Registered with the Lisbon registrar of Companies under 8.122 Share Capital: 479.293.220 Euros - Corporate Tax No. 500 100 144 Rua Tierno Galvan, Torre 3, 9º , Letra J - 1099-008 Lisboa Jerónimo Martins, SGPS, S.A. Public Company Consolidated Financial Statements At 31 December, years 2003 and 2002 (With Report of the Statutory Auditors)

Transcript

Registered with the Lisbon registrar of Companies under 8.122 Share Capital: 479.293.220 Euros - Corporate Tax No. 500 100 144 Rua Tierno Galvan, Torre 3, 9º , Letra J - 1099-008 Lisboa

Jerónimo Martins, SGPS, S.A.

Public Company

Consolidated Financial Statements

At 31 December, years 2003 and 2002

(With Report of the Statutory Auditors)

Jerónimo Martins, SGPS, S.A.

2

Table of Contents

Chairman’s Message

I. Jerónimo Martins Group

1. Group Profile and Positioning

2. Corporate Bodies

3. Business and Ownership Structure

4. Management Structure

5. Operational and Financial Highlights

6. Key Relevant Facts

II. Corporate Governance

Chapter 0. Declaration of Compliance

Chapter 1. Disclosure of Information

1.1. Organizational Structure and Sharing of Powers

1.2. Specific Company Committees

1.3. Risk Control System

1.4. Share Price Performance

1.5. Dividend Distribution Policy

1.6. Stock Option Plan

1.7. Business between Members of the Board and the Company

1.8. Investor Relations Office

1.9. Remuneration Committee

1.10. Amount of Annual Remuneration Paid to External Auditor

Chapter 2. Exercise of Shareholder Voting and Representation Rights

2.1. Statutory Rules on the Exercise of Voting Rights

2.2. Postal Voting

2.3. Electronic Voting

2.4. Requirements in terms of Deadline for the Deposit or Blocking of Shares

2.5. Required Deadline for Receiving Votes sent by Post

2.6. Number of Shares Corresponding to One Vote

Chapter 3. Company Rules

3.1. Code of Conduct and Internal Regulations

3.2. Measures Likely to Interfere with Public Tender Offers

Chapter 4. Board of Directors

4.1. Description of Board of Directors

4.2. Executive Committee

4.3. Structure and Role of Board of Directors

4.4. Remuneration Policy of Board of Directors

4.5. Remuneration of Members of the Board of Directors

Page 5

Page 7

Page 7

Page 8

Page 10

Page 11

Page 12

Page 17

Page 19

Page 19

Page 19

Page 19

Page 21

Page 22

Page 23

Page 27

Page 27

Page 28

Page 28

Page 29

Page 29

Page 29

Page 29

Page 29

Page 29

Page 30

Page 30

Page 30

Page 30

Page 30

Page 30

Page 30

Page 30

Page 32

Page 32

Page 33

Page 33

Jerónimo Martins, SGPS, S.A.

3

III. Consolidated Management Report

1. Macro Economic Environment

1.1. World Economy

1.2. Portugal

1.3. Poland

2. Industry Outlook

2.1. International Food Distribution Market

2.2. Food Retail Market – Portugal

2.3. Wholesale Food Market – Portugal

2.4. Food Retail Market – Poland

3. Overview of Group’s Consolidated Activity

3.1. Consolidated Sales

3.2. Operational Results

3.3. Debt and Financial Results

3.4. Net Results and Cash Flow

3.5. Return Analysis

4. Operating Activity

4.1. Functional Areas of the Holding

4.2. Food Distribution - Portugal

4.2.1. Operating Divisions

4.2.2. Functional Areas of the Operation

4.3. Food Distribution - Poland

4.4. Manufacturing

4.5. Services

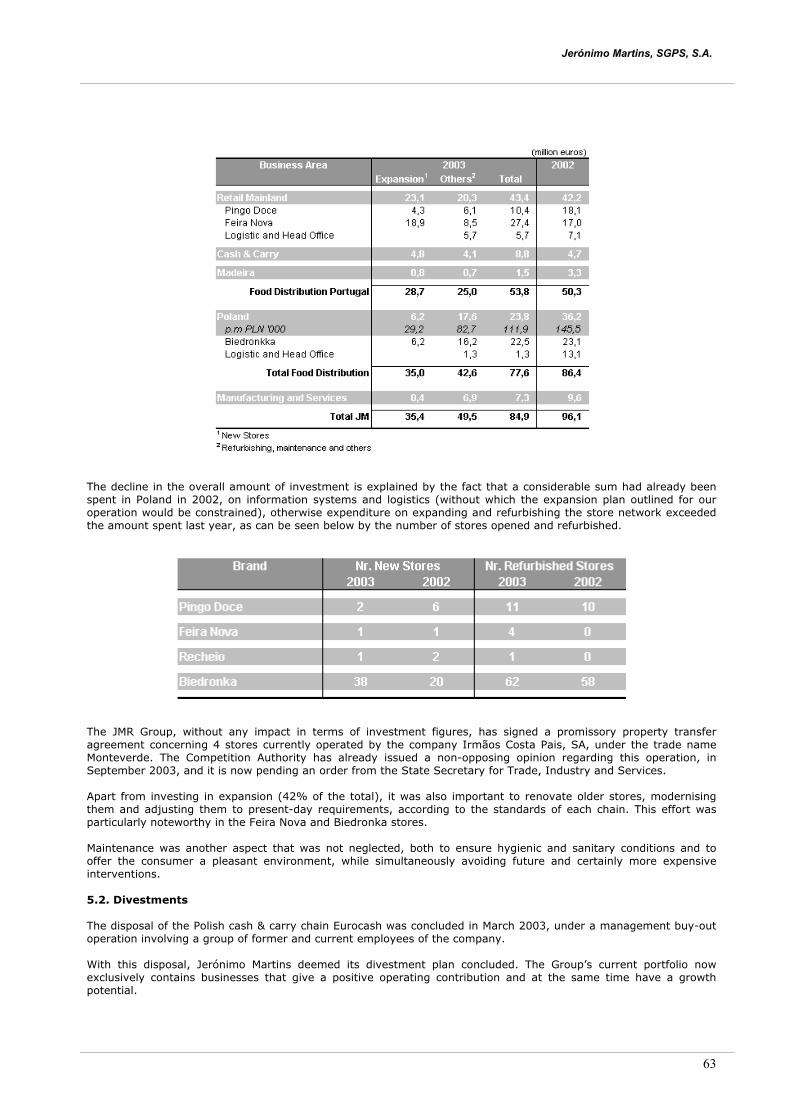

5. Group’s Investment Programme

5.1. Investment

5.2. Divestment

6. Outlook for 2004

7. Events after Balance Sheet Date

8. Proposed Application of Results

Consolidated Management Report Annex

• Information concerning the shares held in the Company by Members of the Board of Directors and Statutory Auditor as at December 31st 2003

• List of shareholders with qualifying shares as at December 31st 2003

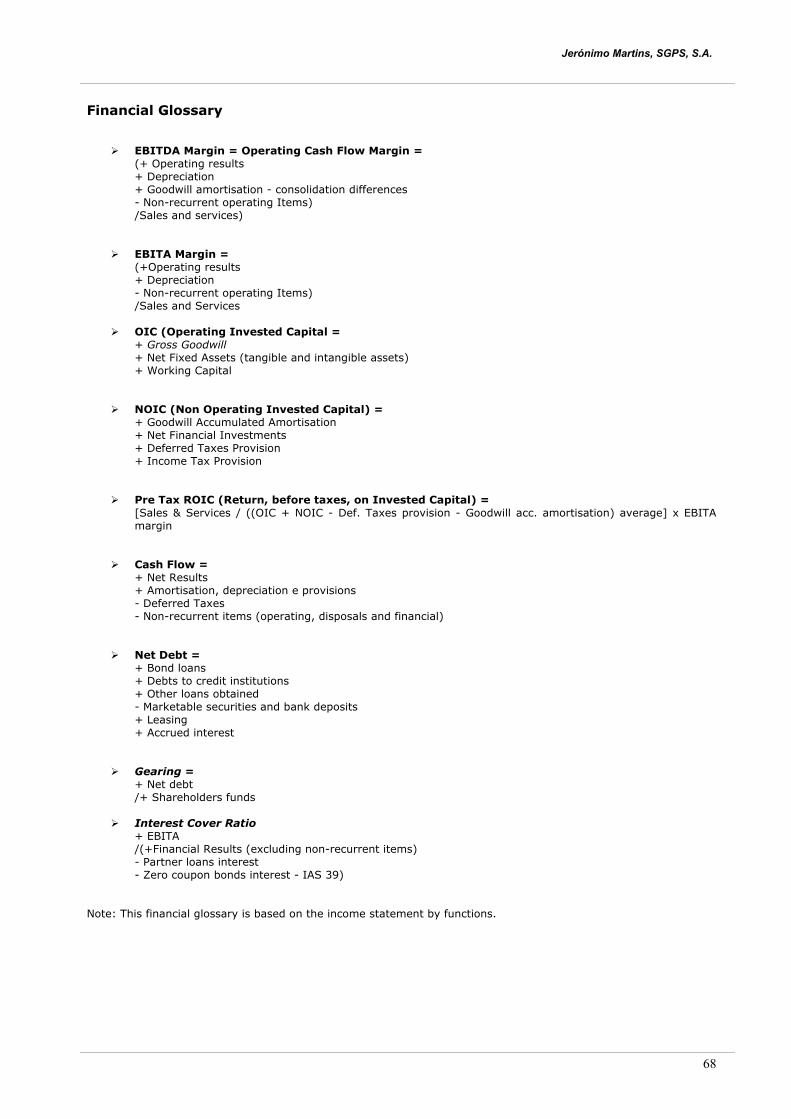

• Financial Glossary

Page 34

Page 34

Page 34

Page 34

Page 34

Page 35

Page 35

Page 35

Page 36

Page 36

Page 37

Page 37

Page 38

Page 40

Page 41

Page 43

Page 44

Page 44

Page 50

Page 50

Page 53

Page 57

Page 58

Page 61

Page 62

Page 62

Page 63

Page 64

Page 65

Page 65

Page 66

Page 66

Page 67

Page 68

Jerónimo Martins, SGPS, S.A.

