32

July 2010 From “V” to “U” Benjamin Tal

| Date post: | 21-Dec-2015 |

| Category: |

Documents |

| View: | 216 times |

| Download: | 0 times |

July 2010

From “V” to “U”

Benjamin Tal

| 2

Impact of US Stimulus Package and Inventory Changes on US GDP Growth

-2

-10

1

23

4

5

67

8

09Q:2

09Q:3

09Q:4

10Q:1

10Q:2

10Q:3

10Q:4

11Q:1

11Q:2

11Q:3

11Q:4

fiscal stimulus inventories

Forecast

impact on quarterly growth (%-pts)

| 3

US Core CPI Slowest in Half Century

-4

0

4

8

12

16

J an-62 J an-70 J an-78 J an-86 J an-94 J an-02 J an-10

(five-month % chg, s.a. annualized)

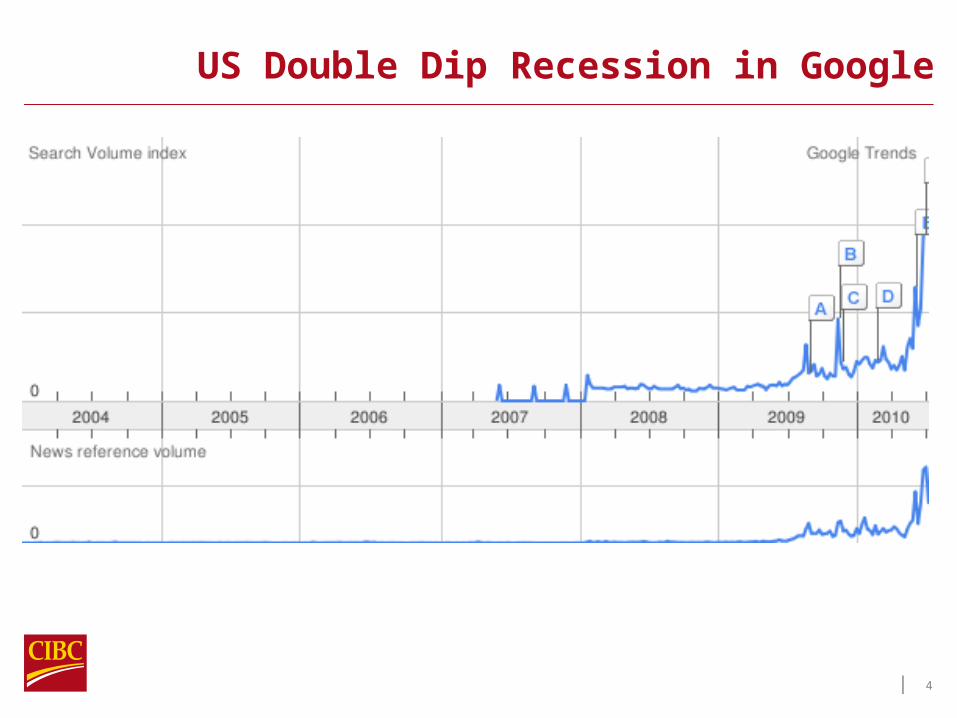

| 4

US Double Dip Recession in Google

| 5

