119

Just Group plc Just Retirement Limited Partnership Life Assurance Company Limited Solvency and Financial Condition Report as at 31 December 2016

Just Group plc

Just Retirement Limited

Partnership Life Assurance Company Limited

Solvency and Financial Condition Report

as at 31 December 2016

Just Group plc

Solvency and Financial Condition Report as at 31 December 2016

Contents

Summary 1

A. Business and Performance 5 A.1 Business 5 A.2 Underwriting Performance 14 A.3 Investment Performance 16 A.4 Performance of other activities 17

B. System of Governance 19 B.1 General information on the system of governance 19 B.2 Fit and proper requirements 28 B.3 Risk management system including the own risk and solvency assessment 31 B.4 Internal control system 35 B.5 Internal audit function 37 B.6 Actuarial function 38 B.7 Outsourcing 39 B.8 Any other information 39

C. Risk Profile 41 C.1 Underwriting risk 43 C.2 Market risk 44 C.3 Credit risk 46 C.4 Liquidity risk 48 C.5 Operational risk 49 C.6 Other material risks 52 C.7 Any other information 52

D. Valuation for Solvency Purposes 55 D.1 Assets 57 D.2 Technical provisions 60 D.3 Other liabilities 65 D.4 Alternative methods for valuation 67 D.5 Reconciliations to IFRS statutory accounts 69

E. Capital Management 72 E.1 Own funds 72 E.2 Solvency Capital Requirement and Minimum Capital Requirement 76 E.3 Internal model 78 E.4 Differences between the standard formula and any internal model used 78 E.5 Non-compliance with the MCR and non-compliance with the SCR 81

F. Other information F.1 Quantitative Reporting Templates (QRTs) 82 F.2 Directors’ statement 109 F.3 Approvals, determinations and modifications 110 F.3 Audit opinion 111 F.4 Glossary 116

1

Summary

Introduction

This is the first Solvency and Financial Condition Report (SFCR) for Just Group plc (formerly JRP Group

plc and Just Retirement Group plc and referred to as “Just Group”) and covers the period to 31

December 2016.

Just Retirement Limited (JRL) and Partnership Life Assurance Company Limited (PLACL), the UK

regulated insurers within the Group, received approval to prepare a single group-wide SFCR.

Consequently this report also contains the SFCR disclosures for JRL and PLACL.

The purpose of the SFCR report is to provide information required by the Solvency II regulatory

framework, and in particular the capital positions of the regulated entities and the Just Group as a

whole. The Solvency II Delegated Act states that no comparatives are required in the first report,

and hence only the current results and financial position are given.

The Group saw significant change during 2016 as a result of the acquisition by Just Retirement

Group (JRG) of Partnership Assurance Group plc (PAG), which was effective from 1 April 2016. The

Group’s holding company changed its name from JRP Group plc to Just Group plc on 18 May 2017.

A. Business and Performance

The Just Group is now the leading specialist provider of retirement income products and services to

both individuals and corporates, and a major provider of lifetime mortgages (LTM). 2016 was a year

that demonstrated Just’s products are well placed in attractive growth markets. Momentum has

been maintained in both the defined benefit (DB) de-risking and LTM markets, and we have seen a

promising return of demand for individual Guaranteed Income for Life (GIfL) solutions.

Just focusses on growing operating profits rather than sales volume, which has resulted in our new

business operating profit increasing to £124m and adjusted operating profit to £164m in the 12

months to 31 December 2016. The operating profit measure is used to assess and manage

underwriting performance within the insurance companies, JRL and PLACL.

The decision was taken subsequent to the JRG/PAG merger to write the principal lines of business in

JRL, with 95% of sales in that company during the final quarter of 2016, and over £2 billion of new

business in 2016 as a whole. In future, PLACL will focus on Care products in both the UK and

through underwriting United States business generated by our partner Genworth.

Section A contains business performance on both a proforma and a statutory reporting basis. The

statutory basis has been prepared consistently with Just Group plc’s and JRL’s 18 month reporting

periods in their IFRS statutory accounts. PLACL’s accounts covered a 12 month period, of which the

final nine months were consolidated into the Group’s consolidated accounts following the

acquisition of Partnership on 1 April 2016 which is accounted for as an acquisition. Proforma

information, as if the Just Group was in existence on 1 January 2016 is also presented.

B. System of Governance

The Just Group’s system of governance is applied across all UK regulated subsidiaries of the Group,

including the insurance regulated entities JRL and PLACL. The Just Group plc Board is committed to

the highest levels of corporate governance, and focuses primarily on strategic, policy and

governance issues, acting in accordance with the best interests of policyholders and shareholders

as a whole. Through delegation to the various committees and functions, the application of best

practice across the Just Group is efficient and effective.

