January 1, 2016 Initiating Coverage ICICI Securities Ltd | Retail Equity Research Supreme in plastic industry... Supreme Industries (SIL) is a strong play in the Indian plastic industry with plastic processing capacity of 4.5 lakh tonnes. We believe SIL is well placed to benefit from India’s long term structural reform considering its diversified product portfolio with strong brand, widespread geographic reach, strong balance sheet that has enabled SIL to generate attractive RoCE & RoEs consistently. The company envisages an outlay of ~ | 1500 crore to ramp up capacity to 6.5 lakh tonnes by FY20. We believe various government social programmes would help absorb the incremental capacity. In addition, a gradual shift towards branded products coupled with implementation of GST would help SIL add market share. We believe EBITDA margin will improve in FY15-18E as passing on benefit of lower raw material prices would be partially offset by rising contribution of value added products. We expect consolidated sales, earnings CAGR of ~12%, ~16%, respectively, in FY15-18E. We initiate coverage on SIL with a BUY recommendation. Piping, packaging segment to drive future growth During FY11-15, the piping and packaging segment (out of four segments of SIL) recorded a volume CAGR of ~11% and ~6%, respectively, led by demand from housing and industrial segments. Going forward, with the ramp up in infrastructure activities coupled with rising demand for quality products in India, we believe plastic piping, packaging products volume will record a CAGR of ~15%, ~13%, respectively, in FY15-18E. With the strong distribution channel (~2500 dealers) in India, we believe sales of piping, packaging segment will likely record CAGR of 16%, 13% for FY15-18E. Valued added products (VAP): Play on premiumisation SIL is taking concrete steps to increase VAP’s contribution to total sales from 31.7% in FY13 to 35% by FY20. VAPs commands EBITDA margin of 17% vs. 14.9% (in FY15) at company level. SIL foresees strong demand for cross laminated products, CPVC and bathroom fittings from housing and industrial segments. SIL is further awaiting government approval for a full fledged launch of composite LPG cylinder in India that would further aid its revenue and margin. We believe SIL would partially pass on the benefit of lower raw material prices to customers. Hence, EBITDA margin would see moderate growth of ~130 bps to ~16% for FY17E & FY18E. Strong fundamental justifies premium valuations At the CMP, SIL is trading at a PE multiple of 21x FY17E and 17x FY18E earnings. We expect the company to maintain high RoE and RoCE considering 1) Healthy topline growth backed by capex plan, 2) maintaining higher operating margin and 3) Efficient working capital management turning lower debt/equity ratio. We believe strong brand coupled with sustained growth justify SIL to command premium valuations. We ascribe PE multiple of 21x on FY18E earnings with TP of | 842 and BUY ratings. Exhibit 1: Financial summery (| Crore) FY14 FY15 9MFY16E FY17E FY18E Net Sales 3,905.2 4,219.5 3,017.1 5,018.4 5,883.0 EBITDA 531.7 630.5 393.2 812.7 952.5 Net Profit 283.4 322.4 176.3 420.6 500.0 P/E (x) 30.5 26.8 49.1 20.6 17.3 Price / Book (x) 8.3 7.1 6.6 5.5 4.8 EPS (|) 22.3 25.4 13.9 33.1 39.4 EV/EBITDA (x) 17.0 14.0 22.5 10.8 9.2 RoCE (%) 31.8 32.4 18.9 34.6 36.8 RoE (%) 27.3 26.6 13.4 26.6 27.6 Source: Company, ICICIdirect.com Research Supreme Industries (SUPIND) | 681 Rating Matrix Rating : Buy Target : | 842 Target Period : 12 months Potential Upside : 24% YoY Growth (%) FY15 9MFY16E FY17E FY18E Net Sales 8.0 (28.5) 66.3 17.2 EBITDA 18.6 (37.6) 106.7 17.2 Net Profit 13.7 (45.3) 138.5 18.9 EPS 13.7 (45.3) 124.0 27.5 Current & target multiple FY15 9MFY16E FY17E FY18E P/E 26.8 49.1 20.6 17.3 Target P/E 33.2 60.7 25.4 21.4 EV / EBITDA 14.0 22.5 10.8 9.2 P/BV 7.1 6.6 5.5 4.8 RoNW 26.6 13.4 26.6 27.6 RoCE 32.4 18.9 34.6 36.8 Stock Data Particulars Bloomberg/Reuters code SI:IN/SUPI.BO Nifty 7909.8 Average Volume (Year) 9988419 Market Capitalization | 8650.5 Crore Total Debt (FY15) | 331.5 Crore Cash and Investments (FY15) | 181.8 Crore EV | 8800.2 Crore 52 week H/L (|) 746/520 Equity capital | 25.4 Crore Face value | 1 MF Holding (%) 7.4 FII Holding (%) 21.2 Comparative return matrix (%) Return % 1M 3M 6M 12M Supreme Ind 3.8 8.7 0.4 12.3 Astral Polytec 3.7 2.5 11.5 9.9 Finolex Ind 0.7 17.1 18.9 18.3 Price movement 0 100 200 300 400 500 600 700 800 Aug-12 Dec-12 May-13 Sep-13 Jan-14 Jun-14 Oct-14 Feb-15 Jun-15 Nov-15 0 2,000 4,000 6,000 8,000 10,000 Price (R.H.S) Nifty (L.H.S) Research Analyst Sanjay Manyal [email protected]Hitesh Taunk [email protected]

Transcript

January 1, 2016

Initiating Coverage

ICICI Securities Ltd | Retail Equity Research

Supreme in plastic industry... Supreme Industries (SIL) is a strong play in the Indian plastic industry with plastic processing capacity of 4.5 lakh tonnes. We believe SIL is well placed to benefit from India’s long term structural reform considering its diversified product portfolio with strong brand, widespread geographic reach, strong balance sheet that has enabled SIL to generate attractive RoCE & RoEs consistently. The company envisages an outlay of ~ | 1500 crore to ramp up capacity to 6.5 lakh tonnes by FY20. We believe various government social programmes would help absorb the incremental capacity. In addition, a gradual shift towards branded products coupled with implementation of GST would help SIL add market share. We believe EBITDA margin will improve in FY15-18E as passing on benefit of lower raw material prices would be partially offset by rising contribution of value added products. We expect consolidated sales, earnings CAGR of ~12%, ~16%, respectively, in FY15-18E. We initiate coverage on SIL with a BUY recommendation. Piping, packaging segment to drive future growth During FY11-15, the piping and packaging segment (out of four segments of SIL) recorded a volume CAGR of ~11% and ~6%, respectively, led by demand from housing and industrial segments. Going forward, with the ramp up in infrastructure activities coupled with rising demand for quality products in India, we believe plastic piping, packaging products volume will record a CAGR of ~15%, ~13%, respectively, in FY15-18E. With the strong distribution channel (~2500 dealers) in India, we believe sales of piping, packaging segment will likely record CAGR of 16%, 13% for FY15-18E. Valued added products (VAP): Play on premiumisation SIL is taking concrete steps to increase VAP’s contribution to total sales from 31.7% in FY13 to 35% by FY20. VAPs commands EBITDA margin of 17% vs. 14.9% (in FY15) at company level. SIL foresees strong demand for cross laminated products, CPVC and bathroom fittings from housing and industrial segments. SIL is further awaiting government approval for a full fledged launch of composite LPG cylinder in India that would further aid its revenue and margin. We believe SIL would partially pass on the benefit of lower raw material prices to customers. Hence, EBITDA margin would see moderate growth of ~130 bps to ~16% for FY17E & FY18E. Strong fundamental justifies premium valuations At the CMP, SIL is trading at a PE multiple of 21x FY17E and 17x FY18E earnings. We expect the company to maintain high RoE and RoCE considering 1) Healthy topline growth backed by capex plan, 2) maintaining higher operating margin and 3) Efficient working capital management turning lower debt/equity ratio. We believe strong brand coupled with sustained growth justify SIL to command premium valuations. We ascribe PE multiple of 21x on FY18E earnings with TP of | 842 and BUY ratings. Exhibit 1: Financial summery (| Crore) FY14 FY15 9MFY16E FY17E FY18ENet Sales 3,905.2 4,219.5 3,017.1 5,018.4 5,883.0 EBITDA 531.7 630.5 393.2 812.7 952.5 Net Profit 283.4 322.4 176.3 420.6 500.0 P/E (x) 30.5 26.8 49.1 20.6 17.3 Price / Book (x) 8.3 7.1 6.6 5.5 4.8 EPS (|) 22.3 25.4 13.9 33.1 39.4 EV/EBITDA (x) 17.0 14.0 22.5 10.8 9.2 RoCE (%) 31.8 32.4 18.9 34.6 36.8 RoE (%) 27.3 26.6 13.4 26.6 27.6

