Islamic banking and customers’ preferences: the case of the UK Walid Mansour Institut Supe ´rieur de Finances et de Fiscalite ´ de Sousse, Universite ´ de Sousse, Sousse, Tunisia Mohamed Ben Abdelhamid International Finance Group, Universite ´ El-Manar, Tunis, Tunisia Omar Masood Royal Docks Business School, East-London University, London, UK, and G.S.K. Niazi Department of Administrative Sciences, Quaid-e-Azam University, Islamabad, Pakistan Abstract Purpose – Islamic banking is an increasingly important factor in the UK financial environment. With Islamic banks entering the industry in significant numbers – and competing directly with the incumbent “conventional” ones – the question of selection criteria of the banks’ customers is of obvious interest. The purpose of this paper is to study the decision-making process of a sample of UK customers and the factors that may influence them. Design/methodology/approach – The paper uses a sample of 156 UK questionnaire respondents, comprising Muslim and non-Muslim bank customers alike. The methodological approach is partly borrowed from Masood et al. with the chosen questions aimed at finding out what drives the selection process of bank customers. Findings – The paper’s major findings show that, irrespective of the demographic features and the religion of the respondents, the criterion “low services charges” is the top customers’ criteria. The Islamic nature of the bank is, however, placed second, pointing to the importance of religious orientation. Research limitations/implications – The major limitation of the paper relates to the size of the sample of respondents. The findings of the paper are likely to be of interest to UK banks determining how best to attract customers in the new era. Future research may usefully focus on an international comparison of bank selection criteria by employing an index of religiosity. Originality/value – The paper is of particular value because it focuses on the choice of banking in the context of the recent significant growth in the Islamic banking industry in the UK. Keywords Islam, Banking, United Kingdom, Customer behaviour Paper type Research paper 1. Introduction Over the last 30-plus years, Islamic banking has become an important part of the investment and finance industries. Indeed, despite stiff competition from incumbent conventional banks, the Islamic institutions have seen increasing success, not only in Islamic counties but also in developed Western economies including the UK and France. In fact, these financial institutions are now regarded as having unique financial intermediary features; for example, Siddiqi (1983) notes that such intermediaries are The current issue and full text archive of this journal is available at www.emeraldinsight.com/1755-4179.htm Islamic banking 185 Qualitative Research in Financial Markets Vol. 2 No. 3, 2010 pp. 185-199 q Emerald Group Publishing Limited 1755-4179 DOI 10.1108/17554171011091746

Transcript

Islamic banking and customers’preferences: the case of the UK

Walid MansourInstitut Superieur de Finances et de Fiscalite de Sousse,

Universite de Sousse, Sousse, Tunisia

Mohamed Ben AbdelhamidInternational Finance Group, Universite El-Manar, Tunis, Tunisia

Omar MasoodRoyal Docks Business School, East-London University, London, UK, and

G.S.K. NiaziDepartment of Administrative Sciences, Quaid-e-Azam University,

Islamabad, Pakistan

Abstract

Purpose – Islamic banking is an increasingly important factor in the UK financial environment. WithIslamic banks entering the industry in significant numbers – and competing directly with theincumbent “conventional” ones – the question of selection criteria of the banks’ customers is of obviousinterest. The purpose of this paper is to study the decision-making process of a sample of UK customersand the factors that may influence them.

Design/methodology/approach – The paper uses a sample of 156 UK questionnaire respondents,comprising Muslim and non-Muslim bank customers alike. The methodological approach is partlyborrowed from Masood et al. with the chosen questions aimed at finding out what drives the selectionprocess of bank customers.

Findings – The paper’s major findings show that, irrespective of the demographic features and thereligion of the respondents, the criterion “low services charges” is the top customers’ criteria. TheIslamic nature of the bank is, however, placed second, pointing to the importance of religiousorientation.

Research limitations/implications – The major limitation of the paper relates to the size of thesample of respondents. The findings of the paper are likely to be of interest to UK banks determininghow best to attract customers in the new era. Future research may usefully focus on an internationalcomparison of bank selection criteria by employing an index of religiosity.

