32

John Lewis – Our Journey to Omni-Channel Customer Relationships Julian Burnett Head of IT Strategy, Architecture & Business Process April 2014

John Lewis – Our Journey to Omni-Channel Customer Relationships

Julian Burnett

Head of IT Strategy, Architecture & Business Process

April 2014

Shops +3.5% Online +19.2%

Results 2013/14: A ‘bricks and clicks’ success

In 1928 after the death of John Lewis,

Spedan acquired sole ownership of the

business.

He drew up the Partnership's first

Constitution and in 1929 the first Trust

Settlement was signed which allowed the

profits of the business to be distributed

amongst the employees.

John Spedan Lewis

1885 - 1963

Origins of the Partnership

John Spedan Lewis, 1929

Origins of the Partnership

We have always had a consistent Customer Proposition

• Value• Assortment• Service• Trust

Our Customers are at the heart of all we do

No conflict of interestNo external shareholders

Allow us to be

counter intuitive

The JLP business model: Our advantages

Purchase

of

buy.com

2001

Allow us to be

counter cyclical

From Evolution to Revolution

• From humble beginnings in Oxford Street in 1864 John Lewis today has...

• 42 John Lewis Shops

• £1bn Online business

• Financial Services

• Joint Ventures (Kuoni, Joe & The Juice, Hotel Chocolat)

• 30,000 Partners

• Sales 2013 £4bn

• Gross Profit 2013 £226.1m

• Bonus to staff 15% of annual in 2013

2.Become

truly Multi

Channel

1.Build JLD

3.Seize

BUSINESS-WIDEbrand

biggerness

Establish online presence Integrate Channels Amplify The Brand

Market matching

Multi Channel retailer

Two channels:

Shops and online

Market leading

Omni Channel retailer

Strategy

2001 2010 2012 >

Our omni-channel strategy has driven growth

Multi-channel

We have made integrated investment in our strategy

We have leveraged our stores to drive omni-channel growth

2010 2011 2012 2013Our stores - The best omni-

channel recruitment tool we

have!

We have seen dramatic uptake of our Click & Collect service

2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

H1 H2

• Over a third of all online sales

• 57% growth in 2013

We offer our Click & Collect customers convenience

New Locations: Birmingham–Leeds–Westfield London–York–Heathrow–Chelmsford–Oxford–Horsham–Basingstoke and more…

Birmingham

2015

FLDSSFLDS

York

Opened 10 Apr 2014

At home

Ashford

Opened Nov 2013

We have an range of new store formats in new places

Heathrow

T2 Jun 2014

Travel

From the defining market moment in 2008 we have seen online sales grow to over 30% of our annual revenue

SIZE OF JL.COM JAN 2008

£269mSIZE OF JL.COM JAN 2013

>£1b

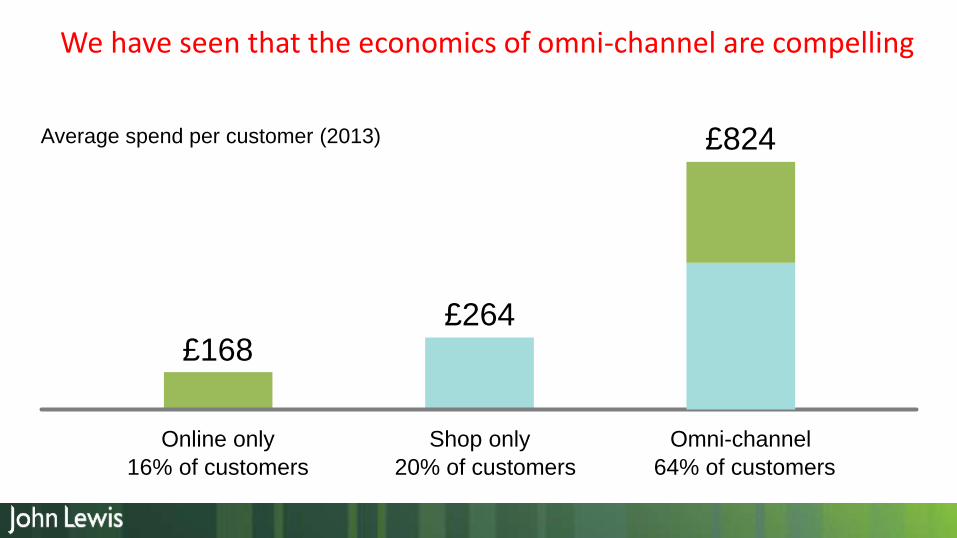

We have seen that the economics of omni-channel are compelling

3.5 xAverage spend per customer (2013)