Page 2ICICI Securities Ltd | Retail Equity Research

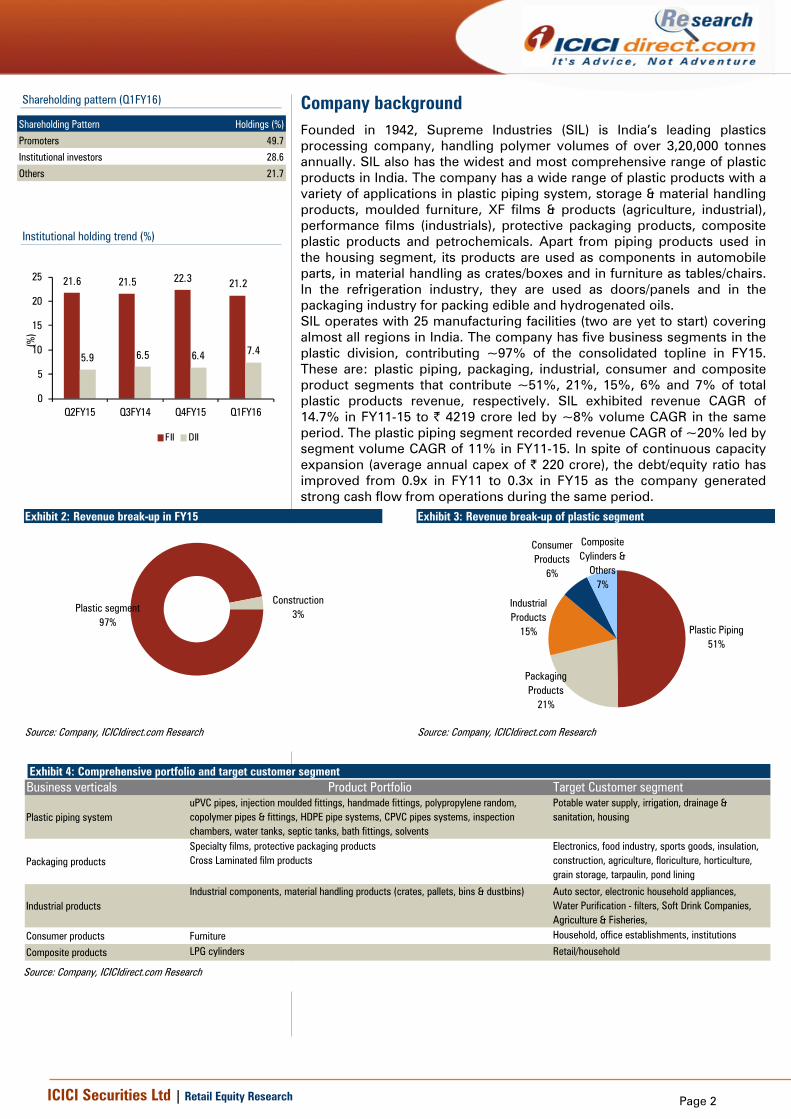

Company background Founded in 1942, Supreme Industries (SIL) is India’s leading plastics processing company, handling polymer volumes of over 3,20,000 tonnes annually. SIL also has the widest and most comprehensive range of plastic products in India. The company has a wide range of plastic products with a variety of applications in plastic piping system, storage & material handling products, moulded furniture, XF films & products (agriculture, industrial), performance films (industrials), protective packaging products, composite plastic products and petrochemicals. Apart from piping products used in the housing segment, its products are used as components in automobile parts, in material handling as crates/boxes and in furniture as tables/chairs. In the refrigeration industry, they are used as doors/panels and in the packaging industry for packing edible and hydrogenated oils. SIL operates with 25 manufacturing facilities (two are yet to start) covering almost all regions in India. The company has five business segments in the plastic division, contributing ~97% of the consolidated topline in FY15. These are: plastic piping, packaging, industrial, consumer and composite product segments that contribute ~51%, 21%, 15%, 6% and 7% of total plastic products revenue, respectively. SIL exhibited revenue CAGR of 14.7% in FY11-15 to | 4219 crore led by ~8% volume CAGR in the same period. The plastic piping segment recorded revenue CAGR of ~20% led by segment volume CAGR of 11% in FY11-15. In spite of continuous capacity expansion (average annual capex of | 220 crore), the debt/equity ratio has improved from 0.9x in FY11 to 0.3x in FY15 as the company generated strong cash flow from operations during the same period.

Exhibit 2: Revenue break-up in FY15

Plastic segment97%

Construction3%

Source: Company, ICICIdirect.com Research

Exhibit 3: Revenue break-up of plastic segment

Composite Cylinders &

Others7%

Consumer Products

6%

Industrial Products

15%

Packaging Products

21%

Plastic Piping51%

Source: Company, ICICIdirect.com Research

Exhibit 4: Comprehensive portfolio and target customer segment Business verticals Product Portfolio Target Customer segment

Starts manufacturing of multilayer sheet unit in Daman to serve automobile, air conditioning and office equipment segment. It also formed a JV with R Raheja Investments to establish Supreme Petrochem

Ties up with Manducher of France for upgradation of auto components business and Schoeller International of West Germany for its technology of new generation bottle crates

Supreme Petrochem signs MoU with Ultrabatch of Italy, a leading manufacturer of high-end additive masterbatches

2014-15

Expanding footprints to eastern and southern markets by establishing plastic piping plants

20091966 1987 1989 1992 1994-95 1998-03

Source: ICICIdirect.com Research

Exhibit 6: Manufacturing facilities spread across India

Source: Company, ICICIdirect.com Research

Supreme Industries’ manufacturing plants are located

across India. Multiple facilities help in reducing risk of

supply to its prominent dealers in case of any natural

calamity. Another significant reason for moving to other

geographies is to gain a competitive edge by strengthening

its distribution network coupled with various tax incentives

(under state rules/regulations)

Page 4ICICI Securities Ltd | Retail Equity Research

Investment Rationale Growth in demand for processed plastic products in India The Indian plastic processing industry has grown at 15% CAGR in volume terms from 6 MTPA in FY08 to 11 MTPA in FY13 while in value terms it recorded 14% CAGR from | 46,585 crore to | 90,000 crore during the same period. Consumption growth was largely driven by increasing usage of plastics in various industries such as agriculture, packaging, automobiles, electronics, telecom, healthcare, infrastructure, transportation and consumer durables. In the last decade, several new applications of plastic products such as use of thermoplastic in the automotive segment and use of packaging products to safeguard the consumer durable items, helped in boosting overall demand. According to Ficci, the plastic processing industry is expected to record a volume CAGR of 14% to 18 MTPA from FY14-18E while in value terms it is expected to record 15% CAGR to | 1,37,000 crore by the end of FY18E.

Exhibit 7: Demand of plastic products (in volume)

6

1112.1

18

02468

101214161820

2008 2013 2014 2018

(MnT

PA)

CAGR 15%

CAGR 14%

Source: Company, ICICIdirect.com Research

Exhibit 8: Plastic processing industry growth trend

The plastic industry chain can be classified into two primary segments: 1) Upstream that entails the manufacture of polymers and 2) downstream that entails the conversion of polymers into plastic articles. The role of the plastic industry (downstream) in the growth of Indian GDP is pivotal as it caters to the entire spectrum of daily use items and covers every sphere of life such as packaging, housing, construction, furniture, automobiles, household items, agriculture, electronics, medical and electrical items. The domestic downstream industry comprises three broad segments: extrusion, injection moulding and blow moulding. The products that are manufactured through these processes can be used in various applications like packaging, automobile, consumer durable, healthcare, etc.

Exhibit 9: Plastic processing industry classification Type of processing Plastic productsExtrusion Films & sheets, fibre and filaments pipes, conduits and profiles, miscellaneous applications

Blow moulding Bottles, containers, toys and housewares

Roto moulding Large circular tanks such as water tanks Source: Company, ICICIdirect.com Research

Extrusion moulding is the most commonly used plastic processing method. Its products contribute ~60% to total consumption in India followed by injection moulding plastics articles, which contribute ~25% to the total consumption in India. It is a fast process and is used to produce large numbers of identical items from high precision engineering components to

According to FICCI, the plastic processing industry is

expected to record volume CAGR of 10% to 18 MTPA in

FY13-18E while in value terms it is expected to record a

CAGR of 15% to | 137000 crore by the end of FY18E

The domestic downstream industry comprises three broad

Page 5ICICI Securities Ltd | Retail Equity Research

disposable consumer goods. Products from other moulding processes contribute the balance ~15% to total plastic consumption in India. Roto moulding and blow moulding are the most commonly used processes after extrusion and injection moulding. Roto moulding is a process used to produce hollow plastic products. Typical products produced are manhole inspection chambers, rainwater tanks, slides and climbing frames, diesel fuel tanks, children’s playhouses, traffic cones and pellets. Blow moulding is used for the production of hollow objects in large quantities. The main applications are in bottles, jars and other containers.

Exhibit 10: Polymer consumption in India according to various process

Other Processes8%

Roto Moulding1%

Blow Moulding6%

Injection Moulding

25%Extrusion

60%

Source: Company, ICICIdirect.com Research

Per capita consumption: India among lowest globally In the last 10 years, the use of plastics has increased notably in various industries due to its unique and diverse blending properties. Despite plastic increasingly becoming a material of choice of widespread consumption, the current per capita consumption in India (in kg/person) is still much below (~9.7 kg) other nations like the US (~109 kg) and China (~45 kg). Keeping the demographic scenario in mind, we believe there is enough scope for a rise in plastic consumption in India.