Originality/value – The paper is of particular value because it focuses on the choice of banking inthe context of the recent significant growth in the Islamic banking industry in the UK.

Keywords Islam, Banking, United Kingdom, Customer behaviour

Paper type Research paper

1. IntroductionOver the last 30-plus years, Islamic banking has become an important part of theinvestment and finance industries. Indeed, despite stiff competition from incumbentconventional banks, the Islamic institutions have seen increasing success, not only inIslamic counties but also in developed Western economies including the UK and France.In fact, these financial institutions are now regarded as having unique financialintermediary features; for example, Siddiqi (1983) notes that such intermediaries are

The current issue and full text archive of this journal is available at

www.emeraldinsight.com/1755-4179.htm

Islamicbanking

185

Qualitative Research in FinancialMarkets

Vol. 2 No. 3, 2010pp. 185-199

q Emerald Group Publishing Limited1755-4179

DOI 10.1108/17554171011091746

characterised by the offering of Shari’ah[1]-complaint contracts. That is, they arerespecting the rules that are instituted by the Muslims’ Holy Qur’an[2].

In the context of the emergence of Islamic finance and large numbers of Muslimcustomers in Western countries, many questions arise. In particular, do customers havethe same selection criteria for the financial institutions (i.e. Islamic vs Conventionalbanks)? Further, do they exhibit the same preferences? On which factors do suchpreferences hinge? The goals of the current study relate to these issues, i.e. customers’preferences and their selection process. Our methodology aims at understanding anddefining the factors that impact upon the process. The study reports statistical analysisof the questionnaire responses of a sample of 156 Muslims and non-Muslims living inthe UK. Reflecting previous contributions in the literature, the central goal of thequestionnaire is to find out which criteria are the most important to the respondents inchoosing their bank. We also examine the extent to which customers are prone to put theIslamic nature of the financial instruments at the top of their selection criteria.

The remainder of the paper is organized as follows. In Section 2, we review the recentliterature that is most closely related to our article. Section 3 is devoted to a succinctdescription of the methodology and some statistical features of the sample. Section 4presents our major findings and Section 5 concludes.

2. Literature reviewIn this section, we review some of the most important studies that deal with theselection criteria of financial institutions. In Section 2.1, we place special emphasis onthose that have focussed on this question in the context of Islamic banking. Section 2.2examines some facts relating to Western economies (especially the UK) regarding theIslamic financial institutions.

2.1 Some preliminariesBank selection criteria are the topic of many research articles in finance and marketing.Most of the studies focus on the criteria that are used by the customers to select aparticular bank (Martenson, 1985; Tan and Chua, 1986; Laroche and Taylor, 1988; Eroland EL-Bdour, 1989; Denton and Chan, 1991; Kaynak et al., 1991; Khazeh and Decker,1992; Devlin and Gerrard, 2005). Most of these studies find a variety of factors thathave a crucial impact on the customers’ decision-making process. Indeed, when theychoose their financial institutions, the customers are influenced by criteria such ascompletive interest rates charged on debts, recommendations by friends, the bank’sbrand (i.e. reputation of the bank), the collaboration the bank staff and otherconvenience factors such as quick and high-quality services.

Martenson’s (1985) study of the Swedish banking sector showed that about 30 per centof the respondents select their financial institution randomly. Further, the location and theparental influence play an important role in driving the choice. Denton and Chan (1991)studied the preferences behaviour of customers in Hong Kong. The selection criteria showthat multiple bank customers display preferences like risk alleviation, convenience and theneed for prestige. However, Khazeh and Decker (1992) document that lower banking feesgreatly influence the banking choice.

Kaynak et al. (1991) used an approach consisting of dividing up their sample ofTurkish respondents on the basis of sex, age and educational level of the customers.They found that the male customers were more influenced by financial criteria

QRFM2,3

186

(for example, the financial advisory services) than were the female ones. Their commonselection criteria were parking facilities, speed and range of services offered.

