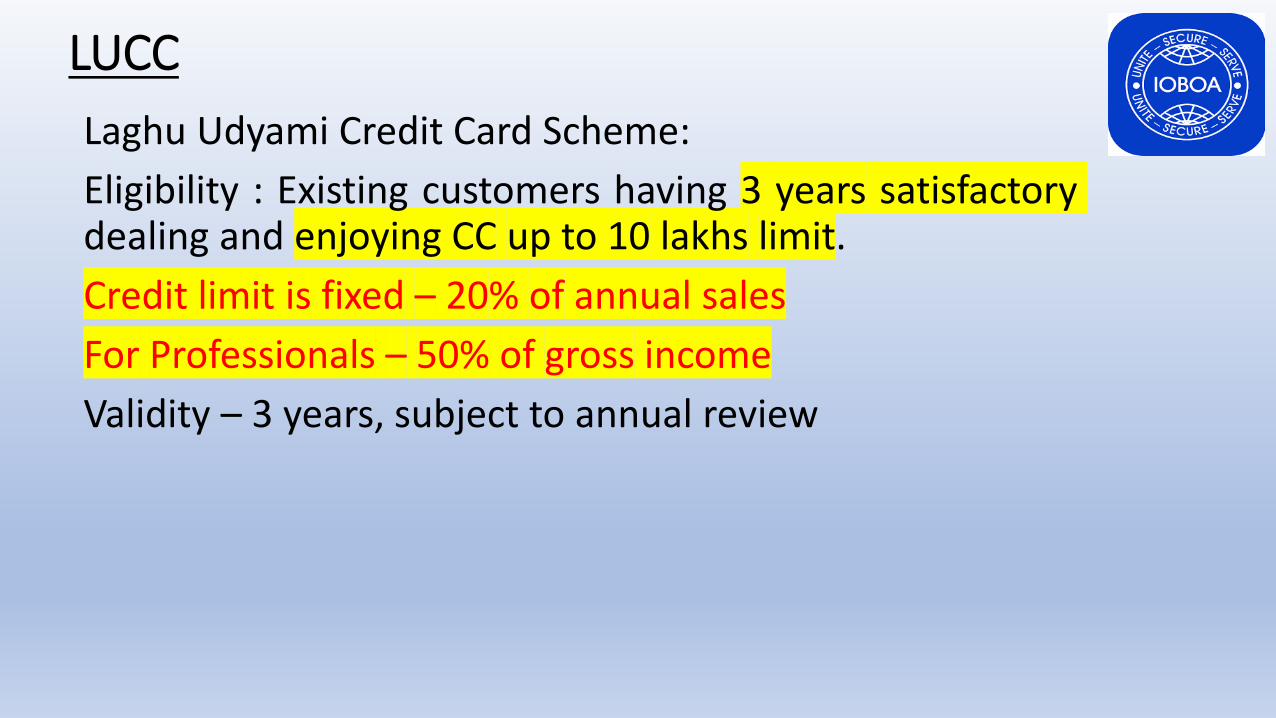

LUCC

Laghu Udyami Credit Card Scheme:

Eligibility : Existing customers having 3 years satisfactorydealing and enjoying CC up to 10 lakhs limit.

Credit limit is fixed – 20% of annual sales

For Professionals – 50% of gross income

Validity – 3 years, subject to annual review