54

Report No. 2015-01 audit.jocogov.org Johnson County Auditor Johnson County, Kansas PERFORMANCE AUDIT February 12, 2015 Johnson County Mental Health Center Review Phase II

| Date post: | 17-May-2018 |

| Category: |

Documents |

| Upload: | trinhxuyen |

| View: | 216 times |

| Download: | 0 times |

Report No. 2015-01 audit.jocogov.org

Johnson County Auditor Johnson County, Kansas

PERFORMANCE AUDIT

February 12, 2015

Johnson County Mental Health Center Review Phase II

Johnson County Audit Services

111 South Cherry Street, Suite 1050 (913) 715-1825 Olathe, KS 66061-3441

February 12, 2015

To: Johnson County Mental Health Center Governing Board Tim DeWeese, Director, Johnson County Mental Health Center

At the request of the County Manager and approval by the Johnson County Board of County Commissioners, Audit Services conducted a review and audit of the Johnson County Mental Health Center (MHC). The first phase of our review was completed in July 2014. This report is the second and final phase of our audit effort and addresses the following areas:

Internal Management Reporting myAvatar, MHC’s new electronic medical records (EMR) system Management of Accounts Receivable Contract Management and Accounts Payable Activities

Phase I identified a number of internal and external factors hindering operational efficiencies at the MHC. Some of these factors continued to exist during Phase II of our audit effort. The attached report identifies the absence of management information needed to direct an operation the size and complexity of the MHC. The report also notes challenges experienced with the MHC’s new EMR system, myAvatar. In our review of accounts receivable, the report notes the MHC is not using all available tools to collect debt. Finally, our review of contract payments indicates internal practices are insufficient to ensure vendors are paid based on contractual requirements. The audit was conducted according to applicable standards contained in Government Auditing Standards, issued by the Comptroller General of the United States, except that Peer Review has not been performed, and included such tests of the procedures and records as considered appropriate. I appreciate the cooperation received from the Johnson County Mental Health Center leadership and staff during this audit. Their dedication and support of the audit effort has been exemplary. I want to recognize members of Audit Services, Michelle Cleveland, CFE and Lynn Smith, CIA, who were contributors to this audit report. Ken Kleffner, CIA Interim County Auditor CC: Johnson County Mental Health Advisory Board

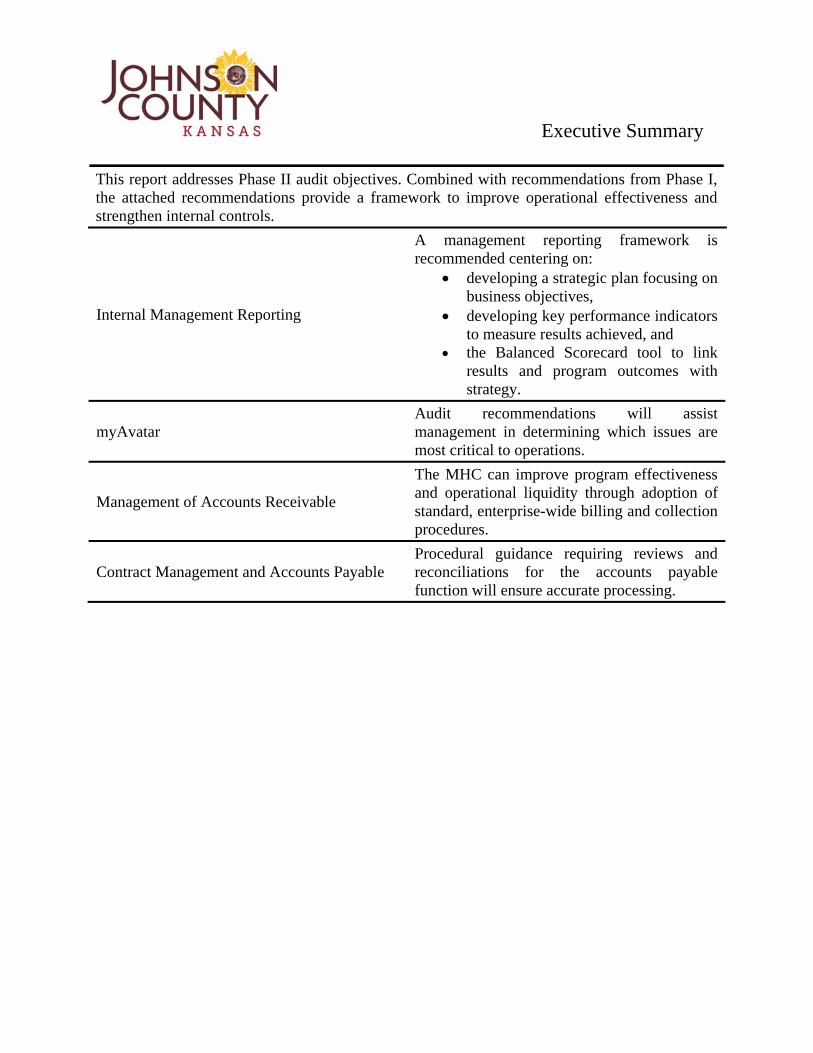

Executive Summary

This report addresses Phase II audit objectives. Combined with recommendations from Phase I, the attached recommendations provide a framework to improve operational effectiveness and strengthen internal controls.

Internal Management Reporting

A management reporting framework is recommended centering on:

developing a strategic plan focusing on business objectives,

developing key performance indicators to measure results achieved, and

the Balanced Scorecard tool to link results and program outcomes with strategy.

myAvatar Audit recommendations will assist management in determining which issues are most critical to operations.

Management of Accounts Receivable

The MHC can improve program effectiveness and operational liquidity through adoption of standard, enterprise-wide billing and collection procedures.

Contract Management and Accounts Payable Procedural guidance requiring reviews and reconciliations for the accounts payable function will ensure accurate processing.

i

Johnson County Mental Health Center Review Phase II

TABLE OF CONTENTS

Page

Introduction ...............................................................................................................................1

1. Internal Management Reporting ................................................................................................3

Recommendations .....................................................................................................................3 Management Comments ............................................................................................................3 Discussion .................................................................................................................................4

2. myAvatar in an Operational Environment .................................................................................9

Recommendations .....................................................................................................................9 Management Comments ..........................................................................................................10 Discussion ...............................................................................................................................11

3. Management of Accounts Receivable .....................................................................................15

Recommendations ...................................................................................................................15 Management Comments ..........................................................................................................15 Discussion ...............................................................................................................................16

4. Contract Management and Accounts Payable .........................................................................19

Recommendations ...................................................................................................................19 Management Comments ..........................................................................................................19

Discussion ...............................................................................................................................20

APPENDICES I. OBJECTIVES, SCOPE AND METHODOLOGY ..................................................................21 II. Example Key Performance Indicators .....................................................................................27

ii

III. Sample Balanced Scorecard – Wyandot Center Inc ...............................................................29 IV. Sample Balanced Scorecard – Tri-County Mental Health Services, Inc. ................................31 V. Sample Balanced Scorecard – Swope Health Services ............................................................35

VI. Recommendations Assessment Rating ....................................................................................45

1

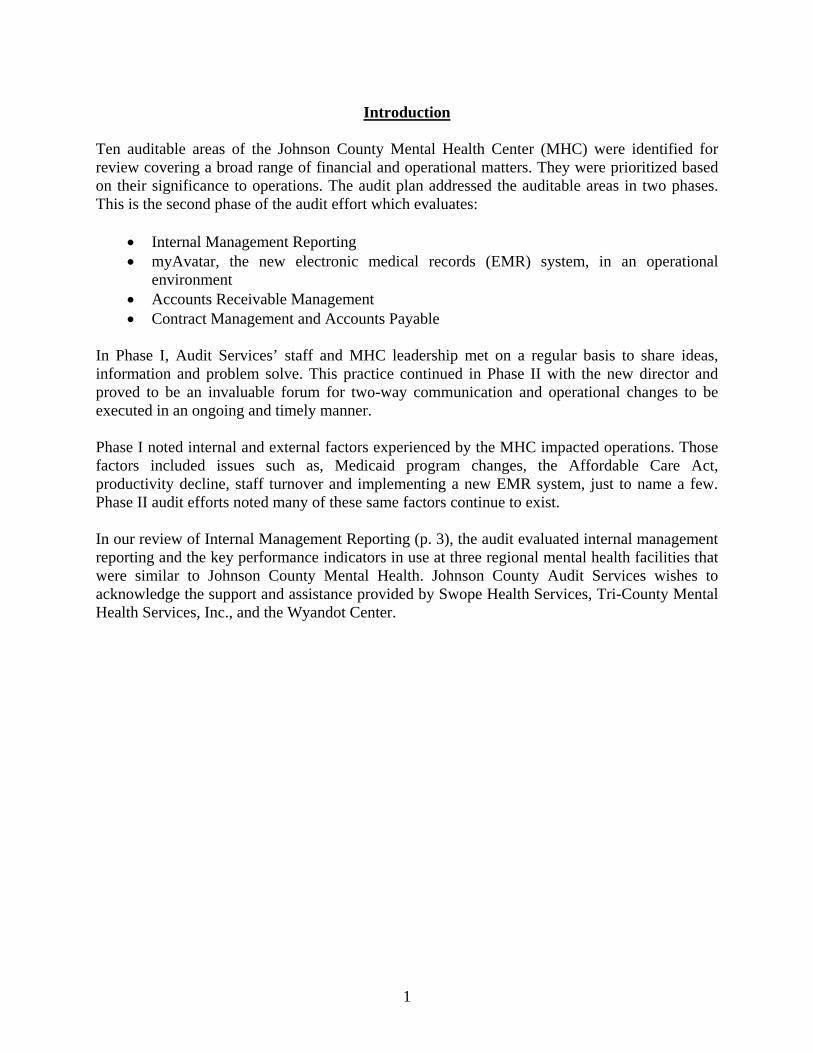

Introduction Ten auditable areas of the Johnson County Mental Health Center (MHC) were identified for review covering a broad range of financial and operational matters. They were prioritized based on their significance to operations. The audit plan addressed the auditable areas in two phases. This is the second phase of the audit effort which evaluates:

Internal Management Reporting myAvatar, the new electronic medical records (EMR) system, in an operational

environment Accounts Receivable Management Contract Management and Accounts Payable

In Phase I, Audit Services’ staff and MHC leadership met on a regular basis to share ideas, information and problem solve. This practice continued in Phase II with the new director and proved to be an invaluable forum for two-way communication and operational changes to be executed in an ongoing and timely manner. Phase I noted internal and external factors experienced by the MHC impacted operations. Those factors included issues such as, Medicaid program changes, the Affordable Care Act, productivity decline, staff turnover and implementing a new EMR system, just to name a few. Phase II audit efforts noted many of these same factors continue to exist. In our review of Internal Management Reporting (p. 3), the audit evaluated internal management reporting and the key performance indicators in use at three regional mental health facilities that were similar to Johnson County Mental Health. Johnson County Audit Services wishes to acknowledge the support and assistance provided by Swope Health Services, Tri-County Mental Health Services, Inc., and the Wyandot Center.

2

[This Page Intentionally Blank]

3

1. Internal Management Reporting The MHC needs an effective internal management reporting system to monitor and evaluate success in achieving program outcomes. Key performance indicators should be developed to assess both day-to-day operations and organization-wide performance. Recent operational and financial issues have driven MHC leadership to focus on daily operational issues. The recent selection of a permanent director, however, makes it an opportune time to establish a management reporting system designed to measure, monitor and disclose information relevant to goals, objectives and to establish accountability within the organization. Recommendations We recommend the Director, Johnson County Mental Health Center: 1.1 Develop a strategic plan, in partnership with Mental Health Center’s Advisory Board,

which identifies strategic and operational objectives and priorities and is aligned with the Board of County Commissioner’s Strategic Priorities.

1.2 Develop key performance indicators to measure and analyze internal business processes and activities in support of strategic priorities and operational objectives.

1.3 Implement the Balanced Scorecard (BSC) methodology as the tool to link program outcomes and financial and non-financial performance to key strategic and operational objectives.

1.4 Develop a recurring, standard financial and operational reporting process for both the Advisory and Governing Boards which includes standard financial and operational reports to effectively report status and historical trends.

Management Comments The Mental Health (MNH) Department concurs with the findings and supports the recommendations made by the Audit team. Fortunately, the Audit team has included MNH management throughout the process allowing the department to be proactive and address several of the concerns in advance of this report being finalized. The MNH Director and the Advisory Board are actively planning a strategic planning process which will enable the department to address all these recommendation in full.

4

Discussion The Technical Assistance Report The Technical Assistance Report1 provided the initial insight into MHC’s internal management reporting. Reference the following excerpts:

There needs to be consideration for Key Performance indicators (KPI’s) for staff, teams, divisions, and the agency. There appears to be plenty of “data”, but it needs to be put to strategic use2.

There were reports by multiple divisions and programs regarding inaccurate and inconsistent data provided them on productivity, finance, etc. It was unclear about the origin of all of these reports, but it is critical for the leadership staff at all levels to have accurate, consistent, and timely data3.

MHC’s Financial Reporting Financial information provided to the MHC Advisory Board in September 2014 included information with conflicting time periods. For example, The Financial Dashboard report reflected information “At June 2014”, while another report, The Consolidated Revenue and Expenditure Report4, reflected information as of “August 2014”. Each report’s revenue numbers, by revenue source, were the same; yet, the “as of” date for both reports differed, making it difficult to evaluate how much progress had been made towards realizing the year’s budgeted fee revenue. Financial reporting, both timely presentation and quality content, is crucial to managing any business. Recent liquidity issues and the projected 2014 end of year Mental Health Fund cash balance have placed an interest on Accounts Receivables (AR). AR information and the collectability of debt were reported to both the Advisory and Governing Boards for the first time in December 2014. The reported AR information raised questions from members of both Boards and in some instances, staff was not successful in explaining the information provided. MHC leadership is to be commended for including additional financial information – financial information should be flexible. Given the current circumstances, it is suggested leadership determine what information and metrics would provide the most value and simplify the presentation. Each Board should be equipped with measuring tools that inform them how efficiently the entire revenue cycle5 is operating. Without this, the Board remains uninformed and could misinterpret the financial reports and discussion. The bottom line - good financial

1 Technical Assistance Report (TA): Johnson County Mental Health Center (JCMHC) November 19-23, 2013 2 TA Report, page 6, paragraph N. 3 TA Report, page 4, paragraph 9. 4 Johnson County Mental Health Center Financial Report, Period Ending August 31, 2014. 5 Defined by Healthcare Financial Management Association (HFMA) as: All administrative and clinical functions that contribute to the capture, management, and collection of patient service revenue.

5

management in the public sector is predicated upon having sufficient, reliable, and meaningful data. Key Performance Indicators MHC’s key performance indicators (KPI’s) are identified in their annual budget along with limited trend and actual performance results. These KPIs are limited to just those required, contractually, by the State of Kansas. The MHC has not developed metrics beyond those required by the State to measure operations or program outcomes. We found the State of Kansas reporting requirement had not been met for the last six months due to the lack of a reporting tool from myAvatar. The information (data) resides in myAvatar; however, the system does not have the functionality to report it in the format required by the State. (See next section for more information regarding State reporting.) Appendix II provides examples of indicators applicable to the health care industry that may be of value to the MHC in their pursuit to develop metrics applicable to their operations. Other Regional Mental Health Facilities We contacted three other mental health centers in the region, Wyandot Center, Tri-County Mental Health Services and Swope Health Services, to review their internal management reporting capabilities. We sought to gain an understanding of the similarities and differences of each. A brief synopsis of each service provider follows:

Wyandot Center: Wyandot Center is located in Kansas City, Kansas, and is a not-for-profit 501c3 organization. They have been in business for 55 years and rely solely on business operations and fundraising efforts as revenue streams. The Center is not affiliated with Wyandotte County yet they share the following similarities with Johnson County’s MHC. For example, they: offer community support services,

have an on-site Genoa pharmacy,

implemented a new EMR system in 2013, and

introduced the “Wyandot Health and Wellness Home” in 2014.

An illustration of their balanced scorecard is shown as Appendix III.

Tri-County Mental Health Services: Tri-County is the primary provider of comprehensive behavioral health services to a community of nearly 400,000 people who live north of the river in Clay, Platte and Ray Counties in Missouri. Tri-County is unique. In addition to hiring agency-based staff to provide services to the community, they: out-source clinical treatment for behavioral health problems to

professionals who live and work throughout the three-county area,

6

have an on-board professional staff, a network of dozens of individual and agency providers and more than a hundred volunteers, and

are accredited by the Council on Accreditation of Rehabilitation Facilities (CARF).

Tri-County’s unique provider network allows the agency to deliver services to nearly 9,000 people annually. An illustration of their balanced scorecard is shown as Appendix IV.

Swope Health Services (SHS): SHS is located in Kansas City, Missouri and opened in 1969 to provide primary health services to the working poor. In 1980, a comprehensive mental health center was added so that behavioral and chemical issues that impacted the lives of the high-risk population served could be addressed. Forty-one percent of their programs are related to mental health issues. SHS is accredited by the CARF and is a Federally Qualified Health Care Center (FQHC) which requires they follow strict criteria enabling them to receive approximately 20% of their funding from the federal government. SHS recently implemented an EMR system in 2010 as well. An illustration of their balanced scorecard is shown as Appendix V.

We found each center to be unique in terms of how they operate and fund their business, however, all three organizations use very similar methods to keep abreast of their business operations. Each organization has developed an internal management reporting framework and is utilizing the balanced scorecard methodology to link program outcomes and financial and non-financial performance to key strategic and operational objectives. Copies of individual scorecards are included to provide the MHC Director examples of actual scorecards in use and the variations of each. Management at one of our benchmarked centers indicated their most relied upon KPI is “total billed amount”. They also noted their operations needed to be adaptable to changing conditions continuously, and their management team viewed the “total billed amount” as an indicator of how successful, and efficiently, their operations were working to combine making money with providing services. Management at a different service provider stated their dashboard6 results included:

all metrics required to meet funding requirements metrics to educate doctors and other board members supporting information when goals were not achieved

6 Defined by Gartner as: a reporting mechanism that aggregates and displays metrics and key performance indicators (KPIs), enabling them to be examined at a glance by all manner of users before further exploration via additional business analytics (BA) tools.