Exhibit 11: Per capital plastic product consumptions (kg/person)

109

65

45

9.7

32

0

20

40

60

80

100

120

USA Europe China India Brazil

(|/k

g)

Lower per capita consumptiontranslates to huge opportunityfor plastic consumption

Source: Company, ICICIdirect.com Research

Exhibit 12: Utilisation of plastic products

35

25

17 15

8

43

2116 18

2

05

101520253035404550

Pack

agin

g

Infra

stru

ctur

e

Auto

Othe

rs

Agric

ultu

re

(%)

Global India

Use of plastic products in agriculture and infrastructure is substantially lower in India compared to global average

Over 30,000 units in the organised/unorganised sector are

engaged in plastic processing across the country. Almost

85% of the small & medium enterprises (SME) segment

employs over 4 million workers across the value chain

Per capita consumption of plastic products in India (in

kg/person) is still much below (~9.7 kg) other nations like

the US (~109 kg) and China (~45 kg)

Page 6ICICI Securities Ltd | Retail Equity Research

Application of plastic products in various industries

Plastic piping industry: Structural reform to drive demand The plastic piping industry (largely PVC) in India has been growing at a CAGR of ~12-15% in the last five years. It is largely due to growth in construction activities in tier-II and tier-III cities, replacement of conventional piping systems like galvanised iron & cast iron piping systems and increase in demand for branded agriculture & plumbing piping. The piping industry consists of two segments viz. 1) plastic piping and 2) metal piping. The size of the total piping industry in India is ~| 27,500 crore largely dominated by the plastic piping industry, which is considered to be ~| 21,500 crore while the metal piping industry is about | 6000 crore. Since replacement of metal by plastic has been happening rapidly, the plastic industry is expected to grow at an accelerated pace in the coming years (we believe at the same historical rate).

Exhibit 13: Structure of Indian piping industry

Domestic piping industryValue: | 27500 crore

Plastic piping Value: | 21500 crore

Industry growth: CAGR 12-15%

Metal piping Value | 6000 crore

Organised segment (65%-70%)Value: | 13900 crore

Unorganised segment (30-35%)Value: | 7500 crore

Source: Company, ICICIdirect.com Research

Exhibit 14: PVC piping industry (with market share of listed players)

PVC piping industryVolume: ~17,00,000

Organised market (60%)

~10,20,000 MT

Unorganised market (40%)

~6,80,000 MT

Finolex IndustriesVolume: 185706 MT

Supreme IndustriesVolume: 204264 MT

Astral PolyVolume 69919 MT

Jain Irrigation*Volume: 240000 MT

OthersVolume: 172933 MT

Source: Company, ICICIdirect.com Research, market share by sales volume, includes CPVC pipe volumes also

We believe, future demand for piping products would largely be driven by various factors such as:

1. Government’s flagship programme of ‘Housing for all by 2022’

According to Census 2011, India had a population of ~121 crore, out of which ~38 crore (~31.2%) lived in urban areas. During 2001-11, the urban population of India grew at a CAGR of 3.1%, resulting in an increase in the level of urbanisation from 27.8% to 31.2%. This growing urbanisation has led to problems of land shortage, housing shortfall and congested transit and also severely stressed existing basic amenities such as water, power and open spaces of the towns and cities. According to Census 2011,

The total piping industry size in India is ~| 27,500 crore

largely dominated by the plastic piping industry, which is

considered to be ~| 21,500 crore while the metal piping

industry is at about | 6000 crore

Source: ICICIdirect.com Research

Growing brand and quality consciousness – share of

organised players to rise further

Government’s focus on increasing irrigation and housing

will help to keep the industry growth strong over the next

3-5 years

Page 7ICICI Securities Ltd | Retail Equity Research

housing stock in urban India is ~7.8 crore for ~7.9 crore urban households. Though the gap between household and housing stock is narrowing, the actual shortage of homes is high as some portion of the current stock is decrepit and people live in congested homes. Rising urbanisation has resulted in people increasingly living in slums. Poor economic condition of the weaker section of society has forced them to adjust to lack of amenities. According to a government estimate, housing shortage in urban India was 18.8 million units in 2012 with ~75% of the estimated housing shortage concentrated in 10 states (shown in Exhibit 15). Considering these factors, currently there exists a wide gap between demand and supply of housing in urban India. According to KPMG, a demographic trend suggests India is on the verge of large scale urbanisation over the next few decades. With more than 1 crore people getting added to urban areas, India’s urban population is expected to reach about 81 crore by 2050.

Exhibit 15: Technical Group estimates show housing shortage of 18.78 million in 2012

Rest of states/Uts,

4.47

Gujarat, 0.99

Karnataka, 1.02

MP, 1.1

Rajasthan, 1.15 Bihar, 1.19 Tamilnadu, 1.25

AP, 1.27

West Bengal, 1.33

Maharashtra, 1.94

UP, 3.07

Source: Census 2011, ICICIdirect.com Research

Exhibit 16: Increment in housing stocks

15.119.2

24.7

14.718.7

24.5

0

5

10

15

20

25

30

1991 2001 2011

( cro

re)

Households Housing Stocks

Source: Census 2011, NHB, ICICIdirect.com Research

To bridge the demand supply gap and acknowledge the importance of housing issue in the country, the government has launched a massive campaign of ‘Housing for All by 2022’. As per KPMG estimates, the vision would require development of ~11 crore houses and outlay of over US$2 trillion (or about US$250-260 billion annual investment until 2022). Most housing development would be expected for the economically weak section/low income group households (in both rural and urban areas) whose income is less than | 2 lakh per annum.

Exhibit 17: Number of housing units required under ‘Housing for all by 2022’ programme Particulars Urban (crore unit) Rural (crore unit) Total (crore unit)

Current housing shortage 1.9 4 5.9

Required housing units by 2022 2.6-2.9 2.3-2.5 4.9-5.4

Total Need 4.4-4.8 6.3-6.5 10.7-11.3

Source: KPMG, ICICIdirect.com Research

We believe housing shortage coupled with lack of proper water management system (sewage/drainage) in slums creates ample opportunity for the piping industry in India. The major application of PVC pipes is in water management for the housing and agriculture sectors. Since SIL earns nearly 65% of its piping revenue from the housing segment, we believe the company would be a direct beneficiary of various government initiatives such as ‘Housing for All by 2022’, 100 smart cities, etc. where PVC pipes & fittings are used for supply of water in households, removal of waste water, linking of drainage systems, pipes for micro irrigations, etc.

Source: ICICIdirect.com Research

As per KPMG estimate, the vision would require

development of ~11 crore houses with investment of over

US$ 2 trillion (or about US$ 250 to 260 billion annual

investment until 2022)

Source: ICICIdirect.com Research

Page 8ICICI Securities Ltd | Retail Equity Research

2. Swachh Bharat Mission: Boost for plastic products Swachh Bharat Mission (SBM) is another flagship programme of the government aimed to stop open defecation through construction of individual household latrines (IHHL), cluster toilets and community toilets (especially via PPP mode). Solid and liquid waste management is also an important component of the programme. According to Census 2011, over 67% of rural households in India lack access to toilets. In other words, more than 11 crore rural households do not have access to a toilet.

The government has also allocated total | 1,96,000 crore to SBM with | 1,34,000 crore coming from the Ministry of Drinking Water & Sanitation and the rest from the Urban Development Ministry. Under the scheme, total 2,47,000 gram Panchayats of India will be provided | 20 lakh each to spend on sanitation. We believe lack of sanitation and drinking water facility at ~13 crore households creates a huge opportunity for PVC pipe manufacturers like Supreme Industries, Astral Poly, Ashirvad and Finolex Pipes.

Exhibit 18: Households without sanitation and drinking water facility (in crore) Total Households 25

Households sources water outside the premises 13

Households have to fetch water from a source located within 500 m in rural areas/100 m in urban areas 9

Fetch drinking water from a source located more than 500 m away in rural areas or 100 m in urban areas 4

Households have no drainage facility (rural + urban) 12

Household without toilets (rural + urban) 12 Source: Census 2011, ICICIdirect.com Research

Exhibit 19: Number of toilets constructed each year for individual rural households

88.0 45.6 49.8 40.1 57.2

1113

0

200

400

600

800

1000

1200

2011-12 2012-13 2013-14 2014-15* 4 yr avg Target by 2019

(Lak

hs)

Source: Census 2011, ICICIdirect.com Research

According to Census 2011, over 67% of rural households in

India lack access to toilets. In other words, more than 11

crore rural households do not have access to a toilet

Source: ICICIdirect.com Research

We believe lack of sanitation and drinking water facility at

~13 crore households creates a huge opportunity for PVC

pipe manufacturers like Supreme industries, Astral Poly,

Ashirvad and Finolex Pipes

Page 9ICICI Securities Ltd | Retail Equity Research

3. AMRUT: Targets 500 cities to raise water supply, sewerage, urban transport system The government has also launched its programme Atal Mission for Rejuvenation and Urban Transformation (AMRUT) to provide basic services to household and build amenities in cities. The purpose of AMRUT is to: 1. Ensure that every household has access to a tap with assured supply of water and sewerage connections. 2. Increase the amenity value of cities by developing greenery and well maintained open spaces (e.g. parks). 3. Reduce pollution by switching to public transport or constructing facilities for non motorised transport (e.g. walking and cycling).

Under the scheme, ~500 cities and towns have been selected on the basis of population i.e. one lakh and above. The project would help improve existing basic infrastructure services like extending clean drinking water supply, improve sewerage networks, develop seepage management, lay storm water drains, improve public transport services and create green public spaces like parks, etc. The ‘High Powered Expert Committee’ has estimated that | 39.2 lakh crore is required for creation of urban infrastructure, including | 17.3 lakh crore for urban roads and | 8 lakh crore for services, such as water supply, sewerage, solid waste management and storm water drains. Moreover, the requirement for Operation and Maintenance (O&M) was separately estimated to be | 19.9 lakh crore. AMRUT, a flagship programme to improve the infrastructure of the country would be the future growth driver of the plastic piping industry.

