9

Updates and best practices for a changing regulatory environment IRAs & the ERISA fiduciary rules

| Date post: | 20-Aug-2015 |

| Category: |

Business |

| Upload: | broadridge |

| View: | 197 times |

| Download: | 2 times |

Updates and best practices for a changing regulatory environment

IRAs & the ERISA fiduciary rules

2

IRAS & THE ERISA FIDUCIARY RULES | EXECUTIVE SUMMARY

EXECUTIVE SUMMARY

Interplay of ERISA Fiduciary Rules & IRA Rollovers

The Department of Labor’s (DOL’s) proposed changes to the fiduciary definition regulations have been the subject of heated debate in our industry over the last few years – causing many advisors to re-examine their business model and analyze whether they are a fiduciary to the plan (and participants) today vs. under the anticipated re-proposed regulations.

The fiduciary conversation has taken an interesting turn in recent months. Much of the discussion has focused on speculation about the potential impact the anticipated regulations could have on Individual Retirement Accounts (IRAs). Why has this become such a big concern? A significant amount of retirement savings dollars are held in IRAs – more than $5.7 trillion dollars as of March 31, 2013 (The U.S. Retirement Market, First Quarter 2013 (ICI)), representing more than 25 percent of retirement savings assets. And this number is expected to grow as baby boomers retire. IRAs are an important component of many advisors’ growth strategy.

The current debate regarding IRAs is focused on how the expanded fiduciary definition will be applied to IRAs:

• Will advising a participant to make a rollover from an employer plan result in ERISA fiduciary status?

• Will investment advice provided to IRA holders be considered “investment advice for a fee” under the same definition as employer plans such as 401(k) plans?

• Will the rules apply both to broker-dealers and registered investment advisors (referred to collectively as “advisors” in this Practice Guide)?

While we don’t know what the re-proposed fiduciary definition regulation will look like, most industry experts anticipate a broader definition of “fiduciary” that will result in more broker-dealers and registered investment advisors becoming ERISA fiduciaries. Activities that today are considered non-fiduciary investment support or education for plan sponsors and participants may be considered fiduciary activity under the DOL regulations expected to be released later in 2013.

Given public comments by Assistant EBSA Secretary Phyllis Borzi, it is likely that the expanded fiduciary definition will also have an impact on how advisors work with IRAs. Advisors may be considered an ERISA fiduciary for investment support activities relating to IRAs and IRA rollovers that today are considered non-fiduciary activities. Ultimately, this means that unless a prohibited transaction exemption is available, an advisor’s business model and compensation structures may need to change if they work with IRAs – or the advisor may be engaged in a prohibited transaction.

Some industry commenters and members of Congress have argued that applying the fiduciary rules to IRA activity without sufficient prohibited transaction exemptions could have a chilling effect on individuals’ access to IRA financial advice, particularly with small rollover balances.

3

IRAS & THE ERISA FIDUCIARY RULES | EXECUTIVE SUMMARY

Expanded IRA DebateThe IRA rollover debate is a complex one that cuts across several regulatory agencies – DOL, IRS, SEC, and FINRA. IRAs have also captured the attention of Congress. The Government Accountability Office (GAO) increased attention to the IRA rollover issue with its March 2013 report entitled 401(k) Plans: Labor and IRS Could Improve Rollover Process for Participants. In the report, the GAO criticized service providers for encouraging IRA rollovers when a rollover may not have been in the best interests of the participant, in some cases by using misleading or incomplete information.

The GAO report played a big role in expanding the IRA rollover debate to explore whether additional support is needed to help plan participants make more informed IRA rollover decisions. Suggestions from the GAO and others include:

• Providing participants who are eligible for a rollover a concise written summary explaining a participant’s distribution options, including the option to roll assets to a new employer plan, and listing key factors a participant should consider when comparing possible investments.

• Mandating expanded fee information for IRAs similar to the disclosures now required under the ERISA 404a-5 regulations for participant-directed plans.

