26

Jindal Poly Films Limited An Enterprise of the ‘B.C. Jindal Group’ Corporate Presentation November 2010 Private & Confidential 1

Jindal Poly Films LimitedAn Enterprise of the ‘B.C. Jindal Group’

Corporate Presentation

November 2010

Private & Confidential 1

Private & Confidential 2

Disclaimer

This presentation is strictly confidential and may not be copied, published, distributed or transmitted. The information in this presentation is being provided by Jindal Poly Films Limited (the “Company”).

This presentation has been prepared for information purposes only and is not an offer or invitation, directly or indirectly, to buy or sell any securities, nor shall part, or all, of this presentation form the basis at or be relied on in connection with, any contract or investment decision in relation to any securities. This presentation is not an offer document or a prospectus under the [Indian] Companies Act, 1956, as amended, the Securities and Exchange Board of India (Issue of Capital and Disclosure Requirements) Regulations, 2009, as amended and any other applicable law.

This presentation contains forward-looking statements based on the currently held beliefs and assumptions of the management of the Company, which are expressed in good faith and, in their opinion, reasonable. Forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause the actual results, financial condition, performance, or achievements of the Company or industry results, to differ materially from the results, financial condition, performance or achievements expressed or implied by such forward-looking statements. The risks and uncertainties relating to these statements include, but are not limited to, risks and uncertainties regarding expansion plans and the benefits there from, fluctuations in our earnings, our ability to manage growth and implement strategies, intense competition in our business including those factors which may affect our cost advantage, costs of raw materials, wage increases in India, our ability to attract and retain highly skilled professionals, time and cost overruns, changes in technology, availability of financing, our ability to successfully complete and integrate our expansion plans, liabilities, political instability and general economic conditions affecting our industries. Given these risks, uncertainties and other factors, recipients of this document are cautioned not to place undue reliance on these forward-looking statements. The Company disclaims any obligation to update these forward-looking statements to reflect future events or developments.

This presentation does not constitute an offer or invitation to purchase or subscribe for any securities in any jurisdiction, including the United States. None of our securities may be offered or sold in the United States, without registration under the U.S. Securities Act of 1933, as amended, or pursuant to an exemption from registration therefrom. Securities offered or sold outside of the United States are being offered or sold in compliance with the applicable laws of the jurisdiction where those offers and sales occur. There will be no public offer of the securities in the United States or in any other jurisdiction.By viewing this presentation you acknowledge that you will be solely responsible for your own assessment of the market and the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own view of the potential future performance of the business of the Company.

Except as otherwise noted, all of the information contained herein is indicative and is based on management information, current plans and estimates in the form as it has been disclosed in this presentation. Industry and market-related information is obtained or derived from industry publications and has not been verified by us. The information contained in this presentation, except as otherwise noted, is only current as of the date of the presentation, and is subject to change without notice. The Company may alter, modify or otherwise change in any manner the content of this presentation, without any obligation to notify any person of such revision or changes. Persons relying on the information in this presentation should do so at their own risk and the Company shall not be responsible for any kind of consequences or liability to any person arising out of, relying and acting upon any such information.

THIS PRESENTATION DOES NOT CONSTITUTE OR FORM ANY PART OF ANY OFFER, INVITATION OR RECOMMENDATION TO PURCHASE OR SUBSCRIBE FOR ANY SECURITIES IN THE UNITED STATES OR ELSEWHERE.

Private & Confidential 3

Agenda

Company Overview11

Industry Overview22

Business Highlights33

Power Generation Foray44

Future Growth Strategy55

Private & Confidential 4

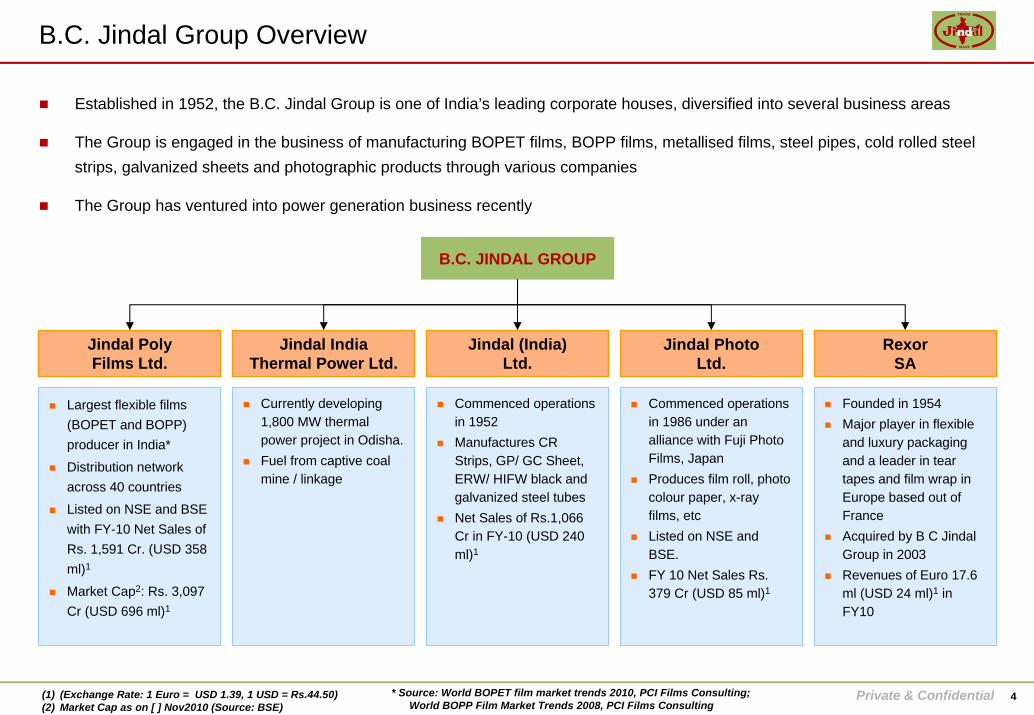

B.C. Jindal Group Overview

Established in 1952, the B.C. Jindal Group is one of India’s leading corporate houses, diversified into several business areas

The Group is engaged in the business of manufacturing BOPET films, BOPP films, metallised films, steel pipes, cold rolled steel strips, galvanized sheets and photographic products through various companies

The Group has ventured into power generation business recently

Jindal (India)Ltd.

B.C. JINDAL GROUP

Jindal PolyFilms Ltd.

RexorSA

Jindal PhotoLtd.

Largest flexible films (BOPET and BOPP) producer in India*

Distribution network across 40 countries

Listed on NSE and BSE with FY-10 Net Sales of Rs. 1,591 Cr. (USD 358 ml)1

Market Cap2: Rs. 3,097 Cr (USD 696 ml)1

Commenced operations in 1952Manufactures CR Strips, GP/ GC Sheet, ERW/ HIFW black and galvanized steel tubesNet Sales of Rs.1,066 Cr in FY-10 (USD 240 ml)1

Founded in 1954Major player in flexible and luxury packaging and a leader in tear tapes and film wrap in Europe based out of FranceAcquired by B C Jindal Group in 2003Revenues of Euro 17.6 ml (USD 24 ml)1 in FY10

Commenced operations in 1986 under an alliance with Fuji Photo Films, JapanProduces film roll, photo colour paper, x-ray films, etcListed on NSE and BSE.FY 10 Net Sales Rs. 379 Cr (USD 85 ml)1

Jindal India Thermal Power Ltd.

Currently developing 1,800 MW thermal power project in Odisha.Fuel from captive coal mine / linkage

(1) (Exchange Rate: 1 Euro = USD 1.39, 1 USD = Rs.44.50)(2) Market Cap as on [ ] Nov2010 (Source: BSE)

* Source: World BOPET film market trends 2010, PCI Films Consulting; World BOPP Film Market Trends 2008, PCI Films Consulting

Private & Confidential 5

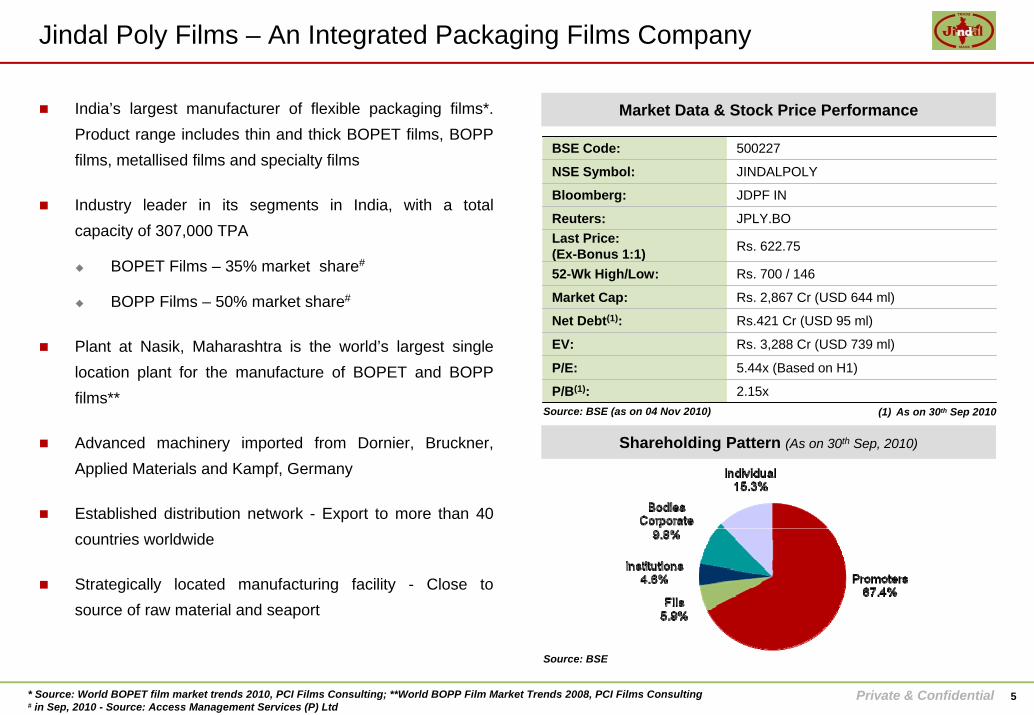

Jindal Poly Films – An Integrated Packaging Films Company

India’s largest manufacturer of flexible packaging films*. Product range includes thin and thick BOPET films, BOPP films, metallised films and specialty films