4. Plasticulture: Rising trend of plastic uses in agriculture Agriculture contributes nearly ~14% to GDP and provides employment to ~58% of the Indian population. Plasticulture refers to use of plastics in agriculture and horticulture. Indian agriculture has witnessed various changes in the form of mechanised farming to improve yield of the crop. Use of plastic products not only helps reduce infrastructure cost but improves both quality and quantity of crops. The application of plastic products in agriculture substantially reduces costs and increases water saving and water use efficiency. Therefore, it can lead to high productivity of crops. According to Ficci, each application can save water by 30-100%. In case of farm ponds lined with plastic film, the total loss by seepage of water can be minimised to zero.

Exhibit 20: Major use of plastics in agriculture Application Comments

Drip irrigation systemPonds and reservoirs linings greenhouse have precise application of irrigation water and plant nutrients at low pressure and at frequent intervals through drippers/emitters directly into the root zone of the plant

Sprinkle irrigation system

-Application of water under high pressure with the help of a pump.-Water is released through a small diameter nozzle placed in pipes

Ponds & reservoir linings-Plastics film lining to prevent seepage in canals, ponds and reservoirs-Also avoids depletion of stored water used for drinking & irrigation purpose

Greenhouse-Greenhouse is a framed structure covered with glass or plastics film-Acts as selective radiation filter, in which plants are grown under the controlled environment

Source: FICCI, ICICIdirect.com Research

Exhibit 21: Benefits from Plasticulture applications Application Water saving (%) Water use Efficiency (%)

Drip irrigation 40-70 30-70Sprinkler irrigation 30-50 35-60Greenhouse 60-85 20-25Farm pond lined with plastic film 100 40-60

Source: FICCI, ICICIdirect.com Research

AMRUT can be considered a remodelled version of

JNNURM wherein the government has worked on many

flaws present in the earlier programme

An estimate of the funds required over a 20 year period (at

2009-10 prices), was made by the High Powered Expert

Committee during 2011

Source: ICICIdirect.com Research

Plasticulture refers to use of plastics in agriculture and

ponds & reservoirs with plastic films, greenhouses, plastic

crates, bins, boxes, etc

Page 10ICICI Securities Ltd | Retail Equity Research

Rising trend of micro irrigation system (MIS) The current domestic industry size of MIS is pegged at ~| 4000 crore (FY14) with penetration at a mere ~9% [6 million hectares (MH) out of the net irrigated area of ~70 MH]. In India, it is more prevalent in Maharashtra, Gujarat, Rajasthan, Tamil Nadu, and Andhra Pradesh among others. The domestic industry has grown at a CAGR of 15% in FY09-14. It is expected to grow at a CAGR of ~15%, going forward, in FY14-17. The payback period for farmers domestically is in the range of one or two years. The below table discusses penetration (in 2011) of MIS in India vis-à-vis other countries. To boost the use of MIS, a wide array of incentives is being provided by central & state governments towards its implementation. The Central government, in the past, has been promoting MIS through its flagship programme National Mission on Micro Irrigation (NMMI) with budget outlay become ~3x in the last five years to ~| 1100 crore in FY15. Exhibit 22: Low penetration of MIS creates huge scope for increasing its penetration in India

CountryTotal Irrigated Area

(MH)Sprinkler Irrigation

(MH)Drip Irrigation (MH) Total MIS (MH) MIS Penetration

Source: International commission on irrigation & drainage, ICICIdirect.com Research

Exhibit 23: Government outlay to support MIS

430

1000 11

50

1500

1342

1121

1800

4 80

972 12

27

120 3 1 271

7 15

0200400600800

100012001400160018002000

FY10 FY11 FY12 FY13 FY14 FY15E FY16E

(| c

rore

)

Budget Outlay Actual Expenditure

Source: Ministry of agriculture,* data as on Nov’14, ICICIdirect.com Research, ICICIdirect.com Research

Plastic piping segment: Sales to record ~16% CAGR in FY15-18E

While the piping industry has been growing at 12-15% CAGR in the last 10 years, SIL’s piping revenue recorded a CAGR of 30% during the same period largely driven by the construction sector and replacement demand. Further, we have modelled revenue CAGR of ~16% in FY15-18E for the piping division, led by ~15% volume growth. Plastic piping capacity is expected to increase at 10% CAGR in the same period. To summarise, the demand for plastic pipes would largely be driven by:

1. Replacement of conventional piping systems like galvanised iron and cast iron piping systems with plastic is ongoing and will continue in the near term

2. Growth in construction, mainly in rural & Tier-II and III cities is going to be supported by demographic change, aspirations of better lifestyle, nuclear family concept & continuous rise of middle class

3. Increase in demand for branded agriculture and plumbing pipes because of increase in income levels

4. The company has introduced a silent pipe system made of PVC for the first time in the country. This is mainly used in high rise buildings, hospitals and high quality hotels.

The domestic micro irrigation system industry has grown

at a CAGR of 15% in FY09-14 and is expected to grow at a

CAGR of 20%, going forward, in FY14-17E

To boost the use of MIS, a wide array of incentives is being

provided by central & state governments towards its

implementation

The plastic piping capacity of SIL is expected to increase at

a CAGR of 10% in FY15-18E. This would help in sales

volume CAGR of 15%

Page 11ICICI Securities Ltd | Retail Equity Research

Safety measures to drive packaging revenue at ~13% CAGR in FY15-18E The Indian packaging industry is pegged at US$33.8 billion (rigid packaging US$26.7 billion, flexible packaging US$7.1 billion) at a CAGR of 13-15%. Processed food packaging with ~48% market share in the overall packaging industry dominates the other three segments i.e. personal care packaging with ~27% market share, pharmaceutical 6% market share and others 19% market share. Plastics are preferred for their ability to pack the processed food. Government data showed the size of the Indian food processing industry is ~US$83 billion and has grown at 8.4% CAGR in the last five years. The growth of the food processing industry is a blend of increasing urbanisation, young population and income level. According to Ficci, the industry is expected to continue to record 8% CAGR for FY15-18E.

On the other hand, under the protecting packaging industry, SIL products protect food items in grain storage and pond lining. Tarpaulin is used to cover products, thereby protecting them from moisture and dust. It can be used as a protective covering in sectors like agriculture, infrastructure, automobiles and also as tents, floor spreads, as a cover for machinery, etc. Under agriculture, tarpaulin is used to cover food grains. According to FCI, over 1.94 lakh metric tonnes of food grains were wasted in India due to lack of proper infrastructure to safeguard foods between 2005 and 2013.

Exhibit 24: Tarpaulin used to cover food grains

Source: Businessline, ICICIdirect.com Research

Exhibit 25: Food grains waste

95075

25353

4426

20114

31480

20000

40000

60000

80000

100000

2005-06 2006-07 2007-08 2008-09 2012-13

(MT)

Damaged stocks

Source: FCI, ICICIdirect.com Research

SIL’s protective packaging products are used in sports goods, electronics, white goods, textiles, healthcare, toys, etc. The large and growing Indian middle class, along with growing organised retailing in India are fuelling growth in the packaging industry. Another factor that has provided substantial stimulus to the packaging machinery industry is the rapid growth of exports, which needs superior packaging standards for the international market. In the packaging segment, we have modelled ~13% revenue CAGR in FY15-18E led by 12.6% volume growth, on the back of good traction of demand from agriculture, construction and white goods segments. The company introduced premium brand Silpaulin (cross laminated films products), which contributes ~49% to packaging products sales. The product is considered to be a value-added product wherein the product margin is above ~17%. In the last three years, cross laminated film products sales have recorded ~11% CAGR led by ~6% price hike. SIL is focused on increasing the proportion of higher margin product (by expanding its distribution network) to sales to improve its overall EBITDA margin.

Source: ICICIdirect.com Research

Source: ICICIdirect.com Research

Page 12ICICI Securities Ltd | Retail Equity Research

Exhibit 26: Protective packaging products, industry size and application of products

ProductsEstimated market

size (| crore)Market share (%) Application

EPE foam 600 34%

1. Packaging of electronic goods, ceramics, handicraft and glassware2. Foam sheets are widely used for insulation of air conditioners, industrial chillers, cold water pipes, air handling units, industrial refrigerators3. Used in automobiles for cabin insulations, door panels, seat linings, engines, bonnets4. Used in fabrication of gymnastics and exercise mats, leg guards, arm elbow/shoulder pads, helmets

Air bubble film 350 15%

1. Packaging of fragile items like crockery2. Packaging of electronic items and protection of screens3. Precious antiques packaging4. Vital packaging in pharmaceutical industry

Cross linked foam (block) 330 22%

1. Medical device packaging2. Military grade tool control3. Orthopaedic soft goods4. Athletic padding/helmet lining5. Protective case inserts

Cross linked foam rolls (chemical)

90 56%Used largely for commerical purpose like thermal insulation, construction expansion joints, industrial gaskets, etc

Nitrile PVC rubber foam 95 7%

1. Ideal sealing material against gas or liquid2. Excellent shock and impact absorbing characteristics uses in gym and athletic equipment

