1 An Investigation into the Awareness, Understanding and Perceptions Held by Consumers of and Towards Islamic Banking and Finance Qazim Ali Sumar May 2009 Dissertation submitted to the University of Leicester in partial fulfilment of the requirements for the degree of BA Management Studies

Transcript

1

An Investigation into the Awareness, Understanding and Perceptions

Held by Consumers of and Towards Islamic Banking and Finance

Qazim Ali Sumar

May 2009

Dissertation submitted to the University of Leicester in partial

fulfilment of the requirements for the degree of BA Management

Studies

2

Chapter 1 – Introduction – 1.1 An End to Capitalism? 5

Chapter 2 – Literature Review 2.1 History of Contemporary Economic Thought 7

2.2 Failures of the Free Market Capitalistic Ideology 8

2.3 The Ills of the Ideology 9

2.4 Islamic Economic Thought, The Ailment? 11

2.5 Islamic Banking and Finance 13

2.6 Opportunities for Islamic Banking and Finance 16

2.7 Challenges 17

Chapter 3 – Methodology 3.1 Multi Strategic theory 20

3.2 Research Design 21

3.3 Analysis 23

3.4 Sample 24

3.5 Channel 25

Chapter 4 – Data Analysis 4.1 Respondent Description 26

4.2 Awareness 26

4.3 Understanding 29

4.4 Perceptions 32

4.5 Triangular Causation Hypothesis 41

Chapter 5 – Conclusions 5.1 Awareness, Understanding and Perceptions 43

5.2 A Platform for growth 44

5.3 Limitations 47

5.4 Recommendations 48

5.5 Reflections 49

Chapter 6 – References 6.1 References 50

6.2 Appendices 63

3

Acknowledgments

This dissertation, in its entirety is dedicated to Zahra, her honourable father, beloved husband

and exemplary sons. Whose guidance continues to shed its light upon the paths I tread. I

extend my appreciation to family and friends, for their kind words of encouragement.

Heartfelt gratitude is offered to my supervisor, who throughout this arduous journey, was truly

a sincere guide, offering the best of advice, and picking me up when I fell.

4

Abstract

One of the substitutes being proposed to replace the current financial system is the

paradigm surrounding Islamic finance. It proved crucial therefore to provide an evaluation of

this proposal, in light of its opportunities and challenges, the foremost of the latter being

discovered as the lack of consumer awareness and understanding of the sector, alongside

the void of managerial insight of consumer perceptions. It was therefore sought to

investigate these aspects, in hope of providing practicing managers the insight they needed

to overcome the challenges faced by the sector and generate growth. The research

incorporated quantitative alongside qualitative elements, the respective principles of which

combined, and became manifest in an interview. Research was focused in Harrow, borough

of London, due to its unique demographic diversity, the sample selected was 15 Muslim / 15

Non Muslim respondents, in order to reflect general opinions, as Islamic Banking and Finance

is increasingly attempting to capture the mainstream market. Levels of awareness and

understanding were found to be significantly low across the sample. The underlying factors of

which were found to be excessive media influence on consumer perceptions. We proposed

the “Triangular causation hypothesis” as an explanation for the lack of awareness and

consequently demand.

5

Chapter 1 – Introduction

1.1 An End to Capitalism?

On April 2nd of 2009, world leaders assembled in London for the G20 summit. The focal

issue was to identify the factors which prompted the current financial crisis and to

propose viable solutions for future prevention. The unequivocal conclusion reached was

that major failures in regulation had been the main catalyst for the crisis; and that

enhanced regulations alongside increased government oversight were vital in the

restructuring of the economic system (Kennedy & Donaldson 2009). Over the past 18

months we have witnessed job losses in the millions, homeowners being forced out of

their homes and severely stinted economic growth; while company directors, managers

and derivative traders responsible for the crisis; have walked away with bonuses

exceeding $500 million (BBC 2009B, Wang et al 2008). Free market capitalism has in

effect increased the autonomy of financial markets to a level of societal detriment (Smart

2003). Alongside enhanced regulation, world leaders have expressed the need for an

ethical code to be embedded in the market. Barack Obama recently stated “It’s not about

dollar and cents, it’s about our fundamental values” (Obama 2009), Gordon Brown

similarly stated “Our markets are in need of morals” (Cooper 2009). In light of economic

reform, a system encompassing regulation and morality; while simultaneously allowing

markets to flourish is highly sought after. Cooper (2008) on this note suggested religion,

with its ethical connotations should not be afraid to voice opinions in search for a global

solution.

The Islamic Banking and Finance (IBF) sector, built on the ideas of Islamic economic

thought yielded to this call many decades ago. It incorporates the morality, balance

between regulation and autonomy world leaders are searching for. Furthermore the

regulations and principles, to which it adheres, meant a complete aversion of the

financial storm; nor would such a crisis even be conceivable (Qadri 2009).

6

In fact, in light of the crisis the sector experienced renewed growth at 30% and

celebrated several new banks openings its doors, while many conventional banks were

closing theirs (Oakley 2009; Safa 2009).

The sector having avoided the financial storm drew the attention of numerous

economists; with experts predicting exponential growth in the near future and others

even proposing its complete implementation, providing it overcomes the obstacles

standing in its way. The foremost of these considered to be consumer’s deficiency of

awareness and understanding of the products and services it offers, and a void of

managerial insight into what consumers actually think and feel about them.

With the proposals of a refurbished economic and financial system bearing large

similarities to IBF, it proves crucial to address the aforementioned barriers of IBF

preventing it from such growth or even implementation. This dissertation therefore,

seeks to investigate the awareness, understanding and perceptions held by consumers of

and towards Islamic Banking and Finance. The findings will provide institutions offering

Islamic financial services, a platform on which to formulate strategies in an attempt to

overcome the challenges it currently faces.

In chapter 2 we commence the evaluation of contemporary literature concerning Islamic

economic thought and IBF in light of the failures of modern economic thought. Chapter 3

outlines the methodology employed alongside its epistemological and ontological

grounding. Chapter 4 provides the analytical discussion pertaining to the findings.

Chapter 5 will draw conclusions stemming from the data collection and literature review;

recommendations and reflection will subsequently be offered at the close of this chapter.

7

Chapter 2 - Literature Review

This chapter endeavours to evaluate the vast body of literature concerning the failures of

contemporary economics and the solutions offered by the Islamic economic paradigm.

We venture to analyse the theory of IBF in views of its application, challenges and

opportunities.

2.1 History of Contemporary Economic Thought

The principles of modern economic thought were extracted from Adam Smith’s (1723 -

1790) famous ‘The Wealth of Nations’; in which he outlined the fundamentals of free

market ideology. A theory which proposed the pursuance of self interests in a market

void of regulations and government intervention would eventually result in societal

welfare (Smart 2003). His ideas were implemented in the early 1900’s, and have

dominated most of the 20th century. The first major collapse of free market ideology

came in 1929 and lasted throughout the thirties, better known as the Great Depression.

Economists attributed the failure to banks predominant involvement in risky activities

(Khan 1999). Unemployment worldwide reached record levels, in the U.S a staggering

25% unemployment was witnessed; many believed this was the end of the free market

ideology (Wolf 2009). What followed was managed capitalism through the ideas of

Keynes, largely based on the manipulation of fiscal policies. As a result, the U.S

experienced thirty years of continuous growth, a period referred to as ‘les trente

gloriuses’. However in 1973, the U.S entered upon recession, and we saw a return to free

market capitalism; termed neo liberalism (ibid). The pursuance of wealth contributing to

optimal social welfare hypothesis was revived (Ibrahim 2000). The ‘rational economic

man’ whose raison d'être was capital accumulation and Say’s law its sole point of

reference, dictating economic health to be the sole result of market fluctuations (Chapra

1999), had been resurrected.

8

2.2 Failures of free market capitalistic ideology

The employment of free market ideology has arguably led to a number of financial crises,

most notably the 1929 Wall Street crash, Black Monday of 1987, Black Wednesday of

1992, the 1997 Asian crisis, the 2000 dot.com crash and the current subprime crisis. The

main instigators of which have been identified as a lack of regulation, speculation and

interest rates (Smart 2003).

2.2.1 The 2007 Subprime crisis

The current crisis has so far taken $3 trillion of bailout and liquidity injections by various

governments in an attempt to relieve its severity (Chapra 2009). The World Bank and

International Monetary Fund (IMF) have predicted slowdown in global economic growth

similar to levels post World War 2 (Farooqi 2009). It has so far claimed 5.1 million jobs in

the U.S alone, experts predict that levels could top 10% by 2010 (Chandra & Benjamin

2009). In the U.K record levels of unemployment have been reached at 2 million (Taylor

2009). The excessive and imprudent lending in the U.S led to the subprime market

collapsing. The bad debt generated was sold worldwide together with good debt through

financial vehicles known as collateralised debt obligations (Chapra 2009). As homeowners

began to default, institutions suffered tremendous losses; leading to the subsequent

credit crunch. The outstanding debt of derivatives has been estimated at $600 trillion,

more than 10 times the size of the world economy; rightfully earning the title ‘financial

weapons of mass destruction’ (ibid). The lack of regulation allowed for such loans to

primarily be issued and secondly be sold. Free market principles encourages financial

markets to increasingly finance its operations on debt, Wolf (2009) reports the U.S

financial sector aggregate debt escalating from 22% of GDP in 1981 to 117% in 2008,

whereas in the UK; the figure reached approximately 250%.

9

A few of the institutions that have failed or been nationalised as a result of the crisis

include Morgan Stanley, Lehman Brothers, AIG, Northern Rock and recently Lloyds TSB;

however it has by no means contained itself to the financial sector, Woolworths and

giant General Motors have also failed (Qadri 2009).

2.3 The ills of the ideology

Free market capitalism has undoubtedly wrought inefficiencies out of the market,

benefiting consumers through enhanced choice and lower prices; yet the question is, at

what price? The income inequality between rich and poor nations is increasing (Wild et al

2008), while simultaneously the lowest levels of foreign aid contributions by developed

countries have been recorded, despite their increasing wealth (Ahmed 2000). Drastic

shifts have also been witnessed in employment. Labour under the free market is

classified alongside the means of production, reducing people to mere commodities;

Slater & Tonkiss (2001) refers to the trend as the liquidation of labour. Klein (2000) has

reported extensively on the downward pressure capitalism has had on wages, labour and

environmental conditions. Reports from the U.S testify to the income inequality; Durrani

(2008) found executives earning 520 times more than the average worker. AIG is yet

another example in light of which Barack Obama commented “...is a corporation that

finds itself in financial distress due to recklessness and greed, It’s hard to understand how

derivative traders at AIG warranted any bonuses, much less than $165m in extra pay,

