62

IT security and compliance update August 10, 2017

IT security and compliance update

August 10, 2017

Moderator: Liz Ziesmer, CPA, CBA

Director of Financial Institution Services• Specializes in audit and consulting

services for financial institution clients– Leads numerous financial statement and

internal audits, SOX 404 and other financial services consulting engagements for the firm’s largest and most complex financial institutions, including SEC registrants

• Works closely with management and audit committees to address technical issues and ensure sound internal controls

• Services as a firm-wide resource for financial institution accounting and auditing matters

Regulatory Compliance UpdatePresented by:

Beth A. Behrend, CCBCO, CBAP

Speaker: Beth A. Behrend, CCBCO, CBAP

Senior Manager• Rehmann• Leader of our firm’s compliance services

for financial institutions.• Worked for and with financial institutions

for more than 30 years. • Expertise includes providing a wide range

of audit and consulting services for our financial institution clients.

• Extensive knowledge of financial institution operations and serves in an advisory role to clients within the BSAand Regulatory Compliance related areas

Regulatory Compliance UpdateFair Lending Issues

Bank Secrecy Act – Beneficial OwnersTips, Tricks and Tidbits

Fair LendingCurrent Regulatory Considerations

Fair Lending Concerns

• FDIC and OCC have highlighted Fair Lending as an Emerging Risk– OCC 2017 Operating Plan– FDIC 2015 Winter Insights

• Specifically mentions underwriting practices• High growth areas and auto lending

• CFPB Activity – trickle down impact

Fair Lending – CFPB

• In 2016, fair lending supervisory and public enforcement actions by the CFPB resulted in approximately $46 million in remediation to harmed consumers

• Focus has been on redlining risk, assessment of lenders intentional discouragement of application for credit in minority neighborhoods

• Additional focus has been on compliance with ECOA in indirect auto lending

Areas of Focus for 2017

• Redlining• Mortgage and Student Loan Servicing• Small Business Lending

Redlining Considerations

• Reasonably Expected Market Area (REMA)– Where the institution actually marketed and provided

credit and where it could reasonably be expected to have marketed and provided credit

– REMA is used in evaluating redlining risk– Considerations:

• Not extending credit in certain areas• Targeting certain areas with less advantageous products• Offering different loans to different areas• Not marketing residential loans to certain areas

Redlining - Continued

• How is REMA determined:– Discussion with the Bank– Assessing Branch network– Marketing efforts: Print, Calling Program, Direct

Mailings– Location of Bank’s Loan Applications, Originations,

and Deposit Customers– Any Significant Barriers to Lending

Mortgage and Student Loan Servicing

• ECOA Baseline Reviews– ECOA Baseline Modules (CFPB Exam Manual)– Evaluate how well the institution’s compliance

management systems identify and manage fair lending risk

– Assess fair lending training of servicing staff; fair lending monitoring of servicing; and servicing of consumers with limited English proficiency

Small Business Lending

• Assess lending practices in regard to women-owned and minority-owned businesses

• Review lending activity for material discrepancies in ratios of approval-to-denial rates for various geographies

Polling Question #1

Have you conducted an internal Fair Lending assessment within the last 18 months?

A. YesB. No

Regulatory Fair Lending Prioritization

• Risk-based prioritization – data driven approach to identify potential fair lending harm to consumers– Strength of compliance management system– Assess emerging developments and trends in key

consumer financial markets – Consumer complaints– Tips/leads from advocacy groups– Supervisory and enforcement history– Analysis of HMDA data

Exam Scoping

• Develop overview of the Financial Institution• Identify Compliance Program Risk Factors• Review Residential Loan Products• Identify Residential Lending Risk Factors• Organize and Focus Risk & Disparity Analysis• Identify Consumer Lending Risk Factors• Identify Commercial Lending Risk Factors• Complete the Scoping process

How to Prepare?• Ensure policies and procedures are in place that accurately reflect

bank practices

• Review current portfolio for pricing exceptions

• Consider establishing a risk based pricing matrix and apply consistently

• Set-up secondary approval for non-compliance loans (pricing and underwriting)