Industry leader in its segments in India, with a total capacity of 307,000 TPA

BOPET Films – 35% market share#

BOPP Films – 50% market share#

Plant at Nasik, Maharashtra is the world’s largest single location plant for the manufacture of BOPET and BOPP films**

Advanced machinery imported from Dornier, Bruckner, Applied Materials and Kampf, Germany

Established distribution network - Export to more than 40 countries worldwide

Strategically located manufacturing facility - Close to source of raw material and seaport

Shareholding Pattern (As on 30th Sep, 2010)

Market Data & Stock Price Performance

BSE Code: 500227

NSE Symbol: JINDALPOLY

Bloomberg: JDPF IN

Reuters: JPLY.BOLast Price:(Ex-Bonus 1:1) Rs. 622.75

52-Wk High/Low: Rs. 700 / 146

Market Cap: Rs. 2,867 Cr (USD 644 ml)

Net Debt(1): Rs.421 Cr (USD 95 ml)

EV: Rs. 3,288 Cr (USD 739 ml)

P/E: 5.44x (Based on H1)

P/B(1): 2.15xSource: BSE (as on 04 Nov 2010) (1) As on 30th Sep 2010

Source: BSE

* Source: World BOPET film market trends 2010, PCI Films Consulting; **World BOPP Film Market Trends 2008, PCI Films Consulting# in Sep, 2010 - Source: Access Management Services (P) Ltd

Private & Confidential 6

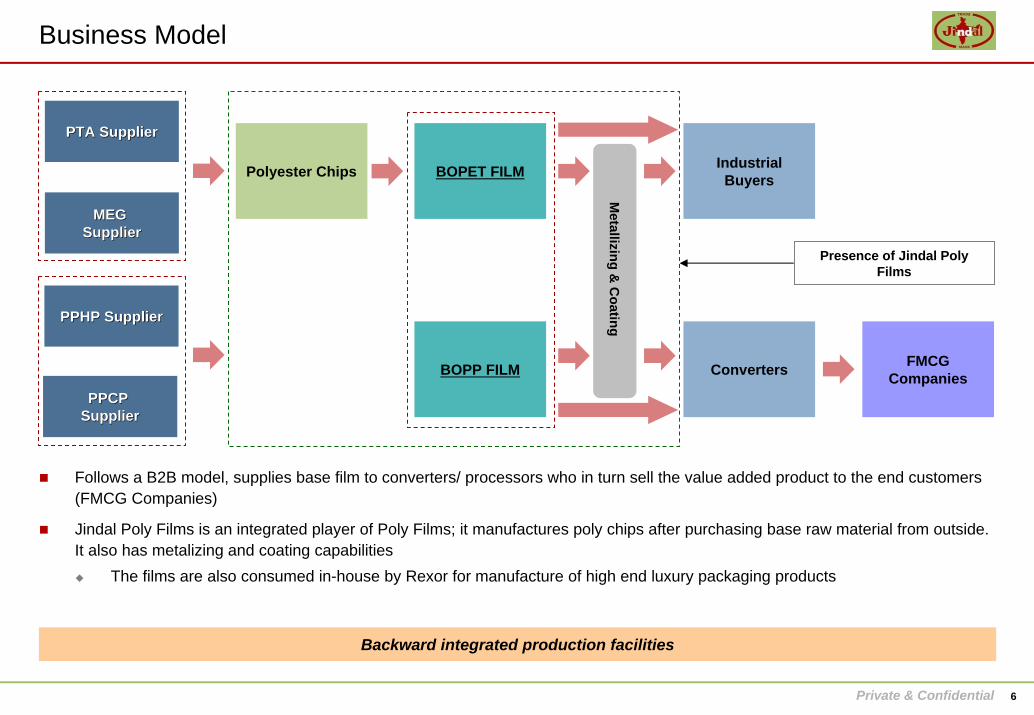

Business Model

Follows a B2B model, supplies base film to converters/ processors who in turn sell the value added product to the end customers (FMCG Companies)

Jindal Poly Films is an integrated player of Poly Films; it manufactures poly chips after purchasing base raw material from outside. It also has metalizing and coating capabilities

The films are also consumed in-house by Rexor for manufacture of high end luxury packaging products