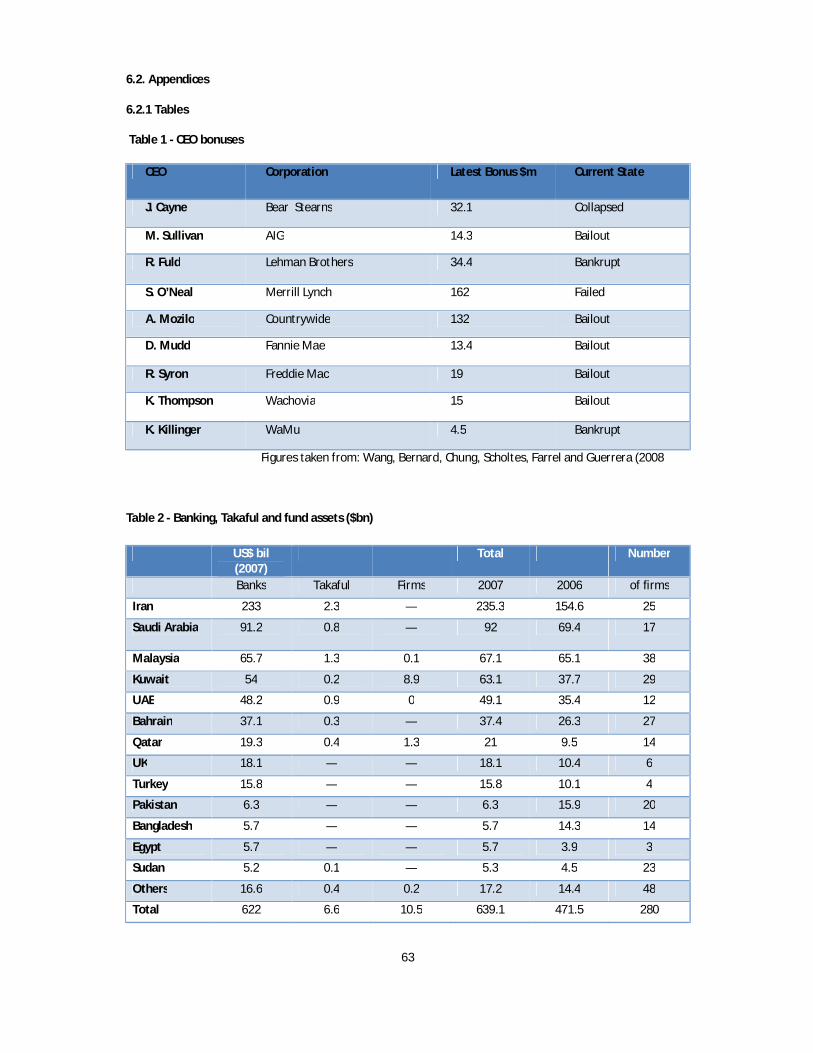

while remaining afloat with tax payers money” (Obama 2009). Furthermore table 1

(insert table 1) show CEO’s of major financial institutions, receiving outrageous bonuses

while their companies were failing. Durrani (2008) on these grounds proposed that what

we’re experiencing, rather than an economic or financial crisis; is the catastrophe of

human values.

10

2.3.1 Interest as a form of exploitation

The inability of homeowners to make interest payments was the main catalyst of the

current crisis. Ahmed (2000) proposes interest as being detrimental to economic activity

as a whole.

As interest payments along with principal amounts are made incumbent upon the

borrower regardless of financial conditions, the borrower; a medium sized business for

the sake of argument, will recover costs by raising, thereby aggravating inflation. Or

perhaps cut costs by downscaling employment levels. Effects of interest rates are evident

in economic tendencies.

High interest rates are associated with a reluctance to spend, negatively impacting

economic growth and new employment; whereas low interest rates are coupled with

enhanced spending leading to positive economic growth, business expansion and job

creation (Ibid). The charging of interest, Saidi (2008) argues, results in the systematic

transfer of money from those that have less to those that have more, leading to the

circulation of wealth among the affluent; evident in the widening gap of income and

poverty levels.

The widespread devastation following the crisis, as well as issues addressed in previous

sections, clearly suggests the failure of free marker ideology; and its theory of social well

being. The very definition of free market capitalism by Marx, “...its primary objective is

not the satisfaction of human need, but the realization of profit” (Smart 2003:9), indicates

the level at which society is prioritized within the free market. Furthermore, Keynes on

such a society wrote: “The love of money as a possession – as distinguished from the love

of money as a means to the enjoyments and realities of life – will be recognized for what

it is, a somewhat criminal, semi-pathological propensities which one hands over with a

shudder to the specialists in mental disease” (1963; 369).

11

2.4 Islamic Economic Thought, The ailment?

Muhammad Baqir Al-Sadr (1935-1980) pioneered the revival of Islamic economic

thought. In his 1960 magnum opus ‘Iqtisaduna’ (‘Our Economics’), he described a

socioeconomic order which sought to replace the capitalistic and socialist principles

which were dominating the Muslim world; an order he believed more capable of solving

the contradictions of the capitalistic system and more able to satisfy human needs (Aziz

n.d). Under the system a welfare state would be instituted, in which the government held

responsibility for the provision of minimum essential needs of society; thereby ensuring

the economic welfare of citizens. This would be achieved through taxes on income and

savings, in adherence to Islamic law (Seestani 2000). These instruments allow for the

funding of the welfare state, simultaneously serving as preventionary mechanisms

against wealth amassing and circulating among the affluent minority.

It is therefore unlike the capitalist state which leaves all functions to fluctuations of the

market, and nor is it like the socialist/communist order advocating full state ownership.

The state merely directs the direction of economic activity, while giving individuals the

right of private ownership (Aziz n.d). The intervention by the government within this

paradigm is therefore not to hinder freedom of trade, but rather oversee economic

activity in ensuring societal well being (Presley & Sessions 2004).

Even though the advent of IBF was relatively recent, its foundations lie in the Holy Quran

(sacred scripture revealed in the 7th century) and the Sunnah (sayings and actions of the

Prophet Muhammad p.b.u.h.f) (Monger & Shadeh 2008). From these sources directly, or

indirectly through analogy and reasoning; Shariah law is derived (Ainley et al 2007; Al-

Omar & Abdel-Haq 1996). It addresses every facet of life, ranging from social, political

and economical spheres; guiding man not in only in the relationship with God, but also

with members of society (Islam 2008). Following are a few verses from the Holy Quran

forming the basis of the Islamic economic/financial system:

12

Chapter 3, Verse 130: “Oh you who believe! Devour not usury (riba), doubled and

multiplied; but fear God that ye may prosper”

Chapter 30, Verse 39: “And remember whatever you may give out in usury (riba) so that it

might increase through other people's possession will bring you no increase in the sight of

God - whereas all that you give out in charity, seeking God's countenance, will be blessed

by him for it is they, they who thus seek His countenance that shall have their recompense

multiplied”

The prohibition of usury/riba forms the basis of the IBF system. Al-Omer & Abdel-Haq

(1996) describe riba as the premium the borrower must pay to the lender along with the

principal amount as a condition for the loan or for an extension in its maturity (modern

day interest), this form of riba is not permissible within IBF as it is seen as exploitative;

bearing negative effects on the economy as previously discussed.

It’s worth mentioning that IBF is not alone in its stance against interest rates and

speculation (Dar & Presley 1999), rather western theorists such as Minsky, Greenwald,

Stiglitz, Bernante and Gertler have all identified a relationship between interest rates,

macroeconomic instabilities and cyclical fluctuations (Matthews et al n.d). There is even

reference within the Old Testament to the prohibition of interest, within the chapter of

Exodus.

The Islamic paradigm encourages entrepreneurship and innovation ensuring maximum

utilization of global resources and economic growth; channelling rewards to individuals

alongside society (Bhatti & Khan 2008). In addition to interest, Shariah prohibits

speculation, business risk is obviously inescapable in any system, rather in reference to

derivatives, swap, futures and CDO’s, the main catalysts of historical financial crises; are

not allowed due to the devastation they cause. Areas of investment are also restricted

within the system, investment in products/services deemed impermissible by the religion

such as alcohol, weapons, pork and pornography are not allowed (Islam 2008).

13

As you can see, Islamic economics is more than just interest free banking, rather it is a

complete concept of an economic system; rejecting many of the norms associated with

contemporary thought (Ahmed 2000); “preferring to marry the freedom and innovation

of the market economy to the fairness and balance of social democracy” (Hassan 2008;

28)

2.5 Islamic Banking and Finance

The establishment of IBF was introduced to allow Muslims to bank in adherence to

religious principles (Zaher & Hassan 2001). Today’s main fully Shariah compliant Islamic

players such as Kuwait Finance House, Dubai Islamic Bank and Faisal Islamic banks were

formed during the 70’s as a result of increased liquidity in the Middle East region

following the boom in oil prices (Grose 2008, Khan & Bhatti 2008C).

In the early 1980’s Iran, Pakistan and Sudan transformed financial sectors to fully

function along Islamic principles (Ibid).

Despite IBF’s 40 year history, it was only following the millennium shift the sector began

experiencing increased growth and sophistication. Products and services currently range

from current/savings accounts, home financing, asset leasing, bonds, insurance, private

equity and asset management through to corporate financing (Ibid).

Retail Islamic products began appearing on UK high streets in the early 1990’s but were

limited in scale (Ainley et al 2007); the first insurance products were introduced as

recently as 2008 through U.K’s and western Europe’s first Islamic insurance company;

‘Principle Insurance’ (Oakley 2008). The U.K was also home to the wests first wholly

Shariah compliant bank, Islamic Bank of Britain (IBB); established in 2004 (FSA 2006). The

sectors growth and potential has led conventional financial institutions such as HSBC,

Citigroup, Merrill Lynch, Deutsche Bank, Barclays and Lloyds TSB; (Zaher & Hassan 2001,

Bundhun 2009) to establish Islamic subsidiaries or ‘windows’ attempting to capitalize on

the growing market (Maurer 2001).

14

The U.K government has shown distinctive determination in the promotion of IBF, with

the intention of establishing London as the western financial centre of IBF (Landberg &

Vina 2006). Efforts include pursuing avenues towards the issuance of Islamic government

bonds, as well as the abolishment of double-stamped duties in a move to further

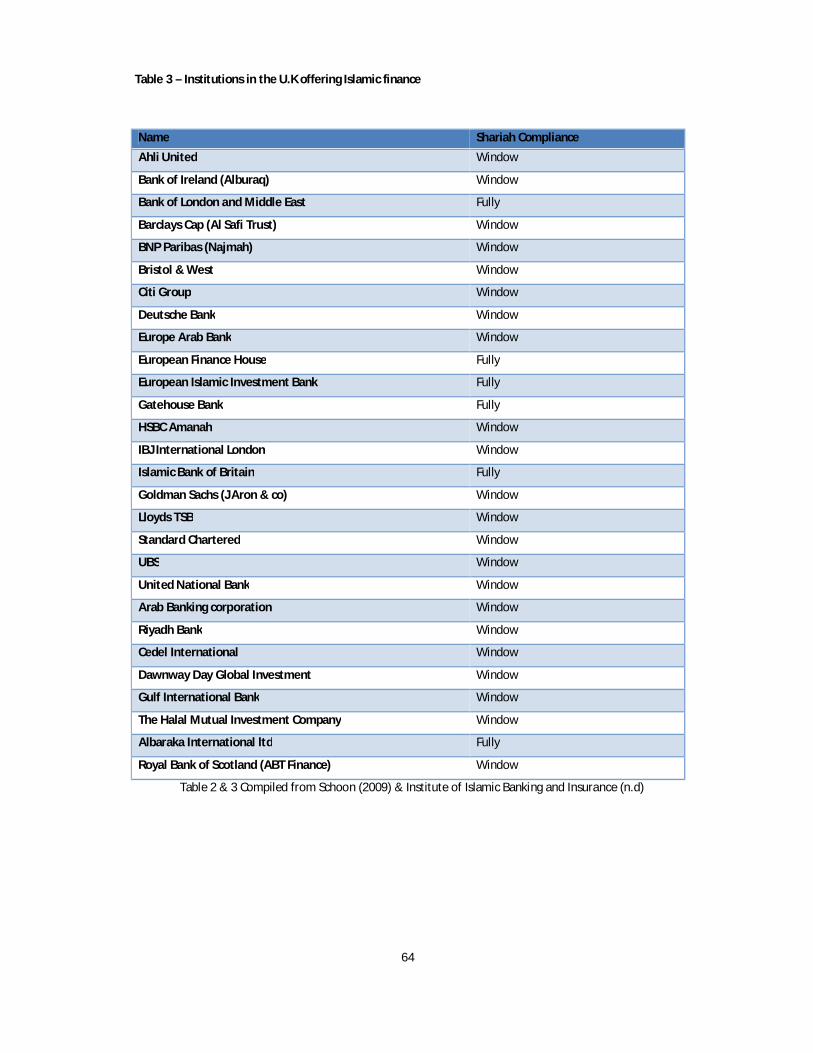

encourage Islamic mortgages (The Economist 2008B). Table 2 (insert table 2) is indicative

of the U.K’s success in pursuance of its objectives; by achieving ranking above Muslim

states such as Pakistan and Egypt. Furthermore, table 3 (insert table 3), lists the 5 wholly

Islamic and 23 subsidiaries of conventional banks who contribute to the success (Shoon

2009).