7

To reiterate, all three mental health centers we contacted are either accredited or have to follow strict guidelines for federal funding. Their scorecards reflect results that may, or may not be adaptable to Johnson County Mental Health operations. As such, the MHC should develop their own KPIs to meet unique management expectations and evaluate program outcomes. Balanced Scorecard Development A balanced scorecard (BSC) is a methodology and framework to assess an organization’s performance. It is used extensively in business and industry, government, and nonprofit organizations worldwide, and involves the development of a tool used to measure KPIs. Organizations set goals, or benchmarks to work towards. Effective goal setting depends upon the care and intelligence invested in selecting the goal. A benchmark that can’t be measured, can’t be reached, or can be reached too easily has little or no value. KPIs can then be compared (or benchmarked) either internally, against past performance, or externally, against other organizations with similar operations. Opportunity for change For some time now, MHC leadership has focused almost solely on day-to-day operational and financial issues, leaving little, if any, time to devote towards strategic planning efforts. Given the recent selection of a permanent director, the timing is appropriate for the Director to initiate strategic planning efforts with the Mental Health Advisory Board. The outcome of the strategic planning efforts will be used to “to set priorities, focus energy and resources, strengthen operations, ensure that employees and other stakeholders are working toward common goals, establish agreement around intended outcomes/results, and assess and adjust the organization's direction in response to a changing environment.”7 Strategic planning efforts and execution should follow the prescribed method for strategy setting governance as illustrated through the following Committee of Sponsoring Organizations literature8 model:

Figure 1.1: Governance model for setting strategy

7 Strategic Planning definition per Balanced Scorecard Institute. 8 Improving Organizational Performance and Governance, Committee of Sponsoring Organizations, February 2014. Available at www.coso.org.

8

The Johnson County Board of County Commissioners Strategic Priorities Report, dated February 2014, was developed to guide the work of County organizations over the next one to two years. The Board’s Strategic Priority No. 1 is:

Support strategic approaches to improving the lives of vulnerable populations by addressing emerging poverty and crime and through job creation. Develop and implement a data-driven decision-making process and systems, in particular for public safety and health & human services.

The Board’s Strategic Priority No. 6 recognizes Johnson County shares common interest with other urban counties in the delivery of social services and the increasing demand for those services. The specific priority is:

Continue Core 4 and initiate discussion and coordination with urban counties. The MHC strategic planning efforts should complement and support the Board’s strategic priorities.

9

2. myAvatar in an Operational Environment MHC’s new EMR system, myAvatar, which went live May 1, 2014, was still not fully functional for MHC’s business processes as of October. Functionality and user issues included:

creation and maintenance of treatment plans, billing secondary guarantors, and reporting to the State of Kansas.

Factors occurring during project implementation not only delayed the eventual system implementation but also impacted the stability of the system once implemented. These factors included:

software customization,

system requirements and user issues not prioritized,

insufficient reporting to MHC leadership regarding implementation and issue resolution, and

insufficient user testing and training. Additionally, contingency planning (emergency and business continuity) has not been updated to reflect the myAvatar environment. Such planning ensures key business operations can continue without loss or duplication of important information in the event of an emergency or absence of key personnel. Recommendations We recommend the Director, Johnson County Mental Health Center: 2.1 Develop a plan of action addressing incomplete system requirements stemming from

implementation for key business processes and prioritize issues required to stabilize the system and improve functionality.

2.2 Document customization and business processes as they relate to the myAvatar system. 2.3 Ensure a proper training program is established in a hands-on, fully functional system

environment once the system is stabilized and fully documented. Include training in myAvatar Executive Reporting system for all key administrative positions responsible for reporting.

2.4 Update Emergency Planning and Business Continuity plans to reflect business processing

in the myAvatar environment.

10

Management Comments The Mental Health (MNH) Department concurs with the findings and supports the recommendations made by the Audit team. Again, the Audit team has included MNH management throughout the process allowing the department to be proactive and address several of the concerns in advance of this report being finalized. The MNH Director, CMO’s office and the DTI Director have developed a plan moving forward to effectively address the barriers in the implementation process and a process for prioritizing an active work list has been implemented.

11

Discussion

Software customization As noted in the Phase I audit report, during system implementation, change orders were submitted to customize standard software. Customization occurred to:

Satisfy unique State of Kansas requirements, Recreate functionality which existed in the previous system, LUCI and Enhance the system even though it was not a priority or requirement.

Starting with the Request for Proposal (RFP) phase and continuing through the implementation phase, little was done to prioritize system requirements to ensure critical business needs and state requirements took precedence over the other customization efforts. Current business industry trend is to adopt standard “off the shelf” systems/software and modify internal business processes to accommodate new software functionality as opposed to procuring “off the shelf” software and customizing it to “fit” existing business processes. Why? Customization of a system makes future upgrades more troublesome and costly. Also, system changes can sometimes conflict with software patches9. We have seen evidence of this with the approach taken by the MHC regarding the myAvatar system implementation. The patches installed sometimes conflicted with customization efforts, notably in the functionality of their custom forms. System requirements In October 2014, five months after the system went live, the vendor had not met all system requirements/specifications agreed to in the Request for Proposal (RFP) and contract. Requirements thought to be complete in May 2014, upon further review, were considered incomplete as the software does not perform as the requirement intended. We performed an analysis of the system requirements identified by the MHC in their RFP with those the vendor stated they could fulfill. The RFP identified a total of 936 requirements or specifications for MHC’s new EMR system. The vendor agreed they could meet 715 of those requirements with their system and provide workarounds for another 133 of the requirements that would meet MHC’s needs. As of October 2014, the vendor had developed workarounds for 127 out of 133 requirements originally identified as workarounds and delivered or met 457 (64%) of the 715 system requirements. Chart 2.1 on the following page illustrates the vendor’s progress satisfying system requirements over time – starting with onset of the project; at May 2014 and again at October 2014.

9 Terminology to describe software updates released for reasons including: fix for a specific problem or problems, new product functionality, fix for a security-related vulnerability or a combination of the items just noted. Source: http://support.microsoft.com.

12

Chart 2.1: RFP Requirements Met - May vs. October 2014

Source: Audit Services Analysis Until recently, MHC leadership was not regularly updated regarding the progress being achieved with system implementation. Regular status meetings were being held, however, the status of the vendor’s progress meeting the RFP’s system requirements was not a reporting element. Consequently, MHC leadership was unaware of the progress being made and could not prioritize the remaining requirements to ensure key business process requirements were met first to stabilize the system. State reporting The RFP required 113 specific reporting requirements for MHC business processes. The vendor indicated they could meet 53 of those requirements with myAvatar. The vendor further noted they could provide workaround solutions for 43 of the reporting requirements, leaving 17 requirements that could not be met. Of the 17 requirements not met, 4 are specific to State and Federal reporting requirements. MHC officials were aware the myAvatar system would not meet all of their reporting requirements. MHC has not met State reporting requirements since implementation. The system collects the data elements needed and required by the state; however, myAvatar cannot provide the data in a format that interfaces with the State’s system. The vendor is currently working with the MHC to provide an interface for state reporting.

13

System training Training provided MHC staff in anticipation of system implementation was performed in a sandbox environment10 which did not include the full complement of production screens. As a consequence, staff were not trained in all of aspects of using and navigating the system. The MHC’s Share Point site contains training materials, such as, process documentation and instruction for all staff to access. However, for some users, written instruction and process documentation are insufficient learning tools. Another characteristic of MHC’s training strategy was to employ “train the trainer” in which team leaders trained their own staff. Due to this strategy, training was not uniform and provided in the same manner from team to team. As the system stabilizes and functionality is added to myAvatar, staff will benefit from additional hands-on user training and a more planned, uniform training program. MHC staff was asked to respond to a survey regarding myAvatar a few months after system implementation. When the survey was administered, not all system requirements had been met by the vendor. The survey helped to detect and communicate some of the issues MHC staff was experiencing with the system. Some respondents noted functionality issues with the new EMR, but some issues identified could be related to the learning curve of a new system. Learning curve concerns and gaining familiarity with a new system are to be expected as noted in the following study:

When organizations implement new information systems, there is often a period of decreased performance and/or quality. This period of decreased performance may be attributed to a variety of influences including the “learning curve” phenomena. Learning curve effects are evidenced by an initial increase in task time and/or decrease in performance, followed by gradual improvement with repeated use.11

The learning curve and period of decreased performance could be shortened for many users with a sufficient training program. How Has the Lack of System Functionality Impacted the MHC? MHC’s clinical and billing activities experienced implementation issues affecting daily business and revenue generation for the MHC. Implementation issues recently identified by MHC personnel noted 43 billing issues and 19 clinical issues related to the EMR. As of September 2014, the vendor resolved 12 of the 43 billing issues and 7 of the 19 clinical issues.

