37

JUNTA GENERAL ACCIONISTAS 2016 Madrid, 6 de abril de 2016

JUNTA GENERALACCIONISTAS 2016

Madrid, 6 de abril de 2016

This presentation has been prepared by MERLIN Properties SOCIMI, S.A. (the “Company”) for informational use only.

The information contained in this presentation does not purport to be comprehensive or to contain all the information that a prospective purchaser of securities of the Company may desire or require in deciding whether or not to purchase such securities. The information contained in this document is subject to change, verification and completion without notice. Neither the Company nor any of affiliates, advisors or agents makes any representation or warranty, express or implied, as to the accuracy or completeness of any information contained or referred to in this document. Each of the Company and its affiliates, advisors or agents expressly disclaims any and all liabilities which may be based on this document, the information contained or referred to therein, any errors therein or omissions therefrom. Neither the Company, nor any of its affiliates, advisors or agents undertakes any obligation to provide the recipients with access to additional information or to update this document or to correct any inaccuracies in the information contained or referred to therein.

Certain statements in this document regarding the market and competitive position data may be based on the internal analyses of the Company, which involve

certain assumptions and estimates. These internal analyses may have not been verified by any independent sources and there can be no assurance that the assumptions or estimates are accurate. Accordingly, undue reliance should not be placed on any of the industry, market or competitive position data contained in this presentation. Additionally, certain information contained herein may be based on management accounts and estimates of the Company and may have not been audited or reviewed by the Company’s auditors. Recipients should not place undue reliance on this information. The financial information included herein may have not been reviewed for accuracy or completeness and, as such, should not be relied upon.

This information is provided to the recipients for informational purposes only and recipients must undertake their own investigation of the Company. The information providing herein is not to be relied upon in substitution for the recipient’s own exercise of independent judgment with regard to the operations, financial condition and prospects of the Company.

The distribution of this presentation in some jurisdictions may also be restricted by law and persons into whose possession this presentation comes should inform themselves about and observe any such restrictions. The securities of the Company have not been

and, should there be an offering, will not be registered under the U.S. Securities Act of 1933, as amended (the “Securities Act”), or the U.S. Investment Company Act of 1940, as amended (the “Investment Company Act”). Such securities may not be offered or sold in the United States except on a limited basis, if at all, to Qualified Institutional Buyers (as defined in Rule 144A under the Securities Act) in reliance on Rule 144A or another exemption from, or transaction not subject to, the registration requirements of the Securities Act. The securities of the Company have not been and, should there be an offering, will not be registered under the applicable securities laws of any state or jurisdiction of Canada or Japan and, subject to certain exceptions, may not be offered or sold within Canada or Japan or to or for the benefit of any national, resident or citizen of Canada or Japan.

THIS PRESENTATION DOES NOT CONSTITUTE OR FORM PART OF ANY OFFER FOR SALE OR SOLICITATION OF ANY OFFER TO BUY ANY SECURITIES NOR SHALL IT OR ANY PART OF IT FORM THE BASIS OF OR BE RELIED ON IN CONNECTION WITH ANY CONTRACT OR COMMITMENT TO PURCHASE SHARES. ANY DECISION TO PURCHASE SHARES IN ANY OFFERING SHOULD BE MADE SOLELY ON THE BASIS OF PUBLICLY AVAILABLE INFORMATION ON THE COMPANY.

This presentation may include forward-looking statements. All statements other than statements of historical facts included in this presentation, including, without limitation, those regarding the financial position, business strategy, management plans and objectives for future operations of the Company are forward-looking statements. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which may cause such actual results, performance or achievements, or industry results, to be materially different from those expressed or implied by these forward-looking statements. These forward-looking statements are based on numerous assumptions regarding the present and future business strategies of the Company and the environment in which they expect to operate in the future.

Forward-looking statements speak only as of the date of this presentation and the Company expressly disclaim any obligation or undertaking to release any update of, or revisions to, any forward-looking statements in this presentation, any change in their expectations or any change in events, conditions or circumstances on which these forward-looking statements are based.

In reviewing this presentation, the recipient is agreeing to, and accepting, the foregoing restrictions and limitations.

DISCLAIMER

Resultados financieros 2015 1 ı 2 ı 3

Rendimiento de la cartera 1 ı 2 ı 3

Composición Consejo de Administración 4

Remuneración 5 ı 6 ı 7 ı 8

Eventos de capital y deuda 9 ı 10 ı 11 ı 12

Mejoras de gobierno corporativo

Perspectivas 2016

Puntos orden del día

JUNTA GENERALACCIONISTAS 2016

Madrid, 6 de abril de 2016

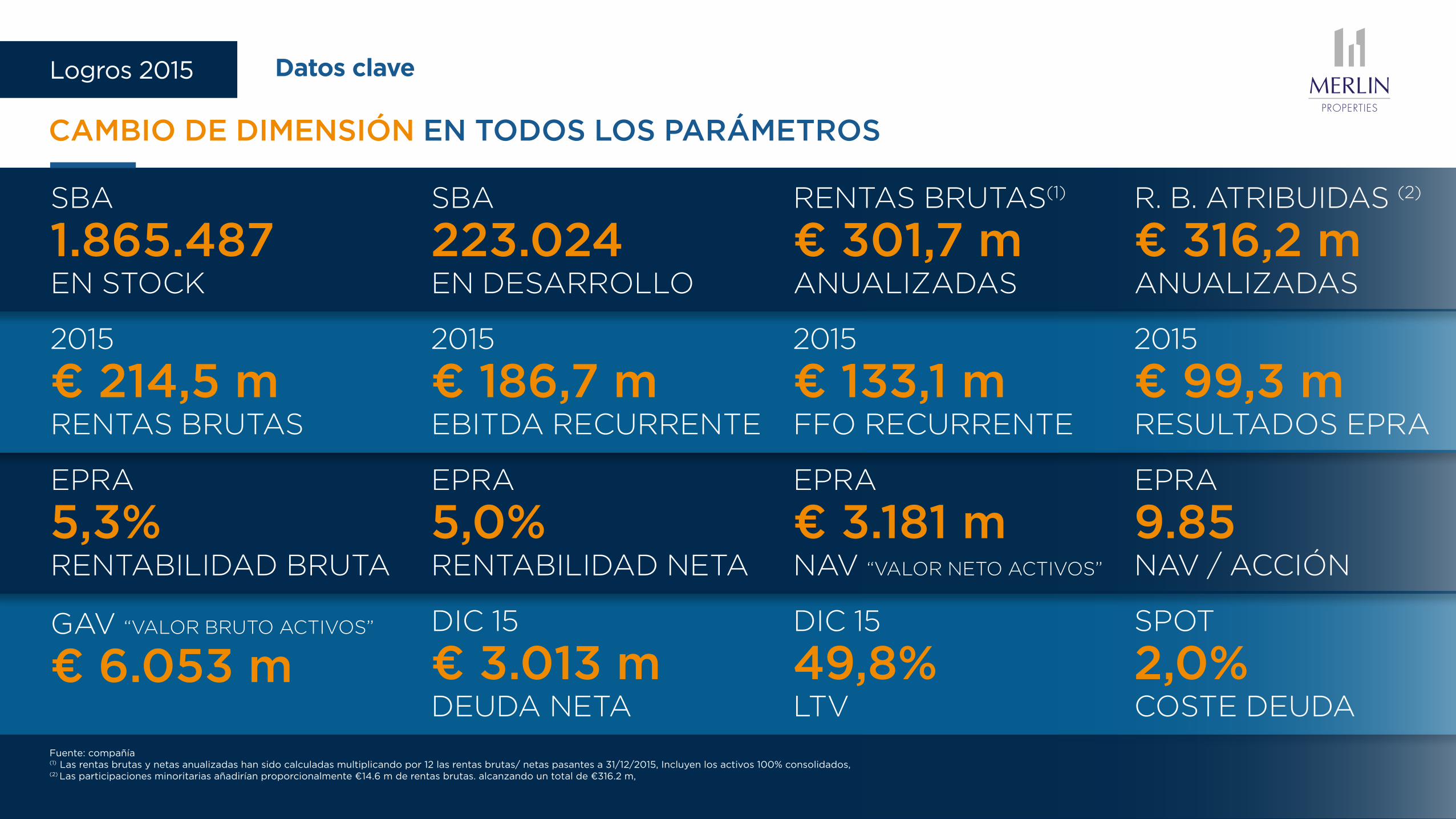

Logros 2015

AÑO INTENSO QUE HA POSICIONADO A MERLIN COMO REFERENTE EN EL MERCADO INMOBILIARIO

ESPAÑOL: OPERADOR NÚMERO UNO EN OFICINAS, LOCALES COMERCIALES Y LOGÍSTICA

Adquisición de 5 activos por un valor agregado de €102 m

Adquisición de Testa por valor de fondos propios de aprox. €2.000 millones creando la compañía inmobiliaria líder del sector en España

Adquisición de 43 activos y ZAL Port por un valor agregado de €325 m

Adquisición de 2 activos logísticos en España y 2 edificios de oficinas en Portugal por un valor agregado de €133 m

Enero 2015 Junio 2015

Junio 2015

Sept 2015 Enero 2016

Marzo 2016

Mayo 2015

Julio 2015

Dic2015

Dic2015

Feb2016

Ampliación de capital de €614 m

Inclusión en el

IBEX-35

Rating BBB de S&P

Refinanciación de la deuda de Testa y repago del préstamo puente asociado a la compra de Testa (€1.700 m)

Ampliación de capital de €1.034 m para

financiar en parte la compra de Testa

GAV “VALOR BRUTO ACTIVOS”

€ 6.053 m

RENTABILIDAD BRUTA

EPRA

5,3%

RENTAS BRUTAS

2015

€ 214,5 m

EN STOCK

SBA

1.865.487

DEUDA NETA

DIC 15

€ 3.013 m

RENTABILIDAD NETA

EPRA

5,0%

EBITDA RECURRENTE

2015

€ 186,7 m

EN DESARROLLO

SBA

223.024

COSTE DEUDA

SPOT

2,0%

NAV / ACCIÓN

EPRA

9.85

RESULTADOS EPRA

2015

€ 99,3 m

ANUALIZADAS

R. B. ATRIBUIDAS (2)

€ 316,2 m

LTV

DIC 15

49,8%

NAV “VALOR NETO ACTIVOS”

EPRA

€ 3.181 m

FFO RECURRENTE

2015

€ 133,1 m

ANUALIZADAS

RENTAS BRUTAS(1)

€ 301,7 m

Logros 2015

Fuente: compañía (1) Las rentas brutas y netas anualizadas han sido calculadas multiplicando por 12 las rentas brutas/ netas pasantes a 31/12/2015, Incluyen los activos 100% consolidados, (2) Las participaciones minoritarias añadirían proporcionalmente €14.6 m de rentas brutas. alcanzando un total de €316.2 m,