Source: Company, ICICIdirect.com Research

Page 13ICICI Securities Ltd | Retail Equity Research

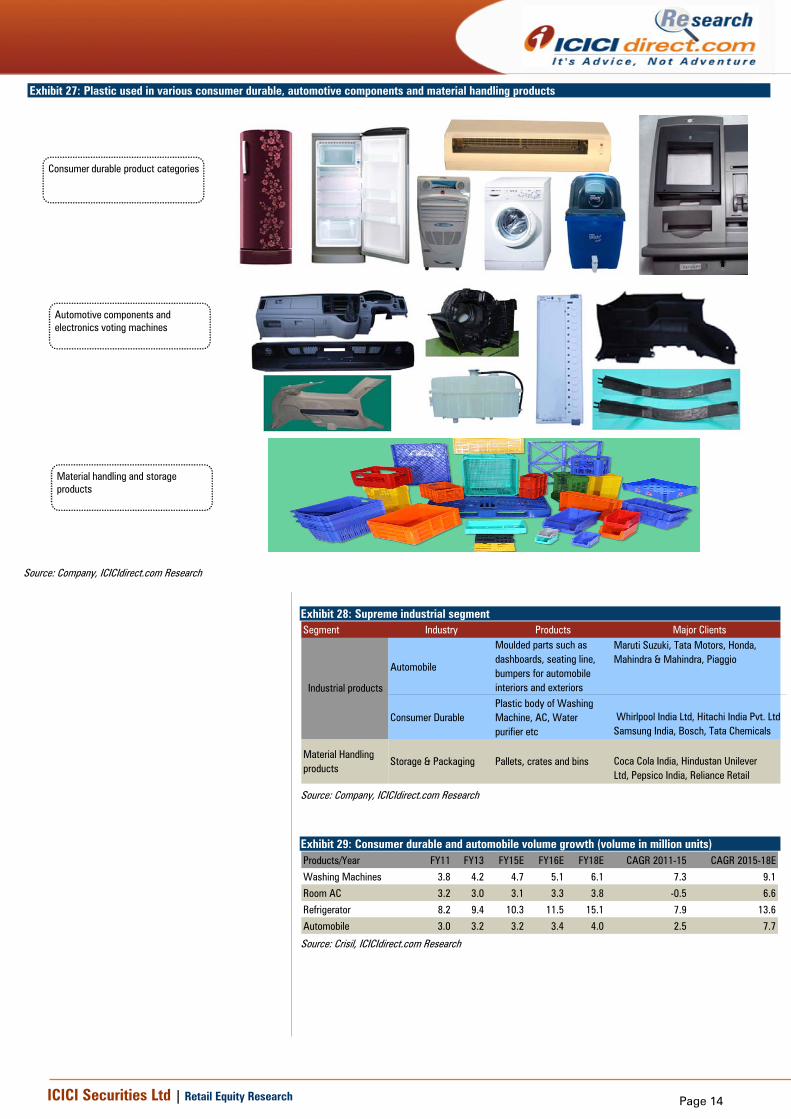

Industrial products: Growth likely with rising demand for consumer goods SIL’s industrial products segment contributes nearly 15% (| 649 crore) to the topline. It has a total capacity of 54,700 MTPA by the end of FY15. The company’s industrial product segment can largely be segregated into two segments 1) industrial components and 2) material handling products.

Industrial components: revival in CD demand and automobile to drive volume growth The company is a prime supplier of plastic parts and assemblies to various consumer durable (CD) and automobile Industry players. In the CD category, it supplies the plastic body of washing machines, ACs, refrigerators, water purifiers and coolers coupled with various other customised solutions like the body of ATMs, electronic voting machines, etc. In the automobile segment, the company supplies various solutions for dashboard, bumpers, fuel system, seating lines, storage battery, etc. As revenues of these segments are dependent on CD and automobile industry performance, lower volume growth in these segments in FY11-15 adversely impacted the performance of the industrial component segment of SIL. During FY15, revenues of industrial components recorded abysmal growth of 3% YoY led by 11% YoY growth in revenue of products sold to the electronics and appliances industry. However, sales from the automotive segment declined 4% YoY. Going forward, we believe the company will benefit from a revival in CD demand (expected volume CAGR in the range of 7-14% for FY15-18E) and automotive segment (volume CAGR of ~15% in FY15-18E). SIL has further added a new MNC client, Bosch to its marquee client portfolio in FY15 for the supply of plastic body of its various appliances. Bosch is expanding it appliances production capacity and is expected to launch new products in near future. Also, the company has also started manufacture of air coolers in Noida for its reputed client.

Material handling products: Marquee clients in portfolio In the material handling segment, the company is one of the largest suppliers to the soft drink industry to the likes of Coca Cola and Pepsi. SIL also supplies pellets and bins to various storage companies, the fisheries industry and government organisations. The segment is highly competitive as majority of the players in this segment are unorganised. Organised players other than SIL present in this segment include Nilkamal, Wimplast and Time Technoplast. The segment recorded value growth of ~23% YoY in FY15, led by volume growth of ~12% YoY. Going forward, we believe the company’s growth will be driven by sustained demand from the soft drink industry as well as expansion of the distributor network in future. SIL has increased the number of its channel partners from 192 to 202 in FY15. The company plans to further increase the number in the coming future. We also believe that being an industrial category product where the customer has substantial bargaining power, the EBITDA margin in this segment may remain at ~ 12% (same as recorded in FY15).

We have modelled revenue CAGR of ~11% in the overall industrial products segments (both industrial, material handling products) led by volume CAGR of ~10% for FY15-18E on the back of a revival in demand in the CD and automobile segments. Demand for this category of products has remained muted in the last three years. Hence, the company has refrained from any major capex in the segment. SIL has taken a cautious approach towards increasing the capacity of this division. However, the company has largely focused on increasing the quality of the product and launching premium products in this category.

During FY15, revenue of industrial components recorded

abysmal growth of 3% YoY led by 11% YoY growth in

revenue of products sold to the electronics and appliances

industry.

The company has further added a new MNC client, Bosch

to its marquee client portfolio in FY15 for supply of plastic

body of its various appliances

Material handling is highly competitive as a majority of the

players in this segment are unorganised. Organised players

other than SIL present in this segment include Nilkamal,

Wimplast and Time Technoplast

Page 14ICICI Securities Ltd | Retail Equity Research

Exhibit 27: Plastic used in various consumer durable, automotive components and material handling products

Consumer durable product categories

Automotive components and electronics voting machines

Material handling and storage products

Source: Company, ICICIdirect.com Research

Exhibit 28: Supreme industrial segment Segment Industry Products Major Clients

Automobile

Moulded parts such as dashboards, seating line, bumpers for automobile interiors and exteriors

Page 15ICICI Securities Ltd | Retail Equity Research

Consumer products: Change in strategy to drive segment profit Supreme is one of the well known players in the plastic furniture industry with 10% market share (in value terms) behind Nilkamal (with ~53% market share) and Wimplast (with ~13% market share). The estimated market size of the plastic furniture industry is ~| 2900 crore. The company is present in economic (plastic chairs, stools) as well as premium (sofa set, table, office furniture, and premium chairs) segments. Currently, SIL manufactures plastic furniture at five different locations. In the last three years, the segment revenue growth remained muted mainly due to the company’s strategy to exit the commodity business and focus more on premium products. This is clearly evident from an increase in proportion of premium products from 38.4% in FY13 to 47.6% in FY15. However, YoY, there was a marginal decline in proportion of premium products by ~90 bps YoY mainly due to a delay in launch of premium products in the key markets. It is further commencing a greenfield project to manufacture new category of furniture products at Kharagpur at an investment of | 30 crore, which will start production by Jan’2016.

Exhibit 30: Focus more on premium products took toll on revenue growth

262.0 268.0 276.0 259.0 276.3

197.9

300.7336.8

050

100150200250300350400

FY11

FY12

FY13

FY14

FY15

FY16

E*

FY17

E

FY18

E

(| c

rore

)

Source: Company, ICICIdirect.com Research * 9MFY16E

Exhibit 31: Market share of consumer plastic segments

Others20%

Prima Plastic4%

Supreme Ind10%

Wimplast13%

Nilkamal 53%

Source: Company, ICICIdirect.com Research

Seventh Pay Commission: To drive premium product sales, going forward

We believe SIL would benefit from implementation of the Seventh Pay Commission wherein the government is expected to hike the pay of ~1.4 crore government employees by ~23.5% (as per Pay Commission recommendation). Post the wage hike, the consumption pattern is likely to shift towards the premium product category. This coupled with rising urbanisation and continuous demand from tier II and tier III cities would help drive the sale of furniture in the near future. SIL plans to continue to increase the proportion of premium furniture in the consumer products category. The company has launched a new range of premium products for exports in coming years. SIL plans to increase the contribution of premium furniture to 65% of segment revenues by the end of FY19E.

In FY15, SIL exported its premium range of furniture to South Korea. The company is further expected to add more countries to its kitty in the coming years. We have modelled moderate revenue CAGR of ~9% for FY15-18E (vs. ~1% CAGR in FY11-15) in the consumer product segment supported by capacity addition in the furniture segment (upcoming plant in south India. The strategy is to focus on the premium product category and increase the number of exporting destinations.

Source: ICICIdirect.com Research

Supreme plans to increase the contribution of premium

furniture to 65% of segment revenues by the end of FY19E

Page 16ICICI Securities Ltd | Retail Equity Research

Composite products: Strong product pipeline The company entered the composite products category in FY12 citing immense growth potential. Composite materials include any products made from a blend of two or more base materials. These typically offer enhanced strength or durability over many other products and may provide additional benefits like resistance to moisture or corrosion. Under the composite products category, SIL largely manufactures composite LPG cylinder and pellets. The company has installed capacity for composite pipes. However, plants are not yet operational. SIL blends various materials to manufacture fibre glass, which is used to manufacture LPG cylinders.