The study of Devlin and Gerrard (2005) examined customer choice criteria in thecontext of multiple banking. Their study focused on conventional rather than Islamicbanks. Using a quantitative investigation technique incorporating 495 respondents,they argue that:

Findings show significant differences between selecting a first and secondary bank.Recommendations from others are influential and significantly more important in promptingchoice of secondary bank. Offering an incentive is also significantly more important in promptingchoice of secondary bank, but is less influential in terms of overall ranking of importance. Serviceexpectation and low fees/overdraft charges are less significant in prompting secondary bankchoice. Implications for the marketing of main and secondary accounts are explored (p. 297).

The essential mission of bankers is based on the clients-products/services dimension.With the growth of demand for Islamic banking instruments and services around theworld, the banking sector teems with a diversity of Islamic services. Such servicescome into the industry to create a rivalry with the services that are already offered bythe incumbent, conventional banks. Such diversity will certainly give the possibility ofchoice to the customers. This choice will be influenced by both the specificities ofIslamic banks and customers’ own preferences.

Many authors have used similar approaches to the aforementioned studies ofconventional banks, but in an Islamic banking context. An early study by Erol andEl-Bdour (1989) reported that the religiosity of the financial institution in Jordan is notthe most important influence on bank choice, with other factors entering the picture inthe decision-making process of the customers. Indeed, Wan Ahmed et al. (2008, p. 284)claim that:

Erol & El-Bdour, when comparing Islamic and conventional bank customers, found thatprofitability motivation supersedes religious motivation in selection of banks. He attributedthis to the fact that customers may have been used to the profit-oriented conventionalbanking environment and the possibility that the respondents may have underestimated theirreligious motivations when answering the survey questions.

In a study comparing Islamic and conventional banks, Hegazy (1995) provided evidencethat the selection criteria of these two kinds of banks are different. More specifically,word-of-mouth and advice by relatives and friends tends to favour Islamic banks ratherthan the conventional ones. However, Gerrard and Cunningham (1997) study Muslimand non-Muslim customers’ perceptions of Islamic banking in Singapore. Their resultsshow that there is no significant difference between the selection criteria between thetwo categories of customers.

Wan Ahmed et al. (2008) choose 27 criteria that previous studies suggest mightinfluence the choice of banks customers, in this case in the context of Malaysia. Some ofthe 27 criteria are related to the religiosity of the bank, for example, Islamic features suchas the absence of riba[3] fees and the confidence in the Sharia Board. The authors developan index reflecting the degree of religiosity[4]. Such an index embeds the central facts ofShari’ah, i.e. faith, Islamic laws, and akhlaq (virtues or ethics). The authors report that“the index was found to be skewed to the right as expected since a Muslim should bereligious” (p. 286), with nearly 72 per cent of the respondents having a medium or highreligiosity index score (Wan Ahmed et al., 2008; Table II).

Islamicbanking

187

The study of Wan Ahmed et al. (2008) is important for two main reasons. The firstrelates to the issue of the degree of religiosity and its impact on the choice of bank. Theauthors show that the most religious customers (i.e. those whose religiosity index ishigh) are more likely to choose an Islamic bank to raise financed or as a holder of theirdeposits. The second relates to the effect of the degree of religiosity on thedeterminants of credit selection criteria. The findings show that:

[. . .] apart from favourable credit terms of the financing products, efficiency in services,especially the after-hour and less hassle services provided by electronic services are the mostimportant factors in choosing where they get their financing. Such factors should be seriouslyconsidered by bankers in designing their products and perfecting their customerservices, especially when developing their market strategies concerning working MalayMuslims. They also considered availability of parking and public transport nearby asimportant (p. 299).

2.2 Islamic banking: some facts from the UKIn this section, we try to identify the reasons for the rise in interest in Islamic bankingand Muslim banking choices in the UK. In recent decades, Islamic finance has gainedprominence in Western countries, especially in the UK. According to the UnitedNations (2009), the UK had the second highest (after Germany) Muslim population with2,475,841 in 2008. This number represents 4 per cent of the total UK population in theUK. Table I provides the detailed figures.

