16

How Markets Work SM January 2007 Recent Trends in Shareholder Class Action Litigation: Filings Plummet, Settlements Soar Todd Foster Ronald I. Miller, Ph.D. Stephanie Plancich, Ph.D.

| Date post: | 10-Feb-2018 |

| Category: |

Documents |

| Upload: | trankhuong |

| View: | 217 times |

| Download: | 3 times |

How Markets WorkSM

January 2007

Recent Trends in ShareholderClass Action Litigation:Filings Plummet, Settlements Soar

Todd FosterRonald I. Miller, Ph.D.Stephanie Plancich, Ph.D.

Only 129 federal shareholder

class actions were fi led

from January 1 through

December 15, 2006, with 135

fi lings for the full year if the

same pace is maintained.

This is a 36% drop from 2005

levels, and a 44% decline from

the post-PSLRA average.

Recent Trends in Shareholder Class Action Litigation:

Filings Plummet, Settlements Soar

January 2007

Todd Foster, Ronald I.Miller, Ph.D., Stephanie Plancich, Ph.D.1

Settlements Break Records, While Filings Continue to Decline

This year will stand out as one of record settlements. There were more settlements over $100 million—the so-called

mega-settlements—in 2006 than in 2005, itself a record-breaking year. In 2006, there were four settlements over

$1 billion.2 This is an astonishing development given that before 2006 only three settlements had ever exceeded

$1 billion. Litigation in the Enron matter continues, with over $7.1 billion allocated to fund settlements so far.

These huge cases have raised average settlement values to their highest level ever.

While eyes have been focused on these settlements, federal court fi lings of shareholder class-actions have plummeted.

The drop-off in fi lings, fi rst observed at the end of 2005, accelerated through 2006. Annual 2006 federal fi lings

are at the lowest level since 1996—a year that was itself unusually low because many fi lings were moved to state courts

in an attempt to bypass the restrictions imposed by the 1995 passage of the Private Securities Litigation

Reform Act (“PSLRA”).

Federal Filings Continue to Drop

Filings in federal courts in 2005 were somewhat low relative to the average over the previous decade. More

specifi cally, there were 211 fi lings for full-year 2005, compared to the annual post-PSLRA average of 239 standard

fi lings each year.3 Examining these fi lings more closely reveals an even more dramatic picture: while fi lings were

roughly in line with prior years through the fi rst half of 2005, they began to drop rapidly starting in July of that year.

There were only 78 fi lings in second-half 2005, compared to 131 in second-half 2004. By contrast, the fi rst half of

2005 had more fi lings than the fi rst half of 2004.

nera.com 1

2 nera.com

We noted this decline in a previous NERA report that

considered year-end 2005 data.4 However, because fi lings

can have substantial month-to-month variation, it was

impossible to tell at that point whether the decline refl ected

a temporary aberration or a new trend. The continued

decline in 2006 allows us to conclude that the change is

indeed statistically signifi cant. Only 129 federal shareholder

class actions were fi led from January 1 through December

15, 2006, with 135 fi lings for the full year if the same

pace is maintained. This is a 36% drop from 2005 levels,

and a 44% decline from the post-PSLRA average.

While the magnitude of this drop-off in fi lings is notable,

the decline has not been evenly distributed across the

circuits. The largest drop in absolute terms has come from

the Ninth Circuit, where, compared to a peak of 68 in

2004, there have been only 27 shareholder class action

suits fi led through December 15, 2006. However, every

circuit has fewer standard fi lings in 2006 than the average

level from 1998-2004. The drop is smallest in the Second

Circuit, which in 2006 has seen fully 87% of the fi lings it

typically received over 1998-2004.5 The rest of the circuits

as a group have received only about half of their typical

1998-2004 fi lings. All but two of the circuits had a

decline of at least one-third from 2005 to the projected

2006 fi gures.

It is not yet clear what is driving this precipitous decline. One

hypothesis is that Sarbanes-Oxley (“SOX”), passed in July

2002, has now had enough time to cause improvements in

Federal FilingsJanuary 1, 1991 – December 15, 2006

550

500

450

400

350

300

250

200

150

100

50

1991

167

1992

206

1993

172

1994

244

1995

213

1996

130

1997

201

1998

277

1999

252

2000

240

2002

288

2005

211

2001

518

2003

250

2004

257

2006

135

Market Timing CasesLaddering Cases Analyst Cases Projected FilingsStandard Filings

15 1131

246225

254

210

129

304

corporate governance that have limited fraud and resulting

shareholder class actions. For this story to hold, however,

SOX would need to have had strongly different effects

across the Circuits, with much less impact in the Second

Circuit. This differential effect seems unlikely. One possible

explanation for the difference is that the fi nance sector,

strongly represented in the Second Circuit, has reacted less

to SOX than have other industries. However, the fi nance

sector has seen lower than average fi lings this year, leaving

us without a clear explanation for why the Second Circuit

has had such a different experience from the rest of

the country.