Backward integrated production facilities

Polyester Chips BOPET FILM

BOPP FILM

PTA SupplierPTA Supplier

MEG MEG SupplierSupplier

Metallizing &

Coating

IndustrialBuyers

Converters FMCGCompanies

Presence of Jindal Poly Films

PPHP SupplierPPHP Supplier

PPCP PPCP SupplierSupplier

Private & Confidential 7

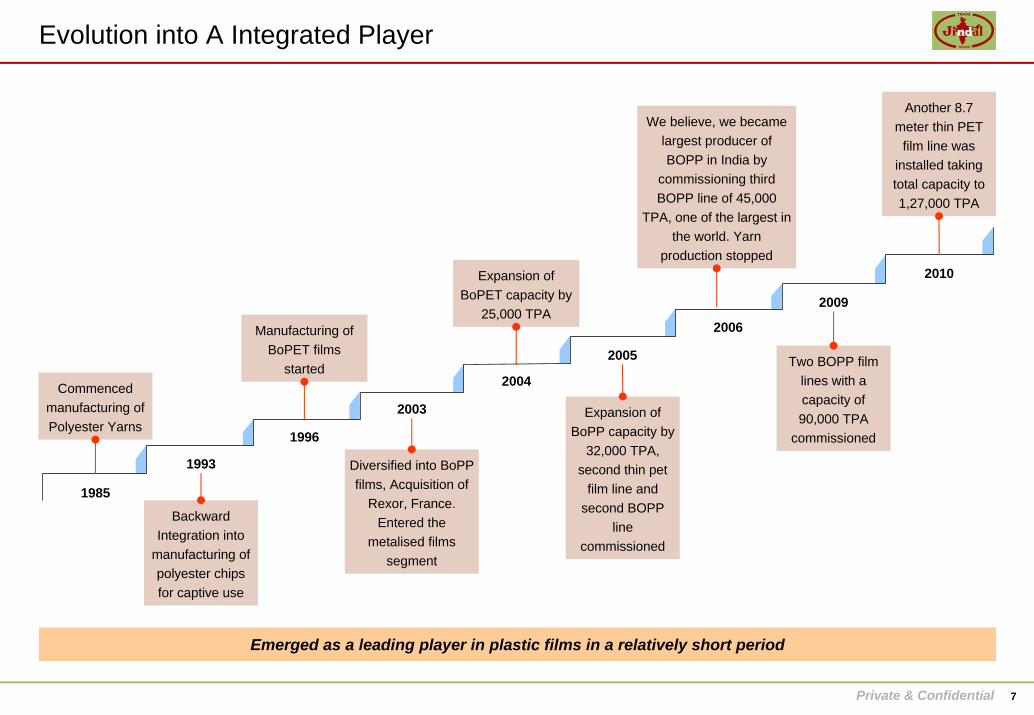

Evolution into A Integrated Player

1985

1993

1996

2003

2004

2005

2006

2009

2010

Commenced manufacturing of Polyester Yarns

Backward Integration into

manufacturing of polyester chips for captive use

Manufacturing of BoPET films

started

Diversified into BoPP films, Acquisition of

Rexor, France. Entered the

metalised films segment

Expansion of BoPET capacity by

25,000 TPA

Expansion of BoPP capacity by

32,000 TPA, second thin pet

film line and second BOPP

line commissioned

We believe, we became largest producer of BOPP in India by

commissioning third BOPP line of 45,000

TPA, one of the largest in the world. Yarn

production stopped

Two BOPP film lines with a capacity of 90,000 TPA

commissioned

Another 8.7 meter thin PET

film line was installed taking total capacity to 1,27,000 TPA

Emerged as a leading player in plastic films in a relatively short period

Private & Confidential 8

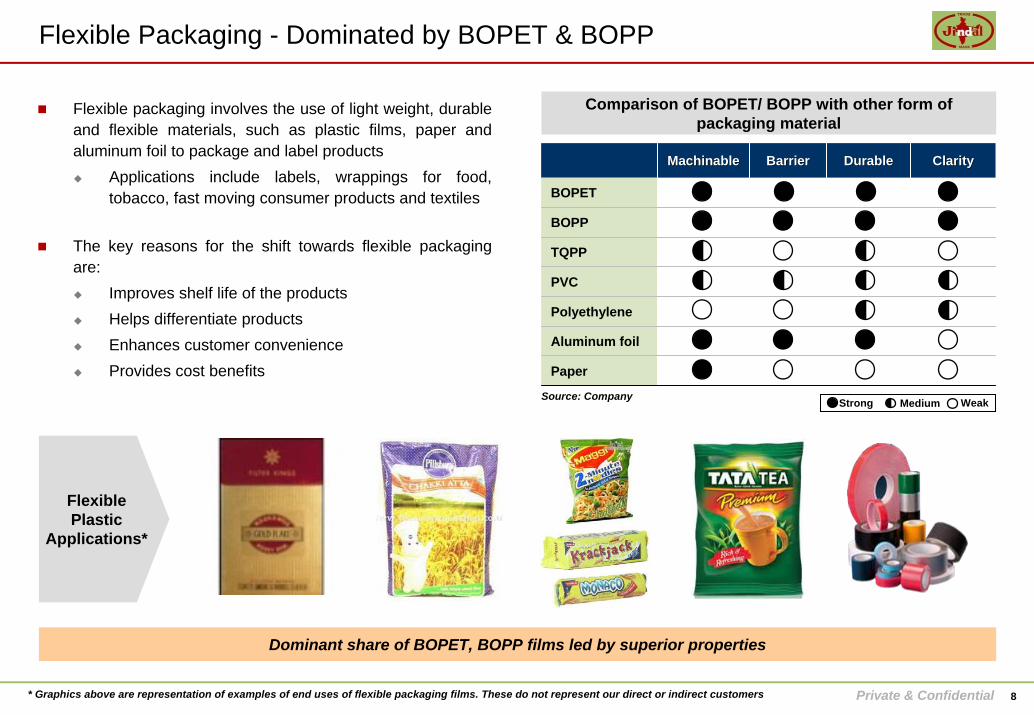

Flexible Packaging - Dominated by BOPET & BOPP

Comparison of BOPET/ BOPP with other form of packaging material

MachinableMachinable BarrierBarrier DurableDurable ClarityClarity

BOPET

BOPP

TQPP

PVC

Polyethylene

Aluminum foil

Paper

Dominant share of BOPET, BOPP films led by superior properties

Flexible Plastic

Applications*

Source: Company Strong Medium Weak

* Graphics above are representation of examples of end uses of flexible packaging films. These do not represent our direct or indirect customers

Flexible packaging involves the use of light weight, durable and flexible materials, such as plastic films, paper and aluminum foil to package and label products

Applications include labels, wrappings for food, tobacco, fast moving consumer products and textiles

The key reasons for the shift towards flexible packaging are:

Improves shelf life of the productsHelps differentiate productsEnhances customer convenienceProvides cost benefits

Private & Confidential 9

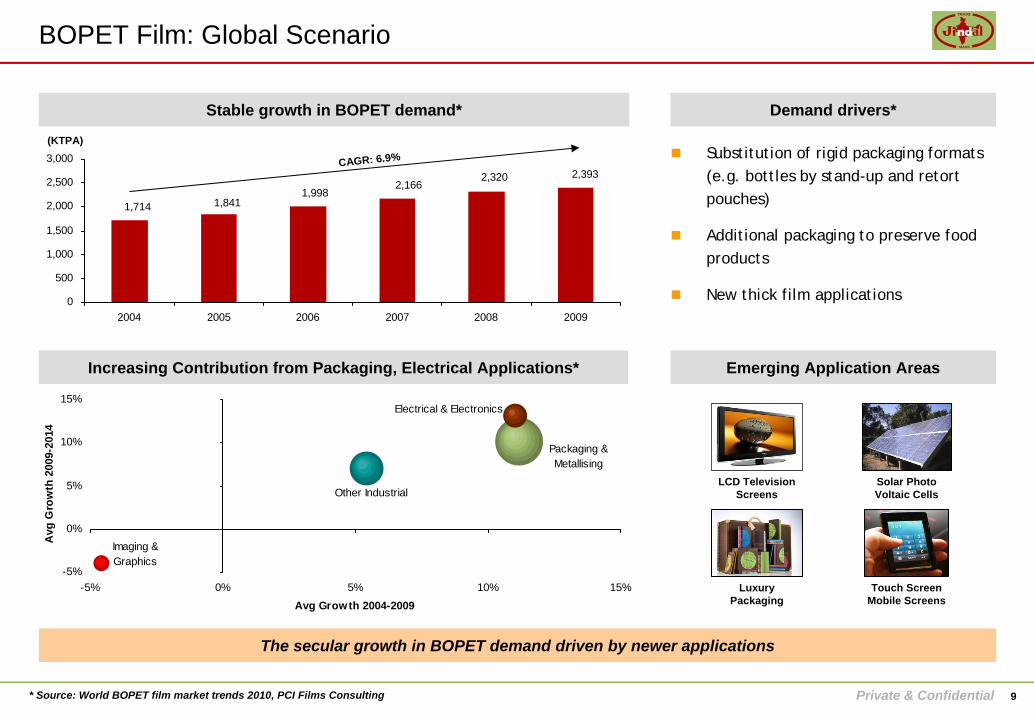

BOPET Film: Global Scenario

1,714 1,8411,998

2,1662,320 2,393

0

500

1,000

1,500

2,000

2,500

3,000

2004 2005 2006 2007 2008 2009

The secular growth in BOPET demand driven by newer applications

Luxury Packaging

Solar Photo Voltaic Cells

LCD Television Screens

Touch Screen Mobile Screens

Increasing Contribution from Packaging, Electrical Applications*

CAGR: 6.9%

Stable growth in BOPET demand* Demand drivers*

Emerging Application Areas

Substitution of rigid packaging formats (e.g. bottles by stand-up and retort pouches)

Additional packaging to preserve food products

New thick film applications

Imaging &Graphics

Other Industrial

Packaging &Metallising

Electrical & Electronics

-5%

0%

5%

10%

15%

-5% 0% 5% 10% 15%

Avg Growth 2004-2009

Avg

Gro

wth

200

9-20

14

(KTPA)

* Source: World BOPET film market trends 2010, PCI Films Consulting

Private & Confidential 10

5,117

3,550 3,8534,188 4,532

4,906

0

1,000

2,000

3,000

4,000

5,000

6,000

2003 2004 2005 2006 2007 2008

(KTPA)