CAMBIO DE DIMENSIÓN EN TODOS LOS PARÁMETROS

Datos clave

SOLIDEZ EN UN AÑO TRANSFORMACIONAL

RESULTADOS FINANCIEROS 2015

1 ı 2 ı 3Puntos orden del día

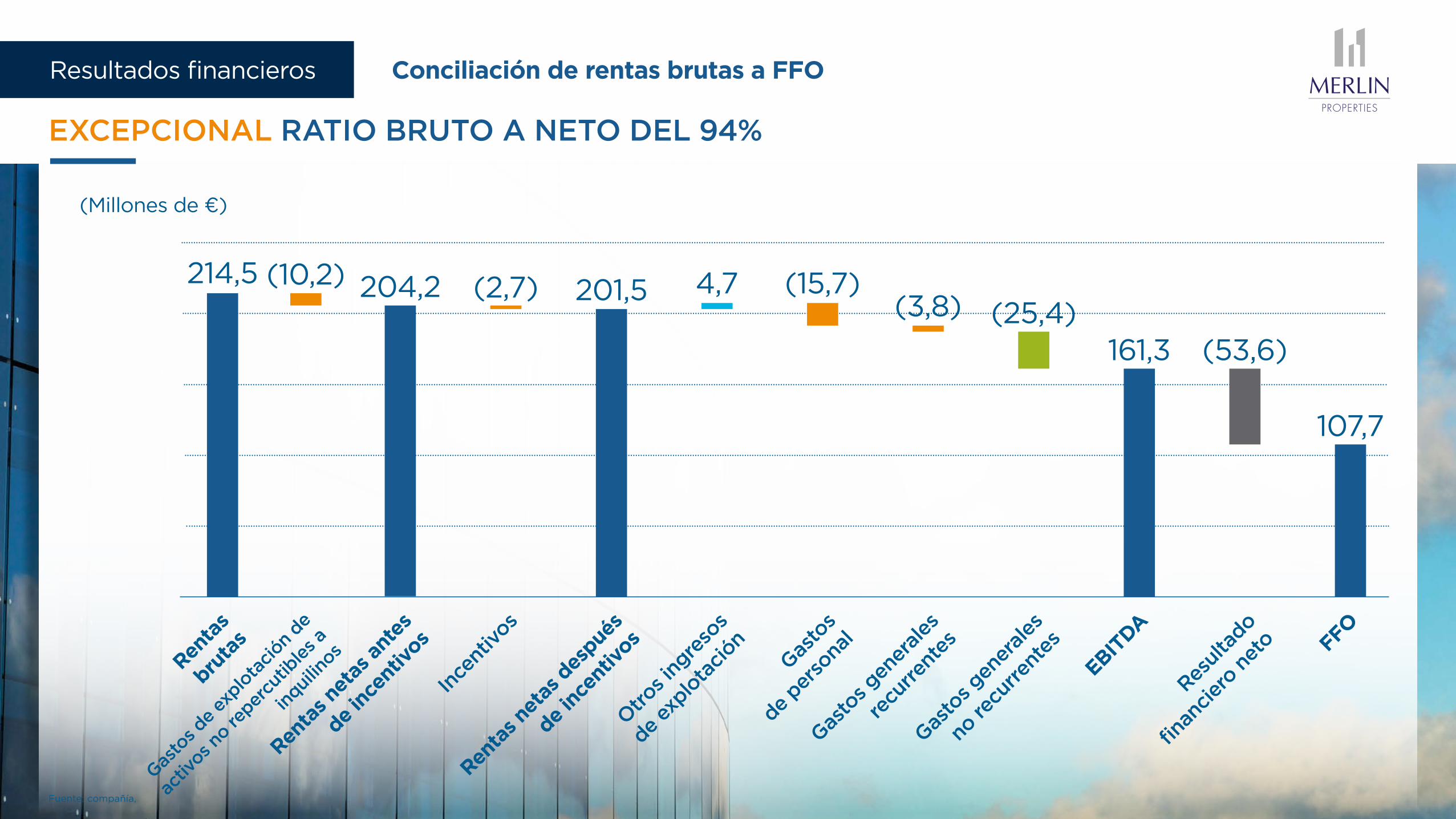

Resultados financierosPérdidas y ganancias consolidado (resultado de Testa sólo del segundo semestre)

LOS RESULTADOS REFLEJAN UN FUERTE CRECIMIENTO DURANTE EL PERIODO

EBITDA recurrente€ 0,58

FFO recurrente€ 0,41

EPRA BPA

€ 0,31

IFRS BPA

€ 0,15

Pérdidas y ganancias consolidado

Rentas brutas anualizadas pasantes

€ 301,7 m1

Rentas netas anualizadas pasantes

€ 284,3 m1

2015 2014

Rentas brutas € 214,5 m € 56,8 m

Rentas netas(2) € 201,5 m € 54,0 m

EBITDA € 161,2 m € 38,0 m

FFO € 107,7 m € 19,9 m

EBITDA recurrente(3) € 186,7 m € 50,4 m

FFO recurrente(4) € 133,1 m € 32,4 m

EPRA beneficio neto € 99,3 m € 20,4 m

IFRS beneficio neto € 49,1 m € 49,7 m

Fuente: compañía. (1) Las rentas brutas y netas anualizadas han sido calculadas multiplicando por 12 las rentas brutas/netas pasantes a diciembre 2015(2) Rentas brutas netas de gastos comunes no repercutibles a los inquilinos, incentivos e impagos(3) EBITDA recurrente igual al EBITDA menos los gastos puntuales no recurrentes (€25,4 m)(4) FFO recurrente igual al FFO menos los gastos puntuales no recurrentes (€25,4 m)

Source: Company. (1) Annualized gross rents and net rents have been calculated as passing gross / net rent as of December 31st, multiplied by 12.(2) Gross rents net of property expenses not recharged to tenants, incentives and collection loss.(3) Recurring EBITDA equals EBITDA less non-recurrent one-off expenses (€ 25.4 m).(4) Recurring FFO equals FFO less non-recurrent one-off expenses (€ 25.4 m).

Por acción

Conciliación de rentas brutas a FFO

EXCEPCIONAL RATIO BRUTO A NETO DEL 94%

Fuente: compañía,

Renta

s

bruta

s

Gas

tos d

e ex

plota

ción

de

activ

os no re

percu

tible

s a

inqui

linos

Renta

s net

as a

ntes

de in

cent

ivos

Ince

ntivos

Gas

tos g

ener

ales

recu

rrent

es

Gas

tos g

ener

ales

no re

curre

ntes

EBITDA

Resul

tado

financ

iero

net

o FFO

Gas

tos

de per

sona

l

Otro

s ing

reso

s

de ex

plota

ción

Renta

s net

as d

espué

s

de in

cent

ivos

(Millones de €)

214,5 (10,2) 204,2 (2,7) 4,7 (15,7)(3,8) (25,4)

161,3 (53,6)

107,7

201,5

Resultados financieros

CRECIMIENTO SIGNIFICATIVO DEL GAV Y NAV, TRAS UNA INTENSA ACTIVIDAD INVERSORA EN 2015 Y LA REVALORIZACIÓN DE LA CARTERA

Dic-15 Ajustado Dic-14 Dic-14

GAV € 6.053 m € 5.389 m (1) € 2.232 m

EPRA NAV € 3.181 m € 2.951 m (2) € 1.355 m

EPRA NAV por acción € 9,85 € 9,13 € 10.50

EPRA NAV Ajustado € 2.982 m € 2.751 m € 1.355 m

EPRA NAV Ajustado por acción

€ 9,23 € 8,92 € 10,50

Valoración

Fuente: compañía(1) GAV incluye el agregado de las valoraciones de MERLIN y Testa a 31/12/14(2) Incluye los ingresos netos provenientes de ampliaciones de capital llevadas a cabo en 2015

ValoraciónResultados financieros

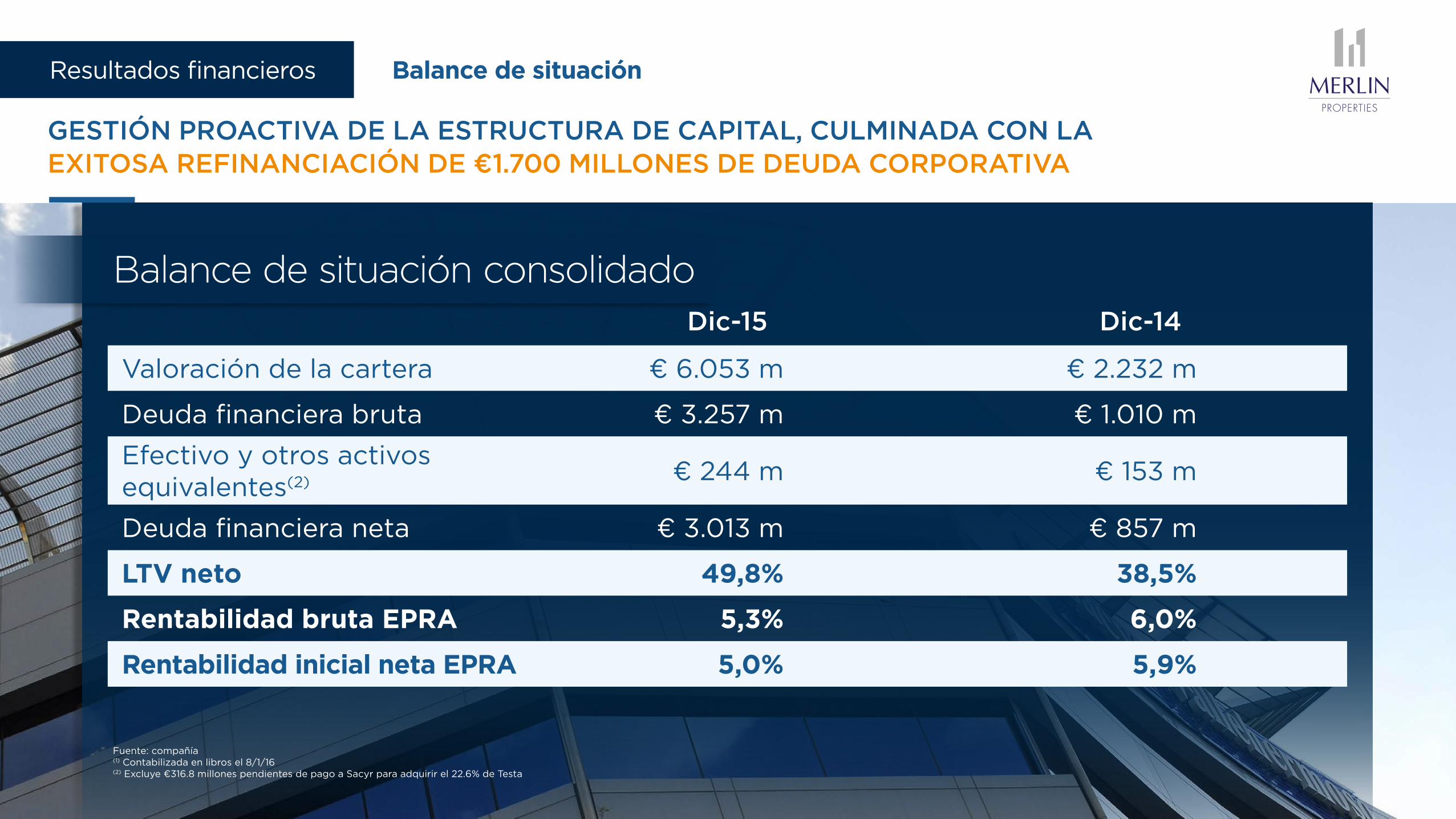

GESTIÓN PROACTIVA DE LA ESTRUCTURA DE CAPITAL, CULMINADA CON LA EXITOSA REFINANCIACIÓN DE €1.700 MILLONES DE DEUDA CORPORATIVA

Dic-15 Dic-14

Valoración de la cartera € 6.053 m € 2.232 m

Deuda financiera bruta € 3.257 m € 1.010 m

Efectivo y otros activos equivalentes(2) € 244 m € 153 m

Deuda financiera neta € 3.013 m € 857 m

LTV neto 49,8% 38,5%

Rentabilidad bruta EPRA 5,3% 6,0%

Rentabilidad inicial neta EPRA 5,0% 5,9%

Fuente: compañía(1) Contabilizada en libros el 8/1/16(2) Excluye €316.8 millones pendientes de pago a Sacyr para adquirir el 22.6% de Testa