4

IV. Social Responsibility

1. Code of Conduct

2. Human Resources

2.1. Recruitment

2.2. Working Conditions, Remuneration and Social Benefits

2.3. Training and Personnel Development

3. Food Quality and Safety

3.1. Distribution

3.1.1 Strict Control of Stores and Distribution Centres

3.1.2 Supporting Rigour in Production

3.1.3 Monitoring Rigour in Private Labels

3.1.4 Investing in Knowledge Sharing

3.2. Manufacturing

3.2.1. Investing in a Rigorous Quality System

3.2.2. Quality System Stages and Processes

4. Environmental Management

4.1. Environmental Policy

4.2. Main Environmental Impacts

4.2.1. Distribution

4.2.2. Manufacturing

4.3. Environmental Management Programmes

4.3.1. Distribution

4.3.2. Manufacturing

5. Patronage

5.1. Social Patronage

5.2. Cultural Patronage

V. Consolidated Financial Statements

1. Consolidated Financial Statements

2. Auditors’ Report

Page 69

Page 69

Page 69

Page 70

Page 71

Page 73

Page 75

Page 75

Page 75

Page 76

Page 76

Page 77

Page 77

Page 77

Page 78

Page 78

Page 78

Page 79

Page 79

Page 79

Page 79

Page 79

Page 81

Page 84

Page 84

Page 87

Page 88

Page 89

Page 129

Jerónimo Martins, SGPS, S.A.

5

Chairman’s Message

Dear Shareholder, It is with great pleasure that I begin by saying that 2003 brought back the success that for so long has characterised Jerónimo Martins. The decisions taken to solve the problems that had affected the Group over the last decade have proved to be the right ones and we can now look to the future with renewed optimism, strengthened by experience and by a common vision as to what we want and where we are going. This is the beginning of a new era for the whole Group and we wanted to mark it by renewing the corporate identity. The new Jerónimo Martins image, launched in 2004, is a symbol of a unified, dynamic Group governed by strict ethical principles of professionalism and transparency and one that implements socially responsible practices. A Group that relies on the capitalisation of its extensive experience and is fully aware that its place in the future can only be guaranteed by continuous improvement based on solid, clear values. In 2003, Jerónimo Martins consolidated sales totalled 3,4 billion euros, with a net profit of 58,2 million euros, attaining an all-time peak in terms of cash flow. Operating cash flow totalled 289,6 million euros, corresponding to a 1.7 p.p. rise in the EBITDA margin. The decline in the total margin of the comparable portfolio by 0.5 p.p. was the result of the higher weight of Distribution in the sales mix, particularly of the Discount format, and also the huge competitive pressure in both Portugal and Poland. This performance reflects the intense work developed and carried out at the operational level, in all Group Divisions and its functional support areas, an effort that clearly constituted the strategic focus. In Food Distribution, the retail business in Portugal remained steady in a very negative economic environment, through continuing commercial aggressiveness and cost containment that was carried out for the second year running. Pingo Doce increased sales by 2%, while Feira Nova, notwithstanding market contraction and the temporary closing down of a significant number of its stores for refurbishment, was able to contain the decline in sales at 0.1%. In terms of store sales, retail business in Portugal increased by 1.1%, the market position being maintained despite the reduced number of openings. An EBITDA margin of 10.1% was posted in spite of adverse market conditions. The Recheio performance was quite remarkable, with substantial gains in the retail and “HoReCa” channels, strengthening its medium-term target to attain leadership in these markets in Portugal. By paying constant attention to cost management, and carrying out projects aimed at increasing growth in geographical areas of greater potential in the “HoReCa” channel, levels of efficiency rose again and operating cash flow (EBITDA) reached a new record high, with an increase of 1 p.p. (percentage of sales). In Poland, Biedronka progressed at the aggressive pace set by the Group. In a year marked by the implementation of a new organisational structure, business fully responded to decision levels coming closer to the market, having achieved substantial market share gains with a growth in sales of 14% in local currency (12% in a like-for-like basis). Due to the continuous improvement in operational efficiency levels, the operating cash flow margin (EBITDA) advanced by 0.8 p.p., despite a drop in the total margin caused by the aggressive behaviour of the market. Manufacturing and Services were favourably affected by the recovery of key markets such as olive oil, favourable weather conditions increased sales of ice cream and beverages, while constant attention was paid to the renewal of the personal and homecare product range. Catering performed excellently and all these facets combined to increase operating cash flow, showing an improvement of over 3% year-on-the year. Having come this far, the important thing is not to forget the lessons learned over the last 15 years, a period during which Jerónimo Martins simultaneously underwent the biggest growth phase in its history and also its most severe restructuring process. The decision to invest in the Food Market as a key area for the Group proved to be a complete success. After attaining leadership in Portugal, both in Manufacturing and Distribution, thanks to an ideal conjunction of activities in the wholesale and retail markets, Jerónimo Martins is today a top reference in this key sector of the national economy. The ability to build long-lasting relationships with international partners, conducted in an atmosphere of mutual respect and through a strategic rationale specific to the businesses in question, has always been one of our greatest strengths. In 1995, the reasons that led us to move into external markets appear even stronger today than they did at the time. The natural limitations of the domestic market have, in fact, now been further exacerbated by restrictions to growth imposed by years of government-led market administration. Poland, however, has confirmed our option for the largest Central European economy, possibly the driving force in the entire European Union enlargement process, whether for political or economic reasons The validity of our options was also revealed at the time of decisions in the disposal process that we had to undertake in 2001 and 2002, and it is further confirmed on a daily basis by the performance of Biedronka. The Group has gained invaluable experience in eight years of intense international activity. We are now a stronger organisation, and one that places great emphasis on keeping control over its various operations. The mistakes made

Jerónimo Martins, SGPS, S.A.

6

during the growth and internationalisation process have also made us more resolute as regards decision making, both at the present time and in the future. We strongly believe in the need to build flexible structures, combining speed of reaction to market proximity. Our decisions are now more strongly founded on known areas, with a management team that combines older members with vast experience with a younger middle management generation that has had close contact with international business realities and intense competitive pressure. Our track record in the discount format will enable us to face with confidence the challenge to deliver strong value-content proposals to the consumer. To this end, every necessary decision will be made to guarantee the highest levels of efficiency in any operating areas in our portfolio. Poland is a firm, definitive investment. The position achieved in this market will be a fundamental growth driver for the Group as a food distributor. Every effort will be put into strengthening business conditions in the East and Southeast of Europe, where we believe there are opportunities to develop operations in areas where Group know-how and, in particular, skills developed in Poland will provide an important competitive advantage. No medium-term growth strategy will be viable, however, unless business stability in Portugal is ensured. The strengthening of the Group position in this market will involve both Distribution and Manufacturing, aimed at addressing the changes in patterns of consumption in today's society. Wherever we are, we will concentrate on the food market. We are now very confident as regards risk and opportunity assessment and clearly want to further optimise our capacities as food operators. Finally, I would like to refer to the important progress made by Jerónimo Martins in 2003 in developing a policy of Social Responsibility as a continuance of work done over the past few years. The Board of Directors is committed to Social Responsibility, for the Company must assume its role in society by becoming a pillar of reference for all its shareholders in these times of uncertainty and rapid social change, where we all have to modify our attitudes not only towards environmental problems, but also to the promotion of the entire development plan. Today, we are more than ever aware that sustainable development is not an option, but the only way to ensure a promising Future, a course of action that entails strict responsible conduct at economic, environmental and social levels. Increasing concerns in the Social Responsibility area plus activities that have been developed over the last three years have led us to organise and formally adopt principles and policies to build focus, concentrate resources and lead the entire Organisation in this matter. The willingness and involvement of all our employees have been key factors in the success of some of the initiatives undertaken, reflecting the importance given to interaction with the community and reiterating Group philosophy, culture and values. Last year, the Board of Directors formally approved the Jerónimo Martins Code of Conduct and Sustainable Development was established as the strategic driver for the food industry, thus reinforcing our earlier decision to join the World Business Council for Sustainable Development. We also joined COTEC Portugal, the Corporate Association for Innovation, as a founder member, and RSE, the Association for Social Responsibility in Corporations. Our concern with Sustainable Development will increasingly be at the core of Group management decisions. It is our sincere belief that in the future there will only be a place for companies that, while delivering economic prosperity and generating value for consumers and shareholders, also integrate sustainability in their management practices and provide an ethically, socially and environmentally responsible attitude that generates value for the whole community. This attitude will govern our business in interactions with various agents and in assessing the satisfaction of customers, shareholders, suppliers and employees, not forgetting supporting underprivileged groups, respecting environmental protection and guaranteeing food quality and safety. As Chairman of the Board of Directors, I must say a word about the particular significance of this year. The position we hold at present resulted solely from the strength of the decisions taken, a strength shared both during the growth and during the restructuring phases. On one hand, this strength stems from the support given by all our shareholders, and, on the other, it comes from the exemplary effort of tens of thousands of Group employees. It is this strength that enables us to face the future with the same determination that led us to build all that we are today. To all those who trusted us and in any way made it possible for us to implement our vision, I wish to express my personal esteem and thanks, and give you our assurance that Jerónimo Martins is committed to the intransigent defence of shareholder interests, and to the construction of a socially responsible economic Group. E. A. Soares dos Santos

Jerónimo Martins, SGPS, S.A.

7

I. Jerónimo Martins Group

1. Group Profile and Positioning Business

The Jerónimo Martins Group has a balanced portfolio, combining the strength of the market positions held by the retail and wholesale operations in Portugal with the potential for growth of the Biedronka operation in Poland and the stability and ability to release cash flow from industrial assets held in partnership with Unilever.

In Portugal, the Group operates retail and wholesale formats, leading the market of fast moving consumer goods distribution through Pingo Doce (Supermarket’s leader), Feira Nova (third Hypermarket operator) and Recheio (second Cash & Carry operator).

In Poland, Biedronka is market leader in its format, clearly ahead of the competition both in the number of stores and brand awareness.

Jerónimo Martins is also the largest industrial Group in Portugal manufacturing fast moving consumer goods, through its joint-venture with Unilever in FimaVG (food products), LeverElida (personal and home care) and IgloOlá (ice cream and frozen food) and retains leadership positions in olive oil, margarine, ice tea, ice cream and laundry detergents, among others.