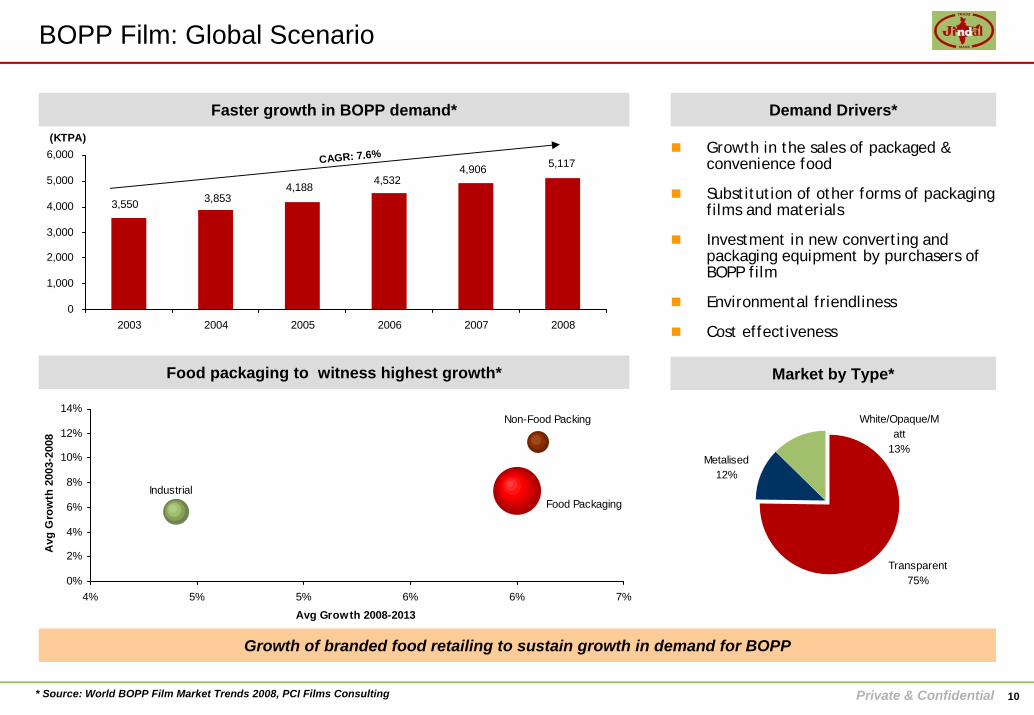

BOPP Film: Global Scenario

Growth of branded food retailing to sustain growth in demand for BOPP

Food packaging to witness highest growth*

Faster growth in BOPP demand* Demand Drivers*

Growth in the sales of packaged & convenience food

Substitution of other forms of packaging films and materials

Investment in new converting and packaging equipment by purchasers of BOPP film

Environmental friendliness

Cost effectiveness

Non-Food Packing

Food PackagingIndustrial

0%

2%

4%

6%

8%

10%

12%

14%

4% 5% 5% 6% 6% 7%

Avg Growth 2008-2013

Avg

Gro

wth

200

3-20

08

CAGR: 7.6%

Transparent75%

White/Opaque/Matt

13%Metalised

12%

Market by Type*

* Source: World BOPP Film Market Trends 2008, PCI Films Consulting

Private & Confidential 11

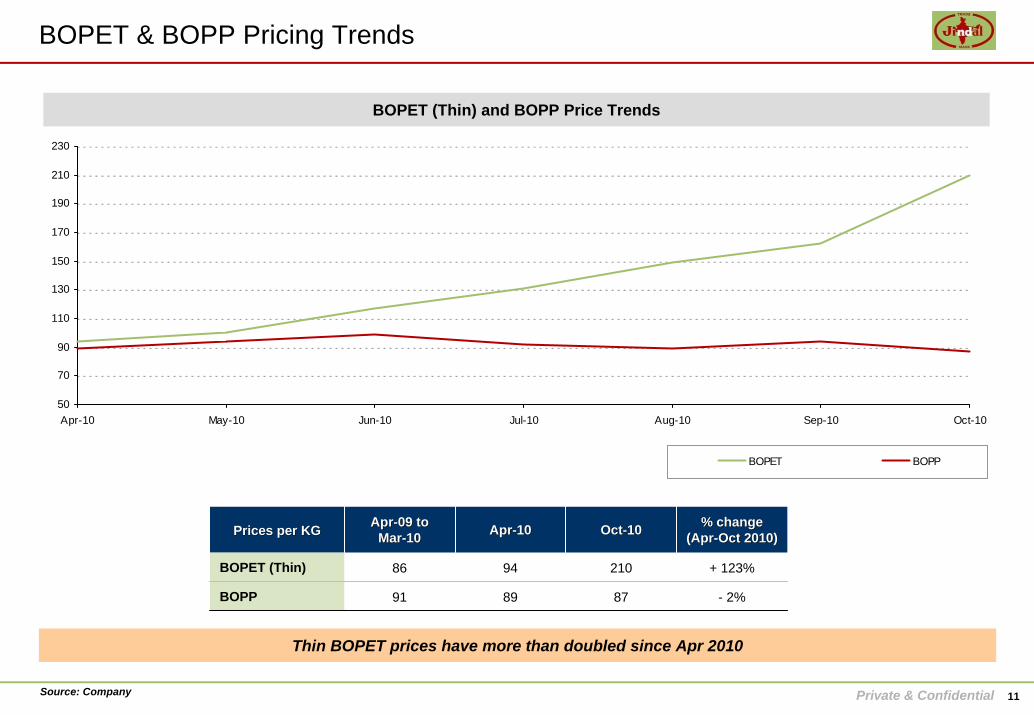

BOPET & BOPP Pricing Trends

50

70

90

110

130

150

170

190

210

230

Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10 Oct-10

BOPET BOPP

BOPET (Thin) and BOPP Price Trends

Thin BOPET prices have more than doubled since Apr 2010

Source: Company

Prices per KGPrices per KG AprApr--09 to 09 to MarMar--1010 AprApr--1010 OctOct--1010 % change % change

(Apr(Apr--Oct 2010)Oct 2010)

BOPET (Thin) 86 94 210 + 123%

BOPP 91 89 87 - 2%

Private & Confidential 12

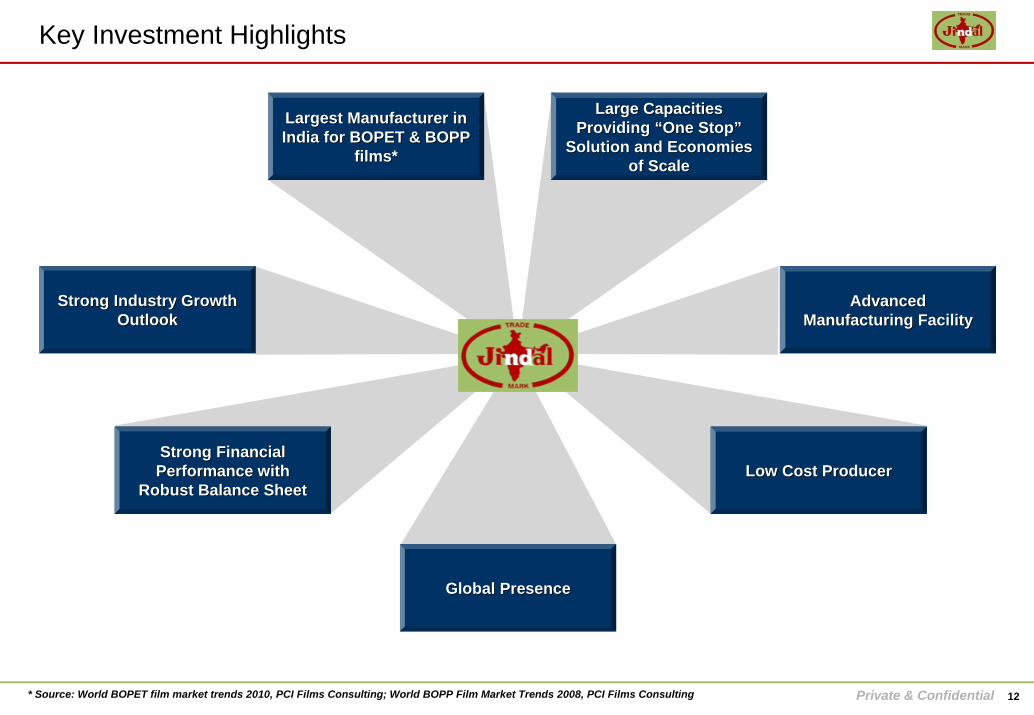

Key Investment Highlights

Largest Manufacturer in Largest Manufacturer in India for BOPET & BOPP India for BOPET & BOPP

films*films*

Strong Financial Strong Financial Performance with Performance with

Robust Balance SheetRobust Balance Sheet

Global PresenceGlobal Presence

Low Cost ProducerLow Cost Producer

Large Capacities Large Capacities Providing Providing ““One StopOne Stop””

Solution and Economies Solution and Economies of Scaleof Scale

Strong Industry Growth Strong Industry Growth OutlookOutlook

Advanced Advanced Manufacturing FacilityManufacturing Facility

* Source: World BOPET film market trends 2010, PCI Films Consulting; World BOPP Film Market Trends 2008, PCI Films Consulting

Private & Confidential 13

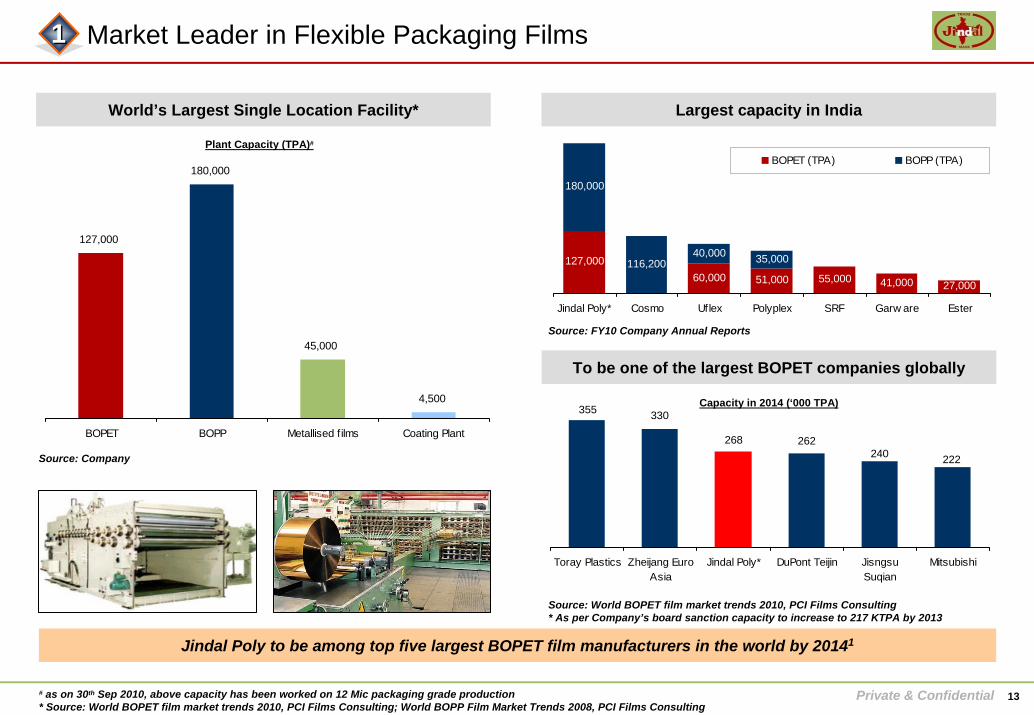

Market Leader in Flexible Packaging Films

127,000

180,000

45,000

4,500

BOPET BOPP Metallised films Coating Plant

World’s Largest Single Location Facility*

Jindal Poly to be among top five largest BOPET film manufacturers in the world by 20141