Balance de situación consolidado

Balance de situaciónResultados financieros

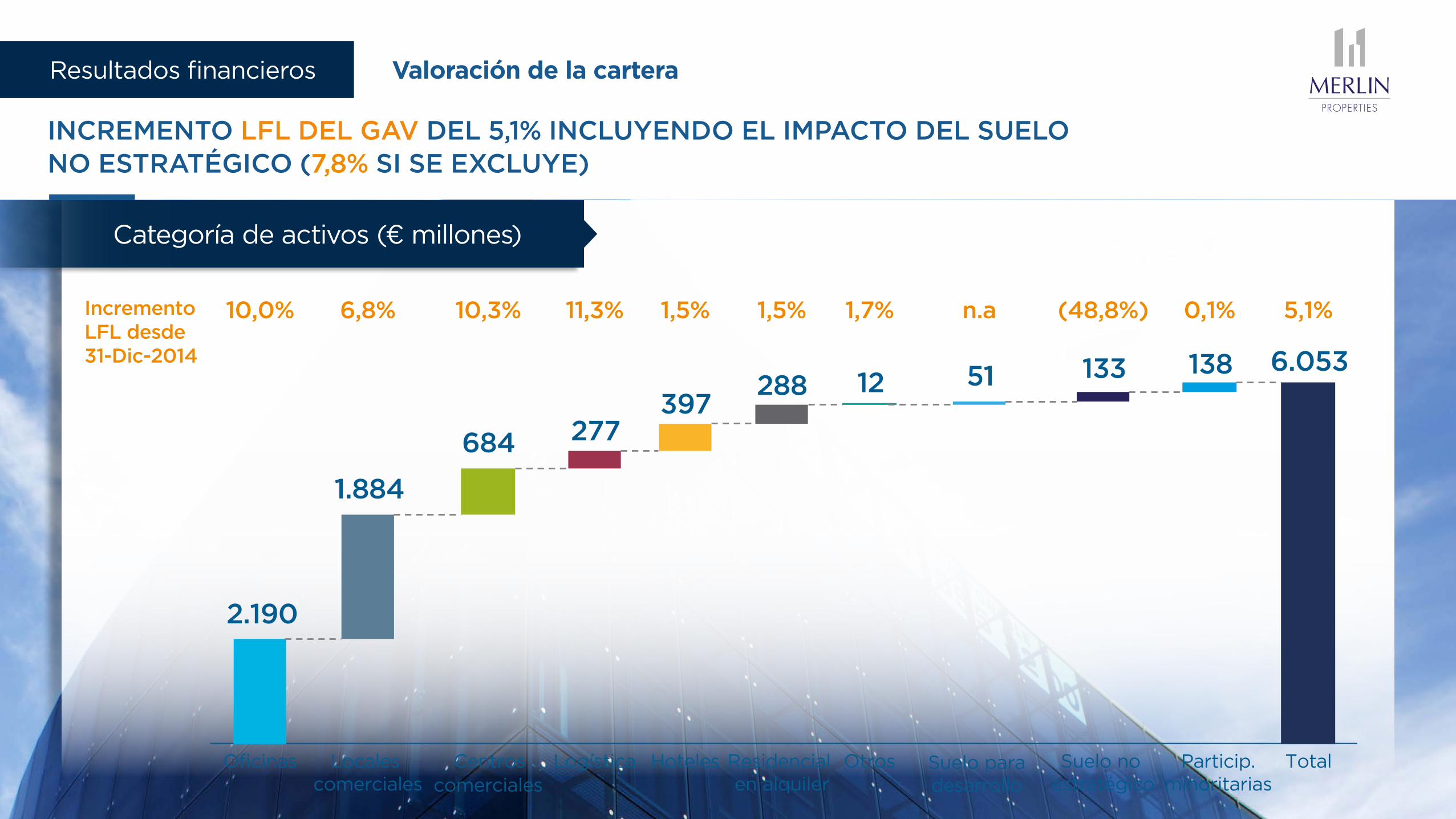

INCREMENTO LFL DEL GAV DEL 5,1% INCLUYENDO EL IMPACTO DEL SUELO NO ESTRATÉGICO (7,8% SI SE EXCLUYE)

Incremento LFL desde 31-Dic-2014

10,0%

2.190

Oficinas

6,8%

1.884

10,3%

684

Centroscomerciales

11,3%

277

Logística

1,5%

397

Hoteles

1,7%

12

Otros

n.a

51

1,5%

288

0,1%

138

Particip. minoritarias

5,1%

6.053

Total

(48,8%)

133

Suelo no estratégico

Locales comerciales

Residencial en alquiler

Suelo para desarrollo

Categoría de activos (€ millones)

Valoración de la carteraResultados financieros

Fuente: compañía

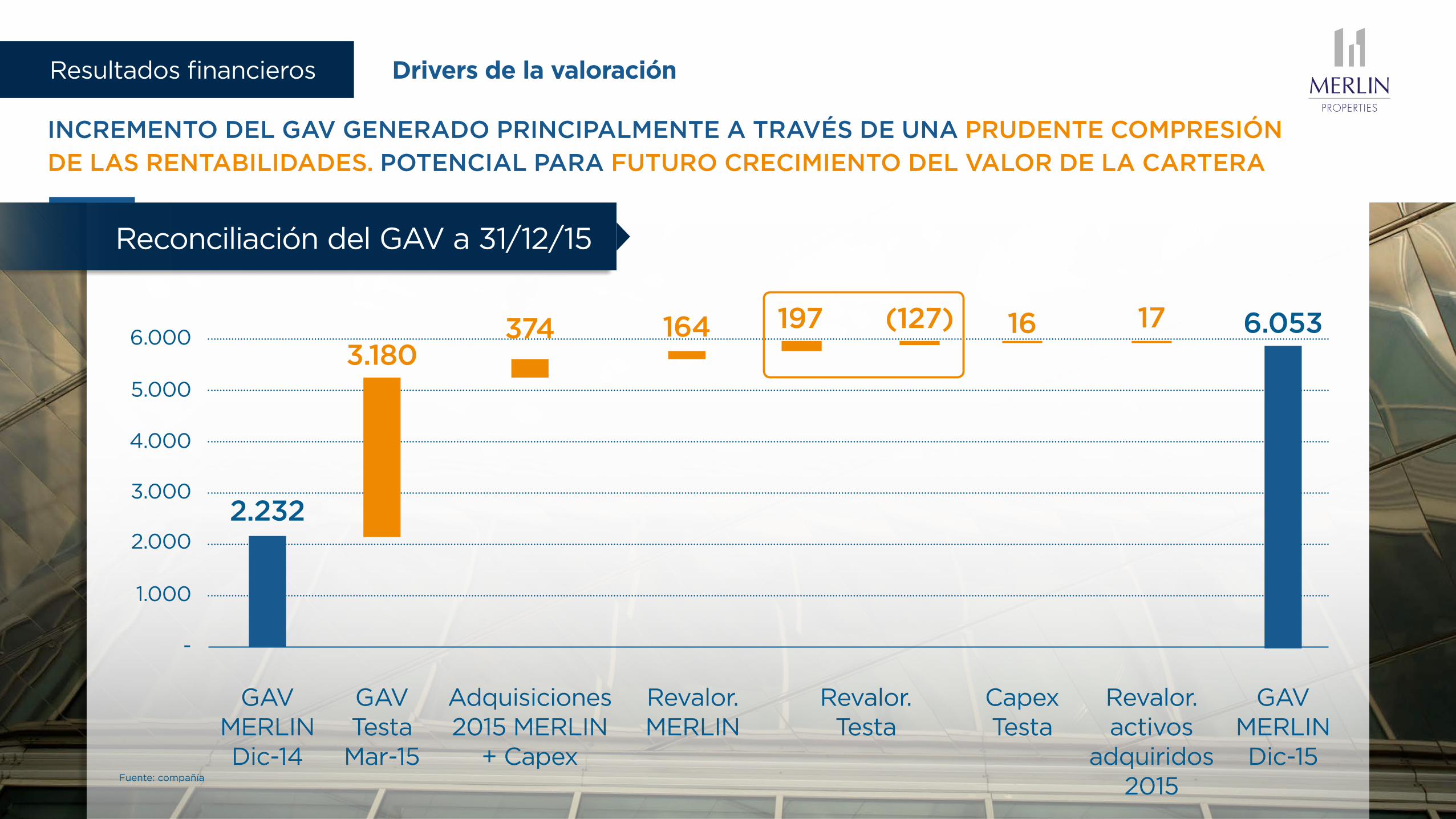

INCREMENTO DEL GAV GENERADO PRINCIPALMENTE A TRAVÉS DE UNA PRUDENTE COMPRESIÓN

DE LAS RENTABILIDADES. POTENCIAL PARA FUTURO CRECIMIENTO DEL VALOR DE LA CARTERA

-

1.000

2.000

3.000

4.000

5.000

6.000

GAV MERLIN Dic-14

2.232

GAV MERLIN Dic-15

6.053

Revalor. MERLIN

164

Revalor. activos

adquiridos 2015

17

Capex Testa

16

Adquisiciones 2015 MERLIN

+ Capex

374

GAV Testa Mar-15

3.180

Revalor. Testa

197 (127)

Reconciliación del GAV a 31/12/15

Drivers de la valoraciónResultados financieros

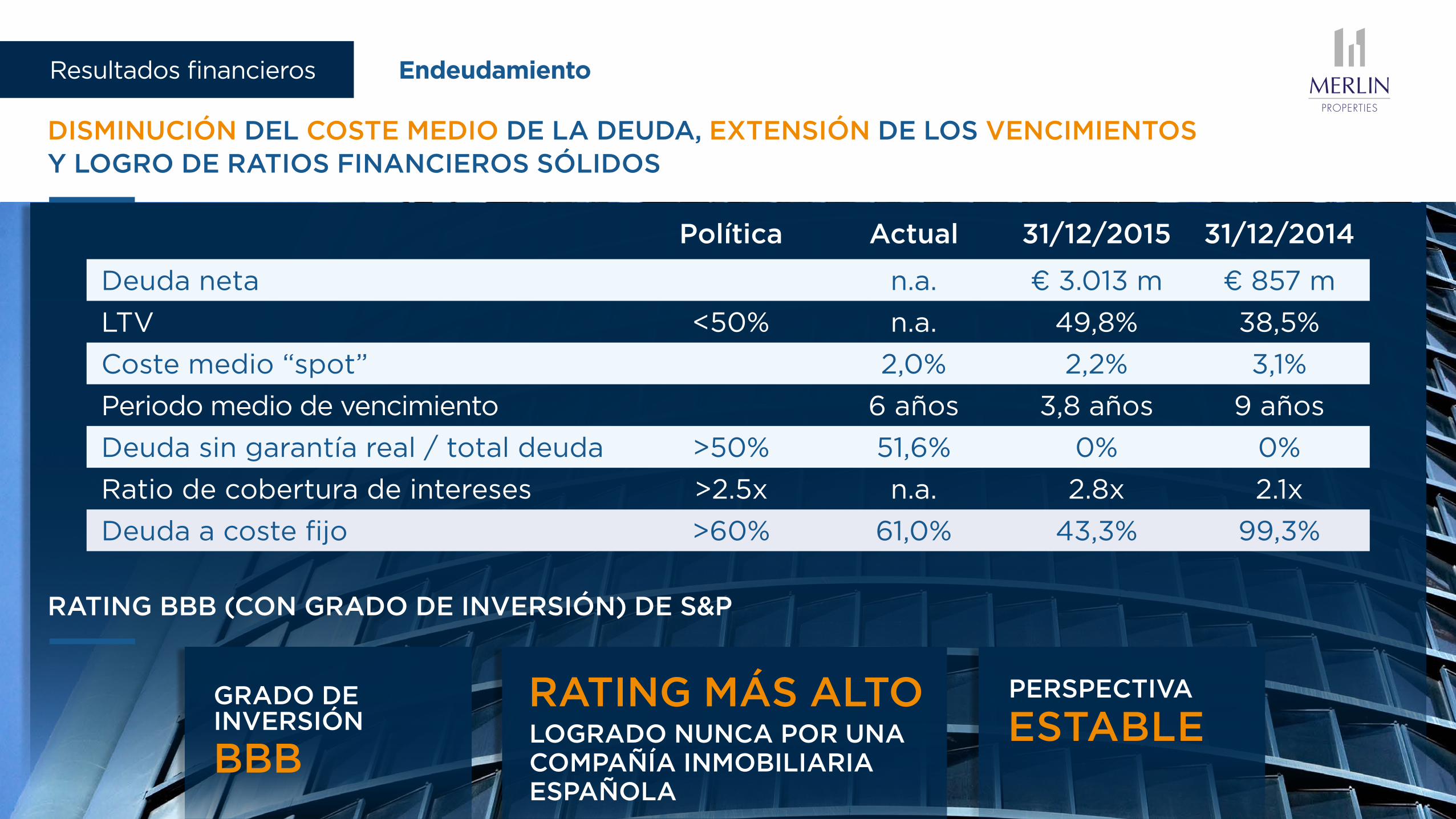

EndeudamientoResultados financieros

DISMINUCIÓN DEL COSTE MEDIO DE LA DEUDA, EXTENSIÓN DE LOS VENCIMIENTOS Y LOGRO DE RATIOS FINANCIEROS SÓLIDOS

Política Actual 31/12/2015 31/12/2014

Deuda neta n.a. € 3.013 m € 857 m

LTV <50% n.a. 49,8% 38,5%

Coste medio “spot” 2,0% 2,2% 3,1%

Periodo medio de vencimiento 6 años 3,8 años 9 años

Deuda sin garantía real / total deuda >50% 51,6% 0% 0%

Ratio de cobertura de intereses >2.5x n.a. 2.8x 2.1x

Deuda a coste fijo >60% 61,0% 43,3% 99,3%

GRADO DE INVERSIÓN

BBBLOGRADO NUNCA POR UNA COMPAÑÍA INMOBILIARIA ESPAÑOLA

RATING MÁS ALTO PERSPECTIVA

ESTABLE

RATING BBB (CON GRADO DE INVERSIÓN) DE S&P

(Total)