The Group portfolio also includes Jerónimo Martins Distribuição de Produtos de Consumo, a marketing and distribution services company representing, in Portugal, international brands of fast moving food products and cosmetics, some of which are leaders of their segment, Hussel (specialised retail of chocolates and confectionery) and Jeronymo (pilot-projects in specialised retail).

Mission

Jerónimo Martins is an international group operating in food industry in the distribution, manufacturing and services sectors. Its aims are sustained development of its companies, operational efficiency and generation of value, acting on principles of integrity and social responsibility.

Strategic Focus

To guarantee the sustainability of its current and future business and the return on its capitals, the Group relies on two factors: (1) offering strong value-content proposals and (2) building a solid relationship of trust with consumers, employees, business partners and institutions in general.

Priority is given to consumer needs in conducting business to guarantee the consistent and systematic delivery of strong value-content proposals in each business, country and point in time in terms of price, quality and innovation.

The conduction of business relies on dynamic and flexible organisations with the human resources to ensure the continuity of accumulated know-how and permanent adaptation to change. To this end, the Group has introduced management tools (strategic scorecard) and performance measures (EVA)1 to ensure that the organisation is focused on the strategic challenges, whether financial, market or efficiency related, and on the activities that truly add value.

In the conducting of business, the Group upholds a rigorous, responsible behaviour at the economic, environmental and social level. Social responsibility is a sine-qua-non condition for the sustainability of its companies, namely in terms of Human Resources, Food Quality and Safety, Environmental Protection2 and Patronage.

Jerónimo Martins has always been a standard reference in its sector and in the market in general, and believes that the pursuance of its strategic focus will ensure the delivery of strong value-content proposals to its Shareholders in the short, medium and long term.

Jerónimo Martins’ shares have been listed on the stock exchange since 1989 and are included in the PSI 20 index. On 31st December 2003 there were 95,858,644 listed shares, with a free float of 26.14%.

Identity

The eventful history of Jerónimo Martins dates back to 1792. In more than 210 years, the last decade has been particularly rich in experiences and learning. Today Jerónimo Martins is an international group, with a clear vision of its strategic focus. It is a cohesive, dynamic group, with modern, strict, ethical and transparent management practices aimed at a sustainable growth strategy.

The strength and vitality of the Group is most clearly expressed in its capacity for renewal, and the renewal of the Jerónimo Martins corporate identity is yet another proof of the profound changes that are taking place. The new

1 EVA = Economic Value Added 2 Jerónimo Martins is member of the Portuguese Chapter of the World Business Council for Sustainable Development

Jerónimo Martins, SGPS, S.A.

8

corporate identity of the Group, introduced in 2004, reflects a new reality and embodies its solidity, rigour, professional excellence, ethics and transparency to reveal a cohesive, innovative Group. This identity reflects a Group that is prepared for a new phase in its history, ready and able to guarantee a stable, solid and lasting future.

Strategy

The strategic focus of the Group is to consolidate its food business in Portugal within its profitability standards, to uphold the growth dynamics in Poland to top level efficiency standards, and to carefully and in due time assess new business opportunities directed at the sustainable growth of the Group.

2. Corporate Bodies

Election Date:

29th June 2001 Composition of the Board of Directors in 2003

Executive Members:

Chairman and Managing Director Elísio Alexandre Soares dos Santos - Aged 69; - Chairman of the Group since February 1996; - In 1957 joined Unilever; From 1964 to 1967 worked as Marketing Manager at Unilever Brazil; In 1968 joined

the Board of Directors of Jerónimo Martins as Managing Director, combining this position with that of Jerónimo Martins representative in a joint venture with Unilever.

Responsible for Food Distribution Operations Pedro Manuel de Castro Soares dos Santos - Aged 44; - Executive Member of Jerónimo Martins’ Board of Directors since 1995; - In 1983 joined the Pingo Doce Operations Division; In 1985 started working in the Sales and Marketing

Department of Iglo/Unilever; In 1990 was appointed Assistant Manager of Recheio Operations; In 1995 was appointed General Manager of Recheio; Between 1999 and 2000 was responsible for operations in Poland and Brazil; In 2001 assumed responsibility for food distribution operations in Portugal.

Responsible for Financial Area Luís Maria Viana Palha da Silva - Aged 48; - Business Management Degree – Universidade Católica Portuguesa; Degree in Economics – Instituto Superior de

Economia e Gestão; - Executive Member of Jerónimo Martins’ Board of Directors since 2001; - Assistant Professor at the Universidade Católica Portuguesa from 1985 to 1992; From 1987 onwards appointed

to board of directors of several companies, namely Covina, SEFIS, EGF, CELBI, SOGEFI and IPE; Secretary of State for Trade from 1992 to 1995; Member of the Board of Directors of Cimpor from 1998 to 2001.

Non-Executive Members:

António Mendo Castel-Branco Borges - Aged 55; - Degree in Economics – Universidade Técnica de Lisboa; PhD in Economics – Standford University; - Non-Executive Member of Jerónimo Martins’ Board of Directors since 2001; - In 1980 joins the INSEAD; Appointed Vice-Governor of the Bank of Portugal in 1990 and INSEAD Dean in 1995;

Taught at Universidade Católica de Lisboa and Stanford University; Advisor to the USA Department of Treasury, the OECD and the Portuguese Government; Held various positions on the Board of Citibank Portugal, Petrogal, Vista Alegre Group, Paribas and SONAE, among others; Vice Chairman of Goldman Sachs since 2000.

Hans Eggerstedt - Aged 65; - Degree in Economics – University of Hamburg; - Non-Executive Member of Jerónimo Martins’ Board of Directors since 2001; - In 1964 joined and remained with Unilever; Among other positions, was Manager of Retail Operations and Ice

Cream and Frozen Products in Germany, Chairman and CEO of Unilever Turkey, Regional Manager for Central and Eastern Europe, and Financial and Information and Technology Manager at Unilever; In 1985 was appointed member of the Board of Directors of Unilever N.V. and Unilever PLC, remaining in this post until 1999.

Jerónimo Martins, SGPS, S.A.

9

José Luís Nogueira de Brito - Aged 65; - Degree in Law – Faculdade de Direito da Universidade de Coimbra; - Non-Executive Member of the Board of Jerónimo Martins since 2001; - Appointed Under-Secretary of State for Labour and Social Security in 1969, and Secretary of State for Urban

Development and Housing in 1972; Executive member of Jerónimo Martins’ Board of Directors from 1980 to 2001; Legal Consultant of Fima/Lever/Iglo from 1980 to 1998; Member of the Board of Directors of the Bank of Portugal in 1981 and Member of the Assembly of the Republic from 1983 to 1989; Elected Vice Chairman of the Portuguese Manufacturing Confederation in 1989; Chairman of the Portuguese Red Cross since 2003.

Rui de Medeiros d`Espiney Patrício - Aged 71; - Degree in Law – Faculdade de Direito da Universidade de Lisboa; - Non-Executive Member of the Board of Jerónimo Martins since 2001; - Assistant Professor in Faculdade de Direito da Universidade de Lisboa from 1958 to 1963; Appointed Under-

Secretary of State for Overseas Development in 1970; Vice Chairman of Monteiro Aranha Group from 1976 to 1991; Subsequently has been on Board of Directors of several Brazilian companies, namely Monteiro Aranha, Masa-Alsthom, Hochtief, Ericson, Telesp Celular, Axa Seguros, and worked as advisor to Group Espírito Santo.

Substitute Member: Álvaro Troncoso

Single Auditor and External Auditor: Bernardes, Sismeiro & Associados, S.R.O.C., Lda. Represented by: José Manuel de Oliveira Vitorino, R.O.C.

Corporate Secretary: Henrique Soares dos Santos

Chairman of Shareholders’ General Meeting: Artur Santos Silva

Secretary of Shareholders’ General Meeting: António Neto Alves

Jerónimo Martins, SGPS, S.A.

10

3. Businesses and Ownership Structure

Jerónimo Martins, SGPS, S.A.

11

4. Management Structure

Jerónimo Martins, SGPS, SA is the Group’s Holding Company. A number of functional areas are part of the Holding Company which is responsible for supporting and assisting the Executive Committee, the Board of Directors and all Group Societies on matters specific to each area – Human Resources, Development and Strategy, Planning and Control, Consolidation and Accounting, Internal Audit and Risk Management, Financial Operations, Fiscal Affairs, Legal Affairs, Communication and Security. There is also an area responsible for Special Projects and another responsible for the Board of Directors’ Assistance.

Group business is divided in three key areas – Distribution, Manufacturing and Services.

Distribution is divided into geographical areas – Poland and Portugal.

The management structure in Portugal is organised under a “near-matrix”, with Business Divisions and Functional Divisions designed to maximise Group synergies in terms of scale, resources and know-how, and to ensure the requisite focus on the consumer and on business formats.

The Business Divisions – Pingo Doce, Feira Nova, Madeira and Recheio, are responsible for category management, operations, marketing and technical areas and are supported by management control and human resources managers, who report to the head of the business division and functionally to the respective areas in the Holding Company.

The Functional Divisions – Sourcing, Logistics, Quality Control, Financial and Information Systems – are grouped under Gestiretalho, a company that provides services to the Business Divisions in their respective areas of activity.

The Business Divisions and the Functional Divisions are represented in the Executive Management Committee of Distribution, a body that coordinates strategic decisions for Distribution in Portugal and Poland.

Jerónimo Martins, SGPS, S.A.

12

In the Polish market, management structure is organised under an in-line model, with the head of the Business Division responsible for category management, marketing, operations, technical, human resources, logistics, financial, quality control and information systems.

Manufacturing management structure also follows a “near-matrix”, being organised into Business Divisions and Functional Divisions, so as to maximise synergies in terms of resources and know-how and ensure the requisite focus on the consumer.

The Business Divisions – FimaVG, LeverElida and IgloOlá – are responsible for sales, marketing, production and quality assurance and are supported by management control and human resources managers, who report in line to the head of the business area and functionally to the respective functional areas.

The Functional Divisions – Human Resources, Supply Chain (which includes purchases, planning and logistics), Financial and Information Systems – provide services to the business divisions in their respective areas of activity.

The General Managers of the Business Divisions and the General Managers of the Functional Divisions are members of the National Conference, the body that is entitled to coordinate the strategic decisions for the various manufacturing businesses.

