45

Market outlook: From red to amber January 2016 www.ashmoregroup.com

Market outlook: From red to amber

January 2016

www.ashmoregroup.com

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

This confidential document is issued by Ashmore. The term “Ashmore” used in this document refers to Ashmore Group plc and its subsidiaries and associated entities, including Ashmore Investment Management Limited, which is authorised and

regulated by the Financial Conduct Authority and Ashmore Investment Advisors Limited, which is also authorised and regulated by the Financial Conduct Authority. Any information on or reference to “Unregulated Collective Investment Schemes”

in this document are only suitable for use with Eligible Counterparties, Professional Clients or investors meeting the FCA’s COBS 4.12 categories as the promotion of these Schemes either within the UK or from the UK is severely restricted by

statute. Shares in any Unregulated Collective Investment Scheme are not available for sale in any jurisdiction in which such a sale would be prohibited and may only be purchased by persons with professional experience of participating in

unregulated schemes, and who understand the high degree and variety of risk involved in Emerging Market investment. The information and any opinions contained in this document have been compiled in good faith, but no representation or

warranty, express or implied, is made as to their accuracy, completeness or correctness. Except where otherwise indicated, the information in this document is based on matters as they are believed to exist as of the date this document was

prepared and not as of any future date, and will not be updated or otherwise revised to reflect information that subsequently becomes available or changes occurring after such date. Save to the extent (if any) that exclusion of liability is prohibited

by any applicable law or regulation, Ashmore, its officers, employees, representatives and agents expressly advise that they shall not be liable in any respect whatsoever for any loss or damage, whether direct, indirect, consequential or otherwise

however arising (whether in negligence or otherwise) out of or in connection with the contents of or any omissions from this document. This document does not constitute an offer to sell, purchase, subscribe for or otherwise invest in units or shares

of any Fund referred to in this document. The value of any investment in any such Fund may fall as well as rise and investors may not get back the amount originally invested. Past performance is not a reliable indicator of future results. All

prospective investors must obtain a copy of the final Scheme Particulars or (if applicable) other offering document relating to the relevant Fund prior to making any decision to invest in any such Fund. This document does not constitute and may

not be relied upon as constituting any form of investment advice and prospective investors are advised to ensure that they obtain appropriate independent professional advice before making any investment in any such Fund. The distribution of this

document in certain jurisdictions is likely to be restricted by law, and persons into whose possession this document comes should inform themselves about, and observe, any such restrictions.

Ashmore offices

2

Ashmore Head Office

61 Aldwych London WC2B 4AE U.K.

T: (44) 20 3077 6000

Ashmore China

Room 3401, Tower 1, China World Trade Centre Office

No.1 Jian Wai Da Jie, Chaoyang District, Beijing, China

T: +86 10 5764 2601

Ashmore-CCSC

Unit 1708, Level 17, Citigroup Tower, No. 33

Huayuanshiqiao Road, Pudong New District, Shanghai,

China, 200120

Ashmore Colombia

Calle 73 # 7 - 06 Piso 8

Bogotá, Colombia

T: +57 1 347 0649

Ashmore India

1103 One Indiabulls Centre, Tower 2A

Jupiter Mills Compound, S.B. Marg, Elphinstone Road

(W), 400 013, Mumbai, India

T: +91 22 6608 0000

Ashmore Indonesia

18 Parc SCBD, Tower E, 8th Floor,

Jl.Jenderal Sudirman Kav. 52-53, Jakarta, Indonesia

12190

T: + 62 21 2953 9000

Ashmore Japan

11F Shin-Marunouchi Building

1-5-1 Marunouchi, Chiyoda-ku, Tokyo, Japan 100-6511

T: +81 0 3 6860 3777

Ashmore Investment Saudi Arabia

3rd Floor, Tower B, Olaya Towers,

Olaya Main Street, Riyadh, Kingdom of Saudi Arabia

T: + 966 11 483 9100

Ashmore Singapore

1 George Street #15-04

Singapore 049145

T: +65 6580 8288

Ashmore Turkey

Comert Sk. Yapı Kredi Plaza C Blok Kat:11

Levent, 34330 Istanbul

T: +90 212 349 40 01

Ashmore USA

Ashmore USA New York

122 East 42nd Street, 50th Floor

New York, NY 10168, USA

T: +1 212 661 0061

Ashmore USA Washington D.C.

1001 19th Street North, 15th Floor

Arlington, VA 22209 USA

T: +1 (703) 243-8800

www.ashmoregroup.com

EM Outlook: From red to amber

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

• The Bid for Developed Markets is losing steam – easy money will continue, but the strong USD is

beginning to hurt the US economy and bond yields are getting too low in Europe

• More Balanced Outlook – after a protracted period of underperformance the outlook for Emerging

Market (EM) assets is now more balanced versus developed markets

• Fed hikes are a positive for EM – resumption of normal monetary policy reduces uncertainty and

hikes are priced into EM asset prices

• Better Value – EM assets offer good value, backed by strong technicals and no bubble risks,

especially compared to QE markets in developed countries

• EM credits stay healthy – cautious market sentiment has forced EM policy makers to respond to

stresses and external balances are now improving

• Domestic factors matter more – quality of policy matters more than external shocks for most EM

countries, so focus on credit differentiation

• Normalisation via inflation and currency debasement - normalisation of global monetary policy is

likely to involve inflation and currency realignment sooner than meaningfully higher real interest rates

• The return of inflation is key – inflation has been missing in the ‘QE economies’, but preparing for its

return is prudent

• China emerges – the reform drive is ambitious and other larger EM countries will eventually emulate

China’s effort to open its markets and seek global reserve currency status

• Rising geopolitical tensions – policy is becoming increasingly populist in developed economies as

short-term stimulus becomes less effective – watch out for policies punishing foreigners and future

generations

Source: Ashmore

EM Outlook: From red to amber

4

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore. JP Morgan, BAML

EM twelve months ahead

5

EM Bull Market Normal Markets UST Shock

Description of scenario Spread compression, 5% EM FX rally

and local bond yields fall to 5.5%

Zero spread compression, FX flat and

no change in yields

100bps USD shocks, spread

widening, -5% EM FX and local bond

yields go to 7%

Sovereign External Debt 10.9% 4.8% -7.6%

Investment Grade 8.8% 3.6% -4.9%

Corporate External Debt 10.5% 6.1% -4.5%

High Yield 16.0% 7.7% -9.8%

High Grade 6.7% 3.1% -4.3%

Local Currency

Government Debt 17.0% 6.3% 2.6%

Local Currency Corporate

Debt 19.9% 8.1% -2.6%

FX forwards 9.2% 4.6% 0.1%

Market scenarios

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore

Assumptions for twelve months ahead scenarios

6

EM Bull Market Normal Markets UST Shock

Sovereign

External Debt

UST go to forwards;

50% UST pass-through;

100bps spread compression;

IG 75bps spread compression

UST go to forwards;

50% UST pass-through;

zero spread compression

UST go to forwards +100 bps;

50% UST pass-through;

150bps spread widening;

IG 75bps spread widening

Corporate

External Debt

UST go to forwards;

Broad: 45% of UST move pass-through,

100bps spread compression;

HY: 20% UST pass-through, 200bps spread

compression;

HG: 56% UST pass-through, 75bps spread

compression

UST go to forwards;

Broad: 45% UST pass-through;

HY: 20% UST pass-through, zero

spread compression;

HG: 56% UST pass-through, zero

spread compression

UST go to forwards;

Broad: 45% UST pass-through,

200bps spread widening;

HY: 20% UST pass-through, 400bps

spread widening;

HG: 56% UST pass-through, 100bps

spread widening

Local Currency

UST go to forwards;

30% UST pass-through;

100bps LC corporate spread narrowing;

Government yield to 5.5%;

FX rallies 5%;

FX implied yield to 3.5%

UST go to forwards;

30% UST pass-through;

LC corporate spread unchanged;

Government yield unchanged;

FX flat;

FX implied yield unchanged

UST go to forwards;

30% UST pass-through;

+200bps LC corporate spread;

Government yield goes to 7%;

FX down 5%;

FX implied yield to 6%

Market scenarios

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore.

The Kilimanjaro trades

7

EM FX under QE policies in developed economies

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

China Roadmap

8

Vision: Transition from export-led to

consumption-led growth

Build political support

Encourage consumption

Adjust growth model to

deleveraging and QE in

developed economies

and diminishing labour

supply in China

Persuade domestic vested

interest groups to change

Facilitate

transmission

of monetary

policy

Consumption has major upside potential due to

49% savings rate; social safety nets, better

savings options

‘Biggest

bang’ in

history to

finance

Reduce turbulence

through foreign central

bank and institutional

participation

To facilitate

greater domestic

demand without

inflation

Supply-side

reforms to

improve

competitiveness

Liberate capital

account

Internationalise

RMB and

expand RQFII

Medium term RMB

appreciation and global

infrastructure investment

Raise

productivity

Reform markets,

SOEs, the

judiciary &

innovate

Slower growth in short term,

sustained long term growth

potential

Liberate interest

rates & develop

yield curves

Reform pensions,

mutual funds and

banks

Supportive for

government bonds,

‘price discovery’ for

muni/corporate bonds

Develop domestic

institutional

investor base

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Yields: Various EM Fixed Income markets and US Treasuries

9

EM under QE: Benign neglect

Source: Ashmore, JP Morgan, Bloomberg. Data as at 17-Nov-15.

0

1

2

3

4

5

6

7

8

9

Lo

ca

lbo

nds

Exte

rnal

de

bt (I

G)

Exte

rnal

de

bt (H

Y)

Co

rpora

tede

bt (I

G)

Co

rpora

tede

bt (H

Y)

10

year

US

T

5 y

ear

US

T

%

Yield today (%)

Yield end-2006 (%)

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

• The vast majority of EM countries are well managed, stable, growing and largely self-funded in

local markets

• About 5-10% of EM countries get into trouble every year – most recover by reforming and

adjusting

• Domestic issues – especially quality of governance - matter more than external shocks

Stylised facts (there are always exceptions though!)

• Riskier EM credits

• Low quality governance

• Single commodity countries

• Cold War casualties

• Internally divided countries

• Countries with weak domestic investor base

• Less risky EM credits

• High quality governance

• Diverse, flexible economies

• Countries that can reform and invest in infrastructure

• Countries that have open markets and local savings institutions

Source: Ashmore

Domestic factors matter more than external factors

10

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

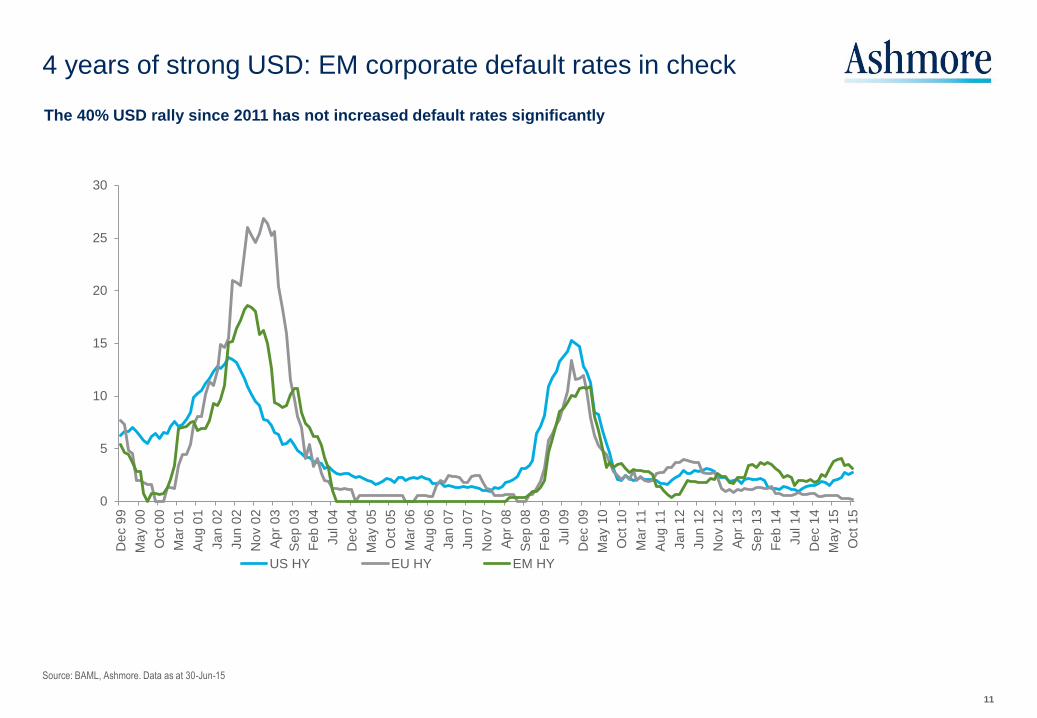

Source: BAML, Ashmore. Data as at 30-Jun-15

The 40% USD rally since 2011 has not increased default rates significantly

4 years of strong USD: EM corporate default rates in check

11

0

5

10

15

20

25

30

De

c 9

9

Ma

y 0

0

Oct 00

Ma

r 01

Aug 0

1

Jan 0

2

Jun 0

2

No

v 0

2

Apr

03

Sep 0

3

Feb

04

Jul 04

De

c 0

4

Ma

y 0

5

Oct 05

Ma

r 06

Aug 0

6

Jan 0

7

Jun 0

7

No

v 0

7

Apr

08

Sep 0

8

Feb

09

Jul 09

De

c 0

9

Ma

y 1

0

Oct 10

Ma

r 11

Aug 1

1

Jan 1

2

Jun 1

2

No

v 1

2

Apr

13

Sep 1

3

Feb

14

Jul 14

De

c 1

4

Ma

y 1

5

Oct 15

US HY EU HY EM HY

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore. Bloomberg, Data as at June 2015

4 years of a strong USD: No signs of inflation pass-through

12

Negative readings means inflation has been lower than expected

-30

-25

-20

-15

-10

-5

0

5

10

Jan 1

0

Ma

r 10

Ma

y 1

0

Jul 10

Sep 1

0

No

v 1

0

Jan 1

1

Ma

r 11

Ma

y 1

1

Jul 11

Sep 1

1

No

v 1

1

Jan 1

2

Ma

r 12

Ma

y 1

2

Jul 12

Sep 1

2

No

v 1

2

Jan 1

3

Ma

r 13

Ma

y 1

3

Jul 13

Sep 1

3

No

v 1

3

Jan 1

4

Ma

r 14

Ma

y 1

4

Jul 14

Sep 1

4

No

v 1

4

Jan 1

5

Ma

r 15

Ma

y 1

5

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

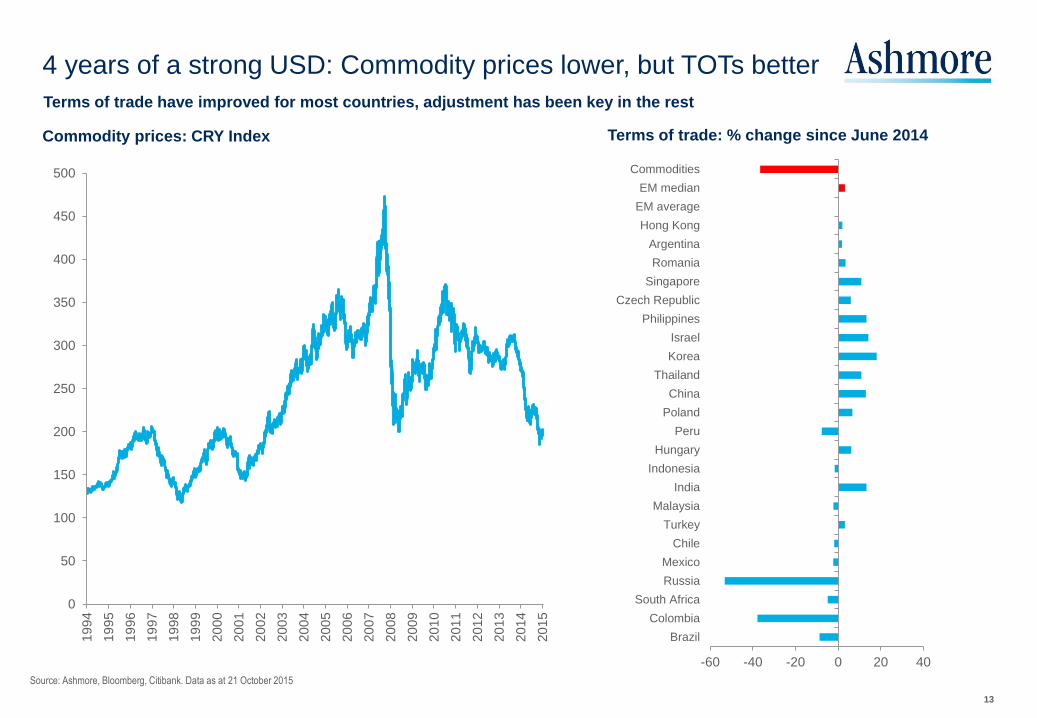

Source: Ashmore, Bloomberg, Citibank. Data as at 21 October 2015

Commodity prices: CRY Index

4 years of a strong USD: Commodity prices lower, but TOTs better

13

Terms of trade: % change since June 2014

Terms of trade have improved for most countries, adjustment has been key in the rest

0

50

100

150

200

250

300

350

400

450

500

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

-60 -40 -20 0 20 40

Brazil

Colombia

South Africa

Russia

Mexico

Chile

Turkey

Malaysia

India

Indonesia

Hungary

Peru

Poland

China

Thailand

Korea

Israel

Philippines

Czech Republic

Singapore

Romania

Argentina

Hong Kong

EM average

EM median

Commodities

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source:: Ashmore, Bloomberg

14

4 years of a strong USD: EM capital flows manageable

Changes in FX reserves for 54 EM countries 2001-March 2015

Current account changes and FX valuation effects dominate capital outflows

-20%

-10%

0%

10%

20%

30%

40%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 toMarch

FX valuation changes

Current account

Capital Flow

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

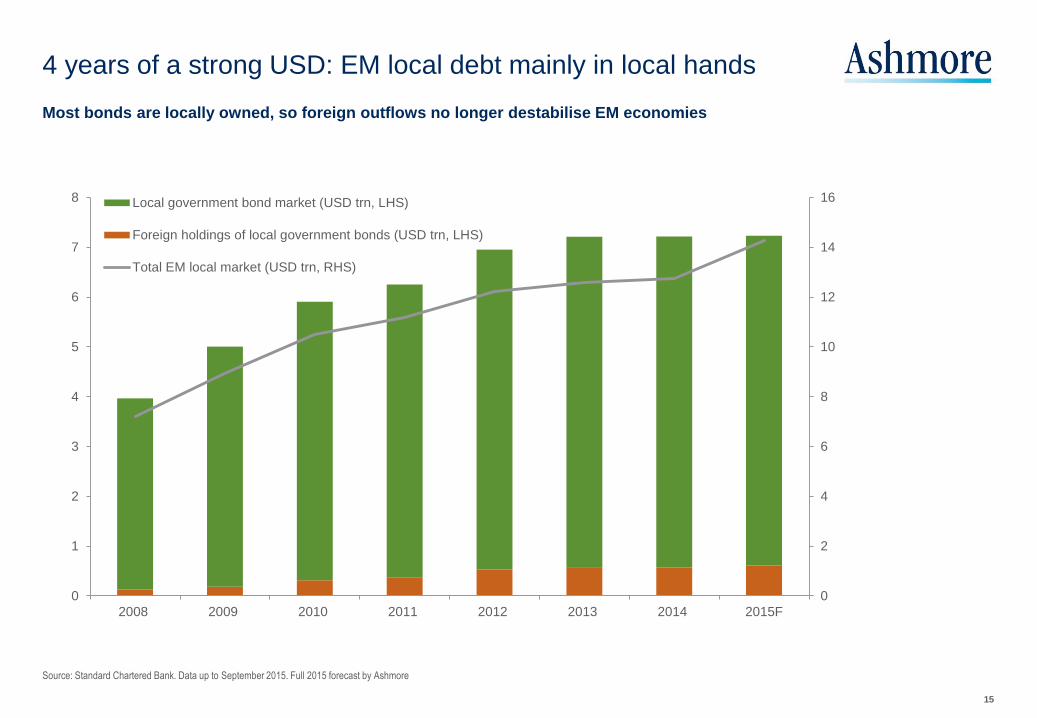

Source: Standard Chartered Bank. Data up to September 2015. Full 2015 forecast by Ashmore

Most bonds are locally owned, so foreign outflows no longer destabilise EM economies

4 years of a strong USD: EM local debt mainly in local hands

15

0

2

4

6

8

10

12

14

16

0

1

2

3

4

5

6

7

8

2008 2009 2010 2011 2012 2013 2014 2015F

Local government bond market (USD trn, LHS)

Foreign holdings of local government bonds (USD trn, LHS)

Total EM local market (USD trn, RHS)

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, Bloomberg. Data as at 20-Oct-15

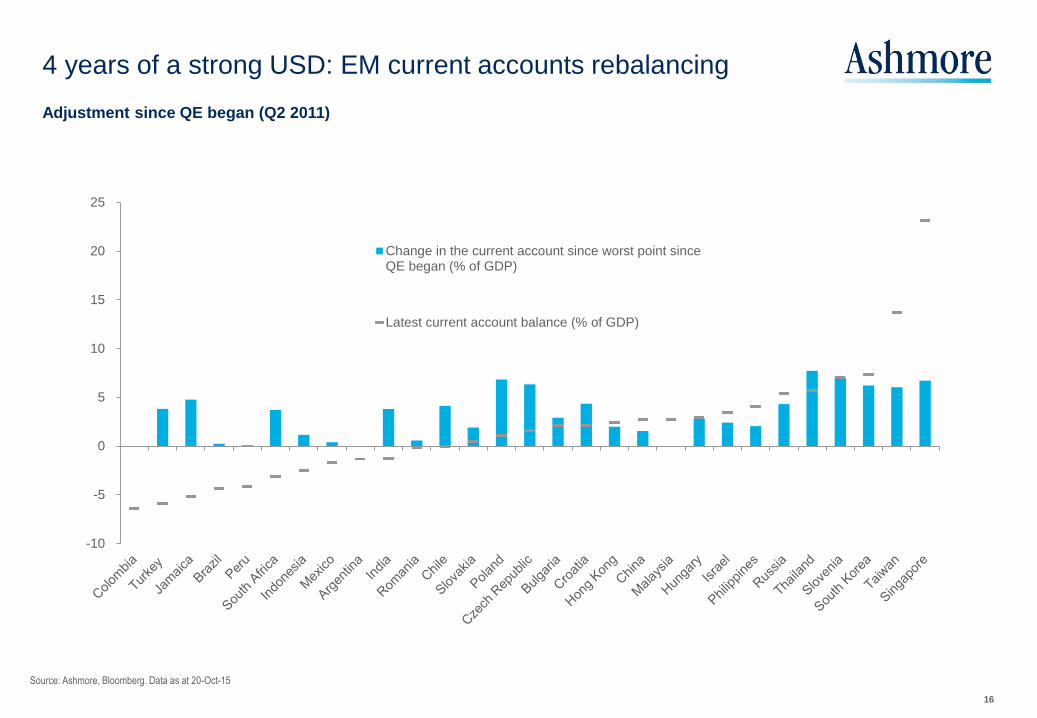

4 years of a strong USD: EM current accounts rebalancing

16

Adjustment since QE began (Q2 2011)

-10

-5

0

5

10

15

20

25

Change in the current account since worst point sinceQE began (% of GDP)

Latest current account balance (% of GDP)

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, BIS, Bloomberg. Data as at 22 October 2015

4 years of a strong USD: REERs restoring competitiveness

17

Real Effective Exchange Rates in EM and DM since QE began

-50

-40

-30

-20

-10

0

10

20

30

40

Bra

zil

Co

lom

bia

South

Afr

ica

Ru

ssia

Hu

nga

ry

Czech R

epu

blic

Me

xic

o

India

Ch

ile

Indon

esia

Pola

nd

Ro

man

ia

Arg

entina

Bulg

aria

Cro

atia

Ma

laysia

Turk

ey

Slo

ven

ia

Lithu

ania

Slo

vakia

La

tvia

Esto

nia

Isra

el

Alg

eria

Taiw

an

Tha

iland

Peru

Sin

gapo

re

Kore

a

Phili

ppin

es

Un

ite

d A

rab E

mira

tes

Saud

i A

rabia

Ho

ng K

on

g

Ch

ina

Japa

n

Austr

alia

Ca

nad

a

Euro

are

a

Fra

nce

Germ

any

Ita

ly

Un

ite

d K

ing

dom

Un

ite

d S

tate

s

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Fed hikes (1): A positive for EM

18

Source: Ashmore, Bloomberg, Data 22-July-15

%

bps

0

200

400

600

800

1,000

1,200

1,400

1,600

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EMBI GD Spread vs. 2yr UST

Fed Fund hiking

2yr UST

EMBI GD Spread

Start of hikes reduce spreads as uncertainty falls and confidence in growth increases

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Fed hikes(2): Impact on various markets

19

2004 hiking cycle: impact on US Treasury curve EM vs DM: Cumulative returns since start of the

rate sell-off on April 1st 2004

0

1

2

3

4

5

6

7

05/2003 05/2004 05/2005 05/2006

Fed Funds UST 2YR UST 5YR UST 10YR UST 30YR

-10% 0% 10% 20%

DM government bonds

USD high grade

EUR corporate IG

USD corporate IG

US high yield

EM Corp high yield

EM GB hard currency

EM GB local currency

3 month return (before hike)

6 month return (3 months pre and 3 months post hike)

12 month return(3 months pre and 9 months post hike)Source: Ashmore, Bloomberg, May-15.

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: IMF Data as at Oct. 2015

GDP per capita (Index rebased, 1980 = 100)

The Case for EM: Better growth

20

Adjustment

Convergence

0

100

200

300

400

500

600

700

800

900

1000

Developed countries

Emerging Market and developing economies

Cold War

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, IMF WEO October 2015

Real GDP growth rates by epoch EM vs DM

The Case for EM: No middle income trap

21

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

EM * DM *

1980-1989 1990-1999 2000-2009 2010-2015 2016-2020 (IMF forecast) Average (1980-2019)

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, IMF WEO October 2015 (2015 estimate, 2016 onwards forecasts)

% global GDP (based on purchasing power parity)

The Case for EM: 57% of Global GDP en route to 61%

22

% of Emerging Markets

(2015 based on purchasing power parity)

0

10

20

30

40

50

60

70

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

20

16

20

18

20

20

Advanced economies

Emerging market and developingeconomies

8%

54%

6%

14%

13%

5%

Commonwealth ofIndependent States

Emerging and developingAsia

Emerging and developingEurope

Latin America and theCaribbean

Middle East, North Africa,Afghanistan, and Pakistan

Sub-Saharan Africa

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, BAML, IMF WEO October 2015 (2015 estimate, 2016 onwards forecasts)

EM has less debt and a bigger share of global GDP

The Case for EM: Domestic credit and tradable debt

23

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

0

20

40

60

80

100

120

140

160

180

EM DM

US

D t

rn

Tradable bonds (Left axis) Domestic Credit (Left axis) Share of Global GDP (%, right axis)

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, BAML, IMF

% of GDP in selected EM and DM countries

The Case for EM: Domestic credit and tradable debt

24

0%

100%

200%

300%

400%

500%

600%

700%

Nig

eri

a

Ecua

dor

Arg

en

tina

Eg

yp

t

Trin

idad

& T

ob

ago

Dom

inic

an R

ep

ub

lic

Sa

ud

i A

rab

ia

Ve

ne

zue

la

Uru

gua

y

Rom

an

ia

Indo

nesia

Sri

La

nka

Qa

tar

Ka

za

kh

sta

n

Pa

kis

tan

Pe

ru

Ku

wait

El S

alv

ad

or

Bu

lga

ria

Russia

Ph

ilipp

ines

Slo

va

kia

Tu

nis

ia

Colo

mbia

Unite

d A

rab

Em

ira

tes

Czech

Rep

ublic

India

Me

xic

o

Po

lan

d

Mo

rocco

Ukra

ine

Vie

tna

m

Tu

rke

y

Ba

hra

in

Cro

atia

Costa

Ric

a

Slo

ve

nia

So

uth

Afr

ica

Pa

na

ma

Hun

ga

ry

Lith

uan

ia

Bra

zil

Chile

Chin

a

Sin

ga

pore

Th

aila

nd

Ma

laysia

So

uth

Ko

rea

Leb

an

on

Cypru

s

Hon

g K

on

g

Jam

aic

a

Neth

erl

an

ds

Unite

d K

ing

do

m

Jap

an

US

Sp

ain

Po

rtug

al

Fra

nce

Italy

Ge

rma

ny

Local

External

Credit

Global Backdrop

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

QE led recoveries in developed markets: theory and practice

26

Source Ashmore

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

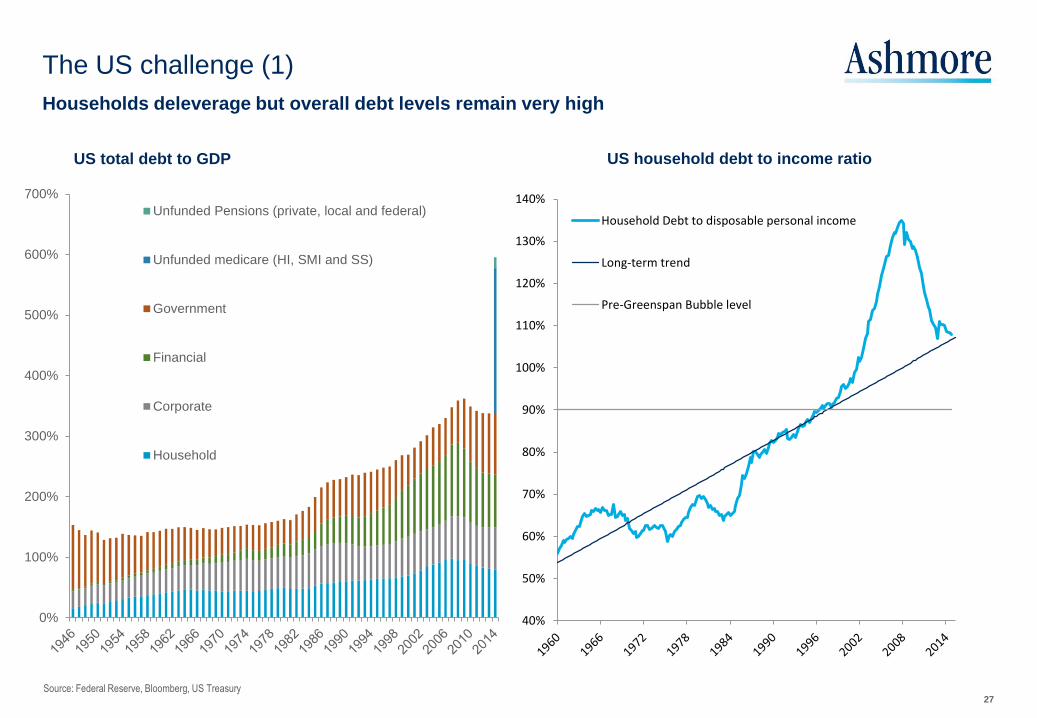

Source: Federal Reserve, Bloomberg, US Treasury

The US challenge (1)

27

Households deleverage but overall debt levels remain very high

40%

50%

60%

70%

80%

90%

100%

110%

120%

130%

140%

Household Debt to disposable personal income

Long-term trend

Pre-Greenspan Bubble level

US total debt to GDP US household debt to income ratio

0%

100%

200%

300%

400%

500%

600%

700%

Unfunded Pensions (private, local and federal)

Unfunded medicare (HI, SMI and SS)

Government

Financial

Corporate

Household

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

American-style ‘Dutch Disease’ points to less directional/more choppy outlook for USD

Source: Ashmore, Bloomberg.

The US challenge (2): Rising REERs and falling productivity

28

US Real Effective Exchange Rate US productivity (% yoy)

-2

-1

0

1

2

3

4

5

6

7

De

c 0

0

Aug 0

1

Apr

02

De

c 0

2

Aug 0

3

Apr

04

De

c 0

4

Aug 0

5

Apr

06

De

c 0

6

Aug 0

7

Apr

08

De

c 0

8

Aug 0

9

Apr

10

De

c 1

0

Aug 1

1

Apr

12

De

c 1

2

Aug 1

3

Apr

14

De

c 1

4

US nonfarm business sector output per person

Linear (US nonfarm business sector output perperson)

95

97

99

101

103

105

107

109

111

113

115

Jan 1

1

Apr

11

Jul 11

Oct 11

Jan 1

2

Apr

12

Jul 12

Oct 12

Jan 1

3

Apr

13

Jul 13

Oct 13

Jan 1

4

Apr

14

Jul 14

Oct 14

Jan 1

5

Apr

15

Jul 15

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

US inflation

29

Source Ashmore, Bloomberg

Power base effects push yoy inflation up sharply in 2016

(yoy projections based on 0.2% mom each month in 2016)

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

Jan 1

1

Mar 1

1

May 1

1

Jul 1

1

Sep 1

1

Nov 1

1

Jan 1

2

Mar 1

2

May 1

2

Jul 1

2

Sep 1

2

Nov 1

2

Jan 1

3

Mar 1

3

May 1

3

Jul 1

3

Sep 1

3

Nov 1

3

Jan 1

4

Mar 1

4

May 1

4

Jul 1

4

Sep 1

4

Nov 1

4

Jan 1

5

Mar 1

5

May 1

5

Jul 1

5

Sep 1

5

Nov 1

5

Jan 1

6

Mar 1

6

May 1

6

Jul 1

6

Sep 1

6

Nov 1

6

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Does debt constrain

growth and rates?

Other structural

challenges to growth?

Can central

bank create inflation?

Is currency a major

reserve currency? Long-term outlook

US

Yes.

Overall debt too high,

but household debt

becoming less onerous

Yes and No.

Banks recapitalised, but

infrastructure and long-

term liabilities still a

problem

Yes.

Financial

intermediation works

and household credit

demand is improving

Yes.

The US can pass the

cost of debt reduction

onto foreigners

Grow, then inflate and devalue

amidst very gentle normalisation of

monetary policy

Europe

Yes.

Households debts and

government debts

excessive

Yes.

Banks and ABS markets

dysfunctional

No.

Financial transmission

mechanism is

dysfunctional

Yes.

But debt mainly held at

home, so ability to

deleverage via FX is

limited

Slow growth, deflation fears and

credit vulnerabilities

Japan Yes.

569% of GDP

Yes.

Demographics, fiscal

position and economic

flexibility

No.

‘Abenomics’ impact is

temporary

No.

Currency devaluation

does not reduce debt

Structural problems return after

short-term stimulus and risks of a

debt crisis re-emerge

EM

No.

Average public debt

about 1/3 of DMs.

Private debt highest in

richer EM countries

Mixed.

Infrastructure is a

general problem, but EM

countries generally

reform

Yes.

But political costs of

inflation tend to be

very high

No.

EM central banks have

almost zero exposure to

EM bonds

Long-term currency appreciation,

slower growth and challenges

transitioning from export-led to

domestic demand-led growth.

Greater credit differentiation

Source: Ashmore.

Global economy: The path back to long-term equilibrium

30

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, October 2015.

The direction of US monetary policy

31

Key developments Approximate time

period

Deleveraging

Improving but sub-par growth and stable low inflation

Now until late-2016 Very gradual normalisation of monetary policy

Long end of yield curve well supported

Strong market bias towards long Dollar positions

Inflation

Inflation begins to emerge as the dominant macroeconomic problem

10 years starting in

late 2016

Debt overhangs, weak trend growth and past QE liquidity constrain Fed tightening

Nominal yields rise, but real yield stay low amidst rising inflation

Dollar commences decade long adjustment lower

Export competitiveness improves

Yield curve bear steepens

Real debt stock declines

‘Volcker II’

The flight against inflation assumes top priority

The period

thereafter

Real rates rise materially without destroying less indebted economy

Recession and rebound

Dollar rallies – still a global reserve currency but now alongside larger EM currencies

Next debt fuelled consumption boom begins

Financial de-regulation

Three phases of monetary policy normalisation

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Federal Reserve , BAML, Bloomberg.

Debt and reserves (USD trn)

Global Imbalances

32

1970’s : Inflation, real rates and the Dollar

70

75

80

85

90

95

100

105

-10

-5

0

5

10

15

20

1967 1969 1971 1972 1974 1976 1977 1979

CPI inflation (LHS, % yoy)

Real 5yr UST yields (LHS, %)

DXY (RHS, 1967 index =100)

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

2003 2005 2007 2009 2011 2013

Reserves in rest of EM (LHS)

Reserves in China (LHS)

Foreign Holdings of UST (LHS)

US total public debt (RHS)

EM Fixed Income: Characteristics

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

• Being an ‘Emerging Market’ says nothing per se about the quality of the investment

- Companies and countries can be managed badly or well regardless of whether they are Emerging Markets or not

• Emerging Markets is not a ‘derivative’ asset class

- Economic and financial performance in EM mainly hinges on domestic factors, not external ones

Emerging Markets are countries that are transcending the stages of economic and financial development that developed

economies have already gone through

Defining Emerging Markets

34

Market characteristics

Emerging Markets Developed Markets

Income per capita Low, growing rapidly High, stable or growing slowly

Capital markets Shallow, developing Sophisticated, mature

Structural change On-going, possibly substantial Minor

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore(forecasts beyond 2014), BAML

EM fixed income (USD trn)

Growing investment universe

35

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

External sovereign

External corporate

Local sovereign

Local corporate

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, JP Morgan , BAML

Risk aversion events are good buying opportunities

36

EMBI GD EMGI GD

IG

EMBI GD

HY CEMBI BD

CEMBI BD

HG

CEMBI BD

HY

GBI EM

GD ELMI+

% outperform

vs.passive 18% 31% 12% 28% 21% 55% 30% 50%

Absolute alpha vs.

passive 2% 2% 1% 2% 1% 5% 2% 3%

12m active return 11% 10% 12% 9% 8% 14% 9% 8%

12m passive return 9% 8% 11% 7% 7% 9% 7% 6%

Month Event Month Event

Apr-94 Fed hikes Aug-07 BNP Paribas gates funds over sub-

prime losses

Oct-97 Asian crisis Sep-08 Lehman

Aug-98 Russian crisis May-10 Greece I

Oct-00 Fear of slowing US economy Mar-11 Japan earthquake

Sep-01 9/11 Aug-11 US debt ceiling and Eurozone crisis

Jul-02 Fear of slowing US economy Oct-14 Rate hike fears

Jun-06 Hike triggers recession fears Aug-15 Fed hike fears

+10 pts VIX spikes – most country specific or developed market events

Passive versus active timing in response to +10 pts VIX spikes: Returns and alpha 1993 to September 2015

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, JP Morgan , BAML.

EM: Poor index representation

37

Asset class Index

name

Index

acronym

Index

provider

No. of

countries

No. of

issuers

No. of

issues

Index market

cap

(USD bn)

Asset class

(USD bn)

Index as %

of asset

class

External

Sovereign Debt

EMBI Global

Diversified EMBI GD JP Morgan 62 125 459 362 793 46%

External

Corporate Debt

CEMBI Broad

Diversified CEMBI BD JP Morgan 49 552 1,166 291 1,284 23%

Local Currency

government Debt

GBI EM Global

Diversified GBI EM GD JP Morgan 16 16 195 941 6,651 14%

Local currency

Corporate Debt

Local EM non-

sovereign LOCL BAML 15 206 412 143 6,113 2%

All EM

Fixed Income 1,737 14,841 12%

As of end 2014

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: JP Morgan.

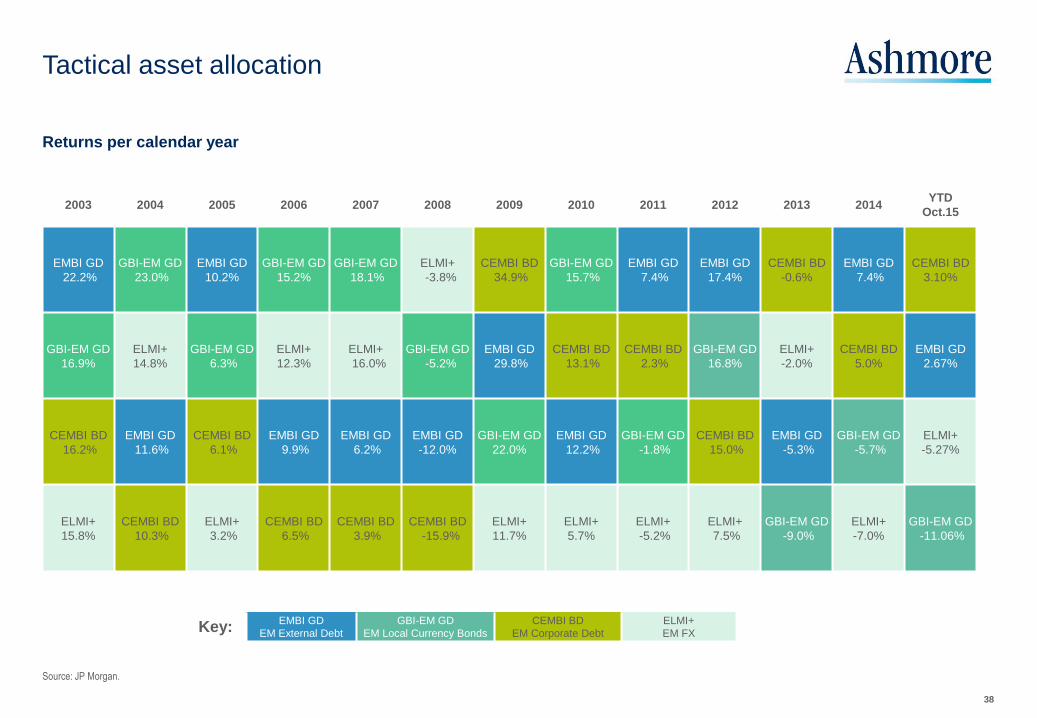

Tactical asset allocation

38

EMBI GD

EM External Debt

GBI-EM GD

EM Local Currency Bonds

CEMBI BD

EM Corporate Debt

ELMI+

EM FX Key:

Returns per calendar year

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 YTD

Oct.15

EMBI GD

22.2%

GBI-EM GD

23.0%

EMBI GD

10.2%

GBI-EM GD

15.2%

GBI-EM GD

18.1%

ELMI+

-3.8%

CEMBI BD

34.9%

GBI-EM GD

15.7%

EMBI GD

7.4%

EMBI GD

17.4%

CEMBI BD

-0.6%

EMBI GD

7.4%

CEMBI BD

3.10%

GBI-EM GD

16.9%

ELMI+

14.8%

GBI-EM GD

6.3%

ELMI+

12.3%

ELMI+

16.0%

GBI-EM GD

-5.2%

EMBI GD

29.8%

CEMBI BD

13.1%

CEMBI BD

2.3%

GBI-EM GD

16.8%

ELMI+

-2.0%

CEMBI BD

5.0%

EMBI GD

2.67%

CEMBI BD

16.2%

EMBI GD

11.6%

CEMBI BD

6.1%

EMBI GD

9.9%

EMBI GD

6.2%

EMBI GD

-12.0%

GBI-EM GD

22.0%

EMBI GD

12.2%

GBI-EM GD

-1.8%

CEMBI BD

15.0%

EMBI GD

-5.3%

GBI-EM GD

-5.7%

ELMI+

-5.27%

ELMI+

15.8%

CEMBI BD

10.3%

ELMI+

3.2%

CEMBI BD

6.5%

CEMBI BD

3.9%

CEMBI BD

-15.9%

ELMI+

11.7%

ELMI+

5.7%

ELMI+

-5.2%

ELMI+

7.5%

GBI-EM GD

-9.0%

ELMI+

-7.0%

GBI-EM GD

-11.06%

Recent Market Developments

39

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: JP Morgan, Ashmore. Data as at 9-Nov-15.

Mapping the EM Fixed Income investment themes

Recent price developments

40

Last 3y Hi 3y Low Last 3y Hi 3y Low

EMBI G.Div 6.6 375 428 237 11 6.12% 6.35% 4.33% 0.22%

IG 7.6 243 295 143 13 4.87% 5.33% 3.37% 0.25%

HY 5.4 596 717 390 -2 8.18% 9.13% 5.82% 0.09%

Cembi B.Div 4.8 383 447 274 25 6.00% 6.26% 4.43% 0.38%

IG 5.2 243 301 193 -2 4.60% 5.24% 3.72% 0.09%

HY 4.1 624 728 439 49 8.41% 9.06% 6.35% 0.64%

GBI EM GD 4.84 6.90% 7.27% 5.16% 0.08%

* Daily data.

** GDI EM GD spreads vs 5yr UST Yields

EM Fixed Income

BenchmarkDuration

Spreads Yields

3m Change 3m Change

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, JP Morgan, Bloomberg. Data as at 28-Sep-15

External Debt Valuation: HY attractive, IG resilient

41

Sovereign spreads (bps over corresponding duration on US Treasury curve)

100

200

300

400

500

600

700

800

EMBI Global Diversified Spread

EMBI GD Spread EMBI GD IG EMBI GD HY

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

• Emerging Markets corporations have historically operated in a different environment, where leverage has been

a result of their operating and investment needs, not a result of LBOs and financial engineering

• Thus, historically their financial leverage (Total Debt/EBITDA) has been significantly lower

• After factoring their wider credit spread, investors can get nearly twice as much compensation per ‘turn of

leverage’ in Emerging Markets high yield debt then in US high yield debt

Source: BAML, as at 31-Dec-14.

Historically lower leverage than their developed markets’

counterparts

42

0

1

2

3

4

5

6

2007 2008 2009 2010 2011 2012 2013 2014

Global EM HY Leverage US HY Leverage

0 50 100 150 200

A

BBB

BB

B

Spread per turn of Leverage (bps/x)

US EM

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Bloomberg, Ashmore. Data as at Jun-15.

Local bonds: GBI-EM vs. 5yr UST: high returns + diversification

43

y = 0.2266x - 0.0022 R² = 0.0404

-0.60

-0.40

-0.20

0.00

0.20

0.40

0.60

-0.50 -0.30 -0.10 0.10 0.30 0.50

GBI EM DailyYield Change

5 Yr UST Yield vs GBI EM Yield (Jan/03 to Jun/15)

-0.8

-0.6

-0.4

-0.2

0

0.2

0.4

0.6

0.8

1

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Jul-0

6

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

Jan

-15

GBI EM vs 5 Yr UST Yield Changes : 3M correlation

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Jan

-03

Jul-0

3

Jan

-04

Jul-0

4

Jan

-05

Jul-0

5

Jan

-06

Jul-0

6

Jan

-07

Jul-0

7

Jan

-08

Jul-0

8

Jan

-09

Jul-0

9

Jan

-10

Jul-1

0

Jan

-11

Jul-1

1

Jan

-12

Jul-1

2

Jan

-13

Jul-1

3

Jan

-14

Jul-1

4

Jan

-15

Yields 5 yr UST

GBI-EM Yield

100

150

200

250

300

350

Jan

03

Jan

04

Jan

05

Jan

06

Jan

07

Jan

08

Jan

09

Jan

10

Jan

11

Jan

12

Jan

13

Jan

14

Jan

15

Total Return

GBI EM

UST 5y index

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore, UBS. Data as at 30-Sep-15.

Local Currency Debt: Real yield at healthy levels with inflation

trending down

44

-2.0

-1.0

-

1.0

2.0

3.0

4.0

5.0

Feb

/03

Jun/0

3

Oct/03

Feb

/04

Jun/0

4

Oct/04

Feb

/05

Jun/0

5

Oct/05

Feb

/06

Jun/0

6

Oct/06

Feb

/07

Jun/0

7

Oct/07

Feb

/08

Jun/0

8

Oct/08

Feb

/09

Jun/0

9

Oct/09

Feb

/10

Jun/1

0

Oct/10

Feb

/11

Jun/1

1

Oct/11

Feb

/12

Jun/1

2

Oct/12

Feb

/13

Jun/1

3

Oct/13

Feb

/14

Jun/1

4

Oct/14

Feb

/15

Jun/1

5

Real GBI Yield GTII5 Govt

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

-60

-40

-20

0

20

40

60

Feb

/03

Jun/0

3

Oct/03

Feb

/04

Jun/0

4

Oct/04

Feb

/05

Jun/0

5

Oct/05

Feb

/06

Jun/0

6

Oct/06

Feb

/07

Jun/0

7

Oct/07

Feb

/08

Jun/0

8

Oct/08

Feb

/09

Jun/0

9

Oct/09

Feb

/10

Jun/1

0

Oct/10

Feb

/11

Jun/1

1

Oct/11

Feb

/12

Jun/1

2

Oct/12

Feb

/13

Jun/1

3

Oct/13

Feb

/14

Jun/1

4

Oct/14

Feb

/15

Jun/1

5

CRY Index YoY (left axis)

GBI-EM GD Weighted CPI

R: 0

G: 41

B: 91

R: 0

G: 174

B: 226

R: 152

G: 152

B: 156

R: 93

G: 92

B: 97

R: 225

G: 160

B: 15

R: 48

G: 144

B: 197

R: 160

G: 1

B: 46

R: 92

G: 146

B: 51

R: 176

G: 194

B: 6

R: 96

G: 187

B: 163

R: 200

G: 98

B: 27

R: 0

G: 127

B: 114

Source: Ashmore. JP Morgan

USD and first Fed funds hike

45

Date Previous 12m DXY Subsequent 6m DXY Subsequent 12m DXY

10/11/15 12.15% TBD TBD

Average previous 4 cycles -5.03% -4.85% --5.62%

30/06/2004 -6.26% -7.86% 0.33%

28/02/1999 1.66% -0.84% 3.88%

28/02/1994 0.56% -4.95% -9.12%

31/12/1986 -16.09% -5.73% -17.56%

Date Previous 12m TWI Subsequent 6m TWI Subsequent 12m TWI

10/11/15 12.31% TBD TBD

Average previous 4 cycles 1.04% -2.63% -1.23%

30/06/2004 -1.32% -4.84% -3.58%

28/02/1999 -0.99% -1.61% 1.23%

28/02/1994 9.60% -0.42% 3.49%

31/12/1986 -4.02% -4.48% -6.06%