Composite LPG cylinder: Ready to use capacity, waiting for government approval

Currently, there are 16.4 crore LPG consumers in India who use steel made LPG cylinders. Steel cylinders have two major drawbacks: 1) Issue of leakage, which may lead to blast in the cylinder and 2) Checking of quantity to avoid theft. The new composite cylinder has been launched to address these two basic problems. However, cylinders are expensive compared to steel cylinders (| 2500-3000 almost double the regular steel cylinder, for which LPG distributors charge | 1,400 as security deposit). However, they are safer and accident free as they do not explode unlike steel cylinders. As the cylinders are translucent, the level of gas can also be seen, which will be an added advantage for consumers. Empty cylinders weigh half as much as present steel cylinders so they are easy to carry and also aesthetically better looking. SIL has incurred an expense of | 70 crore to set up a greenfield capacity to manufacture LPG composite cylinders with an installed capacity of 500,000 cylinders per annum at Halol (Gujarat) with six variants of capacity ranging from 5 kg to 14 kg.

India is the largest market for LPG cylinders. Oil companies have recognised the use of composite cylinders despite higher cost. Oil marketing companies are expected to float a tender for an education order in two sizes, 12.5 lakh and 24 lakh. Considering the higher deposit amount, the government is mulling launching these products for urban consumers first. Since the use of composite cylinder in India is still not permitted, the company is using its capacity for the export market. In FY15, SIL had exported the first lot of composite cylinders of 33.3 lakh to South Korea. The company is in further discussions with many countries for this product and hopes to finalise business. We expect utilisation rates of this product to pick up gradually and be a major revenue driver once the Government of India permits sale of this product in the Indian market.

Exhibit 32: Composite LPG cylinders

Advantage over steel cylinders Disadvantage

Light weight & ergonomic:Cylinders are designed for easy handling and are 1/3rd lighter then traditional metal cylinder

Transparent:cylinders that will make it almost impossible for vendors to deliver lower-than-promised quantity

Explosion proof:100% explosion proof. Withstands three times higher pressure than traditional onesNon-corrosive:It does not corrode or have rust marks like steel cylinders

Eco-friendly:Majority of materials used are recyclable

Composite LPG cylinders

A transparent cylinder is likely to cost | 2,500-3,000, almost double the regular steelcylinder, for which LPG distributors charge |1,400 as security deposit

Source: Company, ICICIdirect.com Research

Composite materials typically offer enhanced strength or

durability over many other products and may provide

additional benefits like resistance to moisture or corrosion.

Under the composite products category, the company

largely manufactures composite LPG cylinder and pellets

Consumption of fibreglass products in India is around 1.2

lakh tonnes per annum compared to consumption in China

of over 1 million tonnes. With excellent properties of

fibreglass and varied application opportunities available,

we expect healthy growth in composite products business

SIL has incurred an expense of | 70 crore to set up a

greenfield capacity to manufacture LPG composite

cylinders with an installed capacity of 500,000 cylinders

per annum at Halol (Gujarat) with six variants of capacity

ranging from 5 kg to 14 kg

Page 17ICICI Securities Ltd | Retail Equity Research

Composite pipe: Production remains stalled

The company planned to start production of composite pipes in collaboration (technical tie-up) with Japan’s NBL. The corporation has patented the technology and process to manufacture high pressure composite pipes. These composite pipes are very suitable for down hole and casing pipes for the oil & gas industry. These are much lighter compared to present special steel pipes in use. They are anti-corrosive, which is very much desirable for these applications. The company completed the plant in Halol, Gujarat (same campus where cylinders are being manufactured) in FY13 at an investment of ~ | 16 crore to produce ~15000 pipes per annum. However, it encountered some technical problems during the trial run, which led to some difference of opinion with its technology provider NBL Corporation of Japan. The issue has remained unsolved. The production capacity has remained idle since its commencement.

Multiple manufacturing plants help reduce geographical concentration and serve dealer network effectively

Exhibit 33: Plant location across region

Source: Company, ICICIdirect.com Research

SIL is a well-diversified plastic processing company with a de-risked manufacturing base in India. The modern manufacturing process (more than 25 plants spread across regions in India) and highly scalable business model enable the company to quickly respond to changing trends of plastic demand. With south and east India fast emerging as the new plastic manufacturing hub of India, the proposed capacity expansion (for

The plant in Halol, Gujarat was completed (same campus

where cylinders are being manufactured) in FY13 at an

investment of ~ | 16 crore to produce ~15000 pipes per

annum

Currently, SIL operates 25 plants across India. The

manufacturing base at different locations reduces its

geographic concentration risk. It also helps the company to

expand its dealer network to new geographies

Malanpur Unit III and Kharagpur unit are under construction

and are likely to commence operations during Q2FY16

Line

Page 18ICICI Securities Ltd | Retail Equity Research

manufacturing plastic piping system in Assam and plastic piping, protective packaging & furniture products in south India) is expected to help SIL to reduce its geographic concentration risk by diversifying operations across India. In addition, having multiple facilities helps reduce risk of supply to its prominent dealers in case of any natural calamities. Another significant factor behind moving to other geographies is to gain a competitive edge by strengthening distribution networks coupled with various tax incentives (under state rules/regulations).

Further, with continuous investments in increasing capacity, a strengthening dealer network and maintaining high product quality SIL has been able to maintain its position as one of the largest players in the PVC pipe industries. Further, the company is better placed than (or at least at par with) its competitors in terms of having a 2469-strong dealer network across India. We believe continuous capacity expansion along with regular addition to the dealer network would result in overall volume CAGR of ~12% for FY15-18E against ~8% during FY11-15. Exhibit 34: Strong dealer network spread across regions Company Distribution Networks

Regular capacity addition to drive topline Backed by strong volume growth over the last five years coupled with its strategy to spread wings across India, the company incurred a capex of over | 1000 crore to increase capacity from 3.3 lakh tonnes to 4.5 lakh tonnes in FY15. Considering better volume growth, going forward, SIL is further planning an aggressive expansion of | 1500 crore across business segments over the next five years. This would increase its capacity to over 6.5 lakh tonnes by FY20. This would be a combination of greenfield as well as brownfield projects. As far as greenfield expansion is concerned, the company would be adding a few more locations by FY20. This would take the number of facilities to 28 from the existing 25. Exhibit 35: Upcoming facility Division Proposed location for 2015-16 to 2017-18

Plastic Piping System Rajasthan

Plastic Piping System Assam

Plastic Piping System, Protective packaging Products & Furniture Southern India Source: Company, ICICIdirect.com Research

During FY16 (9MFY16), SIL is envisaging a capex of about | 200 crore to be funded through accruals and suppliers credit on the following segments:

1. Ongoing work of setting up a plastic products complex in Kharagpur (West Bengal) and Roto moulded products unit at Malanpur (MP)

2. Expansion of capacities of bath fitting products 3. Introduction of several varieties of moulded fittings at Jalgaon &

Malanpur plants 4. To introduce large range of premium furniture products in all its

manufacturing plants 5. To put up Roto moulding capacity at Kanpur (UP) and Kharagpur

(West Bengal) plants 6. To install polyethylene and PVC pipes capacity for sewerage and

drainage applications

Supreme has a total dealer network of ~2469 spread

across India. The company is further planning to expand its

dealer network with the addition of new capacity

In the last five years, the company has incurred a capex of

over | 1000 crore and expanded capacity from 3.3 lakh

tonnes to 4.5 lakh tonnes

Page 19ICICI Securities Ltd | Retail Equity Research

7. To construct new building and install special machines for making varieties of cross laminate film made up products at its Gate Muvala (Gujarat) plant

8. To increase the capacity and range of pellets in material handling products division

9. To increase production capacity of protective packaging products at various locations and invest in a new location

10. To invest in balancing equipment and automation at all its plants as may be required

Focus to enhance share of value-added products in total sales SIL is taking concrete steps to increase the share of value-added products to its total sales to 35% by FY20 from 31.7% in FY13 by launching products in niche categories. As a part of its renewed strategy to launch niche products, the company has added high-rise low-noise SWR systems (required in high rise buildings, hospital and high quality hotels), plastic faucets, CPVC fire sprinkler pipes, and new product verticals within the cross-laminated division like 35 gsm Silpaulin, LPG composite cylinders, composite pipes and bathroom fittings. In the furniture business, the company adopted a strategy to focus more on premium category products. This resulted in short-term hiccups for the furniture segment wherein volumes recorded a continuous decline between FY11 and FY15. Further, SIL plans to increase the share of value-added products under the furniture segment to 65% from the current 48%. To achieve this goal, the company has put up a greenfield project in Kharagpur at an investment of | 30 crore. Considering the superiority of the products, SIL also plans to start export of these products in a big way. Exhibit 36: Increasing share of value-added products

Apart from rising concentration of value-added products to sales, the company also believes in continuous innovations and launching of new products in almost every business segment. Some examples are as follows:

1. Only Indian company to have the technology to manufacture patented cross laminated film products under brand name Silpaulin. It is 100% water-proof and weather resistant (UV stabilised) besides, being tough, light weight, rot proof and having heat sealed joints

2. The company introduced silent pipe system made from PVC for the first time in the country

3. Launching the composite LPG cylinder in the Indian market on a trial basis after the government

4. The company introduced 72 injection moulded pipe fittings during FY15 and total 387 new products to the range of various plastic piping systems. With this, the total product portfolio in this segment has now reached 6500 from 6113 in FY14