The terms of reference of the various committees are tightly defined enabling robust governance

supportive of strong decision making. Oversight is provided by the Risk and Compliance Committee

2

of the risk management and compliance activities across the Just Group including within JRL and

PLACL. Audit activities are overseen by the Audit Committee. Clear distinction is made between the

‘three lines of defence’, with the Risk function, Compliance function and the Chief Actuary’s function

representing the second line which is independent of the Finance and Actuarial reporting teams

constituting the first line, and the Audit function as the third line.

The Risk Management Framework enables risk management to be integrated into Just’s

organisational and decision making processes, with the preparation of Just’s group-wide Own Risk

and Solvency Assessment (ORSA) document providing a comprehensive assessment of the

regulated group companies’ risk and solvency positions.

Section B of this report describes the Group’s system of governance by which the operations of JRL

and PLACL and other group companies are overseen, and explains compliance with Solvency II

requirements.

C. Risk Profile

Risk identification is performed on a continuous basis, and is embedded in the ORSA. The primary

risks to which Just is exposed arise through its regulated insurance entities JRL and PLACL. The key

risks are:

Market risk comprising exposure to interest rate risk affecting the current value of future cash

flows, credit risk and residential property risk which affects the value of guarantees provided

within lifetime mortgages, and

Underwriting risk arising through the exposure to longevity, mortality and morbidity risks.

Risk is measured qualitatively and quantitatively, including through the Solvency II SCR calculations.

Section C describes the risks to which the insurance and other operations are exposed, and how

those risks are mitigated.

D. Valuation for Solvency Purposes

Assets, technical provisions and liabilities are valued in the Solvency II balance sheets according to

the Solvency II Directive and related guidance. Asset and liability valuations other than technical

provisions and reinsurance recoverable are based on IFRS values, representing accounting fair value

valuations.

At 31 December 2016, Just Group’s excess of assets over liabilities amounted to £1,743m, and those

of JRL and PLACL were £1,072m and £401m respectively.

Following approvals from the PRA, JRL and PLACL have used matching adjustment and transitional

measures for technical provisions to mitigate the impact for revaluing their balance sheets onto the

Solvency II basis, including the effect of interest rate movements seen in H1 2016 and 12 months of

amortisation. The release of margins on pre-2016 business is expected to continue to exceed the

amortisation of transitional reliefs.

At Group level, Solvency II net assets were £132m higher than on the IFRS basis mainly due to the

prudent margins held for IFRS reporting, whereas on the Solvency II basis the transitional relief on

technical provisions offset the risk margin.

Section D of this report provides further details on the methods and main assumptions used for the

valuation of items in the Solvency II balance sheet, and a comparison with IFRS reporting.

3

E. Capital Management

Just ensures that Own Funds items within JRL, PLACL and the Just Group as a whole are of sufficient

quality, and are structured and managed in such a way as to support coverage of the Solvency

Capital Requirement (SCR). The annual business planning process includes projection of the

forward-looking view of the adequacy of Own Funds to cover the SCR at entity and group levels,

along with assessment of potential management actions that could be deployed to restore capital

positions in the event of a deterioration. Regular monitoring of capital positions enables any

deterioration in coverage to be identified rapidly.

In managing capital, Just seeks to on a consistent basis:

Match the profiles of assets and liabilities, taking into account the risks inherent in each

business;

Maintain sufficient, but not excessive, financial strength in accordance with risk appetite, to

support new business growth and satisfy the requirements of the Just Group’s regulator and

other stakeholders giving Just’s customers assurance of its financial strength;

Retain financial flexibility by maintaining strong liquidity;

Allocate capital rigorously to support value adding growth and repatriate excess capital where

appropriate; and

Declare dividends with reference to factors including growth in cash flow and earnings.

JRL obtained approval for its internal model in December 2015, and work is well advanced on a

major model change application to include PLACL within the internal model. PLACL currently uses

the Solvency II standard formula to calculate its SCR.

At 31 December 2016, Just Group held £706m of excess own funds representing a capital coverage

ratio of 151% of SCR. Excess Own Funds and coverage ratios were £443m and 147% for JRL, and

£67m and 115% for PLACL respectively. In October 2016 Just issued £250m of subordinated debt

part of which was used to repay bank borrowings.

Our business has achieved strong growth in profits and the Board remains comfortable with our

capital position and sustainable business model.

Section E of this report provides further information on the capital positions of the companies, and

on the Internal model.