Probability of Recession

0

0.10.2

0.3

0.40.5

0.6

0.70.8

0.9Ja

n-6

9Ja

n-7

1Ja

n-7

3Ja

n-7

5Ja

n-7

7Ja

n-7

9Ja

n-8

1Ja

n-8

3Ja

n-8

5Ja

n-8

7Ja

n-8

9Ja

n-9

1Ja

n-9

3Ja

n-9

5Ja

n-9

7Ja

n-9

9Ja

n-0

1Ja

n-0

3Ja

n-0

5Ja

n-0

7Ja

n-0

9

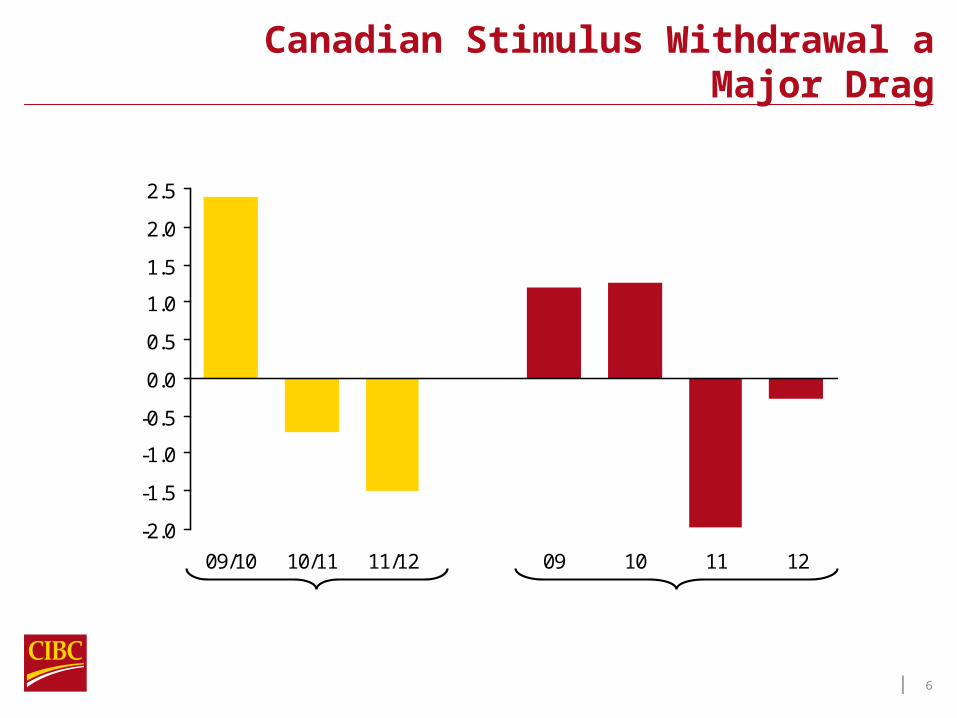

| 6

Canadian Stimulus Withdrawal aMajor Drag

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

09/10 10/11 11/12 09 10 11 12

Fiscal Yr (Accrual Basis) Calendar Yr (Cash Basis)

Chg in Fed-Prov Fiscal Stimulus, % of GDP

| 7

OIS Implied BoC Expectations

0%

20%

40%

60%

80%

100%

1st FAD 2nd FAD 3rd FAD 4th FAD

May 31st J uly 13thMarket Snapshot as of:

Prob of 25 bps Hike

| 8

Hikes Will Still Leave Rates Lowby Historical Standards

0

1

2

3

4

5

6

May- 05 Mar- 06 J an- 07 Nov- 07 Sep- 08 J ul- 09 May- 10 Mar- 11

%

Cdn overnight rate

10- yr USTForecast

10-yr Cda

Dec 2011

| 9

Stability Fund Covers Refinancing

0

100

200

300

400

500

600

700

800

Debt refinancing J un10-Dec11

Stability Fund

€ billion

Spain

Greece

PortugalI reland

IMF

EU

| 10

Size of Fiscal Cuts Needed to Stabilize Net Debt-to-GDP Ratio

% of GDP

0

2

4

6

8

10

12

14

J apan UnitedStates

UK Greece Italy Germany Canada AdvancedG- 20

Economies

| 11

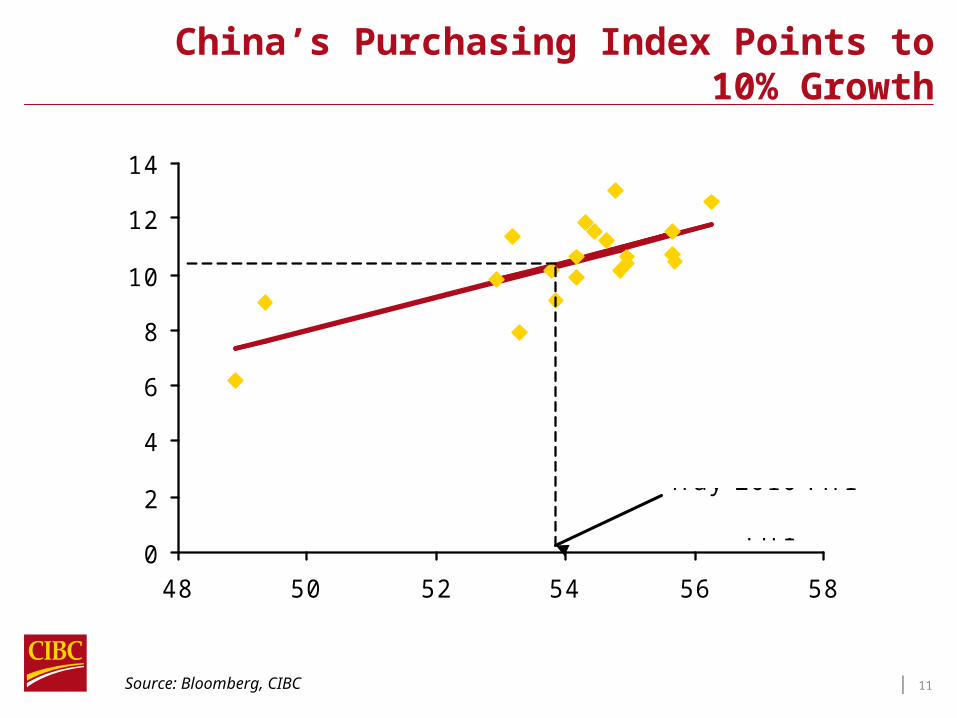

China’s Purchasing Index Points to 10% Growth

0

2

4

6

8

10

12

14

48 50 52 54 56 58

GDP y/y growth (% )

PMI

May 2010 PMI

Source: Bloomberg, CIBC

| 12

Chinese Stocks Don’t Always Reflect Economy

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

00:Q1 01:Q3 03:Q1 04:Q34

5

6

7

8

9

10

11

Shanghai C omposite (LHS)

Real GDP, y/y % chng (RHS)

