Our ServicesWith recent changes in the tax code including the extension and expansion of bonus depreciation and §179 expensing elections there has never been a better time to have a cost segregation study completed. In addition, new laws enacted by Congress and regulations issued by the Internal Revenue Service now enable taxpayers to take further tax advantage of their real estate holdings. At MS Consultants, LLC we refer to it as & More.

1-Cost Segregation Studies (CSS)

• Internal Revenue Service (IRS) approved methodology to properly classify assets into 5,7,15, 27.5 and 39 year depreciable lives

• Taxpayers may go back as far as 1987 to claim any missed depreciation (No amended returns are required)

• MS Consultants has completed over 12,000 studies since 1996

In 2015 a CSS was completed on a $3,000,000 retail plaza (originally placed in service in 2010) and resulted in additional depreciation of over $450,000 in 2015.

• Identify assets eligible for an immediate write off. IRS rules now allow for the immediate expensing of expenditures typically under $2,500 per unit of property (UOP)

• The de minimis safe harbor is an elective provision that requires guidance in invoice preparation and knowledge of unit of properties and building systems

An $800,000 hotel renovation was completed in 2015. A de minimis study resulted in over $500,000 eligible for expensing in 2015.

2-De Minimis Studies

6/14/2017

4

3-Fixed Asset Studies (FAS)

• For assets abandoned or physically removed from a building, the IRS now allows taxpayers to write‐off the remaining net tax value of the asset typically resulting in a large tax deduction

• Opportunities to expense current year expenditures for roofs, windows, HVAC and other structural components as a result of the IRS Tangible Property Regulations (TPR)

A $4,000,000 renovation of retail plaza was completed in 2015 (originally placed in service in 2002). The study resulted in expensing over $600,000 of removed assets. In addition, approximately $400,000 of the 2015 expenditures were deemed to be repairs under the TPR and were expensed in 2015.

• Up to $1.80 per square foot tax deduction for increasing the energy efficiency of HVAC, lighting, and building envelope that meet prescribed energy use reduction standards established by the IRS

• Architects, designers and engineering firms can receive tax deduction for providing services to a government owned building

A 90,000 square foot office building was constructed in 2013. The project met the energy use reduction standards resulting in a $162,000 tax deduction in 2013.

4-§179D Energy Efficient Commercial Building Tax Deduction

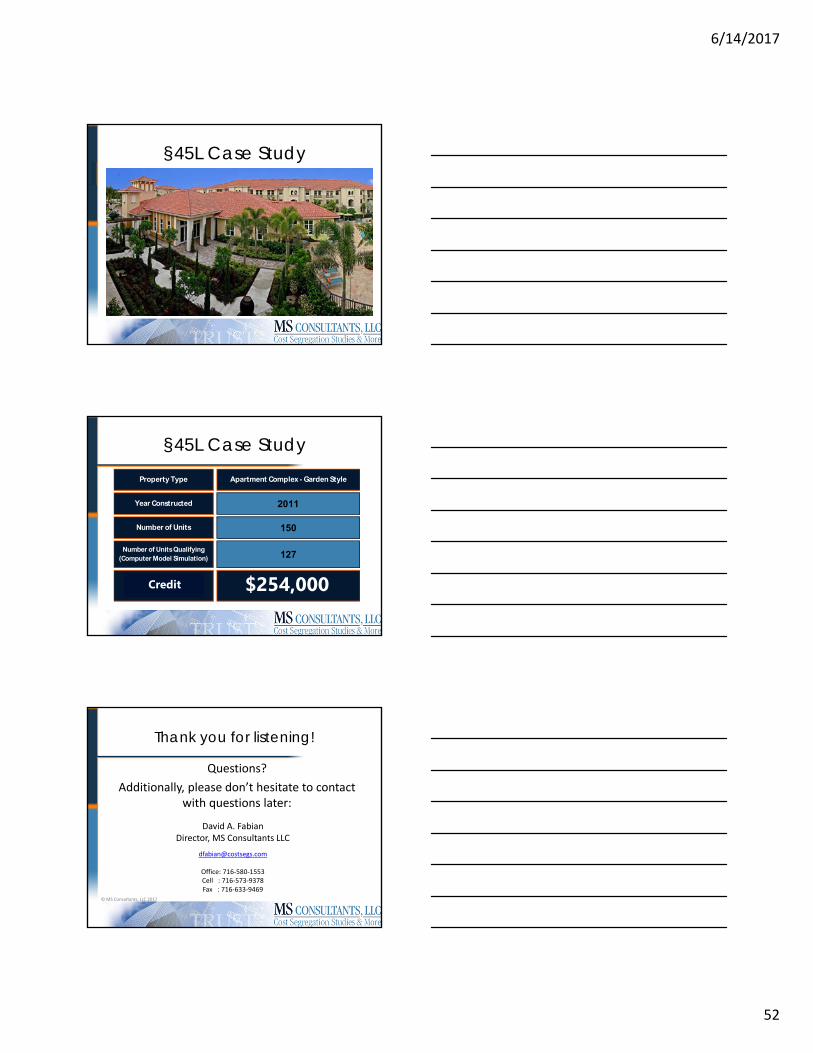

5-§45L Energy Efficient Home Credit (Great for Apartments)