11

Largest capacity in India

Plant Capacity (TPA)#

127,00060,000 51,000 55,000 41,000 27,000

180,000

116,20040,000 35,000

Jindal Poly* Cosmo Uflex Polyplex SRF Garw are Ester

BOPET (TPA) BOPP (TPA)

To be one of the largest BOPET companies globally

262

222240268

330355

Toray Plastics Zheijang EuroAsia

Jindal Poly* DuPont Teijin JisngsuSuqian

Mitsubishi

Capacity in 2014 (‘000 TPA)

Source: Company

Source: FY10 Company Annual Reports

Source: World BOPET film market trends 2010, PCI Films Consulting* As per Company’s board sanction capacity to increase to 217 KTPA by 2013

# as on 30th Sep 2010, above capacity has been worked on 12 Mic packaging grade production* Source: World BOPET film market trends 2010, PCI Films Consulting; World BOPP Film Market Trends 2008, PCI Films Consulting

Private & Confidential 14

Wide Product Portfolio Catering to Diverse Application Markets

“One-Stop-Shop”

One of the few players globally to be able to offer a range of thin and thick BOPET film and BOPP film products

22

Consumer Products

Food packaging

Adhesivetapes

Magnetic media, imaging

Luxury Packaging

Solar Photo Voltaic Cells

Security Threads in Currency Notes

Tear Tapes

Emerging Applications

Specialty Products

Private & Confidential 15

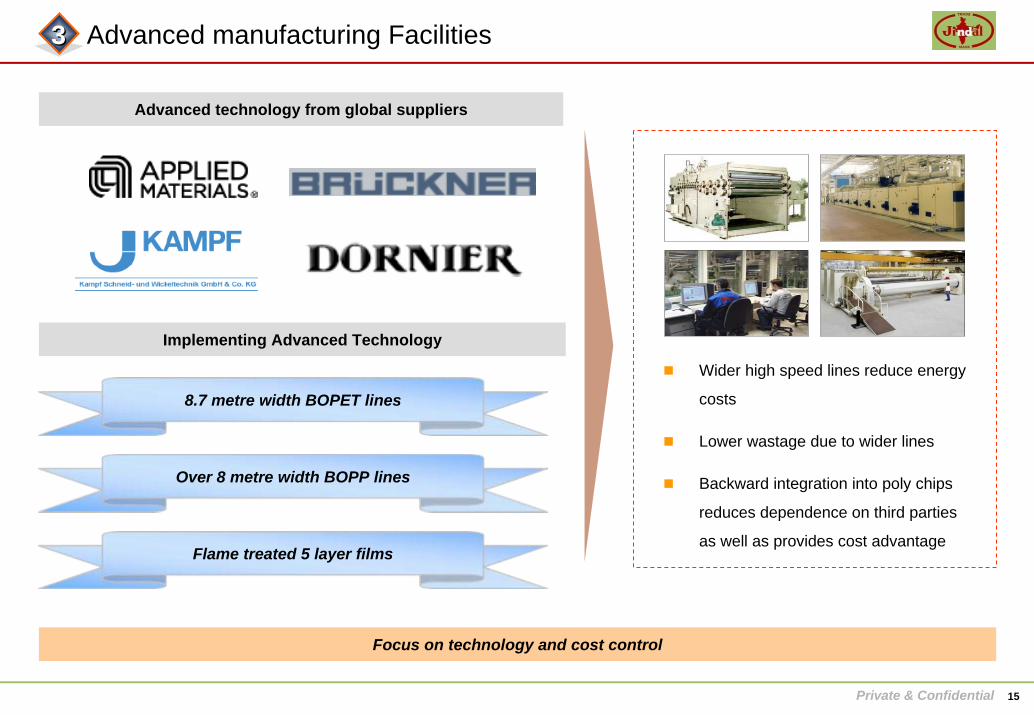

Advanced manufacturing Facilities33

Implementing Advanced Technology

Advanced technology from global suppliers

8.7 metre width BOPET lines

Over 8 metre width BOPP lines

Flame treated 5 layer films

Wider high speed lines reduce energy

costs

Lower wastage due to wider lines

Backward integration into poly chips

reduces dependence on third parties

as well as provides cost advantage

Focus on technology and cost control

Private & Confidential 16

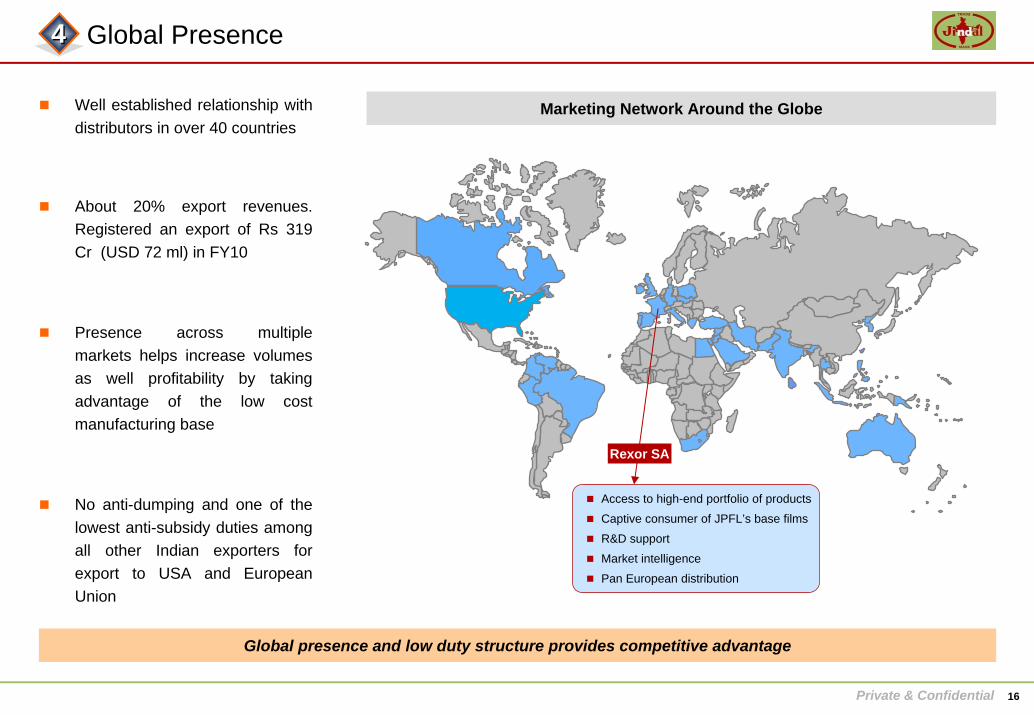

Global Presence

Well established relationship with distributors in over 40 countries

About 20% export revenues. Registered an export of Rs 319 Cr (USD 72 ml) in FY10

Presence across multiple markets helps increase volumes as well profitability by taking advantage of the low cost manufacturing base

No anti-dumping and one of the lowest anti-subsidy duties among all other Indian exporters for export to USA and European Union