2.6.1 The Theory in Practice

The range of products and services are based on 4 main principles, Musharaka,

Murabaha, Mudaraba and Ijara (Insert item 2 for glossary of terms) (Al-Omar & Abdel-

Haq 1996, HSBC Amanah, Khan & Prodhan).

The Current/Savings accounts are based on Murabaha principles; where rather than

payable interest, the funds are invested in commodities, which are subsequently sold to

the bank at a profit earning both client and bank dividends (HSBC Amanah). The

principles behind mortgages are Murabaha, diminishing Musharaka or Ijara. In the

preceding two, the bank purchases the property as a proxy, and then resells it to the

client through fixed installments earning the bank a profit. Upon completion of payment

schedule, property rights are transferred to the client. Ijara, is similar but is essentially a

substitute for leasing, where the installments represent rental payments (Khan &

Prodhan 1992).

Musharaka and Mudaraba principles apply to the investment and corporate finance

products. The latter resembles venture capitalism, where the client provides expertise

and management while the bank provides capital. Profit is shared at pre agree ratios,

whereas the loss is borne solely by the provider of capital.

15

Musharaka can be referred to as a joint venture, where both parties contribute funds as

well as management and expertise. Profit is shared on pre-agreed terms whereas loss is

borne in proportion to capital contribution (Al-Omar & Abdel-Haq 1996). The client/bank

relationship can therefore be likened to mutual shareholders, where profits and losses

are aligned to collective performance (Qorchi 2000). This consequently means Islamic

institutions will be in competition not only with conventional banks, but with venture

capital firms, investment companies and merchant banks as well (Naser & Moutinho

1997).

Due to banks enhanced exposure to risk, the likelihood of client defaults is reduced.

DiVanna (2009) argues that based on the relationship structure, banks will endeavor to

provide more support and are likely to restructure terms; essentially meeting the needs

of clients. IBF in this way assists consumers in securing much needed finance in

circumstances where they perhaps would have failed without it (Tlemsani & Matthews

2004, Saidi 2008). Due to speculation restrictions in instruments such as derivatives and

CDO’s; investors along with society are protected from excessive risk (Balfour 2008, Desai

2008).

IBF’s reliance on classical funding through depositors, rather than on money markets like

their conventional counterparts, who in 2008 were lending out £700 billion in excess of

their deposit base (Hassan 2008, The Economist 2008) means they are less affected by

credit freeze’s (Martin 2008, Billing 2009).

2.6.2. Past, current and predicted growth of Islamic Finance

Wilson’s (1999) prediction of IBF’s ‘meager’ future could not be farther from the truth.

The sector is flourishing in Africa, Asia, Europe and to a lesser extent in North America;

reports show the existence of 300 financial institutions across 70 countries providing

Islamic finance (Khan & Bhatti 2008).

16

The sector has experienced annual growth of 15-20%, however accelerated to 30% over

the past two years (Khan 2009, Safa 2009); Deutsche Bank head of operations has been

quoted stating “Islamic Finance is growing at the speed of light” (Tett 2006; 1).

IBF’s assets under management were estimated by the Boston Consultancy Group at

$400bn in 2008, up from $100bn in 2000 (2008); growing at 23% compared to 10%

compared to assets under conventional management (Bremner & Shameem 2007).

Standard & Poor’s estimate however that the potential market lies close to $4 trillion,

suggesting 90% of the market has yet to be capitalized (2007). Khan & Bhatti (2008) make

similar predictions; within 10 years they propose 40-50% of global Muslim savings being

held under IBF’s management.

2.7 Opportunities for Islamic Banking and Finance

The collapse of financial markets has provided an opportunity for IBF to flourish as many

have lost confidence in conventional finance. The trend towards ethical consumption

coupled with the rapid growth of Islam is briefly discussed in subsequent sections.

2.7.1 Islam, the fastest growing religion

Reports suggest that Muslims account for approximately 20-25% of the world’s

population (The Economist 2008B, Saidi 2008), and is the world’s fastest growing religion

(Albrecht 1998). IBF instruments currently represent 1% of the global Muslim

population’s financial instruments and therefore represent a huge opportunity (The

Economist 2008B).

Paul Sherrin, head of Lloyds Islamic operations said “Britain is home to a large and fast-

growing Muslim community, but many have found their financial needs left wanting”

(Abu-Shakra 2006; 2, Anker 2006). Reports estimate 2-3 million Muslims in the U.K,

representing 50% of ethnic minorities and 3-5% of the total population.

17

The 5,000 richest Muslims in the U.K are reported to have liquid assets of over £3.6

billion, and 5,000,000 have annual incomes in excess of £30,000, making these excellent

prospects for IBF. There are also 0.5 million Muslim visitors annually spending

approximately £600 million (FSA 2006, Duckers 2002, Mawson 2002).

2.7.2 A shift towards ethics and morality

Since the neo liberal turn in the 1970’s we have witnessed an increased interest in ethical

investment and corporate social responsibility (Snider et al 2003). Reports reveal that in

2003, 11.3% of total U.S assets under professional management were invested in ethical

instruments (Benson et al 2006). The ‘greed is good’ mantra which led to the crisis has

affected consumer’s confidence; a Merrill Lynch report suggests consumers will become

more conservative as to where they keep their money (Siddiqi 2008, Miller 2009). On this

note the director of HSBC Amanah Malaysia suggested IBF not being restricted to

conservative or radical Muslims but has become mainstream business (Shameen 2005).

Transactions within IBF are the epitome of honesty, justice and equity (Haron & Azmi

2008); hence embracing the philosophical underpinning of ethical investments.

Furthermore the principles and structures of ethical financial products are more or less

identical to IBF (Knight 2006). The potential for IBF therefore stretches beyond religion,

race or nationality; it appeals to the morality within every man.

2.8 Challenges

The main obstacles of IBF today comprise of the lack of consistency in regulations, the

void of human capital and more importantly the unawareness of IBF’s theological

backdrop.

18

2.8.1 Lack of regulations and regulators

Shariah being derived partly through reasoning and analogy, differences in interpretation

are inevitable and have become a source of inconsistency across banks and products

(Khalaf 2007). The 2002 central bank summit in Washington aimed to address this issue

by pursuing avenues towards establishing an international regulating board

(Sundararajan & Errico 2002), however with a lack scholars grounded in Islamic

jurisprudence alongside an in depth understanding of financial instruments, there are no

regulators to actually serve on the board (Khan & Bhatti 2008, Singh 2009, Bokhari 2008).

Even regular IBF bankers are proving difficult to locate. Iqbal & Mirakhor (1987) and

Alibhai (2006) suggest this is due to the high levels of requirements IBF bankers must

meet; knowledge of conventional finance, Islamic finance, Shariah law and investment

evaluation capabilities, due to the nature of IBF. These factors have translated into

growth hindrance, as innovation, development and consistency requires bankers and in

this case scholars (Poolton & Ismail 2000, Noman 2002).

2.8.2 Awareness, Understanding and Perceptions.

The lack of consumer awareness of IBF and its products has been suggested to be one of

the main barriers in preventing the sector from reaching its potential (Cunningham &

Gerrard, Naser et al 1997, Gait & Worthington 2007). Secondly, those that are aware of

its existence do not understand how they work and are oblivious to the product

structures (DiVanna 2009, Zaher & Hassan 2001). Despite such findings, not much seems

to have been done by banks in order to educate or even promote their products. As Sole’

(2007) emphasized; “the degree of success will lie in whether potential customers are

informed and understand the products” (16). Yet both the HM Treasury (2008) and

Murtuza (2002) agree and acknowledge the minimal mainstream media interest

surrounding IBF; in stark contrast to general promotion and advertising theories; the

purpose of which are to build awareness; in an attempt to remind consumers of the

existence of the brand or product and entice purchase (Fill 2002).

19

Little research has discussed the underlying reasons for this phenomenon; we propose

that the cause may lie in the opinions of Islam held by the general population. Mazrui

(2006) suggests that the image of Muslims across the globe is often one of negative

contexts; Karbhari, Naser & Shahin (2004) concurred with Mazrui in regards to the poor

attitude often held of Islam, this issue will form part of the ‘perceptions’ aspect of the

investigation.

Through the evaluation of the literature we identified many of the economic and social

ills associated with free market ideology. Economists in unison are blaming the system

for the current financial crisis. The analysis of the literature allowed us to grasp the

solutions Islamic economic encompassed; which would lead to the avoidance of the all

too often market collapses. It highlights then, with the current paradigm shift in

economic policy, and IBF a proven substitute; alongside a growing Muslim population

and enhanced interest for ethical investment, the importance of the examination as to

where the industry stands with consumers. The findings of which, will enable institutions

to informatively pursue avenues in which to generate growth.

This study then, seeks to investigate the levels of awareness, understanding and

perceptions held by consumers of and towards IBF; within the general population of

London Borough Harrow.

20

Chapter 3 – Methodology

In this chapter we venture to describe and evaluate the chosen methodology and the

underlying factors for its employment. An outline of each component of the research

process will be provided.

