32

MONEY LAUNDERING ‘Is enough being done to tackle it?’ Group Members: Doushikabye Pandoo Khawsar Soogund Jessica Mootoosamy Karishma Ansaram

| Date post: | 16-Aug-2015 |

| Category: |

Law |

| Upload: | karishma-ansaram |

| View: | 87 times |

| Download: | 0 times |

MONEY LAUNDERING‘Is enough being done to tackle it?’

Group Members:

Doushikabye PandooKhawsar SoogundJessica MootoosamyKarishma Ansaram

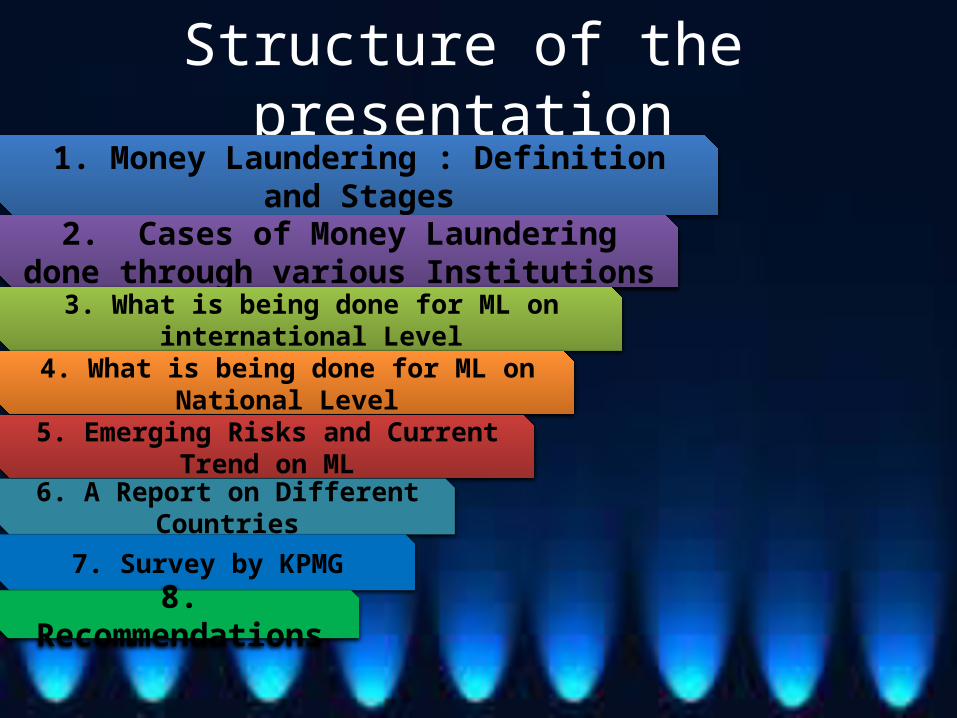

Structure of the presentation1. Money Laundering : Definition and Stages

2. Cases of Money Laundering done through various Institutions

3. What is being done for ML on international Level

4. What is being done for ML on National Level

5. Emerging Risks and Current Trend on ML

6. A Report on Different Countries

7. Survey by KPMG

8. Recommendations

Money LaunderingProcess of disguising illegal origin of

criminal proceeds

Growth of Money LaunderingCriminal proceeds amounted to 3.6% of Global GDP with 2.7%(USD

1.6 trillion) being laundered- Study by UN Office on drugs and crime (UNODC)

Money Laundering Investigations2014 2013 2012

Investigations Initiated1312 1596 1663

Prosecution Recommendations1071 1377 1411

Indictments/Informations934 1191 1325

Sentenced785 829 803

Incarceration Rate* 82.2% 85.4% 84.7%

Average Months to Serve66 68 64

Stages in Money Laundering

Sources of funds tax crimes, fraud,

embezzlement, drugs, theft, bribery

and corruption

Placement

Goal: To deposit criminal proceeds into the financial system Common Methods • Change of currency • Change of denomination • Transportation of cash • Cash deposits

Integration

Goal: Conceal the criminal origin of proceeds Common Methods: • Wire transfers • Withdrawals in cash • Cash deposits in multiple bank accounts • Split and merge of various bank accounts

LayeringGoal: Create an apparent legal origin for criminal processes Common Methods: • Creating fictitious loans, turnover, capital gains, contracts, financial statements etc. • Disguise ownership of assets • Use of criminal proceeds in transactions with third parties

