1 July 22, 2016 Via Federal eRulemaking Portal Robert deV. Frierson Secretary Board of Governors of the Federal Reserve System 20 th Street & Constitution Avenue, N.W. Washington, DC 20551 Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7 th Street, S.W. Suite 3E-218 Mail Stop 9W-11 Washington, DC 20219 Robert E. Feldman Executive Secretary Attention: Comments, Federal Deposit Insurance Corporation Federal Deposit Insurance Corporation 550 17 th Street, N.W. Washington, DC 20429 Alfred M. Pollard General Counsel Attention: Comments/RIN 2590-AA42 Federal Housing Finance Agency 400 7 th Street, S.W. Washington, DC 20219 Gerard S. Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, Virginia 22314-3428 Brent J. Fields Secretary Securities and Exchange Commission 100 F Street, N.E. Washington, DC 20549 Re: Notice of Proposed Rulemaking on Incentive-Based Compensation Arrangements (OCC Docket ID OCC-2011-0001 and RIN 1557-AD39; FRB Docket No. 1536 and RIN 7100 AE-50; FDIC RIN 3064-AD86; NCUA RIN 3133-AE48; FHFA RIN 2590-AA42; SEC File Number S7-07-16 and RIN 3235-AL06) Ladies and Gentlemen: The undersigned banks appreciate the opportunity to respond to the Notice of Proposed Rulemaking and Request for Comment on Incentive-Based Compensation Arrangements (Proposal) by the Board of Governors of the Federal Reserve System (Federal Reserve), the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation, the Federal Housing Finance Agency, the National Credit Union Administration, and the U.S. Securities and Exchange Commission (SEC) (collectively, the Agencies). 1 We are regional banking organizations, focused predominately on domestic and traditional banking activities. Our sizes are modest in relation to the U.S. banking sector and U.S. economic activity, especially when compared to the very largest banks in the country. Collectively, we employ hundreds of thousands of people throughout the United States in a variety of fields and professions. 1 81 Fed. Reg. 37,670 (proposed June 10, 2016). Unless otherwise specified, the citations herein are to the Proposal as set forth by the OCC and the Federal Reserve.

Transcript

1

July 22, 2016

Via Federal eRulemaking Portal

Robert deV. Frierson Secretary Board of Governors of the Federal Reserve System 20th Street & Constitution Avenue, N.W. Washington, DC 20551

Legislative and Regulatory Activities Division Office of the Comptroller of the Currency 400 7th Street, S.W. Suite 3E-218 Mail Stop 9W-11 Washington, DC 20219

Robert E. Feldman Executive Secretary Attention: Comments, Federal Deposit Insurance Corporation Federal Deposit Insurance Corporation 550 17th Street, N.W. Washington, DC 20429

Alfred M. Pollard General Counsel Attention: Comments/RIN 2590-AA42 Federal Housing Finance Agency 400 7th Street, S.W. Washington, DC 20219

Gerard S. Poliquin Secretary of the Board National Credit Union Administration 1775 Duke Street Alexandria, Virginia 22314-3428

Brent J. Fields Secretary Securities and Exchange Commission 100 F Street, N.E. Washington, DC 20549

Re: Notice of Proposed Rulemaking on Incentive-Based Compensation Arrangements (OCC Docket ID OCC-2011-0001 and RIN 1557-AD39; FRB Docket No. 1536 and RIN 7100 AE-50; FDIC RIN 3064-AD86; NCUA RIN 3133-AE48; FHFA RIN 2590-AA42; SEC File Number S7-07-16 and RIN 3235-AL06)

Ladies and Gentlemen:

The undersigned banks appreciate the opportunity to respond to the Notice of Proposed Rulemaking and Request for Comment on Incentive-Based Compensation Arrangements (Proposal) by the Board of Governors of the Federal Reserve System (Federal Reserve), the Office of the Comptroller of the Currency (OCC), the Federal Deposit Insurance Corporation, the Federal Housing Finance Agency, the National Credit Union Administration, and the U.S. Securities and Exchange Commission (SEC) (collectively, the Agencies).1

We are regional banking organizations, focused predominately on domestic and traditional banking activities. Our sizes are modest in relation to the U.S. banking sector and U.S. economic activity, especially when compared to the very largest banks in the country. Collectively, we employ hundreds of thousands of people throughout the United States in a variety of fields and professions.

1 81 Fed. Reg. 37,670 (proposed June 10, 2016). Unless otherwise specified, the citations herein are to the Proposal as set forth by the OCC and the Federal Reserve.

2

The Proposal seeks to implement the requirement in Section 956 of the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act), which requires the Agencies to prohibit, by rule or guideline, incentive-based compensation that the Agencies determine encourage inappropriate risks by providing excessive compensation or compensation that could lead to material financial loss.2 The Proposal includes a range of requirements applicable to incentive-based compensation arrangements at covered institutions.

We appreciate the difficult task and significant efforts undertaken by the Agencies in drafting the Proposal. We believe certain revisions are necessary, notwithstanding, to establish a workable and more appropriate framework for identifying institutions and their employees properly subject to certain additional incentive-based compensation requirements. Regional institutions are quite different than the largest, most complex banks. As the Proposal is structured currently, it would have significant and unintended adverse impacts on regional banks. Our suggestions are intended to account for the variations of business models across the banking industry and serve the Agencies’ goals, while reducing arbitrary and uneven impacts on covered institutions.

Utilizing a risk-based approach rather than a quantitative approach, we submit, would be a preferable methodology for categorizing institutions and their respective employees. We are concerned the Proposal, if finalized as proposed, would impose certain compensation requirements on a mix of employees different than what is intended by the Agencies or appropriate given the purpose of the Proposal. The result would significantly impact our ability to attract and retain the level of talent needed to operate in a challenging and competitive business environment. Because compensation levels differ among banks, under the Proposal’s current structure, employees serving in similar positions across the industry could be exempt from portions of the Proposal at one institution but subject to it at another. This reality would create unique retention risks for regional banks, where most employees often have lower compensation levels compared to larger banks. Many of our employees could have significant amounts of their compensation deferred and subject to other restrictions; yet, because of the compensation levels and structure, such employees likely would not be covered by the same restrictions at a larger institution. This incongruity could harm our ability to recruit and retain top talent. It also could impede our ability to attract and retain employees with critical and highly-valued skillsets whose expertise is not confined to the banking industry, such as technology and finance.

Over the past several years, our institutions (and others) have followed the principles-based approach set forth in the 2010 Interagency Guidance on Sound Incentive Compensation Policies3 (2010 Interagency Guidance) to formulate and implement compensation arrangements that appropriately balance performance measures, effectively deter imprudent and excessive risk-taking, and allow for the continued safety and soundness of our organizations. These arrangements are appropriately tailored to reflect the diversity of our respective business models and allow us to remain competitive not only within the banking industry, but also with unregulated competitors in the financial services sector and beyond.

Our primary concern with the Proposal is the departure from this principles-based framework to a rigid and prescriptive structure – one that does not account for the variations that exist among our business models and risk profiles. Instead, the Proposal would group otherwise dissimilar institutions together for application of rules based on arbitrary asset thresholds. We urge the Agencies to return to a principles-based approach for determining the applicability of the compensation restrictions that is more in-line with the 2010 Interagency Guidance. Our organizations already have expended significant efforts to incorporate these principles into our compensation practices, including risk management oversight, controls, training, and corporate governance. We believe these arrangements have worked quite well at requiring institutions to undertake a process to determine the compensation arrangements and to identify the appropriate employees that may put the institutions at risk while also allowing the companies to remain attractive employers. A principles-based approach also would enable our compensation practices to continue evolving over time in a manner that is appropriately tailored to our respective institutions without being confined to a static and potentially unworkable structure.

To the extent the Agencies intend to pursue a more prescriptive approach, we submit certain comments below that seek to draw on existing, well-established regulatory regimes and definitions for categorizing covered institutions and covered persons. The undersigned institutions have participated separately in the development of various comment letters submitted by industry trade associations and other organizations, some of which include The Clearing House Association, the American Bankers Association, the Securities Industry and Financial Markets Association, and the Financial Services Roundtable. We generally support the comments and concerns raised in their letters. The comments in this letter are intended to expand on some of these comments to emphasize certain issues that are of particular interest to regional banks.

I. Summary of Comments

For ease of reference, below is a summary of our comments:

• For purposes of categorizing covered institutions, we recommend the Agencies adopt a risk-based approach – specifically, the existing systemic indicator approach that has been developed internationally and implemented in the United States by the Federal Reserve – as opposed to a strictly asset-based approach for determining which entities will be subject to additional requirements and restrictions.

• We recommend the Agencies define “covered persons” as category 1, 2 and 3 material risk takers, in accordance with the existing supervisory process under the 2010 Interagency Guidance. If the Agencies maintain the definition of covered persons as proposed, we recommend revising the definition to exclude employees whose incentive-based compensation does not exceed a specific dollar amount.

• We recommend that the Agencies make several adjustments to the definition of Significant Risk Taker (SRT). Specifically, we suggest that the Agencies limit the definition of SRT to those individuals who actually engage in risk-taking. We also suggest that the Agencies remove the percentage-based benchmarks and return to the material risk taker approach from the 2010 Interagency Guidance. If the Agencies

4

determine that some form of compensation test is required, we suggest the final rule utilize a dollar threshold rather than a percentage threshold for the relative compensation test and eliminate the exposure test. We further suggest that the final rule allow for only covered institutions to designate additional covered persons as SRTs.

• Finally, we recommend the Agencies amend the definition of Senior Executive Officer (SEO) to draw on existing, well-established regulatory definitions for the types of executive officers intended to be captured by the Proposal. If the Agencies continue to employ a new definition of SEO, we suggest the final rule omit “head of a major business line or control function” from that definition.

More detail regarding each of these comments is found below.

II. Specific Comments

A. Categorization of Covered Institutions

In attempting to implement Section 956 of the Dodd-Frank Act, the Proposal seeks to apply a broad range of requirements and recordkeeping responsibilities on all covered financial institutions with average total consolidated assets of $1 billion or more.4 To achieve this goal, the Proposal would create a three-tiered structure based solely on asset size, imposing additional requirements and restrictions on institutions with total consolidated assets of at least $50 billion (Level 2 institutions) and more stringent requirements and restrictions on institutions with total consolidated assets of at least $250 billion (Level 1 institutions).5 Covered institutions having average total consolidated assets less than $50 billion (Level 3 institutions) are not automatically subject to the additional requirements and restrictions imposed on Level 1 and Level 2 institutions, although the Agencies have reserved authority potentially to impose additional requirements on certain Level 3 institutions with total consolidated assets of at least $10 billion based on a consideration of the institution’s “activities, complexity of operations, risk profile, . . . compensation practices . . . in addition to other relevant factors.”6 Under the Proposal’s current approach, the undersigned banks would be categorized as either Level 1 or Level 2 institutions.

In the Proposal, the Agencies state the purpose of distinguishing among the covered institutions is to capture the most complex institutions or those for which risk-taking and their potential failure “implicates the greatest risks for the broader economy and financial system.”7 The Proposal further states that when an institution crosses the $250 billion threshold, it tends to be “significantly more complex and thus exposed to a higher level of risk” than smaller institutions.8 We assume the Agencies drew similar conclusions with respect to the $50 billion threshold used for identifying Level 2 institutions. Thus, we understand that the Agencies have

4 81 Fed Reg. at 37,803 (§ 42.3 & § 42.4); 81 Fed. Reg. at 37,808 (§ 236.3. & § 236.4); see also 81 Fed. Reg. at 37,685-88. 5 81 Fed Reg. at 37,803-06 (§ 42.5 & §§ 42.7-42.11); 81 Fed. Reg. at 37,808-13 (§ 236.5. & §§ 236.7-236.11). 6 81 Fed Reg. at 37,803-04 (§ 42.6); 81 Fed. Reg. at 37,810 (§ 236.6). 7 81 Fed. Reg. at 37,688. 8 Id.

5

determined that more stringent requirements should apply as the systemic risk footprint of a covered institution increases.

The current asset-based categorization proposed by the Agencies exacerbates a growing and troubling trend of using rudimentary and arbitrary asset thresholds as a proxy for identifying the most complex institutions that present significant systemic risks. The Proposal does not provide any reasonable basis for utilizing varying thresholds, except to indicate that the $250 billion threshold has been used elsewhere when determining the institutions subject to domestic implementation of international capital and liquidity standards.9 This approach is misguided and outdated, resulting in miscalibrated regulatory standards. Importing the same approach into the Proposal is equally as unsuitable for tailoring incentive-based compensation arrangements under Section 956.

The use of asset-based thresholds to categorize institutions results in incongruent groupings of banking organizations, with more traditional regional banking organizations with assets of $250 billion or more (Covered Regional Banks) being grouped together with the largest, most complex institutions – the global systemically important banking organizations (G-SIBs). This grouping occurs despite the vast differences in terms of business models, complexity, and risk to financial stability between the largest and most complex banking organizations and the more traditional, regional banking organizations that would be captured by the Level 1 threshold. Level 2 institutions, particularly those approaching the $250 billion threshold, could confront a similar challenge in the near future.

Given that the Agencies indicate that limits to incentive compensation should be tailored based on a measure of the systemic risk at issue,10 we urge the Agencies to adopt a risk-based approach for determining the thresholds for covered institutions, as opposed to an asset-based approach. Although various risk-based models could be employed – such as the approach outlined for certain Level 3 institutions described above – we recommend the Agencies use the existing systemic indicator approach that has been developed internationally and implemented in the United States by the Federal Reserve. The systemic indicator approach is a more sophisticated, dynamic tool that should be used to calibrate incentive compensation arrangements requirements, among other requirements, based on systemic risk. It accounts not for size only, but also for interconnectedness, substitutability, complexity, and cross-jurisdictional activity, each of which are key inputs for determining the level of risk presented by an institution to the U.S. financial system.

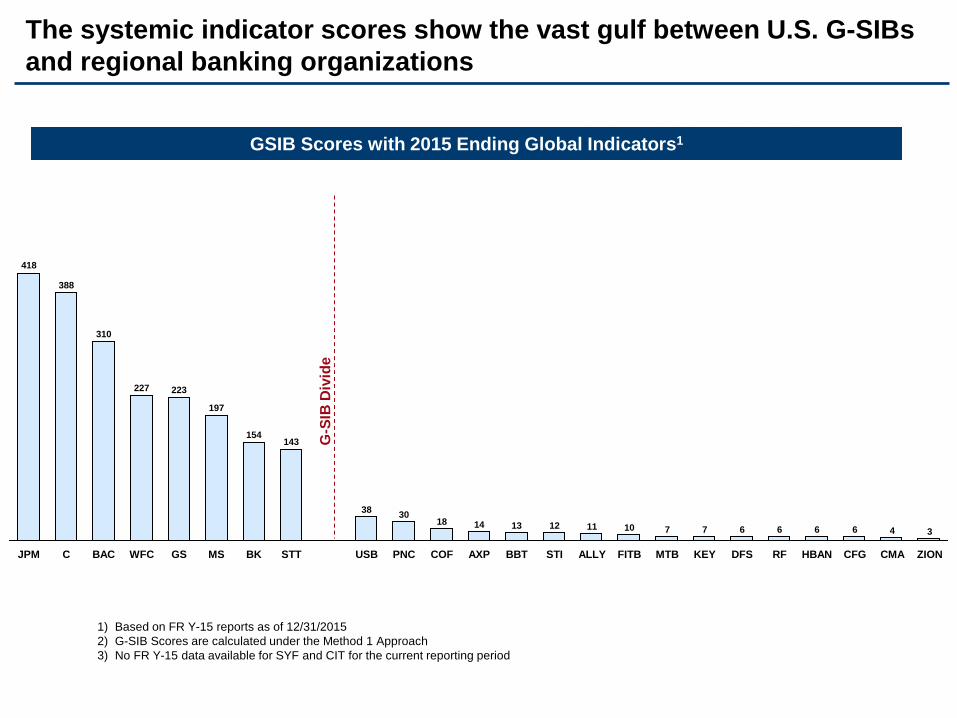

A cursory review of the systemic indicator approach aptly demonstrates that it would provide more powerful insights into complexity and the actual risk profile of an institution than the rudimentary asset threshold. Moreover, the systemic indicator data highlights the significant differences between regional banking organizations, on the one hand, and the largest, most complex banking organizations, which the Level 1 categorization appears intended to capture. For example:

9 Id. 10 Id. at 37,684.

6

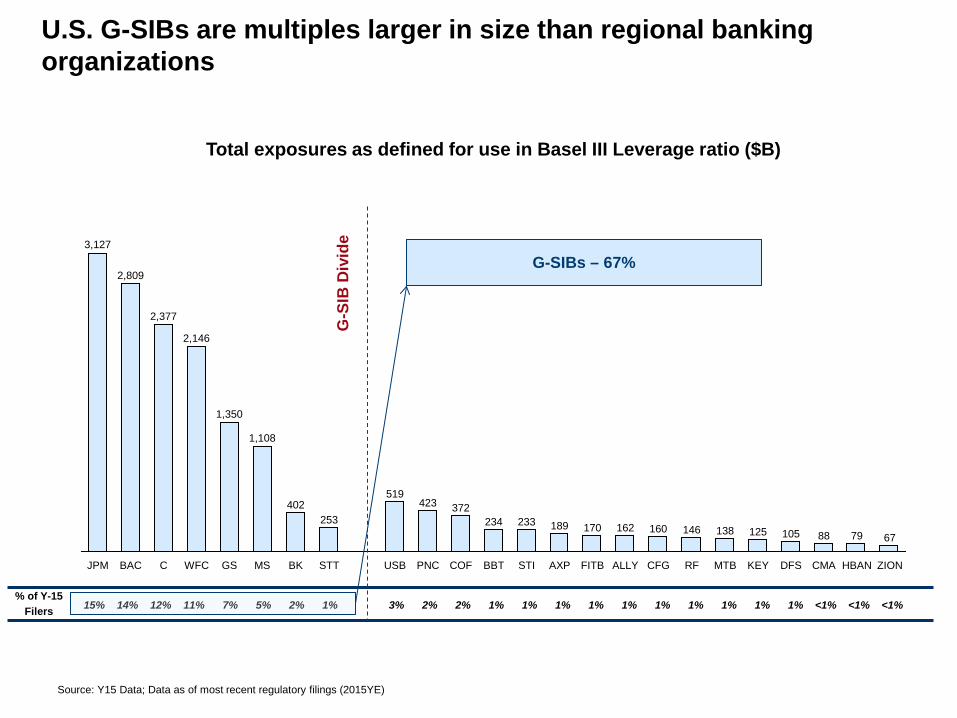

• As for size, the eight U.S. banking organizations identified as G-SIBs account for 67% of total exposures for all U.S. bank holding companies required to submit the Federal Reserve’s FR Y-15 Banking Organization Systemic Risk Report (“FR Y-15 Filers”),11 whereas the smallest non-custody G-SIB has total exposures of $1.1 trillion and the largest Covered Regional Bank has only $519 billion.

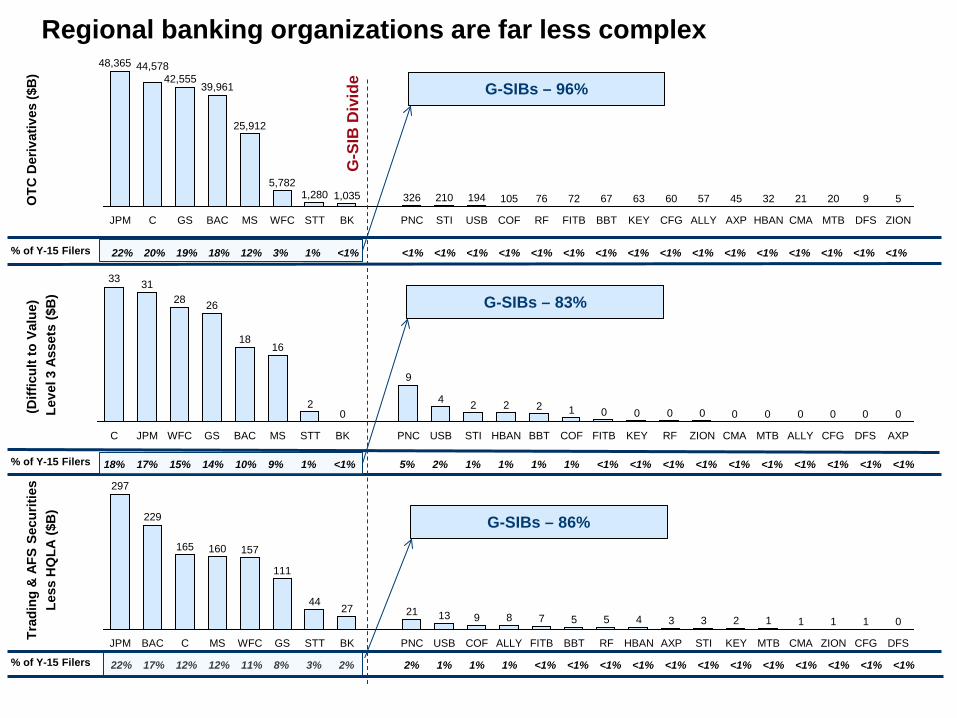

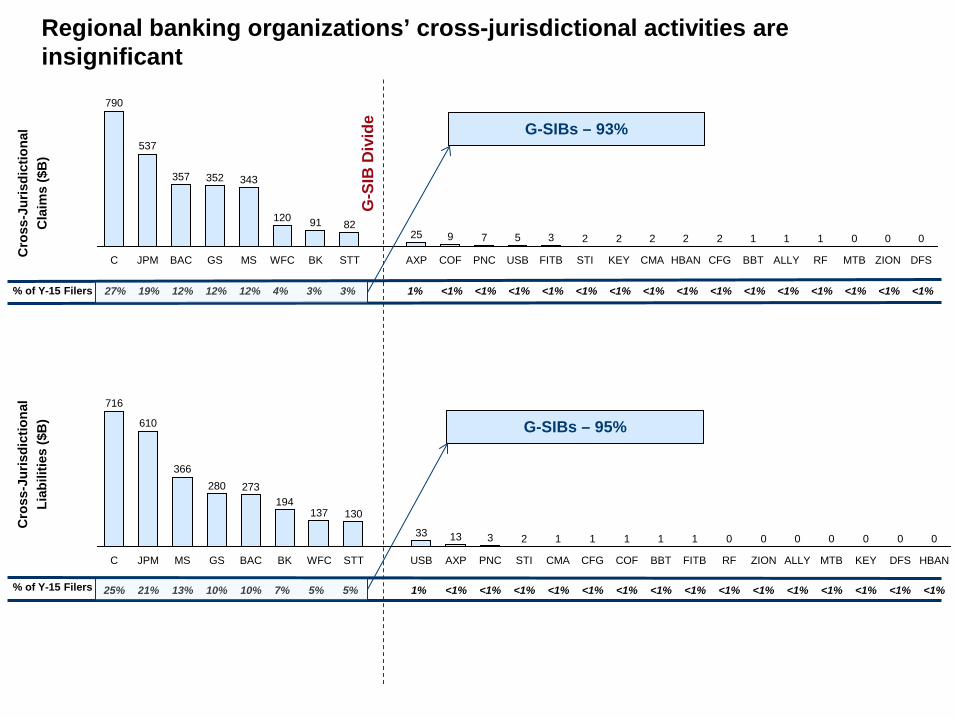

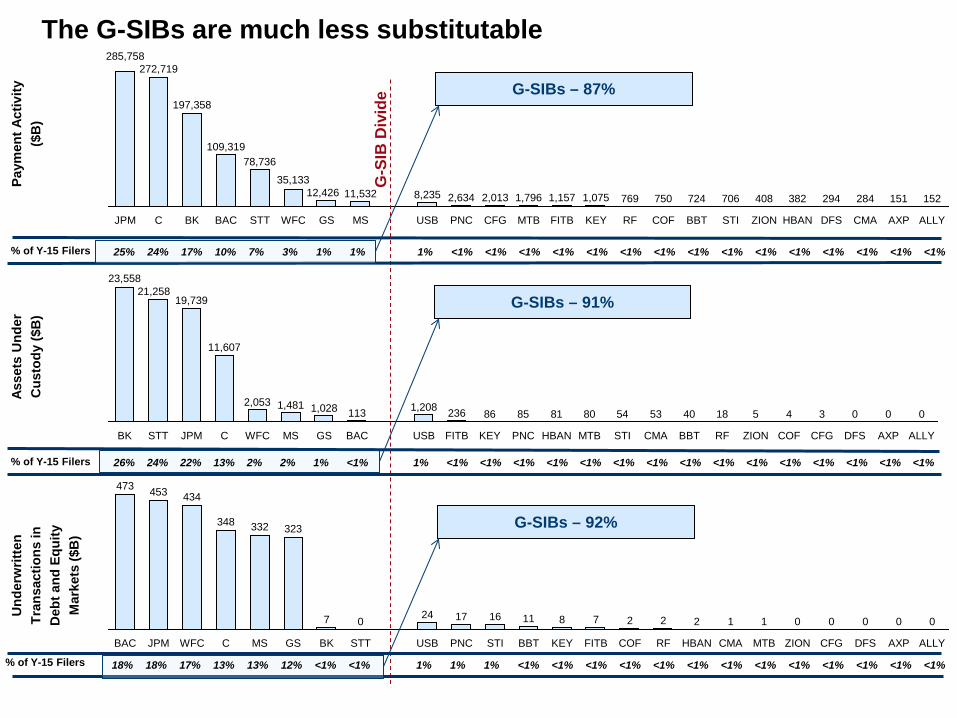

• With respect to the amount of over-the-counter (“OTC”) derivatives, an important measure of complexity, U.S. G-SIBs account for 96% of the notional value of all OTC derivatives for all FR Y-15 Filers, and the smallest non-custody G-SIB has OTC derivatives with a notional value of $5.8 trillion, compared to the largest Covered Regional Bank, which has only $326 billion. Similarly, U.S. G-SIBs account for 86% of trading and available-for-sale securities (less high quality liquid assets) for all FR Y-15 Filers, and the smallest non-custody G-SIB has $111 billion of such securities, compared to only $21 billion for the largest Covered Regional Banks.

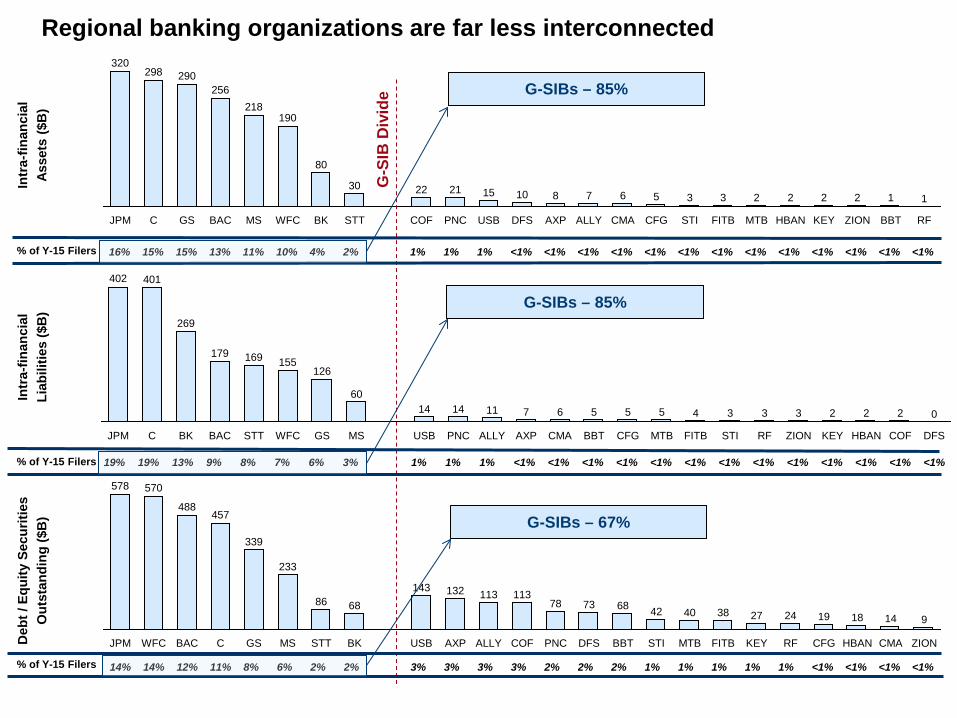

In addition to size and complexity, the remaining systemic indicators similarly demonstrate the vast gulf between U.S. G-SIBs and regional and traditional banking organizations. See the Appendix to this letter for additional data.

Perhaps as telling are the ultimate scores of systemic importance derived using the systemic indicator data. For example:

• Under the Federal Reserve’s systemic indicator methodology, a U.S. bank holding company is deemed to be a G-SIB if its systemic indicator score is 130 or more. The G-SIB cutoff (130) is more than three times greater than the systemic indicator score of the largest non-custody U.S. banking organization that is not identified as a G-SIB (42); and

• The average systemic indicator score of the eight U.S. G-SIBs (258) is almost seven times greater than that of the largest non-custody U.S. banking organization that is not a G-SIB (38).12

The systemic indicators and score data make clear that regional banking organizations, even those above the $250 billion threshold, are significantly less complex and present significantly fewer risks to financial stability than a U.S. G-SIB. More specifically, we believe that the data demonstrate that, whereas the U.S. G-SIBs present the types of increased systemic risk for which the Agencies have proposed Level 1 status, the data similarly demonstrate that regional banking organizations do not.

11 All FR Y-15 data in this letter are as of December 31, 2015. 12 Systemic indicator scores were calculated based on FR Y-15 reports as of December 31, 2015, and the Basel Committee’s 2015 systemic indicator denominators (converted into U.S. Dollars based on the spot USD/EUR exchange rate prevailing on December 31, 2014). A report compiled by the Office of Financial Research (“OFR”) draws similar conclusions using the Basel Committee’s essentially identical methodology. See Allahrakha et al., Office of Financial Research Brief, Systemic Importance Indicators for 33 U.S. Bank Holding Companies: An Overview of Recent Data (Feb. 12, 2015), available at http://financialresearch.gov/briefs/files/2015-02-12-systemic-importance-indicators-for-us-bank-holding-companies.pdf.

7

Moreover, an examination of the business model and risk profile of regional banking organizations demonstrates that they do not implicate the incentive compensation practices that Section 956 was intended to capture. Regional banks engage predominately in domestic consumer and commercial lending and deposit gathering. Regional banks have bank-centric business models, limited capital markets activities, and limited derivatives exposures. The business activities of regional banks are not, as the Proposal’s commentary notes, “significantly more complex” or related to “the [type of] risk-taking of [institutions], and their potential failure, [that] implicates greater risks of the financial system and the overall economy.”13

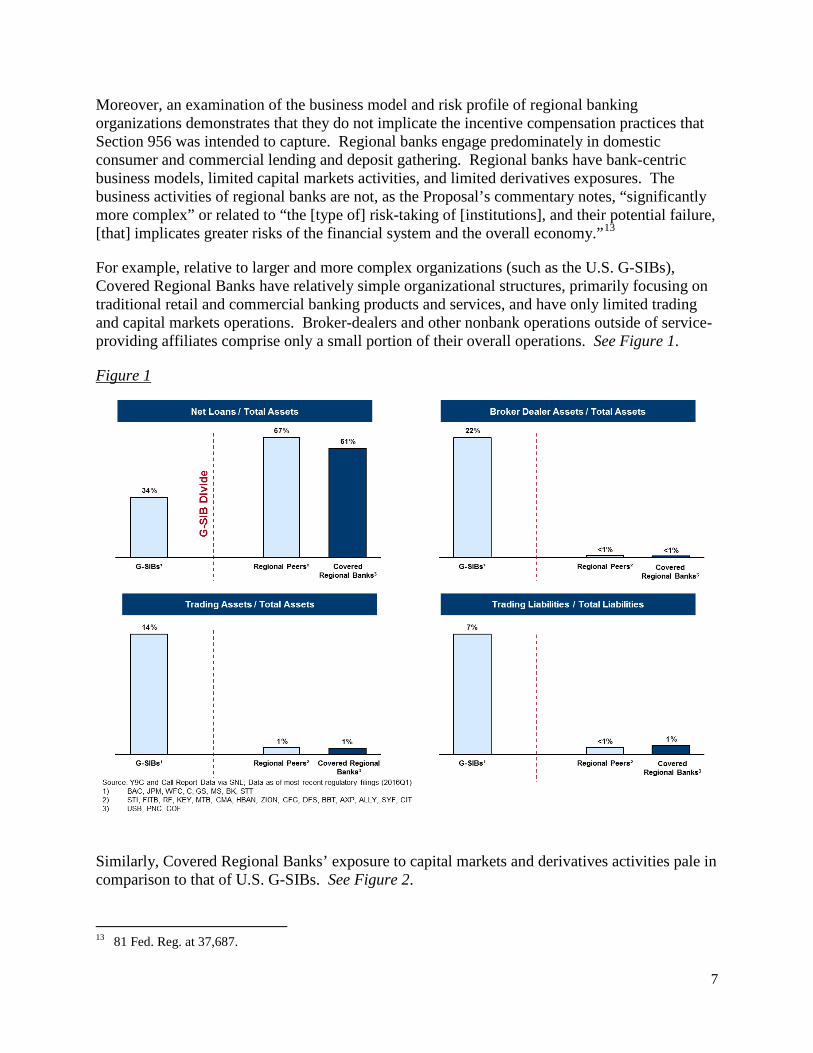

For example, relative to larger and more complex organizations (such as the U.S. G-SIBs), Covered Regional Banks have relatively simple organizational structures, primarily focusing on traditional retail and commercial banking products and services, and have only limited trading and capital markets operations. Broker-dealers and other nonbank operations outside of service-providing affiliates comprise only a small portion of their overall operations. See Figure 1.

Figure 1

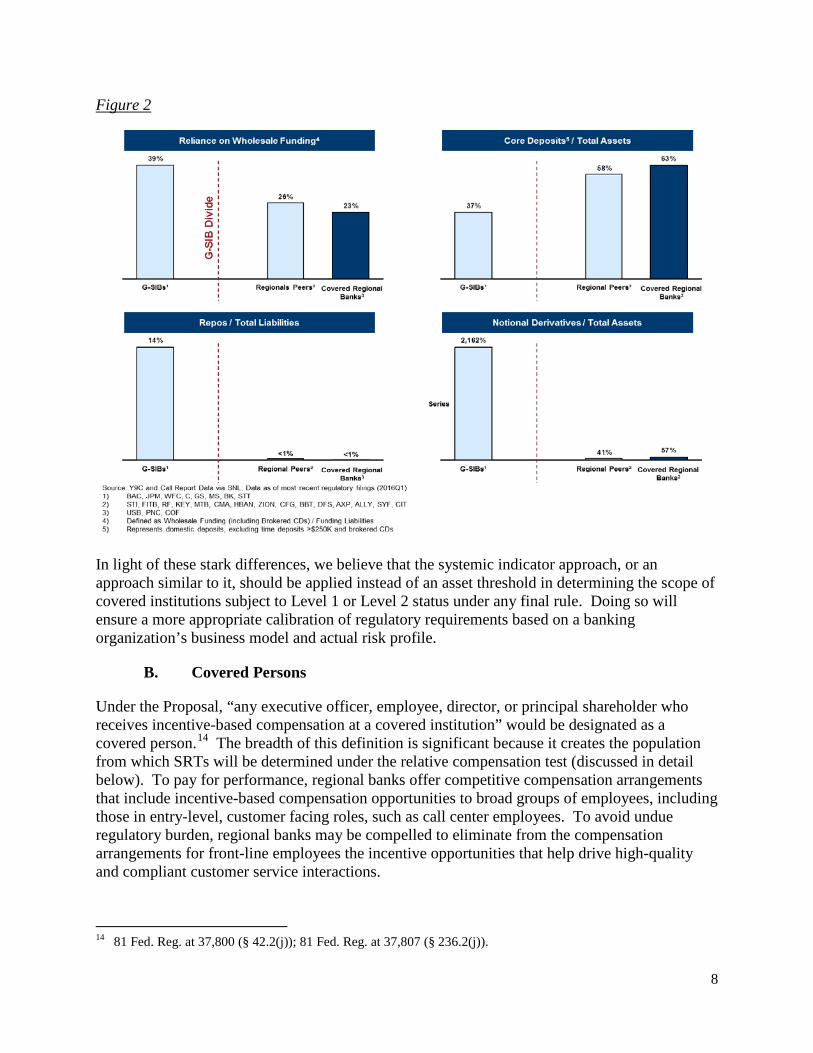

Similarly, Covered Regional Banks’ exposure to capital markets and derivatives activities pale in comparison to that of U.S. G-SIBs. See Figure 2.

13 81 Fed. Reg. at 37,687.

8

Figure 2

In light of these stark differences, we believe that the systemic indicator approach, or an approach similar to it, should be applied instead of an asset threshold in determining the scope of covered institutions subject to Level 1 or Level 2 status under any final rule. Doing so will ensure a more appropriate calibration of regulatory requirements based on a banking organization’s business model and actual risk profile.

B. Covered Persons

Under the Proposal, “any executive officer, employee, director, or principal shareholder who receives incentive-based compensation at a covered institution” would be designated as a covered person.14 The breadth of this definition is significant because it creates the population from which SRTs will be determined under the relative compensation test (discussed in detail below). To pay for performance, regional banks offer competitive compensation arrangements that include incentive-based compensation opportunities to broad groups of employees, including those in entry-level, customer facing roles, such as call center employees. To avoid undue regulatory burden, regional banks may be compelled to eliminate from the compensation arrangements for front-line employees the incentive opportunities that help drive high-quality and compliant customer service interactions.

14 81 Fed. Reg. at 37,800 (§ 42.2(j)); 81 Fed. Reg. at 37,807 (§ 236.2(j)).

9

With respect to the covered person definition, we recommend that the Agencies utilize existing material risk taker definitions in the 2010 Interagency Guidance. Specifically, we recommend defining covered persons to include category 1, 2 and 3 material risk takers, which would appropriately limit the final rule to only those individuals who could, either individually or collectively as part of a group, take the type of inappropriate risks that might lead to material financial loss. Under the existing supervisory process and 2010 Interagency Guidance, financial institutions and their regulators have identified material risk takers at their institutions based on the facts and circumstances specific to each institution.

We believe a decision to offer competitive incentive opportunities to company employees at all levels should not be influenced by the exposure to the Proposal’s covered person definition. If the Agencies maintain the proposed definition of covered person, we recommend that definition be revised to exclude employees whose incentive-based compensation does not exceed $50,000 (periodically adjusted for inflation). This proposed revision would reduce the inclusion of non-risk taking employees who may be exposed to the broad and prescriptive requirements and prohibitions of the Proposal.

C. Significant Risk Taker

i. Definition of Significant Risk Taker

We also have concerns regarding the Proposal’s current definition of an SRT, which is intended to target non-executives who are “in the position to put a Level 1 or Level 2 covered institution at risk of material financial loss….”15 An SRT includes covered persons whose incentive compensation makes up at least one-third of their total compensation and who meet either the relative compensation test or the exposure test.16 The basic SRT definition only utilizes quantitative measures, which could lead to a dramatic over-inclusion of employees as SRTs.

The definition of SRT is overly broad and would include employees beyond the Proposal’s contemplated population of risk takers. The Agencies’ stated goal in identifying an SRT is to apply the incentive-based compensation limits to individuals such as “managing directors, directors, senior vice presidents, relationship and sales managers, mortgage brokers, financial advisors, and product managers.”17

Unlike the Proposal’s definition of SEO, the nature of a particular position is not a factor in the Proposal’s current approach to identifying SRTs. Thus, the proposal potentially could designate extensive numbers of employees in support-type functions who are not involved in risk-taking, such as control functions. These potential restrictions on non-risk-takers’ compensation could negatively affect efforts to attract and retain talent, particularly in the area of cybersecurity and other technology fields, without supporting the underlying policy goals of the Proposal.

15 81 Fed. Reg. at 37,692. 16 81 Fed Reg. at 37,801 (§ 42.2(hh)); 81 Fed. Reg. at 37,808 (§ 236.2(hh)). 17 81 Fed. Reg. at 37,695.

10

To prevent non-risk-takers from being designated as SRTs, we recommend limiting SRTs to individuals actually engaged in risk-taking activities and excluding non-executive personnel in control functions, including second-line, third-line, and other support personnel. Excluding non-risk-takers will preserve the goal of identifying risk-taking employees and more closely align the Proposal with a principles-based approach to compensation management.

ii. The Relative Compensation Test

The Proposal’s relative compensation test attempts to capture non-executive employees who take significant risk and who have incentive compensation that is at least one-third of their total compensation. This test would require Level 1 institutions to designate as an SRT the highest paid 5% of all covered persons meeting the one-third incentive compensation criteria (excluding SEOs), including any subsidiaries that also are covered institutions; for Level 2 institutions, the threshold is 2%.18

We believe that the relative compensation test’s percentage-based threshold for SRT does not accurately capture covered persons who engage in substantial risk-based activities because it ignores qualitative risk activities of employees in favor of a blunt quantitative mechanism. Several factors inform our position.

First, the relative compensation test would be over-inclusive. The 5% and 2% thresholds for Level 1 and Level 2 institutions, respectively, reach too deep into these institutions’ organizations, which would apply compensation restrictions to individuals beyond those to be considered to have received “excessive compensation, fees, or benefits,” as described in Section 956.19 Because the threshold test only examines compensation levels vis-à-vis other employees, certain employees – such as those who provide technology development and support – could qualify as SRTs due to the high demand for technology expertise and the need to compensate them accordingly, even though such employees generally are not incented by business metrics that could put the company at risk for a material financial loss in the manner contemplated by the Proposal.

Second, the relative compensation test would undermine a level-playing field and negatively affect talent acquisition and retention, especially at regional banks. Because compensation levels differ among banks, an employee designated as an SRT at a regional bank could move to a similar position at a different institution and be exempt from the SRT designation. Smaller institutions may be subject to a lower threshold or otherwise be exempt from the SRT requirements. For the very largest banks, the presence of a greater number of higher-earning employees at these institutions could create competitive disadvantages for non-G-SIBs with lower overall compensation levels. As an example, a covered person employed in a small capital markets division at a regional bank could be designated as an SRT on the basis of relative compensation while an employee in the same position at a large investment bank could be free of any designation, despite having a similar or higher level of compensation.

18 81 Fed Reg. at 37,801 (§ 42.2(hh)); 81 Fed. Reg. at 37,808 (§ 236.2(hh)). 19 12 U.S.C. § 5641(b)(1).

11

The test also could disadvantage regional banks as compared to non-financial services companies. Employees engaged in non-risk taking support functions, such as technology, human resources, legal, finance, and compliance (among others) could be subject to the deferral requirements and, therefore, may choose to seek employment outside the financial services industry, where they could perform similar work but not be subject to the proposed compensation restrictions. An over-inclusive SRT definition will make it more difficult for banks to attract and retain highly-skilled employees with sought-after expertise. By limiting banks’ compensation options in attracting talent, the Proposal could subject regional banks to additional risks associated with difficulty in attracting high-quality talent, while doing little to alter risks from incentive compensation.

Third, the relative compensation test creates uncertainty for employees and is administratively burdensome. The relative compensation test would not provide clear advance notice to employees who may be designated as SRTs. Even if an employee on the margins of the test does not meet the relative threshold in a given year, that individual may meet the threshold in the future and such volatility may be enough to drive talent to other institutions or industries.

The quantitative aspects of the relative test also undermine the goal of consistently including employees who take significant risks. Variable compensation could have the effect of removing employees from SRT designation year-over-year, either with a change in the compensation mix of the company or if an individual’s incentive compensation did not trigger the one-third total compensation threshold. As a result, employees could move in and out of SRT designations each year, not based on changes in their role or risk-taking practices, but simply because of dollar amounts in their incentive compensation. The proposed percentage test also would greatly increase the complexity of compensation recordkeeping at our institutions.

To address these concerns, we recommend removing the percentage-based benchmarks and return to the material risk taker approach found in the 2010 Interagency Guidance.20 Although this group believes the inclusion criteria for SRTs should be based solely on the risk profile of the role, if the Agencies determine that a compensation test is required, we suggest the final rule utilize a dollar threshold (periodically adjusted for inflation), rather than a relative threshold, to identify individuals with total compensation above a certain level. In the Proposal, the Agencies ask for comment on replacing the relative compensation test with a dollar threshold test for a covered person at a Level 1 or Level 2 institution “who receives an annual base salary and incentive base salary compensation of $1 million or more.”21 We agree that the relative compensation test should be replaced with the compensation level described in the Proposal. The dollar threshold would better reflect those who are able to take meaningful risks at the institutions. Furthermore, setting a dollar threshold allows current and prospective employees to

20 Such material risk takers include “[i]ndividual employees, including non-executive employees, whose activities may expose the organization to material amounts of risk (e.g., traders with large position limits relative to the organization’s overall risk tolerance); and . . . [g]roups of employees who are subject to the same or similar incentive compensation arrangements and who, in the aggregate, may expose the organization to material amounts of risk, even if no individual employee is likely to expose the organization to material risk (e.g., loan officers who, as a group, originate loans that account for a material amount of the organization’s credit risk).” 75 Fed. Reg. at 36,407. 21 81 Fed. Reg. at 37,699.

12

understand with greater certainty the implications of a compensation level and how it would be impacted by these rules.

iii. The Exposure Test

Separate from the relative compensation test, the Proposal also would designate as an SRT any covered person who “may commit or expose 0.5% or more of the [institution’s] common equity tier 1 capital,”22 regardless of whether that individual is employed by the impacted entity. The exposure threshold is the same for both Level 1 and 2 institutions and is calculated on the aggregate lending or trading authority of the individual, rather than a per transaction basis. Additionally, the exposure test would include an employee whose lending authority is subject to approval on a rolling basis but with no individual specified and aggregated maximum.23

Although we appreciate the Agencies’ efforts at incorporating risk-based measures into the SRT designation, the structure of the exposure test is too broad and could implicate all lending officers as SRTs at many institutions, since the proposal does not distinguish employees with individual deal transaction caps but no annual aggregate limit. Many regional banks do not calculate exposure with an aggregate limit, and the Proposal likely would require arbitrary caps and burdensome recordkeeping requirements for individual lending, even when the exposure is subject to further approval. Furthermore, the test measures an individual’s authority or potential to commit or expose the institution, as opposed to actually committing or exposing the institution to that threshold. The result would be that individual lenders may be subject to the exposure test even if they will not come close to risking 0.5% of tier 1 capital on an annual basis.

To address these concerns, we restate our recommendation to return to a principles-based approach that is more in-line with the 2010 Interagency Guidance. However, if the Agencies proceed with the Proposal, we propose eliminating the exposure test and instead adopting the compensation dollar threshold above as the sole test to identify SRTs.

iv. SRT Designation by the Agencies

The Agencies recognize the limitations of a quantitative-based method of determining SRTs and, as such, have proposed allowing the Agencies (as well as institutions) to designate persons as SRTs.24 The Proposal would allow each Agency the flexibility to use its own procedures to document and describe the proposed designations, while giving the covered person and institution an opportunity to respond.25 Although we agree that a principles-based approach and analysis is the preferred approach, our concern here is that Agencies will be able to designate individuals as SRTs according to standards that are not articulated in current regulations or guidance or otherwise communicated to the industry. This authority may result in inconsistent treatment among different Agencies creating confusion and additional complexity to compensation programs.

22 81 Fed Reg. at 37,801 (§ 42.2(hh)); 81 Fed. Reg. at 37,808 (§ 236.2(hh)). 23 81 Fed Reg. at 37,696. 24 81 Fed. Reg. at 37,693; see also 81 Fed Reg. at 37,802 (§ 42.2(hh)(2)); 81 Fed. Reg. at 37,808 (§ 236.2(hh)(2)). 25 81 Fed. Reg. at 37,693.

13

Instead of allowing an Agency to designate an SRT, institutions should be responsible for designating their employees as SRTs in accordance with principles and rules articulated by the Agencies. Regional banks and other institutions are required to know their own risk profiles and compensation structures, and thus it should be a covered institution’s responsibility to identify and manage its employees’ risk-taking activities, subject to the Agency’s examination and supervision.

D. Senior Executive Officer

The Proposal seeks to impose certain additional requirements on individuals who meet the definition of SEO. SEOs are defined to include a list of specified officer titles or functions,26 as well as the “head of a major business line or control function.”27 This definition expands upon the definitions of “senior executives” from the 2010 Interagency Guidance28 and “executive officer” from the 2011 proposed rule.29

Similar to our concerns with the Proposal’s definition of SRT, we are concerned about the impact an expansive definition of SEO will have on regional banks and our ability to recruit and retain talent. As noted above, we already operate in a highly and increasingly competitive environment. Including additional personnel under the final rule could disadvantage regional banks as compared to other financial institutions, unregulated financial providers and servicers, and companies outside of the financial services industry.

Rather than creating a new regulatory definition for senior executive officers, we suggest the Agencies draw on existing, well-established regulatory definitions for the types of executive officers intended to be captured by the Proposal. Specifically, we recommend tying the definition of SEO to “executive officers” under Rule 3b-7 of the Securities Exchange Act of 193430 or “officers” under Rule 16a-1(f) of the same Act.31 These definitions cover almost an identical group of individuals: the president; vice presidents in charge of principal business units, division, or functions; and other persons who perform a policy-making function. The only difference between the two is Rule 16a-1(f) explicitly includes a company’s principal financial officer and principal accounting officer.

Utilizing existing regulations would allow covered institutions to leverage processes already well-known and often used for identifying impacted executives and reviewing their incentive compensation, thereby minimizing any unnecessary confusion and increased regulatory burden. Both of the proffered definitions include persons in charge of principal business units, divisions,

26 Specifically, the enumerated list includes “President, chief executive officer, executive chairman, chief operating officer, chief financial officer, chief investment officer, chief legal officer, chief lending officer, chief risk officer, chief compliance officer, chief audit executive, chief credit officer, [and] chief accounting officer.” 81 Fed. Reg. at 37,801 (§ 42.2(gg)); 81 Fed. Reg. at 37,808 (§ 236.2(gg)). 27 Id. 28 75 Fed. Reg. at 36,407 & n.10. 29 76 Fed. Reg. 21,170, 21,204 (§ 42.3(f)) (proposed April 14, 2011). See also 81 Fed. Reg. at 37,691. 30 See 17 C.F.R. § 240.3b-7. 31 See 17 C.F.R. § 240.16a-1(f).

14

or functions, arguably the same as individuals intended to be captured as the “head of a major business line.” All publicly-traded financial institutions have compensation committees that already review and approve incentive compensation for all executive officers’ and officers’ under either Rule 3b-7 or Rule 16a-1(f), respectively.

To the extent the Agencies retain a separate definition of SEO, we suggest that definition omit “head of a major business line or control function,” as the inclusion of this phrase is redundant with other definitions of the Proposal and overly broad. Oversight of compensation arrangements for the head of any major business line already would be captured under the rule, either directly as executive officers or officers under existing regulations or under the definition of SRT. If an individual is not captured within either of these definitions, that individual, we submit, should not otherwise be considered an SEO under the final rule. Alternatively, if the Agencies wish to retain a reference to business lines, the final rule could refer to the head of a “core business line,” a known and well-established definition used in the context of resolution planning.32 This definition also includes the concept of material loss, similar to Section 956 of the Dodd-Frank Act – specifically, that the failure of a core business line would result in a material loss of revenue, profit, or franchise value.

As for the head of a control function, the Agencies note in the commentary that they seek to encompass as SEOs not only individuals who generate risk of material financial loss, but also those who “play a role in identifying, addressing, and mitigating that risk.”33 However, we do not believe this rationale supports expanding the definition of SEO to include the head of a control function as currently defined.34 As an initial matter, many heads of control functions already are included as “executive officers” under current SEC regulations (e.g., heads of legal, HR, risk, etc.). The head of a control function who is not a policymaker – and therefore not within the scope of the SEC regulations – does not play an important enough role to be included as an SEO.

More importantly, senior executives at financial institutions set the tone from the top that risk management is everyone’s responsibility. Our institutions have enhanced risk management, controls, and training as we have conformed to the 2010 Guidance to create risk sensitive cultures. Attempting to identify each head of every group “responsible for identifying, measuring, monitoring, or controlling risk-taking” would be extremely difficult and could carve too deep within a covered institution, especially to the extent the agencies continue to determine SEOs on an entity-by-entity basis. In addition, compensation arrangements for business line personnel and control functions generally are not analogous. Although certain business line personnel may be incentivized through compensation to take risk, the same is not true for personnel in control functions at regional banks, whose ordinary job responsibility is to manage and mitigate risk. Employees in control functions do not receive incentive-based compensation 32 “Core business lines means those business lines of the covered company, including associated operations, services, functions and support, that, in the view of the covered company, upon failure would result in a material loss of revenue, profit, or franchise value.” 12 C.F.R. § 243.2(d). 33 81 Fed. Reg. at 37,691. 34 A control function is defined in the Proposal as “a compliance, risk management, internal audit, legal, human resources, accounting, financial reporting, or finance role responsible for identifying, measuring, monitoring, or controlling risk-taking.”81 Fed Reg. at 37,800 (§ 42.2(h)); 81 Fed. Reg. at 37,807 (§ 236.2(h)).

15

based on performance metrics (for example, the number of deals they review or prevent), as control functions are not easily subject to measurable outcomes.

The proposed definition also has the potential to overstate an individual’s “ability to influence the risk measures and other information and judgments that a covered institutions uses for risk management, internal control, or financial purposes.” 35 Individuals senior enough to influence risk behavior would be captured under other definitions of the Proposal (such as SRTs) or otherwise would have their incentive compensation directly overseen by SEOs pursuant to corporate governance and reporting structures generally utilized by financial institutions.

If the Agencies were to utilize the phrase “head of a major business line or control function” in the final rule, we request the additional specificity for which executive officers are intended to be captured beyond the titles and functions otherwise enumerated in the Proposal.

We further suggest that SEOs be identified on a consolidated (i.e., parent company) level, instead of for each covered institution individually. Allowing a consolidated approach would be more aligned with existing governance structures, eliminate redundancies, and be less burdensome on our institutions. Officers of a subsidiary can be deemed officers of a parent company if those officers perform a policy-making function for the parent itself under the Securities Exchange Act regulations identified above.

III. Conclusion

We thank the Agencies for the opportunity to comment on the Proposal and respectfully ask for consideration of the recommendations and suggestions in this letter. If you have any questions or would like more information regarding our comments, please do not hesitate to contact any of the individuals listed in Attachment 1.

Sincerely,

BB&T Corporation

Capital One Financial Corporation

PNC Financial Services Group

U.S. Bancorp

35 81 Fed. Reg. at 37,691.

Attachment 1

Robert J. Johnson Senior Executive Vice President, General Counsel, Secretary and Chief Corporate Governance Officer BB&T Corporation (336) 733-2180 [email protected]

Vicki C. Henn Chief Human Resources Officer PNC Financial Services Group (412) 768-8083 [email protected]

Jory A. Berson Chief Human Resources Officer Capital One Financial Corporation [email protected]

Jennie P. Carlson Executive Vice President, Human Resources U.S. Bancorp (612) 303-7699 [email protected]

Appendix

GSIB Scores with 2015 Ending Global Indicators1

RF

6

DFS

6

KEY

7

MTB

7

FITB

10

STI

12

BBT

13

AXP

14

COF

18

PNC

30

USB

38

STT

143

BK

154

ALLY

11

ZION

3

CMA

4

CFG

6

HBAN

6

MS

197

GS

223

WFC

227

BAC

310

C

388

JPM

418

1) Based on FR Y-15 reports as of 12/31/2015 2) G-SIB Scores are calculated under the Method 1 Approach 3) No FR Y-15 data available for SYF and CIT for the current reporting period

G-S

IB D

ivid

e

The systemic indicator scores show the vast gulf between U.S. G-SIBs and regional banking organizations

U.S. G-SIBs are multiples larger in size than regional banking organizations

DFS

105 146 79

RF MTB

138

KEY

125

HBAN CMA

88

372

PNC

423

USB

519

STT

253

BK

402

MS

1,108

GS

1,350

CFG

160

ALLY

162

FITB

170

AXP

189

STI

233

BBT

234

COF WFC

2,146

C

2,377

BAC

2,809

JPM

3,127

67

ZION

Total exposures as defined for use in Basel III Leverage ratio ($B)

G-S

IB D

ivid

e

Source: Y15 Data; Data as of most recent regulatory filings (2015YE)