Source: Bloomberg, CIBC

| 13

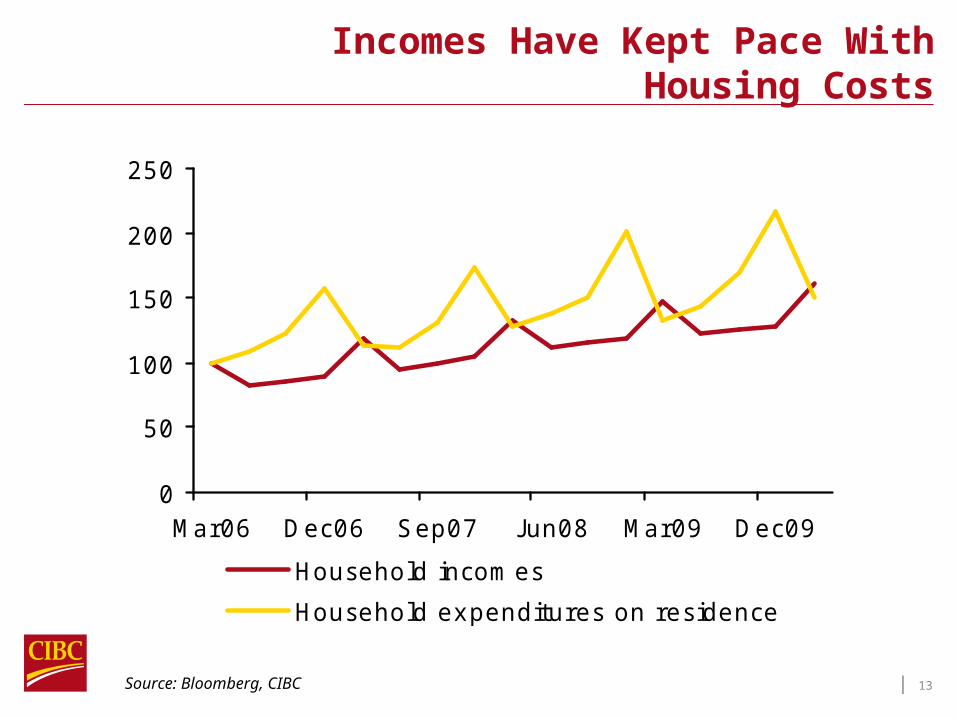

Incomes Have Kept Pace With Housing Costs

Source: Bloomberg, CIBC

0

50

100

150

200

250

Mar06 Dec06 Sep07 J un08 Mar09 Dec09

Household incomes

Household expenditures on residence

I ndex=100 in March 2006

| 14

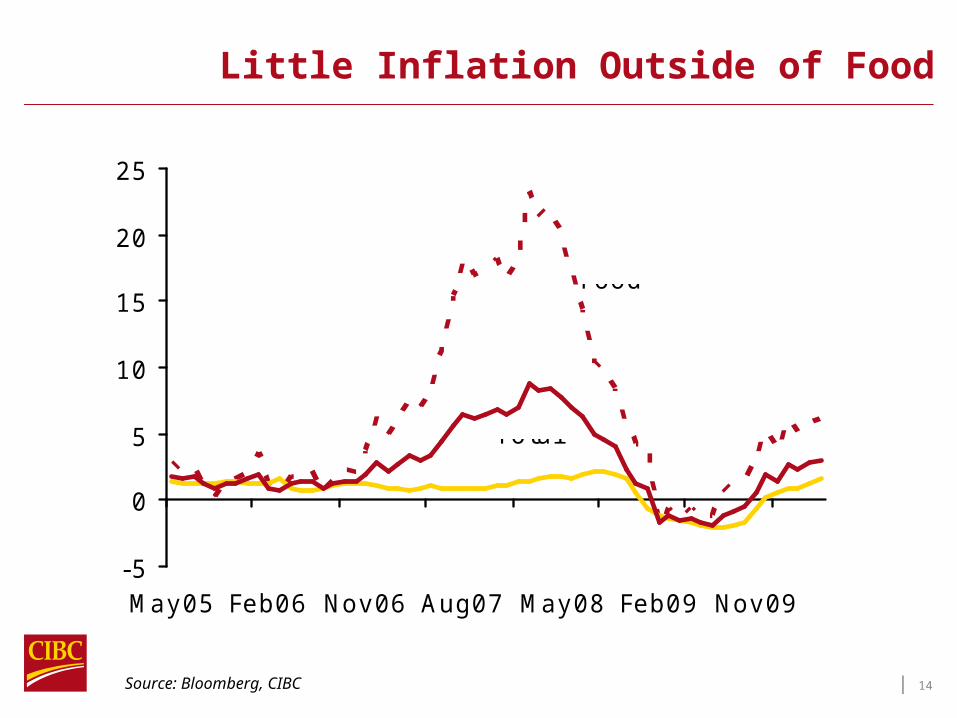

Little Inflation Outside of Food

Source: Bloomberg, CIBC

-5

0

5

10

15

20

25

May05 Feb06 Nov06 Aug07 May08 Feb09 Nov09

Food

Non-Food

Total

y/y % chg. in C PI

| 15

Canadian Dollar Rich Relative to Commodities

300

400

500

600

700

800

900

1000

Jan-08 May-08 Sep-08 Jan-09 May-09 Sep-09 Jan-10 May-10

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

1.30

BoC Commodity Price I ndex (L) Canadian Dollar (R)

C$ per US$ (reverse scale)

Index, 1972 =100

| 16

Fixed Income Inflows Driving C$ Appreciation: C$ to Average Near Parity Through 2011

-10

-5

0

5

10

15

20

25

Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09

75

80

85

90

95

100

105

Net Purchases of C$ Bonds (L) Canadian Dollar (R)

$billions (3mn Total) US¢/C$

n/a

| 17

Global Economy to Slow in the Second Half

0

2

4

6

8

10

12

US Eurozone C hina

1H10F 2H10F

annualized q/q real GDP growth, %

Source: CIBC

| 18

Analysts’ Track Record in PredictingS&P 500 Earnings

0

20

40

60

80

100

120

140

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

08

09

Index-adjusted

Note: Line shows evolution of "bottom-up" consensus reported by Thomson Reuters over time. Last obs is actual for year.