Use of proceeds

for personal benefit

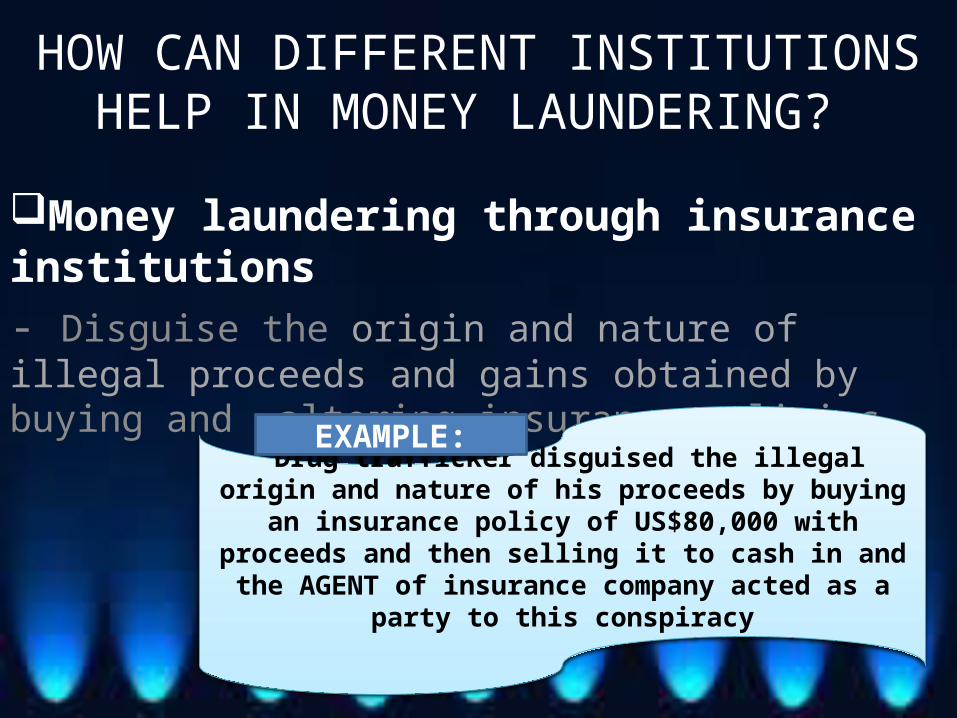

HOW CAN DIFFERENT INSTITUTIONS HELP IN MONEY LAUNDERING?

Money laundering through insurance institutions - Disguise the origin and nature of illegal proceeds and gains obtained by buying and altering insurance policies

Drug trafficker disguised the illegal origin and nature of his proceeds by buying an insurance policy of US$80,000 with proceeds and then selling it to cash in and the AGENT of

insurance company acted as a party to this conspiracy

EXAMPLE:

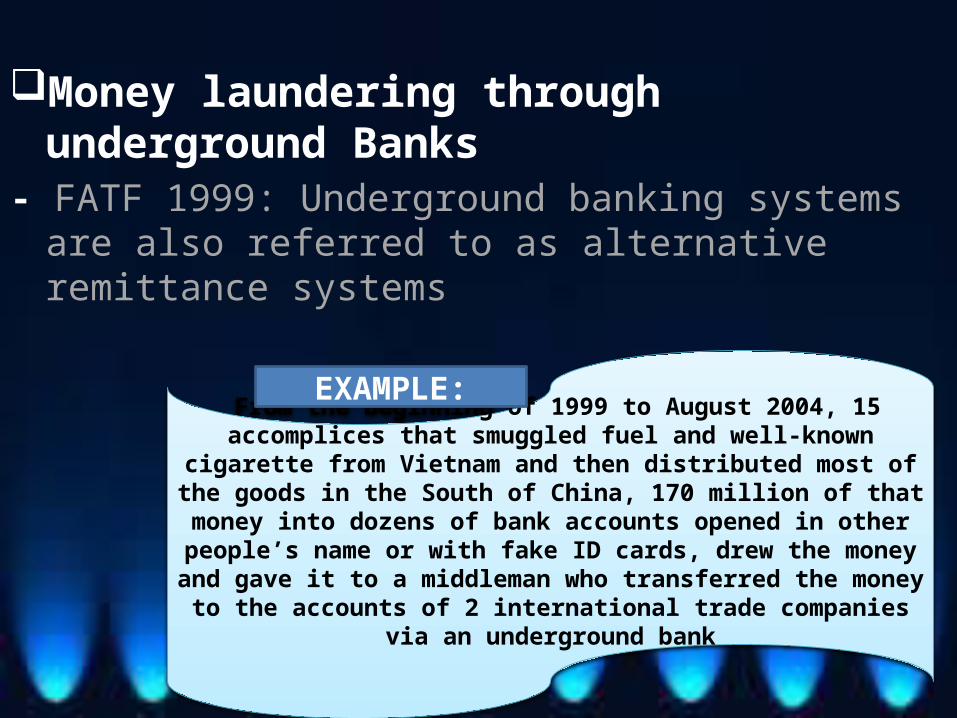

Money laundering through underground Banks- FATF 1999: Underground banking systems are also referred

to as alternative remittance systems

From the beginning of 1999 to August 2004, 15 accomplices that smuggled fuel and well-known cigarette from Vietnam and then distributed most of the goods in the South of China, 170 million of that money into dozens of bank accounts opened in other people’s name or with fake ID cards, drew the money and gave it to a middleman who transferred the money to the

accounts of 2 international trade companies via an underground bank

EXAMPLE:

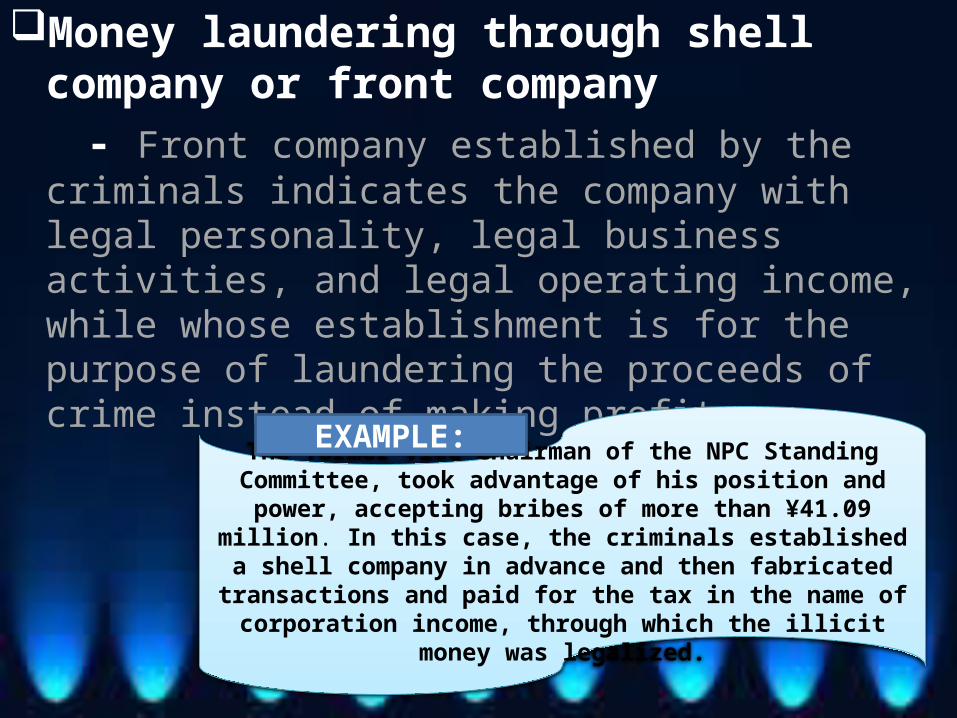

Money laundering through shell company or front company

- Front company established by the criminals indicates the company with legal personality, legal business activities, and legal operating income, while whose establishment is for the purpose of laundering the proceeds of crime instead of making profits

The former Vice-Chairman of the NPC Standing Committee, took advantage of his position and power, accepting bribes of more than

¥41.09 million. In this case, the criminals established a shell company in advance and then fabricated transactions and paid for the tax in the

name of corporation income, through which the illicit money was legalized.

EXAMPLE:

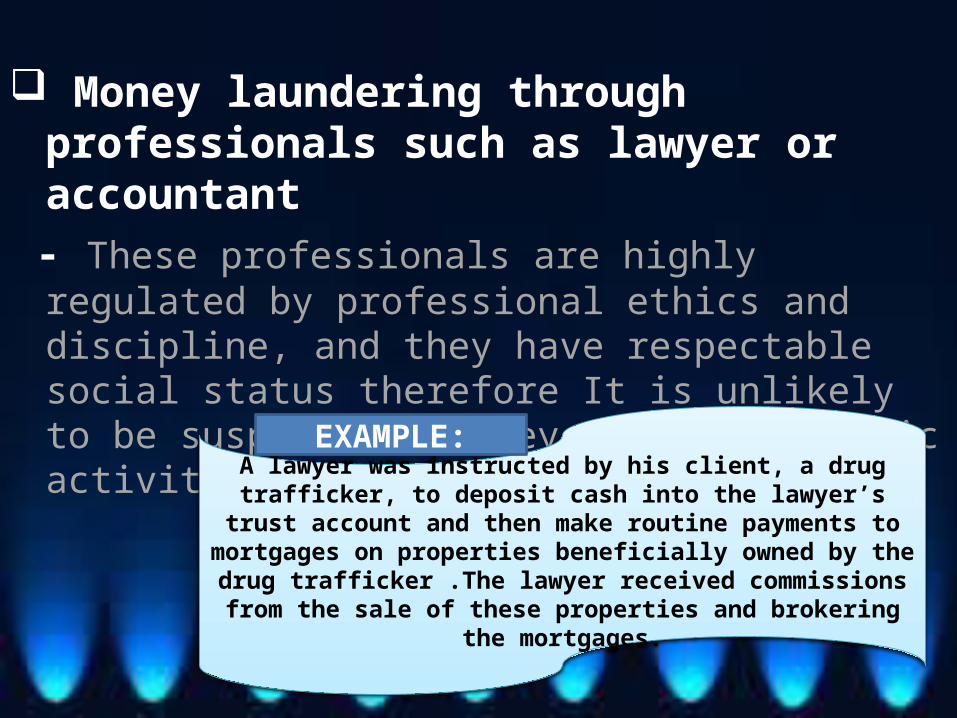

Money laundering through professionals such as

lawyer or accountant - These professionals are highly regulated by professional

ethics and discipline, and they have respectable social status therefore It is unlikely to be suspected if they perform economic activities on behalf of their clients.