Clearly, the sheer number of Muslims in the country might motivate the UKGovernment to move in the direction of adopting social and financial regulations thatare more in compliance with Shari’ah stipulations, thus facilitating further growth inthe Muslim community in the UK. The increasing Muslim population in the UK makesthe study of the financing preferences an important task. However, a UK context waschosen for several other reasons. The most important ones being as follows:

. The financial status of London as a financial center.

. The UK being home to the first Quranic law retail bank in the Western countries– the Islamic Bank of Britain (authorized by the financial services authority(FSA) in 2004). After 2004, the UK financial environment has been marked by theappearance of many other FSA-approved Islamic banks.

The UK is, therefore, an important centre for Islamic finance and it is currently thedevelopmental core of Islamic finance in Europe. To establish a broader global context,Table II shows the volume of Islamic bank assets around the world. With $18.1 billionin asset values, the UK ranks eighth, between Turkey and Qatar.

Table I.Muslim populationestimation inNorthwestern Europe

QRFM2,3

188

To provide a further indication of the UK’s key position in the sector, Table III showsthat 22 Islamic banks operate in the UK, outnumbering the combined total in the USA,France, South Africa, Switzerland and Australia.

Table IV, however, shows that the sheer numbers of banks may not provide acomplete picture, as 17 of the 22 are actually conventional banks that have Islamicwindows. Although the products and services by these banks are not compliant with theShari’ah premises, their windows offer some Shari’ah-compliant financial instruments.

3. Methodological approach and description of the sampleThis section of the paper describes our methodological approach. The researchquestions were addressed using statistical study of the respondents’ answers to aquestionnaire partly inspired by Masood et al. (2009). The questionnaire wasdistributed to 200 respondents either by face-to-face contacts or through emails; thetotal number of returned and usable questionnaires was 156, representing a highresponse rate of 78 per cent[5].

We present some background statistics relating to the general characteristics of therespondents. In particular, we report on gender, religion, age, education level, job typeand annual income level as the aforementioned factors are believed to represent the keydemographics that might affect attitudes towards Islamic bank products.

Source: The Banker Special Supplement: Top 500 Islamic Financial Institutions, November 2008,available at: www.thebanker.com

Table II.Islamic banks assets

around the world

Country Number of Islamic banks

UK 22US 9France 3South Africa 3Switzerland 3Australia 2

Source: The Banker (2008)

Table III.Numbers of Islamic

banks in Westerncountries

Islamicbanking

189

3.1 Respondents’ genderTable V shows that the number of the valid, eligible respondents is 156; thenon-eligible questionnaires, therefore, amount to 44. Table VI provides a classificationof the respondents on the basis of their gender; 43.6 per cent (56.4 per cent) of therespondents are male (female).

3.2 Respondents’ religionThe main goal of the study is to analyse the choices of Islamic bank’s products andservices in the UK. Although it has been documented in some recent studies that thereligiosity is an important factor of the customer choice of an Islamic bank(Wan Ahmed et al., 2008), in our case, the sample of respondents is not comprisedexclusively of Muslim customers. As inspection of Table VII reveals, Muslimsconstitute 58.97 per cent of total respondents with the remaining 41.03 per centcharacterising themselves as non-Muslims.

Valid 156Missing 0

Table V.Eligibilityof the respondents

Frequency %

Male 68 43.6Female 88 56.4Total 156 100.0

Table VI.Respondents’ gender

Fully Shari’ah-compliant banks Islamic windows

Bank of London and Middle East Ahli United BankEuropean Finance House AlburaqEuropean Islamic Investment Bank Bank of IrelandGatehouse Bank BarclaysIslamic Bank of Britain BNP Paribas

Bristol & WestCiti GroupDeutsche BankEurope Arab BankHSBC AmanahIBJ International LondonJ Aron & Co.Lloyds Banking GroupRoyal Bank of ScotlandStandard CharteredUBSUnited National Bank

Source: IFSL Research (2009)