Source: Thomson Reuters, CIBC

| 19

US Earnings Growth Expectations Have Been Ratcheted Up More Aggressively Than in

Canada

Source: Thomson Reuters, CIBC

15

20

25

30

35

40

J an-09

Mar-09

May-09

J ul-09

Sep-09

Nov-09

J an-10

Mar-10

May-10

TSX C omposite S&P 500

Date of Analysts' Survey

concensus expectations for 2010 earnings growth (% )

| 20

Capital Intensive IndustriesBehind Manufacturing Rebound

Source: US Bureau of Economic Analysis, CIBC

* Thousand US$ per worker (2004)

-15 -10 -5 0 5 10 15

Semiconductors

C hemical

Primary metal

PaperC omputer &

electronicWood

TextilesApparel &

leatherPrinting

Furniture

Avgcapital intensity* = $53.3

Avgcapital

intensity* = $210

| 21

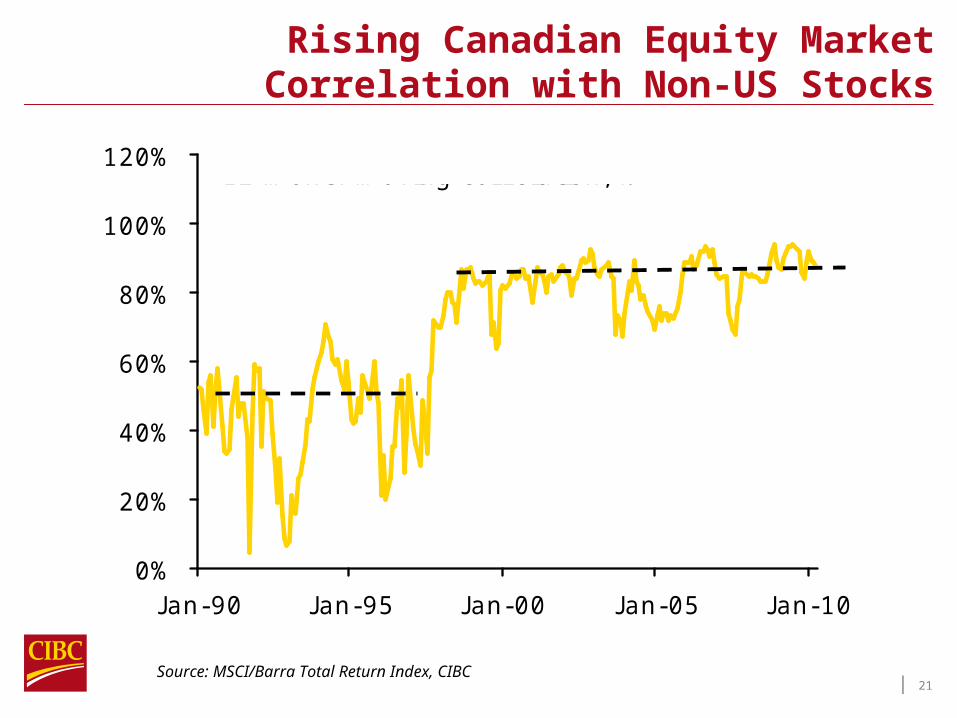

Rising Canadian Equity Market Correlation with Non-US Stocks

Source: MSCI/Barra Total Return Index, CIBC

0%

20%

40%

60%

80%

100%

120%

J an-90 J an-95 J an-00 J an-05 J an-10

12 month moving correlation, %

(44% avg)

(83% avg)

| 22

Canadian Equities More Correlated with Global Stocks in Bad Times

Source: MSCI/Barra Total Return Index, CIBC

Correlation - World vs. Canada

0%10%20%30%40%50%60%70%80%

World Total Return 1std deviation or more

above average

World Total Return 1std deviation or more

below average

| 23

Correlation of TSX Sector Returns to World Equities During Periods of Global Underperformance*

Source: MSCI/Barra Total Return Index, CIBC

0% 20% 40% 60% 80%

FinancialsI ndustrials

MaterialsC ons. Disc.