Services’ management structure is organised by business areas – JMD (which comprises the Food, Cosmetics and Caterplus divisions), Hussel and Jeronymo – all of which are under the same General Management.

Each business area is responsible for sales, customer service and marketing in the case of JMD, and for operations, marketing and purchases in the case of Hussel and Jeronymo.

Logistics, Financial and Information Systems are functional areas that provide services to JMD, Hussel and Jeronymo and all report to the same General Management.

General Management accumulates responsibility for human resources, along with the functional area of Human Resources in the Holding.

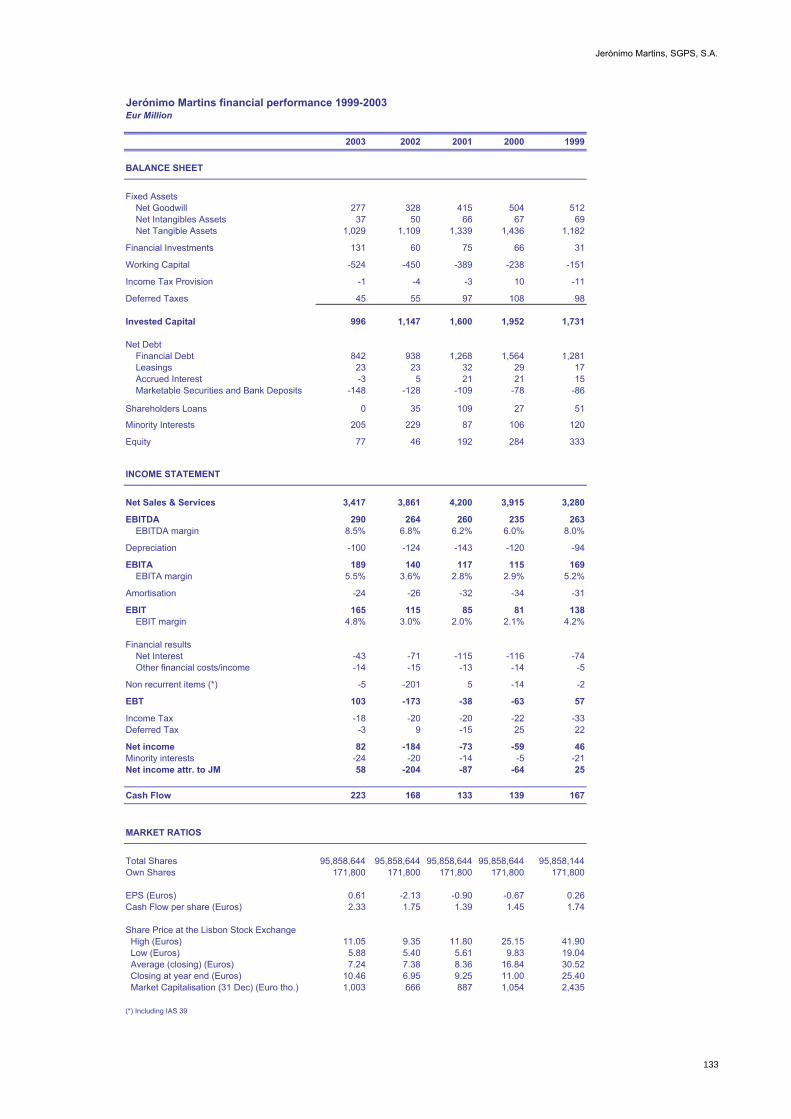

5. Operating and Financial Highlights

Group Operating Indicators

Store Network Evolution

Key Figures in Distribution

1999 2000 2001 2002 2003

Pingo Doce 173 189 190 192 190

Feira Nova 21 23 23 24 25

Recheio 29 30 32 34 33

Biedronka 579 589 621 638 672

Jerónimo Martins, SGPS, S.A.

13

Group Financial Indicators

Sales and Services

1.891 2.1532.1062.1322.046

1.0581.509 982

1.4851.701331

360

282

270367

0500

1.0001.5002.0002.5003.0003.5004.0004.500

1999 2000 2001 2002 2003

Distribution Portugal Distribution o ther Countries M anufacturing & Services

€' 000.000

6,4%6,0%

4,7%

1,3%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

7,0%

Retail Portugal * Cash & Carry M adeira B iedronka

EBITA Margin 2003 YE

* % store sales

% sales

799

125

42

152

0

100200

300

400500

600700

800

R etail P o rtugal C ash & C arry M adeira B iedro nka

* excluding Sé, Águas, Turismo, Lillywhites, Jumbo, JM &M and Eurocash but including Bakery and Diversey disposed in 2002.

Jerónimo Martins, SGPS, S.A.

16

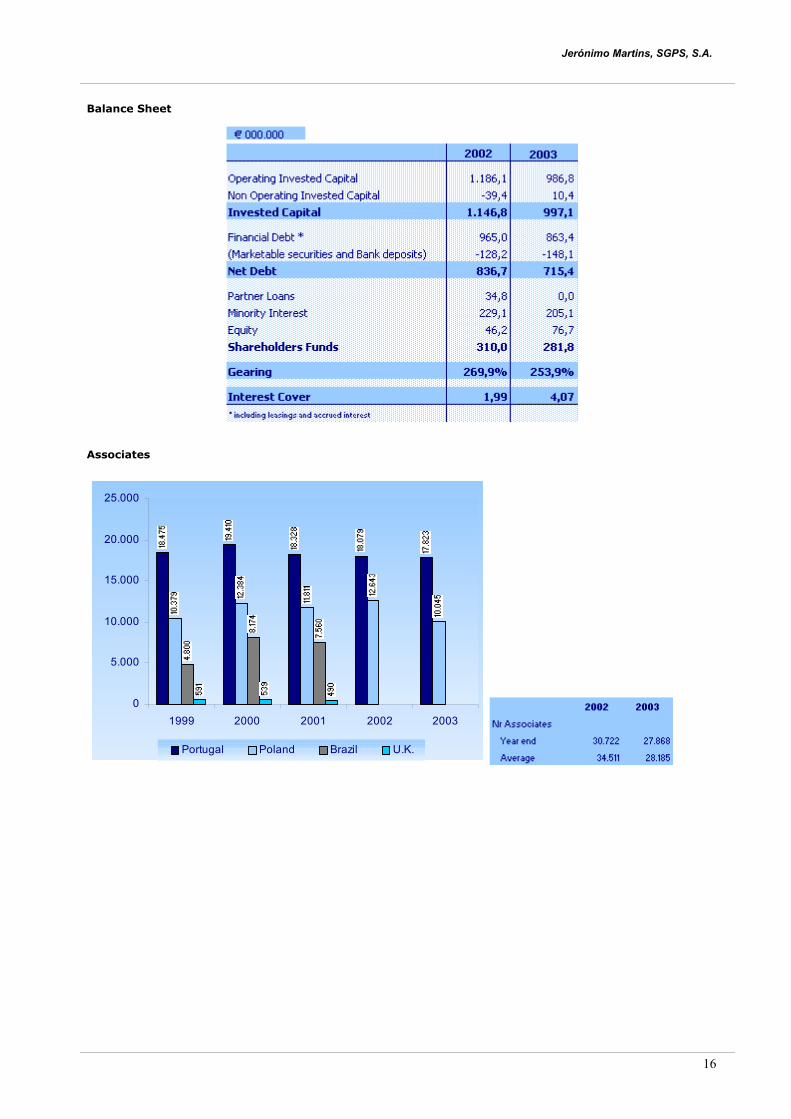

Balance Sheet

Associates

0

5.000

10.000

15.000

20.000

25.000

1999 2000 2001 2002 2003

Portugal Poland Brazil U.K.

Jerónimo Martins, SGPS, S.A.

17

6. Key Relevant Facts

Operations

January - Transfer of Leiria Recheio store to new location. - Refurbishing of Feira Nova store in Rio Tinto (closed 2 weeks). - Start of the operational restructure of Biedronka – division into four integrated geographical regions.

February - Refurbishing of Feira Nova store in Valongo (closed 6 weeks). - Sale of Eurocash effective as of March 1st (Poland).

April - Opening of new warehouse for fresh fish in Portugal (Azambuja). - Opening of Feira Nova Hypermarket in Odivelas (first store with graphic interface POS and with the new

ElectricCo concept). - Opening of two Hussel stores (Odivelas Parque and Forum Montijo). - Closing of two Pingo Doce stores (Central de Francos and D. João V) to be transferred to new location.

May - Launching of Pingo Doce campaign “More than 1,000 prices lowered” in Madeira. - Visit of financial analysts and journalists to Biedronka (stores and warehouses).

June - JMR issues euro 115,000,000 bond loan. - Process of transfer to net price is concluded in Portugal.

July - Opening of first Hussel-Olá store, at Forum Aveiro in partnership with IgloOlá. - Anniversary Campaign “30 years of Recheio”. - Launch of Pingo Doce private label TV campaign. - Signing of property transfer promissory contract for 4 stores operated by Irmãos Costa Pais, SA, under the

Monteverde brand. - Closing of Pingo Doce Online (press release).

August - Feira Nova innovates on textile management, through a joint venture. - Closing of two Pingo Doce stores (Estrada da Falagueira and Passos de Ferreira), to be transferred to new

locations. - Refurbishing of Pingo Doce at Linda-a-Velha.

September - JM, SGPS, S.A. places euro 25,000,000, 5 years commercial paper programme. - Launch of “100% Feira Nova” promotional campaign. - Refurbishing of Feira Nova in Caldas da Rainha (closed two months). - Launch of Pingo Doce’s advertising campaign “This is not a promotion; PD has really lowered its prices…”. - New Biedronka advertising campaign “Half of Poland buys at Biedronka. Come and see why”.

October - JM, SGPS, S.A. issues euro 40,000,000 bond loan. - Opening of two Pingo Doce stores (Póvoa de Santa Iria and Damaia). - Refurbishing of Feira Nova in Loures (closed for one month). - Pingo Doce concludes introduction of the automatic restocking planning system (MRP) in all stores and all

product areas.

November - Biedronka consolidates position in Warsaw with 10 new stores.

December - Pingo Doce campaign – accepting payments in escudos. - Closing of Pingo Doce store in Alcântara, for two years, to be re-opened in a new residential complex.

Social Responsibility

January - Introduction of environmental management approach, which includes the requirements, defined in

Accounting Standard no. 29 “Environmental Matters”. - Introduction of productivity bonus in the distribution warehouses. - Performance appraisal system is extended to all non-management staff in FimaVG, LeverElida and IgloOlá.