Table IV.Islamic banksand Islamicwindows in UK

QRFM2,3

190

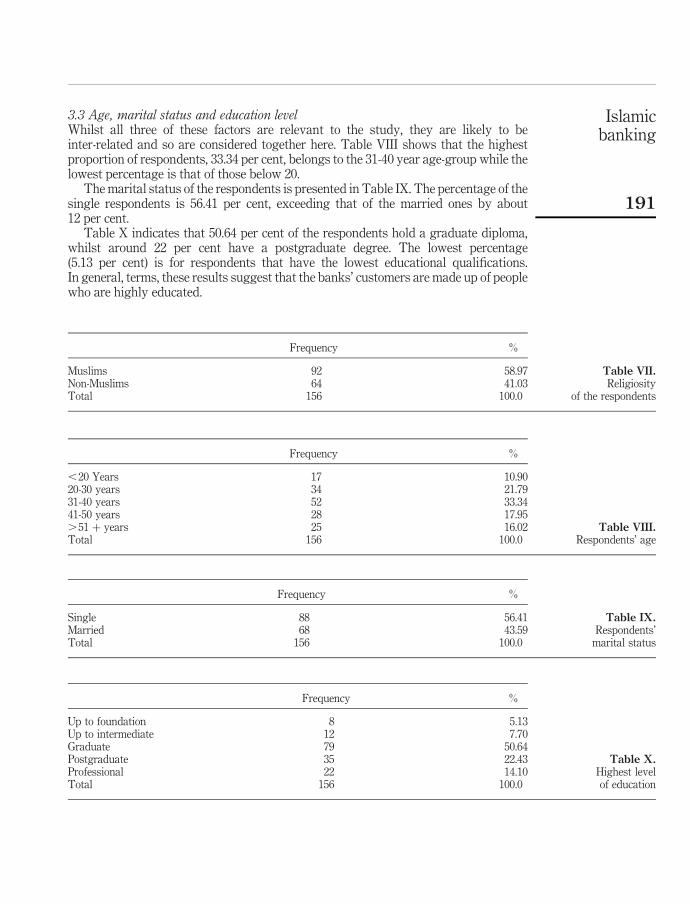

3.3 Age, marital status and education levelWhilst all three of these factors are relevant to the study, they are likely to beinter-related and so are considered together here. Table VIII shows that the highestproportion of respondents, 33.34 per cent, belongs to the 31-40 year age-group while thelowest percentage is that of those below 20.

The marital status of the respondents is presented in Table IX. The percentage of thesingle respondents is 56.41 per cent, exceeding that of the married ones by about12 per cent.

Table X indicates that 50.64 per cent of the respondents hold a graduate diploma,whilst around 22 per cent have a postgraduate degree. The lowest percentage(5.13 per cent) is for respondents that have the lowest educational qualifications.In general, terms, these results suggest that the banks’ customers are made up of peoplewho are highly educated.

,20 Years 17 10.9020-30 years 34 21.7931-40 years 52 33.3441-50 years 28 17.95.51 þ years 25 16.02Total 156 100.0

Table VIII.Respondents’ age

Frequency %

Single 88 56.41Married 68 43.59Total 156 100.0

Table IX.Respondents’

marital status

Frequency %

Up to foundation 8 5.13Up to intermediate 12 7.70Graduate 79 50.64Postgraduate 35 22.43Professional 22 14.10Total 156 100.0

Table X.Highest levelof education

Islamicbanking

191

3.4 Job type, duration and income levelThe next part of the questionnaire requested information relating to job type, durationand income. Table XI shows that the largest proportion of the respondents (32.05 per cent)have a management-oriented job, while 17.30 per cent are professionally employed.

The duration of employment is also an indicator of the demographic features of therespondents. Here, Table XII reveals that the highest percentage of the respondents(37.8 per cent) had experience ranging between five and ten years, while the lowestpercentage relates to respondents whose experience is longer than 20 years.

Income is likely to be informative about the sample of respondents, with an obviouspotential influence on the extent to which banking services are required. Table XIIIshows that the highest percentage of the respondents have annual income in the interval£15,000-18,000. The wealthier respondents’ percentage – whose income is in the interval£55,000-65,000 – is 9.61 per cent, the lowest figure in the table.