EnergyUtility

I nfo TechC ons. S tp.

HealthTelcomm

* MSC I World Total Return 1 std deviation or more

| 24

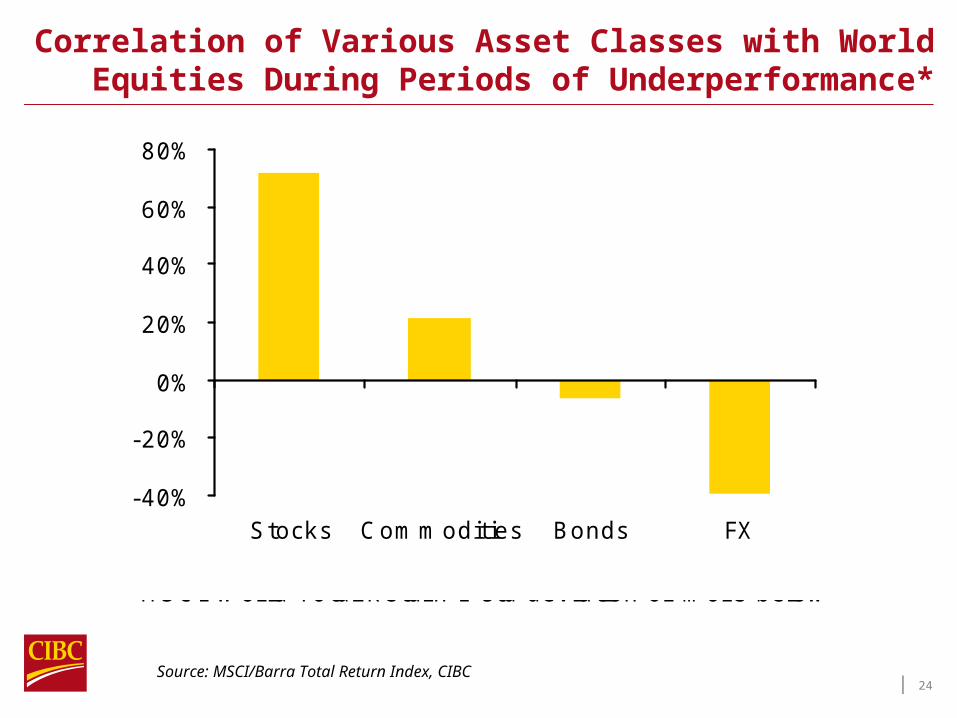

Correlation of Various Asset Classes with World Equities During Periods of Underperformance*