Scope of this Practice GuideThe purpose of this Practice Guide is to provide a framework to help advisors understand this fast-evolving issue by addressing the following questions:

• What are the rules today?

• What is being proposed?

• How would some of the proposed changes impact an advisor’s practice?

• Are there any action steps an advisor can take today in anticipation of the new rules?

4

IRAS & THE ERISA FIDUCIARY RULES

Current Rules – Under the current law and regulations,

• An advisor who is not otherwise a plan fiduciary does not become an ERISA fiduciary merely because they are advising plan participants regarding rollovers, even if the advisor will receive compensation if the assets are rolled to an IRA (DOL Advisory Opinion 2005-23A).

• If an advisor is a fiduciary to the plan, however, rollover advice potentially gives rise to a prohibited transaction because the fiduciary is providing guidance that can potentially increase their compensation.

Proposed DOL Changes – In 2010, the DOL proposed changes to the definition of who is considered a fiduciary under ERISA Section 3(21) as a result of providing investment advice for a fee.

• The DOL proposed modifying the current five-part test by eliminating the requirement that the advice be provided on a “regular basis” and that the advice be the “primary basis” for the investment decisions. These two changes would significantly expand the group of advisors who would be considered ERISA fiduciaries based on providing investment advice.

• The DOL also asked for comments as to whether advising plan participants regarding rollovers should be subject to a fiduciary standard.

Re-proposed fiduciary definition regulations are expected later in 2013. While we do not know at this time what will be included in the re-proposed regulations, given public comments made by Assistant Secretary Phyllis Borzi, most industry commenters believe there will be a broader definition of advisor activities that will result in fiduciary status and that the regulations will clarify how that broader fiduciary standard applies to IRAs – particularly IRA rollovers. Assistant Secretary Borzi has also indicated that the re-proposed regulations will be accompanied by a robust economic analysis and a list of proposed exemptions to types of transactions prohibited by the regulations.

The Changing IRA LandscapeLet’s begin by sizing up the IRA rollover opportunity. According to estimates by the ICI, at the end of first quarter 2013, defined contribution plans held more than $5.4 trillion, and IRAs held more than $5.7 trillion of the estimated $20.8 trillion in total retirement assets.

A substantial portion of these IRA assets originated in an employer retirement plan or other retirement arrangement that was rolled over to the IRA. Rollovers from employer plans to IRAs that occur when people change jobs or retire are the greatest source of dollars flowing into IRAs. It is estimated that 10,000 baby boomers (born between 1946 and 1964) turn 65 each day. With more than 78 million baby boomers expected to retire over the next 20 years, most industry experts anticipate substantial growth in IRAs. Capturing these rollovers and incorporating them into a retirement income strategy is an important practice focus for many advisors.

Regulatory Environment For Advisors

IRAs Snared in the ERISA Fiduciary Regulations DebateIRAs are subject to the same prohibited transaction rules as employee retirement plans, although the underlying statutory basis is Internal Revenue Code Section 4975 rather than ERISA. The IRS has primary responsibility for ensuring that IRAs and employer plans follow the requirements set forth in the Internal Revenue Code. However, by agreement between the Treasury Department and the DOL under Section 2 of the Reorganization Plan of 1978, the interpretation and rulemaking authority for prohibited transactions under both ERISA and the Internal Revenue Code were consolidated and transferred to the DOL. The IRS retained the responsibility to enforce the tax laws and impose excise taxes on prohibited transactions.

IRAs Are a Big Source of Retirement Savings ...and Getting Bigger

With more than 78 million baby boomers expected to retire over the next 20 years, most industry experts anticipate substantial growth in IRAs.