Jerónimo Martins, SGPS, S.A.

18

March - Environmental awareness campaign on energy consumption.

April - Introduction of productivity bonus in Recheio operations (Mainland and Madeira). - Implementation of water quality monitoring plan in the Stores and Distribution Centres. - Jerónimo Martins sponsors refurbishing of pediatric surgery ward Hospital Santa Maria. - Pingo Doce give financial support to Oceanário de Lisboa for 3 years.

August - Renewal of NP EN - ISO 14001:1999 Vítor Guedes certification.

September - Pingo Doce gets certification for its free-range chicken. - Start of Skip “Mão Amiga” fund-raising campaign to open a new home “Associação Novo Futuro”.

October - Publication of Jerónimo Martins Code of Conduct. - Víctor Guedes plant obtains approval in Japan Institute of Plant Maintenance (JIPM), level I audit, and is

awarded with respective prize for excellence. - Environmental awareness campaign on waste management.

November - LeverElida launches environmental initiative under the motto “Lever – an open plant”.

December - Accident Rate in Feira Nova falls by 20%. - Increase of 113% in audits and visits to suppliers of Perishables and Private Label and rate of returned

articles in the warehouses dropping by 28%.

Jerónimo Martins, SGPS, S.A.

19

II. Corporate Governance Following the entry into force of the changes introduced by the Securities and Exchange Commission Regulation no. 11/2003 to Regulations no. 7/2000 and no. 07/2001 on the governance of listed companies, the Board of Directors of Jerónimo Martins SGPS, S.A. hereby presents the main guidelines followed by the Company on this matter following the reports of previous years. In full compliance with the requirements of legislation regarding the disclosure of information, this chapter is organised into the following sections: (Chapter 0) Declaration of Compliance, (Chapter 1) Disclosure of Information, (Chapter 2) Exercise of Shareholder Voting and Representation Rights, (Chapter 3) Company Rules and (Chapter 4) Board of Directors. Chapter 0. Declaration of Compliance The Company fully complies with the Securities and Exchange Commission’s recommendations on the governance of listed companies. However, it is our understanding that, in the light of the text in question, some of the recommendations are not fully respected in Company practice, namely as regards:

The Company actively encourages the exercise of shareholder voting rights, being in near full compliance with the provisions of the Securities and Exchange Commission’s recommendation on this matter. However, it should be mentioned that in the course of 2003, particularly with respect to the notice convening the annual general meeting, the deadline for the blocking of shares for shareholder participation was set at 8 days prior to the meeting, and no ballot papers were adopted for votes submitted by mail. To facilitate integration and full compliance with this recommendation, at the next General Meeting the Company will make ballot papers available to shareholders wishing to vote by post, and is considering a change in the by-laws regarding the deadline for the blocking of shares for shareholder participation.

As to the recommendation as to discrimination of individual remuneration paid to members of the Board of

Directors, the Company feels that there are other alternatives for verifying the internal distribution of remuneration and assessing the relationship between the performance of each sector in the Company and the remuneration level of members of the Board of Directors responsible for monitoring such sectors, which may be achieved by indicating separately the overall remuneration of Executive Members and that of Non-Executive Members. In addition, it is the opinion of the Board of Directors that the disclosure of such information may raise susceptibilities that will, in no way, contribute to improving the performance of the members of the Board of Directors, therefore, this recommendation is adopted only with regard to collective remuneration with discrimination of remuneration paid to Executive Members and Non-Executive Members.

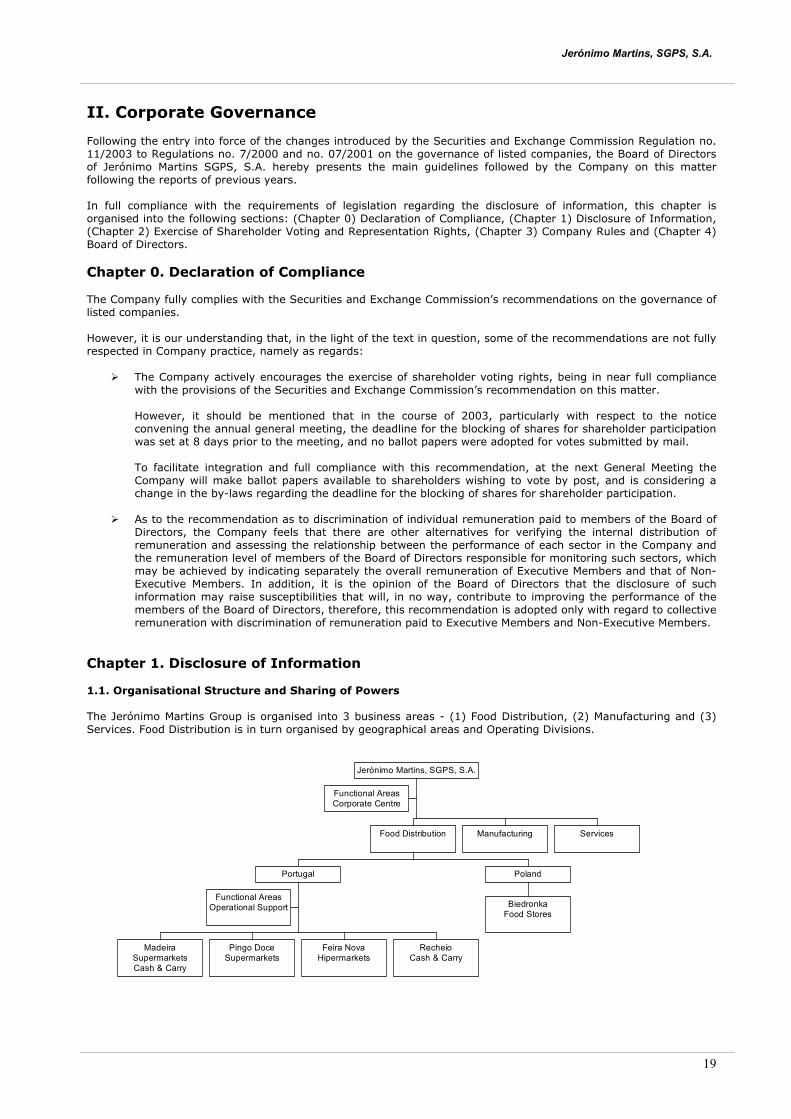

Chapter 1. Disclosure of Information 1.1. Organisational Structure and Sharing of Powers The Jerónimo Martins Group is organised into 3 business areas - (1) Food Distribution, (2) Manufacturing and (3) Services. Food Distribution is in turn organised by geographical areas and Operating Divisions.

Functional AreasCorporate Centre

Functional AreasOperational Support

MadeiraSupermarketsCash & Carry

Pingo DoceSupermarkets

Feira NovaHipermarkets

RecheioCash & Carry

Portugal

BiedronkaFood Stores

Poland

Food Distribution Manufacturing Services

Jerónimo Martins, SGPS, S.A.

Jerónimo Martins, SGPS, S.A.

20

Operating Divisions The Jerónimo Martins Group organisational model is aimed to ensure focus on the various Group businesses by the creation of operating areas and divisions that guarantee proximity to the different markets. The Food Distribution business is divided into geographical areas, and currently has four operating divisions in Portugal - Pingo Doce (supermarkets), Feira Nova (hypermarkets), Recheio (cash & carry) and Madeira (supermarkets and cash & carry) - and one operating division in Poland - Biedronka (food stores). The Manufacturing business comprises a joint venture with Unilever in FimaVG (food products), LeverElida (personal and home care) and IgloOlá (ice cream and frozen food). The Services business includes Jerónimo Martins Distribuição de Produtos de Consumo (representation of international brands of fast moving food products and cosmetics), Hussel (specialised chocolates and confectionery retail) and Jeronymo (pilot-projects in specialised retail). Functional Divisions of Operational Support The Functional Divisions of operational support ensure that Group synergies are maximised through the sharing of resources and functions in relevant markets, thus boosting organisational efficiency and the sharing of relevant skills and know-how. The functional divisions of operational support are Sourcing, Logistics, Quality Control, Financial and Information Systems. These areas provide services to the various operating divisions in accordance with the Holding guidelines, ensuring the uniformity of policies and procedures.

Functional Areas in the Holding

Corporate SecretaryHenrique Santos

Fiscal AffairsCíntia Melo

Legal AffairsAntónio Neto Alves

Financial OperationsConceição Tavares

Internal AuditNuno Sereno

Planning and ControlAna Luísa Virginia

CommunicationAna Vidal

Special ProjectsFrancisco Martins*

Consolidation and AccountsAntónio Pereira

Human ResourcesJosé Padinha Ribeiro*

Development and StrategyMargarida Martins Ramalho

SecurityEduardo Dias Costa

Jerónimo Martins GroupFunctional Areas of Corporate Support

Jerónimo Martins SGPS S.A., as the head of the Group, is responsible for ensuring consistency between the objectives established and resources available. Holding is responsible for the definition and implementation of the portfolio development strategy, strategic planning and control of the various businesses, guaranteeing consistency with global objectives, the definition and control of Group financial policies, and the definition of human resources policies, taking direct responsibility for the implementation of the executive staff development policy (Management Development). Holding functional areas give support to the corporate centre, while simultaneously providing services to the operational and functional divisions of the Group. They are organised as follows: Corporate Secretary - Prepares the Board of Directors and Executive Committee meetings, ensuring that decisions taken are duly communicated and monitoring their implementation when necessary. Legal Affairs - Monitors Group corporate affairs and ensures compliance with the legal obligations of the Group companies; Assists the Board of Directors in the preparation and negotiation of contracts to which Jerónimo Martins SGPS, S.A. is a party and leads the development and implementation of strategies aimed at protecting Group interests in case of disputes and manages external counsel dealings. Internal Audit - Assesses the quality and effectiveness of internal control operating and non-operating systems set up by the Board of Directors and ensures its compliance with the Group manual of procedures; Also responsible for

Jerónimo Martins, SGPS, S.A.