Source: MSCI/Barra Total Return Index, CIBC

-40%

-20%

0%

20%

40%

60%

80%

Stocks C ommodities Bonds FX

* MSC I World Total Return 1 std deviation or more below

| 25

Exposure of Exporting Nations to the Eurozone

0 10 20 30 40 50 60

C anada

Korea

J apan

I ndia

US

C hina

Brazil

Russia

UK

% of total exports going to Eurozone in 2009

Source: EuroStat, CIBC

| 26

Canada’s Government Debt Burdenthe Least Onerous

Note: Based on IMF projections

0

50

100

150

200

250

Net

Gross

2010 general govt debt- to-GDP ratio, %

| 27

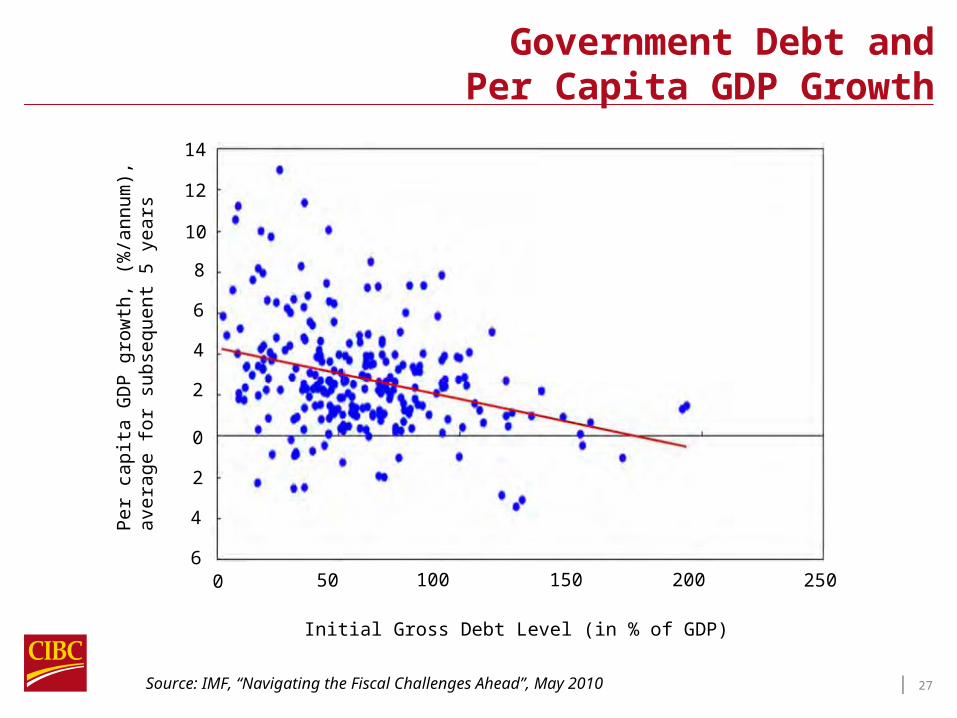

Government Debt and Per Capita GDP Growth

Source: IMF, “Navigating the Fiscal Challenges Ahead”, May 2010

0 50 100 150 200 250

14

12

10

8

6

4

2

0

2

4

6

Per

capit

a G

DP g

row

th, (%

/ann

um

),

avera

ge f

or

subse

quent

5 y

ears

Initial Gross Debt Level (in % of GDP)