A lawyer was instructed by his client, a drug trafficker, to deposit cash into the lawyer’s trust account and then make routine payments to

mortgages on properties beneficially owned by the drug trafficker .The lawyer received commissions from the sale of these properties and

brokering the mortgages.

EXAMPLE:

What is being done internationally to combat

money laundering ?

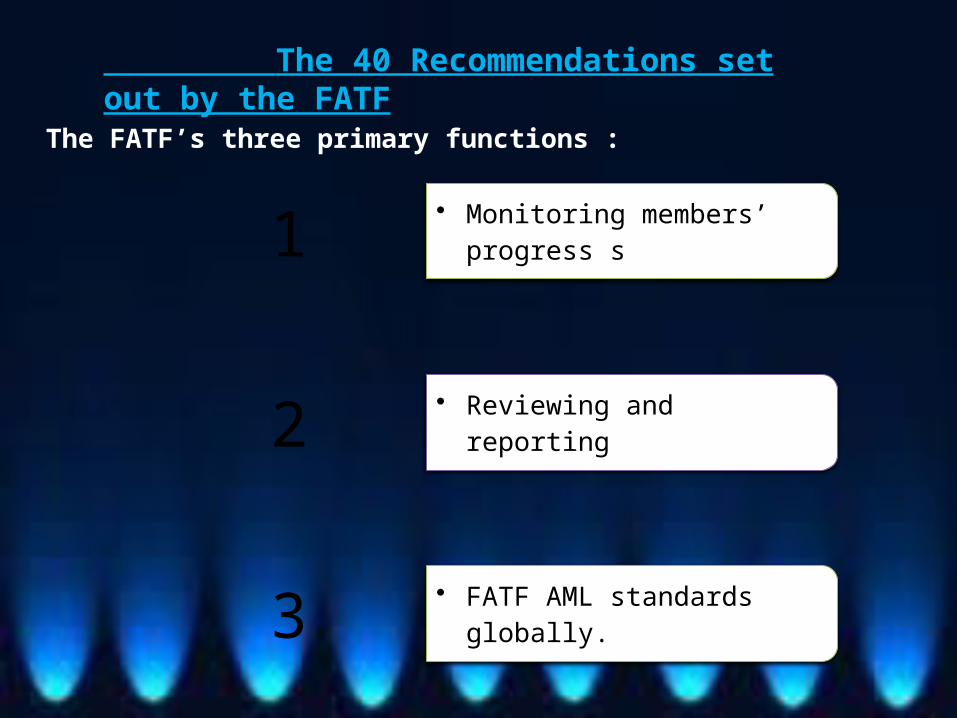

The 40 Recommendations set out by the FATF

The FATF’s three primary functions :

1 • Monitoring members’ progress s

2 • Reviewing and reporting

3 • FATF AML standards globally.

IOSCO “Resolution on Money Laundering

Customer identifying

record-keeping

suspicious transactions

control of securities and futures businesses

informationMonitoring & compliance procedures

The resolution provides as

follows:

1) Global Programme against Money Laundering by the United Nations

The GPML is a resource for information, expertise and technical assistance in establishing or improving a country’s AML infrastructure.

2) Customer Due Diligence set out by the Basel Committee

Standards set out in Customer Due Diligence are intended to benefit banks beyond the fight against money laundering by protecting the safety and soundness of banks and the integrity of banking systems.

3) AML Guidance Notes for Insurance Supervisors and Insurance Entities set out by the IAIS

Those Guidance Notes are intended to be implemented by individual countries taking into account the particular insurance companies involved, the products offered within the country, and the country’s own financial system, economy, constitution and legal system.

AML Principles forPrivate Banking set outby the Wolfsberg Group of Banks

guidelines when dealing with the high net worth individuals and the private banking departments .

-customer identification-extra due diligence-Establishing beneficial ownership a/c.

Egmont Group of Financial Intelligence Units

Governments have created agencies to analyze information submitted by covered entities and persons pursuant to money laundering reporting requirements.

Such agencies are commonly referred to as financial intelligent units (FIUs).

Monitoring Screening and Searching Technique

Suspicious Transactions

Reporting

This set of principles identifies issues that should be addressed in order for financial institutions to develop suitable monitoring, screening and searching processes using a risk-based profile approach

Financial institution suspecting or has reasonable grounds to suspect that funds are the proceeds of a criminal activity, or are related to terrorist financing, report its suspicions to the applicable financial intelligence unit