(céntimos de € por

acción)€ 7,75

€ 25m € 1.8m € 33m € 60m

Dividendo a cuenta

28 Octubre 2015 27 Abril 2016

€ 0,569

Dividendo complementario

€ 10,261

Distribución de prima de emisión

€ 18,58

Total

SE CUMPLE CON LA INDICACIÓN DADA AL MERCADO

Propuesta de distribución al accionista con cargo a 2015Resultados financieros

CARTERA DE ACTIVOS DIVERSIFICADA CON ALTA RENTABILIDAD, ABSORCIÓN POSITIVA

RENDIMIENTO DE LA CARTERA

1 ı 2 ı 3Puntos orden del día

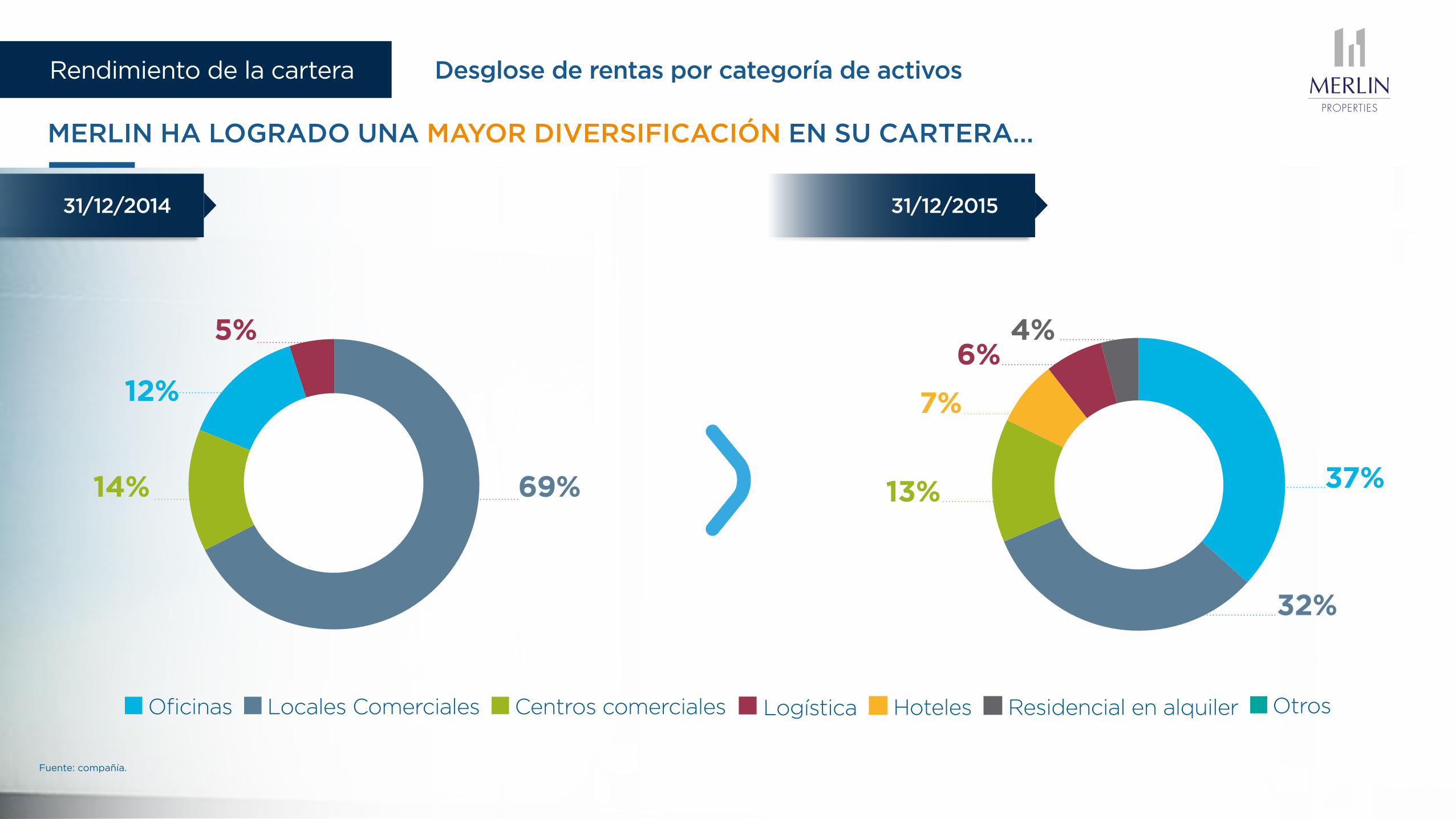

MERLIN HA LOGRADO UNA MAYOR DIVERSIFICACIÓN EN SU CARTERA…

Fuente: compañía.

Oficinas Locales Comerciales Centros comerciales Logística Hoteles Residencial en alquiler Otros

Logistics

O�ce

Shopping Centers

High Street Retail

12%

14%

5%

69%

31/12/2014 31/12/2015

13%

7%

Other

Rented residential

Hotels

High Street Retail

Logistics

Shopping centers

O�ce32%

6%

37%

4%

Desglose de rentas por categoría de activosRendimiento de la cartera

Fuente: compañía. (1) Las rentas brutas están calculadas dividiendo la renta bruta pasante de diciembre multiplicada por 12 entre GAV

… MANTENIENDO UNA ALTA RENTABILIDAD…

5,1%

Oficinas

5,1%

Locales comerciales

5,9%

Centros comerciales

6,9%

Logística

5,6%

Hoteles

4,2%

Residencial en alquiler

7,4%

Otros1

5,3%MEDIA MERLIN

Rentabilidad bruta por categoría de activo según EPRARendimiento de la cartera

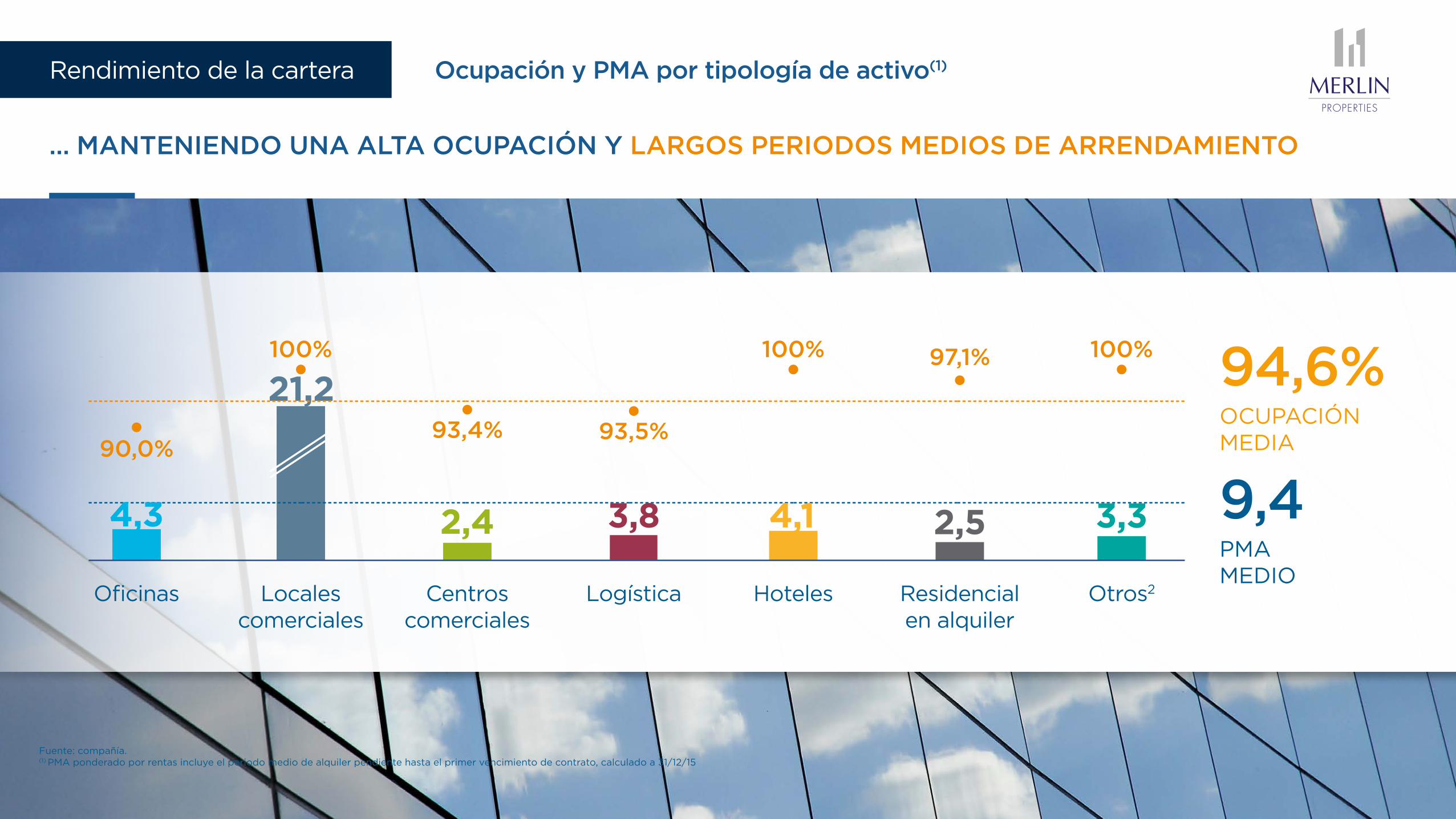

Fuente: compañía. (1) PMA ponderado por rentas incluye el periodo medio de alquiler pendiente hasta el primer vencimiento de contrato, calculado a 31/12/15