10 Sandbox environment mimics an operational environment. It can best be defined as “a testing environment” where new programming code is tested and allows independent evaluation, monitoring or testing. Source: Audit Services 11 The Impact of Information Systems on End User Performance: Examining the Effects of Cognitive Style Using Learning Curves in an Electronic Medical Record Implementation by Alexander J. McLeod Jr., Accounting and Information Systems, University of Nevada, Reno.

14

A significant billing issue since “Go Live” was a system functionality issue with the mechanics of billing in the order of guarantors (Medicaid, Medicare, third party insurance providers, and client self-pay). Primary guarantor billings were being sent to the payor as the progress notes were created and services provided, however, the secondary and subsequent guarantors were not successively billed automatically. On the clinical side, forms and screens required to be completed by a clinician/case worker to create a proper Treatment Plan (POC – Plan of Care in myAvatar) were noted by users to be cumbersome and confusing. Issues were first thought to be a functionality issue which prohibited the Treatment Plan from being completed. Upon further review, it was discovered the issues were not functionality issues; rather, customization of the form, with its many screens to complete, made it difficult for users to complete the Treatment Plan. Much of the customization related to these forms was a State requirement and the data needed by the State to validate Medicaid payments. User training and experience, over time, should aid users in gaining familiarity with the system. System Documentation and Business Continuity A critical requirement in all systems implementation is to document the system and ensure business continuity and emergency planning efforts include formal written procedures reflecting the new system’s environment. MHC’s emergency planning and business continuity plans have not been updated to reflect the myAvatar system and its related business processes. GTAG Scope Limitation An audit objective in Phase II was to review and complete the Global Technology Audit Guide (GTAG) requirements for the transition from system’s implementation to a live production environment. We were unable to meet that audit objective due to an extended absence of certain personnel and a lack of system documentation.

15

3. Accounts Receivable Management The MHC has delayed adopting internal guidelines required to comply with the County-wide Billing, Accounts Receivable, and Collections Policies and Procedures and is relying on past billing and collection practices which do not optimize collection of delinquent debt. The delay can be attributed to the MHC devoting resources to implement their new EMR system, myAvatar. The MHC can improve program effectiveness and operational liquidity through adoption of standard, enterprise-wide billing and collection procedures. We recommend the Director, Johnson County Mental Health Center: 3.1 Implement internal guidelines supportive of the County’s Policy for Billing, Accounts

Receivable, and Collections, Section No. 170. Internal guidelines shall include the following features: Kansas Set-off Program as one of the tools used to collect delinquent debt. Write-offs of delinquent debt and Discharge of Debt approved by the MHC Director.

3.2 Analyze open and closed accounts receivable (approximately 3,400 accounts valued at

$589,000) residing in LUCI at the time of conversion to determine if they, or some portion of that portfolio, can be submitted to the Kansas Set-off Program for collection action. If the decision is made to not pursue collection action, determine if County Procedure 170.20, Discharge of Debt, is the correct approach for processing these accounts.

Management Comments The Mental Health (MNH) Department concurs with the findings and supports the recommendations made by the Audit team.

16

Discussion Background Johnson County’s Billing, Accounts Receivable, and Collections Policy Section # 170, approved in March 2014, addresses:

standard definitions, internal control considerations, uniform billing practices, suggested collection methodology, and proper recording, monitoring & reporting accounts receivable.

Departments and agencies are required to develop internal billing and collection guidelines to comply with these policies and procedures and are allowed the flexibility to design their internal guidelines to meet unique business needs. The MHC has not implemented internal guidelines in support of the County’s accounts receivable policies and procedures. When asked why action had not been initiated, MHC staff responded “we’ve been implementing myAvatar since July of 2013 in some way and have not had the time. The ‘perfect storm’ we’ve experienced in MHC has prohibited (us) from making that kind of accomplishment.” Each mental health client’s unique background may hinder their ability to pay for services provided. In many cases, the client simply does not have the wherewithal to pay the County for the services provided. Nonetheless, the MHC should adopt and follow sound business practices and principles to collect debt in a timely manner, while recognizing the uniqueness of the clients being served. Debt collection practices should be established and employed during all phases of the accounts receivable life cycle, even in organizations where clients may be limited in their ability to pay. Mental Health’s existing billing and collection practices MHC’s existing billing, collection, accounting and reporting practices are inadequate to affect the timely resolution of accounts receivable and do not optimize the Center’s ability to collect delinquent debt. For example:

Only closed accounts are sent to the MHC’s external collection agency for collection action.

The MHC does not use the Kansas Set-off Program to collect delinquent accounts. (In November 2010, Audit Services recommended they develop procedures to begin using the Kansas Set-off Program and they responded favorably to that recommendation.)

Write-off’s occur if the client’s account has been closed for five years with the exception of those that have a family member with an active account. (This is a system limitation linked to their legacy system – LUCI.)

17

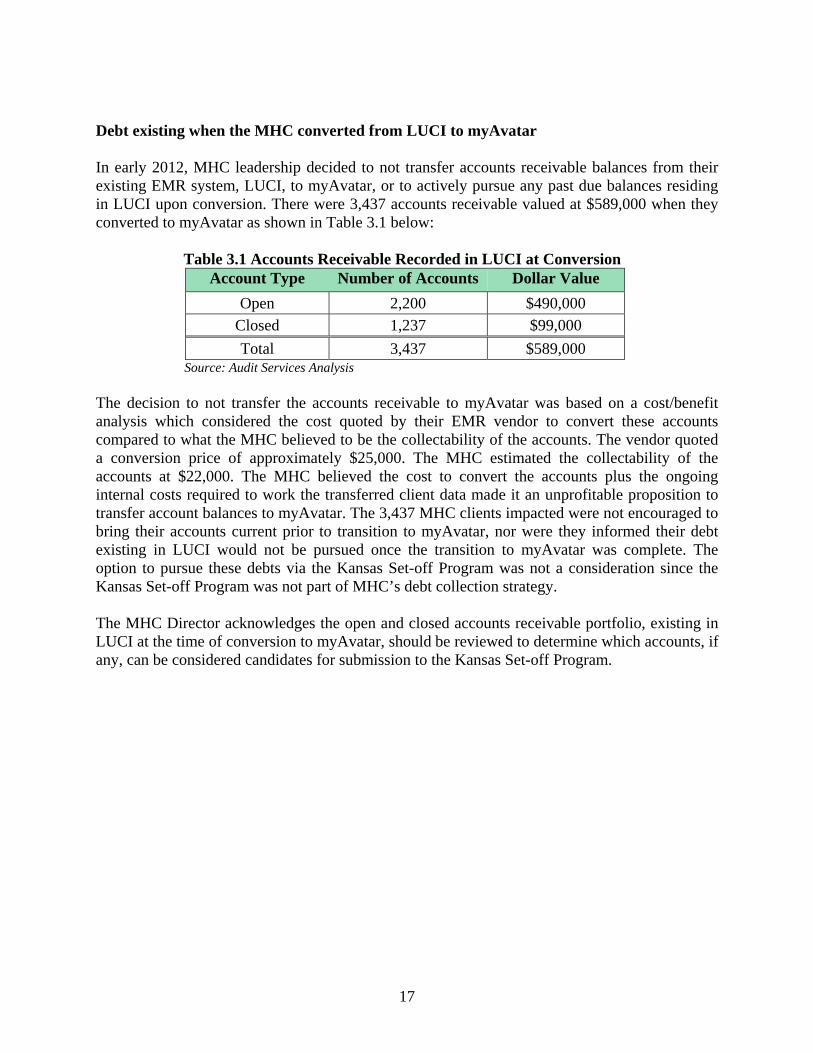

Debt existing when the MHC converted from LUCI to myAvatar

In early 2012, MHC leadership decided to not transfer accounts receivable balances from their existing EMR system, LUCI, to myAvatar, or to actively pursue any past due balances residing in LUCI upon conversion. There were 3,437 accounts receivable valued at $589,000 when they converted to myAvatar as shown in Table 3.1 below: Table 3.1 Accounts Receivable Recorded in LUCI at Conversion

Source: Audit Services Analysis The decision to not transfer the accounts receivable to myAvatar was based on a cost/benefit analysis which considered the cost quoted by their EMR vendor to convert these accounts compared to what the MHC believed to be the collectability of the accounts. The vendor quoted a conversion price of approximately $25,000. The MHC estimated the collectability of the accounts at $22,000. The MHC believed the cost to convert the accounts plus the ongoing internal costs required to work the transferred client data made it an unprofitable proposition to transfer account balances to myAvatar. The 3,437 MHC clients impacted were not encouraged to bring their accounts current prior to transition to myAvatar, nor were they informed their debt existing in LUCI would not be pursued once the transition to myAvatar was complete. The option to pursue these debts via the Kansas Set-off Program was not a consideration since the Kansas Set-off Program was not part of MHC’s debt collection strategy. The MHC Director acknowledges the open and closed accounts receivable portfolio, existing in LUCI at the time of conversion to myAvatar, should be reviewed to determine which accounts, if any, can be considered candidates for submission to the Kansas Set-off Program.