3.1 Multi Strategic Theory

Research tends to encompass a particular research theory, pending upon nature of

research; it will either be quantitative or qualitative or a combination of both. The

research theories can “...be viewed as exhibiting a set of distinctive but contrasting

preoccupations; that reflect epistemologically grounded beliefs about what constitutes

acceptable knowledge” (Bryman & Bell 2003;21); the theories in essence seeks to discern

matters in contrasting fashions. Quantitative research emphasizes quantification in the

collection and analysis of data. It adopts a deductive approach to the relationship

between theory and research, in an attempt to test hypothesis (ibid). The focus of

qualitative research however “lies with depth rather than breadth” (ibid; 289). It

predominantly emphasises an inductive approach to the relationship between theory

and research, where emphasis is placed on the generation of theories. The

epistemological position can be described as interpretivist, meaning that an

understanding of the social world is sought rather than the static view of social life which

quantitative research provides (ibid). The ontological position associated with qualitative

research can be described as constructionist implying that social properties are outcomes

of the interactions between individuals, in contrast to the objectivist ontology assigned to

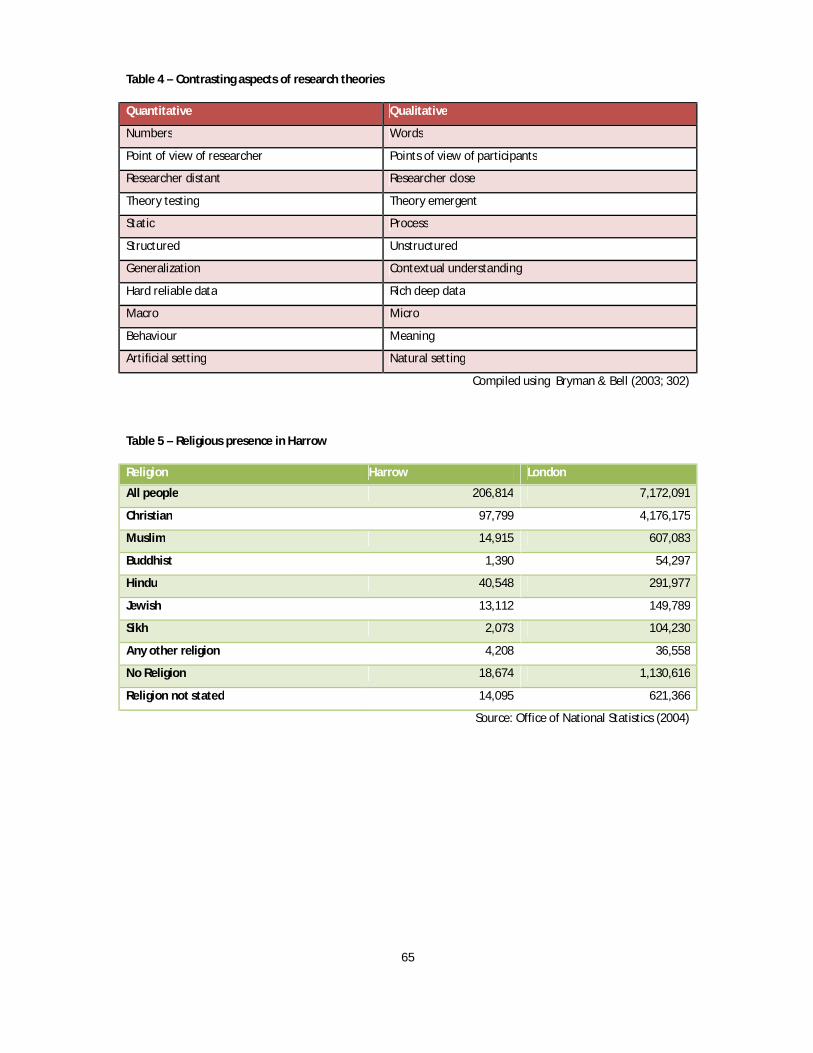

quantitative methods that reifies the social world (ibid). In table 4 (insert table 4) you

can further see the contrasting concepts of the two theories.

The use of each theory can be justified by its own merits. Quantitative research tends to

signify higher validity and reliability, through the opportunity and ease of re-testing,

establishing causation by using variables and the possibility of generalising findings

21

(Bryman & Bell 2003). However, what this means as we briefly mentioned earlier, is that

it fails to distinguish people and social institutions from the world of nature. It describes

phenomenon through mere figures thereby discarding any social context (ibid).

In contrast to which qualitative research seeks to explore the experiences, perceptions

and feelings of participants; in relation to contextual characteristics (ibid). The contextual

significance is extremely important in this investigation. With the current economic

climate and sudden escalated growth of IBF, it proves crucial to analyse the perceptions

of consumers in light of these factors. However qualitative research is also far from ideal.

Criticisms levelled at the theory include issues of subjectivity, validity and problems with

replication and generalisation (Kumar 2005). Furthermore, the process of coding in the

analysis of qualitative data has been accused of being unreliable; due to the inevitable

impact of researchers own demographics while interpreting responses (Bryman & Bell

2003).

As the research question comprises of two distinct aspects; awareness alongside

understanding (quantitative) on one hand and perceptions (qualitative) on the other; the

theory chosen would be required to facilitate both these aspects. As each theory in and

by itself would fail to do so, we decided to employ a multi strategy theory. Several

approaches of this theory exists, however we chose the complimentary approach

classified by Hammersley (1989); in which the two separate theories are employed in

order that different aspects of an investigation can be dovetailed.

3.2 Research Design

In order to capture aspects of both quantitative and qualitative elements; an interview

encompassing both structured and semi structured facets will be employed. Bryman &

Bell (2003) suggests the interview being a prominent data collection technique for both

quantitative and qualitative research. Robson (2002) suggested that an interview allows

the researcher to elicit all types of information from the respondent, ranging from

beliefs, attitudes, values and perceptions.

22

The quantitative aspects of the interview will be structured, coupled with close ended

questions. This will allow for increased standardization, reducing any error of variability

that may occur due to interviewer inconsistency or misinterpretation and enhancing the

facilitation for comparability and analysis of data (Bryman & Bell 2003). “Close ended

questions are extremely useful for eliciting factual information...” (Kumar 2005; 134), and

enhances the validity and reliability of the study.

On the other hand, the qualitative aspects demand a semi structure nature alongside

open ended questions. Referring back to Kumar’s statement, “...whereas open questions

are useful for seeking opinions, attitudes and perceptions” (2005; 134). As responses or

hints are not offered, it encourages respondents to volunteer more of their personal

information, allowing the researcher to gauge pure attitudes and opinions (Bryman & Bell

2003). The semi structured nature will allow for deviation and probing from and into

predetermined questions, where opportunities to gain a deeper understanding arises

(Saunders et al 2007). The structure cannot however be classified as solely semi

structured, it undoubtedly incorporates elements of a focused interview as termed by

Merton et al (1956; Bryman & Bell 2003), due to the relatively narrow focus of the

questions.

The combination of structures and question types provides the unique combination

which will yield responses satisfactory to the posed question. By employing a mixed

method, it allows for the avoidance of criticisms associated with each theory in its

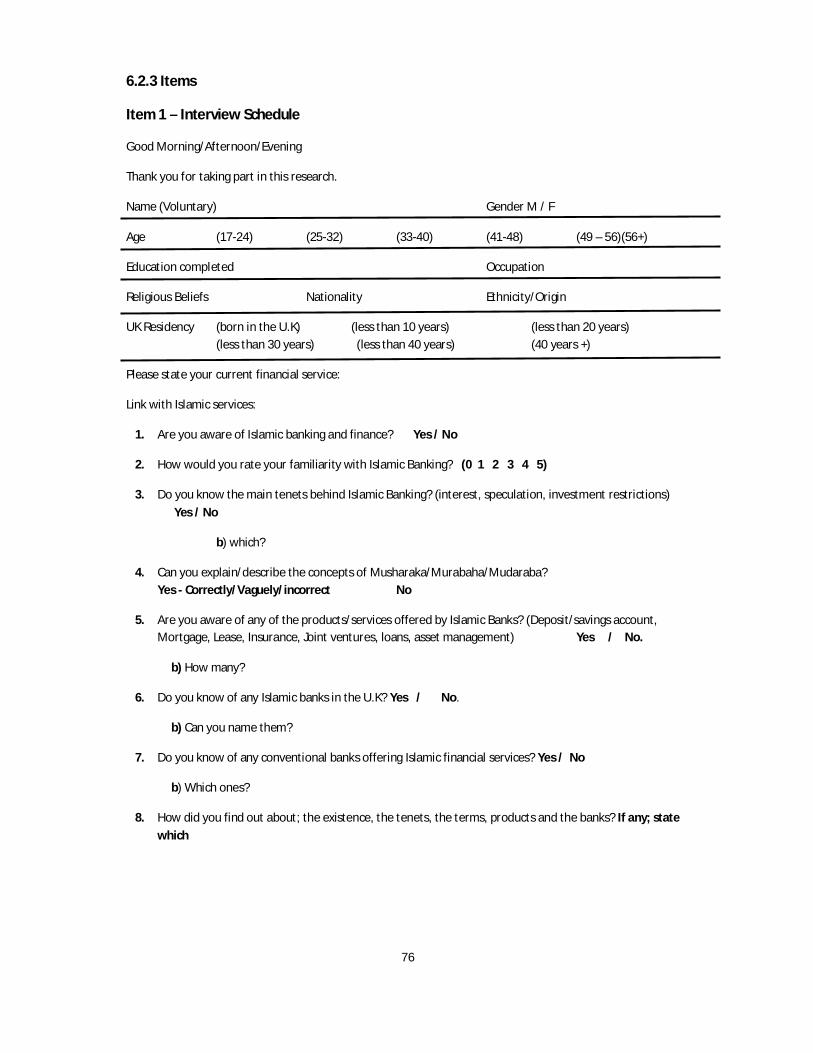

singularity, while facilitating for the capitalization of strengths in their plurality. Item 1

(insert item 1) a blank copy of the interview schedule, as you can see, each quantitative

element is complemented by qualitative features.

The informal conversational style of the interview is suggested to lead to respondents

feeling more comfortable in sharing opinions and feelings; more so than in a

questionnaire (Saunders et al 2007). The physical proximity also allows for questions and

concepts to be explained, discussed or clarified if necessary.

23

Moreover, face to face contact allows for non verbal reactions to be gauged and if

deemed fruitful probed and investigated (Bryman & Bell 2003). However, personal

contact could also act as a catalyst for respondent bias, “where the respondent makes an

attempt to construct an account that hides some data, or generates false data in order to

portray him/herself in a socially desirable role” (Saunders et al 2007; 600). Another bias

that may influence responses is the interviewer bias; where researcher’s comments, tone

or non verbal behaviour may manipulate responses.

3.3 Analysis

The first step in the analytical process is deciding how to record the information. One

option would by the use of a tape recorder, the use of which allows the researcher to

fully concentrate on the responses and behaviour of the subject; it would subsequently

facilitate easier analysis (Saunders et al 2007). However while conducting the pilot

interview, we found the test respondent focusing quite excessively on the device,

showing signs of anxiety and hesitance when answering questions, especially question 9

onwards. Kumar (2005) suggests that the use of a recording device may inhibit or alter

responses to a certain degree, due to an increased likelihood of respondent bias. We

therefore resorted to note taking as we felt that brief yet ‘true’ responses held greater

value in comparison to extensive yet potentially ‘contaminated’ ones. Microsoft Excel

will be employed to statistically analyse and graphically present quantitative findings.

From the blank interview, you will notice several personal factual questions at the outset;

these will take shape as variables in trying to establish causation and trend identification.

More sophisticated methods of analysis such as models of bivariate analysis were

deemed unnecessary in relation to the question at hand and were therefore discarded

(Bryman & Bell 2003). With the qualitative data being in the form of words, sentences

and at times even paragraphs; the analysis proves more difficult. Common forms of

analysis include ethnographic coding and grounded theory; both requiring a process of

coding (ibid).

24

The issue with coding is the possible loss of context as responses are categorized and

removed from their sequential order; as well as likelihoods of errors in measurement

arising as a result of the variability of the coding process (ibid). Based on these factors,

examination of qualitative data will take the form of descriptive analysis. Bryman & Bell

(2003; 295) state “...qualitative researchers are more inclined to provide a great deal of

descriptive data when reporting the fruits of their research”. Descriptive analysis

emphasizes the importance of contextual understanding, the very foundation of an

interpretivist epistemology; grasping perceptions of a social group in relation and context

to the specific environment in which they operate.

3.4 Sample

Dar & Presley (2004) reported London as being the home of 45.2% of the U.K’s Muslim

population, the choice of London and Harrow was therefore primarily influenced by its

demographic nature alongside its residential proximity; Harrow being one of the few

local authorities with an ethnic majority population, and the most diverse religious make

up (Harrow council 2008). Table 5 and 6 (insert table 5 & 6), statistically represents the

various ethnic and religious groups within the borough. This provides an additional

aspect to the findings due to the enhanced exposure of respondents to different cultures

and religions.