… MANTENIENDO UNA ALTA OCUPACIÓN Y LARGOS PERIODOS MEDIOS DE ARRENDAMIENTO

2,4

21,2

Oficinas Locales comerciales

Centros comerciales

Logística Hoteles Residencial en alquiler

Otros2

94,6%OCUPACIÓN MEDIA

9,4PMA MEDIO

90,0%93,5%93,4%

100% 100% 100%97,1%

4,3 3,8 4,1 2,5 3,3

Ocupación y PMA por tipología de activo(1)Rendimiento de la cartera

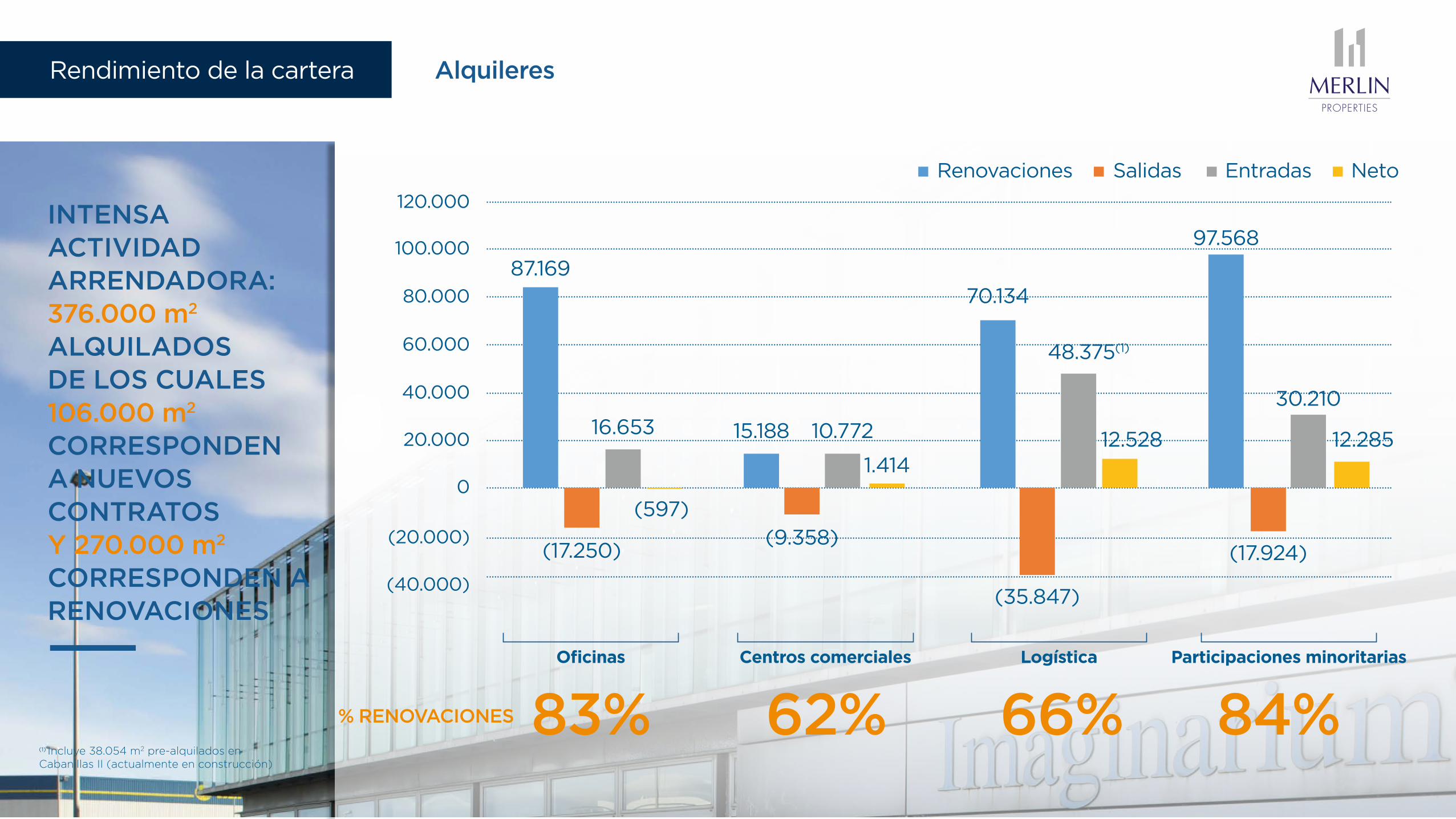

Alquileres

INTENSA ACTIVIDAD ARRENDADORA: 376.000 m2 ALQUILADOS DE LOS CUALES 106.000 m2 CORRESPONDEN A NUEVOS CONTRATOS Y 270.000 m2 CORRESPONDEN A RENOVACIONES

Rendimiento de la cartera

(1) Incluye 38.054 m2 pre-alquilados en Cabanillas II (actualmente en construcción)

% RENOVACIONES 83% 62% 66% 84%

SalidasRenovaciones Entradas Neto

120.000

100.000

80.000

60.000

40.000

20.000

0

(20.000)

(40.000)

(597)

87.169

16.653

(17.250)

Oficinas

70.134

48.375(1)

12.528

(35.847)

Logística

97.568

(17.924)

30.210

12.285

Participaciones minoritarias

15.188 10.772

1.414

(9.358)

Centros comerciales

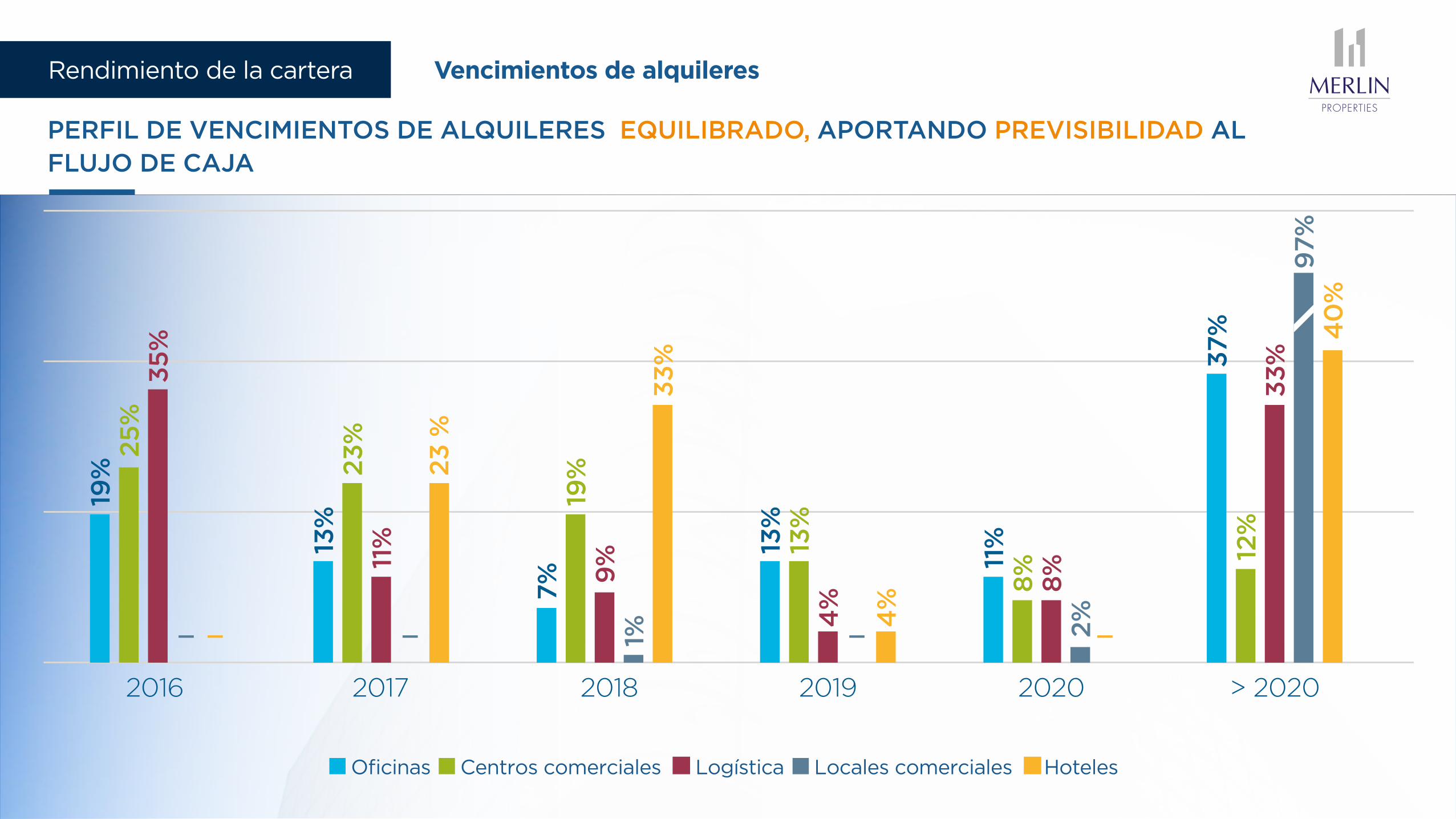

Vencimientos de alquileresRendimiento de la cartera

PERFIL DE VENCIMIENTOS DE ALQUILERES EQUILIBRADO, APORTANDO PREVISIBILIDAD AL FLUJO DE CAJA

2016 2017

19%

35

%

2018 2019 2020 > 2020

Office High Street retail Shopping centers Logistics Hotels

25

%

13%

11%

23 %

23%

7% 9

%1%

33%

19%

13%

4%

4%

13%

11%

8%

8%

2%

37%

33%

97%

40

%

12%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

2016 2017

55% 47% 30% 68%

24%

4%

4%

65%

17%

8%

10%

63%

37%

24%

0%

4%

66%

6%

30%7%29%

7%

17%

27%

18%

2018 2019 2020 2021 > 2021

Office High Street retail Shopping centers Logistics Hotels

3%

30%

2016 2017

19%

35

%

2018 2019 2020 > 2020

Oficinas Locales comerciales Centros comerciales Logística Hoteles

25

%

13%

11%

23 %

23%

7% 9

%1%

33%

19%

13%

4%

4%

13%

11%

8%

8%

2%

37%

33%

97%

40

%

12%

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

2016 2017

55% 47% 30% 68%

24%

4%

4%

65%

17%

8%

10%

63%

37%

24%

0%

4%

66%

6%

30%7%29%

7%

17%

27%

18%

2018 2019 2020 2021 > 2021

Office High Street retail Shopping centers Logistics Hotels

3%

30%

COMPOSICIÓN DEL CONSEJO DE ADMINISTRACIÓN

4Punto orden del día

Formado por 10 miembros comprometidos de reconocido prestigioComposición del consejo

70% DE LOS MIEMBROS DEL CONSEJO SON INDEPENDIENTES / COMITÉS DELEGADOS CON 100% DE SUS MIEMBROS INDEPENDIENTES

Secretaria Dña. Mónica Martín de Vidales Vicesecretario D. Ildefonso Polo del Mármol

Comisión de Auditoría y Control Comisión de Nombramientos y Retribución Consejeros independientes