4. Selection criteria and Islamic banking: empirical findingsThe goal of this section is to determine the factors upon which the sample of customersbase their selection of banks. The factors we choose to investigate are primarily influencedby previous studies (Masood et al., 2009; Wan Ahmed et al., 2008). These factors are: low

service charges; religiosity or Islamic nature of the bank; reputation; recommendations (orword of mouth); staff friendliness; uniqueness; speed of service; bank location and parkingfacilities. Other studies (Rehman and Ahmed, 2008) adopt additional criteria such as onlinebanking, internal environment, knowledge about the business, bank timings, etc. but weconcentrate here on those used most often in prior literature. Our approach consists ofstatistically analysing the responses of the respondents regarding the nineaforementioned criteria. We attempt to rank these criteria in order to find out which isthe most important for the customers. We first present the statistical results pertaining toeach criterion separately; the order is based on the total percentage of respondentsstrongly agreeing or agreeing that a particular factor is important.

4.1 Low service chargesTable XIV shows that 55.76 per cent of the respondents strongly agree that low chargesare an important factor for the choice of the bank. As our sample of respondents is madeup of similar numbers of Muslims and non-Muslims, it appears reasonable to argue thatthe importance of low charges in bank selection decisions is not an exclusive belief ofeither type of customer.

4.2 Islamic nature of the bankWan Ahmed et al. (2008) argue that the religiosity of the customers may encourage them torank this factor at the top of their bank selection criteria. Here, we find that a bank beingIslamic is ranked as the second most important consideration (after low charges)(Table XV). As nearly 68 per cent of respondents agreed or strongly agreed that this wasan important consideration, such views were not the exclusive preserve of the Muslimswho took part in the survey. One might argue that this evidence is consistent with therebeing increased interest amongst UK customers as a whole in the Islamic banks that haveemerged in the recent years as a pivotal component of the British financial system.

4.3 Bank reputationThere is a common, prima facia belief that bank reputation is the most important factor incustomers’ decision making. However, here bank reputation was ranked only third,suggesting that the respondents place more importance on service charges and Islamicorientation. As Table XVI reveals, 52.56 per cent of the respondents strongly agree thatreputation is an important factor in bank selection, a further 10.89 per cent agreeing.

4.4 Recommendation from friends and relativesPrior literature suggests that the influence of friends/relatives may also be important tosome customers, and as Table XVII demonstrates, 48.07 per cent of the respondentsstrongly agreed with this fact. Only 10.25 per cent of the respondents strongly disagreedwith the view that such recommendations do not influence them in choosing a bank.

4.5 Fast and efficient servicesInspection of Table XVIII reveals that exactly 50 per cent of the respondents stronglyagree that speed and efficiency in services is important when selecting a bank; while

this was not seen as being as important as the factors outlined above, the evidence doessuggest that prospective customers attach importance to being served quickly and inan efficient manner.

4.6 Uniqueness of bank products/servicesA wide range of the products and services also appears to be an important criterion forcustomers when selecting their bank. This is evident from the results shown in Table XIX,where nearly 43 per cent of the respondents strongly agreed with the notion thatuniqueness of this type is important, while another 10 per cent agreed. However, whencompared to other criteria, the uniqueness of bank products/services is not one of the mostimportant and the relative priority given to this factor is therefore relatively low.

4.7 Staff friendlinessGood ties with a bank’s staff may be an important influence on customers; they mayeven prefer one bank to another on the basis of this factor. In our case, Table XXdemonstrates that 44.23 per cent of respondents strongly agree that staff friendliness isimportant, although more than 19 per cent of them do not.

4.8 Parking facilitiesThe convenience of parking facilities has been explored in prior literature and logicallyit might be relevant to customers, especially in peak hours. However, as Table XXIshows, less than half the sample claimed that this factor was important.

4.9 Bank locationThe results suggesting limited importance of parking facilities are consistent with theevidence regarding bank location; taken together these suggest that conveniencefactors are not the major determinants of customers’ choice of bank. As the figures in

Table XXII demonstrate, only 39.74 per cent of customers strongly agreed that locationwas important, the lowest figure in the survey.