21

ensuring full compliance with the procedures set out in the manual of operations of each business unit, and the legislation and regulations applicable to the respective operations. Communication - Defines and implements Group communication strategy in the areas of Media Relations and Social Responsibility; Also responsible for developing external and internal communication instruments and actions involving Jerónimo Martins’ corporate image, and for co-ordinating media coverage for marketing initiatives undertaken by the business units. Consolidation and Accounts - Prepares consolidated financial information to comply with legal obligations and to assist the Board of Directors; Also implements and monitors the accounting principles and policies adopted by the Board of Directors and applicable to all Group companies and verifies compliance with the respective statutory obligations. Development and Strategy - Supports analysis of strategic focus and medium-term planning, ensuring that the strategic development of businesses is consistent with the strategic objectives of the Group. It also assists the Executive Committee in defining and assessing these objectives, and monitors the ensuing development projects; In addition, it is responsible for contacts with official entities and for representing and managing the Group interests vis-à-vis institutions and corporate associations in the Food Distribution Industry. Fiscal Affairs - Advises all Group companies on fiscal matters, ensuring compliance with legislation in force and the optimisation of business management initiatives; Manages tax litigation matters and also relations with external consultants and tax authorities. Financial Operations - Ensures the availability of more appropriate financial resources in terms of value, timing and cost, as well as selects and implements for selecting and implementing risk management solutions, in co-ordination with risk identification and control activities developed by the Internal Audit of the Group. Planning and Control - Defines and monitors policies and procedures in the planning and control area: validation of medium and long-term projections, performance analysis, budget control and analysis and control of investment projects; Also responsible for the relation with the Capital Market and for co-ordinating and supporting acquisition, disposal and corporate restructuring operations. Special Projects - Heads the simplification processes project, the main objective of which is to define and implement Best Practices in the various Food Distribution operational divisions in Portugal and respective functional divisions, in conjunction with the best functional solutions for the business, to optimise available resources across the organisation and improve productivity levels. Human Resources - Defines and implements Group policies in this area, specifically as regards wages and incentives, recruitment, career management, training and staff development; Also provides technical support to the Group’s Operating Divisions. Security - Defines and controls procedures aimed at preserving the safety of personnel and assets within the Group, as well as for monitoring any matters involving the police or legal authorities; Also provides support for the audit of safety systems and risk prevention. 1.2. Specific Company Committees Ethics Committee In 2003 the Board of Directors appointed an Ethics Committee, which succeeded the “Working Group for rules of conduct”. The first objective of the Committee was to draw up a code defining the guiding principles applicable to the activities of the companies in the Jerónimo Martins Group, namely responsibility to investors, customers, suppliers, competitors and employees. The Code of Conduct was approved at the beginning of the second half of 2003 and the Ethics Committee is responsible for divulging it and ensuring compliance with it. The Ethics Committee is made up of Ana Vidal (Communications Director), José Padinha Ribeiro (Director of Human Resources) and António Neto Alves (Director of Legal Affairs). Audit Committee The Audit Committee appointed by the Board of Directors, has as specific responsibilities on the assessment and supervision of risks and critical processes, reporting directly to the Executive Committee on all situations classified as high risk. The Audit Committee meets on a monthly basis. It is composed of the Committee Chairman (José Guimarães Assédio) and three members (José Gomes Miguel, Nuno Sereno and Henrique Santos), none of whom is a member of the Board of Directors.

Jerónimo Martins, SGPS, S.A.

22

In the course of 2003, the Audit Committee held 10 meetings, of which minutes were taken, and assessed 42 reports that had been prepared by the Internal Audit Department. These meetings were attended by one external audit representative. The close collaboration between Internal Audit and this representative greatly contributed to increase efficiency and maximise work-team synergies. Internal Audit also co-operated with its counterpart in Ahold, which participated in the cross-audit programme simultaneously implemented in all the companies where Ahold has holdings. Work carried out within the ambit of this programme added greatly to information reporting procedures. Internal Control Committee The Company is currently considering the creation of an Internal Control Committee with responsibility for the assessment of corporate organisation and governance, as well as supervision of the risk management process. This Committee would be composed of three Non-Executive Members. 1.3. Risk Control System

The Company, and in particular its Board of Directors, regards risks inherent in its businesses as a very important issue. Given their relevance to the internal decision-making process and to market agents in general, the Group is committed to transparency and the quality of information disclosed with regard to issues having an impact, whether positive or negative, on its future. The aim is to convey a clear idea of value creation mechanisms as well as of any potential value-destructing causes while information is prepared with a view to presenting confident, accurate performance estimates. In this way, the Company hopes to provide its shareholders with as accurate as possible a picture of all endogenous and exogenous factors liable to have a significant impact on its profitability. Risk Management Objectives Risk management in Jerónimo Martins aims to achieve the following objectives:

• Identify and assess business and process risks; • Identify key value drivers and regularly assess strong and weak points; • Develop and implement risk hedging and prevention programmes; • Integrate risk management in business planning; • Define a risk identification, management and monitoring terminology common to the whole Group. • Consistently add maximum value to all activities within the Group in order to raise employee awareness of

the risks and the positive and negative effects of all factors influencing operations and constituting value creation sources;

• Improve the decision-making process and priority-definition process with a structured understanding of the Group’s business processes, their volatility and their opportunities and threats.

The Risk Management Process The Group’s risk management uses an Economic Value Added (EVA) approach applied to two universes - Consolidated and Operating. The objective is to make a bottom-up analysis, assessing first the elements that are at the basis of either the NOPAT (net operating profit after tax) or the cost of capital, so as to get an objective notion of how these interact, and ultimately, to discover the main risks in the value creation process, as a core management objective. The business processes in the various activities developed in the Jerónimo Martins Group form a value chain that includes a strategic group of key value drivers. The risk management process stems from the identification of these key value drivers and from the analysis of underlying risks. This approach will provide a systematic, interconnected perspective of the risks inherent in processes, functions and organisational divisions. The risk management process has a cyclical nature that addresses: (1) identification and assessment of risks, (2) definition of management strategies, (3) implementation of control processes, and (4) the monitoring of the risk management process. The “owners” of critical business processes are also responsible for the design and implementation of risk control processes, together with those responsible for Risk Management integrated in the functional area of Financial Operations in the Holding. In turn, the efficiency of the risk control processes is assessed by the Internal Audit Department. Insurance coverage, financial risk management and property risk management are some of the main risk control processes in force in Jerónimo Martins.

Jerónimo Martins, SGPS, S.A.

23

Assessment of Internal Control The quality of internal control of the Group is assessed by an internal audit plan prepared every year to cover the auditing of processes, conformity, finances, and information systems. Having identified business and process risks and management procedures it is decided what critical processes will be taken to manage them. The steps to be taken by the Internal Audit Department are defined based on the connection between critical processes and risks (these steps are described in detail in the chapter on the activity of Functional Areas in Holding). Monitoring the Risk Management Process The Board of Directors, Operating and Functional Divisions, the Board of Auditors and Risk Management and Internal Audit are responsible for monitoring the risk management process within the Group. The Board of Directors has the following set of objectives and responsibilities as the body responsible for the success of Group strategy:

• Know the more significant risks affecting the Group; • Make sure that there is adequate knowledge within the Group as to risks likely to affect operations and how

to manage them; • Ensure that the Group risk management strategy is conveyed to all hierarchical levels; • Ensure that the Group has the capacity to minimise both the possibility of risks and their impact on the

business; • Make sure that the Group knows how to react to crisis situations; • Make sure that the risk management process is adequate and that Risk Management closely monitors more

probable risks and their impact on the Group operations. 1.4. Share Price Performance In 2003, stock markets went through three distinct periods, reflecting global geopolitical developments. Until mid-March, the world was submerged in a climate of pessimism and uncertainty that preceded the war with Iraq. Stock markets in general fell to their lowest over the last few years, the Portuguese PSI-20 index reaching a 6-year low on 28 February. As the war developed and the scenario became more optimistic, the second quarter showed a gradual recovery and a slight acceleration in stock markets. Investor confidence picked up and the world economy became more stable, positively translated into improved expectations. The second half of the year was marked by an acceleration of growth in most stock markets, the main indexes rising by 30% to 40%. Because these are weighted averages, they hide the much better performance of small caps, some of which soared by more than 100%. This growth in European reflected the increase of private consumption and GDP in the USA. Performance of Jerónimo Martins Share During the first quarter of the year the Jerónimo Martins share followed its 2002 trend reinforced by the pre-war situation, hitting a bottom-low of 5.88 on February 27th. The conclusion of the restructuring process with the sale of Eurocash (Poland) in February 2003 may have had a small positive impact on the Jerónimo Martins share price. During the second and third quarters the Jerónimo Martins share remained stable at euro 6.5 and 7.5, notwithstanding the upward revision of price targets and recommendations of all analysts monitoring the company and sector. Following the announcement of third quarter results on October 30th and the road show in London, Boston and New York between November the 10th and the 13th, which confirmed analysts' expectations and a return to profits, there was a strong demand for Jerónimo Martins share and the trading volume rose sharply - average trading on Jerónimo Martins share more than trebled over the first three quarters of the year - and the share price climbed, reaching the year’s high on December 17th: 11.05 euros per share.

Jerónimo Martins, SGPS, S.A.

24

Increases occurred in the fourth quarter, both in the trading volume of Jerónimo Martins shares and in the share price (up by 55%), which greatly surpassed that of the general PSI-20 index (up by 10%).

The Investor Relations Office continued to provide updated information on performance indicators and to release Group results, having answered all the analyst and investor questions, either by phone or by the e-mail address - [email protected]. In May, journalists and analysts visited Biedronka operations in Poland (stores and warehouses), where they could learn about Group activities and the Polish market. In 2003, two Road Shows were part of the communication strategy with the Market. The first, in May, took place in Holland and in London, and the second, in November, was conducted in London, Boston and New York. These road shows presented the results of the restructuring process, the return to profits in 2003 and the Group’s strategic guidelines for 2004-2006. The following chart lists press releases and event communications issued in 2003 to keep analysts and investors informed about relevant Group activities:

Jerónimo Martins, SGPS, S.A.