5

IRAS & THE ERISA FIDUCIARY RULES

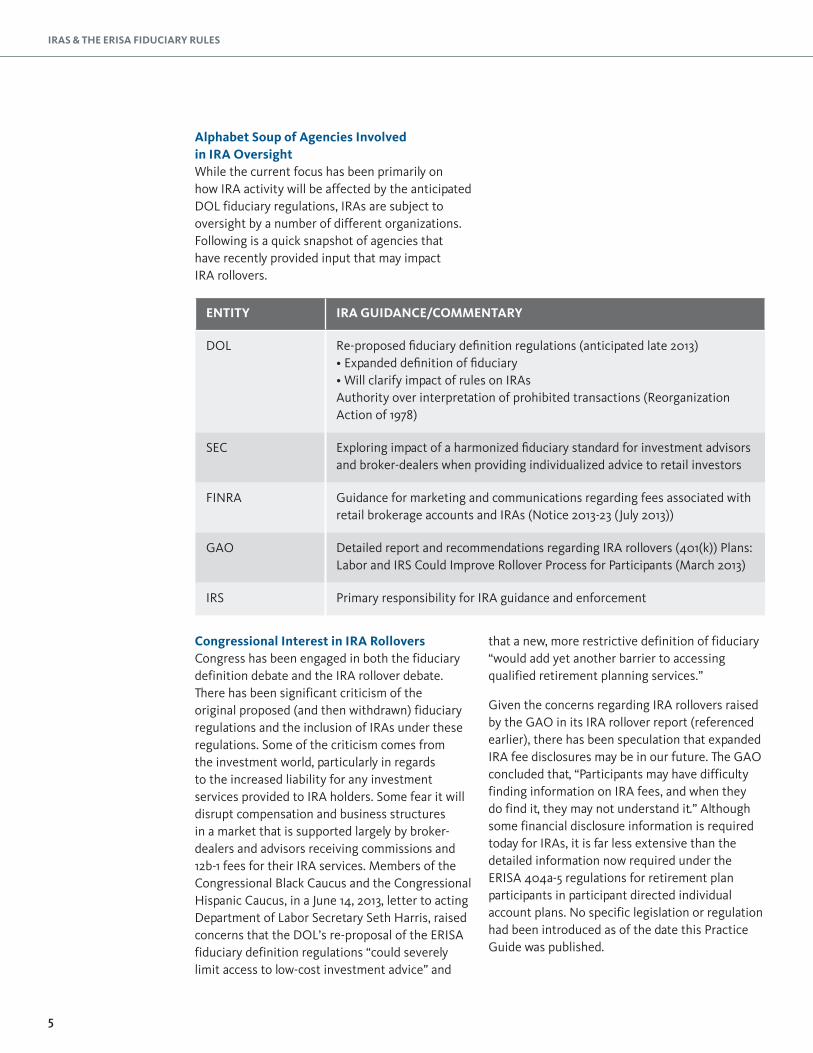

ENTITY IRA GUIDANCE/COMMENTARY

DOL Re-proposed fiduciary definition regulations (anticipated late 2013)• Expanded definition of fiduciary• Will clarify impact of rules on IRAsAuthority over interpretation of prohibited transactions (Reorganization Action of 1978)

SEC Exploring impact of a harmonized fiduciary standard for investment advisors and broker-dealers when providing individualized advice to retail investors

FINRA Guidance for marketing and communications regarding fees associated with retail brokerage accounts and IRAs (Notice 2013-23 (July 2013))

GAO Detailed report and recommendations regarding IRA rollovers (401(k)) Plans:Labor and IRS Could Improve Rollover Process for Participants (March 2013)

IRS Primary responsibility for IRA guidance and enforcement

Alphabet Soup of Agencies Involved in IRA OversightWhile the current focus has been primarily on how IRA activity will be affected by the anticipated DOL fiduciary regulations, IRAs are subject to oversight by a number of different organizations. Following is a quick snapshot of agencies that have recently provided input that may impact IRA rollovers.

Congressional Interest in IRA RolloversCongress has been engaged in both the fiduciary definition debate and the IRA rollover debate. There has been significant criticism of the original proposed (and then withdrawn) fiduciary regulations and the inclusion of IRAs under these regulations. Some of the criticism comes from the investment world, particularly in regards to the increased liability for any investment services provided to IRA holders. Some fear it will disrupt compensation and business structures in a market that is supported largely by broker-dealers and advisors receiving commissions and 12b-1 fees for their IRA services. Members of the Congressional Black Caucus and the Congressional Hispanic Caucus, in a June 14, 2013, letter to acting Department of Labor Secretary Seth Harris, raised concerns that the DOL’s re-proposal of the ERISA fiduciary definition regulations “could severely limit access to low-cost investment advice” and

that a new, more restrictive definition of fiduciary “would add yet another barrier to accessing qualified retirement planning services.”