• Up to a $2,000 tax credit per dwelling unit that meets prescribed energy use reduction standards established by the IRS

• Includes apartment buildings, adult care facilities, single and multi‐family residences

A 120 unit garden style apartment complex was constructed in 2014. The project met the prescribed energy use reduction standards resulting in $240,000 of tax credits in 2014

6/14/2017

5

6-§1031 Exchange Tax Planning (We are not an intermediary)

• Opportunity to complete a CSS and FAS on a building before it is sold and the election is made to complete a §1031 Exchange. Typically results in tax deduction prior to sale

• This will increase the gain on sale but the gain is being deferred anyway as a result of the §1031 Exchange

MS Consultants performed a CSS in 2015 on an office building (originally placed in service in 2003) sold (exchanged) in 2016 resulting in a 2015 tax deduction of $400,000.

What are the benefits of Cost Segregation Studies, cont?

‐ No amended return for catch‐up depreciation ‐ Savings taken all in one year‐ Taxpayers receive an extra 30% ‐ 100% on “non‐real estate” assets (for assets acquired after 9/11/01)

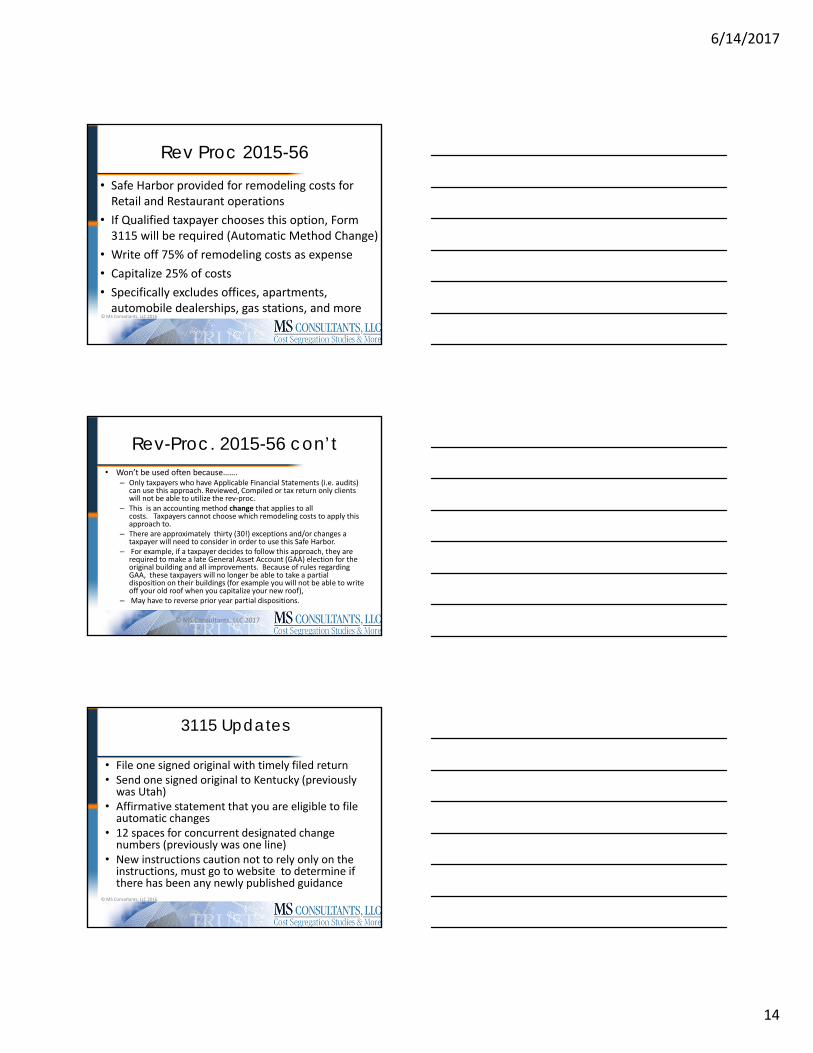

Rev-Proc. 2015-56 con’t • Won’t be used often because…….

– Only taxpayers who have Applicable Financial Statements (i.e. audits) can use this approach. Reviewed, Compiled or tax return only clients will not be able to utilize the rev‐proc.