26

PRESS RELEASES AND EVENT COMMUNICATIONS

6-Jan Calendar of presentation of results 2003

8-Jan 2002 preliminary sales

3-Feb Sale of Eurocash

20-Mar Presentation of 2002 results and Conference with Analysts held in the Company

26-Mar Participation in the Iberian Mid-Cap Conference in Madrid, organised by the Deutsche Bank

28- Mar Notice convening general shareholders’ meeting

2 –Apr Meetings with Portuguese institutional investors, organised by BCP Investimentos

29-Apr Presentation of first quarter results

6-8-May RoadShow – Holland and London

15-16-May Visit of journalists and analysts to Poland

16-Jun Participation in the Food Retail Conference in Madrid, organised by the Deutsche Bank

8-Jul Disclosure of first half preliminary sales

18-Sep Presentation of first half results

2-Oct Participation in the European Retail conference in Paris organised by CDC IXIS

3-Oct Press Release on Bond Loan

30-Oct Presentation of third quarter results

10–13-Nov RoadShow - London, Boston and New York

Jerónimo Martins, SGPS, S.A.

27

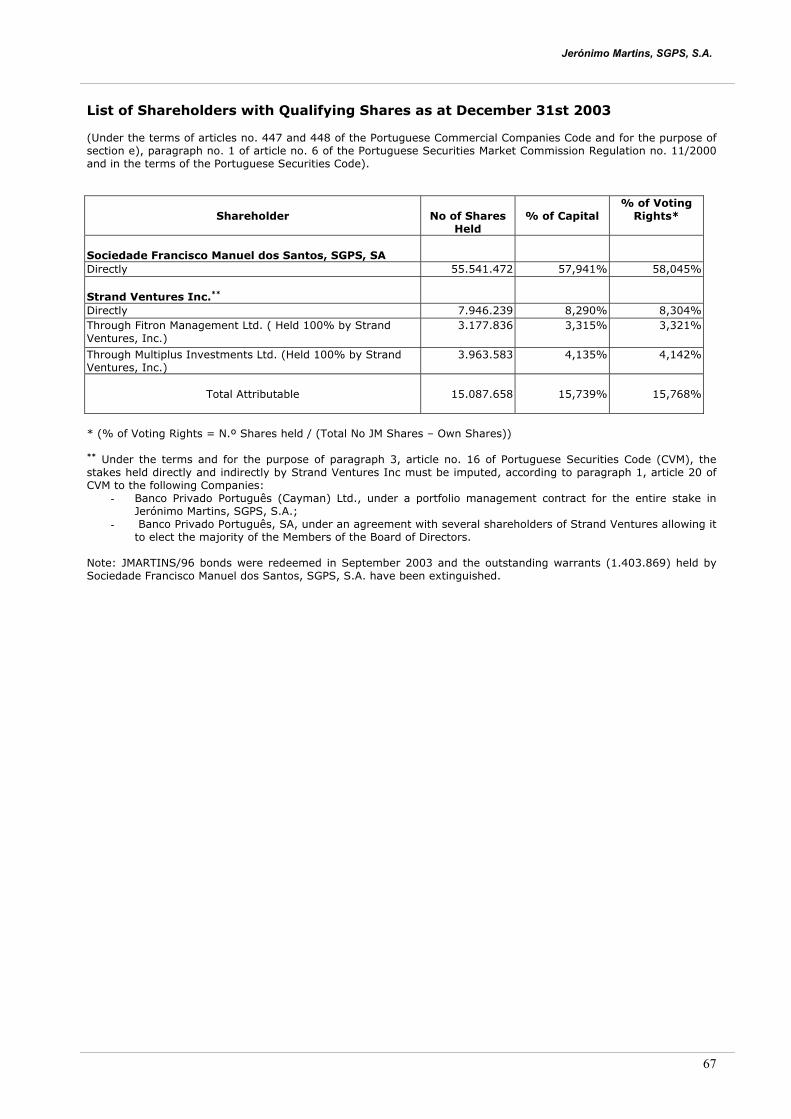

Shareholder Structure

In 2003, Companies, whose rights of voting, under the terms of Article 20, paragraph 1 of the Securities and Exchange Code are attributable to Banco Privado Português (see note to “List of Holders of Qualified Stakes as of 31 December 2003” on part III. Consolidated Management Report Annex), increased their holdings in Jerónimo Martins, SGPS, S.A. by 0.5 percentage points against December the 31st 2002. Plan to Acquire Own Shares In 2003, there were no movements in the treasury stock account. Jerónimo Martins SGPS, S.A. maintains a portfolio of 171,800 own shares purchased in 1999 at the average price of euro 35.28 each, representing 0.18% of its share capital. 1.5. Dividend Distribution Policy The Board of Directors of Jerónimo Martins SGPS, SA has established a dividend distribution policy based on the following assumptions:

The value of the dividend distributed should correspond to between 40% and 50% of ordinary consolidated

earnings. If as a result of the application of this criteria, the dividend distribution in a given year is lower than in the preceding year, the Board of Directors, if they consider that the reduction is a result of abnormal, merely circumstantial situations, may propose that the preceding year value is maintained. Or they may even resort to existing free reserves, providing that the use of these reserves does not jeopardise the principles adopted for balance sheet management. In accordance with the referred criteria, a gross dividend per share of PTE 60.00 was distributed in 1999, the last year in which dividends were distributed. Due to the consolidated losses posted in 2000, 2001 and 2002, no dividends were distributed for these years. Considering the net results of 2003, and viewing the reinforcement of equity, the Board of Directors of Jerónimo Martins SGPS, S.A. will propose to the General Shareholders’ Meeting the distribution of no dividends this year, as was the case in the previous years. 1.6. Stock Option Plan At its meeting on August 9th, 1996, the General Shareholders’ Meeting of the Company gave the Board of Directors full powers to establish the terms and conditions of a capital stake-holding plan, suppressing shareholders’ preference rights to subscribe 337,098 ordinary shares which, under the terms of the plan, were reserved for subscription by the Group board members and senior management. The capital increase was fully subscribed by Jerónimo Martins Stock Option Plan Trust, which is entirely independent of the Company and is managed separately.

Shareholder Structure

15,7%

26,3%

57,9%

Soc. Francisco Manuel dosSantos

BPP (StrandVentures+Multiplus+FitronManagement)

Floating and Own Shares

Jerónimo Martins, SGPS, S.A.

28

Under the terms of the Trust, Jerónimo Martins shares exclusively subscribed by the Trust will be kept with the Trust and only transferred between it and the Company under due authorisations to acquire own shares approved by the shareholders at a general meeting, thus providing for its funding needs arising from the application of the incentive plan. The introduction of this plan is linked to the implementation in the whole Group of a target-led management system based on parameters of profitability analysis, business growth and value generation for the shareholders, which ensures that the Group’s management is highly committed to the strategic goals established. 1.7. Business Between Members of the Board and the Company In 2003 there were no business or transactions carried out between, on the one hand, the members of the Company’s Board or Directors and its Supervising Bodies, and on the other, the holders of Qualified Stakes or Companies under a Parent-Subsidiary or Group Relationship. 1.8. Investor Relations Office The objective of this Office is to give the market an up-to-date picture of the various Jerónimo Martins areas of business, in terms of performance and outlook. It is the favoured source of information for all institutional and private investors, as well as for analysts who give their opinions and recommendations on listed securities. The Office supplies information that may affect stock prices, which is also provided through institutional channels, especially through the Stock Exchange Commission web site. In addition, it offers general information and explanations about the various business areas. The Investor Relations Office is responsible for drawing up a financial market communication plan as part of the Group’s global communication strategy, and for implementing this plan. This includes not only releasing communications, but also co-ordinating and making conference calls and individual or joint meetings, preparing presentations and organising visits to the companies. E-mail is increasingly used to disclose this type of information, since it allows the Office to establish an individual, personalised contact to specifically reply to Shareholders’ queries on publicly disclosed information and Group Jerónimo Martins relevant facts. Quarterly results releases and convening notices for general meetings are examples of regular communications to the market that are also widely available on the Group’s institutional site. The Office may be contacted, not only through its Market Relations Representative, Ana Luísa Abreu Coelho Virgínia, but also through the Group’s institutional site, at www.jeronimo-martins.pt. The purpose of the site is also to facilitate access to certain types of information. In addition to disclosure of information as required by the new Article 3-A of Regulation no. 11/2003, the site provides general information on the Jerónimo Martins Group and the companies of which it is composed, as well as other information considered important, such as:

• Communications to the market concerning relevant facts; • The Group’s quarterly, semi-annual and annual accounts; • Economic and financial indicators and statistical data updated every six months or annually depending on

the company or business area; • Annual reports of the listed Companies in the Group; • Information on share price performance; • Calendar of corporate events issued at the beginning of each semester including, among others, General

Shareholders’ Meetings and presentation of annual, semi-annual, and when applicable, quarterly accounts; • Information concerning General Shareholders’ Meetings; • Information on corporate governance; • The Jerónimo Martins Group Code of Conduct;

Besides providing information, the site also includes a form for fast e-mail contacts/queries and the possibility of subscribing to a mailing list. Contacts for accessing the Investor Relations Office are as follows: Address: Rua Actor António Silva, nº 7, 14º andar, 1600-404, Lisboa Phone: +351 21 752 61 05 Fax: +351 21 752 61 65 E-mail: [email protected]

Jerónimo Martins, SGPS, S.A.