Marketing Network Around the Globe

Access to high-end portfolio of products

Captive consumer of JPFL’s base films

R&D support

Market intelligence

Pan European distribution

Global presence and low duty structure provides competitive advantage

Rexor SA

44

Private & Confidential 17

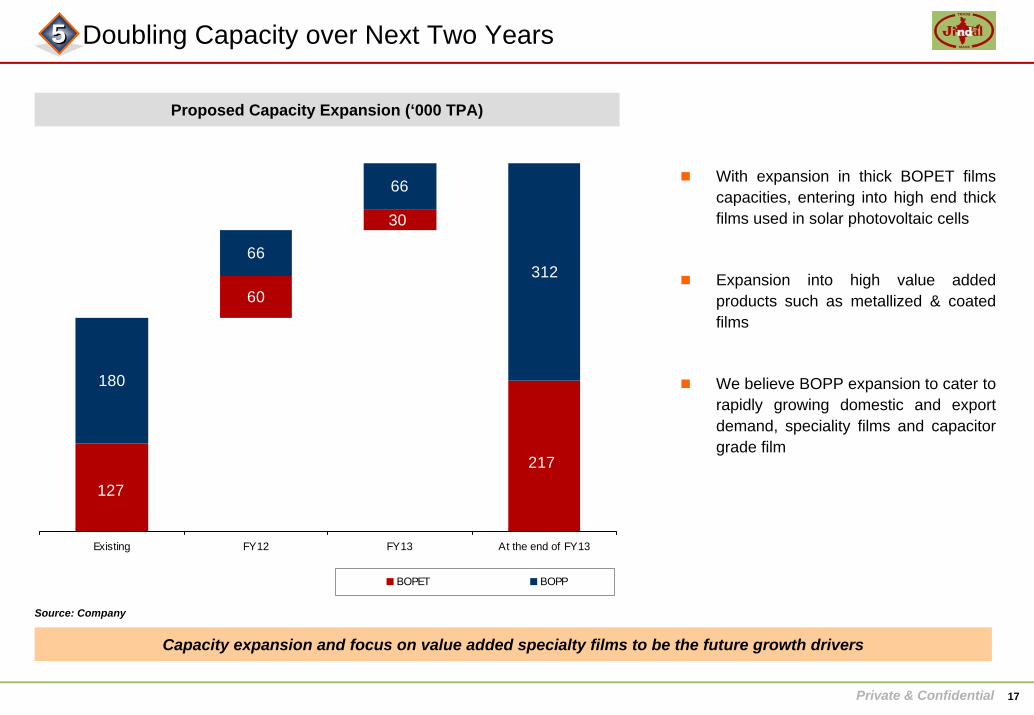

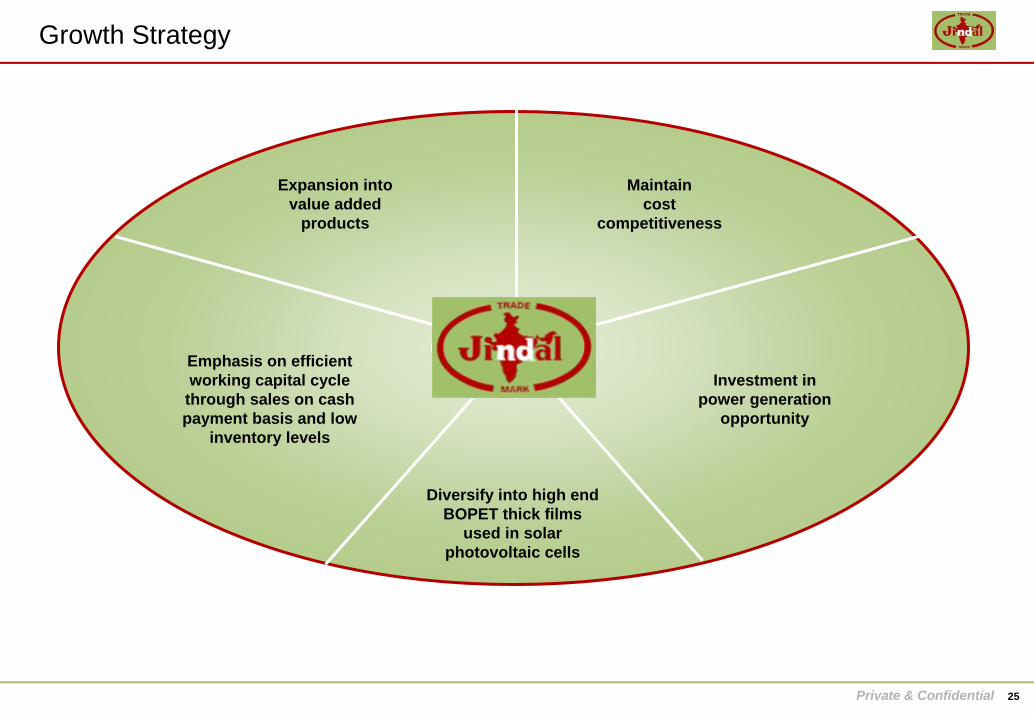

Doubling Capacity over Next Two Years 55

Capacity expansion and focus on value added specialty films to be the future growth drivers

With expansion in thick BOPET films capacities, entering into high end thick films used in solar photovoltaic cells

Expansion into high value added products such as metallized & coated films

We believe BOPP expansion to cater to rapidly growing domestic and export demand, speciality films and capacitor grade film

180

66

66

312

217

30

60

127

Existing FY12 FY13 At the end of FY13

BOPET BOPP

Proposed Capacity Expansion (‘000 TPA)

Source: Company

Private & Confidential 18

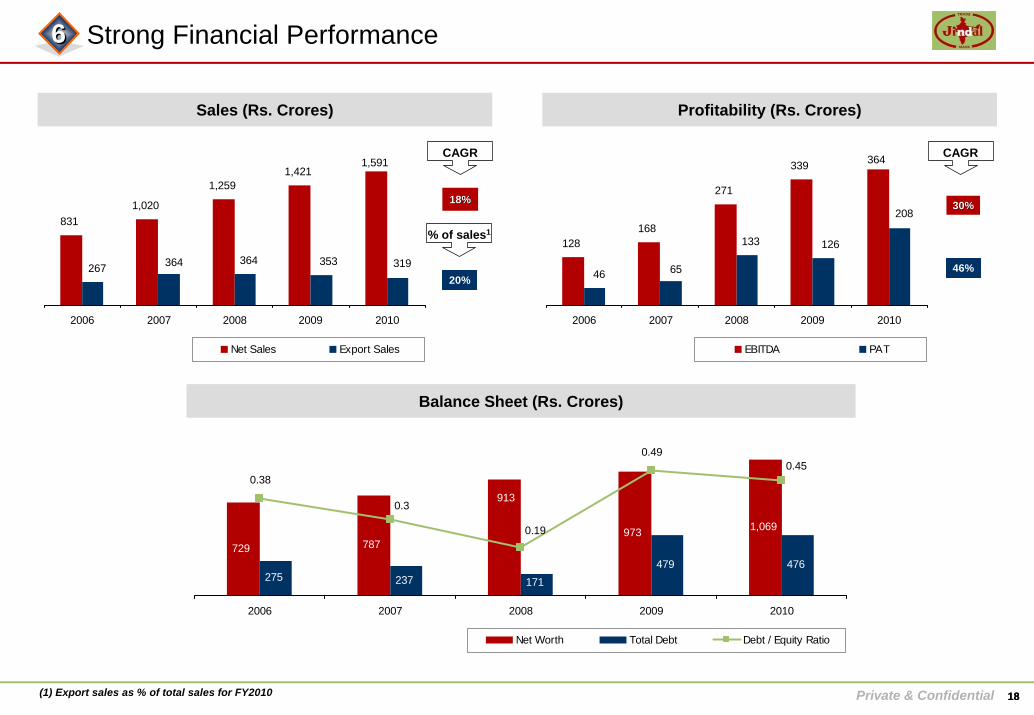

Strong Financial Performance

Sales (Rs. Crores)

8311,020

1,2591,421

1,591

267 364 364 353 319

2006 2007 2008 2009 2010

Net Sales Export Sales

Profitability (Rs. Crores)

18%18%

128168

271

339 364

46 65

133 126

208

2006 2007 2008 2009 2010

EBITDA PAT

CAGR

30%30%

46%

Balance Sheet (Rs. Crores)

729 787973 1,069

913

275 237 171479 476

0.45

0.19

0.3

0.38

0.49

2006 2007 2008 2009 2010

Net Worth Total Debt Debt / Equity Ratio

66

% of sales1

20%

CAGR

(1) Export sales as % of total sales for FY2010 18

Private & Confidential

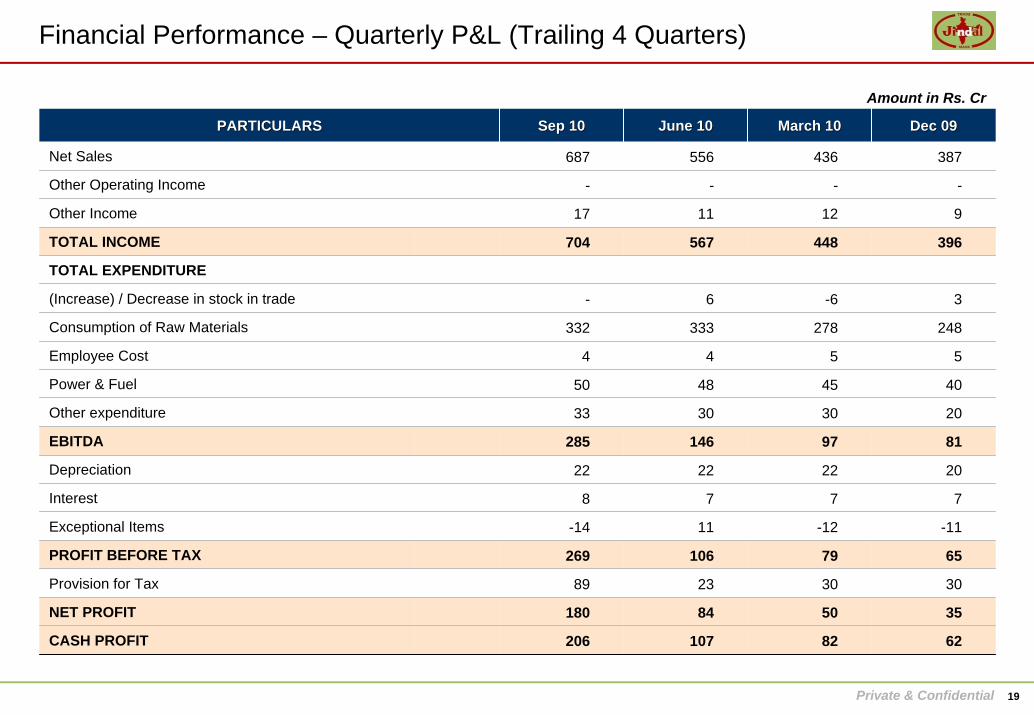

Financial Performance – Quarterly P&L (Trailing 4 Quarters)