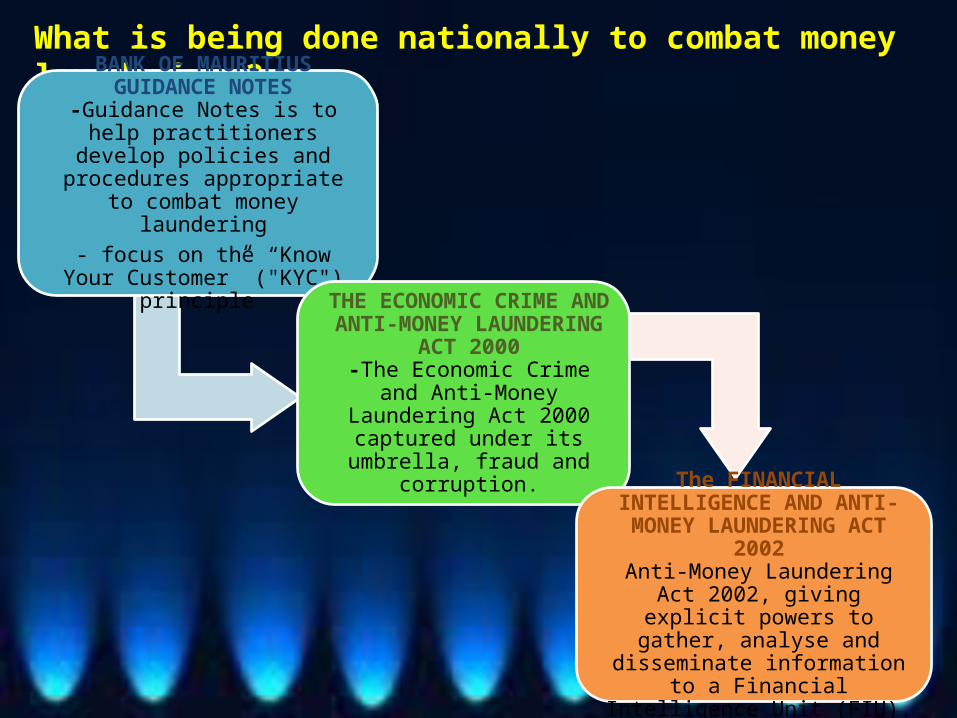

What is being done nationally to combat money laundering ?

BANK OF MAURITIUS GUIDANCE NOTES

-Guidance Notes is to help practitioners develop policies and procedures appropriate to combat

money laundering- focus on the “Know Your Customer”

("KYC") principle

THE ECONOMIC CRIME AND ANTI-MONEY LAUNDERING ACT

2000-The Economic Crime and Anti-

Money Laundering Act 2000 captured under its umbrella, fraud

and corruption.

The FINANCIAL INTELLIGENCE AND ANTI-MONEY LAUNDERING ACT

2002Anti-Money Laundering Act 2002, giving explicit powers to gather,

analyse and disseminate information to a Financial Intelligence Unit (FIU).

• The Act is the result of recommendations made by the (FSAP) mission of the lMF and the World Bank and has brought certain changes to the institutional and regulatory framework with regards to AML

Anti-Money Laundering Act 2003

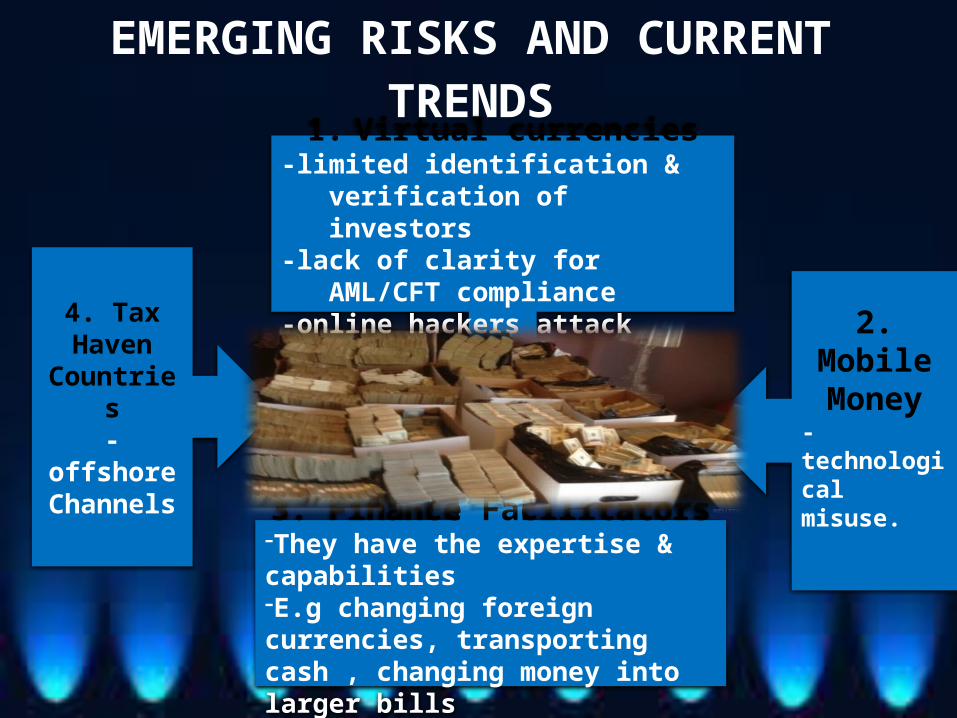

EMERGING RISKS AND CURRENT TRENDS

4. Tax Haven Countries-offshore Channels

1. Virtual currencies-limited identification & verification of

investors-lack of clarity for AML/CFT compliance-online hackers attack

2. Mobile Money

-technological misuse.