Another possibility is that the decline is the result of

distraction on the part of some of the largest plaintiffs’

law fi rms. Milberg Weiss has been the subject of federal

indictment and has suffered the highly-publicized loss of

some partners, while Lerach Coughlin has been occupied

with a mass of litigation surrounding Enron. If limitations

in the resources of the plaintiffs’ bar turn out to be the

cause of the trend in fi lings then we would expect fi lings

to return to higher levels in the future. In this case, we

might also expect average settlements to rise going

forward (or dismissal rates to fall) as an entrepreneurial

plaintiffs’ bar would focus its energy on the most

promising cases.

nera.com 3

Companies Face a 1.6% Chance of a Suit each Year

1993-1995 2004-2006 %Change

No. of Publicly Traded Companies 11,688 12,339 5.6%

Annual Filings 210 201 -4.2%

Probability of Shareholder Class Action (SCA) 1.8% 1.6% -9.3%

Probability of Dismissal 19.4% 38.2% 97.0%

Probability of SCA that Surivives Motion to Dismiss 1.4% 1.0% -30.4%

Standard Federal Filings By Circuit2005 vs. Projected 2006

60

50

40

30

20

10

DC23

1st

8

2nd

44

3rd

13

4th

4

5th 6th

3

7th

2

8th 9th

28

11th

13

10th

3

45

Projected 20062005

1310

14

52

21

11 10 12

69 11

7

Moreover, the decline in the likelihood of facing a suit

has been augmented by an increased dismissal rate

so that the probability of a company facing a suit that

survives a motion to dismiss has fallen by more than 30%.

Based on the fi ling rate from 2004 to 2006, the average

public corporation faces a 7.9% probability that it will face

at least one shareholder class action lawsuit over a fi ve-year

period.6 The annual likelihood of a suit has fallen 9%

since the period from 1993 to 1995, from 1.8% to 1.6%.

Every circuit but two had a decline of at

least one-third from 2005 to the projected

2006 fi gures.

4 nera.com

Filings Dropped Despite Options

Backdating Litigation

The drop in fi lings in 2006 is even more surprising given

that the count of 129 fi lings through December 15 includes

22 fi lings involving allegations of options backdating. These

cases represent something novel and distinct from more

typical issues for shareholder class action litigation. Indeed,

as the litigation plays out, it may make sense to group

these cases with the IPO laddering and Wall Street analyst

cases as non-standard fi lings. As with these other litigations,

options backdating cases may be a short-term block of

litigation that is unlikely to recur. If this is correct, then

the numbers above understate the drop in the volume

of standard shareholder class action litigation, and the

trend rate of fi lings has fallen even further than it

currently appears.

These counts of fi lings for options backdating cases may

appear low given the volume of media and professional

attention that backdating has received. This is because the

majority of backdating litigation involves derivative actions,

not shareholder class actions. Indeed, there have been

at least 80 derivative actions fi led through December 15.

Filing of a shareholder class action suit with a substantial

chance of success requires an unusual drop in share prices,

a feature not shared by many of the backdating cases

where derivative actions have been fi led.

Dismissal Rates By Circuit Within Two Years Of FilingFilings December 15, 2000 – December 15, 2004

40%

35

30%

25%

20%

15%

10%

5%

1st

25%

2nd

19%

3rd

10%

4th

31%

5th

20%

6th

21%

7th

16%

8th

28%

9th

20%

10th

5%

11th

22%

Dismissal Rates

Dismissal rates have nearly doubled since PSLRA.7 Dismissals

accounted for only 19.4% of dispositions for cases fi led

between 1991 and 1995. More recently, for cases fi led

between 2000 and 2004, dismissals have accounted for

38.2% of dispositions.8 Our post-PSLRA dismissal rate may

be slightly overstated, as it may include some dismissals

without prejudice that will be reversed by amended and

better-pled complaints or dismissals with prejudice that

will be successfully appealed. There is no indication that

dismissal rates have continued to rise after an initial

adjustment to the tougher pleading provisions of PSLRA.

