4 February 2019 Japan tax newsletter Ernst & Young Tax Co. 2019 Japan tax reform outline On 14 December 2018, the ruling party (a coalition comprised of the Liberal Democratic Party and Komeito) released the 2019 Tax Reform Outline (below “the outline”). This newsletter provides an overview and explanation of the major amendments and revised provisions contained in the outline, which affect such matters as corporate taxation and international taxation. To accomplish the twin goals of the Abe Cabinet, i.e. converting the social security system into a reliable system for all ages which provides comfort to all generations from the young to the elderly and ensuring the nation’s fiscal health, the consumption tax rate will be raised to 10% in October 2019. In order to smooth the fluctuations in demand that are expected to occur prior to and following the rate hike, sufficient support will be provided in terms of both national budget and tax rules. Tax measures to stimulate automobile and home purchases will be implemented. Furthermore, in order to secure a path for continuous growth amidst the aging of Japanese society, the “productivity revolution” and “human resource development revolution” continue to be issues of the highest priority. R&D tax rules will be revised from the perspective of encouraging innovative R&D. Various tax measures to assist small and medium- sized enterprises (SMEs) will be implemented and simultaneously, new tax payment deferment and exemption rules for inheritance tax and gift tax will be established to promote business succession of sole proprietors. Furthermore, transfer pricing taxation rules and earnings stripping rules will also be significantly revised to match the international standards concerning taxation agreed to in the OECD’s BEPS project and other forums. Please note that the contents of this newsletter may be partially revised, deleted or added in response to future Diet deliberations on the reform bill. Contents • Corporate taxation ...........................2 • International taxation .......................8 • Individual income taxation and asset taxation.................................20 • Tax administration/Other ................23 EY Global tax alert library Access both online and pdf versions of all EY Global Tax Alerts. • Copy into your web browser: http://www.ey.com/GL/en/Services/Tax/ International-Tax/Tax-alert-library%23date

Transcript

4 February 2019

Japan tax newsletterErnst & Young Tax Co. 2019 Japan tax

reform outline

On 14 December 2018, the ruling party (a coalition comprised of the Liberal Democratic Party and Komeito) released the 2019 Tax Reform Outline (below “the outline”). This newsletter provides an overview and explanation of the major amendments and revised provisions contained in the outline, which affect such matters as corporate taxation and international taxation.

To accomplish the twin goals of the Abe Cabinet, i.e. converting the social security system into a reliable system for all ages which provides comfort to all generations from the young to the elderly and ensuring the nation’s fiscal health, the consumption tax rate will be raised to 10% in October 2019. In order to smooth the fluctuations in demand that are expected to occur prior to and following the rate hike, sufficient support will be provided in terms of both national budget and tax rules. Tax measures to stimulate automobile and home purchases will be implemented. Furthermore, in order to secure a path for continuous growth amidst the aging of Japanese society, the “productivity revolution” and “human resource development revolution” continue to be issues of the highest priority. R&D tax rules will be revised from the perspective of encouraging innovative R&D. Various tax measures to assist small and medium-sized enterprises (SMEs) will be implemented and simultaneously, new tax payment deferment and exemption rules for inheritance tax and gift tax will be established to promote business succession of sole proprietors. Furthermore, transfer pricing taxation rules and earnings stripping rules will also be significantly revised to match the international standards concerning taxation agreed to in the OECD’s BEPS project and other forums.

Please note that the contents of this newsletter may be partially revised, deleted or added in response to future Diet deliberations on the reform bill.

1. Revision of R&D tax rulesFrom the perspective of promoting active investment in R&D, R&D tax rules (special corporate tax credits available for conducting experimental research, etc.) will be revised as follows.

(A) The maximum credit available to certain startups which conduct R&D (Note 1) will be increased to 40% (from the current 25%) of corporation tax of the applicable fiscal year.

(B) High expense level tax credits will be abolished as a standalone measure but will be extended for 2 years after integrating it into the gross-amount tax credits as an additional measure which further increases the maximum credit enjoyed by entities with a high level of R&D expenses. The maximum credit will be 10% of corporation tax of the applicable fiscal year.

(C) The credit rate curve (calculation formula for tax credit rates) for R&D expenses will be revised.

(D) The applicable period of the special measure designating a maximum credit rate of 14% (c.f. the general rate of 10%) will be extended by 2 years.

A maximum credit of 45%(For startups, a maximum of 60%)

(C)High expense

level tax credits

(A’)Additional

increase of the maximum credit

(A)Gross-amount tax credits

(B) Open innovation tax credits

(A)Gross-amount tax credits

(B) Open innovation tax credits

(A’)Additional increase of the maximum

credit in cases where the ratio of R&D expenses to sales exceeds 10%Temporary measure lasting 2 years

5% of corporation tax

10% of corporation tax

25% of corporation tax

10% of corporation tax

(Elective rules)(Temporary measure)

Increased to 40% for startups

Increased to 10%

Abolishment of high expense level tax credits

Extension of A’

(Prepared based on “Key Points of the FY2019 Tax Reform on Economy and Industry,” published by the Ministry of Economy, Trade and Industry in December 2018 (hereinafter, “METI materials”))

3Japan tax newsletter 4 February 2019 |

(2) Open innovation tax credits (tax credit rules pertaining to special R&D expenses)

Certain research consigned to private-sector companies (including R&D startups (Note 2)) will be added to the list of eligible R&D expenses. The tax credit rate for research consigned to R&D startups and joint research conducted with R&D startups will be 25%, while the tax credit rate for research consigned to private-sector companies will be 20%. In addition, the maximum credit will be increased to 10% (from the current 5%) of corporation tax liability in the applicable fiscal year.

Current rules Credit rateCounterparty is a university or special research institution etc. 30%

Counterparty falls under the category “Other” (private-sector companies etc.)

20%

Research consigned to a large enterprise etc. Not eligible

Post-reformCredit rate

(Current rules → Post-revision)

Joint research with R&D startups 20% → 25%

Research consigned to large enterprises etc. (Note 3) Not eligible → 20%

(Prepared based on METI materials)

(Note 1) Companies established within the previous 10 years and which have NOLs which will be carried over into the next fiscal year (excluding subsidiaries of large enterprises etc.).

(Note 2) Eligible companies are startups that receive investments from venture funds that have been certified under the Industrial Competitiveness Enhancement Act or from national university corporations and national research and development agencies that meet certain requirements.

(Note 3) Limited to basic research, applied research and R&D for the purpose of utilizing intellectual property, and excludes the mere consignment of R&D operations.

Even if an early stage startup has a cumulative deficit, if it posts a profit in any given fiscal year, it must pay taxes (e.g., in the case of companies with stated capital exceeding JPY100 million). This year’s revision (i.e. the increase of the maximum tax credit from 25% of the applicable fiscal year’s corporation tax to 40% of the same) will result in an increased amount of cash at hand remaining after such tax payments are made. This increase in cash at hand will act as a source of funds for further R&D investment.

Furthermore, the consignment of research to large enterprises, which was formerly ineligible for open innovation tax credits before the revision, will henceforth be eligible for the open innovation tax credit.

Use of the open innovation tax credits, whose scope was significantly expanded during the FY2015 tax reforms, stood at JPY300 million in FY2014, but increased to JPY3,900 million in FY2015 and to JPY 4,200 million in FY2016 (Source: “Report of Results of the Survey Concerning Application of the Special Measures Concerning Taxation” published by the Ministry of Finance (submitted to the Diet in February 2018)). As the application criteria were relaxed in the FY2017 reforms, and the FY2019 tax reforms will increase the maximum tax credit (5% to→ 10%), it is thought that the importance of open innovation tax credits to companies will continue to increase.