3. Finance Facilitators-They have the expertise & capabilities -E.g changing foreign currencies, transporting cash , changing money into larger bills

EMERGING RISKS AND CURRENT TRENDS

Banking Sector

Correspondent Banking

Offshore Banking

Private Banking Cyber

Currency

EMERGING RISKS AND CURRENT TRENDS

Offshore Sector-lack of political will-strong banking confidentiality

A conflict between the western AML laws and the benefit they

enjoy

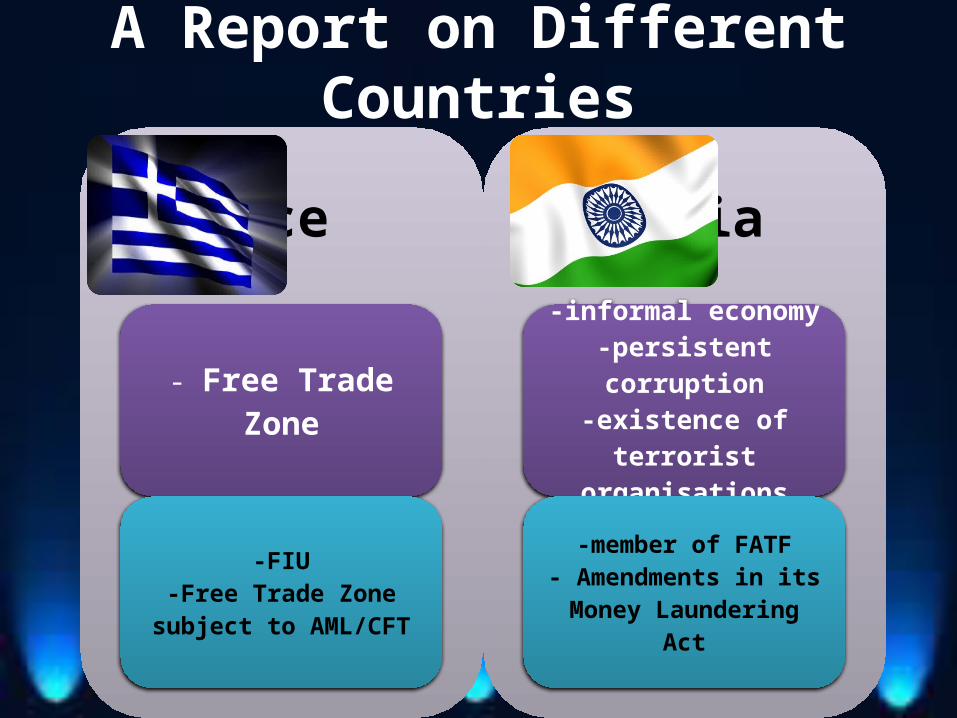

A Report on Different Countries

Greece

- Free Trade Zone

-FIU-Free Trade Zone subject to

AML/CFT

India

-informal economy-persistent corruption-existence of terrorist

organisations

-member of FATF- Amendments in its Money

Laundering Act

Singapore

-lack of reporting of large currencies-rapid growth of private banking

-use of stand alone ML charges

-the suspicion transaction reporting office

France

-large informal sector-informal transfer system -hawalas

-tracfin hired new officers-updated investigation

methods-updated vigilance

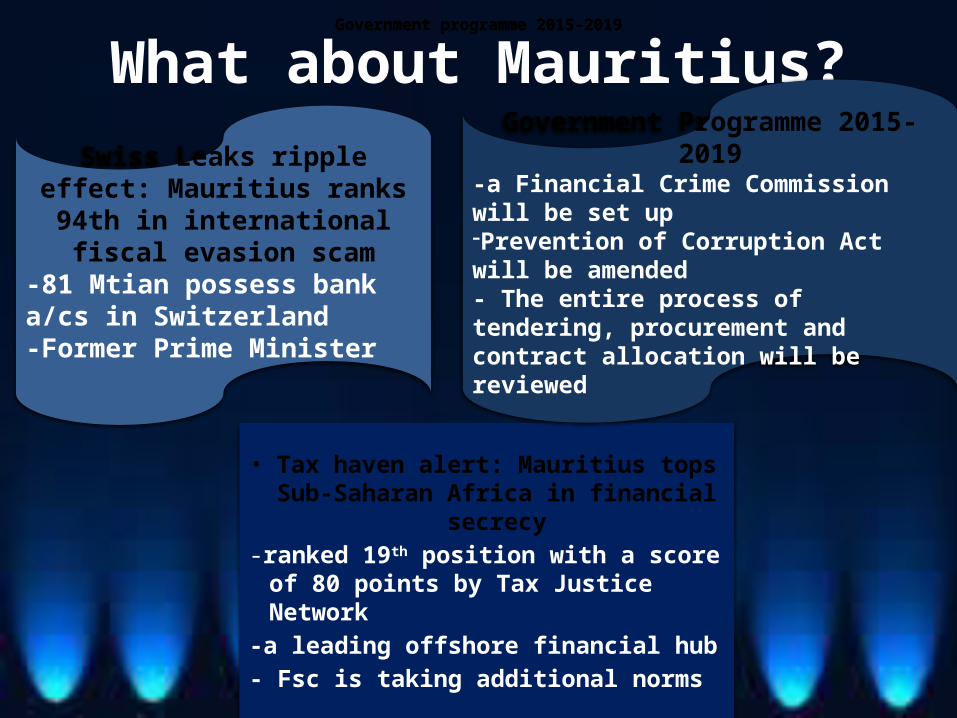

What about Mauritius?