| 28

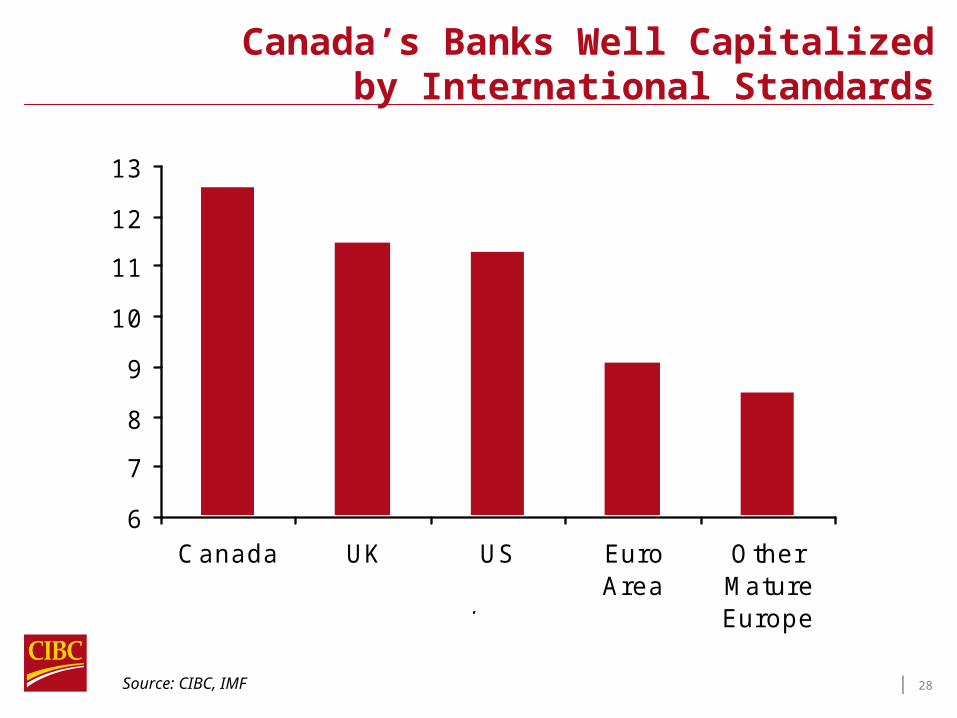

Canada’s Banks Well Capitalizedby International Standards

Source: CIBC, IMF

6

7

8

9

10

11

12

13

C anada UK US EuroArea

OtherMatureEurope

Average Tier 1 C apital Ratio, %

Source: CIBC WM, IMF

| 29

Projected Growth in Economically Active Population, 2010-2015

Source: International Labour Organization

-4

-3

-2

-1

0

1

2

3

4

5

C anada UnitedStates

WesternEurope

J apan

%

| 30

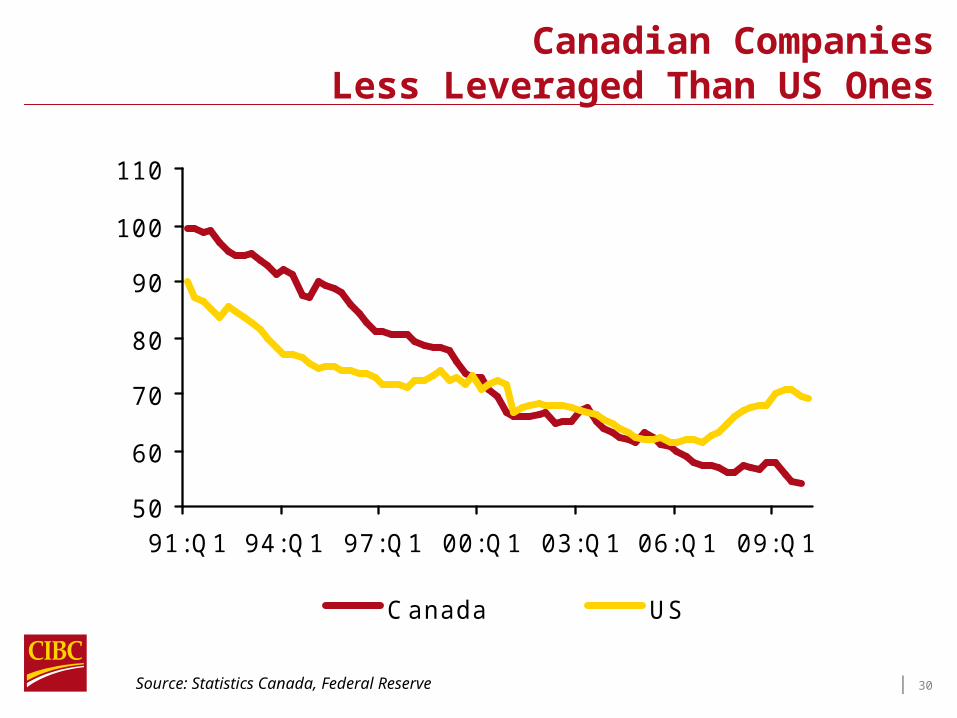

Canadian Companies Less Leveraged Than US Ones

50

60

70

80

90

100

110

91:Q1 94:Q1 97:Q1 00:Q1 03:Q1 06:Q1 09:Q1

C anada US

Debt-to-Equity Ratio ex financials, %

09:Q4

Source: Statistics Canada, Federal Reserve

| 31

Thank You

This material was prepared for investment professionals only and is not for public distribution. It is for informational purposes only and is not intended to convey investment, legal, or tax advice. The material and/or its contents may not be reproduced without the express written consent of Renaissance Investments.

| 32

Questions &

Answers