Selecting an appropriate sample is crucial. We established Muslim and ethical consumers

as the natural market for IBF, but in light of recent financial developments and

subsequent confidence issues; the general consumer market also holds potential. Hence

the sample needs to be representative of these factors. A system of stratified random

sampling was therefore chosen, where random selection takes place within defined

respondent categories (Bryman & Bell 2003). The pursuit of an ‘ethical’ consumer group

would prove unfeasible, so two categories were established; Muslim (MU) and Non

Muslim (NM).

25

Through the division of respondents, enhanced levels of causation and trends can be

identified for each category; a system of random or systematic sampling may not have

captured a sufficient fraction of each market and data would therefore be rendered

shallow.

The sample will consist of 30 respondents, 15 for respective categories; reflecting a

compromise between the constraints of time and need for precision (ibid). The

compromise in size facilitates for enhanced insight of qualitative elements, while still

providing significant breadth for validation of quantitative aspects. In light of this sacrifice

Saunders et al (2007) suggest that data collection and analysis, with regards to the

understanding and validity that can be gleaned from the data; is more important than the

size of the sample.

3.5 Channel

The success of stratified sampling is reliant upon the relative ease of category

identification (Bryman & Bell 2003). Avenues were therefore pursued which allowed for

alleviated respondent classification; the vicinity surrounding the local mosque (Muslim

place of worship) was therefore approached for gathering data for the MU category,

whereas the town centre was used to fulfil the NM quota.

Actual research subsequently took place upon completion of interview schedule and

determination of time and locality. The research took place over a two week period; the

MU category was sought on two consecutive Fridays due to the weekly prayers being

held in the mosque providing the opportunity to gather data. Whereas the NM sample

was gathered throughout the two week period, with no attention paid to day or time. We

felt the interview process was quite successful, with relatively positive levels of

willingness to participate and insightful responses given. The next chapter seeks to

analyse and discuss the collected data.

26

Chapter 4 – Data Analysis and Discussion

In this chapter we endeavour to analyse and discuss the findings. An analytical discussion

will unfold drawing contrasts between the lack of awareness and consumer perceptions.

While some respondents gave consent to use their names, others did not. Respondents

will be therefore by referred to as either MUx signifying Muslim respondent x, or NMx

representing Non Muslim respondent x, with ‘x’ representing the number of the

participant. Respondents range from MU1 – MU15, and NM1 to NM15. Prior to the

analytical sections, a brief description of the sample will be given.

4.1 Respondent description

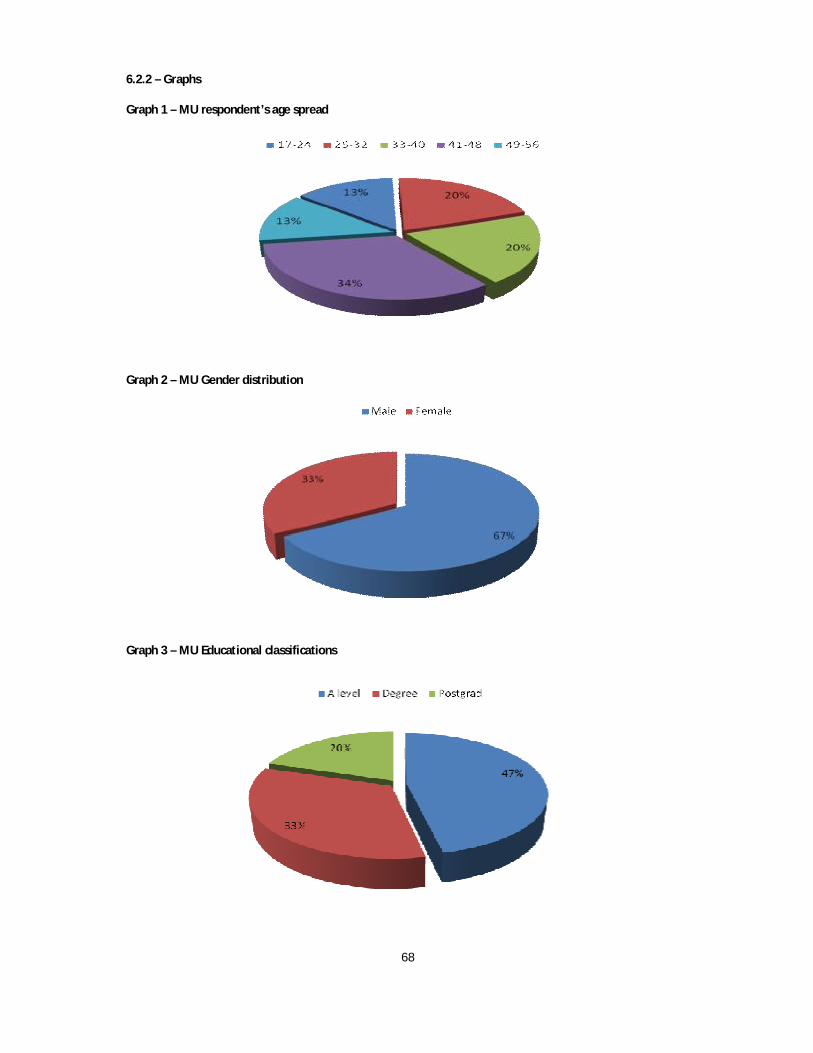

In graphs 1 – 5 (insert graphs 1 - 5), a demographic breakdown of MU respondents is

graphically presented. With the MU category, we see the sample had a male majority of

67%. Age wise respondents were fairly evenly spread out between 25-48 years. Majority

of respondents had completed A-levels, but degree level was also significant. The sample

consisted of 53% British nationals, and 47% of immigrants. The 47% included Indian,

Pakistani and Bangladeshi nationals. However, descents of all British nationals were

found in these three countries. The majority of foreign nationals had lived in the U.K for

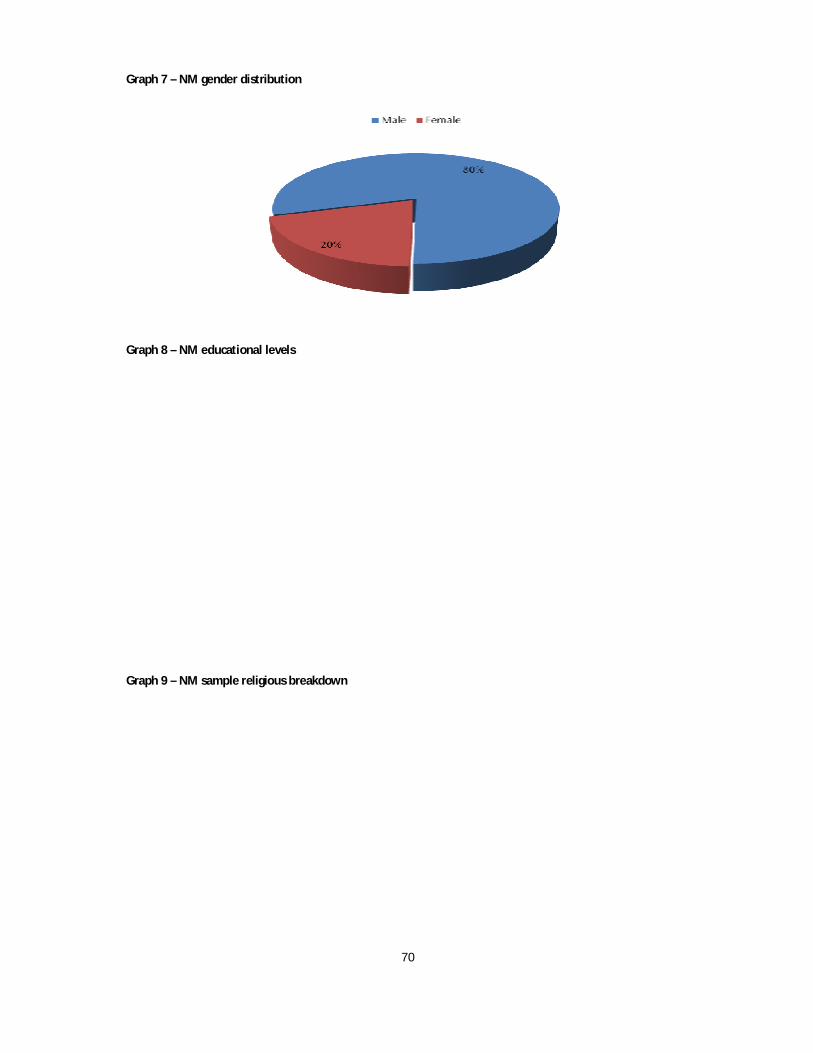

less than 20 years. The NM sample was relatively similar (insert graphs 6 - 9); a fairly

equal distribution of ages 25-48 was found. Majority of respondents were university

graduates, however A-level completion was also significant. The gender distribution was

one sided, with 80% male respondents. Concerning religious beliefs, majority of 47%

were atheists with Christianity following at 33%.

4.2 Awareness

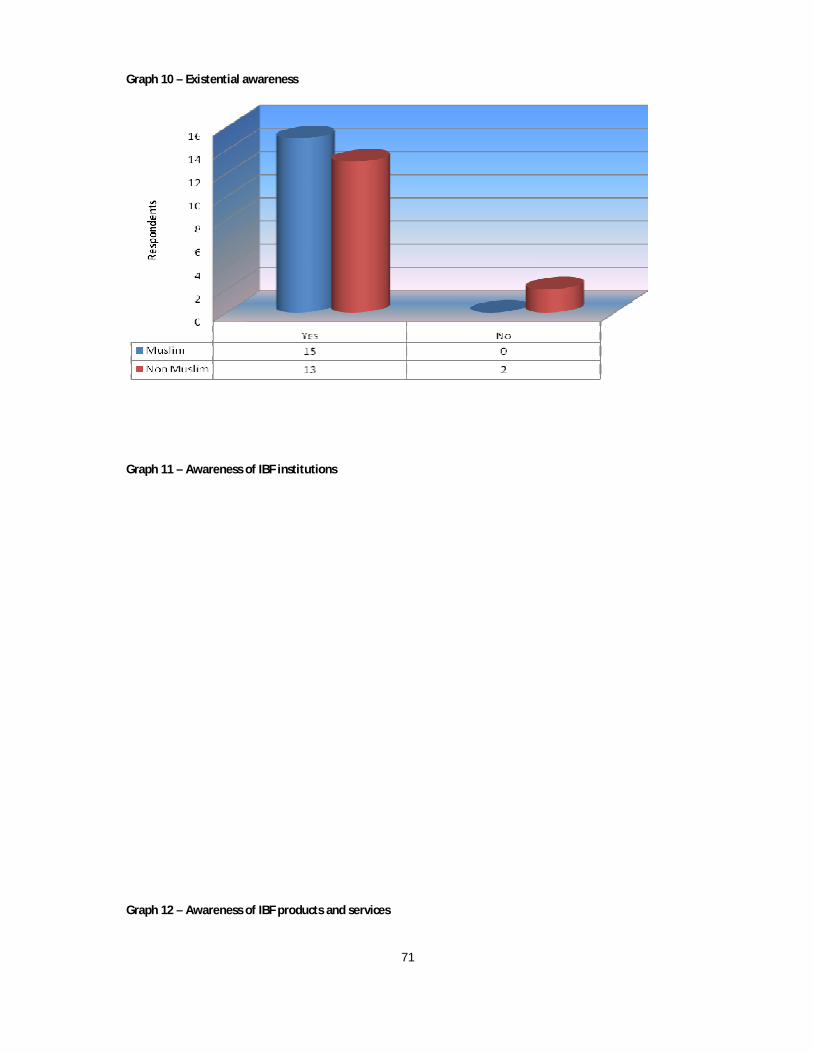

Graph 10 (inserts graph 10) depicts basic existential awareness of IBF, 100% of MU and

86% NM respondents were aware of IBF; though the extent of their awareness differed

substantially.