Given the concerns regarding IRA rollovers raised by the GAO in its IRA rollover report (referenced earlier), there has been speculation that expanded IRA fee disclosures may be in our future. The GAO concluded that, “Participants may have difficulty finding information on IRA fees, and when they do find it, they may not understand it.” Although some financial disclosure information is required today for IRAs, it is far less extensive than the detailed information now required under the ERISA 404a-5 regulations for retirement plan participants in participant directed individual account plans. No specific legislation or regulation had been introduced as of the date this Practice Guide was published.

6

IRAS & THE ERISA FIDUCIARY RULES

We may also see further discussion regarding the GAO suggestion to provide retirement plan participants who become eligible for rollovers more information on their distribution options, including

• the option to roll over assets to a new employer plan, and

• key factors a participant should consider when comparing possible investments.

Potential Impact on Advisors Who Work With IRAsAs of the date this Practice Guide was published, we don’t know precisely what will be included in the re-proposed ERISA fiduciary rules or whether additional IRA disclosures will become a reality. If the proposed changes being discussed by the DOL and Congress are adopted, however, it could have a substantial impact on the way advisors work with IRAs. Possibilities include:

• Advisors may be considered a fiduciary for investment support activities relating to qualified plan sponsors and participants that today are considered non-fiduciary activities.

• Soliciting IRA rollovers may result in fiduciary status.

• Investment (advice) support to IRAs may be subject to the ERISA fiduciary standard.

Ultimately, this means an advisor’s business model and compensation structures may need to change if they work with IRAs – or they may be engaged in a prohibited transaction.

In the interim, the current rules remain in effect:

• If an advisor is not an ERISA fiduciary to the plan or participants under ERISA 3(21) or 3(38), a recommendation to roll assets to an IRA does not make the advisor an ERISA fiduciary, even if the advisor will receive compensation if the assets are rolled to an IRA. Examples include advisors who do not have a relationship with the plan or who provide investment education, and other non-fiduciary support to the plan.

• If an advisor is a fiduciary to the plan or participants, their recommendation regarding rollovers may result in a prohibited transaction.

REGULATORY CHECKPOINTS

1. If you pursue IRA rollovers from retirement plan participants, do you provide services to the plan from which the rollover will be made?• No – Under current rules, advice regarding

the rollover does not alone result in ERISA fiduciary status.

• Yes – Evaluate your service model to determine whether you are an ERISA fiduciary.

2. Do you limit your support services to investment education and other non-fiduciary support?• Yes – Under current rules, advice regarding

the rollover does not alone result in ERISA fiduciary status.

• No – If you are an ERISA 3(21) investment advisor or 3(38) investment manager, solicitation of rollovers from that plan may result in a prohibited transaction.

The advisor should consult with a legal advisor regarding their business model.

Advisor Action StepsIn this section of the Practice Guide, we’ll suggest three actions that may help advisors evaluate how the current rules regarding rollover advice and solicitation may affect their practice and what advisors can do to stay on top of this rapidly evolving issue.

Action #1: Evaluate Your Rollover Business Model

Analyze your current IRA rollover practices

Given the current focus on IRA rollover activity, it is prudent to analyze your current practices relative to IRA rollovers from retirement plans. Consider both whether your business model raises regulatory concerns under ERISA as well as how your model affects your growth objectives. The following questions may be helpful as a starting point to understand the regulatory impact of your current business model relative to IRA rollovers.

