34

Iranian Gas Prospect H.E S.R.Kassaeizade Deputy Oil Minister and Managing Director of NIGC Presented by Turkey June.2008

| Date post: | 24-Dec-2015 |

| Category: |

Documents |

| Upload: | andra-cross |

| View: | 214 times |

| Download: | 0 times |

Iranian Gas Prospect

H.E S.R.Kassaeizade Deputy Oil Minister and Managing Director of NIGC

Presented by

Turkey June.2008

Iranian Gas Prospect

A Regional Perspective

Overview• NIGC Organization 2008 • Natural Gas Refineries & Dehydration Units• Iran In 2007• NIGC Transmission Systems• Pipeline Projects• Compressor Stations Plans• Underground Gas Storage Projects• Gas Treatment Capacity• LNG Production• Investment on Gas Infrastructure• Achievements in 2025• Advantages for Iranian Gas Market

NIGC Organization 2008

Oil Ministry

NIOC NIGC NPCNIORDC

44 Sub Companies

8 Gas Ref. Co.

30 Province Gas Co.

UGS Co.

Eng & Dev Co.

.Transmission Co

CNGCo.

Commercial Co.

TMS

Fajr

Hashemi nejad

Ilam

South Pars

Parsian

Sarkhon

Masjed Soleyman

In OperationPlan

Gavarzin

Sarajeh

Shorijeh

Gonbadly

Dalan

Refinery

Dehydration units

Natural Gas Refineries & Dehydration Units

Bidboland I

Caspian Sea

Bidboland II

South Gasho

Natural Gas Production*(2001-2012)

77 87 100 106117 132

180 180195

247274

0

50

100

150

200

250

300

BC

M

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

(*Received Natural Gas From NIOC)

Iran’s Share in the World Natural Gas Production (2007)

21.4

2.8

2.953

3.7 6.5

18.3

Russian

USA

Canada

Iran*

Norw ay

Algeria

United Kingdom

132 BCM

68 7886 98 103 109 123

155 174205

245277

0

50

100

150

200

250

300

BC

M

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Domestic Natural Gas Sales (2001-2012)

3.43.23

32.72.6

2.3

22

3.7

16.8

USA

Russian

Iran*

Canada

United Kingdom

Germany

Japan

Italy

Saudi Arabia

Ukraine

Iran’s Share in the World Natural Gas Consumption (2007)

132 BCM

Iran in 2007• High pressure Gas Transmission pipelines 28000 Km

• Gas Distribution Networks 150000 Km

• No. of Natural Gas Consuming Cities 660

• No. of Natural Gas Consuming Rural Areas 5700

• Natural Gas Consuming Population 76%

• Share of Natural Gas in fossil fuels Basket 61%

• No. of Natural Gas Consuming Industries 18000

• Export 5.6 BCM

• Import 6.2 BCM

Top 5 Gas Reserves

Russia

Iran

Saudi Arabia

United Arab Emirates

Qatar

48

28

25

6

7TCM

Natural Gas Sector Breakdown in 2007

37, 30%

31.5, 26%

54, 44%

Residential

Power Plants

Industries

BCM)%(

Principle 44 of I.R.of Iran Constitution

All oil and Gas related activities except for Oil Industry Upstream will be privatized and offered to private sector. Principle 44 concerns with privatization of the natural gas market and thus formation of a financially stable and transparent markets, so as to ensure supply of good-quality natural gas at competitive prices to consumers . Iranian gas market will be opened to foreign investors as well.

NIGC Transmission Systems (Under Implementation)

• IGAT- V• IGAT- VI• IGAT- VII• IGAT- VIII• IGAT- IX• IGAT- X• IGAT- III Last segment (Saveh-Qazvin-Rasht)• North-Northeast Pipeline• Northwest Pipeline

IGAT 5• Length 504 km

• Diameter 56 inches’

• Capacity 95 MCM/D

• Investment 2000 millions

USD

• Compressor St. 5

• Commencement date 2008

IGAT 6• Length 510 km

• Diameter 56 inches’