27

Graph 11 (insert graph 11) shows respondents awareness of banks offering IBF. 80% of

total respondents were able to identify IBB as one of the providers, beyond that however

levels were significantly low. From MU respondents, 60% and 33% identified HSBC and

Lloyds respectively, with only 20% exhibiting awareness beyond these three. Moreover,

the insignificant 20% that did identify beyond IBB, HSBC and Lloyds could be explained

through contextual analysis. MU3 expressed a particular interest in IBF, and said he had

been following its development; whereas MU5, had exposure to the finance sector as a

whole due to his occupation as an investment banker. Only one NM respondent

managed to indentify beyond IBB; NM8. He displayed awareness of 9 out of the 11

institutions mentioned; his awareness however, similarly to MU3 and MU5, can be

attributed to context, upon investigation we notice his occupation as a bank manager,

therefore suggesting particular exposure to developments in the industry.

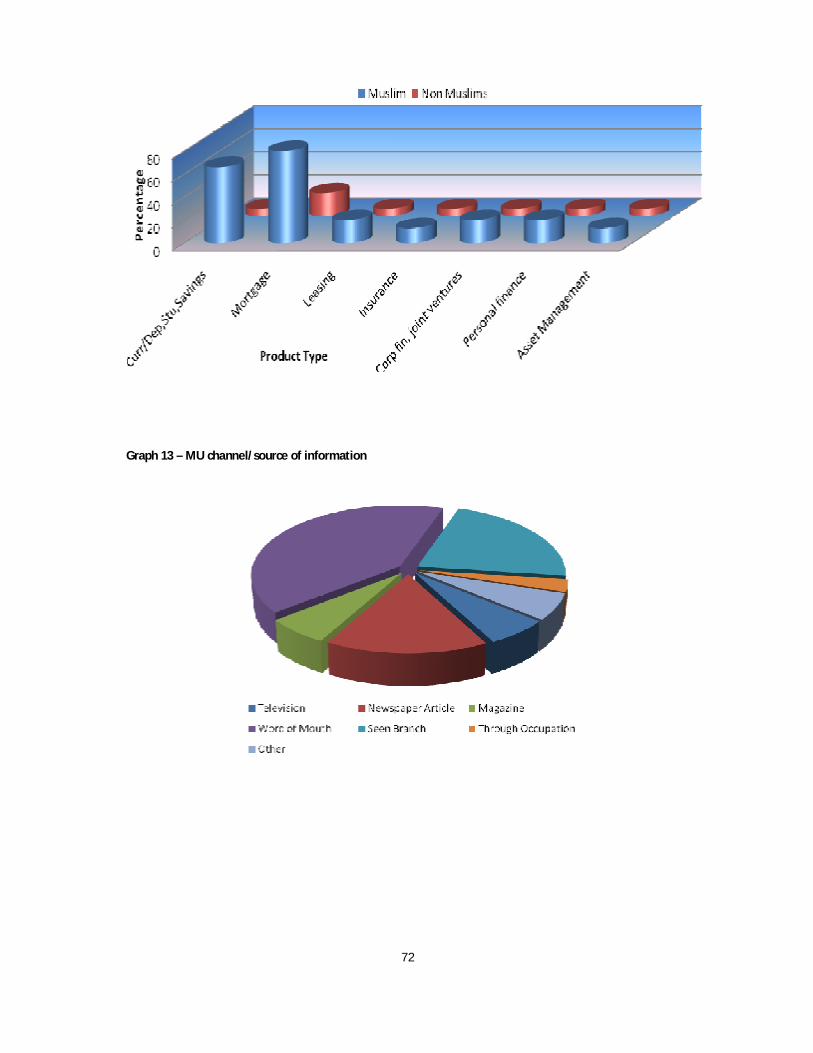

Respondents awareness of products and services offered within IBF are displayed in

graph 12. MU respondents exhibited high levels of awareness of current, savings and

deposit accounts along with mortgages; with 66% identifying the former and 80% the

latter. However yet again, 20% of respondents were responsible for the remaining

product awareness levels. Investment banker MU5 exhibited awareness of 6 out of the 7

products that were mentioned. MU6 managed to identify all products, upon contextual

investigation; we find he actually held an Islamic corporate loan, and furthermore was a

Pakistani national; Pakistan as we mentioned earlier has an entirely Islamic financial

system. These factors can therefore be said to contribute to his awareness.

In regards to NM respondents, we notice similarly to bank identification, levels were

extremely low. In this instance only two respondents could identify any products. Bank

manager NM8 again displayed high levels of awareness by identifying all of the products

mentioned. NM9 exhibited awareness of the Islamic mortgage; however we find the

respondent being an estate agent who had come into contact with the product; providing

additional evidence of awareness being a result of particular circumstances.

28

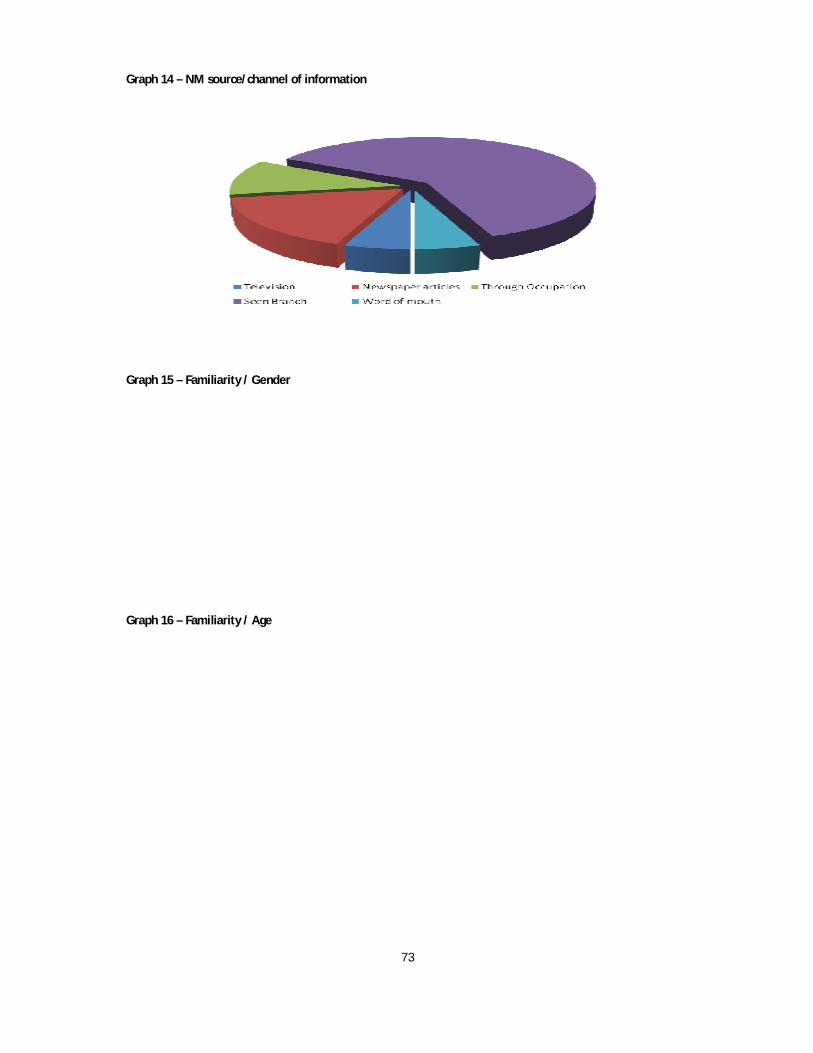

Graphs 13 and 14 (insert graphs 13, 14) depicts respondents source and channel of

information. As suggested by graph 13, 85% of MU respondents stated word of mouth as

one of the sources through which they gained awareness. 46% proposed that the mere

sight of an Islamic bank’s branch contributed to their awareness; upon further inquiry

this was found exclusively to be IBB. Newspaper articles were a source of awareness for

33% of respondents; additional probing revealed these to be limited to broadsheets

including The Financial Times and Daily Telegraph. Television adverts represented 13%.

Further questioning found the adverts were aired solely on foreign channels available

only via satellite TV, adverts were further found to be for IBB only. Two respondents

stated Magazines as a source, but yet again these were not mainstream, rather specialist

magazines dedicated solely to finance developments. Awareness through occupation was

only found to be true to one participant. The ‘other’ category included sources such as

awareness through nationality.

For NM respondents (insert graph 14) the majority’s source of information was the mere

sight of an IBB branch, representing 73% of respondents, which was reflected in the

extent of awareness exhibited. Newspapers (broadsheets) were proposed by 20% of

respondents. Awareness through occupation represented 13%, these were the bank

manager and estate agent mentioned earlier. Word of mouth and Television was stated

by one respondent respectively. Upon further questioning, it was found that the TV

advert was similarly to MU respondents, on a foreign satellite channel and related to IBB.

The results collectively gesture towards considerably high levels of awareness, yet the

extent of which is considerably low. Only respondents with circumstances leading to

increased exposure were found to have significant levels of awareness. Further elaborate

discussions will unfold in subsequent sections.

29

4.3 Understanding

The understanding element will be quantitatively analysed using a familiarity rating.

Several variables will be examined in correspondence to familiarity in order to identify

any trends.

Graph 15 (insert graph 15) shows the relationship between gender and familiarity for the

MU category. A significant difference was discovered between genders; males with an

average familiarity rating of 2.4 whereas females a mere 1. Even bearing in mind the

unequal distribution in gender (graph 2), a closer look revealed every female respondent

having a rating of 1.

As the NM category displayed a general lack of familiarity across the board; similar

analyses would prove futile. The significance of age in relation to familiarity is showed in

graph 16 (insert graph 16). The 33-40 MU group exhibited the highest level of familiarity.

However as investment banker MU5 and engineer MU7, who also owned an Islamic

mortgage, both displaying significantly high levels of familiarity fell within this group; it

inevitably influenced the group’s average. The NM respondents in the 41-48 bracket

showed higher levels of familiarity than the MU respondents. However, bearing in mind

contextual features; bank manager NM8 and estate agent NM9 both exhibiting

considerable familiarity, belonging to this age bracket naturally offset the average.

Disregarding contextual factors however, a clear trend of familiarity among ages 33-56

was found.