• Clearly document mitigating factors for non-compliance loans

How to Prepare?• Review legally prohibited factors and train staff

• Determine your REMA and use these parameters when conducting a redlining risk assessment; be aware of where you are lending and marketing, as well as where you are not

• Assess current mortgage and student loan servicing practices

• Consider performing geocode analysis of small business loans

Bank Secrecy Act Beneficial Ownership

Beneficial Ownership

• Final rule: compliance date May 11, 2018

• Impact: effectively a fifth “pillar” for AML programs

• Requirement: Financial Institutions will be required to establish risk-based procedures for conducting ongoing customer due diligence

Coverage

• Applies to “covered financial institutions”:– Depository institutions– Securities broker-dealers– Mutual funds– Futures commission merchants

Requirement

• Establish and maintain written procedures reasonably designed to identify and verify beneficial owners of legal entity customers:– “Legal Entity Customer”: a corporation, LLC, or other

entity form created by filing a public document with a Secretary of State or similar office, a general partnership

– Exclusions include: banking organizations; entities with listed stocks; SEC-registered investment companies; state-regulated insurance companies

Types of Beneficial Owners

• Ownership Prong: “beneficial owner” includes each natural person who, directly or indirectly, owns 25% or more of the equity interest of the legal entity

• Control Prong: “beneficial owner” means a single natural person with significant responsibility to control, manage, or direct the legal entity customer (i.e. a CEO, VP, or Treasurer)

Identification

• At least one beneficial owner is required to be identified for each legal entity customer with respect to the control prong.

Identification and Verification

• Must establish and maintain written procedures reasonably designed to identify, verify, and certify beneficial owners of a legal entity customer

• Procedures must allow financial institution to identify all beneficial owners of each legal entity at the time of account opening

Identification and Verification

• Verify the identity of each beneficial owner using risk-based procedures “to the extent reasonable and practicable”– These procedures must contain the elements required

under the existing CIP

• Retain records obtained regarding beneficial ownership for 5 years. At a minimum: identifying information obtained and a description of documents reviewed to verify the beneficial owner’s identity

Certification

• Use of a model Certification Form, or

• “Obtain from the individual the information required by the form by another means, provided the individual certifies, to the best of the individual’s knowledge, the accuracy of the information”

Polling Question #2

Where is your institution at in implementing the Beneficial Ownership rule?

A. Completely implementedB. Policies and procedures updated, testing of

systems completedC. In process of creating policies and proceduresD. Not yet started

Other Points of Interest

• Rule is not retroactive – only need to obtain information going forward– If a legal entity opens a new account another

certification must be obtained – even with existing relationship

– Examiners will expect a risk-based approach to updates if during normal monitoring there appears to be changes to beneficial ownership information

• The rule applies to all accounts including checking, savings, certificates, and loans

Other Points of Interest

• Beneficial ownership information will need to be in your CTR and AML monitoring system, as you are required to aggregate

• A copy of the identification for beneficial owners is acceptable – retention of these copies is not required but documentation of what was collected is required for 5 years after the account is closed.

Other Points of Interest

• Ownership prong:– May rely on information provided on the certification

form– Potentially no beneficial owner with 25% or more– If entity is an owner, no requirement to identify

natural person behind that entity

• Control prong:– Must collect at least one individual

Other Points of Interest

• If individual opening account does not provide CIP on beneficial owners, account should not be opened

• Non-documentary verification for CIP is allowed for beneficial owners as detailed in your policy/procedures

• OFAC checks are required on beneficial owners

Conclusion

• Ensure policies and procedures are updated to incorporate these requirements

• Review/update forms: signature cards, certification forms, new account worksheets