Swiss Leaks ripple effect: Mauritius ranks 94th in international fiscal

evasion scam-81 Mtian possess bank a/cs in Switzerland-Former Prime Minister

• Tax haven alert: Mauritius tops Sub-Saharan Africa in financial

secrecy-ranked 19th position with a score of

80 points by Tax Justice Network-a leading offshore financial hub- Fsc is taking additional norms

Government Programme 2015-2019-a Financial Crime Commission will be set up-Prevention of Corruption Act will be amended - The entire process of tendering, procurement and contract allocation will be reviewed

Government programme 2015-2019Government programme 2015-2019Government programme 2015-2019

SURVEY BY KPMG

The overarching aims of this year’s global AML survey include:

• Identifying emerging trends, opportunities and threats;• Capturing industry perceptions on regulation, cost, and effectiveness; and• Benchmarking AML efforts in the financial services industry.

Global Anti Money Laundering Survey 2014

Senior managem

ent

Asset mgt

sector

Compliance cost

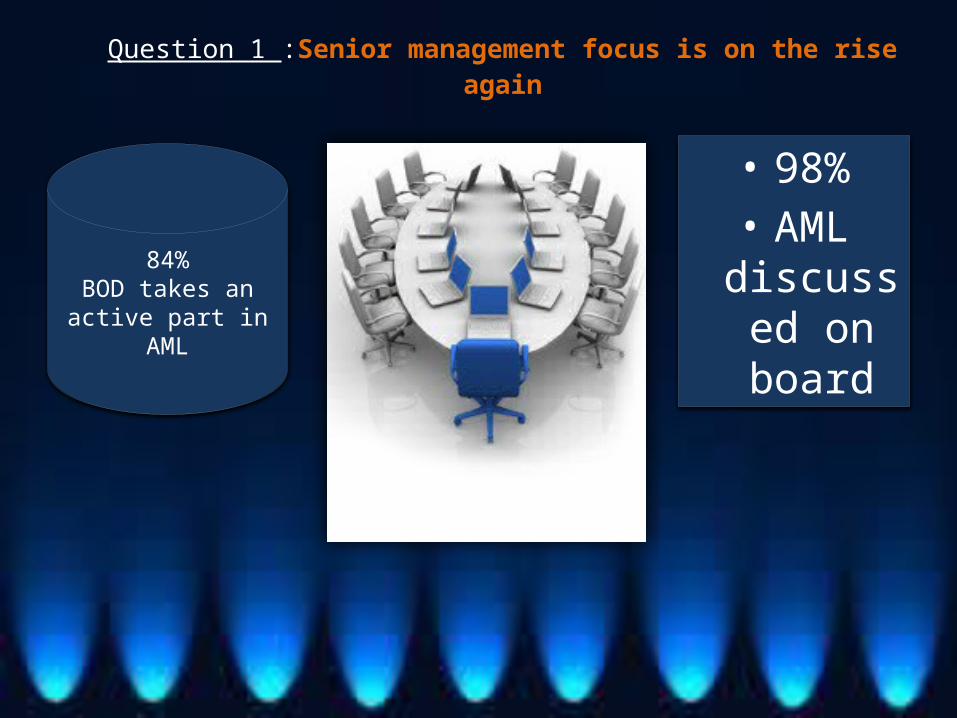

Question 1 :Senior management focus is on the rise again

84%BOD takes an active

part in AML

• 98%• AML discusse

d on board

Question 2 :How challenging respondents consider

implementing a globally consistent AML framework

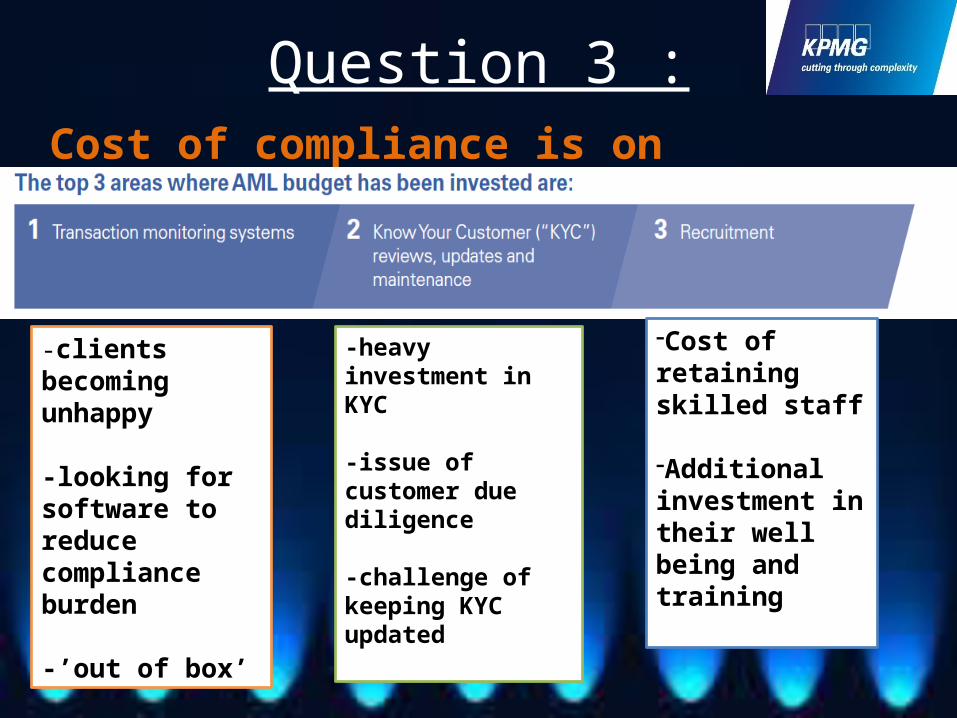

Question 3 :Cost of compliance is on increase

-clients becoming unhappy

-looking for software to reduce compliance burden

-’out of box’

-heavy investment in KYC

-issue of customer due diligence

-challenge of keeping KYC updated

-Cost of retaining skilled staff