Account Type Number of Accounts Dollar Value

Open 2,200 $490,000 Closed 1,237 $99,000

Total 3,437 $589,000

18

[This Page Intentionally Blank]

19

4. Contract Management and Accounts Payable The MHC does not have an adequate internal control structure in place to ensure vendor invoices are reconciled to contract requirements ensuring the vendor is billing and being paid accurately. Of the vendor invoices examined, we found:

Eight percent were not billed accurately and MHC potentially overpaid one of their vendors.

Thirty-four percent did not indicate they were reviewed, reconciled or approved by MHC staff.

We also found $232,078 in annual licenses and maintenance fees charged to the EMR implementation CIP Project fund, potentially leaving the CIP project funding deficient to pay remaining obligations. Control activities, such as, procedural guidance requiring reviews and reconciliations of accounts payable will improve the accuracy of the accounts payable process. Recommendations We recommend the Director, Johnson County Mental Health Center: 4.1 Develop standard operating procedures outlining practices to review and reconcile

contract invoices to MHC supporting documentation and contractual requirements. 4.2 Ensure annual reoccurring expenses, such as licenses and maintenance fees, are included

in future annual operating budgets. Management Comments The Mental Health (MNH) Department concurs with the findings and supports the recommendations made by the Audit team. Again, the Audit team has included MNH management throughout the process allowing the department to begin the process of reviewing, revising, and developing a set of standard operating procedures across all clinical and business operations.

20

Discussion We reviewed MHC’s non-payroll administrative costs and found Contractual Services to be one of MHC’s major cost drivers. The MHC has effectively managed contracts ensuring:

Contracts did not lapse, Request for Proposal Procedures have been carried out as required by County policy, and MHC officials have renegotiated contract costs according to the contract specifications

and requirements. We reviewed a sample of invoices for the six largest vendors the MHC contracted with during 2012 and 2013. The invoices within our sample comprised 17% of all expenses in the Contractual Services and Commodities categories. Internal guidance describing the procedures for reviewing, reconciling and paying vendor invoices do not exist. Absent audit criteria, we established the following criteria for our examination:

Did the vendor provide a detailed invoice when the contract was based on per hour or per person cost?

Was the invoice accurate based on contract terms and criteria? Did the invoice indicate that an authorized MHC individual reviewed and authorized the

invoice for payment? We found:

Eight percent of the invoices in our sample were not billed accurately according to the contract terms. For example, one of the vendors whose billing was based on “per person per day” did not provide

any detail regarding the number of persons served at each of three locations they provided service to, and

the same vendor included billing for one location on another location’s invoice and charged for as many as 33 days in a 30 day billing cycle.

Sixty-five percent of the invoices in our sample were approved by MHC personnel leaving 34% indicating no signs of review, reconciliation or approval.

We also examined all invoices charged to the primary project purchase order for the EMR implementation project (CIP fund). We found two of the invoices charged to the purchase order (PO) which encumbered funds for the contract, were annual recurring operating expenses for licenses and maintenance and should not have been charged to the CIP project. They should have been charged to the administration operating budget. MHC personnel have been advised of our findings to initiate corrective follow-up action. Results indicate a control weakness in the Accounts Payable function – specifically, the lack of procedural guidance, reviews and reconciliations.

Appendix I

21

OBJECTIVES, SCOPE AND METHODOLOGY Objectives The second phase of the audit included objectives in the following priority areas:

1) Key Performance Indicators 2) myAvatar in an operational (production) environment 3) Billing and Accounts Receivable Management 4) Contract Management and Accounts Payable 5) Analyze the MHC fee structure to determine changes in the pricing of services from 2010

through 2014. Audit Note: We found the fee structure changed in 2013 when the state of Kansas introduced KanCare and the service code structure changed for billing purposes – some services were combined and some service codes were no longer allowed. The pricing of services not impacted by KanCare had not changed since 2010. On January 26, 2015, the Mental Health Center’s Advisory Board was presented with, and approved, a proposal to modify the Ability Fee Scale and the Service Fee Schedule.

The following statements further refine our objectives in the above audit areas.

1) Key Performance Indicators. Assess current methods to keep leadership informed of operations by determining:

a) Are present day key performance indicators sufficient to evaluate program outcomes?

b) Is present day reporting to management, Governing and Advisory Boards sufficient to manage a $30M business?

c) What financial information is provided to management, Governing and Advisory Boards to support the MHC financial position and trends?

2) myAvatar System Implementation and Management. Objectives:

a) Review post implementation issues related to functionality and business processes in a production environment.

b) Determine if business continuity planning has been prepared and covers potential risks.

c) Review plans for measuring Return on Investment (ROI) Audit Note: Our review found the MHC never developed plans for measuring the ROI for the implementation of the new EMR system.

3) Billing and Accounts Receivable Management. Objectives:

a) Determine how MHC manages write-offs: What is their policy? How often do write-offs occur? Do they follow their policy?

b) Determine how MHC is managing available tools to collect debt – Are they using state set off? An outside collection agency?

Appendix I

22

4) Contract Management and Accounts Payable. Objectives: a) Review/evaluate non-personnel administrative costs:

1. Trend analysis of non-personnel costs 2. Identify/analyze major cost drivers

b) How is MHC managing contracts and vendor payments? 1. Are vendors fulfilling contractual requirements? 2. Are vendors paid according to the contract compensation? 3. Are proper procedures in place to ensure payments are accurate and

charged to proper accounts?

Audit Note: We found contractual services to be a significant non-personnel cost driver. Another major cost driver was mileage reimbursement for staff use of personal vehicles (POV) while performing their job responsibilities. The MHC has reduced mileage reimbursements from $607,313 in 2010 to $485,098 in 2013; however, there were still a number of employees (23) receiving over $5,000 per year in mileage reimbursements. The MHC Director is currently working with Central Fleet Services to determine if some other alternative in lieu of POV use can be provided to further reduce costs.

Background During Phase I of the Mental Health Center Audit, we provided an extensive background and historical information of the Johnson County Mental Health Center. The first phase of our review, completed in July 2014, focused on the following areas:

Billing and collection policies, procedures and activities Productivity Technical Assistance (TA) Report dated November 19-20, 2013 Implementation of myAvatar – conversion to a clinical Electronic Medical Records

program

During the course of our review, we cited numerous factors impacting operational effectiveness and efficiencies including:

leadership turnover, high staff turnover, dissolution and establishment of a new mental health governing board, programming changes, introduction of new medical coding structure, and implementation of a new electronic medical records (EMR) system.

These internal factors may individually negatively affect operations. Collectively, when considered with other external changes such as Medicaid program changes and the establishment of KanCare and the Affordable Care Act, a “perfect storm” ensued. During the course of reviewing collection policies and practices in Phase I, we encountered a security issue at one of the MHC locations which was addressed in that report. The report also

Appendix I

23

identified components of the MHC’s Internal Control Program that could be strengthened and offered recommendations that would improve operational effectiveness. The report also offered suggestions which appeared in the last section based on our audit observations. We believe these suggestions have merit and warrant management’s consideration; however, they will not be included in our Follow-Up Program. Since the release of our first audit report in July 2014, a permanent Director has been appointed. Audit Services’ staff and MHC leadership met on a regular basis to share ideas and information and problem solve allowing some operational changes to be executed in an ongoing and timely manner. History and Evolution of the MHC EMR system A request for proposal (RFP 2011-041) was released August 25, 2011 to obtain electronic medical records (EMR) for the MHC that would meet its business processes and support the new diagnostic and medical coding system that the United States Medical and Mental Health professionals will need to use for Medicaid and Medicare in 2015. Since 1979, the US has required ICD-9-CM codes for Medicare and Medicaid claims, and most of the rest of the American medical industry followed suit. The International Statistical Classification of Diseases and Related Health Problems, usually called by the short-form name International Classification of Diseases (ICD), is the international standard diagnostic tool for health management and clinical purposes. The ICD is maintained by the World Health Organization, the directing and coordinating authority for health within the United Nations System. The ICD is designed as a health care classification system, providing a system of diagnostic codes for classifying diseases, including nuanced classifications of a wide variety of signs, symptoms, abnormal findings, complaints, social circumstances, and external causes of injury or disease. This system is designed to map health conditions to corresponding generic categories together with specific variations, assigning for these a designated code, up to six characters long. Thus, major categories are designed to include a set of similar diseases. The ICD – 10 was developed in 1992 and the United States has generally been slow to adopt the revised standards that the rest of the United Nations countries have been using to increase tracking of health statistics since 1994. On August 21, 2008, the US Department of Health and Human Services (HHS) proposed new code sets to be used for reporting diagnoses and procedures on health care transactions. Under the proposal, the ICD-9-CM code sets would be replaced with the ICD-10-CM code sets, effective October 1, 2013. On April 17, 2012 the Department of Health and Human Services (HHS) published a proposed rule that would delay, from October 1, 2013 to October 1, 2014, the compliance date for the ICD-10-CM. Then Congress delayed the implementation date to October 1, 2015, after another bill was passed. Revisions to ICD-10-CM Include:

Relevant information for ambulatory and managed care encounter. Expanded injury codes.