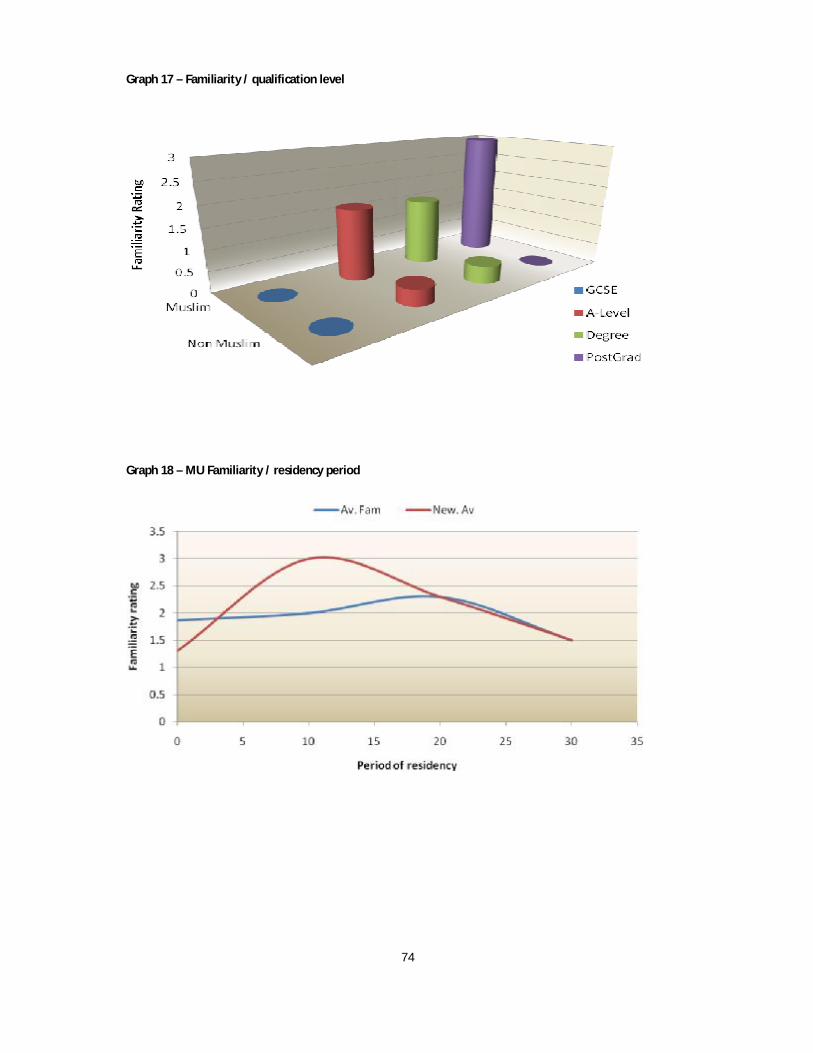

A relationship was also found between qualification levels and familiarity. Graph 17

(insert graph 17) gestures towards the notion that higher levels of education signified a

greater level of familiarity, especially within the MU sample. The exception is the

apparent higher familiarity within the A-level group in comparison to the degree group.

30

Upon contextual analysis, we find that the A-level average was influenced by MU6 who

had a familiarity rating of 4. By discarding his rating, we find the average would have

been a mere 1, thereby supporting the trend of heightened familiarity corresponding to

qualification.

The period of residency in relation to familiarity also revealed a relationship, yet slightly

less significant. In graph 18 (insert graph 18, blue line) you can see the level of familiarity

continuing to increase corresponding to period of residency. Familiarity at point 0

represents the average level of familiarity of British nationals, the relationship may have

proved stronger had this value not been offset. Both investment banker MU5 and

engineer MU7, were British nationals, by discarding their ratings, the average would have

been 1.3; thus highlighting the trend between familiarity and period of residency. The

New Average series (insert graph 18) plots the new average.

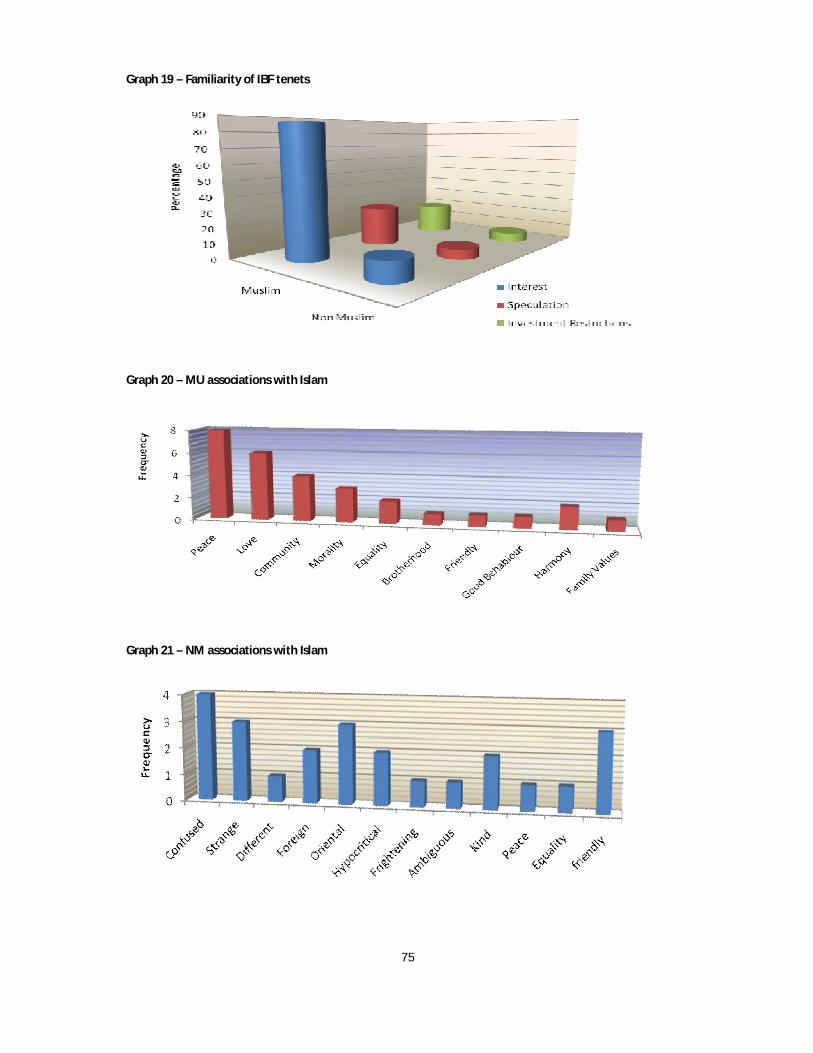

Further insight was sought of respondent’s familiarity concerning the underlying tenets

of IBF. As discussed in section 2.4, these comprise of prohibitions in the charging of

interest, speculation and restrictions on investment. Graph 19 (insert graph 19) depicts

86% of MU respondents correctly identifying the prohibition of interest, whereas a

meagre 26% and 20% identified speculation and investment restrictions respectively. This

also stemmed from contextual factors, as MU3, MU5 and MU6; all of whom had high

levels of familiarity and understanding due to personal circumstances, were the only

respondents successfully identifying the other two principles. This further emphasises the

low levels of familiarity found among the MU category. The levels shown for NM

respondents were based solely on responses by bank manager NM8 and estate agent

NM9, accentuating the role of occupation or special context in awareness and familiarity

for Non Muslims.

31

An evaluation of respondent’s knowledge concerning specific terms and product

structures surrounding IBF was also desired.

This refers to question 4 of the interview, where respondents ability to explain the terms

Musharaka, Murabaha and Mudaraba was examined; these being the main product

structures used in IBF.

In keeping to expectations, majority of the sample were oblivious to the terms and

product structures, in exception of the respondents to who frequent reference has been

made. MU5 and MU6 correctly defined the terms, MU3 vaguely managed to do so. MU7

correctly identified the term and structure of mortgages, Murabaha; due to the

respondent owning an Islamic mortgage. From the NM sample we find NM8 was not

aware of the actual terms, but correctly described the product structures and NM9

similarly to MU7; correctly described the mortgage principles.

In summary of the above outlined findings then, we find the level of awareness being

quite high. However, the extent of this awareness was fairly shallow; especially among

NM respondents; whereas the MU sample exhibited a slightly superior awareness being

able to identify a few institutions and a small selection of products. In relation to

understanding, general findings revealed a significant lack of familiarity across the

variables. Higher familiarity was found in males, between ages 33-56, with higher

educational qualifications and especially among foreign nationals.

Even though MU respondents displayed slightly enhanced awareness and understanding

in comparison to NM, which was expected, the extent and level of the awareness and

understanding was significantly low among the majority.

The data supports findings by Cunningham & Gerrard (1997) who found similar levels of

awareness. In their study, a mere 20.7% of respondents were aware of the term Riba

(interest) and a further insignificant 31% knew what Shariah meant. What this shows is

not only a lack of awareness in regards to IBF, but towards the religion in general.

32

The findings also correspond with Naser et al (1997), who found a complete unawareness

of the terms and product structuring associated with IBF.

The analysis revealed that only respondents with special circumstances, such as an

occupation providing exposure, an explicit interest or actually owning an Islamic financial

product were likely to have particularly high levels of awareness and understanding. The

contextual analysis allowed for this enhanced insight to be grasped; highlighting its

importance within business research. The relationships discovered between familiarity,

education and residency were also supported by Dar & Presley (1999) and Metawa &

Almossawi (1998), who found a majority of potential and current IBF customers, were

well educated and of Middle Eastern or Indo/Pak nationality.

In regards to the sources of information, a crucial point to note is the nonexistence of IBF

within mainstream media. Internet, TV, magazines and billboards promoting the services

and products were completely absent. The TV and magazine sources that were

mentioned, were not mainstream, rather satellite TV and specialist magazines. The

insignificant levels of awareness and understanding can therefore be attributed to the

lack of promotion and advertising. Institutions appear to have neglected the marketing

and promotional aspects of their operations. The possible reasons pertaining to this will

be discussed in subsequent sections.

4.4 Perceptions

This section seeks to offer an insight into the opinions, feelings and general views held by

respondents towards not only IBF, but Islam as an entity; which was mentioned briefly in

section 2.8.2 as being a possible hindrance to the sectors growth. Responses from

question 9 onwards of the interview provide the basis of analysis.

4.4.1 Perceptions of IBF

Due to the general lack of understanding found across the sample, the main tenets of IBF

were explained, especially in relevance to the financial crisis; prior to asking questions.

33

Concerning the support for a completely Islamic financial system, 93% of MU expressed

direct support for the proposal, whereas 93% of NM articulated the antonym.

The negative consequences of the crisis and the ethical considerations IBF encompasses

were found to be the foremost factors underlying the unequivocal support by MU

respondents. We find MU R5 stating:

“Yes if it can help the economy. The current financial system seems to be based on greed.

We’ve all heard about the excessive bonuses and frauds”

MU R14 stated “Yes, would be good. As I said earlier, I’m self employed, I run a small

business and the credit crunch has made things very difficult”

On the other hand, several MU respondents including MU R3, MU R5 and MU R7

motioned towards the idea that an Islamic financial system would never be

implemented; regardless of its array of benefits. MU R5 suggested that as the

government would forego tax payments from industries restricted under the Islamic

system, it would not be implemented. He states “Didn’t you know the pornography

industry has received bailouts?” It’s interesting to note that respondents with such

opinions all had either significant qualifications or higher levels of awareness and

understanding of IBF. The factors behind the collective rejection by NM respondents

were primarily based on concerns for choice and freedom within the market. NM R1

stated:

“No, I mean it’s good that Muslims here can bank the way they need to, but I don’t see a

need for the whole system to be like that. There needs to be a choice for everyone; and

I’m sure there is a way out of the financial mess other than Islamic banking”

NM R14 stated “No, there should be a choice for everyone; you cannot force everyone to

have Islamic accounts, when not everyone is Muslim”

34

From the NM sample, only NM R12 expressed support for an Islamic system. He stated:

“Yes, if it can provide a system that accommodates everyone and not just Muslims”.