Amount in Rs. Cr

PARTICULARSPARTICULARS Sep 10Sep 10 June 10June 10 March 10March 10 Dec 09Dec 09

Net Sales 687 556 436 387

Other Operating Income - - - -

Other Income 17 11 12 9

TOTAL INCOME 704 567 448 396

TOTAL EXPENDITURE

(Increase) / Decrease in stock in trade - 6 -6 3

Consumption of Raw Materials 332 333 278 248

Employee Cost 4 4 5 5

Power & Fuel 50 48 45 40

Other expenditure 33 30 30 20

EBITDA 285 146 97 81

Depreciation 22 22 22 20

Interest 8 7 7 7

Exceptional Items -14 11 -12 -11

PROFIT BEFORE TAX 269 106 79 65

Provision for Tax 89 23 30 30

NET PROFIT 180 84 50 35

CASH PROFIT 206 107 82 62

19

Private & Confidential

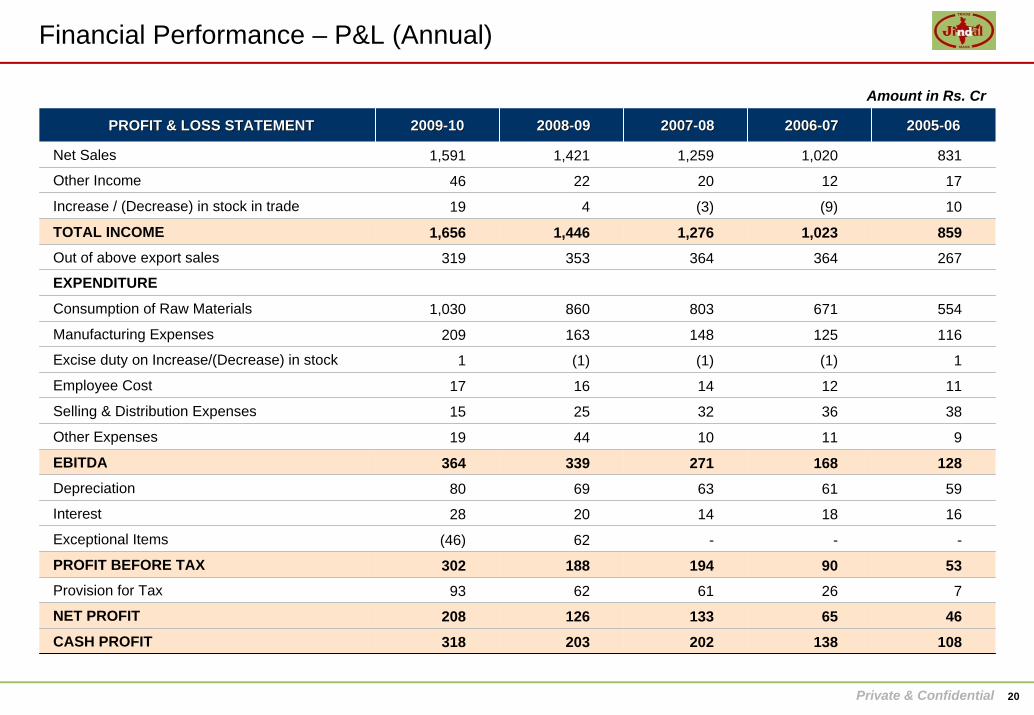

Financial Performance – P&L (Annual)

Amount in Rs. Cr

PROFIT & LOSS STATEMENTPROFIT & LOSS STATEMENT 20092009--1010 20082008--0909 20072007--0808 20062006--0707 20052005--0606

Net Sales 1,591 1,421 1,259 1,020 831

Other Income 46 22 20 12 17

Increase / (Decrease) in stock in trade 19 4 (3) (9) 10

TOTAL INCOME 1,656 1,446 1,276 1,023 859 Out of above export sales 319 353 364 364 267

EXPENDITURE

Consumption of Raw Materials 1,030 860 803 671 554

Manufacturing Expenses 209 163 148 125 116

Excise duty on Increase/(Decrease) in stock 1 (1) (1) (1) 1

Employee Cost 17 16 14 12 11

Selling & Distribution Expenses 15 25 32 36 38

Other Expenses 19 44 10 11 9

EBITDA 364 339 271 168 128 Depreciation 80 69 63 61 59

Interest 28 20 14 18 16

Exceptional Items (46) 62 - - -

PROFIT BEFORE TAX 302 188 194 90 53 Provision for Tax 93 62 61 26 7

NET PROFIT 208 126 133 65 46 CASH PROFIT 318 203 202 138 108

20

Private & Confidential

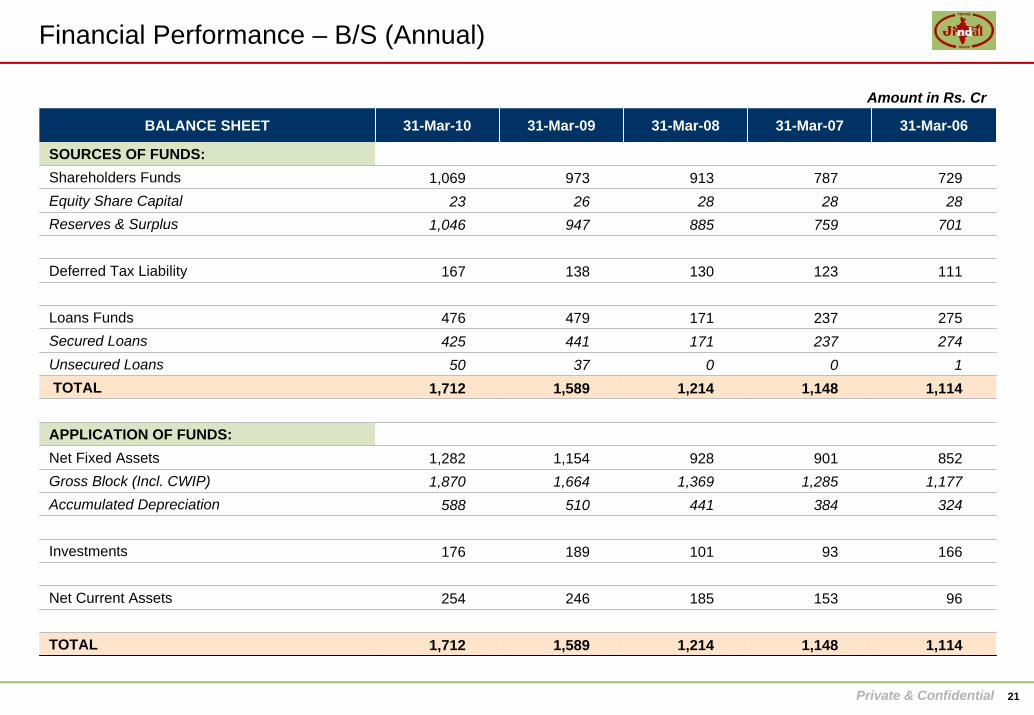

Financial Performance – B/S (Annual)

Amount in Rs. Cr

BALANCE SHEET 31-Mar-10 31-Mar-09 31-Mar-08 31-Mar-07 31-Mar-06

SOURCES OF FUNDS:Shareholders Funds 1,069 973 913 787 729Equity Share Capital 23 26 28 28 28Reserves & Surplus 1,046 947 885 759 701

Deferred Tax Liability 167 138 130 123 111

Loans Funds 476 479 171 237 275Secured Loans 425 441 171 237 274Unsecured Loans 50 37 0 0 1TOTAL 1,712 1,589 1,214 1,148 1,114

APPLICATION OF FUNDS:Net Fixed Assets 1,282 1,154 928 901 852Gross Block (Incl. CWIP) 1,870 1,664 1,369 1,285 1,177Accumulated Depreciation 588 510 441 384 324

Investments 176 189 101 93 166

Net Current Assets 254 246 185 153 96

TOTAL 1,712 1,589 1,214 1,148 1,114

21

Private & Confidential

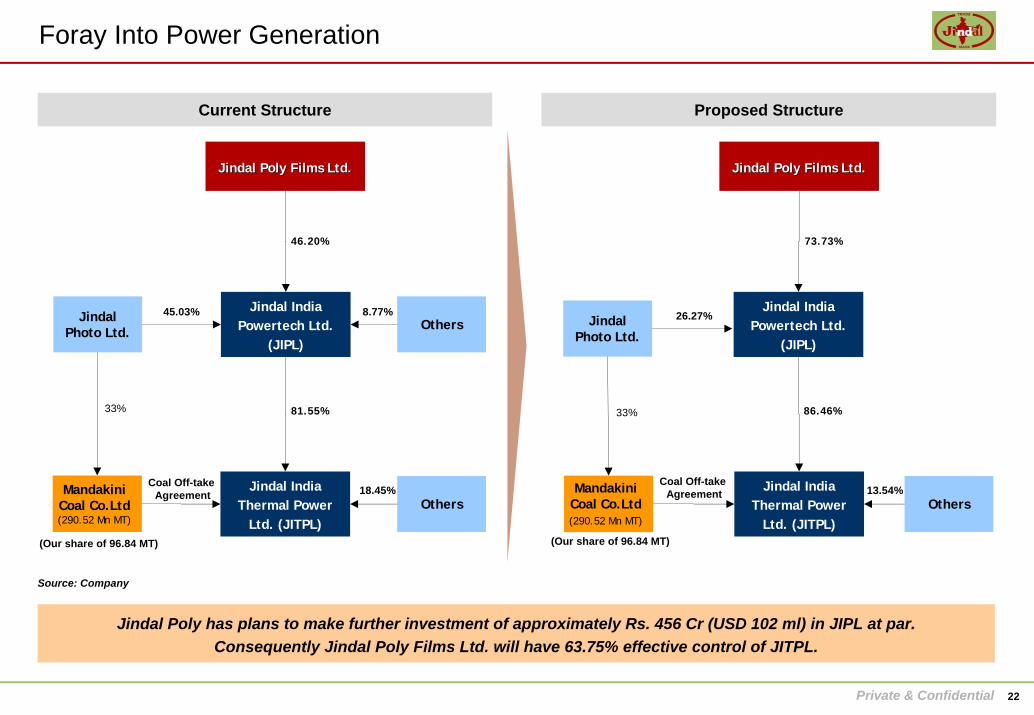

Foray Into Power Generation

Jindal India Powertech Ltd.