Appendix I

24

New combination codes for diagnosis/symptoms to reduce the number of codes needed to describe a problem fully.

Addition of sixth and seventh digit classification. Classification specific to laterality. Classification refinement for increased data granularity.

In addition to the implementation of a new ICD system, the US Mental Health field is also implementing new standards specific to the classification of Mental Health disorders. The Diagnostic and Statistical Manual of Mental Disorders (DSM), published by the American Psychiatric Association, offers a common language and standard criteria for the classification of mental disorders. It is used, or relied upon, by clinicians, researchers, psychiatric drug regulation agencies, health insurance companies, pharmaceutical companies, the legal system, and policy makers together with alternatives such as the International Statistical Classification of Diseases and Related Health Problems (ICD), produced by the World Health Organization (WHO). The DSM is now in its fifth edition, DSM-5, published on May 18, 2013. The fifth edition of the Diagnostic and Statistical Manual of Mental Disorders (DSM), the DSM-V, was approved by the Board of Trustees of the American Psychiatric Association (APA) on December 1, 2012. Published on May 18, 2013, the DSM-5 contains extensively revised diagnoses and, in some cases, broadens diagnostic definitions while narrowing definitions in other cases. The DSM-5 is the first major edition of the manual in twenty years, and the Roman numerals numbering system has been discontinued to allow for greater clarity in regard to revision numbers. Audit Services’ June 2008 audit report recommended the MHC:

Use County ITS expertise in conjunction with the Mental Health staff to develop a needs analysis leading to a Request for Proposal for an Electronic Medical Records system which will meet the Center’s current requirements and provide the flexibility to meet future needs.

In Phase I, we reported implementation of MHC’s new EMR system, myAvatar, went live on May 1, 2014. Management of the IT implementation project complied with the Global Technology Audit Guide’s (GTAG) recommendations for implementing a new system. After the system went live, areas that worked fine in the test environment (sandbox) were found to not be fully functional in the live production environment which can expected with any systems implementation. The audit did not review any of these failures (post implementation) to determine if they could have been avoided. Scope and Methodology To accomplish the audit objectives we:

Interviewed: Director Billing manager Project manager, Technology and Innovation Department

Appendix I

25

Contract Administrators Leadership at three other regional mental health organizations

Reviewed:

Departmental policies and procedures (as available) Organization chart Billing and collections processes Project documentation Previous audit and consultant reports Kansas Statutes County policy and procedures Contracts with seven vendors Invoices from vendors Key performance indicators for three other regional mental health organizations Institute of Internal Auditors certification training materials

Analyzed:

Billing and collection data Non payroll administrative expenditures Status reports for IT project implementation

Computer Data We used data from the Oracle financial and human resources system. The Oracle system data has been validated by others before being provided to Audit Services. Statistical Sampling We reviewed a sample of invoices for the six largest vendors the MHC contracted with during 2012 and 2013. These vendors submitted 313 invoices charging the MHC a total of $1,011,978 in 2012 and 2013. These invoices comprised 17% of all expenses in the Contractual Services and Commodities categories. Using the MACORR’s Sample Size Determinator, the sample size of 146 was selected to project our findings with 90% confidence and a +/- 5% interval to the population. We then used IDEA Audit software to randomly select the statistical sample from the population. The selected statistical sample contained 146 invoices totaling $454,882.. The primary PO for the CIP project encumbers $944,578.58, of which $853,830 had been spent through 13 invoices. We reviewed all 13 of the invoices charged to that PO. We reviewed the invoices for accuracy, signs of review and approval, and detail in the cases where contract compensation relied on per person or per hour billing. Key Performance Indicators and Benchmark Organizations We interviewed MHC management to evaluate internal key performance indicators (KPIs) in use. Additionally, we contacted Sedgwick County, and four other Kansas City metro mental health centers with requests to obtain knowledge and/or documentation of what KPIs were in use

Appendix I

26

within their organization to gauge operations. Next, we developed standard questions to determine how other CMHC’s compare to the MHC and identify common KPIs, if possible. Information Limitation During the course of Phase II, the myAvatar implementation Project Management responsibilities were not sufficiently defined and as a consequence, the Project Sponsor and Project Manager had a miscommunication regarding roles and responsibilities. The Project Manager was not informed of project documentation that may or may not have occurred and was excluded from department communication regarding myAvatar. The Project Sponsor was absent towards the end of the verification phase of our audit and was not available to provide information related to project implementation and documentation of processes; therefore, much of the business simulation and production environment requirements from the GTAG (Global Technology Audit Guide) could not be answered and we were limited in our review of this area.

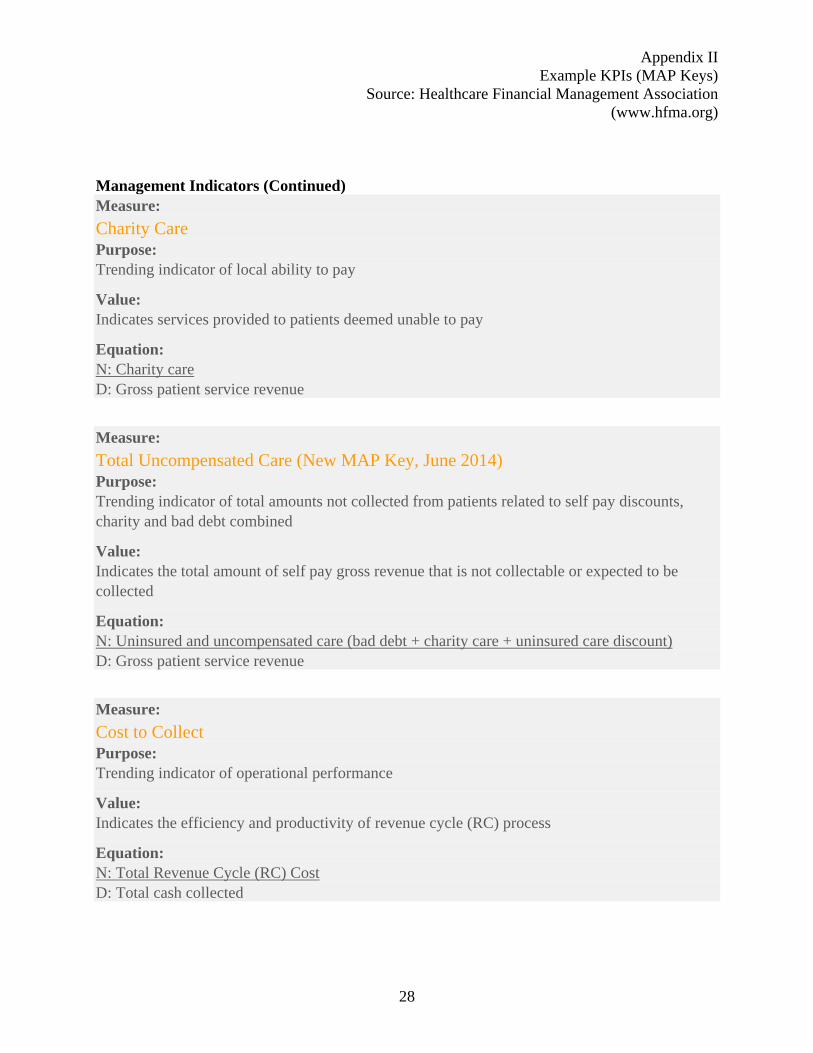

Appendix II Example KPIs (MAP Keys)

Source: Healthcare Financial Management Association (www.hfma.org)

27

Revenue Integrity Indicator Measure:

Days in Total Discharged Not Final Billed (DNFB) Purpose: Trending indicator of claims generation process

Value: Indicates revenue cycle performance and can identify performance issues impacting cash flow

Equation: N: Gross dollars in A/R (not final billed) D: Average daily gross revenue

Management Indicators Measure:

Aged A/R as a Percentage of Billed A/R Purpose: Trending indicator of receivable collectability

Value: Indicates revenue cycle’s ability to liquidate A/R

Equation: N: 0-30, >30, >60, >90, >120 days D: Total billed A/R

Measure:

Bad Debt Purpose: Trending indicator of the effectiveness of self-pay collection efforts and financial counseling

Value: Indicates organization’s ability to collect self-pay accounts and identify payer sources for those who can’t meet financial obligations

Equation: N: Bad debt D: Gross patient service revenue

Appendix II Example KPIs (MAP Keys)

Source: Healthcare Financial Management Association (www.hfma.org)

28

Management Indicators (Continued) Measure:

Charity Care Purpose: Trending indicator of local ability to pay

Value: Indicates services provided to patients deemed unable to pay

Equation: N: Charity care D: Gross patient service revenue

Measure:

Total Uncompensated Care (New MAP Key, June 2014) Purpose: Trending indicator of total amounts not collected from patients related to self pay discounts, charity and bad debt combined

Value: Indicates the total amount of self pay gross revenue that is not collectable or expected to be collected

Equation: N: Uninsured and uncompensated care (bad debt + charity care + uninsured care discount) D: Gross patient service revenue