4.10 Comparing findings across factorsSo far the analysis has proceeded one factor at a time, but here we analyse the resultsas a whole using the cumulative distributions derived from the data presented above.As can be observed from Figure 1, the ranking[6] of the criteria confirms that the

existence of low service charges is the most important factor. This result confirmsthose of many prior studies. Also evident from Figure 1 is that a bank being Islamic innature was the second most important influence on the respondents (despite less than60 per cent of the sample characterising themselves as Muslims in the survey).

4.11 Combining Islamic and conventional banksThe survey document also included a question about which kind of banks thecustomers are more prone to use. The results in Table XXIII show that nearly 50 per centof the respondents tend to use the products and services of the Islamic bank, whilst23.07 per cent express their preference for using conventional ones. The remaining19.97 per cent of the respondents used both types. Accordingly, the results point toa preference for Islamic products. Indeed, the total proportion of respondents whouse Islamic banks, either in isolation or in combination with conventional ones, is70.61 per cent. It is reasonable to argue that this high figure does not only reflect thefact that most of the respondents (although less than 60 per cent) are Muslims, butinstead indicates several additional reasons. As noted earlier, Islamic banks haveemerged as one of the pivotal components of the modern British financial environment.Indeed, the FSA has recently approved the establishment of many Islamic banks,which have, therefore, entered into rivalry with the conventional incumbent banks.Seeing the clear differences between Islamic banks and conventional ones (especially inthe design and terms of lending contracts, and the characteristics of their instrumentsand services more generally), non-Muslim customers may be placing value on thealternatives that Islamic banks provide. Wan Ahmed et al. (2008) claim that customerswhose religiosity index is high put the Islamic nature of the financial products at thetop of their criteria when choosing their bank. This does not seem to apply in a UKcontext, however, as the respondents, while placing importance on an Islamic nature,place more emphasis on low charges.

5. ConclusionThe long standing existence of a large variety of financial institutions in the UK,coupled with the emergence of several Islamic banks with the approval of the FSA,brings forth an important question regarding the bank selection criteria used bycustomers. Previous studies have attempted to understand the decision-making processby customers. Whilst many previous studies have focussed solely on the selectioncriteria of conventional bank customers, others embed Islamic banks in theirmethodology. For instance, Wan Ahmed et al. (2008) study the impact of the religiosityon the customers’ choice and find that when the religiosity index is high, the customersare more prone to place the Islamic nature of the bank at the top of their criteriairrespective of any other factors.

Frequency %

Conventional bank 36 23.07Islamic bank 89 50.64Both Islamic and conventional bank 31 19.97Total 156 100.0

Table XXIII.Bank used by

respondents

Islamicbanking

197

In the present study, we have used a sample of 156 respondents from the UK that includesMuslims and non-Muslims, as well as Islamic and conventional bank customers. Ourmethodological approach is partly borrowed from Masood et al. (2009) and involveda questionnaire aimed at finding out what drives the selection process of the customers.Our statistical results document that, irrespective of the demographic and the bank’snature, customers place see low services charges as their main selection criterion. Thisresult means that, in the UK at least, Muslims are more interested in costs than in whetheror not the bank is Islamic in nature. However, this latter criterion was placed second in thegeneral ranking, pointing to significant interest amongst the respondents in the Islamicbanks that have emerged in the UK recently. Furthermore, as Table IV demonstrated,there are not only several Islamic banks now operating in the UK, but also a large numberthat have Islamic windows available. This service is presumably intended to provideaccess to specificities such as Shari’ah-compliant financial instruments and services.In this context, future research might focus on an international comparison of the bankselection criteria by encompassing an index of religiosity and studying its impact on theprocess of selection as well as identifying similarities and discrepancies across countries.

Notes

1. The Shari’ah is the Islamic law that organizes the rules that must be followed by Muslims intheir transactions. It also prohibits many kinds of techniques common in conventionalfinance, such as the riba (interest) and the gharar (risky and complex financial instruments).

2. One should note that Shari’ah-compliant finance is based on the Muslims’ Holy Qur’an andthe Sunnah of the Prophet (i.e. his sayings, behaviour and advices). The two bases of Islamicfinance are the main source of the prejudices underlying the Islamic banking industry.