• Assess your onboarding process

• Assess system for any necessary changes

• Training

Tips, Tricks and TidbitsMiscellaneous Compliance Highlights

Compliance Highlights for 2017 and Beyond

• HMDA revisions implementation

• Consumer Complaint monitoring

• Increased focus on Compliance Management Systems

• Website ADA Compliance

Continued Focus:• TRID

• Loan Officer Compensation

• UDAAP

• New Compliance Rating System

• Third-party risk

Cyber securityPresented by:

Jessica Dore, CISA

Speaker: Jessica Dore, CISA

Principal• Technology Risk Management• Specializes in technology

consulting & security and SOX 404 compliance

• Experience in leading teams and performing IT security assessments for clients

Cyber Security

• The National Institute of Standards and Technology (NIST) defines cyber security as "the process of protecting information by preventing, detecting, and responding to attacks."

• As part of cyber security, institutions should consider management of internal and external threats and vulnerabilities to protect information assets and the supporting infrastructure from technology-based attacks.

Data Breach History

Source: ID Theft Resource Center

Category 2017 (as of 8/2/17) 2016 2015

Banking/Financial 50 (5.7%)2,776,000

52 (4.8%)72,262

71 (9.1%)5,063,044

Business 470 (53.3%)9,219,263

495 (45.3%)5,669,711

312 (39.9%)16,191,017

Educational 93 (10.6%)1,080,151

98 (9.0%)1,048,342

58 (7.4%)759,600

Government/Military 44 (5.0%)216,521

72 (6.6%)13,869,571

63 (8.1%)34,222,763

Medical/Healthcare 224 (25.4%)3,497,804

376 (34.4%)15,942,053

277 (35.5%)112,832,082

Data Breach Costs Are Rising

• The difference a year makes

• The average total cost of a data breach increased from $3.79 to $4 million (+5.3%)– Up 29% since 2013

• The average cost paid for each lost or stolen record containing sensitive and confidential information increased from $154 to $158 (+2.6%)– Up 15% since 2013

Source: Poneman 2016 Cost of Data Breach Study

Average Size of Data Breach By Country

Source: Poneman 2016 Cost of Data Breach Study

The Main Root Causes of A Data Breach

Source: Poneman 2016 Cost of Data Breach Study

• The most common types of malicious or criminal attacks include malware infections, criminal insiders, phishing/social engineering and SQL injection.

• Negligent insiders are individuals who cause a data breach because of their carelessness

Who’s Behind The Breaches?

• 75% were perpetrated by outsiders.

• 25% involved internal actors.

• 18% were conducted by state-affiliated actors.

• 3% featured multiple parties.

• 51% involved organized criminal groups.

Source: Verizon 2017 Data Breach Investigations Report

What Tactics Do They Use?

• 62% of breaches featured hacking

• 51% of breaches included malware

• 81% of hacking related breaches leveraged either stolen and/or weak passwords

• 43% were social attacks

• 8% included physical actions

Source: Verizon 2017 Data Breach Investigations Report

Who Are The Victims?

• 24% of breaches affected financial organizations.

• 15% of breaches involved healthcare organizations.

• 12% of breaches affected public sector entities.

• 15% of breaches affected retail and accommodation.

Source: Verizon 2017 Data Breach Investigations Report

What Else Is Common?

• 66% of malware was installed via malicious e-mail attachments.

• 73% of breaches were financially motivated.

• 21% of breaches were related to espionage.

• 27% of breaches were discovered by third parties.

Source: Verizon 2017 Data Breach Investigations Report

Source: progressbangladesh.com

Cyber Crime Is Here To Stay

• Cyber warrior ‘mercenaries’ for hire worldwide

• Cyber crime is a multi-billion dollar underground economy

• Cyber crime is an industry of suppliers, distributors and manufacturers

• Information is the commodity

Small Organizations A Big Target

• Don’t believe they will be attacked

• Cybersecurity not a priority

• Weak cybersecurity/ outdated tools

• Poor employee training• Poor or no data breach

response plan• Lead to bigger fish

Source: ameriscope.com

Polling Question #3

Has your institution suffered a ransomware attack?

A. YesB. NoC. No, but I know of an institution that has

Phishing

How Do Cyber Criminals Get In?