Measure:

Cost to Collect Purpose: Trending indicator of operational performance

Value: Indicates the efficiency and productivity of revenue cycle (RC) process

Equation: N: Total Revenue Cycle (RC) Cost D: Total cash collected

Appendix III Wyandot Inc

29

Key Performance Indicators All Level Program Jul C14 Aug C14 Sep C14 Oct C14 Nov C14 Persons Served Persons Served Agency Adult

PACES Persons Enrolled Agency Adult

PACES Number of Agency Admits Agency Adult

PACES Number of Agency Discharges Agency Adult

PACES Productivity Billable Hours Agency Adult

PACES Billed Amount Agency Adult

PACES Number of Events Agency Adult

PACES Resource Utilization Avg Days Service to Finalize Agency Adult

PACES No Show Number Agency Adult

PACES No Show Percent Agency Adult

PACES Treatment Appropriateness Avg Days Since Seen Agency Adult

PACES Clients Not Seen in 181+ Days Agency Adult

PACES Intake To First Service Agency Adult

PACES Request To Intake Agency Adult

PACES Avg Program Length of Stay Agency Adult

PACES

30

[This Page Intentionally Blank]

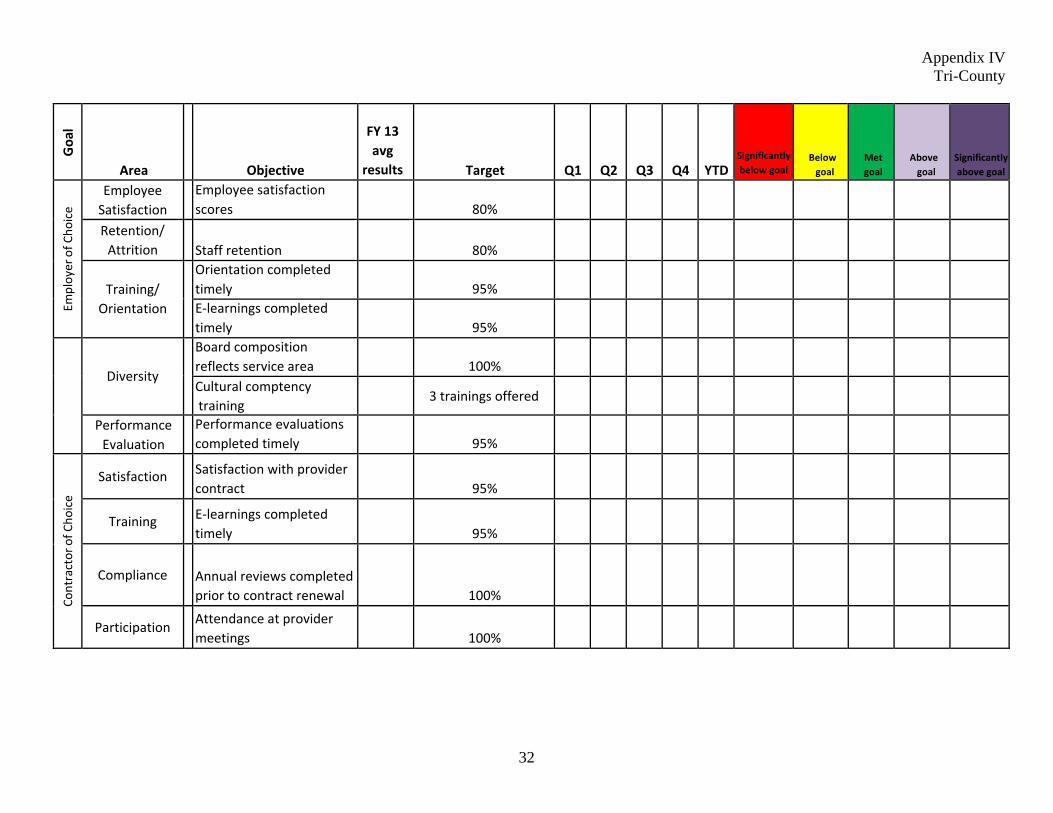

Appendix IV Tri-County

31

Goa

l

Area

Objective

FY 13 avg

results

Target

Q1

Q2

Q3

Q4

YTD

Significantlybelow goal

Below goal

Met goal

Above goal

Significantly above goal

Provider of C

hoice

Loyalty Recommend Tri‐County toOthers

85%

Consumer Satisfaction

Case management satisfaction

90%

Intake satisfaction 95%

Medication services satisfaction

91%

Therapy services satisfaction

90%

Employment services satisfaction

90%

Substance abuse treatment satisfaction

95%

Fidelity

Fidelity Score "good" or better

Wait Times

Agency wait times‐ Intake‐14 days

meet standard or better

Agency wait times‐ Substance Abuse‐ 5 days

meet standard or better

Agency wait times‐ Psychiatric Evaluation‐ 28 days

meet standard or

better

CARF Award of accreditation Full Accreditation Met

Appendix IV Tri-County

32

Goa

l

Area

Objective

FY 13 avg

results

Target

Q1

Q2

Q3

Q4

YTD

Significantly below goal

Below goal

Met goal

Above goal

Significantly above goal

Employer of C

hoice

Employee Satisfaction

Employee satisfaction scores

80%

Retention/ Attrition

Staff retention

80%

Training/

Orientation

Orientation completedtimely

95%

E‐learnings completedtimely

95%

Diversity

Board composition reflects service area

100%

Cultural comptency training

3 trainings offered

Performance Evaluation

Performance evaluationscompleted timely

95%

Contractor of C

hoice

Satisfaction

Satisfaction with provider contract

95%

Training

E‐learnings completed timely

95%

Compliance

Annual reviews completed prior to contract renewal

100%

Participation

Attendance at provider meetings

100%

Appendix IV Tri-County

33

Goa

l

Area

Objective

FY 13 avg results

Target

Q1

Q2

Q3

Q4

YTD

Significantly below goal

Below goal

Met goal

Above goal

Significantly above goal

Fiscal Respo

nsibility/ Co

rporate Co

mpliance

Effective Budget

Management

Operating margin vs. budget

3%

Effective Cash Management

Average daily balance

$1,000,000

Effective AR Management

Days in AR

75

Effective AP Management

Days in AP

35

Reduction of unapplied cash

Unapplied Cash

$1,000,000

Adherence to False Claims Act

Identification and timely repayment of overpayments

100% completed within 60 days

Identification of compliance risk

Compliance Risk Assessment and Workplan

Completed annuallyand reviewed

Effective compliance

Update and review of Compliance Audit Plan

Completed annuallyand reviewed

ND=No data for this quarter

34

[This Page Intentionally Blank]

Appendix V Swope Health

35

CELL FILL COLORS

Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

1 UDS: Diabetes last HbAlc 592 80%

2 UDS: Asthma Pharmacologic therapy 80%

3 UDS: Coronary Artery Disease Lipid Therapy 85%

4 UDS: Ischemic Vascular Disease Aspirin Therapy new

5 UDS: 3 year old Immunization Rate 90%

7 UDS: Infant Low Birth Weight <9%

8 UDS: Hypertension last measurement of <140/90 85%

9 Multiple Anti-psychotic Medications Documentation

10 Medication Occurrences and Errors

Appendix V Swope Health

36

CELL FILL COLORS

Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

11 Critical Lab Results Reporting and Actions

12 UDS: Adult Weight Screening and Follow- up 45%

13 UDS: Tobacco Use Screening and Cessation (changed for 2014 from separate assessment and intervention measures.)

45%

14 UDS: Childhood Weight Assessment and Counseling

66%

15 UDS: Cervical Cancer Prevention {Pap) 65%

16 330: Child Dental Treatment Plan completed within 12 months (Quarterly monitoring)

50%

17 UDS: 1st Trimester of Entry into Care (Quarterly Monitoring)

60%

18 UDS: Colorectal Cancer Screen (Quarterly Monitoring)

New

19 330: Metabolic Syndrome Screening (Quarterly Monitoring)

65%

Appendix V Swope Health

37

CELL FILL COLORS Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

20 UDS: HIV Prenatal Screening 100%

21 lmani House Physicals (Clients) (Monthly monitoring)

100%

22 lmani House TB Testing (Clients) (Monthly monitoring)

100%

23 Two Patient ldentifiers -Med Passing at Residential Care Facilities

100%

24 Two Patient Identifiers -Specimens and Samples (each opportunity compliant) NOTE: Although not counted in this total, WY LabCorp was audited for April report with 100% compliance (25/25)