Dismissal rates vary by circuit. Both the Second and Ninth

Circuits, which together receive the preponderance of

cases, dismiss approximately 20% of cases within two years

of the fi ling date. The Fourth Circuit has the highest rate,

dismissing more than 31% of fi lings within two years, while

the Tenth Circuit has the lowest. Note that these rates

are lower than the 38.2% rate cited above as the overall

dismissal rate because they include only dismissals within

two years of fi lings. This different calculation is performed

for technical statistical reasons relating to the smaller

number of observations for individual circuits.

Top Ten Shareholder Class Action SettlementsAs of December 2006

Settlement

Value

Ranking Company Year ($MM)

1 Enron Corp.� 2006 $7,144

2 WorldCom, Inc. 2005 6,156

3 Cendant Corp. �� 2000 3,561

4 AOL Time Warner Inc. 2006 2,650

5 Nortel Networks (I) 2006 1,143

6 Royal Ahold, NV 2006 1,100

7 Nortel Networks (II) 2006 1,074

8 McKessson HBOC Inc. 2006 960

9 Lucent Technologies, Inc. 2003 517

10 BankAmerica Corp. and NationsBank Corp. 2002 490

� This is a partial settlement including only some defendants.

�� The settlement value incorporates a $374 million settlement in the Cendant PRIDES cases.

The Era of Mega-Settlements: Seven of the Ten

Largest Settlements Occurred in 2005-2006

In 2000, the $3.6 billion Cendant settlement dwarfed

all prior class action settlements.9 For the next four years,

no settlement would approach even one-fi fth of its size.

In 2005, however, Cendant lost its title as the largest

settlement, bumped by the $6.2 billion WorldCom

settlement. Now, in 2006, with only some of the

defendants settled, Enron’s $7.1 billion settlement has

already knocked WorldCom out of the top spot. In

fact, seven of the ten largest securities class action

settlements have occurred in 2005 and 2006.

These mega-settlements share a common feature: they

are associated with enormous “investor losses.” Investor

losses—an estimate of what investors lost over a class

period relative to an investment in the S&P 500—are the

single most powerful predictor of settlement size.10 Thus,

while eye-popping settlements have grabbed headlines

recently, their magnitude is not surprising in light of the

losses involved.11

In what will surely be chilling news to non-US issuers

already wary of being embroiled in US litigation, three of

the six 2006 settlements on the top ten list, two for Nortel

Networks of Canada and one for Royal Ahold NV of the

Netherlands, were by non-US companies. The larger of the

Nortel settlements exceeds the previous record for a foreign

issuer, Daimler-Chrysler, by a factor of more than three.

nera.com 5

Seven of the ten largest

securities class action

settlements have occurred

in 2005 and 2006.

Driven by Mega-Settlements, Average Settlement

Values Hit Post-PSLRA High

In 2006, average settlements rose 37% relative to 2005,

even excluding the partial Enron settlement and other

complete settlements over $1 billion (AOL Time Warner,

Royal Ahold NV, and Nortel Networks). Through

December 15, the average settlement, excluding the

settlements mentioned above, is approximately $34

million. If we include the settlements over $1 billion, the

average rises to $86.7 million. This average is even higher

than the 2005 average of $73.6 million, which included

the record-breaking WorldCom settlement. Note that

these averages do not include the Enron settlement

because not all parties in that litigation have settled.

6 nera.com

This sharp spike in average settlement values is driven by a shift in the distribution pattern of settlements: in 2006,

10% of settlements were “mega-settlements” of over $100 million. This is a marked difference from prior years,

when an average of only 3% of settlements crossed the $100 million threshold. Almost all of the increase in average

settlement values is associated with these very large settlements.

Mega-Settlements By Year (%)

10%

8

6

4

2

1991

1.1%

1992

1.7%

1993

0.0%

1994

1.5% 1.5%

1995

2.1%

1996 1997

0.0%

1999

2.0%

2000

2.8%

2001

2.3%

2002

4.1%

2003

5.2%

2004

3.4%

2005

6.4%

2006

10.0%

1998

1.8%

Average Settlement Value ($MM)

$35

30

25

20

15

10

5

Average: $11.5 MM Average: $24.3 MM

1996

$9

1997

$9

1998

$11

1999

$11

2001

$14

2000

$16

2002

$24

2005

$25

2004

$20

2006

$34

2003

$22

Note: The average settlement values exclude the 2000 Cendant, 2005 Worldcom, and the 2006 Royal

Ahold, AOL Time Warner, and two Nortel Networks settlements.

Note: We defi ne mega-settlements to be those exceeding $100 million.

nera.com 7

Median Settlement Value ($MM)

$8

7

6

5

4

3

2

1

Median: $4.7 MM Median: $6.2 MM

1996

$3.9

1997

$4.4

1998

$5.4

1999

$4.4

2001

$5.0

2000

$5.0

2002

$6.0

2005

$7.0

2004

$5.2

2006

$7.3

2003

$5.6

Median Settlements Continued to Rise in 2006

While average settlements tend to be dominated by the

very largest settlements, the median is more descriptive of

typical cases. Median settlements continued to rise in 2006,

hitting a new peak of $7.3 million.

Again, these median statistics are driven by the distribution

of settlement values. Settlements under $3 million remained

historically low, with 22% of 2006 settlements less than

or equal to $3 million compared to 44% of settlements in

1996. The 2006 results are similar to 2005, when 26% of

settlements resolved for less than $3 million.

Despite these higher averages, however, we fi nd no

statistically signifi cant change in settlement values since the

passage of SOX once we control for other factors, including

investor losses. Higher investor losses for more recently

resolved cases explain the rise in settlements, as we will

discuss further below.

Explaining Settlements

NERA has estimated a settlement prediction model that

explains over 60% of the variation in settlements, using

data on more than 600 settled cases fi led after January 1,

1996.12 This section discusses the sensitivity of settlement

values to various lawsuit characteristics; the sensitivity

measures described are calculated controlling for other

characteristics of the suit and remove the effect of overall

price infl ation.

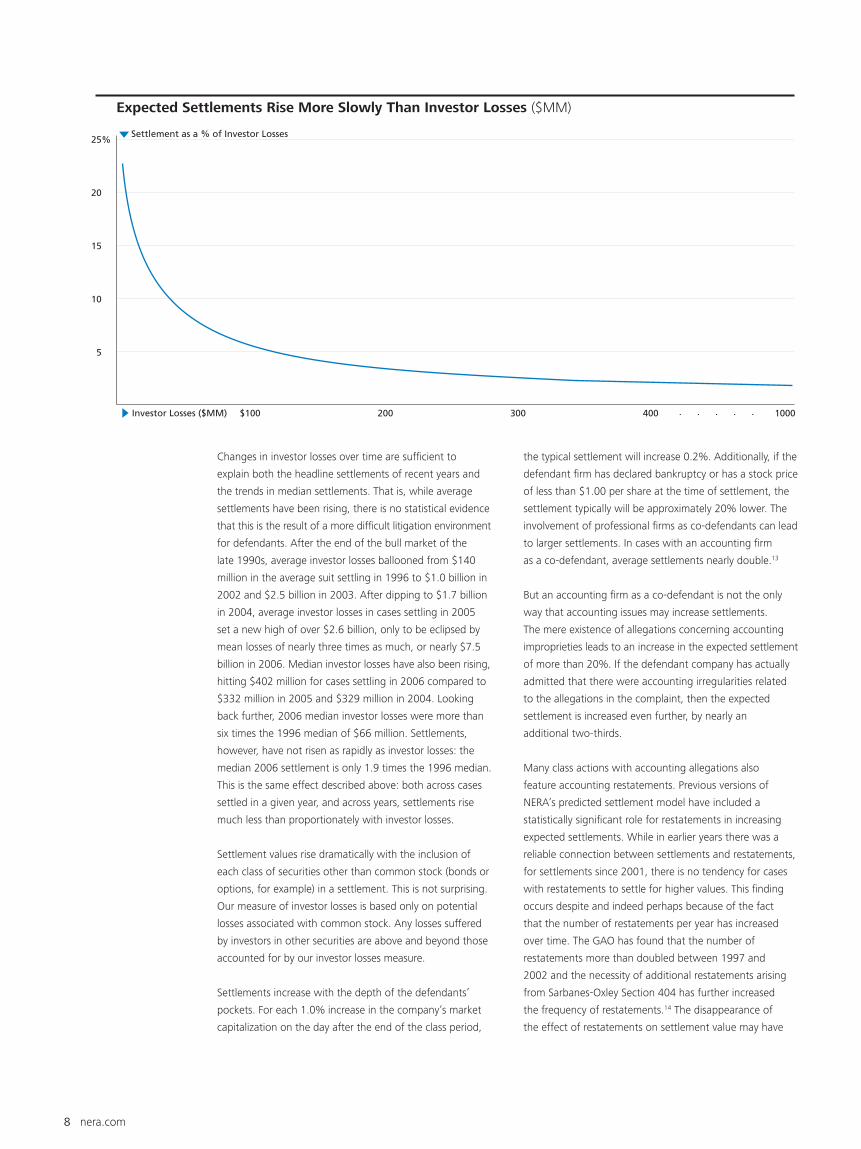

Investor losses constitute the single most powerful

publicly available determinant of settlements, explaining

approximately 50% of their variation. Settlements increase

far less than one-to-one with investor losses. A 1.0%

increase in investor losses results in a 0.4% increase in

the size of the expected settlement.

8 nera.com

Changes in investor losses over time are suffi cient to

explain both the headline settlements of recent years and

the trends in median settlements. That is, while average

settlements have been rising, there is no statistical evidence

that this is the result of a more diffi cult litigation environment

for defendants. After the end of the bull market of the

late 1990s, average investor losses ballooned from $140

million in the average suit settling in 1996 to $1.0 billion in

2002 and $2.5 billion in 2003. After dipping to $1.7 billion

in 2004, average investor losses in cases settling in 2005

set a new high of over $2.6 billion, only to be eclipsed by

mean losses of nearly three times as much, or nearly $7.5

billion in 2006. Median investor losses have also been rising,

hitting $402 million for cases settling in 2006 compared to

$332 million in 2005 and $329 million in 2004. Looking

back further, 2006 median investor losses were more than

six times the 1996 median of $66 million. Settlements,

however, have not risen as rapidly as investor losses: the

median 2006 settlement is only 1.9 times the 1996 median.

This is the same effect described above: both across cases

settled in a given year, and across years, settlements rise

much less than proportionately with investor losses.

Settlement values rise dramatically with the inclusion of

each class of securities other than common stock (bonds or

options, for example) in a settlement. This is not surprising.

Our measure of investor losses is based only on potential

losses associated with common stock. Any losses suffered

by investors in other securities are above and beyond those

accounted for by our investor losses measure.

Settlements increase with the depth of the defendants’

pockets. For each 1.0% increase in the company’s market

capitalization on the day after the end of the class period,

Expected Settlements Rise More Slowly Than Investor Losses ($MM)

25%

20%

15%

10%

5%

$100Investor Losses ($MM) 200 300 400 1000

Settlement as a % of Investor Losses

. . . . .

the typical settlement will increase 0.2%. Additionally, if the

defendant fi rm has declared bankruptcy or has a stock price

of less than $1.00 per share at the time of settlement, the

settlement typically will be approximately 20% lower. The

involvement of professional fi rms as co-defendants can lead

to larger settlements. In cases with an accounting fi rm

as a co-defendant, average settlements nearly double.13

But an accounting fi rm as a co-defendant is not the only

way that accounting issues may increase settlements.

The mere existence of allegations concerning accounting

improprieties leads to an increase in the expected settlement

of more than 20%. If the defendant company has actually

admitted that there were accounting irregularities related

to the allegations in the complaint, then the expected

settlement is increased even further, by nearly an

additional two-thirds.

Many class actions with accounting allegations also

feature accounting restatements. Previous versions of

NERA’s predicted settlement model have included a

statistically signifi cant role for restatements in increasing

expected settlements. While in earlier years there was a

reliable connection between settlements and restatements,

for settlements since 2001, there is no tendency for cases

with restatements to settle for higher values. This fi nding

occurs despite and indeed perhaps because of the fact

that the number of restatements per year has increased

over time. The GAO has found that the number of

restatements more than doubled between 1997 and

2002 and the necessity of additional restatements arising

from Sarbanes-Oxley Section 404 has further increased

the frequency of restatements.14 The disappearance of

the effect of restatements on settlement value may have

nera.com 9

Investor Losses Have Risen More Rapidly Than Settlements, But May Be Stabilizing

$450

400

350

300

250

200

150

100

50

1991

$54

1992

$96

1993

$62

1994

$63

1995

$85

1996

$66

1997

$93

1998

$119

1999

$108

2000

$158

2001 2003

Median Investor Losses ($MM)

2002

$302

2005

$332

2004

$329

2006

$402

Median Ratio of Settlement to Investor Losses (%)

8%

7

6

5

4

3

2

1

5.2%

4.8%

5.9%

5.8%6.1%

7.2%

5.6%

4.9%

4.8%

4.0%

3.4%

2.9%2.7%

2.8%

2.4%2.2%

$176

$215

occurred simply because restatements have become too

common to make their presence a factor that affects

settlement values.15

It is diffi cult to quantify the merits of the allegations in a

particular case. The strength of the merits is, of course,

normally a major point of contention between defense

counsel and plaintiffs’ counsel, underscoring the diffi culty

of objective measurement. As described above, admissions

of accounting irregularities are taken into account in our

model as one indicator of the merits of a case. We have

also found that cases with any kind of offi cial investigation,

consent decree, or penalty settle for, on average,

approximately 20% more than cases without any offi cial

action. This includes any announced investigation by any

offi cial body (SEC, the New York Attorney General’s Offi ce,

etc.) relevant to the allegations in the complaint. Although

many investigations result in no fi nding of fault, this broad

measure of offi cial action has greater predictive power for

settlement values than measures based on some actual

fi nding of fault.

One of Congress’s major goals for the PSLRA was to involve

institutional investors as lead plaintiffs, with the intention

that institutional investor plaintiffs play a more active role

in litigation and generate better outcomes for plaintiffs.

Cases with an institutional investor acting as lead plaintiff

settle for approximately one-third more on average. It is

impossible to judge whether this correlation refl ects the

actions of the lead plaintiff, or the nature of the cases in

which institutions choose to be lead plaintiffs. It could

be that institutional lead plaintiffs retain more effective

counsel, supervise counsel more effectively, or provide

an independent contribution to the plaintiffs’ strategy.

Alternatively, it could be that institutional investors choose

to become involved in cases where the allegations have

greater merit or the defendants’ capacity to pay is greater.

This would only be true to the extent that the merit or

capacity to pay is not fully captured by other variables in

the statistical model.

Settlements increase by an average of approximately

one-third if an IPO is involved. Such cases involve potential

Section 11 claims, which have a lower burden of proof for

plaintiffs than the accompanying 10b-5 claims.

10 nera.com

Changes in investor losses

over time are suffi cient to

explain both the headline

settlements of recent years

and the trends in median

settlements. That is, while

average settlements have

been rising, there is no

statistical evidence that

this is the result of a more

diffi cult litigation environment

for defendants.

nera.com 11

8 Because it is not uncommon for judges to take up to two years

from the fi ling date to rule on motions to dismiss, it would be

premature to evaluate dismissal rates of cases fi led in 2005-2006.

The increase in dismissals is statistically signifi cant.

9 Including the $374 million Cendant PRIDES settlements.

10 We use investor losses as a proxy for the damages estimates

presented by plaintiffs’ side prior to settlement because we

generally do not have access to plaintiffs’ fi gures.

11 This is not to suggest that these settlements are necessarily fair

or reasonable. Our measure of investor losses does not take

into account any of the merits of the case.

12 Technically, the model explains over 60% of the variation of the

logarithm of settlement values. The current version of the predicted

settlement model contains cases settled through June 15, 2006.

13 Settlement values throughout this report are taken to be the total

settlement from all defendants.

14 GAO 03-138, Financial Statement Restatements: Trends, Market

Impacts, Regulatory Responses, and Remaining Challenges,

October 2002.

15 As with all of the other estimates described in this section, the

measured effect is conditional on other features of the case.

Thus, the correct interpretation of the fi nding of no effect from

restatements is that given other features of the case, including

the presence of accounting allegations, irregularities, or

accounting co-defendants, there is no additional role for

restatements in explaining settlements.

1 This edition of NERA’s research on recent trends in securities class

action litigation expands on previous work by our colleagues Lucy

Allen, Elaine Buckberg, Frederick C. Dunbar, Vinita M. Juneja,

Denise Neumann Martin, and David I. Tabak. We gratefully

acknowledge their contributions to previous editions as well as

this current version. In addition, the authors thank Brian Saxton

for coordinating the research effort and Inna Bruter, Dean Chang,

Rachel Herbold, Stacey-Ann Johnson, Janeen McIntosh, Plamen

Petkov, Sheena Siu, Steven Towler, and Ivelina Velikova for further

assistance. These individuals receive credit only for improving this

paper; all errors and omissions are ours.