• Capacity 95 MCM/D

• Investment 900 millions

USD

• Compressor St. 5

• Commencement date 2008

IGAT 7• Length 902 km

• Diameter 56 inches

• Capacity 110 MMCM/D

• Investment 2 billions

USD

• Compressor St. 2

• Commencement date 2009

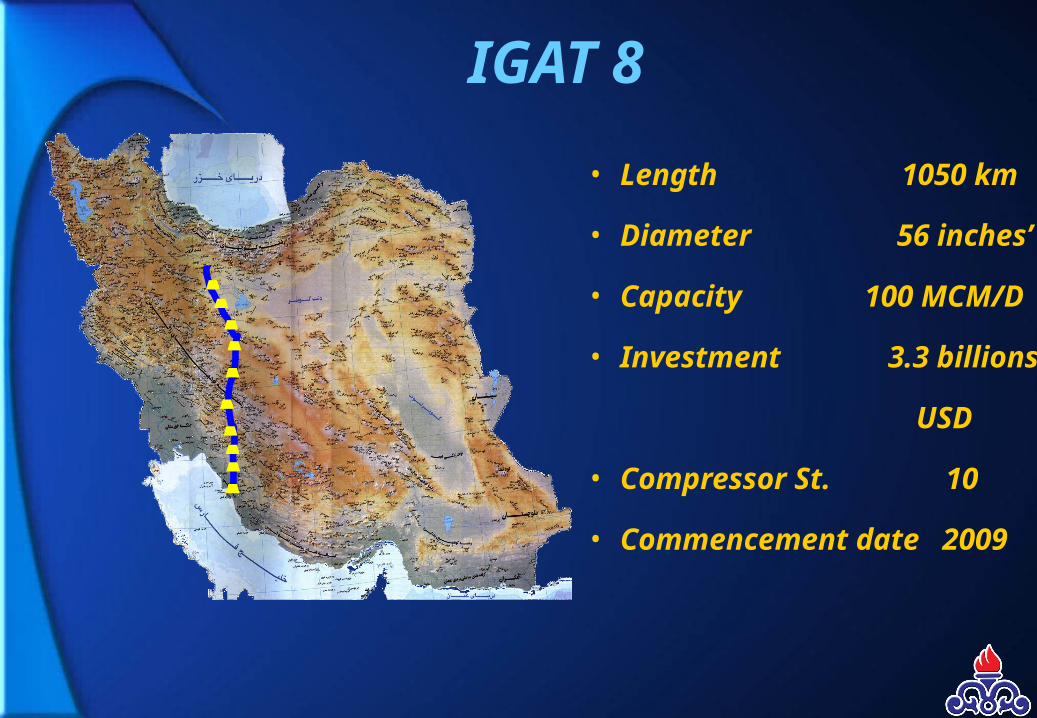

IGAT 8

• Length 1050 km

• Diameter 56 inches’

• Capacity 100 MCM/D

• Investment 3.3 billions

USD

• Compressor St. 10

• Commencement date 2009

IGAT 9

• Length 1860 km

• Diameter 56 inches’

• Capacity 110 MMCM/D

• Investment 8 billions USD

• Compressor St. 17

• Commencement date 2014

IGAT 10

• Length 824 km

• Diameter 56 inches’

• Capacity 65 MMCM/D

• Investment 635 millions

USD

• Compressor St. 4

• Commencement date 2009

)IGAT III(Last segment (Saveh-Qazvin-Rasht)

• Length 237 km

• Diameter 56 inches’

• Investment 500 millions

USD

• Source of gas South Pars

• Commencement date 2009

North-Northeast Pipeline

• Length 790+105 km

• Diameter 48,42 inches’

• Investment 1.5 billions

USD

• Compressor St. 6

• Commencement date 2009

Northwest Pipeline

• Length 280 km ,190 km

• Diameter 48,40 inches’

• Investment 750 millions

USD

• Compressor St. 3

• Commencement date 2008

NIGC Transmission Systems

Caspian Sea

Persian Gulf

IGAT V

IGAT VI

IGAT X

IGAT IX

IGAT IV

IGAT VIII

IGAT VII

�ُSarakhs-Neka-Rasht

IGAT X

IGAT XI

Parchin-Mashhad

IGAT III

IGAT I

IGAT II

AZAR I

AZAR II

AZAR III

Pipeline Projects)2005-2025(

Facilities4th Plan5th plan6th Plan7th PlanTotal

(2025)

Major Pipelines4,6,7,8,99,10,11,1213,1415,16-

40 to 56 inches Pipelines (km)

8262111055100510029567

Other Pipelines (km)8923119945511551031938

Total Length (km)1718023100106001060061500

Compressor Stations Plans )2005-2025(

Facilities4th Plan5th plan6th Plan7th Plan

Total(2025)

Compressor Stations(NO.)

35403530140

Underground Gas Storage Projects

No. of Storages 3

Operating capacity 60 MMSCMD

(3 Months)

Investment USD 560 Million

Gas Treatment Capacity (Under Implementation)

Refinery Capacity(MMSCMD) Commencement date

Bidboland-II 57 2011

Ilam (Expansion) 3.4 2010

South Pars (Phases 6,7,8) 100 2008

South Pars (Phases 9,10) 50 2008

South Pars (Phases15,16,17,18) 100 2012

South Pars (Phases 19,20,21) 80 2013

South Pars (Phases 22,23,24) 40 2014

LNG Production

Projects Capacity (mt/y) Commencement date

• Iran LNG 10 2011

• Pars LNG 10 2012

• Persian LNG 16.2 2013

Investment in 2007

Plans and Projects under implementation

)Downstream(

(28 Billions USD)

Investment on Gas Infrastructure (2005-2025)

(Downstream)

Section4th Plan5th plan6th Plan7th PlanTotal

(2025)

Distribution45.34770.285247.5

Transmission(Pipelines,Compressor stations)

107.6163.8126.1127.2524.6

Refinery & Underground Storage

56.746.757.259.7203.9

Staff7.41131.3154.2204

TOTAL (1000 Billion Rials(

201218.7305421.71172.6

TOTAL(USD Billions(22293147129

1000 billions Rls

Achievements in 2025

• The second natural gas producer in the world

• 10 percent share in global natural gas trade, through pipeline or by LNG

• Domestic pricing deregulation on the track

• Natural gas, dominant energy as feed stock and fuel

• Privatization based on principle 44 of constitution completely achieved