100%

25 Two Patient Identifiers -Process (each opportunity compliant)

100%

26 Management of Sample Meds -Expiration Dates 100%

27 Management of Stock Meds-Expiration Dates 100%

Appendix V Swope Health

38

CELL FILL COLORS Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

28 Management of Multi-Dose Medications- Expiration Dates

100%

29 Consent to Treat and Education for Psychotropic Medication-Psychiatry/ Adult

90%

30 Consent to Treat and Education for Psychotropic Medication-Psychiatry/Child

90%

31 Consent to Treat for Oral Surgery--Dental 100%

32 Medical Supplies Management of Expiration Dates (clinic 100% compliant)

100%

33 Hand Hygiene 90%

34 CPRP Adult -Peer Review 90%

35 CPRP Child -Peer Review 90%

36 lmani House-Peer Review 90%

Appendix V Swope Health

39

CELL FILL COLORS

Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

37 Behavioral Health Outpatient Peer Review 90%

38 Behavioral Health Psychiatry Peer Review-- ADHD

90%

39 Behavioral Health Psychiatry Peer Review-- Depression

90%

40 Behavioral Health Crisis Notes Completion 100%

41 Credentialing Compliance 100%

42 Behavioral Health Initial Privileging 100%

43 Behavioral Health Reprivileging 100%

44

Behavioral Health Continuity of Assessment withCare Plan

90%

45

Behavioral Health Measurability of Care Plan 90%

Appendix V Swope Health

40

CELL FILL COLORS Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

46

Board of Directors' Utilization of Services 51%

47

340B Medication-Walgreens Compliance 100%

48

Clinic Support Staff Waived Testing Competencies

100%

49

Business Associate Agreements 100%

50 Compliance and Ethics Training 100%

51

Patient Safety Training 100%

52

Diversity Training 100%

53

Hazard Vulnerability Assessment 100%

54

Vehicle Inspections

Appendix V Swope Health

41

CELL FILL COLORS

Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

55 Visit Summary Compliance

56

Work Place Injury Rate (Quarterly monitoring)

4.50%

57

Work Force Flu Vaccination 80%

58

Work Force Flu Vaccination Declinations 20%

59

Work Force Flu Prevention Plan Compliance(Received vaccine or completed Declination Form)

100%

60

Associate TB Test Compliance 100%

61

Associate Flu Vaccination Compliance 90%

62

Associates Flu Season Mask Compliance 100%

63

General Consent to Treat-Psychiatry/Adult 100%

Appendix V Swope Health

42

CELL FILL COLORS Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

64

General Consent to Treat-Psychiatry/Child 100%

65

General Consent to Treat--Dental 100%

66

General Consent to Treat-Pediatrics 100%

67

General Consent to Treat-Adults at Central (seen only before Central Registration)

100%

68

General Consent to Treat-Adults at Central (seen after Central Registration)

100%

69

QPR Staff Training 100%

70

Consumer Complaints

71

Incidents

72

Quality of Care Determinations

Appendix V Swope Health

43

CELL FILL COLORS

Green-meeting or exceeding goal Yellow-slightly below goal, or slight downward trend Red-not close to meeting goal

ROW FILL COLORS Pink -Clinical Outcomes/Treatment Blue- Patient Safety/Infection Control Purple-Regulatory/Accreditation Tan - Associate Safety/Infection Control Gray-Organizational Risk Management Orange-Operations

"Month" indicates month of report; not the reporting period, with the exceptions of 'Work Place Injuries', 'DNKA', and "Stay Times', which are reported in the month of occurrence.

Indicator Goal Jan Feb Mar Apr May

June July Aug Sept Oct Nov Dec YTD

73 DNKA Rate Behavioral Health (Report Quarterly)

<20%

74 DNKA Rate Dental (Report Quarterly)

<20%

75 DNKA Rate Optometry (Report Quarterly)

<20%

76 DNKA Rate Ambulatory (Report Quarterly)

<20%

77 Stay Times Dental (Minutes)

60 min

78 Stay Times Ambulatory AduIt Services( Minutes)

60 min

79 Stay Times Optometry {Minutes)

60 min

80 Call Center Abandonment Rates <5%

44

[This Page Intentionally Blank]

Appendix VI Recommendations Assessment Rating

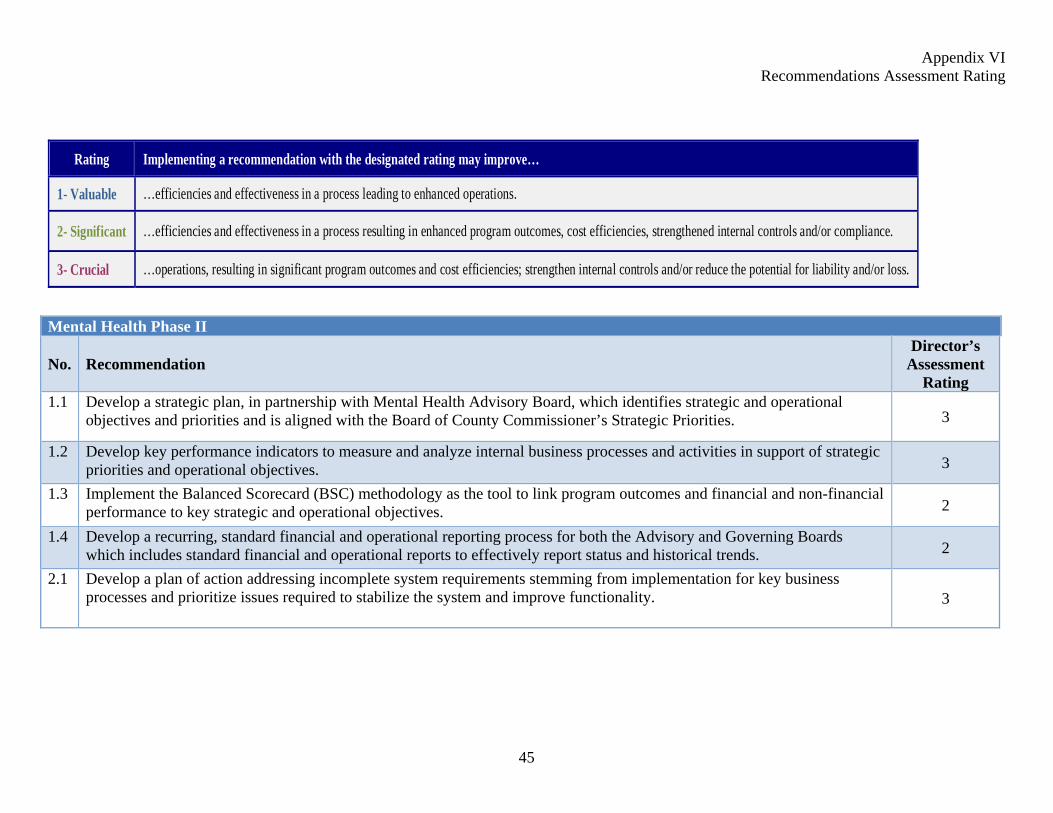

45

Mental Health Phase II

No. Recommendation Director’s

Assessment Rating

1.1 Develop a strategic plan, in partnership with Mental Health Advisory Board, which identifies strategic and operational objectives and priorities and is aligned with the Board of County Commissioner’s Strategic Priorities. 3

1.2 Develop key performance indicators to measure and analyze internal business processes and activities in support of strategic priorities and operational objectives. 3

1.3 Implement the Balanced Scorecard (BSC) methodology as the tool to link program outcomes and financial and non-financial performance to key strategic and operational objectives. 2

1.4 Develop a recurring, standard financial and operational reporting process for both the Advisory and Governing Boards which includes standard financial and operational reports to effectively report status and historical trends. 2

2.1 Develop a plan of action addressing incomplete system requirements stemming from implementation for key business processes and prioritize issues required to stabilize the system and improve functionality. 3

Rating Implementing a recommendation with the designated rating may improve…

1- Valuable …efficiencies and effectiveness in a process leading to enhanced operations.

2- Significant …efficiencies and effectiveness in a process resulting in enhanced program outcomes, cost efficiencies, strengthened internal controls and/or compliance.

3- Crucial …operations, resulting in significant program outcomes and cost efficiencies; strengthen internal controls and/or reduce the potential for liability and/or loss.

Appendix VI Recommendations Assessment Rating

46

Mental Health Phase II

No. Recommendation Director’s

Assessment Rating

2.2 Document customization and business processes as they relate to the myAvatar system. 3

2.3 Ensure a proper training program is established in a hands on, fully functional system environment once the system is stabilized and fully documented. Include training in myAvatar Executive Reporting system for all key administrative positions responsible for reporting.

2

2.4 Update Emergency Planning and Business Continuity plans to reflect business processing in the myAvatar environment. 1

3.1 Implement internal guidelines supportive of the County’s Policy for Billing, Accounts Receivable, and Collections, Section No. 170. Internal guidelines shall include the following features:

Kansas Set-off Program as one of the tools used to collect delinquent debt. Write-offs of delinquent debt and Discharge of Debt approved by the MHC Director.

2

3.2 Analyze open and closed accounts receivable (approximately 3,400 accounts valued at $589,000) residing in LUCI at the time of conversion to determine if they, or some portion of that portfolio, can be submitted to the Kansas Set-off Program for collection action. If the decision is made to not pursue collection action, determine if County Procedure 170.20, Discharge of Debt, is the correct approach for processing these accounts.

3

4.1 Develop standard operating procedures outlining practices to review and reconcile contract invoices to MHC supporting documentation and contractual requirements. 3

4.2 Ensure annual reoccurring expenses, such as licenses and maintenance fees, are included in future annual operating budgets. 3