(JIPL)

Jindal India Thermal Power

Ltd. (JITPL)

81.55%

Jindal Poly Films Ltd.Jindal Poly Films Ltd.

46.20%

OthersJindal Photo Ltd.

8.77%45.03%

Current Structure Proposed Structure

Others18.45%

Jindal India Powertech Ltd.

(JIPL)

Jindal India Thermal Power

Ltd. (JITPL)

86.46%

Jindal Poly Films Ltd.Jindal Poly Films Ltd.

73.73%

Others13.54%

Jindal Poly has plans to make further investment of approximately Rs. 456 Cr (USD 102 ml) in JIPL at par. Consequently Jindal Poly Films Ltd. will have 63.75% effective control of JITPL.

Mandakini Coal Co.Ltd (290.52 Mn MT)

(Our share of 96.84 MT)

33%

Coal Off-take Agreement

Jindal Photo Ltd.

26.27%

Mandakini Coal Co.Ltd (290.52 Mn MT)

33%

Coal Off-take Agreement

(Our share of 96.84 MT)

22

Source: Company

Private & Confidential 23

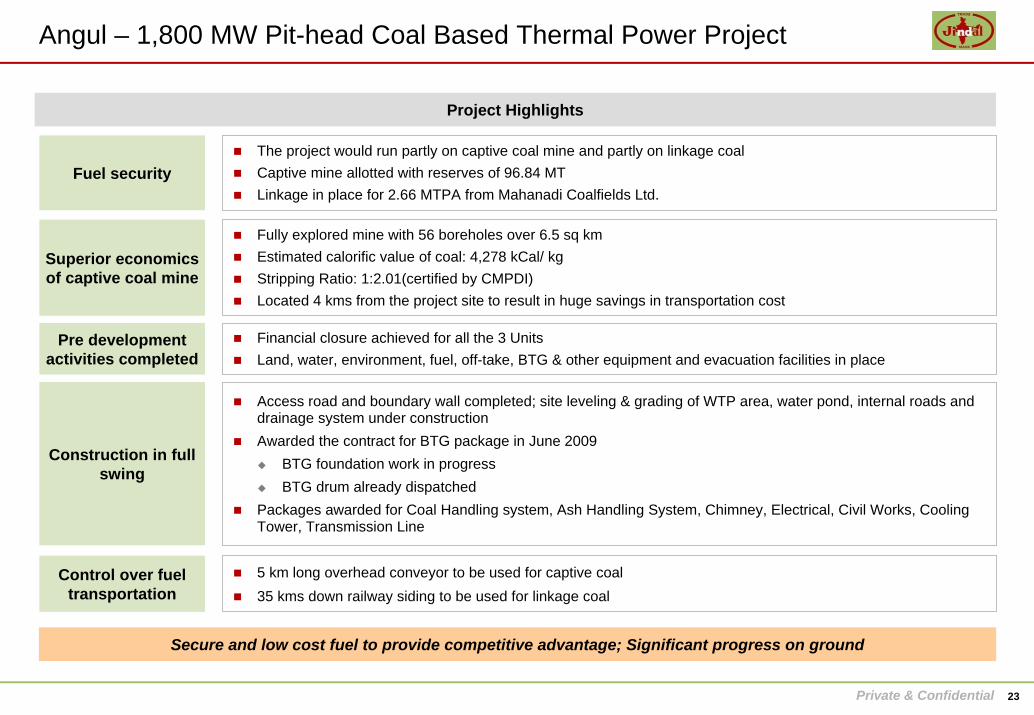

Angul – 1,800 MW Pit-head Coal Based Thermal Power Project

Secure and low cost fuel to provide competitive advantage; Significant progress on ground

Fuel security The project would run partly on captive coal mine and partly on linkage coalCaptive mine allotted with reserves of 96.84 MTLinkage in place for 2.66 MTPA from Mahanadi Coalfields Ltd.

Superior economics of captive coal mine

Fully explored mine with 56 boreholes over 6.5 sq kmEstimated calorific value of coal: 4,278 kCal/ kgStripping Ratio: 1:2.01(certified by CMPDI)Located 4 kms from the project site to result in huge savings in transportation cost

Pre development activities completed

Financial closure achieved for all the 3 UnitsLand, water, environment, fuel, off-take, BTG & other equipment and evacuation facilities in place

Construction in full swing

Access road and boundary wall completed; site leveling & grading of WTP area, water pond, internal roads and drainage system under constructionAwarded the contract for BTG package in June 2009

BTG foundation work in progressBTG drum already dispatched

Packages awarded for Coal Handling system, Ash Handling System, Chimney, Electrical, Civil Works, Cooling Tower, Transmission Line

Control over fuel transportation

5 km long overhead conveyor to be used for captive coal35 kms down railway siding to be used for linkage coal

Project Highlights

Private & Confidential 24

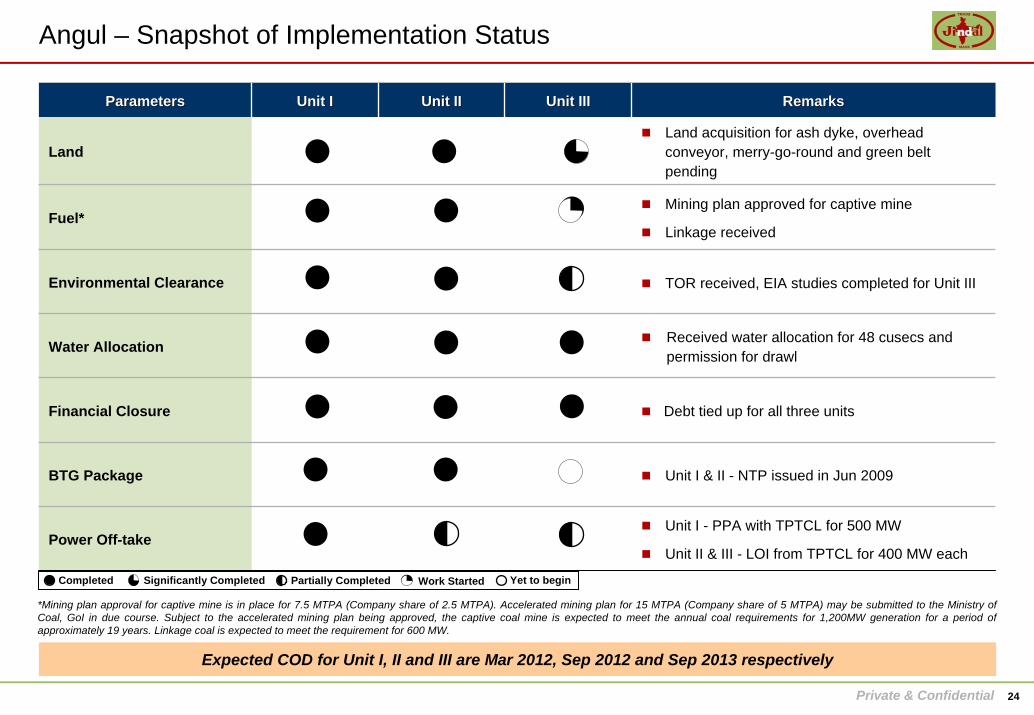

Angul – Snapshot of Implementation Status

ParametersParameters Unit IUnit I Unit IIUnit II Unit IIIUnit III RemarksRemarks

LandLand acquisition for ash dyke, overhead conveyor, merry-go-round and green belt pending

Fuel*Mining plan approved for captive mine

Linkage received

Environmental Clearance TOR received, EIA studies completed for Unit III

Water Allocation Received water allocation for 48 cusecs and permission for drawl

Financial Closure Debt tied up for all three units

BTG Package Unit I & II - NTP issued in Jun 2009

Power Off-takeUnit I - PPA with TPTCL for 500 MW

Unit II & III - LOI from TPTCL for 400 MW each

Expected COD for Unit I, II and III are Mar 2012, Sep 2012 and Sep 2013 respectively

*Mining plan approval for captive mine is in place for 7.5 MTPA (Company share of 2.5 MTPA). Accelerated mining plan for 15 MTPA (Company share of 5 MTPA) may be submitted to the Ministry of Coal, GoI in due course. Subject to the accelerated mining plan being approved, the captive coal mine is expected to meet the annual coal requirements for 1,200MW generation for a period of approximately 19 years. Linkage coal is expected to meet the requirement for 600 MW.

Completed Partially Completed Yet to begin Significantly Completed Work Started

Private & Confidential

Expansion into value added

products

Maintaincost

competitiveness

Investment in power generation

opportunity

Diversify into high end BOPET thick films

used in solar photovoltaic cells

Emphasis on efficient working capital cycle

through sales on cash payment basis and low

inventory levels

25

Growth Strategy

Thank You