4 | Japan tax newsletter 4 February 2019

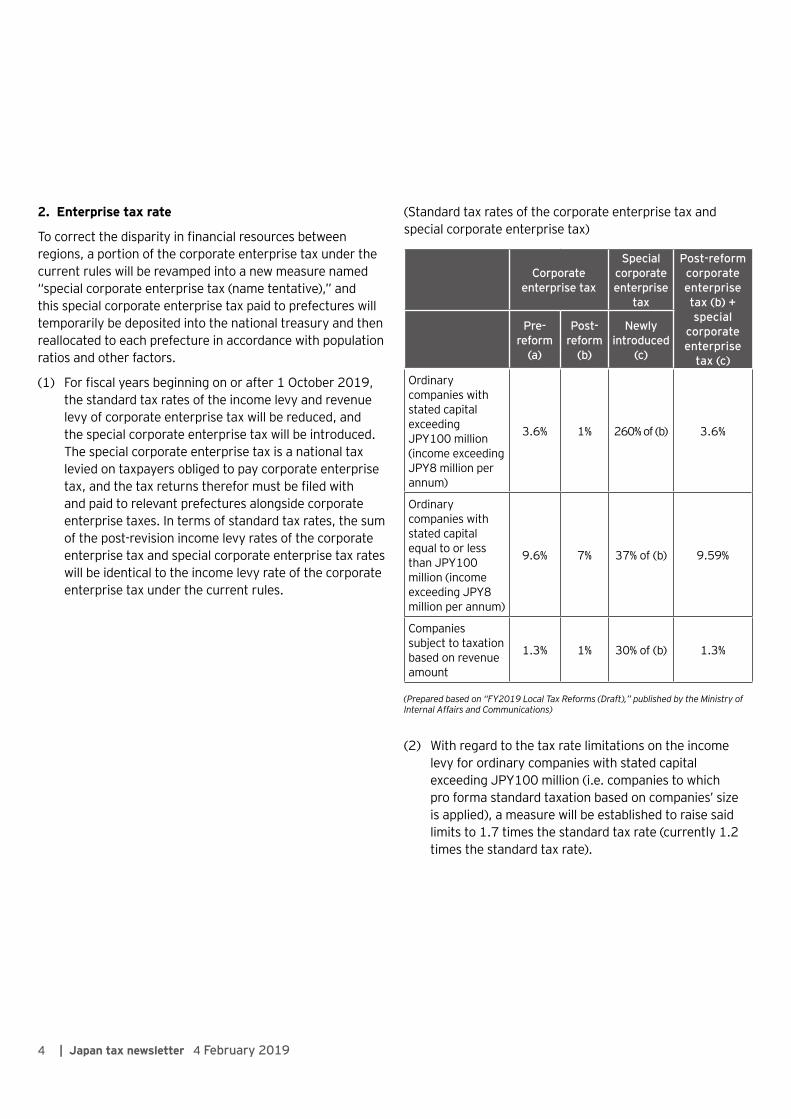

2. Enterprise tax rate

To correct the disparity in financial resources between regions, a portion of the corporate enterprise tax under the current rules will be revamped into a new measure named “special corporate enterprise tax (name tentative),” and this special corporate enterprise tax paid to prefectures will temporarily be deposited into the national treasury and then reallocated to each prefecture in accordance with population ratios and other factors.

(1) For fiscal years beginning on or after 1 October 2019, the standard tax rates of the income levy and revenue levy of corporate enterprise tax will be reduced, and the special corporate enterprise tax will be introduced. The special corporate enterprise tax is a national tax levied on taxpayers obliged to pay corporate enterprise tax, and the tax returns therefor must be filed with and paid to relevant prefectures alongside corporate enterprise taxes. In terms of standard tax rates, the sum of the post-revision income levy rates of the corporate enterprise tax and special corporate enterprise tax rates will be identical to the income levy rate of the corporate enterprise tax under the current rules.

(Standard tax rates of the corporate enterprise tax and special corporate enterprise tax)

Corporate enterprise tax

Special corporate enterprise

tax

Post-reform corporate enterprise tax (b) + special

corporate enterprise

tax (c)

Pre-reform

(a)

Post-reform

(b)

Newly introduced

(c)

Ordinary companies with stated capital exceeding JPY100 million (income exceeding JPY8 million per annum)

3.6% 1% 260% of (b) 3.6%

Ordinary companies with stated capital equal to or less than JPY100 million (income exceeding JPY8 million per annum)

9.6% 7% 37% of (b) 9.59%

Companies subject to taxation based on revenue amount

1.3% 1% 30% of (b) 1.3%

(Prepared based on “FY2019 Local Tax Reforms (Draft),” published by the Ministry of Internal Affairs and Communications)

(2) With regard to the tax rate limitations on the income levy for ordinary companies with stated capital exceeding JPY100 million (i.e. companies to which pro forma standard taxation based on companies’ size is applied), a measure will be established to raise said limits to 1.7 times the standard tax rate (currently 1.2 times the standard tax rate).

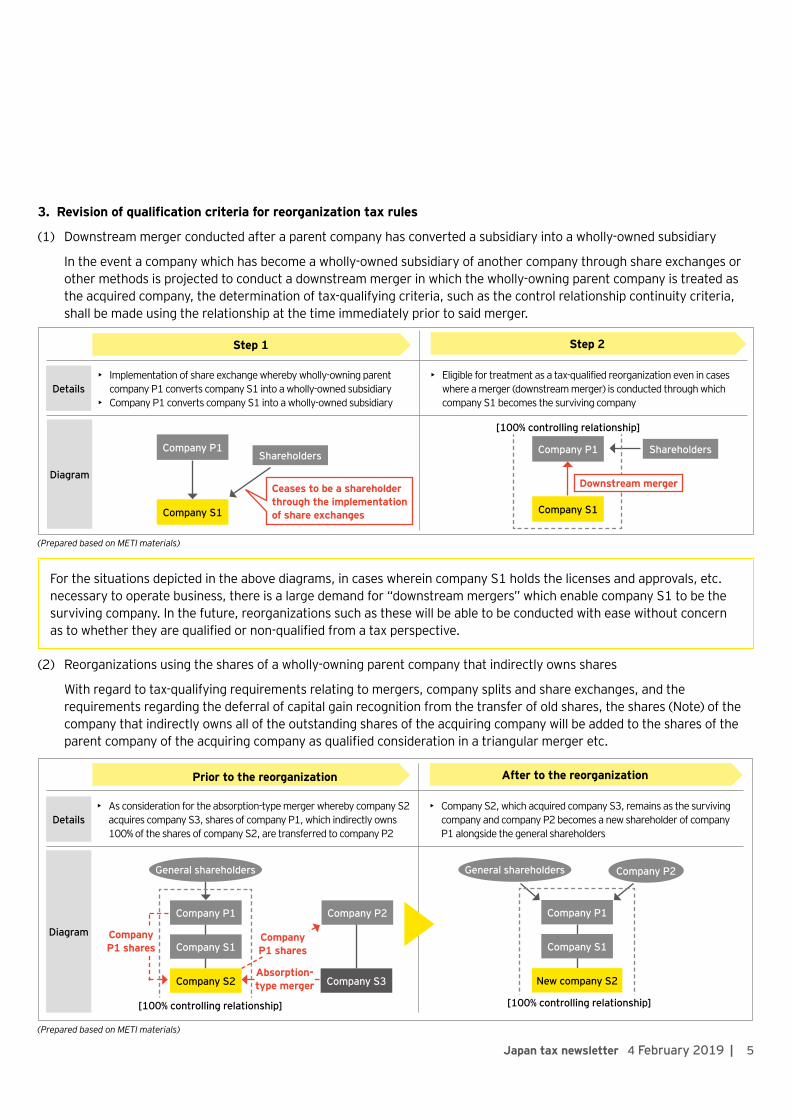

(1) Downstream merger conducted after a parent company has converted a subsidiary into a wholly-owned subsidiary

In the event a company which has become a wholly-owned subsidiary of another company through share exchanges or other methods is projected to conduct a downstream merger in which the wholly-owning parent company is treated as the acquired company, the determination of tax-qualifying criteria, such as the control relationship continuity criteria, shall be made using the relationship at the time immediately prior to said merger.

Company P1Shareholders

Company S1

Ceases to be a shareholder through the implementation of share exchanges

Details

Diagram

• Implementation of share exchange whereby wholly-owning parent company P1 converts company S1 into a wholly-owned subsidiary

• Company P1 converts company S1 into a wholly-owned subsidiary

• Eligible for treatment as a tax-qualified reorganization even in cases where a merger (downstream merger) is conducted through which company S1 becomes the surviving company

Step 1 Step 2

Company P1

Company S1

Shareholders

(Prepared based on METI materials)

[100% controlling relationship]

Downstream merger

For the situations depicted in the above diagrams, in cases wherein company S1 holds the licenses and approvals, etc. necessary to operate business, there is a large demand for “downstream mergers” which enable company S1 to be the surviving company. In the future, reorganizations such as these will be able to be conducted with ease without concern as to whether they are qualified or non-qualified from a tax perspective.

(2) Reorganizations using the shares of a wholly-owning parent company that indirectly owns shares

With regard to tax-qualifying requirements relating to mergers, company splits and share exchanges, and the requirements regarding the deferral of capital gain recognition from the transfer of old shares, the shares (Note) of the company that indirectly owns all of the outstanding shares of the acquiring company will be added to the shares of the parent company of the acquiring company as qualified consideration in a triangular merger etc.

Details

Diagram

• As consideration for the absorption-type merger whereby company S2 acquires company S3, shares of company P1, which indirectly owns 100% of the shares of company S2, are transferred to company P2

• Company S2, which acquired company S3, remains as the surviving company and company P2 becomes a new shareholder of company P1 alongside the general shareholders

Priortothereorganization Aftertothereorganization

General shareholders

Company P1

Company S2

Company S1

Company P2

Company S3

Company P1

New company S2

Company S1

Company P2General shareholders

(Prepared based on METI materials)

Company P1 shares

[100% controlling relationship]

Company P1 shares

Absorption-type merger

[100% controlling relationship]

6 | Japan tax newsletter 4 February 2019

(Note) With regard to certain mergers conducted between companies within a corporate group, in the event that the shares of certain foreign companies indirectly owning all of the outstanding shares of the acquiring company (hereinafter, “specially-related foreign company”) are provided as consideration, the merger will not be considered to have met the tax-qualification requirements. Furthermore, in the event that a merger in which shares of a specially-related foreign company are provided as consideration is not deemed as a qualified merger, then the capital gains on old shares owned by shareholders at the time of the merger will be taxed.

In the event that company P1 in the above diagram is a listed company, there are cases where company P2, the shareholder of company S3 (the non-surviving entity), desires the acquisition of shares of company P1, which have higher liquidity (convertibility to cash). After the revision, even if consideration for this triangular merger is paid through the provision of company P1 shares to company P2, said merger will fulfill the qualification requirements.

(1) With regard to SMEs issuing shares that are partnership property of investment limited partnerships (referred to as “business succession funds”) in relation to certification of business restructuring investment plans under the Small and Medium-sized Enterprises Business Enhancement Act, determination of whether an SME is deemed to be a large enterprise (i.e. enterprises to which SME tax rules such as the following cannot be applied: The SME investment tax incentive, special depreciation in the event specified SMEs acquire management capability enhancement equipment, and SME business enhancement tax rules) will be conducted by excluding the shares owned by the Organization for Small & Medium Enterprises and Regional Innovation (categorized as a large enterprise) when it has invested in said business succession fund.

(2) With respect to the determination of “enterprises categorized as large enterprises,” which are not considered as SMEs that are qualified for application of various special tax measures for SMEs provided for in the Act on Special Measures Concerning Taxation, the following companies will be added to the scope of large enterprises.

(A) Wholly-owned subsidiaries of large enterprises (stated capital of JPY500 million or more)

(B) Companies whose outstanding shares or investments are all owned by multiple large enterprises within a 100% capital relationship group

Due to the measure in (2) above, companies such as company S2 which were qualified for application of various tax incentives since they were deemed as SMEs under the Act on Special Measures Concerning Taxation despite the fact that they did not qualify as SMEs under the Corporation Tax Act, are expected to lose eligibility for the application of various tax incentives.

Corporation Tax Act

Act on Special Measures

Concerning Taxation

Company S1 Non-SME Non-SME

Company S2 Non-SME

(Pre-revision) SME

↓(Post-revision)

Non-SME

Company P (stated capital of

JPY500 mil.)

Company S2 (stated capital of

JPY100 mil.)

Company S1 (stated capital of

JPY100 mil.)

100%

100%

(Prepared based on METI materials)

5. Revision of requirements in relation to deductible performance-linked compensation

Requirements in relation to procedures for deductible directors’ performance-linked compensation paid by companies will be revised as follows.

(1) [Revised] Procedures concerning decisions made by the compensation committee and compensation advisory committee (hereinafter, “compensation committee(s) etc.”)

(A) The requirement that companies that have set up compensation committee(s) etc. not employ executive directors as members of the compensation committee(s) etc. will be removed, and a new requirement stipulating that executive directors cannot participate in resolutions concerning decisions concerning their own performance-linked compensation will be added.

(B) New requirements will be added such that a majority of the members of compensation

7Japan tax newsletter 4 February 2019 |

committee(s) etc. must be independent outside directors and that the approval of all independent outside directors who are members of said committee(s) etc. must be obtained concerning decisions on performance-linked compensation.

(2) [Abolished] Procedures concerning decisions made by companies that have a board of corporate auditors

The following two procedures will be removed from the scope of procedures which qualify as procedures to approve directors’ performance-linked compensation that are deemed as deductible expenses:

(A) A decision made by the board of directors of a company that has a board of corporate auditors where appropriate documents have been submitted and approval has been obtained from the majority of the corporate auditors; and

(B) A decision made by the board of directors of a company that has an audit committee where approval has been obtained from the majority of audit committee members.

6. Other

(1) Introduction of special depreciation rules concerning disaster prevention and mitigation equipment for SMEs

For SMEs that have received certification of their business continuity capability enhancement plans or collaborative business continuity capability enhancement plans (names tentative) under the Small and Medium-sized Enterprises Business Enhancement Act and that have acquired specified business continuity capability enhancement equipment (e.g. private electric generators, data backup systems and fire shutters) in relation to said business continuity capability enhancement plans or collaborative business continuity capability enhancement plans for said certification by 31 March 2021, and which have used said equipment for said business purposes, a tax measure will be introduced to allow a special depreciation of 20% of the equipment acquisition price.

(2) Revision of requirements for special measures for taxation of investment companies investing in silent partnerships

With regard to special measures pertaining to taxation of investment companies and special measures pertaining to taxation of trustee companies in relation

to specified investment trusts, the requirement limiting ownership to less than 50% of the outstanding shares of or investments in other companies will be revised so that “investments in other companies” includes investments in silent partnerships (Tokumei Kumiai or TK in Japanese).

(3) Extension of applicable periods

(A) The applicable period of special measures for the reduction of the corporation tax rate of SMEs (15% of income equal to or less than JPY8 million per annum) will be extended by two years.

(B) The applicable period of the SME investment tax incentive and SME business enhancement tax rules and other measures will be extended by two years upon the revision of certain application requirements etc.

8 | Japan tax newsletter 4 February 2019

International taxation

Revision of earnings stripping rulesThe earnings stripping rules under the current taxation system are based on the same concept as that of Action 4 of the Base Erosion and Profit Shifting (BEPS) Final Report. However, since there are discrepancies between the two rules in terms of qualified interest categories, the definition of adjusted income and the standard maximum deductible amount, revisions will be made to the current Japanese rules to match Action 4 of the BEPS Final Report while taking into consideration its impact on normal economic activities (e.g. loans from domestic (i.e. Japanese; same hereinafter) banks).

1. Overview of the rules

An overview of the current earnings stripping rules is as follows.

Related party net interest expenses only

(A)*Interest included in the

Japanese taxable income of the recipient is excluded

Other(Depreciation/amortization and domestic and foreign

dividend income)

Taxable income in the applicable fiscal year

(income before taxes)

Deductible

Non-deductible (*)

* Non-deductible interest expenses from a given year can be carried over and deducted over the subsequent 7 year period.

Adjusted income×

50%(C)

Enforcement: April 2013

Maximum deductible amountAdjusted income (B)

An overview of the earnings stripping rules after the revision is as follows.

Net interest expenses (A)

*Interest included in the Japanese taxable income of

the recipient is excluded

Other(depreciation)

Deductible

Non-deductible (*)

Enforcement: April 2020

Adjusted income (B)

Adjusted income×

20%(C)

Maximum deductible amount

Taxable income in the applicable fiscal year

(income before taxes)

* Non-deductible interest expenses from a given year can be carried over and deducted over the subsequent 7 year period.

Current rules Revision

(A) Qualified interest

Related party net interest expenses only (interest included in the Japanese taxable income of the recipient is excluded)

Net interest expenses (including that paid to or received from third parties; interest included in the Japanese taxable income of the recipient is excluded)

(B) Adjusted income

Income before deduction of interest, taxes and depreciation/ amortization expenses (EBITDA) (includes non-taxable domestic and foreign dividend income)

Income before deduction of interest, taxes and depreciation/ amortization expenses (EBITDA) (does not include non-taxable domestic and foreign dividend income)

(C) Standard maximum deductible amount

50% 20%

Requirements for exemption

• The amount of related party net interest expenses is less than or equal to JPY10 million

• The amount of interest expenses paid to related parties is 50% or less of the total amount of interest expenses

• The amount of net interest expenses is less than or equal to JPY20 million

• The total amount of net interest expenses of all domestic group companies (share ownership ratio in excess of 50%) is 20% or less of total adjusted income

Interest qualifying under the revised earnings stripping rules will equal the amount remaining (hereinafter, “amount of qualified net interest expenses”) after deducting from the total amount of qualified net interest expenses for the applicable fiscal year (refers to the amount remaining after deducting the “non-qualified interest expense amount” from the interest expense amount; same hereinafter), the total amount of interest income calculated as corresponding to the aforementioned qualified net interest expenses (hereinafter, “total amount of deductible interest income”).

The aforementioned “non-qualified interest expense amount” refers to the following amounts prescribed for each category of interest expenses also described below.

9Japan tax newsletter 4 February 2019 |

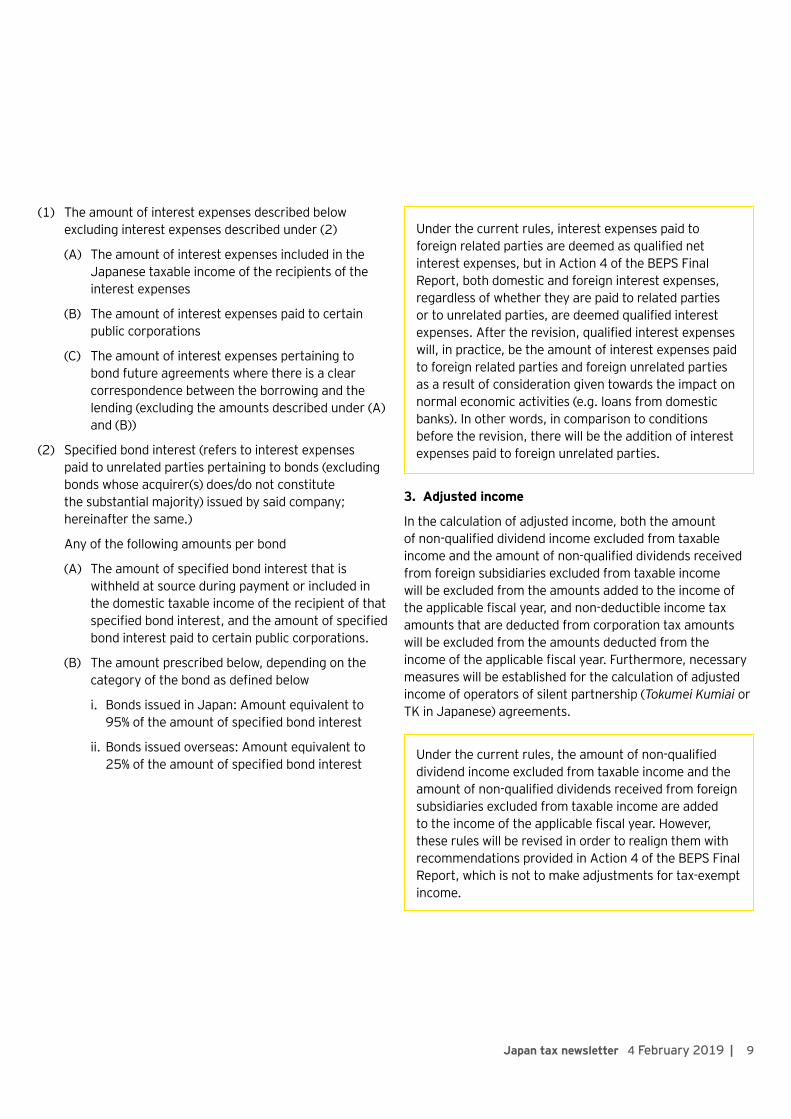

(1) The amount of interest expenses described below excluding interest expenses described under (2)

(A) The amount of interest expenses included in the Japanese taxable income of the recipients of the interest expenses

(B) The amount of interest expenses paid to certain public corporations

(C) The amount of interest expenses pertaining to bond future agreements where there is a clear correspondence between the borrowing and the lending (excluding the amounts described under (A) and (B))

(2) Specified bond interest (refers to interest expenses paid to unrelated parties pertaining to bonds (excluding bonds whose acquirer(s) does/do not constitute the substantial majority) issued by said company; hereinafter the same.)

Any of the following amounts per bond

(A) The amount of specified bond interest that is withheld at source during payment or included in the domestic taxable income of the recipient of that specified bond interest, and the amount of specified bond interest paid to certain public corporations.

(B) The amount prescribed below, depending on the category of the bond as defined below

i. Bonds issued in Japan: Amount equivalent to 95% of the amount of specified bond interest

ii. Bonds issued overseas: Amount equivalent to 25% of the amount of specified bond interest

Under the current rules, interest expenses paid to foreign related parties are deemed as qualified net interest expenses, but in Action 4 of the BEPS Final Report, both domestic and foreign interest expenses, regardless of whether they are paid to related parties or to unrelated parties, are deemed qualified interest expenses. After the revision, qualified interest expenses will, in practice, be the amount of interest expenses paid to foreign related parties and foreign unrelated parties as a result of consideration given towards the impact on normal economic activities (e.g. loans from domestic banks). In other words, in comparison to conditions before the revision, there will be the addition of interest expenses paid to foreign unrelated parties.

3. Adjusted income

In the calculation of adjusted income, both the amount of non-qualified dividend income excluded from taxable income and the amount of non-qualified dividends received from foreign subsidiaries excluded from taxable income will be excluded from the amounts added to the income of the applicable fiscal year, and non-deductible income tax amounts that are deducted from corporation tax amounts will be excluded from the amounts deducted from the income of the applicable fiscal year. Furthermore, necessary measures will be established for the calculation of adjusted income of operators of silent partnership (Tokumei Kumiai or TK in Japanese) agreements.

Under the current rules, the amount of non-qualified dividend income excluded from taxable income and the amount of non-qualified dividends received from foreign subsidiaries excluded from taxable income are added to the income of the applicable fiscal year. However, these rules will be revised in order to realign them with recommendations provided in Action 4 of the BEPS Final Report, which is not to make adjustments for tax-exempt income.

10 | Japan tax newsletter 4 February 2019

4. Standard maximum deductible amount

In the event that qualified net interest expenses exceed 20% of adjusted income in the applicable fiscal year (from the current 50%), the amount equivalent to the amount in excess of said limit will not be included in deductible expenses.

The standard fixed ratio under current Japanese tax rules is 50% which exceeds the best practice range for standard fixed ratios recommended in Action 4 of the BEPS Final Report set between 10% to 30%. Therefore, tax rules will be revised to lower said ratio to 20%.

5. Application exemption criteria

The earning stripping rules will not be applied when any of the following criteria are met.

(1) The amount of qualified net interest expenses in the applicable fiscal year is JPY20 million or less (from the current JPY10 million or less)

(2) The ratio of the amount under (A) in the applicable fiscal year to the amount under (B) is 20% or less

(A) The amount remaining after deducting the total amount of qualified net interest income (refers to the amount remaining after deducting the total amount of qualified interest expenses from the total amount of deductible interest income) of a domestic company* from the total amount of qualified net interest expenses

(B) The amount remaining after deducting the total amount of adjusted losses (refers to the amount less than zero in the event that an amount less than zero is derived from the calculation of adjusted income) of a domestic company* from the total amount of adjusted income

* Domestic companies refers to any company located in Japan and other companies located in Japan that are related to said company through ownership of more than 50% of outstanding shares (limited to companies whose start date and last date of a fiscal year both respectively equal the start date and last date of the fiscal year of said domestic company).

Under the current rules, a de minimis standard exempting companies from application of the earning stripping rules has been established for companies whose qualified net interest expenses equal JPY10 million or less. In addition, a standard has been established for companies whose qualified interest is equal to or less than 50% of interest expenses, exempting such companies from application of the earning stripping rules. These revisions will increase the de minimis standard from JPY10 million to JPY20 million. Furthermore, the standard for “companies whose qualified interest is equal to or less than 50% of interest expenses” will be abolished and a new standard for holding companies will be established as described in (2) above.

6. Amount of deductible excess interest

(1) In the event that qualified net interest expense is less than 20% of adjusted income of the applicable fiscal year (from the current 50%, as mentioned in 4. above), and if there were any amounts which were treated as non-deductible interest in any fiscal years beginning within the previous 7 years due to application of earnings stripping rules (hereinafter, “excess interest”), then an amount equivalent to said excess interest can be included in deductible expenses not to exceed a limit which equals the difference between the qualified net interest expenses and 20% (from the current 50%) of adjusted income.

(2) A revision will be made to allow application of (1) above, even if the applicable amounts are indicated in documents attached to amended tax returns or requests for correction.

There is no change to the rule that excess interest can be carried over for 7 years.

11Japan tax newsletter 4 February 2019 |

7. Application period

The above revisions (excluding 6. (2)) are applicable to corporation tax for fiscal years beginning on or after 1 April 2020. The above revision described in 6. (2) is applicable to corporation tax whose submission deadlines for final tax returns, etc. is on or after 1 April 2020.

Furthermore, although the aforementioned revisions are related to national taxation, the necessary local tax (corporate inhabitant tax and corporate enterprise tax) measures will also be established in accordance with the treatment in national taxation concerning the revision of the earning stripping rules.

Although earning stripping rules will be revised to not include non-qualified domestic and foreign dividend income (excluded from taxable income) in adjusted income, and the standard maximum deductible amount will be lowered from 50% to 20%, through revisions to limit qualified interest, in practice, to interest expenses paid to foreign parties and the introduction of the rule described in 5. (2) above, the new rules give due consideration to the economic activities of Japanese companies. On the other hand, this will require foreign companies in Japan which have large amounts of loans from overseas, companies employing structured finance products, and companies issuing bonds overseas to exercise caution.

Revision of transfer pricing tax rulesIn view of the amendments made to the BEPS Report and the OECD Transfer Pricing Guidelines (hereinafter, “TPG”), revisions will be made to the transfer pricing tax rules in Japanese laws concerning methods for calculating arm’s length prices and transactions of certain hard-to-value intangible assets.

1. Clarificationofthedefinitionofintangibleassetssubject to transfer pricing tax rules

Intangible assets subject to transfer pricing tax rules are said to be assets other than tangible assets and financial assets (cash, deposits and securities) that are owned by companies, and for which consideration should be paid in the event they are transferred or lent out in accordance with the terms of ordinary transactions conducted between independent business operators.

The TPG provides that “the word ‘intangible’ is meant to address something which is not a physical or a financial asset, which is capable of being owned or controlled for use in commercial activities and whose use or transfer would be compensated had it occurred in a transaction between independent parties in comparable circumstances.” In response, the reforms will clarify the scope of intangible assets for tax purposes. These provisions are thought to define intangible assets under the transfer pricing tax rules.

2. Revision of methods for calculating arm’s length prices (TPMs)

The discounted cash flow method (DCF method) will be added to the methods allowed for the calculation of arm’s length prices (hereinafter, “transfer pricing methods” or “TPM”). The DCF method is recognized as an effective TPM for intangible asset transactions when comparable transactions allowable under the TPG cannot be identified.

Along with this revision, in the event companies do not submit documents deemed necessary for calculating arm’s length prices, the DCF method will be added to TPMs that can be employed in the calculation of estimated taxation by National Tax Agency employees to calculate an amount deemed as the arm’s length price (based on information that would have been available to them at the time the foreign related transactions were conducted).

TPMs proposed by the TPG and the necessity of referencing comparable transactions.

Prepared based on “Ministry of Finance Explanatory Materials (Concerning International Taxation) (2 of 2),” a document prepared for the 20th Tax Commission Meeting (7 November 2018)

3. Cost plus method (CP method)4. Transactional net margin

method (TNMM)

5. Transactional profit split method

6 Other methodsExpansion of TPG concerning the DCF method during the BEPS Project

TPMs that reference comparable transactions

Cannot be used when there are no comparable transactions

12 | Japan tax newsletter 4 February 2019

The TPG recommends use of the DCF method as the TPM for intangible asset transactions and other transactions. In practice, although there are cases wherein the DCF method is used to calculate transfer prices of intangible assets, in Japan, legal treatment of the DCF method is unclear. Revisions will be made for this reason, but in the future, public announcements providing clear guidance concerning the application of the DCF method are desired.

3. Introduction of price adjustment measures pertaining to transactions involving hard-to-value intangibles (specifiedintangibleassettransactions)

With regard to transactions involving specified intangible assets (hereinafter, “specified intangible asset transactions”), in the event that there is a difference between the forecasts used as a base for the calculation of arm’s length prices and the results, the District Director of the Tax Office will be given the authority to make corrections by deeming as the arm’s length price the amount calculated using the most appropriate TPM for the specified intangible asset transaction under review, after taking into consideration the results of the specified intangible asset transaction under review and the probability of the occurrence of the events that caused the difference. However, notwithstanding the foregoing are cases where the difference between the foregoing calculated amount and initial transaction price does not exceed 20%.

(1) Specified intangible assets

“Specified intangible asset” refers to an intangible asset that meets all of the following requirements.

(A) Is unique and has significant value

(B) Revenue forecasts are used as a base for the calculation of its arm’s length price

(C) Projections used as a base for the calculation of its arm’s length price are deemed to be uncertain

The definition of specified intangible assets is thought to be largely identical to the definition of “hard-to-value intangibles (HTVI)” described in the TPG. Although many countries (e.g. the UK, the Netherlands, Australia and New Zealand) are thought to be in line with the TPG, caution is necessary when conducting transactions with countries that have established their own rules concerning intangible asset transactions (e.g. the US and Germany). Public announcements providing clear guidance concerning specified intangible assets are desired.

(2) Application exemption criteria

This price adjustment measure will not be applied in cases wherein National Tax Agency employees request submission of documents described in (A) or (B) below from a company and the company submits said documents within a fixed period following the request date.

(A) Documents described below

i. Documents that include details of forecasts used as a base for the calculation of arm’s length prices of specified intangible asset transactions

ii. Documents that provide evidence that the events that caused the difference between said forecasts and results were natural disasters or other similar events and that it was extremely difficult to forecast its occurrence at the time of transaction, or that the arm’s length price was calculated after appropriately taking into consideration the probability of the occurrence of said events at the time of transaction

(B) Documents that provide evidence that the difference between the forecast revenue amount between the period lasting from the first day of the fiscal year that includes the first day when unrelated party revenue was generated through the use of a specified intangible asset until 5 years have passed from the first day of the first fiscal year and the actual revenue amount does not exceed 20%

(Note) If a company submits the documents described in (B) above, the price adjustment measure will not be applied to days subsequent to the submission date.

13Japan tax newsletter 4 February 2019 |

Companies are required to prepare documents that include details of forecasts used in the calculation of the arm’s length price at the time of transaction when conducting a specified intangible asset transaction. Furthermore, in the event an unforeseeable event occurs in fiscal years after the transaction and the actual revenue greatly deviates from the forecast revenue, the company is required to prepare documents that include analyses of the causes.

4. Extension of the period for a correction decision relating to transfer pricing tax rules

The periods for correction decisions and requests for the correction of corporation tax relating to transfer pricing tax rules will be extended to seven years (from the current six years).

Caution is necessary not only for specified intangible asset transactions or when selecting the DCF method as a TPM, but also regarding the fact that the general period for correction decisions etc. under transfer pricing tax rules will be extended by one year.

5. Establishment of the difference adjustment method

With regard to adjustments of differences made in relation to a TPM for referencing the profit margin of comparable transactions, when necessary adjustments cannot be made due to the fact that assessing quantitative differences is extremely difficult, use of a method based on the interquartile method will be allowed for adjusting such differences.

Public announcements providing clear guidance concerning specific operation methods are desired, such as explanations of the type of situations deemed as cases “when necessary adjustments cannot be made due to the fact that assessing quantitative differences is extremely difficult.”

6. Application period

The above revisions are applicable to corporation tax for fiscal years beginning on or after 1 April 2020 and income tax for 2021 or after.

Furthermore, although the aforementioned revisions are related to national taxation, the necessary local tax (individual inhabitant tax, corporate inhabitant tax and corporate enterprise tax) measures will also be established in accordance with the treatment in national taxation concerning the revisions of the transfer pricing tax rules.

Revision of foreign subsidiary income inclusion taxation rules (CFC rules)1. Shell companies

The following foreign related companies will be excluded from the scope of shell companies (or “paper companies” in Japanese).

Even if companies are excluded from the scope of shell companies as a result of qualifying as foreign related companies under (1) to (3), there may be cases when they are classified as cash boxes. Furthermore, foreign related companies with an effective tax rate of less than 20% will be excluded from application of this revision.

In addition, it is necessary to heed future developments concerning whether there will be requirements to attach documents to final tax returns to fulfill the exemption requirements described below, as was required for exemption under the former tax rules, or whether submission of documents will be required each time the tax authorities request documents that show that requirements are being met as is the case with the presumptive provisions under the current tax rules.

14 | Japan tax newsletter 4 February 2019

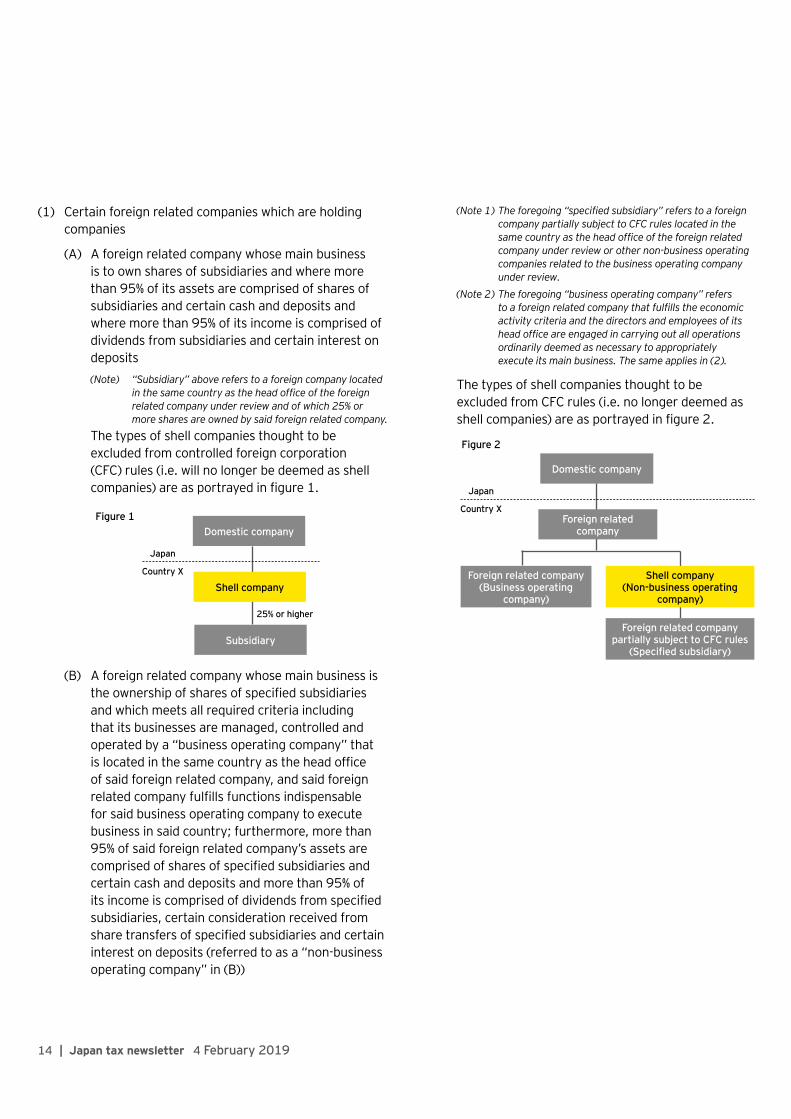

(1) Certain foreign related companies which are holding companies

(A) A foreign related company whose main business is to own shares of subsidiaries and where more than 95% of its assets are comprised of shares of subsidiaries and certain cash and deposits and where more than 95% of its income is comprised of dividends from subsidiaries and certain interest on deposits(Note) “Subsidiary” above refers to a foreign company located

in the same country as the head office of the foreign related company under review and of which 25% or more shares are owned by said foreign related company.

The types of shell companies thought to be excluded from controlled foreign corporation (CFC) rules (i.e. will no longer be deemed as shell companies) are as portrayed in figure 1.

Figure 1

25% or higher

Domestic company

Shell company

Subsidiary

Japan

Country X

(B) A foreign related company whose main business is the ownership of shares of specified subsidiaries and which meets all required criteria including that its businesses are managed, controlled and operated by a “business operating company” that is located in the same country as the head office of said foreign related company, and said foreign related company fulfills functions indispensable for said business operating company to execute business in said country; furthermore, more than 95% of said foreign related company’s assets are comprised of shares of specified subsidiaries and certain cash and deposits and more than 95% of its income is comprised of dividends from specified subsidiaries, certain consideration received from share transfers of specified subsidiaries and certain interest on deposits (referred to as a “non-business operating company” in (B))

(Note 1) The foregoing “specified subsidiary” refers to a foreign company partially subject to CFC rules located in the same country as the head office of the foreign related company under review or other non-business operating companies related to the business operating company under review.

(Note 2) The foregoing “business operating company” refers to a foreign related company that fulfills the economic activity criteria and the directors and employees of its head office are engaged in carrying out all operations ordinarily deemed as necessary to appropriately execute its main business. The same applies in (2).

The types of shell companies thought to be excluded from CFC rules (i.e. no longer deemed as shell companies) are as portrayed in figure 2.

Figure 2

Domestic company

Japan

Country XForeign related

company

Foreign related company(Business operating

company)

Shell company(Non-business operating

company)

Foreign related company partially subject to CFC rules

(Specified subsidiary)

15Japan tax newsletter 4 February 2019 |

While a foreign related company that falls under (A) is subject to application of the foreign subsidiary income inclusion taxation rules (CFC rules) under the current tax system, dividends received from companies that fulfill requirements such as share ownership ratios of 25% or more will not be included in the calculation of the applicable amount pertaining to said foreign related company and as a result, income inclusion taxation (or unitary taxation) will not occur for said amount. It is thought that this measure was established after taking into account the fact that income inclusion taxation does not occur even under the current rules.

Moreover, in the event a foreign related company that falls under (A) transfers its subsidiary shares, it will become difficult to fulfill the income requirements therein. On the other hand, since income requirements under (B) include “certain consideration received from share transfers of specified subsidiaries,” it will become easier for a foreign related company to fulfill said requirements. However, this category is subject to the following additional requirements in comparison to (A).

(i) Main business is the ownership of shares of specified subsidiaries (refer to Note 1 for requirements of a specified subsidiary)

(ii) Its businesses are managed and controlled by a business operating company located in the same country as its head office (refer to (Note 2) for requirements of a business operating company)

(iii) Fulfills functions indispensable for said business operating company to execute business

With regard to (iii), it is necessary to heed future developments since it is currently unclear what functions specifically are recognized by these rules (the same applies for (2) and (3)).

(2) Certain foreign related companies relating to the ownership of real estate

(A) A foreign related company whose main business is to own certain real estate located in the same country as that of its head office or shares of specified subsidiaries and which meets all required criteria including that its businesses are managed, controlled and operated by a business operating company located in the same country, and said foreign related company fulfills functions indispensable for said business operating company to execute business (limited to the real estate business) in said country; furthermore, more than 95% of said foreign related company’s assets are comprised of said real estate, shares of specified subsidiaries and certain cash and deposits and more than 95% of its income is comprised of income earned from said real estate and from shares of specified subsidiaries, and certain interest on deposits (referred to as a “non-business operating company” in (A))(Note) The foregoing “specified subsidiaries” refers to other

non-business operating companies related to the business operating company under review.

The types of shell companies thought to be excluded from controlled foreign corporation (CFC) rules (i.e. will no longer be deemed as shell companies) are as portrayed in figure 3.

Realestate

Figure 3

Domestic company

Japan

Country X

Foreign related company

(Business operating company)

Shell company(Non-business

operating company)

Shell company(Non-business

operating company/specified subsidiary)

16 | Japan tax newsletter 4 February 2019

(B) A foreign related company whose main business is to own real estate located in the same country as that of its head office and actually used by a business operating company located in the same country as the head office of said foreign related company and which meets all required criteria including that its businesses are managed, controlled and operated by said business operating company; furthermore, said foreign related company fulfills functions indispensable for said business operating company to execute business in said country and more than 95% of said foreign related company’s assets are comprised of said real estate and certain cash and deposits and more than 95% of its income is comprised of income earned from said real estate and certain interest on deposits.

It is thought that type (A) was established to cover foreign related companies engaged in the real estate business owning real estate for the purpose of selling or lending them to third parties, and type (B) to cover foreign related companies that own real estate for its own use such as an office building.

Moreover, if certain requirements are fulfilled, foreign related companies whose main business is to own shares of specified subsidiaries (intermediary holding companies; refer to the note for criteria concerning specified subsidiaries) are also allowed under type (A), while such ownership is not allowed under type (B), since it is limited to foreign related companies whose main business is to own real estate.

Concerning type (B), it is thought that the requirements for matters other than real estate are roughly the same as those described in 1. (1) (B) above.

(3) Certain foreign related companies relating to resource development and other projects

A foreign related company whose main business is the ownership of shares of specified subsidiaries, provision of funds procured from unrelated parties to specified subsidiaries or ownership of real estate located in the same country as that of its head office, and which meets all required criteria including that its businesses are managed, controlled and operated by a business operating company located in the same country

and said foreign related company fulfills functions indispensable for said business operating company to execute businesses to develop or establish resources, such as petroleum or natural gas, or social capital in said country (referred to as “resource development projects” in (3)); furthermore, more than 95% of said foreign related company’s assets are comprised of shares of specified subsidiaries, certain loans provided to specified subsidiaries, said real estate and certain cash and deposits and more than 95% of its income is comprised of income earned from shares of specified subsidiaries, said loans and said real estate, and certain interest on deposits(Note 1) The foregoing “specified subsidiaries” refers to foreign

companies located in the same country as the head office of the foreign related company under review and of which 10% or more of shares are owned by said foreign related company, and they fulfill functions indispensable for the business operating company under review to carry out resource development projects in said country.

(Note 2) The foregoing “business operating company” refers to a foreign related company that fulfills the economic activity criteria and whose directors and employees of its head office are engaged in carrying out all operations ordinarily deemed as necessary to appropriately execute resource development projects. In addition, it also includes other foreign companies located in the same country as the head office of said foreign related party and where the directors and employees of said other foreign companies jointly engage in carrying out all of the foregoing operations.

The types of shell companies thought to be excluded from controlled foreign corporation (CFC) rules (i.e. will no longer be deemed as shell companies) are as portrayed in figure 4.Figure 4

Domestic company

Japan

Country X

Shell company(Non-business

operating company)

Functions indispensable for

executing resource development

projects (specified subsidiary)

Shell company(Non-business

operating company)

Foreign related company

(Business operating company)

10% or higher

Resources

Provision of funds

17Japan tax newsletter 4 February 2019 |

Foreign related companies whose main business is any of the following and which meet certain requirements will be excluded from the scope of shell companies.

(i) Owns shares of specified subsidiaries (foreign companies that fulfill functions indispensable for executing resource development projects; refer to (Note 1))

(ii) Provides funds procured from unrelated parties to specified subsidiaries

(iii) Owns certain real estate located in the same country as that of the head office of the foreign related company under review

Moreover, “loans” have been added to the same asset requirements described in 1. (2)(A) and (B) above, while “income earned from loans” have likewise been added to the income requirements.

In addition, under this measure, “other foreign companies located in the same country as the head office of said foreign related party and where the directors and employees of said other foreign companies jointly engage in carrying out all of the foregoing operations” are added to the same “business operating company” requirement described in 1. (1)(B) and (2)(A) and (B) above.

2. De facto cash boxes

Foreign related companies which meet all of the following criteria will be included in the scope of de facto cash boxes.

(i) A foreign related company whose ratio of the total of certain insurance premium revenue (refers to “specified insurance premium revenue” in (ii)) received from unrelated parties to total insurance premium revenue in the applicable fiscal year is less than 10%

(ii) A foreign related company whose ratio of the total of certain reinsurance premiums paid to unrelated parties in relation to insurance premium revenue (excludes specified insurance premium revenue; the same applies for the term “insurance premium revenue” used in (ii)) to total insurance premium revenue in the applicable fiscal year is less than 50%

Foreign related companies whose insurance premium revenue from unrelated parties is minimal and amount of reinsurance premiums paid to unrelated parties is low have been added to the scope of cash boxes. These rules are thought to have been developed to cover captive insurance companies.

The amount of income calculated based on provisions set forth by laws and regulations pertaining to foreign corporation tax of the country where the head office of the foreign related company under review is located will be prescribed to be the amount of income of the foreign related company calculated by excluding provisions concerning consolidated tax payment and provisions concerning pass-through treatment from the foregoing provisions set forth by laws and regulations and then adding adjustments to that amount for non-taxable income.

(2) Foreign corporation tax

The amount of foreign corporation tax levied in the country where the head office of the foreign related company under review is located will be prescribed to be the amount of foreign corporation tax calculated as the amount of foreign corporation tax levied on the amount of income of the foreign related party calculated by excluding provisions concerning consolidated tax payment and provisions concerning pass-through treatment from the provisions set forth by laws and regulations pertaining to the foregoing foreign corporation tax.

18 | Japan tax newsletter 4 February 2019

In the sections entitled “Examples of Application of US Consolidated Tax Payment Rules” and “Examples of US Subsidiaries Owning Shares of US LLCs Electing Pass-through Taxation” in the “Tax Treatment of Foreign Subsidiary Income Inclusion Taxation Rules (CFC Rules or Anti-Tax Haven Rules)” published by the Japan Tax Association in September 2014, it states that it is appropriate to calculate effective tax rates based on calculations of standalone income and corresponding standalone corporation taxes based on the presumption that each company has paid taxes on a standalone basis.

The US federal corporation tax rate in 2014 exceeded 30%, and thus US subsidiaries were generally not subject to CFC rules when the foregoing concept was applied. Therefore, detailed and accurate calculations were not required at the time. However, since the US federal corporation tax rate has been reduced to 21%, detailed and accurate calculations will be required due to the fact that there is large difference in tax treatments in cases wherein the effective tax rate is equal to or higher than 30% as opposed to cases wherein it is less than 20%. In the future, it will become necessary to heed future developments concerning details of calculation methods, including calculation methods of state taxes.

4. Amounts subject to application of entity-level income inclusion tax rules

The standard income amount in cases wherein amounts subject to income inclusion are calculated using standards set forth by local laws and regulations will be prescribed to be the amount of income of the foreign related company calculated by excluding provisions concerning consolidated tax payment and provisions concerning pass-through treatment from provisions set forth by laws and regulations pertaining to corporate income tax of the country where the head office of the foreign related company is located and then adding adjustments to that amount for non-taxable income.

It is thought that this revision will be made in order to match the income amounts described in 3. (1) above. Moreover, since this revision specifies “provisions concerning consolidated tax payment and provisions concerning pass-through treatment,” it is thought that the UK’s group relief measure and Germany’s tax grouping (“organschaft”) rules are not included in the scope thereof (same concept applies in section 5.)

5. Calculation of foreign tax credit

Out of the amount of foreign corporation tax deducted in cases wherein a domestic company will be subject to income inclusion taxation, the amount of foreign corporation tax levied in the country where the head office of the foreign related company under review is located will be prescribed to be the amount of foreign corporation tax calculated as the amount of foreign corporation tax levied on the amount of income of the foreign related party calculated by excluding provisions concerning consolidated tax payment and provisions concerning pass-through treatment from the provisions set forth by laws and regulations pertaining to the foregoing foreign corporation tax.

It is thought that this revision will be made in order to match the foreign corporation tax amounts described in 3. (2) above.

6. Amounts subject to partial application of partial income inclusion tax rules

The amount after reducing the amount described in (ii) from the amount described in (i) will be added to the amount of specified income subject to partial income inclusion tax rules in relation to foreign related companies partially subject to income inclusion rules (excluding companies deemed as foreign financial subsidiaries).

(i) The balance after deducting total reinsurance premiums paid from total insurance premiums received

(ii) The balance after deducting total reinsurance claims received from total insurance benefits paid

These rules are thought to target captive insurance companies as in 2. above.

19Japan tax newsletter 4 February 2019 |

7. Other

(1) Requirements for the application of double taxation adjustments relating to dividends received from foreign subsidiaries

With regard to double taxation adjustments for dividends received from foreign subsidiaries that a domestic company is subject to income inclusion for, revisions will be made to expand the permissible scope of the application of such adjustments to include cases wherein the applicable amounts are indicated in documents attached to amended tax returns or requests for correction.

(2) Certain measures regarding foreign financial subsidiaries (limited to companies whose main business is the insurance business) will be introduced.

(3) Formulation of related rules

Revisions similar to the ones described above will be implemented with regard to foreign subsidiary income inclusion taxation rules relating to residents and special rules concerning the taxation of income relating to foreign related companies of domestic companies which are specially-related shareholders.

8. Application period

(1) The above revisions (excluding 2., 6., and 7. (1)) are applicable to the income inclusion taxation of the fiscal years of domestic companies ending on or after 1 April 2019 (limited to the fiscal years of foreign related companies beginning on or after 1 April 2018).

(2) Revisions 2. and 6. above are applicable to the fiscal years of foreign related companies beginning on or after 1 April 2019.

(3) The above revision described in 7. (1) is applicable to corporation taxes of domestic companies whose submission deadlines for final tax returns are on or after 1 April 2019.

The “Outline of METI’s FY2019 Tax Reform Requests” published by the Ministry of Economy, Trade and Industry on 31 August 2018 mentions that “the US federal corporation tax rate was reduced from 35% to 21%,” “in US business, joint businesses are commonly conducted with business entities such as limited liability companies (LLC) and limited partnerships (LP), which can be established by following relatively simple procedures and whose management methods can be decided with flexibility,” and “shell companies are utilized for business purposes.” Therefore, it is thought that these revisions were implemented in view of requests to implement revisions to deal with the following concerns.

• Exceedingly large tax burden levied through income inclusion taxation which deviates from the actual situations of companies (including the application or non-application of foreign tax credits)

• Determination of shell companies

• Exceedingly large administrative burden in relation to the calculation of income and taxes

The revisions of the scope of shell companies and the calculations of the applicable income amount, effective tax rates and foreign tax credits for companies employing consolidated tax payments and pass-through treatments - topics of great interest to companies - are applicable to the income inclusion taxation of the fiscal years of domestic companies ending on or after 1 April 2019. As a result, these provisions will generally be applicable from the first fiscal year of the new taxation system established by the FY2017 tax reform.

Revision of foreign corporation taxes eligible as foreign tax creditsAdded to the amount of foreign corporation taxes not eligible as foreign tax credits (i.e. taxes imposed on amounts not recognized in Japan as income) will be certain amounts of foreign corporation taxes imposed upon the deemed payment of dividends to domestic companies; other necessary measures will also be introduced.

20 | Japan tax newsletter 4 February 2019

Individual income taxation and asset taxation

Individual income taxation1. Expansionofthescopeofpersonscoveredbyqualified

stock options rules

The scope of covered persons will be expanded to include highly skilled professionals who contribute to companies as an external party (external collaborators) in accordance with a “new business domain development plan (name tentative)” for which a “certified new small or medium enterprise, etc. (name tentative)” has received certification as stipulated in the Small and Medium-sized Enterprises Business Enhancement Act.

2. Usability improvements to the NISA scheme

Certain procedures will enable the continued use of NISA accounts while NISA account holders are away from Japan in circumstances wherein said account holders temporarily leave the country due to unavoidable reasons such as overseas transfers, etc. In addition, in accordance with the revision of the Civil Code, the minimum age required to open an account will be lowered to 18 years of age.

3. Other

(1) Revision of the hometown tax donation program (furusato nozei)

For the healthy expansion of the hometown tax donation program, and for the program to contribute to the revitalization of rural areas across the country as a result of the creativity of local governments expressed within the framework of certain rules, local governments meeting the following criteria will be designated as the organizations eligible for the hometown tax donation program.

• Local governments which solicit donations in an appropriate manner.

• Reciprocal gifts are locally produced and valued at 30% or lower of the donated amount.

This revision will apply to donations made on or after 1 June 2019.

Local governments which send excessive gifts and deviate from the intention of the program will be ineligible for the hometown tax donation program.

(2) Expansion of the scope of measures for the non-imposition of inhabitants tax

To combat child poverty, those fathers or mothers of children receiving the payment of child-rearing allowances whose total income in the prior year is JPY1.35 million or less and who are either a) not presently married or b) in circumstances wherein it is unclear whether their spouse is still living, will be added to the persons eligible for the measures for the non-imposition of individual inhabitants tax. This revision will apply to individual inhabitants tax for FY2021 and thereafter.

Asset taxation1. Establishment of business succession tax rules for

sole proprietors

Following the comprehensive revision to expand the scope of the business succession tax rules relating to non-listed shares, etc. which occurred during the 2018 tax reform, rules creating deferment or exemption for the payment of inheritance tax and gift tax in circumstances wherein a successor acquires assets for business use (excluding assets for use in a real estate lending business) through gifting or inheritance and continues the business will be established to foster the succession of the businesses of sole proprietors.

The new tax payment deferment or exemption rules are time-limited measures lasting for a 10-year period (from 1 January 2019 to 31 December 2028), and the residential land for business use (the portion thereof up to 400 m²), buildings (the portion thereof up to 800 m2 of floorspace) and certain depreciable assets of decedents filing blue tax returns are eligible therefor. The portions of inheritance tax and gift tax eligible for payment deferment or exemption are each respectively 100%, and the provision of collateral is a requirement.

Furthermore, an election may be made between these rules and the “special measures for the calculation of the taxable value for inheritance tax purposes of small-scale residential land (specified residential land used for business)”.

21Japan tax newsletter 4 February 2019 |

In addition, the provisions of these rules will be drafted in accordance with the business succession tax rules relating to non-listed shares, etc., and the submission of succession plans to an applicable prefecture during the period from 1 April 2019 to 31 March 2014 will be required in order to receive their application.

Sole proprietors age 70 or older are predicted to number approximately 1.5 million in 2025, and it is thought that the majority thereof have not yet determined a successor. As the pace of the aging of the population continues to increase, ensuring the continued development of businesses through smooth generational transitions is imperative.

2. Revision of the special measures for small-scale residentiallandinrelationtospecifiedresidentiallandused for business

To prevent the application of the measures in a manner which deviates from the original intention thereof, such as surges in application of the measures for the purpose of tax savings, residential land used for business purposes within three years prior to the start of an inheritance will be excluded from the scope of specified residential land used for business.

These revisions will apply to inheritance tax relating to assets acquired due to inheritance, etc. on or after 1 April 2019. However, residential land used for business purposes since prior to said date and residential land whose value of depreciable assets used for business located on said residential land is 15% or greater than the inheritance tax valuation amount of said residential land will remain items that are not excluded from the scope of specified residential land used for business.

3. Revision of the business succession tax rules relating to non-listed shares

The following revisions to the tax payment deferment or exemption rules concerning inheritance tax and gift tax relating to non-listed shares, etc. took place.

(1) Easing of revocation criteria

In circumstances wherein, due to unavoidable circumstances, a company certified for succession qualifies as an asset holding company or an asset

management company, if said company no longer qualifies as either of the two aforementioned types of companies within 6 months from the date in which it initially qualifies as such, said company will be treated as if it had not met the conditions for the revocation of the tax payment deferment or exemption.

(2) Lowering of the age requirement

The requirement for the age of the recipient of a gift for the purpose of the payment deferment or exemption of gift tax will be lowered from the current 20 years of age to 18 years of age.

(3) Simplification of procedures

Procedures will be simplified, such as no longer requiring attachments of the “Notice of Exemption from Payment Deferment of Gift Tax” in the event of the death of the grantor of non-listed shares and in case the successor applies for the payment deferment or exemption of inheritance tax.

4. Addition of requirements for lump-sum gifts of funds for education, weddings and childcare

From the perspective of ensuring equal opportunity and thereby preventing the entrenchment of inequality, important revisions including the addition of income requirements for gift recipients (i.e., the total income of gift recipients must be JPY10 million or less), the scope of funds for education and other important matters will occur, and the period of application therefor will be extended by 2 years.

5. Alignment of tax law regulations in accordance with the revision of the Civil Code

(1) Method of evaluating spousal rights of residence

Reforms to the Civil Code were published on 13 July 2018; included therein as a policy to protect the rights of spouses to a residence, from the perspective of responding to changes in society and out of consideration for the livelihoods of surviving spouses, were spousal rights of residence. In accordance with the foregoing, the methods of evaluating spousal rights of residence for inheritance tax purposes will be stipulated.

22 | Japan tax newsletter 4 February 2019

(i) Spousal rights of residence

Value of the

building for inheritance

tax purposes

-

Value of the

building for inheritance

tax purposes

×

Remaining useful life

(*1) -

Duration of rights

(*2)(*3) ×

Present value multiplicand derived

using compound interest based on the

statutory interest rate prescribed by the Civil Code for the corresponding duration of rights (remaining years)

Remaining useful life(*1)

(ii) Ownership rights to the building (below, “residence”) in which spousal rights of residence have been established

Value of the building for inheritance tax purposes - (minus) the value of the spousal rights of residence

(iii) Rights relating to the use of the grounds of the residence in accordance with the spousal rights of residence

Value of the land, etc. for

inheritance tax

purposes

-

Value of the land, etc. for

inheritance tax

purposes

×

Present value multiplicand derived using compound interest based on the statutory interest rate prescribed by the Civil Code for the corresponding duration of rights (remaining years)

(iv) Ownership rights to the grounds of the residence

Value of the land, etc. for inheritance tax purposes - (minus) the value of the rights relating to the use of the grounds

The aforementioned value for inheritance tax purposes shall be the value for inheritance tax purposes as calculated in the absence of the establishment of spousal rights of residence.

*1. Remaining useful life:

The useful life (for dwellings) of the residence as stipulated in accordance with the Income Tax Act x (multiplied by) 1.5 - (minus) the age of the residence

*2. Duration of rights: The number of years as determined in the following circumstantial categories:

(i) When the period in which the spousal rights of residence continues is the lifetime of the spouse: The average remaining life expectancy of the spouse

(ii) In cases other than A.: The number of years in which the spousal rights of residence continue as determined in an agreement for the division of inherited property (The maximum shall be the average remaining life expectancy of the spouse)

*3. In the event that the remaining useful life or the number of years remaining after deducting the duration of rights from the remaining useful life is zero or less than zero, this amount shall be zero.

(2) Tax law measures implemented in accordance with the lowering of the age of adulthood

The requirements for the age of gift recipients under the gift tax rules and the tax credit for minors in the inheritance tax rules will be lowered from the current 20 years of age to 18 years of age.

These reforms will be applied to inheritance tax and gift tax relating to assets acquired due to inheritance or gifting on or after 1 April 2022.

23Japan tax newsletter 4 February 2019 |

Tax administration/Other1. Preparation of information query procedures

(1) Requests for cooperation from business operators

The ability of tax authority employees to make requests to business operators (persons/entities; same hereinafter) for the viewing or provision of ledgers, documents and other objects, or for other types of cooperation which may be of reference in relation to a national tax audit will be clarified in the laws and regulations.

(2) Requests for reports from business operators

The ability of the Commissioner of a Regional Taxation Bureau to, upon fulfillment of all of the following conditions, request that a business operator report the names or titles, addresses or residences, and individual numbers or corporate numbers of specified transaction parties (unspecified persons/entities conducting transactions with said business operator) by a certain date will be prescribed.

• In relation to the national tax of specified transaction parties, there is a high likelihood that a correction decision will be required

• It would be difficult to identify the specified transaction parties without the request of such a report

In case a request for a report is made, consideration will be given to the administrative burden placed on the business operator, and a document listing reporting items will be sent to said business operator. Business operators will be allowed to file appeals.

(3) Applicability

The aforementioned revisions will be applied to requests for cooperation or reports beginning on or after 1 January 2020.