7

IRAS & THE ERISA FIDUCIARY RULES

If your answers to the questions raise concerns that your rollover solicitations may be prohibited, you should review your service model with your legal advisor to confirm whether your services are in fact fiduciary services and whether any exemptions are available. Some legal advisors believe there are alternatives that may enable an advisor to segment the fiduciary investment support and non-fiduciary IRA rollover support they provide to a plan and its participants, subject to written plan and participant-level agreements. You should consult with a legal advisor before pursuing this alternative.

Action #2: Assess the Rollover IRA Opportunity1. Understand the differences and benefits of Traditional IRAs and Roth IRAs. Just as employee contributions to certain retirement plans may be made as either pre-tax or Roth contributions, contributions to IRAs can be made as pre-tax Traditional IRA contributions or Roth contributions. Nondeductible contributions may also be made to a Traditional IRA. Both types of IRAs offer flexible tax-planning opportunities; you should understand the advantages and disadvantages of each. The IRS has developed a Traditional and Roth IRAs Comparison Chart that you may find helpful.

IRA comparison chart: http://www.irs.gov/Retirement-Plans/Traditional-and-Roth-IRAs

2. Invest the time to learn more about the rollover rules. The options for moving money between different types of retirement plans have become more liberal over the years, allowing more opportunity for individuals to roll over their retirement assets. In response to the heavy volume of rollover activity among retirement savings arrangements, the IRS has developed a number of resources and tools to assist taxpayers and retirement professionals who may be involved in these transactions. The IRS has developed a chart illustrating the types of rollovers that are permitted between the various types of plans. As the chart illustrates, there are special rules for certain types of retirement plans.

For example, an individual’s designated Roth account in an employer’s plan may only be rolled over to another Roth plan or a Roth IRA. If you know the type of plan holding your clients’ retirement assets, you can obtain a quick snapshot of the types of plans that may accept a rollover of those assets using this IRS chart. The chart, along with frequently asked questions about rollovers and other information, is available on the IRS website.

Rollover chart: http://www.irs.gov/pub/irs-tege/rollover_chart.pdf

Rollover FAQs: http://www.irs.gov/Retirement-Plans/Plan-Participant,-Employee/Retirement-Topics---Rollovers-of-Retirement-Plan-Distributions

3. Evaluate the role of IRA rollovers in your business model. If you are not currently pursuing rollovers in your practice, you may want to review whether there is an opportunity to add IRA rollover support to your business model, depending upon your role with respect to the retirement plans you support. As a result of the aging baby boomer population, the volume of IRA rollovers is expected to increase. And IRAs are a key component of many retirement income strategies. If you provide IRA investment support today for clients, be sure to inquire about employer retirement plans that may have rollover potential.

If you decide to pursue rollovers, you will need to determine the impact on any fiduciary services you provide (See Action #1). You will also need to pay close attention to any legislative or regulatory developments on the definition of fiduciary so you understand how potential rule changes can impact your business model.

As you evaluate your rollover services, include a review of the broader rollover services that may be appropriate for your clients. For example, many plans have adopted a plan feature that enables the plan sponsor to distribute balances of not more than $5,000 owned by former employees. If these mandatory distributions are greater than $1,000 (but not more than $5,000),

8

IRAS & THE ERISA FIDUCIARY RULES

the balance may be distributed from the plan but must be rolled to an IRA, unless the former participant elects a different option. These rollovers are often referred to as “automatic rollovers.” This feature can help plan sponsors control plan costs by reducing the burden of administering these small balances and tracking terminated employees with small balances. It is important to understand the scope of mandatory distribution and automatic rollover services available through your network of service providers.

MG Trust, a Broadridge Company, offers a wide range of IRA services, including administration of automatic rollovers. To learn more about MG Trust’s IRA services contact Janet Moore at +1 720 956 5445 or [email protected].

Broadridge’s Marketing Communications solutions group also provides a platform for client communications. These offerings include paper statements, e-delivery, confirms, enrollment kits, storage and more. To learn more about these services contact Broadridge at +1 888 237 1900.

Action #3: Monitor New DevelopmentsStaying abreast of legislative and regulatory developments is critical to the success of any advisor working in the retirement industry. This is especially true with respect to the evolving guidance regarding the ERISA fiduciary definition and IRA rollovers. Listed below are three resources that you may want to tap into.