3. The riba is prohibited in Islamic economics. That is, all raised debts are not charged with arate. Debt contracts in Islamic economics differ from those in conventional finance in severalkey respects.

4. A higher degree of religiosity means that the customer had received a higher formal religiouseducation exposure.

5. Returned questionnaires were deemed as ineligible if some of the responses were missing.

6. Masood et al. (2009) use the mean value rule to rank their criteria. The x-axis in Figure 1shows the choices that are available to the respondents in every question (i.e. strongly agree,agree, uncertain, disagree, strongly disagree.).

References

Denton, L. and Chan, A. (1991), “Bank selection criteria of multiple bank users in Hong Kong”,International Journal of Bank Marketing, Vol. 9 No. 5, pp. 23-34.

Devlin, J. and Gerrard, P. (2005), “A study of customer choice criteria for multiple bank users”,Journal of Retailing and Customer Services, Vol. 12 No. 4, pp. 297-306.

Erol, C. and El-Bdour (1989), “Attitudes behaviour and patronage factors of bank customerstowards Islamic bank”, International Journal of Bank Marketing, Vol. 7 No. 6, pp. 31-7.

Gerrard, P. and Cunningham, J.B. (1997), “Islamic banking: a study in Singapore”, InternationalJournal of Bank Marketing, Vol. 15 No. 6, pp. 204-16.

Hegazy, I. (1995), “An empirical comparative study between Islamic & commercial banks’selection criteria in Egypt”, International Journal of Commerce & Management, Vol. 5No. 3, pp. 45-61.

QRFM2,3

198

IFSL Research (2009), available at: www.scribd.com/doc/21213777/IFSL-Research-Islamic-Finance-2009

Kaynak, E., Kucukemiroglu, O. and Odabasi, Y. (1991), “Commercial bank selection in turkey”,International Journal of Bank Marketing, Vol. 9 No. 4, pp. 30-9.

Khazeh, K. and Decker, W.H. (1992), “How customers choose banks”, Journal of Retail Banking,Vol. 14 No. 4, pp. 41-4.

Laroche, M. and Taylor, T. (1988), “An empirical study of major segmentation issues in retailbanking”, International Journal of bank Marketing, Vol. 6 No. 1, pp. 31-48.

Martenson, R. (1985), “Consumer choice in retail bank selection”, International Journal of BankMarketing, Vol. 3 No. 2, pp. 64-75.

Masood, O.M., Aktan, B. and Amin, Q. (2009), “Islamic banking: a study of customer satisfactionand preferences in non-Islamic countries”, International Journal of Monetary Economicsand Finance, Vol. 2 Nos 3/4, pp. 261-85.

Rehman, H. and Ahmed, S. (2008), “An empirical analysis of the determinants of bank selectionin Pakistan: a customer view”, Pakistan Economics and Social Review, Vol. 4 No. 2,pp. 147-60.

Siddiqi, M.N. (1983), Banking Without Interest, The Islamic Foundations, Leicester.

Tan, C. and Chua, C. (1986), “Intention, attitude and social influence in bank selection: a studyof oriental culture”, International Journal of Bank Marketing, Vol. 4 No. 2, pp. 27-88.

United Nations (2009), Population and Vital Statistics Report, Statistical Papers, Series AVol. LXI, No. 1, Statistics Division, Department of Economic and Social Affairs, UnitedNations, New York, NY, September.

Wan Ahmed, W., Ab Rahman, A., Ali, N.A. and Seman, A.C. (2008), “Religiosity and bankingselection criteria among Malayas in Lembah Klang”, Shariah Journal, Vol. 16 No. 2,pp. 279-304.

Further reading

FSA (2007), Report, November, available at: www.fsa.gov.uk

Mosad, Z. (1996), “Bank strategic positioning and some determinants of bank selection”,International Journal of Bank Marketing, Vol. 14 No. 6, pp. 12-22.

Corresponding authorWalid Mansour can be contacted at: [email protected]

Islamicbanking

199

To purchase reprints of this article please e-mail: [email protected] visit our web site for further details: www.emeraldinsight.com/reprints