Ransomware Smishing

Social Engineering DDOS

Keylogging Skimming

Vishing

Malware/Spyware

2016 Most Common Passwords

1. 123456 2. 1234567893. qwerty 4. 12345678 5. 1111116. 12345678907. 12345678. password 9. 12312310. 987654321

Employees Are The Weakest Link

• Negligent insiders are the top cause of data breaches

• Clicking on links in emails

• Sending work email to personal accounts

• Using data on insecure lines

• Not following corporate policies

• Not securing mobile devices

Vulnerability: Weak IT Security

• Poor access controls• Poor patch management• Improper device configuration• Lack of security audits• Weak enforcement of remote login policies

Hot Topics

• Vendor Management– Risk Assessment– Due Diligence at Selection– Annual Due Diligence for Critical Vendors– Contract Reviews

Hot Topics

• Patch Management– Apply patches timely– Ensure system reporting is working appropriately– Board Reporting

Polling Question #4

Does your institution backup data daily?A. YesB. NoC. I’m not sure

Hot Topics

• Backups & BCP – Backup at least daily– Testing of backups and BCP– Manual processes

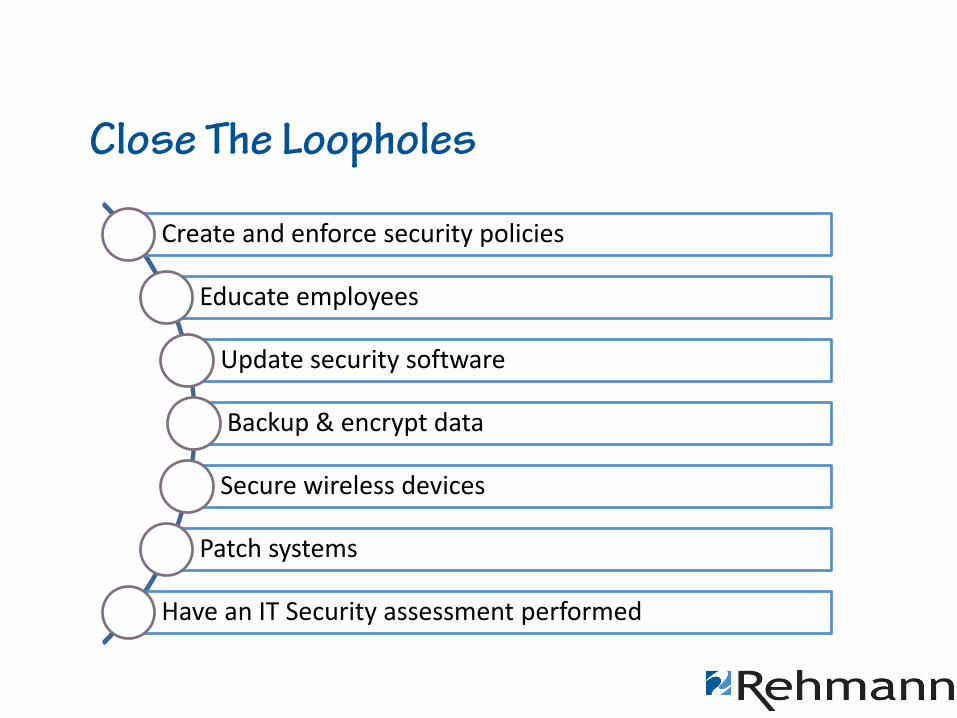

Close The Loopholes

Create and enforce security policies

Educate employees

Update security software

Backup & encrypt data

Secure wireless devices

Patch systems

Have an IT Security assessment performed

Source: blog.zopim.com

In The End …

Q&A Session

Thank you!

Beth Behrend, CCBCO, CBAPPhone: 616.975.4100

Email: [email protected]

Jessica Dore, CISAPhone: 989.797.9580

Email: [email protected]

Liz Ziesmer, CPA, CBAPhone: 616.975.4100

Email: [email protected]