£168

Online only

£264

Shop only

16% of customers 20% of customers

We have seen that the economics of omni-channel are compelling

Average spend per customer (2013)

£168

Online only

£264

Shop only Omni-channel

£824

16% of customers 20% of customers 64% of customers

9,500

10,000

10,500

11,000

10.07m

2012

Feb Apr May Jun Jul Aug Sep Oct Nov DecMar

10.95m

JL customers, rolling 12 months New target customers

Crave right brands

and new products

Use convenience of

online

Love shops

Provenance matters

We understand who are customers are and what they like

0 20,000 40,000 60,000 80,000 100,000

Debenhams

Royal Mail

Asda

Boots

Morrisons

Tesco

Marks & Spencer

Sainsbury's

John Lewis

Positive

Negative

Neutral

Balanced

SOURCE: Precise Media

Monitoring (December 2013)

Competitors

We use social networks to know what customers think about us

We have plenty of evidence to show our strategy is working.Two thirds of our customers now shop more than one channel.

Over 60% of johnlewis.com

customers buy in JL shops

33% of johnlewis.com sales

were “Click&Collect” in 2013

65% research online and

buy in a shop

30% research in a shop and

buy online50% of shop customers buy

at johnlewis.com

In store Mobile sales were up 120%

in 2013 50% of johnlewis.com traffic

is from mobile (28% 2012)

By telephone

Online

In Store

Mobile

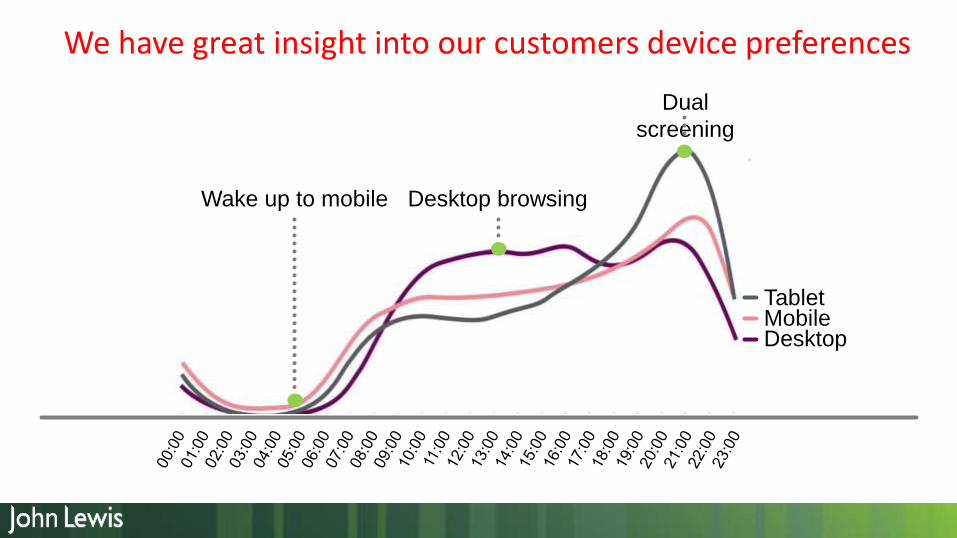

We have seen hyper growth in mobile with 50% of traffic coming from smart phones and tablets, contributing 29% of online sales