– This is an accounting method change that applies to all costs. Taxpayers cannot choose which remodeling costs to apply this approach to.

– There are approximately thirty (30!) exceptions and/or changes a taxpayer will need to consider in order to use this Safe Harbor.

– For example, if a taxpayer decides to follow this approach, they are required to make a late General Asset Account (GAA) election for the original building and all improvements. Because of rules regarding GAA, these taxpayers will no longer be able to take a partial disposition on their buildings (for example you will not be able to write off your old roof when you capitalize your new roof),

– May have to reverse prior year partial dispositions.

– New safe harbor determined at invoice item level.

– A taxpayer may rely on de minimis safe harbor only if the amount paid for property does not exceed $2,500 per invoice, or per item as substantiated by the invoice. Limit is $5,000 if AFS applies

• The de minimis safe harbor does not preclude a taxpayer from reaching an agreement with the IRS that the IRS examining agents will not review certain items‐same as Temporary regs

• Must apply same treatment to books and tax return

• A taxpayer is not required to include in the cost of the property the additional costs if these costs are not included on the same invoice as the tangible property

• However, a taxpayer electing the de minimis must include in the cost of the property all additional costs (for example, delivery fees, installation services, or similar costs) of acquiring or producing the property if these costs are included on the same invoice with the tangible property

• For tax years beginning _________, and forward, (Name of Business) elects to treat as an expense for both book and income tax purposes property with a cost of $____________ or less, including items that have a useful life of 12 months or less. It is (Name of Business’s) intention that this election complies with the IRS Section 1.263(a)‐1(f) de minimis safe harbor election.

• Building and its structural components are a single UOP

– The regulations define the building structure as the building (as defined in §1.48‐1(e)(1)) and its structural components (as defined in §1.48‐1(e)(2)) other than the components specifically enumerated as building systems.

• This new term consists of the following nine structural components. Each of them (including their sub‐components) is a building system that is separate from the building structure, and to which the improvement rules must be separately applied:

At the end of the day you end up with

• Building structure: roof, walls, floors, windows, doors, etc. and

• UOP for assets other than buildings. In general, for real or personal property that isn't classified as a building by the temp regs. all the components that are functionally interdependent comprise a single UOP. Components of property are functionally interdependent if the placing in service of one component by the taxpayer is dependent on the placing in service of the other component by the taxpayer.

BETTERMENT of the Unit of Property• 1‐ Ameliorate a material condition or defect that existed

prior to the acquisition of the property or arose during the production of the property.– Example 2: Taxpayer bought a store that had previously been used as a gas

station, located on land that had contained underground gasoline storage tanks. At the time of purchase, taxpayer did not know that the tanks had leaked, causing soil contamination. In 2012, taxpayer discovered the contamination and incurred costs to remediate the soil

• Result = Costs are CAPITALIZED (The remediation costs result in a betterment of the land, because the costs ameliorate a material condition or defect that existed prior to the taxpayer’s purchase of the land. Because there is a betterment, there is an improvement, and therefore is a capitalized cost.)

• 2‐ Material addition to the unit of property (including the physical enlargement, expansion, or extension);– Example 1: Taxpayer owns a 100,000 SF manufacturing building

that needed to extend the production area for their growing business. They construct a 30,000 SF addition.

• 3‐ Material increase in the capacity, productivity, efficiency, strength, or quality of the unit of property or its output– Example 1: Taxpayer owns a factory building with a storage area

on the 2nd floor, they replace columns and girder supports to permit greater weight capacity in the area for new products.

• A taxpayer must capitalize amounts paid to restore a unit of property, including amounts paid in making good the exhaustion for which an allowance is or has been made.

RESTORATION of the Unit of Property‐con’t• 1. Replacement of a component of a UOP and the taxpayer

has properly deducted a loss for that component;

• 2. Replacement of a component of a UOP and the taxpayer has properly taken into account the adjusted basis of the component in realizing gain or loss resulting from the sale or exchange of the component;

RESTORATION of the Unit of Property‐con’t• 3. Repair of damage to a UOP for which the taxpayer has

properly taken into account the basis adjustment as a result of a casualty loss under Sec. 165 or relating to and event described in Sec. 165;‐different from old casualty rules

• 4. Returns the UOP to its ordinarily efficient operating condition if the property has deteriorated to a state of disrepair and was no longer functional for its intended use;

Remodeling ExpendituresBuilding Refresh; Limited Improvement (ex. B7) –refresh the look and layout, along with adding building addition for additional storage space and loading dock. In order to accomplish this, the store:

– All of the above, plus

– Add the storage space and loading dock

– Expand the electrical system for the new additionRESULT =

– Refresh costs are EXPENSED (not a Betterment)

– Building Addition costs are CAPITALIZED (Structural/Building system)

Remodeling ExpendituresBuilding Remodel (Ex. B8) – upgrade the look and layout to compete for a different type of customer. In order to accomplish this, the store:

– Replace flooring

– Replace large parts of exterior walls to insert windows

• If a TP expends costs in consideration of capitalization issues, the TP will go through the following “filters”

1. De minimis application (will not be on depreciation schedule)2. Are the costs indirect or removal and not capital in nature? 3. Are the costs M&S?4. Are they safe harbor for small taxpayers?5. Are they routine maintenance costs?6. Are they betterments, improvements, adaptions, restorations?