-Additional investment in their well being and training

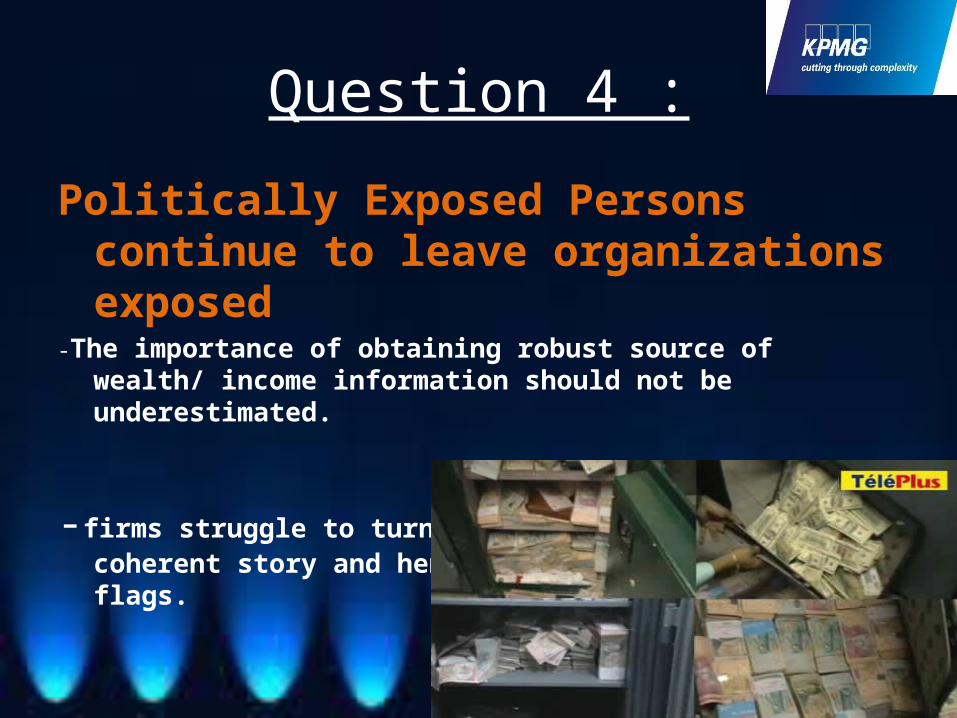

Question 4 :

Politically Exposed Persons continue to leave organizations exposed

-The importance of obtaining robust source of wealth/ income information should not be underestimated.

-firms struggle to turn the information into a coherent story and hence identify gaps and red flags.

Question 5 : Asset Management Sector

• Asset managers face particular challenges in:

managing the risks arising from the use of or reliance upon third

parties

obtaining appropriate data

to enable meaningful transaction monitoring

implementing appropriate

customer risk assessment

models.

Recommendations of KPMG

• Nominate a member of the Board with responsibility for maintaining effective AML controls.

• Ensure a broad-ranging assurance program is in place which tests systems, processes.

• Prepare effectively for regulator visits, and ensure that the

Board can demonstrate awareness and oversight.

Recommendations for a better AML Framework

Ensuring True Commitment and Resolute Political Will

Providing Clear Policy Guidance to the Private Sector

Launching an Awareness Raising Campaign

Developing Regional/International Collaboration

Ensuring Continuous Training for Both the Public and the Private Sectors

Conclusion• Combating illegal profits is certainly not a recent, revolutionary

development.

• Rules will not always be obeyed.

• These problems cannot be solved simply by generating more and more regulations.

• More regulations also increase the likelihood of information overload and false positives.