29

1.9. Remuneration Committee On November 13th, 2001, the General Shareholders’ Meeting elected a Remuneration Committee composed of the shareholders Artur Santos Silva, José Queirós Lopes Raimundo and Arlindo do Amaral, none of whom is a member of the Board of Directors of the Company or has a spouse, relative or family member in that position. As provided by law, the establishment of remuneration payable to members of the Board of Directors was delegated to this Committee. At a meeting on November 15th, 2001, the Remuneration Committee, acting within its powers, established parameters for the above-mentioned remunerations, as well as the possibility of allowing the Chairman, following disclosure of the year’s results, to submit a proposal to the Committee concerning the attribution to other members of the Board a bonus linked to the Group’s performance. 1.10. Amount of Annual Remuneration Paid to External Auditor Total remunerations paid to the auditor in the reporting year was of 638,104 euros, which excludes travelling expenses and other costs borne directly by Group companies. In percentage terms, this amount may be broken down as follows: 1) Statutory audit services: 97% 2) Other non-statutory audit services and external audits: 3% Other non-statutory audit services totalling the amount of 20,454 euros concern to: (1) a training course on IAS, (2) the consideration paid for access to a fiscal database, (3) maintenance and use of the CLIME consolidation tool and (4) an opinion on the tax incidence of bank guarantee stamp duty. All these services were aside from the regular auditing works and were provided by officers who did not participate in any auditing works within the Group. Chapter 2. Exercise of Shareholder Voting and Representation Rights 2.1. Statutory Rules on the Exercise of Voting Rights The exercise of voting rights through representation and the form of exercising these rights are fully ensured in accordance with the law and Company by-laws under the terms set down in the notices convening general meetings. The Company is actively committed to promoting the exercise of shareholder voting rights, namely through votes submitted by mail. The Company guarantees the availability of suitable information to enable shareholders represented to give voting instructions, namely by providing them with the proposals to be submitted to the General Shareholders’ Meeting, within legally established time limits. Since 2003, preparatory documents for General Meetings have also been made available on the Group’s institutional site on the Internet. Under the terms of Company by-laws shareholders with voting rights who, no later than eight days prior to the day of the meeting, have their shares registered under their name in a securities account, may participate in General Shareholders’ Meetings. Shareholders owning a small number of shares may form a group in order to reach one hundred shares equivalent to one vote and be represented by one of the members of the group. Shareholders may be represented at General Shareholders’ Meetings by a spouse, ascendant or descendant, or by another shareholder, or else by a member of the Company’s Board of Directors, by means of a letter addressed to the Chairman of the General Meeting indicating the name and address of the representative and the date of the meeting. The instruments of representation, as well as communications from credit institutions confirming the register of shares must be addressed to the Chairman of the General Meeting and delivered to the Company at least eight days prior to the date established for the meeting. 2.2. Postal Voting The Company has established the right of shareholders to vote by post, in accordance with the form provided in the last convening notices, which aims to facilitate easier means of voting while, at the same time, ensuring the safety of the vote. In 2004, the Company intends to provide shareholders with ballot papers to make it even easier to vote by post. 2.3. Electronic Voting Although recognising that the use of the new technologies promotes the exercise of shareholder voting rights, particularly through absentee votes submitted by electronic mail, the Company has not yet instituted this mechanism as it considers that the underlying information systems do not offer guarantees of reliability, particularly for the reception of votes.

Jerónimo Martins, SGPS, S.A.

30

2.4. Requirements in terms of the deadline for the deposit or blocking of shares Under the terms of the Company’s by-laws, shareholders with voting rights who, no later than eight days prior to the day of the meeting, have their shares registered under their name in a securities account, may participate in General Meetings. In this specific matter, the Company is constrained by a provision in its by-laws that limits the possibility of complying with the Securities and Exchange Commission’s recommendation in this regard. However, the Board of Directors may propose a change in the by-laws so as to include this recommendation. 2.5. Required Deadline for Receiving Votes Sent by Post As Company by-laws fail to provide an indication in this matter, the Company has established a deadline of 48 hours prior to the date of the General Meeting for the receipt of votes sent in by post, thus complying and even surpassing the Securities and Exchange Commission recommendation in this regard. 2.6. Number of Shares corresponding to One Vote According to Company by-laws, each one hundred shares corresponds to one vote. Chapter 3. Company Rules 3.1. Code of Conduct and Internal Regulations The Company must comply with the legislation in force and the appropriate rules of good conduct for its activity, adopting codes of conduct and internal regulations whenever the matters in question so justify. The Jerónimo Martins Group has always acted upon principles of absolute respect for rules of good conduct in the management of conflicts of interest, incompatibilities, confidentiality and the non-use of inside information by members of the Board of Directors. Although existing instruments and practice have proved adequate for the regulation of these matters, it was decided to draw up a code for existing rules of good conduct on the above-mentioned matters, as well as others that specifically apply to the activities of the companies in the Jerónimo Martins Group. The objective is to incorporate commitments that require high standards of behaviour from all involved with the Group and to provide a tool for optimising management. In 2002 the Board of Directors appointed a “Working Group for Rules of Conduct”. After a process of internal consultations, this Working Group submitted its conclusions to the Board of Directors at the end of the first half of 2003. The Code of Conduct was approved on July 30th 2003 and the process of divulgation was concluded on February 29th 2004. At the same time the Board of Directors also appointed an Ethics Committee to monitor the divulgation of and compliance with the Code of Conduct. The Code of Conduct is available for easy, free consultation on the Group’s institutional website, at www.jeronimo-martins.pt or may be requested from the Investor Relations Office.

3.2. Measures Likely to Interfere with Public Tender Offers No special rights are conferred upon shareholders or restraints on the exercise of voting rights are listed in the Company by-laws. As far as the Board of Directors is aware no shareholder agreements or any other arrangements exist that might interfere with public tenders. The Board of Directors feels that clear information must be provided in such matters and that the existence of such limitations may not be in the interest of shareholders. Chapter 4. Board of Directors 4.1. Description of the Board of Directors During the 2001-2003 mandate, the Board of Directors was composed of seven members, three of whom are Executive Members - Elísio Alexandre Soares dos Santos (Chairman of the Group), Luís Palha da Silva and Pedro Soares dos Santos - and four are Non-Executive Members - António Borges, Rui Patrício, Hans Eggerstedt and José Luís Nogueira de Brito.

Jerónimo Martins, SGPS, S.A.

31

According to the principles governing the Company, all Board Members are accountable to all shareholders equally, but the existence of Independent Board Members further reinforces the independence of the Board of Directors work in relation to shareholders. According to the last amendment to Article 1, paragraph 2 of the Securities and Exchange Commission’s Regulation no. 07/2001, Board members regarded as independent are Luís Palha da Silva, António Borges and Rui Patrício. Members of the Board of Directors also holding positions in other companies are as follows: Elísio Alexandre Soares dos Santos Member of the Supervisory Board of Banco Comercial Português, S.A. Member of the Board of Sindcom, SGPS, S.A. Pedro Soares dos Santos Member of the Board of Jerónimo Martins Serviços, S.A.* Member of the Board of Imocash - Imobiliário de Distribuição, S.A.* Member of the Board of Recheio Cash & Carry, S.A.* Member of the Board of Recheio, SGPS, S.A.* Member of the Board of Noredis-Sociedade de Representações e Distribuição do Norte S.A.* Member of the Board of Lidosol II - Distribuição de Produtos Alimentares, S.A.* Member of the Board of Funchalgest - Sociedade Gestora de Participações Sociais, S.A.* Member of the Board of Lidinvest - Gestão de Imóveis, S.A.* Member of the Board of Larantigo - Sociedade de Construções, S.A.* Manager of Idole Utilidades, Equipamentos e Investimentos Imobiliários, Lda* Member of the Board of João Gomes Camacho, S.A.* Member of the Board of JMR - Gestão de Empresas de Retalho, SGPS, S.A.* Member of the Board of FEIRA NOVA - Hipermercados, S.A.* Member of the Board of COMESPA - Gestão de Espaços Comerciais, S.A.* Member of the Board of GESTIRETALHO - Gestão e Consultoria para a Distribuição a Retalho, S.A.* Member of the Board of SUPERTUR - Imobiliária, Comércio e Turismo, S.A.* Member of the Board of IMORETALHO - Gestão de Imóveis, S.A.* Member of the Board of CUNHA & BRANCO - Distribuição Alimentar, S.A.* Member of the Board of MOSER & BRANCO - Distribuição Alimentar, S.A.* Member of the Board of DANTAS & VALE, S.A.* Member of the Board of PINGO DOCE - Distribuição Alimentar, S.A.* Member of the Board of CASAL DE S. PEDRO - Administração de Bens, S.A.* Manager of FRIEDMAN - Consultoria e Serviços, Lda* Manager of HERMES - Soc. de Investimentos Mobiliários e Imobiliários, Lda* Manager of SERVICOMPRA - Consultores de Aprovisionamento, Lda* Luís Palha da Silva Member of the Board of Jerónimo Martins Serviços, S.A.* Member of the Board of Jerónimo Martins Restauração e Serviços, S.A.* Member of the Board of JMR - Gestão de Empresas de Retalho, SGPS, S.A.* Member of the Board of LIDOSOL II - Distribuição de Produtos Alimentares, S.A.* Member of the Board of FUNCHALGEST - Sociedade Gestora de Participações Sociais, S.A.* Member of the Board of LIDINVEST - Gestão de Imóveis, S.A.* Member of the Board of JOÃO GOMES CAMACHO, S.A.* Manager of DESIMO - Desenvolvimento e Gestão Imobiliária, Lda* Manager of EVA - Sociedade de Investimentos Mobiliários e Imobiliários, Lda* Manager of FRIEDMAN - Consultoria e Serviços, Lda* Manager of HERMES - Sociedade de Investimentos Mobiliários e Imobiliários, Lda* Manager of IDOLE - Utilidades, Equipamentos e Investimentos Imobiliários, Lda* Manager of PSQ - Sociedade de Investimentos Mobiliários e Imobiliários, Lda* António Borges Vice-Chairman of Goldman Sachs International Member of the Supervisory Board of Sonae.com Chairman of Audit Board of Banco Santander de Portugal Chairman of Audit Board of Banco Santander de Negócios Portugal Hans Eggerstedt Member of Supervisory Board of Rodamco Europe N.V. Member of Supervisory Board of Unilever Deutschland Gmbh Non-Executive Director of Bolero.net Ltd. Non-Executive Director of Colt Telecom Group, plc Member of Advisory Board of the ING Group Member of Advisory Board of the Amsterdam Institute of Finance

* Companies that are part of Jerónimo Martins Group

Jerónimo Martins, SGPS, S.A.

32

Rui Patrício Member of Board of Directors of Monteiro Aranha, SA Member of Board of Directors of Monteiro Aranha Participações, SA Member of Board of Directors of Companhia Industrial São Paulo e Rio Member of Board of Directors of Klabin SA Member of Board of Directors of UAP International do Brasil Member of Board of Directors of Espírito Santo International Holding Member of Board of Directors of Portugal Telecom do Brasil Member of Board of Directors of Companhia Brasileira de Botucatu J. L. Nogueira de Brito Chairman of Board of Sociedade Francisco Manuel Santos, SGPS, S.A. Chairman of General Meeting of Douro - Sociedade Gestora de Participações Sociais, S.A. Álvaro Troncoso Director of Uniarme, crl 4.2. Executive Committee The main role of the Executive Committee is to assist the Board of Directors in the exercise of management functions. As a delegate body of the Board of Directors, and according to its regulation, the Executive Committee is responsible for exercising the following functions: