Strictly private and confidential - Disclaimer This presentation has been prepared by Hiroshi Hashimoto for delivery on Wednesday 5 April 2017 at the Gastech 2017

Makuhari Messe Chiba, Japan. It has not been prepared for the benefit of any particular attendee and may not be reliedupon by any attendee or other third party. If, notwithstanding the foregoing, this presentation is relied upon by any person,Hiroshi Hashimoto does not accept, and disclaims, all liability for loss and damage suffered as a result.

The presentation may contain forward-looking statements concerning some companies’ or organisations' strategy,operations, financial performance or condition, outlook, growth opportunities or circumstances in the countries, sectors ormarkets in which those entities operate. By their nature, forward-looking statements involve uncertainty because theydepend on future circumstances, and relate to events, not all of which can be controlled or predicted.

Although Hiroshi Hashimoto believes that the expectations reflected in such forward-looking statements are reasonablyreasonable, no assurance can be given that such expectations will prove to have been correct. Actual results could differmaterially from the guidance given in this presentation for a number of reasons. For a detailed analysis of the factors thatmay affect somebody’s business, financial performance or results of operations, Hiroshi Hashimoto urges you to thinkyourself very carefully.

Nothing in this presentation should be construed as a profit forecast and no part of this presentation constitutes, or shallbe taken to constitute, an invitation or inducement to invest in any specific entity, and must not be relied upon in any wayin connection with any investment decision. Hiroshi Hashimoto undertakes no obligation to update any forward-lookingstatements.

No representation or warranty, express or implied, is or will be made in relation to the accuracy or completeness of theinformation in this presentation and no responsibility or liability is or will be accepted by Hiroshi Hashimoto andassociated persons in relation to him.

These slides and the contents of this presentation may not be disclosed to any other person or published by any meanswithout Hiroshi Hashimoto’s prior written permission and related monetary compensation to him.

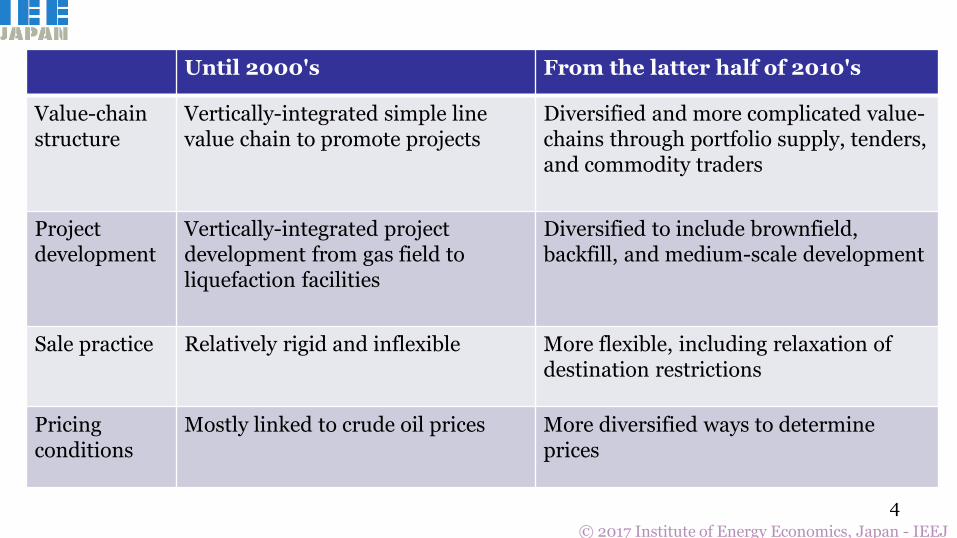

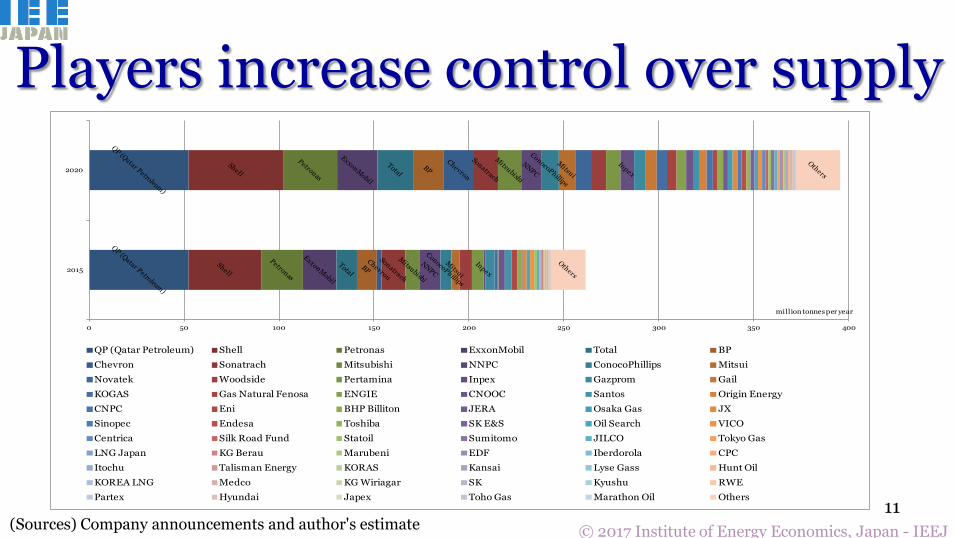

The global LNG market is undergoing a structural shift

3

Until 2000's From the latter half of 2010's

LNG supply sources

Developed mainly in Southeast Asia, Oceania, Middle East and Africa

Major expansion in Australia and the United States The United States remains as the largest consumer of gas in the world and becomes one of the largest LNG exporters in the world

LNG consuming markets

Developed in industrial nations in North Asia and Europe, followed by India and China

Market saturation in traditional importers and new markets emerging in Latin America, Southeast Asia, the Middle East and Africa

Status of LNG Premium energy and natural gas supply source

A major driving force to expand new natural gas demand (including newly emerging markets and emerging demand sectors)

• At the height of the Asian and Japanese premium of LNG prices in 2013

– The main cause of the unfavourable LNG prices (for the buyers at that time) were thought to be:

• the lack of its own pricing system that can reflect supply and demand balance of LNG in the region; and

• the lack of an actively traded market.

• During the last five years LNG players in the region, mostly LNG buyers, as well as government authorities, have discussed how they can develop such an LNG market in the region

14Thank you for your attentionContact: Hiroshi Hashimoto [email protected]

Japan’s LNG market continues evolving with larger and more flexible LNG supply options with different pricing Japan’s LNG users (electric power and city gas utility companies) enter each others’

markets, at the same time as different pricing and diversification of the global LNG market.

The greater flexibility should be enhanced from the LNG supply in the global market and the energy distribution system within the domestic market.

Anticipated partnerships and consolidations, as well as different mindsets, will alter faces of players.

Japan (and Asia) should be able to take advantage of their own market positions and information assets to establish their own equitable and fair LNG market.

An LNG hub does not necessarily mean a spot trading hub but can be a combination of more flexible term contracts and enhanced spot trading.