Sujeto a reelección

Sujeto a ratificación

Presidente Ejecutivo D. Ismael Clemente

Consejero Ejecutivo D. Miguel Ollero

Consejero Dominical D. Hammad Khan

Consejero Independiente Dña. Ana de Pro

Consejera Independiente Dña. María Luisa Jordá

Consejera Independiente Dña. Ana García Fau

Consejero Independiente D. Alfredo Fernández

Consejero Independiente D. Fernando Ortiz

Consejero Independiente D. Donald Johnston

Consejero Independiente D. John Gómez Hall

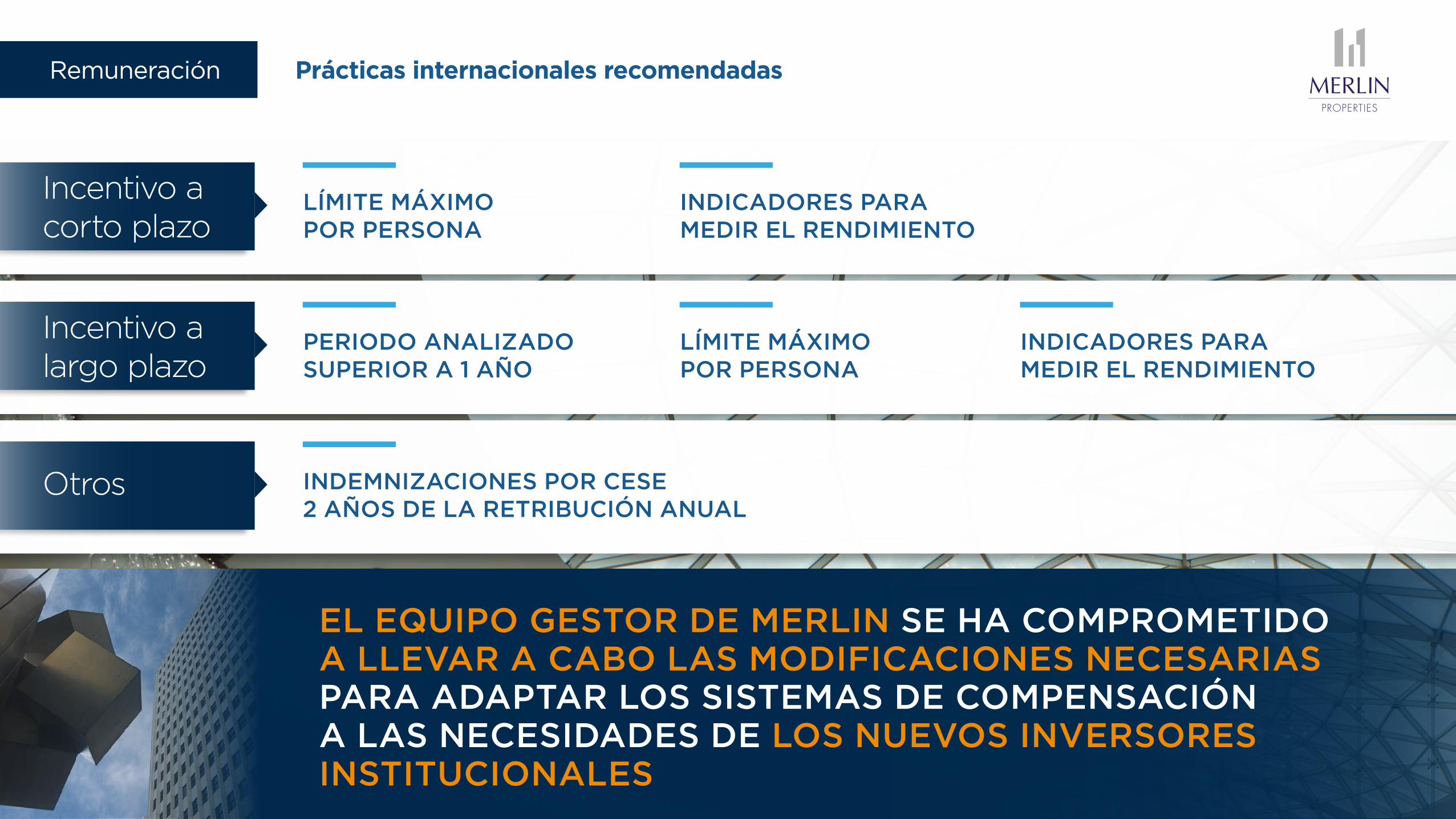

REMUNERACIÓN

5 ı 6 ı 7 ı 8Puntos orden del día

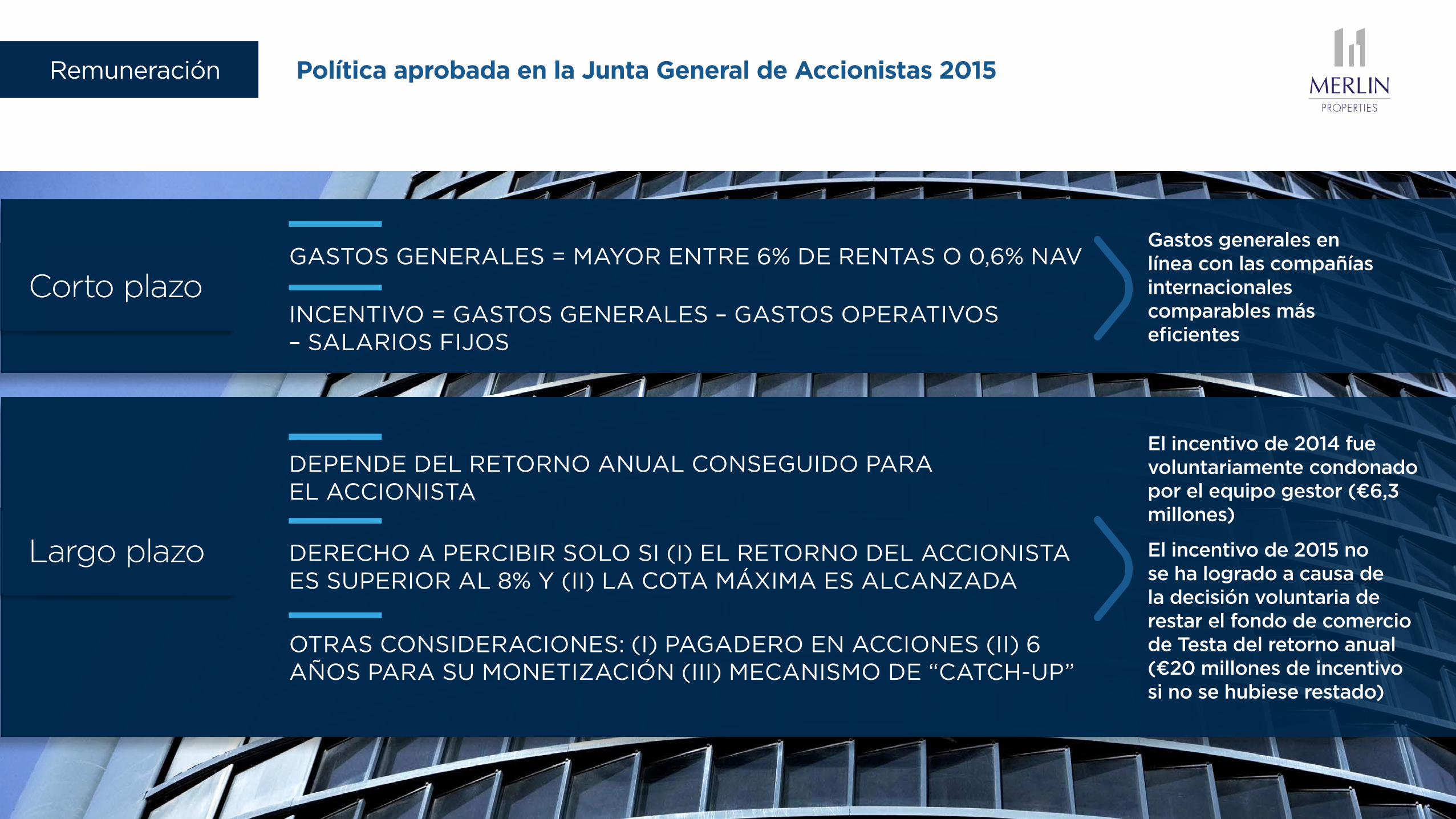

Política aprobada en la Junta General de Accionistas 2015Remuneración

GASTOS GENERALES = MAYOR ENTRE 6% DE RENTAS O 0,6% NAV

INCENTIVO = GASTOS GENERALES – GASTOS OPERATIVOS – SALARIOS FIJOS

Corto plazo

DEPENDE DEL RETORNO ANUAL CONSEGUIDO PARA EL ACCIONISTA

DERECHO A PERCIBIR SOLO SI (I) EL RETORNO DEL ACCIONISTA ES SUPERIOR AL 8% Y (II) LA COTA MÁXIMA ES ALCANZADA

OTRAS CONSIDERACIONES: (I) PAGADERO EN ACCIONES (II) 6 AÑOS PARA SU MONETIZACIÓN (III) MECANISMO DE “CATCH-UP”

Largo plazo

Gastos generales en línea con las compañías internacionales comparables más eficientes

El incentivo de 2014 fue voluntariamente condonado por el equipo gestor (€6,3 millones)

El incentivo de 2015 no se ha logrado a causa de la decisión voluntaria de restar el fondo de comercio de Testa del retorno anual (€20 millones de incentivo si no se hubiese restado)

Remuneración

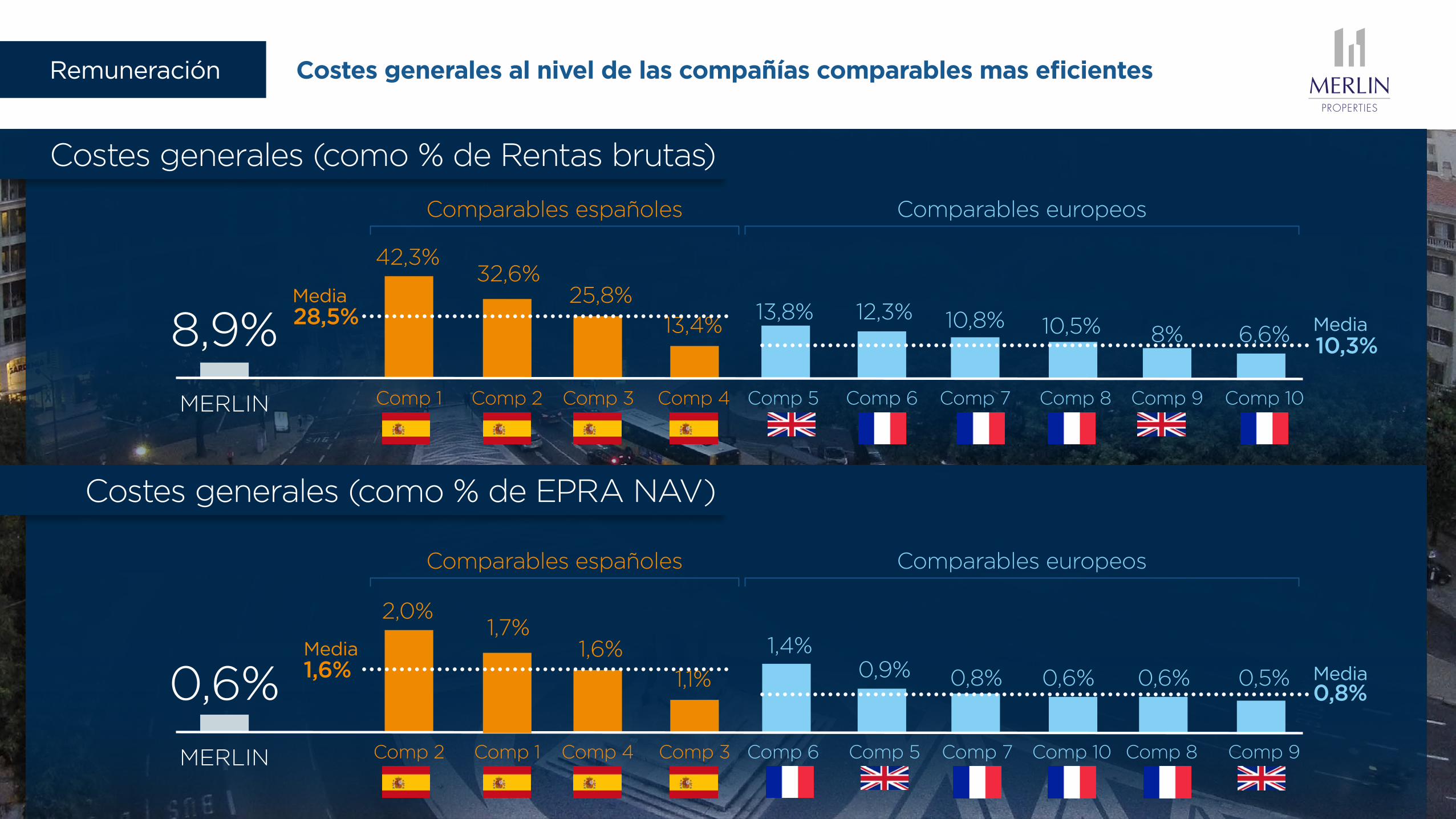

Costes generales (como % de Rentas brutas)

Costes generales (como % de EPRA NAV)

Comparables españoles Comparables europeos

Comparables españoles Comparables europeos

Costes generales al nivel de las compañías comparables mas eficientes

Comp 1 Comp 2 Comp 3 Comp 4 Comp 5

Comp 6 Comp 5 Comp 7 Comp 10 Comp 8 Comp 9

Comp 6 Comp 7 Comp 8 Comp 9 Comp 10

6,6%8%10,5%10,8%12,3%13,4%

25,8%32,6%

42,3%

8,9%MERLIN

28,5%10,3%

13,8%

Comp 2 Comp 4 Comp 3

0,5%0,6%0,6%0,8%0,9%1,4%

1,1%1,6%

Comp 1

1,7%2,0%

0,6%MERLIN

1,6%0,8%

Media

Media

Media

Media

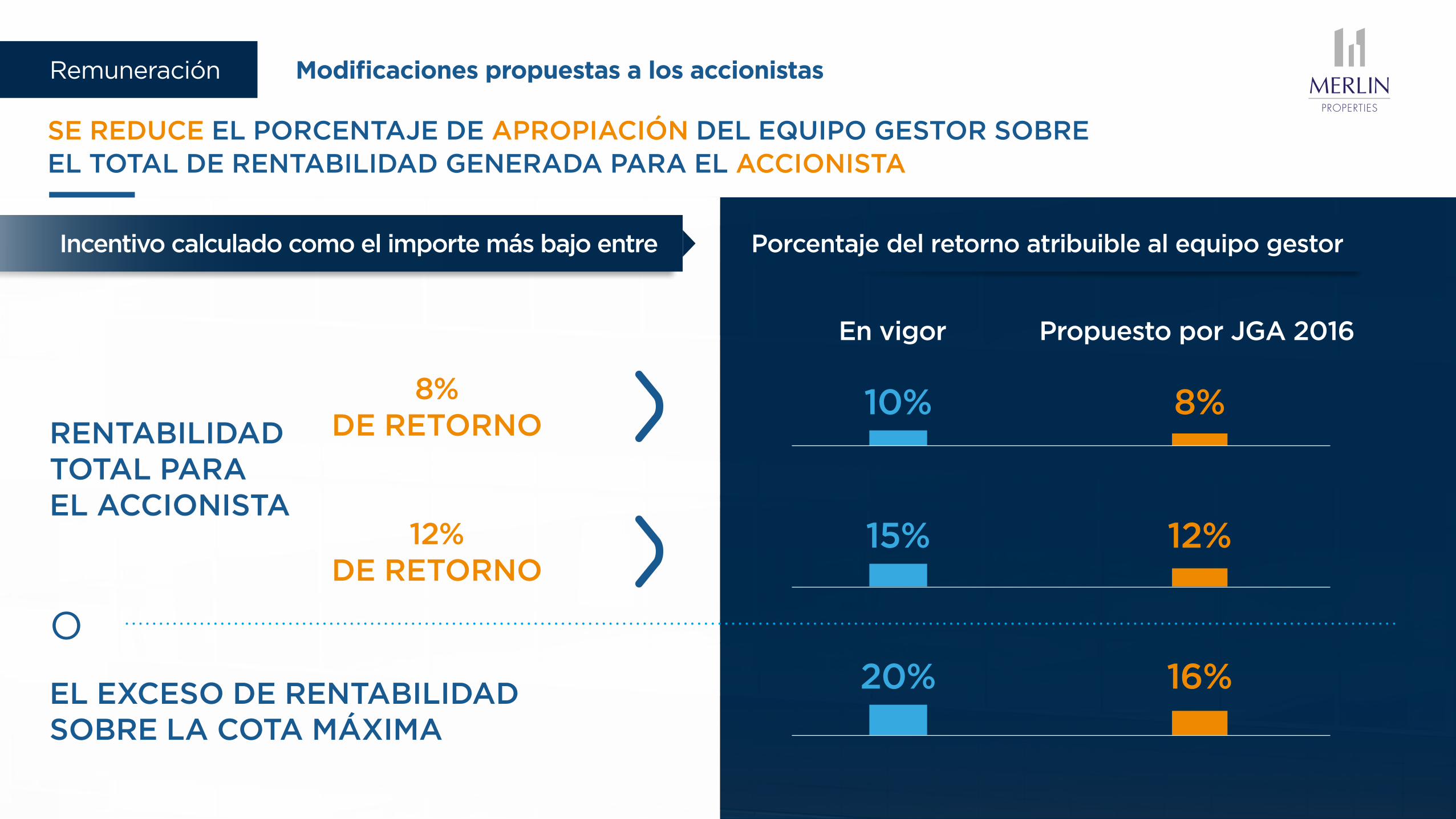

10% 8%

15% 12%

20% 16%

En vigor Propuesto por JGA 2016

O

RENTABILIDAD TOTAL PARA EL ACCIONISTA

8% DE RETORNO

12% DE RETORNO

EL EXCESO DE RENTABILIDAD SOBRE LA COTA MÁXIMA

Incentivo calculado como el importe más bajo entre Porcentaje del retorno atribuible al equipo gestor

SE REDUCE EL PORCENTAJE DE APROPIACIÓN DEL EQUIPO GESTOR SOBRE EL TOTAL DE RENTABILIDAD GENERADA PARA EL ACCIONISTA

Modificaciones propuestas a los accionistasRemuneración

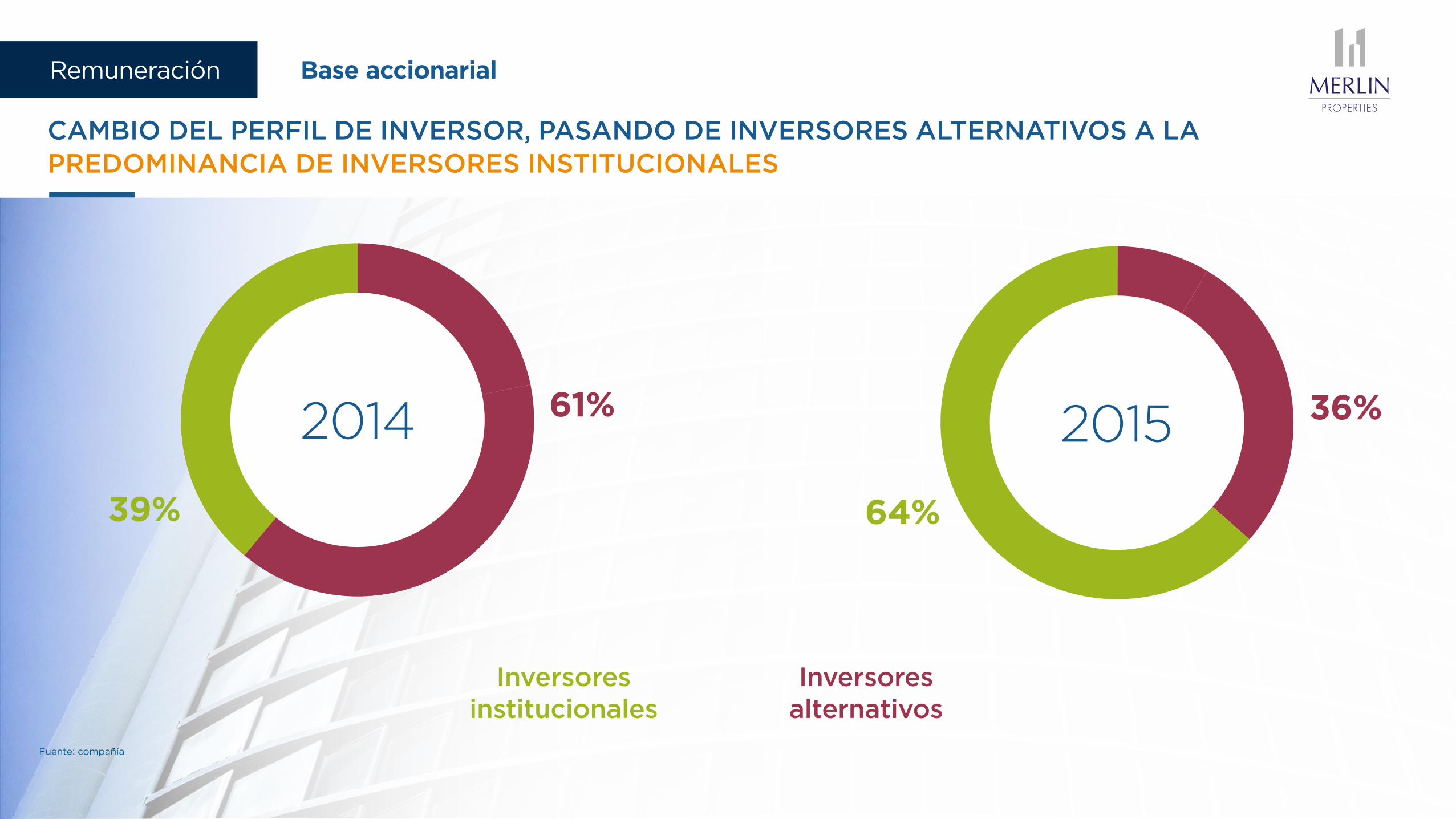

Inversores institucionales

Inversores alternativos

39%

61%2014

64%

36%2015

CAMBIO DEL PERFIL DE INVERSOR, PASANDO DE INVERSORES ALTERNATIVOS A LA PREDOMINANCIA DE INVERSORES INSTITUCIONALES

Fuente: compañía

Base accionarialRemuneración

Prácticas internacionales recomendadas

LÍMITE MÁXIMO POR PERSONA

INDICADORES PARA MEDIR EL RENDIMIENTO

Incentivo a corto plazo

LÍMITE MÁXIMO POR PERSONA

INDICADORES PARA MEDIR EL RENDIMIENTO

PERIODO ANALIZADO SUPERIOR A 1 AÑO

Incentivo a largo plazo

INDEMNIZACIONES POR CESE 2 AÑOS DE LA RETRIBUCIÓN ANUAL

Otros

EL EQUIPO GESTOR DE MERLIN SE HA COMPROMETIDO A LLEVAR A CABO LAS MODIFICACIONES NECESARIAS PARA ADAPTAR LOS SISTEMAS DE COMPENSACIÓN A LAS NECESIDADES DE LOS NUEVOS INVERSORES INSTITUCIONALES