1. Matrix webinars & updates As discussed throughout the Practice Guide, the fiduciary issues are in a state of flux. Matrix will be monitoring these issues carefully and anticipates upcoming webinars and articles as new developments occur. Watch for emails from Matrix with details on webinars and other materials. To get on the Matrix email list for updates, contact the Matrix advisor help desk at +1 866 935 6824.

In the meantime, you can stay up-to-date on fiduciary issues by accessing the free resources referenced in 2 and 3 below.

2. DOL newsletter The best resource for staying current with regulatory developments on fiduciary issues is the DOL itself. The Assistant Secretary for the Employee Benefits Security Administration at the DOL provides a bi-weekly newsletter covering the DOL’s initiatives on a variety of topics, including the anticipated fiduciary regulations. Subscribe to this newsletter, Before It’s Too Late: A Retirement Security Update From Assistant Secretary Phyllis C. Borzi, to receive first-hand information.

To subscribe to the newsletter, go to: https://public.govdelivery.com/accounts/USDOL/subscriber/new?topic_id=USDOL_422

3. GAO report on rollovers If you haven’t reviewed the Government Accountability Office (GAO) report on rollovers, 401(k) Plans: Labor and IRS Could Improve the Rollover Process for Participants, you may want to learn more about what the GAO found when they posed as consumers and contacted service providers to obtain information about retirement plan distribution options. The GAO conducted the study to identify challenges participants may face in understanding their distribution options and implementing rollovers.

You can access the GAO report at http://www.gao.gov/assets/660/652881.pdf

4. Congressional letter to acting DOL Secretary Seth Harris The June 14, 2013 letter from members of the Congressional Black Caucus and the Congressional Hispanic Caucus to acting Department of Labor Secretary Seth Harris raised concerns about the DOL’s re-proposal of the fiduciary definition regulations. This letter is one example of the criticism certain members of Congress have directed toward the DOL’s fiduciary initiative.

You can obtain a copy of the letter atwww.financialservices.org/uploadedFiles/FSI-Letter-to-DOL-on-Fiduciary-Redefinition-2013.pdf

No part of this document may be distributed, reproduced or posted without the express written

permission of Broadridge Financial Solutions Inc. © 2014 Broadridge Financial Solutions, Inc.

Broadridge and the Broadridge logo are registered trademarks of Broadridge Financial Solutions, Inc.

MKT_501_14

Contact UsCindy Dash COO, Matrix Financial Solutions Broadridge Financial Solutions, Inc. +1 720 956 5414

Pamela S. O’Rourke Senior Vice President and Senior Counsel Integrated Retirement Initiatives +1 877 731 3947

About BroadridgeBroadridge Financial Solutions, Inc. (NYSE:BR) is the leading provider of investor communications and technology-driven solutions for broker- dealers, banks, mutual funds and corporate issuers globally. Broadridge’s investor communications, securities processing and business process outsourcing solutions help clients reduce their capital investments in operations infrastructure, allowing them to increase their focus on core business activities. With 50 years of experience, Broadridge’s infrastructure underpins proxy voting services for over 90% of public companies and mutual funds in North America, and processes more than $5 trillion in fixed income and equity trades per day. Broadridge employs approximately 6,400 full-time associates in 13 countries. For more information about Broadridge, please visit broadridge.com.

About Matrix Financial SolutionsMatrix Financial Solutions, a part of Broadridge Financial Solutions, Inc., is a leading provider of TrueOpen™ retirement and mutual fund processing products and services for third party administrators, financial advisors, banks and other financial professionals. Matrix serves more than 300 financial institutions with over $230 billion in customer assets processed through its trading platform. For more information about Matrix please visit matrix.broadridge.com.

About Integrated Retirement Integrated Retirement contributed to this report. Integrated Retirement is an independent privately held corporation with deep retirement plan expertise and industry insights and has a proven track record of helping elite financial organizations achieve retirement plan mastery across all sales, marketing, service and support disciplines.