Wake up to mobile Desktop browsing

Dual

screening

TabletMobileDesktop

We have great insight into our customers device preferences

We are recognised as

an innovator and have

put technology

innovation at the heart

of the approach we

take to driving our

Omni-channel strategy

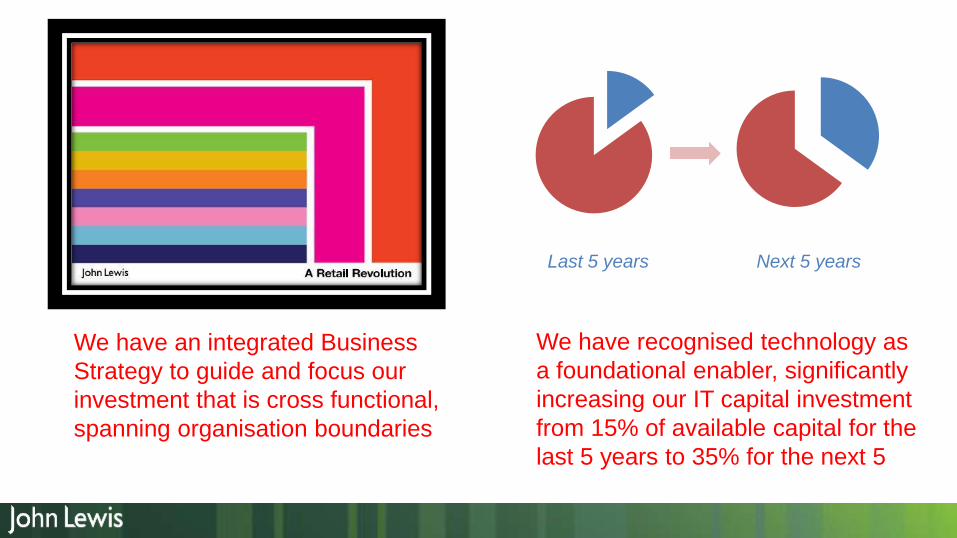

Last 5 years Next 5 years

We have an integrated Business

Strategy to guide and focus our

investment that is cross functional,

spanning organisation boundaries

We have recognised technology as

a foundational enabler, significantly

increasing our IT capital investment

from 15% of available capital for the

last 5 years to 35% for the next 5

We have an integrated training offer

for Partners to equip them with the

technology skills needed to deliver

Omni-channel service & sales

We have introduced new KPI’s and

measures to recognise the changing

channel mix of our business and

incentivise Omni-channel behaviour

We have created a specialist team

to ensure change projects deliver

business processes that are joined

up across our end to end business

operation

We are delivering an integrated IT

roadmap to ensure our technology

and data supports Partners and

Customers seamlessly and

consistently wherever they are

Bu

sin

es

s A

rch

itec

ture

Info

rma

tio

n A

rch

ite

ctu

re

Ap

pli

ca

tio

n A

rch

ite

ctu

re

Te

ch

nic

al A

rch

itec

ture

We have strengthened our

Architecture capability and created

a framework to ensure all aspects

of change – people, process,

information and

technology – are

planned, designed

and delivered in an

integrated and

capital efficient way

Info

rma

tio

n A

rch

itec

ture

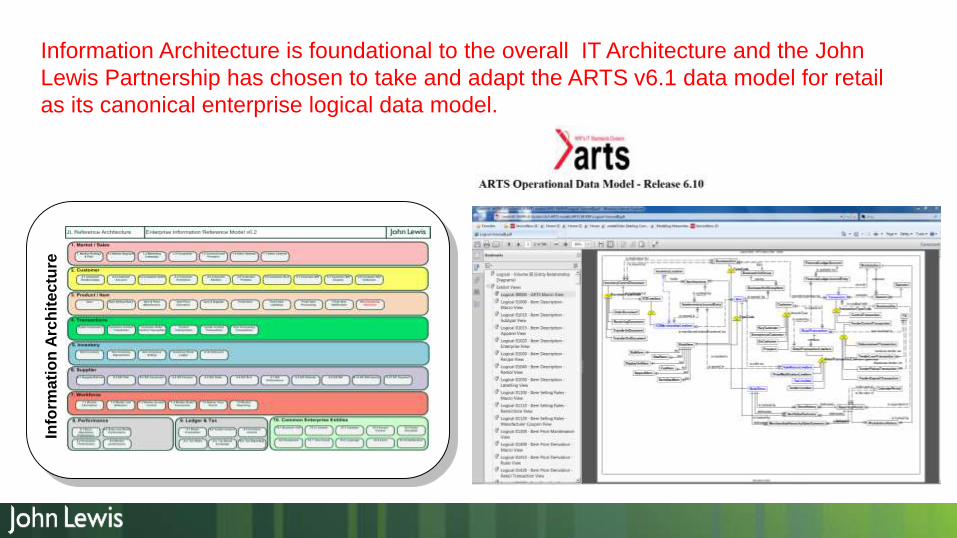

Information Architecture is foundational to the overall IT Architecture and the John

Lewis Partnership has chosen to take and adapt the ARTS v6.1 data model for retail

as its canonical enterprise logical data model.

Happy 20th Birthday ARTS

Our Customers are at the

heart of all we do

ARTS v7 Operational Data Model

ARTS v3 Data Warehouse ModelCustomer Case management

Essential View of Customer

![OMNI-400 / OMNI-600 - bienbacsecurity.com.vnbienbacsecurity.com.vn/DownloadFolder/OMNi_400-600[1].pdf · OMNI-400 / OMNI-600 Unattended downloading 4 - 8 fully programmable zones](https://static.documents.pub/doc/80x56/5bb5f82709d3f250788ddad9/omni-400-omni-600-1pdf-omni-400-omni-600-unattended-downloading-4-.jpg)