If not, they are R&M7. If the above do allow a 162, does the taxpayer elect to

capitalize?8. Section 179? (will be on depreciation schedule) 9. Bonus? (will be on depreciation schedule)

1250 Property - Options• Expense under unofficial IRS 33% rule• Expense under “traditional” repair rules

– (A sewer repair is still a sewer repair)

• Expense under Routine Maintenance Safe Harbor• Expense under 179, if qualified property• Expense removal or demo costs with Change #21• Expense or Capitalize based on new capitalization

standards – (Betterment, Restoration, Adaptation)

• Capitalize, and depreciate over 27.5 or 39 years• Capitalize with Bonus, if applicable

Depreciation Today

• PATH Act of 2015– Signed December 18, 2015

– Extends Bonus Depreciation

• 50% deduction on qualified assets acquired & placed in service in 2015 through 2017

• Applies to most qualified tangible personal property and land improvements, as well as qualified leasehold improvements

• Internal Structural Framework• Regs. Sec. 1.48‐12

– (3) DEFINITION OF INTERNAL STRUCTURAL FRAMEWORK. For purposes of this section, the term “internal structural framework” includes all load‐bearing internal walls and any other internal structural supports, including the columns, girders, beams, trusses, spandrels, and all other members that are essential to the stability of the building. (THIS MEANS MOST IMPROVEMENTS ARE ELIGIBLE such as drywall, plumbing, electric, etc…)

–An improvement to a building, if more than 50% of the building's square footage is devoted to preparation of, and seating for on‐premises consumption of, prepared meals.

• An internal improvement (structural component) that benefits a common area does not qualify for a 15‐yr recovery period in the case of a leased building property or a retail building. HOWEVER, QI property does not contain this restriction. Therefore, such an internal improvement to a common area may nevertheless qualify for bonus depreciation as qualified improvement property.

Section 179 PlanningFor taxable years beginning in 2015, the provision extends the limitation on carryovers and the maximum amount available with respect to qualified real property of $250,000.

The provision removes the limitation related to the amount of section 179 property that may be attributable to qualified real property for taxable years beginning after 2015.

What is §179D?• A tax deduction for energy‐efficient expenditures made

to depreciable commercial, government/municipal, or large (3+ stories) residential buildings that reduce energy use by 50% compared with similar structure built to ASHRAE/IES Standard 90.1‐2001.

• NOTE: Beginning in 2016 a taxpayer must utilize ASHRAE/IES Standard 90.1‐2007. SET to EXPIRE in 2016

• Maximum deduction: $1.80/SFPartial deductions allowable of $0.60/SF for buildings that do not meet overall threshold but have systems which are individually energy efficient

What qualifies under §179D?• Buildings constructed or improved between January 1, 2006 and December 31, 2016 are eligible for deductions

• Owner of a building, or lessee who installs energy‐efficient systemsIf multiple taxpayers install energy‐efficient systems in the same building, the deduction may be split between them, as long as the total deduction does not exceed the maximum $1.80/SF

Energy Efficient Systems• HVAC Systems that Tend to Qualify:

– Geothermal– Thermal Storage– High Energy VRF Units– Centralized HVAC in Apartments– Energy Recovery ventilation– Chillers (buildings > 150,000 SF)– Direct Fired Heaters– VAV (Variable Air Volume) in smaller buildings– Chilled Beam– Magnetic Bearing Chillers– Gas‐fired Chillers Combined with electric chillers

• Colleges‐State University of New York at Buffalo

• Municipal Buildings‐Macon County Administration Building.

Government Buildings do not include:

• Not‐for‐profit tax‐exempt entities

• Colleges ‐ Harvard doesn’t, Arkansas does

• Schools ‐ Pace Academy for the Arts doesn’t, School 54 does

6/14/2017

49

§179D for architects and designers

• With Notice 2008‐40, the IRS solidified its rules allowing architects, designers, and builders to take advantage of §179D for government‐owned buildings. Because of this, we’ve seen a large influx of these projects.

• Any project built since 2006 could potentially qualify, and most modern buildings qualify for at least one of the three systems