Source: ICICIdirect.com Research

SIL is taking concrete steps to increase the share of value

added products to its total sales to +35% from current

34% by 2019-20

Page 20ICICI Securities Ltd | Retail Equity Research

Tie-ups with experts to improve quality of the products Supreme Industries being a market leader is concerned about the relevance and quality of the products. In order to provide a better experience and quality products to end users, the company has entered into technical tie-ups with various multinational companies across the world. The technical collaboration has helped SIL improve the quality (by adopting new technology) thereby producing international standard products at minimal operating costs. This has also helped the company to create strong brand value of its products and helped increase the contribution of value added products in total sales. Exhibit 37: Technical collaboration with various MNC to drive expertise Company Country Product Line

Rasmussen Polymer Development Switzerland Cross-laminated Films

Wavin Netherlands Plastic Piping Systems

Foam Partner Switzerland Reticulated PU Foam

Sanwa Kako Japan 2 stage Foam

PE Tech Korea Cross Linked Foam

Kumi Kasai Co. Ltd Japan Automotive Components

Kautex GMBH Germany Composite LPG Cylinders

Spears Mfg. Co Los Angeles Fire Sprinkler Pipes from CPVC

Calcamite Sanitary Services South Africa Septic Tanks

Source: Company, ICICIdirect.com Research

Real estate monetisation to be one time event As a part of company’s strategy to unlock the value of land located in the prime location of Andheri (West) Mumbai, SIL has developed a commercial real estate project with the help of the R Raheja Group. The company has developed ground plus 10 storied state-of-the-art commercial complexes called Supreme Chambers. The complex has a total saleable area of 2,82,835 sq ft. Of this, the company has already sold about 2,12,286 sq ft. raising ~| 338.6 crore. The complex has modern facilities like health club, conference room, parking for 350+ cars, etc. with green building rating from the US Green Building Council (USGBC).

The management plans to sell the entire complex excluding about 6681 sq ft (kept for self use). The management expects another | 125 crore from the sale of remaining portion available for sale, even higher realisation than previously considering limited availability of good office premises in the vicinity of the company’s premise. The total cost of the project is ~| 145 crore. Cash flow from monetisation will be funding capex and reduce debt on the balance sheet. We have factored in an inflow of | 107 crore from the sale of property (on a conservative basis and below management expectation) on our assumption, considering the major inflow had happened in FY17E.

To provide a better experience and quality products to end

users, the company has entered into technical tie-ups with

various multinational companies across the world

The management expects another | 125 crore from the

sale of the remaining portion available for sale, even higher

realisation than previously considering limited availability

of good office premises in the vicinity of the company’s

premise

Page 21ICICI Securities Ltd | Retail Equity Research

Supreme Petrochem: Strategic investment Supreme Petrochem is an associate company wherein Supreme Industries and the R Raheja Group own 29.99% each in the company. The company is mainly into four products: 1) Polystyrene, 2) Expandable Polystyrene, 3) Speciality Polymers and Compounds Business and 4) Extruded Polystyrene Insulation Board (XPS). Supreme Petrochem operates a modern polystyrene facility with an installed capacity of 2,85,000 tonnes per annum (Polystyrene and compounded polymers) at Raigad (Maharashtra) and Chennai (Tamil Nadu). Polystyrene is a thermoplastic resin being applied in television cabinets, car components, novelty items, food packaging, computers, air-conditioners and washing machines, beads, bangles, etc. The company also has an Expandable Polystyrene (EPS) capacity of ~65,000 tonnes per annum technical collaboration with Nova Inc US with a buyback arrangement of EPS cup grade production. The company accounts for 2% of global capacity and 60% of domestic installed capacity.

In the last five years, annual sales of the company recorded moderate CAGR of 8%, due to a decline in volume of Polystyrene. The company is expected to restrict investment in the four verticals of Supreme Petrochem as SIL has built adequate capacity to deal with future demand. With the recovery in demand of polystyrene, low level of capex and almost debt free status of the company we believe Supreme Petrochem would remain a positive contributor to the PAT of Supreme Industries, going forward.

Exhibit 38: Volatility in sales led by volume

1943.72272.67

2967.163264.3

2652.54

0500

100015002000250030003500

FY11 FY12 FY13 FY14 FY15

(| c

rore

)

0.0

2.0

4.0

6.0

8.0

10.0

(%)

Net sales EBITDA Margin

Source: Company, ICICIdirect.com Research

Exhibit 39: EBITDA margin movement hits PAT

87.7

33.4

73.5

30.6 35.7

0

20

40

60

80

100

FY11 FY12 FY13 FY14 FY15

(| c

rore

)

PAT

Source: Company, ICICIdirect.com Research

Supreme Petrochem is an associate company wherein

Supreme Industries and the R Raheja Group own 29.99%

each in the company

Page 22ICICI Securities Ltd | Retail Equity Research

Key Financials Sales CAGR of ~12% backed by expansion plan During the last five years, SIL recorded sales CAGR of 14.7% driven by volume CAGR of 8%. The volume growth was largely driven by good demand of piping products. However, rising contribution of value-added products in the total portfolio helped drive realisation growth to the tune of 6.4% during the same period. The piping segment, contributes ~50% to the topline, recording sales CAGR of 20% during FY11-15, led by volume CAGR of 11% during the same period. Volume growth of the piping segment came on the back of better demand (translated into regular capacity addition) from the housing segment in tier II and tier III cities. We believe, rising contribution of value added products in the total portfolio from 31.7% in FY13 to over 35% by FY20 would help drive realisations northward for the company. We have modelled revenue CAGR of 12% for FY15-18E (in line with historical growth rate) largely supported by volume CAGR of ~14% during the same period. The volume growth is expected to be largely be driven by strong demand for piping products (volume CAGR ~15%) from the expansion in the new geographies. Packaging products contribute 21% to the topline and are expected to record sales CAGR of ~13% supported by good traction of cross laminated products. Further, industrial segment sales are expected to grow 11% largely supported by a revival in demand for automotive and consumer durable segment, going forward. Additionally, the consumer products segment where the company remained a passive player for the last few years is expected to record a sales CAGR of 11% attributable to increasing the focus on the premium product category. In addition, we have modelled revenue inflow of | 107 crore from sale of real estate business (~15% lower than the management expectation).

Exhibit 40: Capacity expansion on the cards to drive volume growth

2219

18

2457

00

2706

47

2754

63

3019

30

2293

02

3885

06 4425

61

0

100000

200000

300000

400000

500000

FY11 FY12 FY13 FY14 FY15 9M'16E FY17E FY18E

CAGR 8%

CAGR ~14%

Source: Company, ICICIdirect.com Research

Exhibit 41: Net sales growth driven by piping division

Source: Company, ICICIdirect.com Research, Financial year FY16 is for 9 month

The topline is expected to grow at a CAGR of ~12%

during FY15-18E to | 5883 crore in FY18E from | 4219

crore during FY15 led by growth in the piping segment

Supreme Industries has a diverse range of products. We

believe sales of the company will grow on the back of rising

investment in infrastructure, housing, packaged foods, sports

goods, potable water supply & sanitation, auto, electronics,

horticulture, floriculture etc.

Page 23ICICI Securities Ltd | Retail Equity Research

Rising contribution of value added products coupled with lower raw material prices to drive EBITDA margin In the last five years, the EBITDA margin has grown ~160 bps to 14.9% on account of a strong brand, rising contribution of value added products, lower commodity prices, higher contribution of in-house manufactured product into sales. We believe raw material (largely derivative of crude oil like PVC, Polypropylene and Polyethylene) prices will remain subdued in the near term. The company being a strong brand in the plastic business is least likely to pass on the entire benefit of lower raw material prices. This coupled with rising focus on launching premium products and increasing the contribution of value added products (as value added products command EBITDTA margin more than 17%) in revenue would drive EBITDA margins, going forward. The company’s value added products like cross laminated products (Silpaulin) and CPVC have performed well in the last three years wherein sales recorded CAGR of 11% and 16%, respectively, with growth in realisation by 5-6% during the same period. We model an EBITDA margin of ~16% for FY17E & FY18E considering the benefit of lower raw material prices with rising contribution of value-added products. The moderate expansion in margin is expected in the backdrop of the ongoing expansion plan into new geographies, which may seize some benefits of lower raw material prices, going forward.

Exhibit 43: Rising sales coupled with lower RM cost to drive EBITDA

324.2433.6 490.7 531.7

630.5

393.2

812.7952.5

0

200

400

600

800

1000

1200

FY11 FY12 FY13 FY14 FY15 9MFY16EFY17E FY18E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Exhibit 44: Saving from lower material cost to drive EBITDA margin

13.3 14.8 14.6 13.6 14.9 13.016.2 16.2

35.3 35.4 33.8 31.7 33.6 33.3 35.6 35.3

05

1015202530354045

FY11 FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(%)

EBITDA margin Gross Margin

Source: Company, ICICIdirect.com Research

Exhibit 45: Softening price of HDPE (YTD decline ~12% YoY)

HDPE price

020,00040,00060,00080,000

100,000120,000140,000

Jan-

07

Aug-

07

Mar

-08

Oct-0

8

May

-09

Dec-

09

Jul-1

0

Feb-

11

Sep-

11

Apr-1

2

Nov

-12

Jun-

13

Jan-

14

Aug-

14

Mar

-15

(|/to

nne)

Source: Crisil, ICICIdirect.com Research

Exhibit 46: Decline in LDPE price (YTD decline ~24% YoY)

LDPE price

020,00040,00060,00080,000

100,000120,000140,000

Jan-

07

Jan-

08

Jan-

09

Jan-

10

Jan-

11

Jan-

12

Jan-

13

Jan-

14

Jan-

15

(|/to

nne)

Source: Crisil, ICICIdirect.com Research

We believe raw material (largely derivative of crude oil

like PVC, Polypropylene and Polyethylene) prices will

remain subdued in the near term. As the company has a

strong brand in the plastic business it is least likely to

pass on the entire benefit of lower raw material prices.