2 The four 2006 settlements were AOL Time Warner, Royal Ahold,

and the two Nortel Networks settlements. In the table of top

settlements, Enron is dated as 2006 because litigation continues,

but there have been no important new settlements related to Enron

in 2006. Unless otherwise noted, data on settlements and fi lings in

this report are as of December 15, 2006.

3 The post-PSLRA average is calculated for the period from 1998

to 2005, and therefore excludes 1996 and 1997. A large drop

in federal fi lings occurred in those year as plaintiffs fi led in state

courts to avoid the restrictions of PSLRA, making them atypical.

Standard fi lings for the period 1998 to 2005 are defi ned to

exclude laddering, analyst, and mutual fund market timing cases.

4 Ronald I. Miller, Todd Foster, and Elaine Buckberg, Recent Trends in

Shareholder Class Action Litigation: Beyond the Mega-Settlements, is

Stabilization Ahead?, NERA Economic Consulting, April 2006.

5 Excepting the DC circuit, which saw its typical level of just two

fi lings this year.

6 The probability of not facing a suit is 98.4% per year. Assuming

that the probability of facing a suit in each year is independent and

compounding over fi ve years yields a 92.1% chance of no suit, or

a 7.9% chance of at least one suit, in fi ve years. The 2004-2006

fi ling rate is based on the number of fi lings projected for all of 2006.

7 Our dismissal statistics include summary judgments but exclude

partial dismissals.

End Notes

We have investigated whether defendants in different

industries end up paying signifi cantly different settlements.

Only in the health services sector do defendants pay

markedly different settlements, typically one-third higher

than in other industries. This fi nding may relate to the

existence of concurrent billing fraud allegations against

health services companies brought under the federal

False Claims Act.

Conclusion

In 2006, two divergent trends observed in 2005 have

continued. The sharp decline in federal fi lings, which began

in mid-2005 and was particularly apparent in the Ninth

Circuit, has persisted and accelerated in 2006, spreading

to all of the other circuits. The relatively smaller decline in

the Second Circuit suggests that the overall decline is

not the result of the passage of SOX and an associated

benefi cial effect on corporate governance, however.

Until the root causes can be understood, the durability

of this decline remains in doubt.

The era of mega-settlements ushered in by WorldCom

and the Enron partial settlement in 2005 has also

continued into 2006, with the AOL Time Warner, Royal

Ahold, and Nortel settlements leading the way. These

mega-settlements have increased as a proportion of all

settled cases, driving up average settlement values. It

seems likely that such large settlements will continue for

at least the near future, as cases with enormous investor

losses continue to work through the court system.

12 nera.com

About NERA

NERA Economic Consulting is an international fi rm of economists who understand how

markets work. We provide economic analysis and advice to corporations, governments, law

fi rms, regulatory agencies, trade associations, and international agencies. Our global team

of more than 600 professionals operates in over 20 offi ces across North and South America,

Europe, Asia, and Australia.

NERA provides practical economic advice related to highly complex business and legal issues

arising from competition, regulation, public policy, strategy, fi nance, and litigation. Our

more than 45 years of experience creating strategies, studies, reports, expert testimony, and

policy recommendations refl ects our specialization in industrial and fi nancial economics.

Because of our commitment to deliver unbiased fi ndings, we are widely recognized for our

independence. Our clients come to us expecting integrity and the unvarnished truth.

NERA Economic Consulting (www.nera.com), founded in 1961 as National Economic

Research Associates, is a unit of Mercer Specialty Consulting, an MMC company.

Contact Information

Todd Foster

Vice President

NERA Economic Consulting

Two Logan Square

Suite 800

Philadelphia, PA 19103

Tel: +1 215 864 3876

Fax: +1 215 864 3840

Dr. Ronald I. Miller

Senior Consultant

NERA Economic Consulting

1166 Avenue of the Americas

34th Floor

New York, NY 10036

Tel: +1 212 345 3141

Fax: +1 212 345 4650

Dr. Stephanie Plancich

Senior Consultant

NERA Economic Consulting

1166 Avenue of the Americas

34th Floor

New York, NY 10036

Tel: +1 212 345 7719

Fax: +1 212 345 4650

Visit www.nera.com to learn

more about our practice areas

and global offi ces.

© Copyright 2007

National Economic Research

Associates, Inc.

All rights reserved.

Printed in the USA.

SEC1288-G03