Alongside the MU respondents undeniable support for an Islamic financial system, 93%

also expressed an interest for the products and services; highlighting the potential

market within Muslim consumers. Yet the question arises as to why they had yet to adapt

the services, bearing in mind 100% of MU respondents had an awareness of IBF.

However, as discussed earlier, the awareness exhibited was considerably basic, while

only a select few had an understanding of the sector; this was found to be the main

reason why the majority of MU respondents had yet to switch their services.

MU R14 stated “Yes I would be interested, perhaps if someone explained how it works

and if it’s competitive”. Future considerations based on further investigations were also

expressed, such as MU R15 who stated “Yes, I’m actually looking for a mortgage at the

moment; I will now definitely look into it and see what’s available”. When asked about

the main reasons or motivators pertaining to the willingness and interest in switching

services; the societal benefits of the system and its embedded ethical principles were

again found to be the main attractors rather than Shariah legislation.

With the lack of understanding being identified as the main antagonist of consumption, it

however fails to account for respondents with significant understanding who have yet to

‘convert’ their finances to Islam. Investment banker MU5 is an example of this, he states:

“I’m quite weary of the service, even though it’s got the Shariah stamp; the fact that they

charge payments at levels similar to interest, suggests it’s exactly the same, just with a

different name. Even the assistance in granting credit they supposedly offer those less

qualified for loans, the fact that the bank becomes a partner and is therefore exposed to

risk, means they will be even more stringent than conventional banks. Therefore even

though it may be called Shariah, in my opinion I think it’s just the same”.

35

As you can see he felt IBF bore similarities to conventional banking, and did not therefore

see a need to switch. This issue will be addressed briefly in the conclusion.

MU6 similarly exhibited significant levels of understanding; however, he actually owned

an Islamic financial product; a corporate loan from IBB.

Upon enquiry of the underlying motivations pertaining to this, he suggests the

willingness to comply with religious beliefs led to his decision. Upon analysis however, we

notice besides the Islamic loan; he also held a conventional mortgage with Lloyds and

current/savings accounts with NatWest. The enquiry emerged as to why he had not

acquired Islamic versions of these, in keeping with his beliefs.

He stated: “I got the loan from IBB at a fairly competitive price and with the partnership

structure enabling me to get expert advice I thought it was a really good deal. However, I

found with the current account, they weren’t as competitive, and I would only use the

fully Islamic banks as I don’t quite trust the conventional banks offering the services”.

Suggesting that perhaps rather than compliance with belief; the actual motivation was

based on the competitiveness and benefits of the product. In similar fashion we find

MU3, who also showed considerable understanding stating:

“I don’t feel the service and competitiveness of the Islamic products will be as good, but if

I were to purchase any product, I would probably use IBB or another fully Islamic bank, as

I suspect the conventional banks might not operate strictly to Shariah law, I feel like

they’re just trying to make money in this growing market”.

Additionally, postgraduate engineer, Islamic mortgage owner MU7; stated when asked

about his services: “IBB just seemed like the natural choice for the mortgage. I tried

comparing between the Islamic and conventional banks offering the Islamic mortgage,

but it was quite hard to locate any information from the conventional banks, whereas on

IBB’s website it clearly explained the terms and product structuring, it therefore seemed

like the safest bet”.

36

As you can see then, while the majority of MU respondents with limited understanding

quite happily entertained the idea of consuming Islamic financial products, the minority

exhibiting understanding actually expressed degrees of hesitance, especially regarding

conventional banks and the emphasis of competitiveness. With NM respondents, a

manifest 86% expressed a lack of interest. The samples collective attitude can be

captured by NM14’s response; “No, not at this time”. Even NM8 and NM9, despite their

understanding and IBF’s ethical connotations, did not express any form of interest.

Two respondents however, did convey an interest. One was NM12, who had also

expressed support for an Islamic system; the other was NM4 who stated “Yes, from what

you’ve told me, it sounds quite good”.

These respondents however share important characteristics which we believe were the

main factors underlying their interest for Islamic financial products; these were positive

opinions and attitudes towards Islam.

4.4.2 Perceptions of the brand Islam

We seek to evaluate respondent’s views and feelings towards Islam as an entity;

attempting to test some of the theoretical views put forward in section 2.8.2; as well as

proposing the theory we labelled the triangular causation hypothesis.

An examination of why respondents felt there was a lack of promotion revealed quite

interesting opinions. MU respondents in unison felt banks, Islamic and conventional

respectively had failed to promote their Islamic services; and attributed this to their lack

of understanding. MU11 stated:

“Usually every other advert on TV is about mortgages or some kind of financial service,

which is why we know about them and buy them. Whereas with Islamic finance, we

haven’t seen anything and consequently as you saw earlier I hardly know anything about

it”

37

Similarly MU12 stated “I don’t know why they haven’t advertised. I mean as a Muslim I

feel like I should know more about it, but then really I feel like I haven’t been told”.

Majority of NM respondents, similarly agreed banks had not sufficiently promoted their

Islamic services, and were quite confounded by the phenomenon. For example, NM2

stated: “Don’t know really, quite surprising as the normal banks have so many adverts for

all their other products”. We also found estate agent NM9 stating “I don’t know to be

honest, they really should though. We get quite a few people asking about it, but they

haven’t got a clue about what it is or how it works”. According to market research,

demand for Islamic mortgages is estimated at £4.5bn (BBC 2002).

These responses from the MU and NM sample reflect the opinions of the majority; a few

respondents did however offer a contrasting view, MU5 stated:

“I think if perhaps Lloyds or Barclays carried out extensive advertising for their Islamic

services, it would impact and perhaps reduce demand for their conventional products,

due to the associations people have with Islam”. Similarly MU7 stated: “Well in my

opinion it’s to do with the general public feelings about Islam”

In addition, marketing executive NM11 said “I’ve worked with marketing for a long time

now, and no offense to you, but in all honesty, if I were Lloyds, I wouldn’t advertise either,

I don’t think it will be good for business”

These minority responses clearly make a connection between Islam and advertising. It is

interesting to note that above quoted respondents, had qualifications at degree level or

above, whereas the majority of respondents failing to identify this connection had lower

level qualifications. While this partially supports our proposed triangular hypothesis; with

only a few respondents actually identifying the link, we sought to further examine how

respondents felt Islam was portrayed in the media. We expected to find severely

contrasting views, however surprisingly respondents from both categories exhibited

similar opinions. MU1 stated:

38

“Not very well, it’s quite bias and unfair and there is no real voice defending the claims

being made by the media”. Similarly MU 4 said “I think everyone would agree the

representation is quite negative”.

From the NM respondents we find NM11 stating: “I work in the media, and I can say that

yes unfortunately more often than not they emphasize the negative aspects” As well as

NM14 who said “Well it’s always associated with terrorism and all that, even though that

may not be the truth”

We notice all respondents agreeing on Islam being portrayed in a negative light and most

suggesting it being a false attribution. The next question sought to examine how

respondents personally viewed Islam, through ascribing adjectives they felt were

associated with the ‘brand’ Islam.

Graphs 20 and 21 (insert graphs 20-21) plot the range and frequency of the

characteristics mentioned. A choice of responses was not offered as it would have

influenced the validity of findings. MU respondents as expected associated Islam with

purely positive qualities such as ‘love, peace, morality and equality’ whereas we found a

range of characteristics from NM respondents. As you can see, the majority were neutral

but with slight negative connotations such as ‘confused, strange and different’, while

others were purely negative; ‘hypocritical and frightening’. If we look at the extended

responses of the purely negative ascriptions, we find NM5 stating:

“No offense to you, but from what I’ve seen and heard, I would say it’s quite hypocritical

and confused. I mean you’ve got the peaceful and the radical extremist”. Likewise NM2

said: “I mean from 9/11 to 7/7 and all the stuff you hear about beheadings and stoning,

I’d say frightening to be honest, no offense”.

A few of the positive associations from NM respondents were also explored further. NM6

stated: “Well the basic teachings are actually quite similar to Christianity even though

most people don’t know that, so I would say love and peace”

39

Similarly NM4 said: “I’m actually good friends with many Muslims, so I’d say friendly and

kind”. Along the same lines NM12 suggested: “You know I’ve actually been to some

Muslim countries on holiday, like Morocco and Egypt, so I think I’ll say friendly and

oriental”.

We wish to highlight here that respondents NM4 and NM12, who formed part of the

minority ascribing positive qualities to Islam, were the only NM respondents expressing

an interest in Islamic financial products. While those who associated Islam with negative

attributes articulated opposition to an Islamic system including the products.

In an attempt to further establish this relationship, we enquired whether respondents

would be interested in ethical financial products; which in effect are identical to Islamic

financial products (discussed in section 2.7.2). In the event of respondents exhibiting an

interest for ethical finance, the conclusion could be drawn that the ‘brand Islam’ is the

antagonist of IBF consumption.

A staggering 100% of MU respondents expressed an interest for ethical financial

products, however many patronized IBF over ethical finance. For example MU11 stated:

“Yes sounds good, but if it’s the same as Islamic, I’d opt for that” Similarly MU15 said:

“Yes, but between this and the Islamic products; obviously being Muslim I would support

the Islamic products”. Interestingly, investment banker MU5 who was mentioned holding

quite alarming reservations regarding Islamic financial products displayed an interest in

ethical financial products suggesting they were more ‘Shariah compliant’. In relation to

NM respondents, a dominant majority of 86% exhibited an interest for ethical financial

services, however much emphasis was placed on the need for competitiveness. NM10

stated: “Yeah sounds good, as long as they’re not more expensive”. Likewise NM6 said: “I

didn’t even know there was such a thing, well if it’s proven competitive I don’t see why

not”.

These responses leave open the possibility of drawing the conclusion mentioned earlier;

that the negative perceptions and attitudes of Islam were the repellents of mainstream

40

IBF consumption. However the arrival at such a conclusion, by simply drawing parallels

between responses leaves the findings and triangular causation hypothesis vulnerable to

criticisms based on interpretation effects. In avoidance of this, we sought to further

strengthen the relationship by investigating whether respondents believed IBF would

generate increased interest were it to change name. 100% of MU respondents agreed

with the proposition, where we found MU10 stating:

“Well yes, I mean if you change the name, people wouldn’t know its Islamic banking, they

would think its ethical banking, and I think more people would be interested in that”.

Likewise MU3 said: “Yes definitely, well because of the media issues we discussed earlier,

I believe the mainstream are more likely to associate with ethics and moral principles

rather than Islam”.

Opinions of NM respondents were however slightly more diverse. While 53% felt

changing the name would generate interest, 47% felt it would not. Three main categories

of responses emerged. The first of which, felt changing the name of IBF would lead to

enhanced appeal due to media and public opinions, the second group suggesting the

name was of no relevance and the third group, felt changing the name ‘to hide’ it’s

Islamic principles would be deceptive and ethically questionable. An example of each is

given below.

NM6: “Obviously with the opinions people have of Muslims and Islam, you know with the

terrorism and all that, they might not trust it, especially with all the Arabic terms you

mentioned”. NM13: “I don’t see why it would. People that want the service wouldn’t care

about what it’s called”. NM2: “I mean if it’s the same thing, but just changing the sign on

the wall, that’s kind of deceptive aint’ it? If it’s Islamic banking, then people should know

that”

A minor majority of 53% then, believed a change of name would generate more interest,

whereas the 47% that did not; were still part of the group who were interested in ethical

finance.

41

What this suggests is that regardless of whether all NM respondents made a connection