We model EBITDA margin of ~16% for FY17E & FY18E

considering benefit of lower raw material prices with

rising contribution of value added products

Page 24ICICI Securities Ltd | Retail Equity Research

Better margin coupled with lower interest outgo to drive PAT CAGR of 16% for FY15-18E The company recorded a net profit CAGR of 13% in the last five year led by increase in sales and EBITDA margin. However, being a capital intensive business, SIL required continuous capex to fund expansion and working capital requirement. Over the years, capital expenditure has yielded better inflows resulting in a reduction in debt by 35% from FY11. As a result, the interest expanses reduced 24% YoY in FY15 leading to a 100 bps YoY increase in PAT margin. A further reduction in interest outgo (I-direct view: reduction by ~19% by the end of FY18E) coupled with sales CAGR ~12% for FY15-18E would further help in driving PAT growth by 16% for FY15-18E.

Exhibit 47: Net profit to grow at ~16% CAGR in FY15-18E

195.

8 241.

7 290.

1

283.

4

322.

4

176.

3

420.

6 500.

0

0

100

200

300

400

500

600

FY11 FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(| c

rore

) CAGR ~13%

CAGR ~16%

Source: Company, ICICIdirect.com Research

Exhibit 48: Asset turnover to improve gradually with recovery in demand for plastic products

2.0

2.42.1

2.2 2.3

1.5

2.22.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

FY11 FY12 FY13 FY14 FY15 9MFY16 FY17 FY18

(x)

Source: Company, ICICIdirect.com Research

Over the years, capital expenditure has yielded better

inflow resulting in a reduction in debt by 35% from FY11.

As a result, the company’s interest expanses reduced

24% YoY in FY15 helping 100 bps YoY increase in PAT

margin

The company recorded a net profit CAGR of 13% in the last

five year led by increase in sales and EBITDA margin. We

believe with a reduction n debt outgo coupled with

marginal increase in EBITDA margin, the net profit of the

company will record CAGR 16% for FY15-18E

Fixed assets turnover (FAT) of Supreme Industries Limited

has been stable in the range of 2-2.3 during the last five

years. We believe, company’s operating efficiency to

improve going forward with the stability in the new plants

Page 25ICICI Securities Ltd | Retail Equity Research

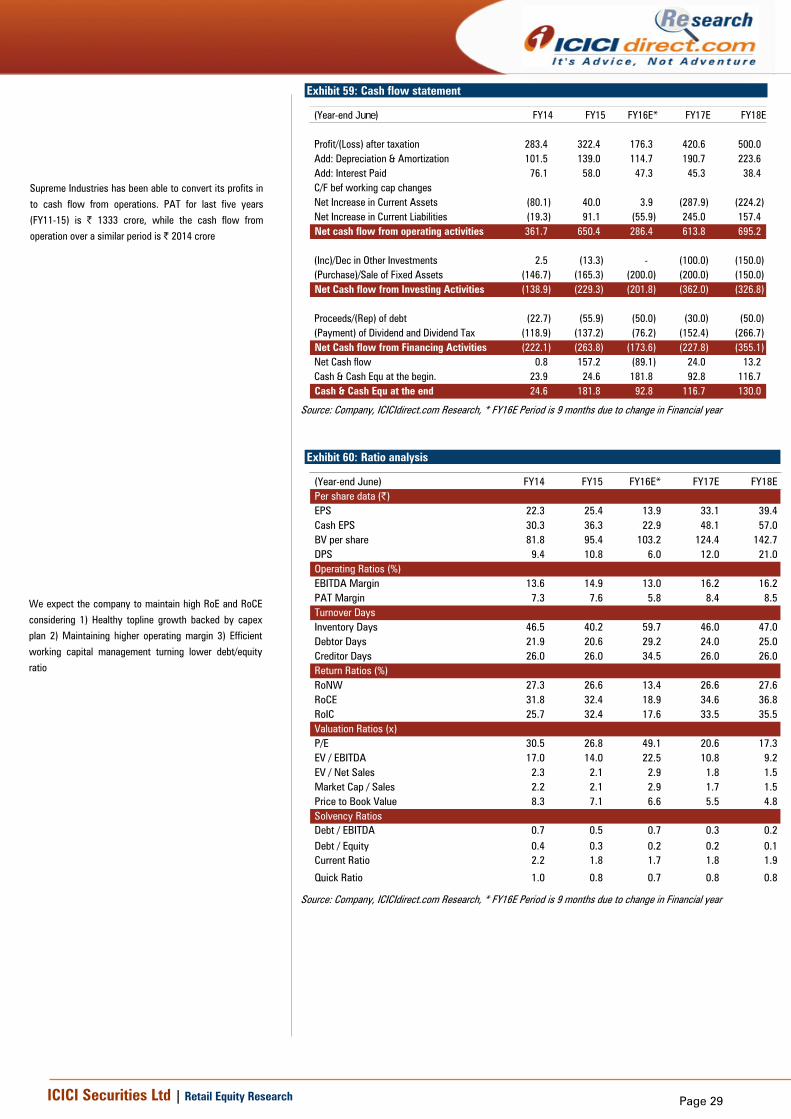

Strong free cashflow leads to reduction in debt With efficient working capital management coupled with continuous growth in earnings, the company has garnered free cash flow of ~| 1062 crore in the last four years. Due to a strong brand, SIL has power of negotiation with its dealers to manage receivables days under control. This has helped the company to fund its capex as well as reduce debt over the years. We believe the strong fundamental of the company followed by a revival in the economy would further help generate strong operating cash flow in the FY17E and FY18E and would help in further reduction in debt level by | 130 crore by FY18E. Consequently, the company recorded a strong return ratio over the last five years (RoE & RoCE recorded at 27% & 37%, respectively during FY15).

Exhibit 49: Strong operating cashflow flows into free cashflow….

403.9

14.6

222.8

421.0

84.6

251.7

368.4

050

100150200250300350400450

FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Exhibit 50: Helps in reduction in debt level

255

410387

331281

251201

050

100150200250300350400450

FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(| c

rore

)

Source: Company, ICICIdirect.com Research

Exhibit 51: Free cash flow to help in reduction in debt level

0.40.5

0.40.3

0.2 0.2 0.1

0.9

0

0

0

1

1

1

FY11 FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(%)

D/E

Source: Company, ICICIdirect.com Research

Exhibit 52: Efficient capital management translates into strong ratios

34.7 33.027.3 26.6

13.4

26.6 27.6

38.932.9 31.8 32.4

18.9

34.6 36.835.8

26.4

0

10

20

30

40

50

FY11 FY12 FY13 FY14 FY15 9MFY16E FY17E FY18E

(%)

RoE RoCE

Source: Company, ICICIdirect.com Research,

Supreme Industries has been able to convert its profits to

cash flow from operations. PAT for the last five years

(FY11-15) is| 1333 crore while the Cash Flow from

operation over the similar period is | 2014 crore

Page 26ICICI Securities Ltd | Retail Equity Research

Risk & concerns Volatility in crude prices Major raw materials consumed by the company are poly vinyl chloride (PVC), polyethylene (PE) and polypropylene (PP), which are linked to crude prices. SIL imports 50% of raw materials. Thus, a sharp increase in crude prices could hurt the EBITDA margin of the company as it passes on a rise in crude price with a lag of two to three weeks.

Exhibit 53: EBITDA margin movement with respect to crude oil price

82 85

70

87

114 111 108

86

0

20

40

60

80

100

120

FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

(US$

/bar

rel)

0

2

4

6

8

10

12

14

16

(%)

Crude oil price EBITDA margin

Source: Company, ICICIdirect.com Research

Delay in capacity expansion Being a capital intensive business, it is necessary for the company to continuously invest in the business to sustain growth. Sales of the company may get negatively affected if there is any hurdle (regulatory, environmental) in the expansion plan.

Influence of government policies in irrigation segment

Use of plastics in agriculture is still in a nascent stage in India. However, rising awareness on micro irrigation and government subsidies helped the industry to get good exposure from the agriculture industry. We believe any change in government policy (in terms of subsidy) could hurt demand for the products and, thus, sales of the company. Delay in government flagship programmes

Government programmes like Housing for All, Swachh Bharat and AMRUT would be a strong boost to the plastic piping industry in India, going forward. However, any delay in execution of such projects could hurt the demand for plastic products in India.

Competition from unorganised players The plastics industry is considered to be highly fragmented, with a large unorganised segment. Thus, the company has to continuously spend on a brand building exercise and technological innovations to improve its market share.

Page 27ICICI Securities Ltd | Retail Equity Research

Valuation Supreme Industries, with a plastic processing capacity of over 4,50,000 tonnes in FY15, is one of the largest plastic processors in India. The company is a pan-India player with 25 manufacturing plants and ~2500-strong dealer network. This makes Supreme a strong brand in all plastic product verticals.