Remuneración

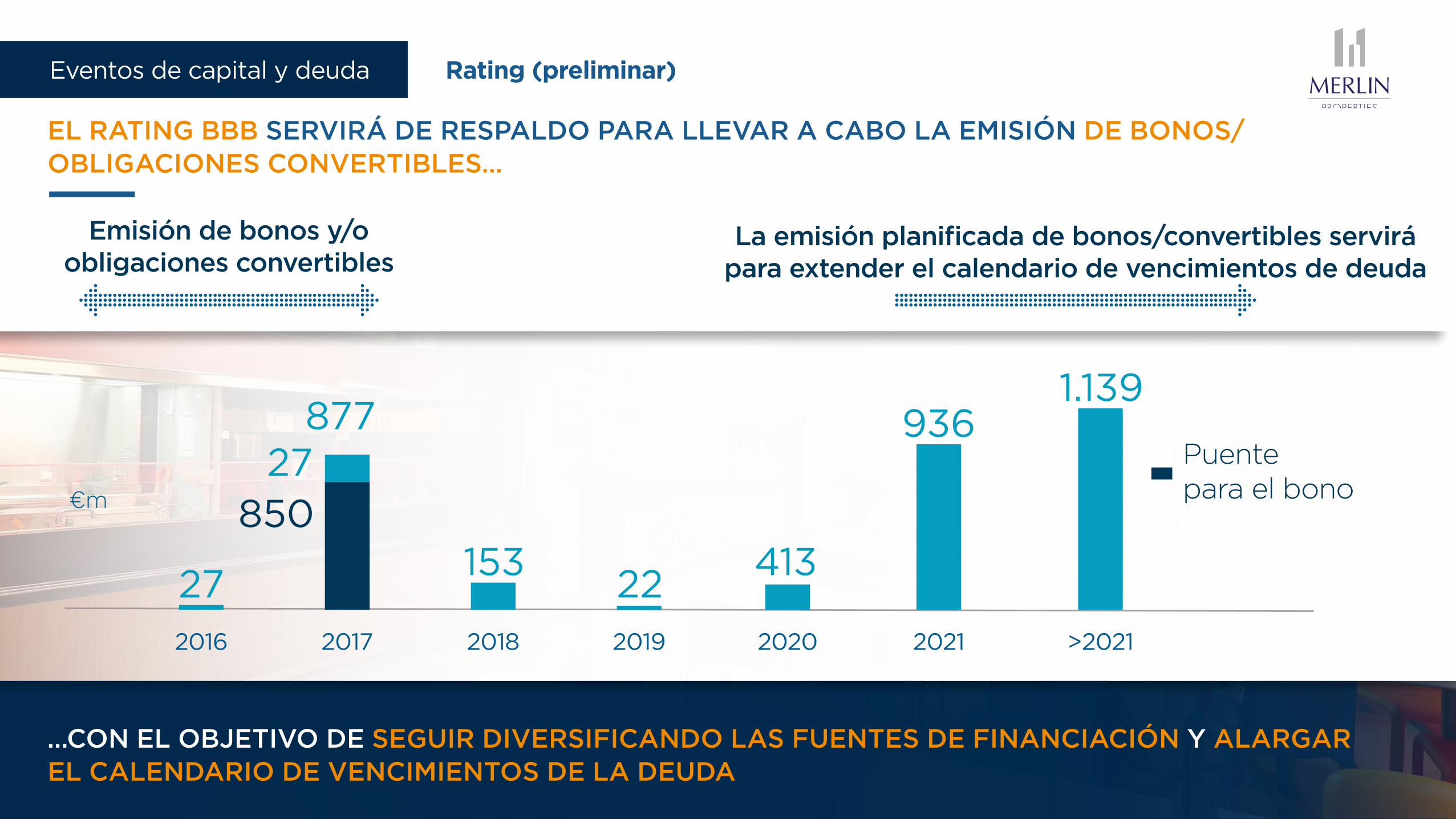

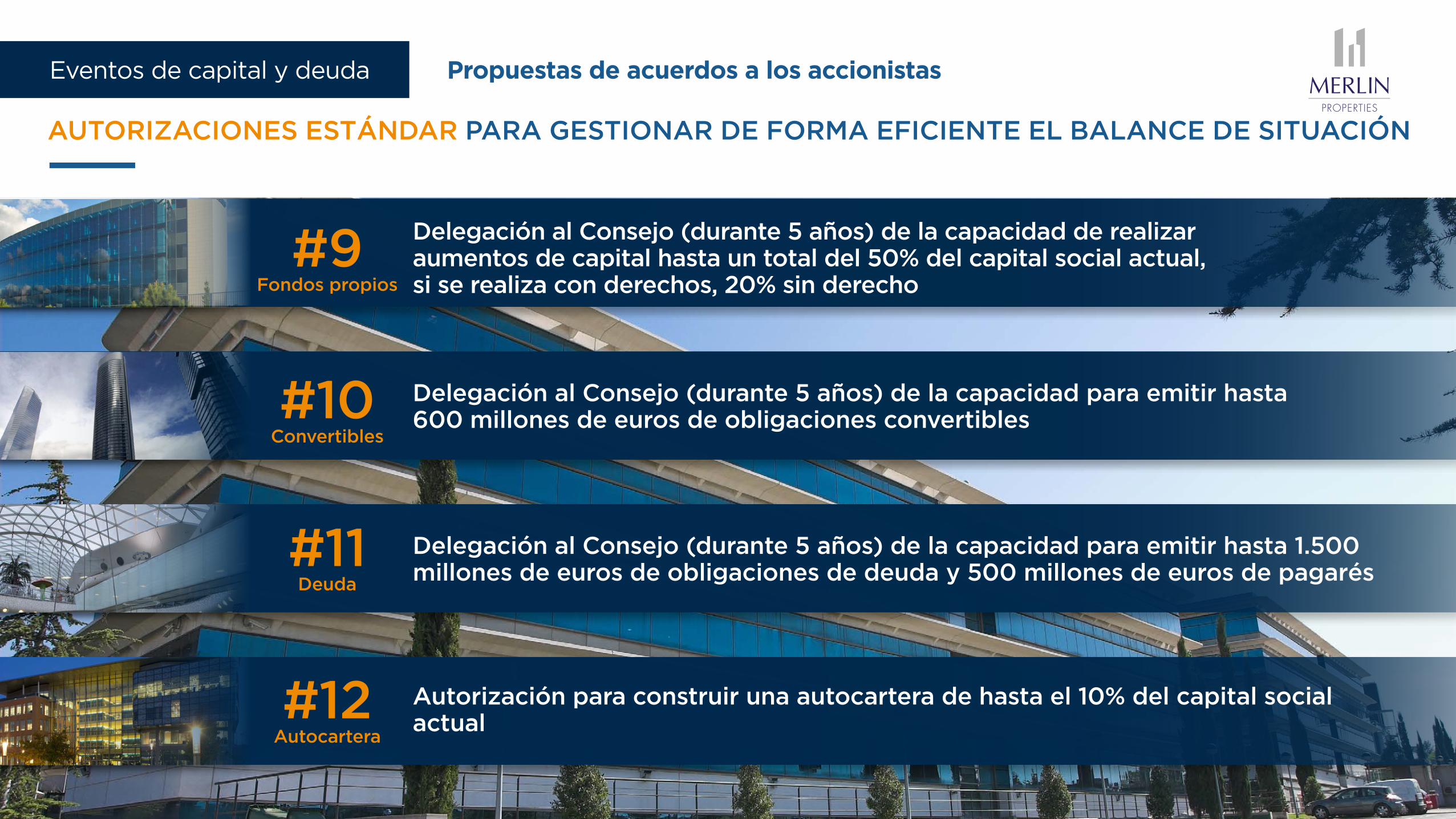

EVENTOS DE CAPITAL Y DEUDADELEGACIÓN EN EL CONSEJO DE ADMINISTRACIÓN

9 ı 10 ı 11 ı 12Puntos orden del día

Puente para el bono€m

27153

22413

9361.139

850

87727

2016 2017 2018 2019 2020 2021 >2021

Emisión de bonos y/o obligaciones convertibles

La emisión planificada de bonos/convertibles servirá para extender el calendario de vencimientos de deuda

…CON EL OBJETIVO DE SEGUIR DIVERSIFICANDO LAS FUENTES DE FINANCIACIÓN Y ALARGAR EL CALENDARIO DE VENCIMIENTOS DE LA DEUDA

EL RATING BBB SERVIRÁ DE RESPALDO PARA LLEVAR A CABO LA EMISIÓN DE BONOS/OBLIGACIONES CONVERTIBLES…

Rating (preliminar)Eventos de capital y deuda

Propuestas de acuerdos a los accionistasEventos de capital y deuda

AUTORIZACIONES ESTÁNDAR PARA GESTIONAR DE FORMA EFICIENTE EL BALANCE DE SITUACIÓN

#9 Fondos propios

Delegación al Consejo (durante 5 años) de la capacidad de realizar aumentos de capital hasta un total del 50% del capital social actual, si se realiza con derechos, 20% sin derecho

Delegación al Consejo (durante 5 años) de la capacidad para emitir hasta 600 millones de euros de obligaciones convertibles#10

Convertibles

Delegación al Consejo (durante 5 años) de la capacidad para emitir hasta 1.500 millones de euros de obligaciones de deuda y 500 millones de euros de pagarés

#11 Deuda

Autorización para construir una autocartera de hasta el 10% del capital social actual#12

Autocartera

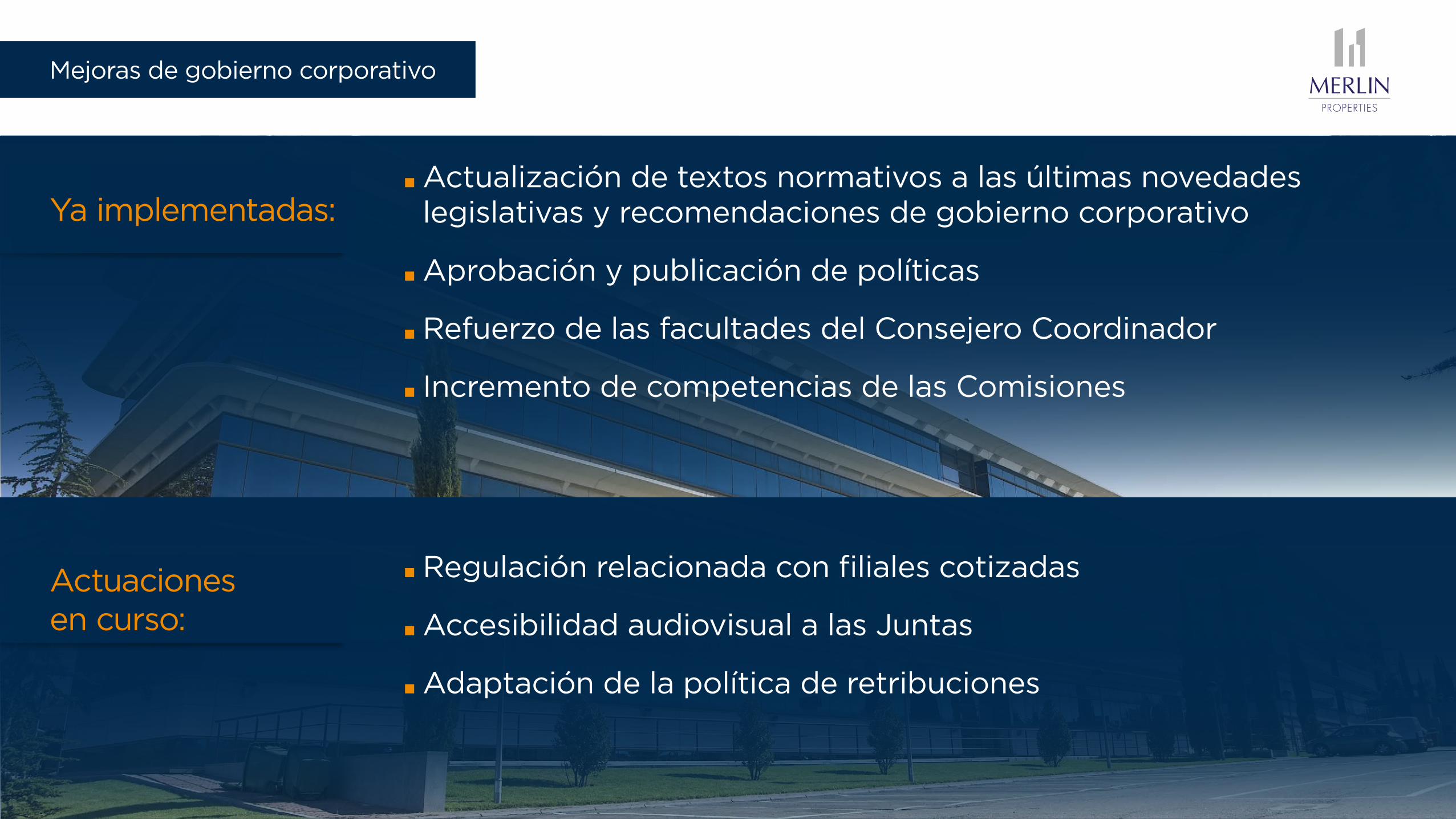

MEJORAS DE GOBIERNO CORPORATIVO

Mejoras de gobierno corporativo

Actualización de textos normativos a las últimas novedades legislativas y recomendaciones de gobierno corporativo

Aprobación y publicación de políticas

Refuerzo de las facultades del Consejero Coordinador

Incremento de competencias de las Comisiones

Regulación relacionada con filiales cotizadas

Accesibilidad audiovisual a las Juntas

Adaptación de la política de retribuciones

Ya implementadas:

Actuaciones en curso:

PROPUESTA DE DIVIDENDOS ATRACTIVA

PERSPECTIVAS PARA EL 2016

INCIPIENTE RECUPERACIÓN DE RENTAS EN OFICINAS, LOGÍSTICA Y CENTROS COMERCIALES

PROGRAMA DE COMPRAS CENTRADO EN ACTIVOS LOGÍSTICOS Y OFICINAS EN LISBOA

COMPRESIÓN DE RENTABILIDADES EN LÍNEA CON OTROS MERCADOS EUROPEOS. SE ESPERA CIERTA COMPRESIÓN ADICIONAL, ESPECIALMENTE EN ACTIVOS LOGÍSTICOS

ESCASA INCORPORACIÓN DE NUEVA OFERTA AL MERCADO

DESCONSOLIDACIÓN DE RESIDENCIAL EN ALQUILER

PROGRAMA LEED/BREAAM

MENOR ACTIVIDAD INVERSORA TRAS UN AÑO RÉCORD

DESARROLLOS: DOS PROYECTOS LOGÍSTICO “LLAVE EN MANO” Y UN EDIFICIO DE OFICINAS AAA

PROGRAMA PARA REFINANCIAR EL PRÉSTAMO PUENTE DE 850 MILLONES DE EUROS CON UNA EMISIÓN DE BONOS

MERLIN

Mercado

Perspectivas 2016

EN EFECTIVO DIVIDIDO EN DOS PAGOS

€ 0,19€ 0,43+

Dividendo a cuenta1

Septiembre de 2016

2017

Dividendo complementario

(tras la aprobación de Cuentas 2016 por la JGA)

Total Dividendo mínimo

propuesto para el ejercicio 2016

PREVISIÓN DE REMUNERACIÓN AL ACCIONISTA CON CARGO A LOS RESULTADOS DE 2016: MÍNIMO DE 140 MILLONES DE EUROS (+0,43 EUROS POR ACCIÓN) CON LAS SIGUIENTES CARACTERÍSTICAS:

Perspectivas 2016 Previsión de remuneración al accionista 2016

€ 0,24+

JUNTA GENERALACCIONISTAS 2016

Madrid, 6 de abril de 2016