Just Group plc SFCR 31 December 2016

4

Chapter A contents

A Business and Performance ........................................................................................................................................... 5

A.1 Business ......................................................................................................................................................................... 5

A.1.1 Significant events in the period ....................................................................................................................... 6

A.1.2 Business objectives ............................................................................................................................................. 6

A.1.3 Material lines of business .................................................................................................................................. 8

A.1.4 New business sales ............................................................................................................................................. 9

A.1.5 Current business performance ....................................................................................................................... 11

A.1.6 Other information ............................................................................................................................................. 13

A.2 Underwriting Performance...................................................................................................................................... 14

A.3 Investment Performance ....................................................................................................................................... 16

A.3.1 Income and expenses by asset class ........................................................................................................... 16

A.3.2 Gains and losses recognised directly in equity .......................................................................................... 17

A.3.3 Investments in securitisation ......................................................................................................................... 17

A.4 Performance of other activities ............................................................................................................................. 17

Just Group plc SFCR 31 December 2016

5

A Business and Performance (Unaudited)

The Business and performance section of the report explains the business objectives, key operations and financial performance of the Group as a whole and of its two principal insurance subsidiaries.

A.1 Business

Just Group plc (formally JRP Group plc and Just Retirement Group plc) is a specialist UK financial services group focussing on attractive segments of the UK retirement income market. The Group is a leading and established provider of retirement income products and services to individual and corporate clients.

The Group had circa 500,000 customers and 1,045 employees at 31 December 2016.

Just Group plc is a public company limited by shares incorporated and registered in England and Wales on 13 June 2013.

The principal insurance subsidiaries of Just Group plc are Just Retirement Limited (JRL) and Partnership Life Assurance Company Limited (PLACL). JRL focuses on providing Retirement income products to individual and corporate clients and lifetime mortgages. PLACL focuses on Care and Protection products.

The chart below provides a simplified view of the group structure; information on the Group’s subsidiaries is included in public disclosure template S.32.01 ‘Undertakings in scope of the Group’ in section F.2.

The activities of other companies in the Group are:

Just Retirement Holdings Limited and Partnership Assurance Group - Intermediate holding companies

Just Retirement Solutions Limited - provision of services and distribution of products for the at-and-in retirement market

TOMAS Acquisitions Limited - intermediate holding company with two operating subsidiaries:

• The Open Market Annuity Service Limited - the provision of licensed software for the financial advisors and administration, and an annuity referral service

• TOMAS Online Development Limited - software development.

Just Retirement Money Limited and Partnership Home Loans Limited – Mortgage broking

Just Retirement Management Services Limited, Partnership Services Limited and Partnership Life US Company – Ancillary service companies

Just Retirement South Africa – insurance underwriting

The Group’s business in South Africa is out of scope for regulatory reporting to the PRA due to its limited materiality (see section D). Just Group statutory reporting basis figures and commentary in this document include South Africa; Solvency II regulatory reporting figures exclude South Africa.

The scope of the entities which make up the Group is otherwise consistent between the IFRS statements and Solvency II, however there are differences in the consolidation approach, as noted in Section D. All of the principal group entities are 100% held, and all are incorporated in the United Kingdom with the exception of Just

Just Group plc

Just

Retirement

Limited

Just

Retirement

Solutions /

Tomas

(HUB)

Just

Retirement

Money

Limited

Just

Retirement

Management

Services

Limited

Just

Retirement

South Africa

Partnership

Life

Assurance

Company

Limited

Partnership

Services

Limited

Partnership

Home Loans

Limited

Partnership

Life US

Company

Just Retirement

(Holdings)

Limited

Partnership

Assurance

Group plc

Just Group plc SFCR 31 December 2016

6

Retirement South Africa (South Africa) and Partnership Life US Company (United States). A full listing of all companies is included on schedule S.32 in section F.2.

The Group organisational structure is explained in Section B. A.1.1 Significant events in the year to 31 December 2016

A key milestone in the history of Just Group plc passed on 1 April 2016 with the acquisition by Just Retirement Group plc of Partnership Assurance Group plc. This has proved to be an excellent transaction, with the combined Group the leading specialist provider of retirement income products and services to both individuals and corporates, and a major supplier of lifetime mortgages.

HUB Financial Solutions, the Group’s division that provides services to UK businesses and their customers, continued to win new mandates, including a deal with Prudential UK and Phoenix Life.

In December 2015, Just Retirement Group plc (JRG) was successful in obtaining approval from the Prudential Regulation Authority (PRA) for use of its internal model for the calculation its solvency capital requirement. At the same time, JRG’s lifetime mortgage portfolio was restructured, and product pricing and reinsurance arrangements modified in anticipation of the Solvency II regime commencing on 1 January 2016.

In October 2016, Just Group plc successfully issued £250m of subordinated debt providing additional tier 2 capital to further enhance its capital position.

A.1.2 Business objectives

Following the merger, the strategic objectives of the Group have been reviewed and reset in line with the ambitions of the new Group. As a result of the decision that JRL should underwrite Just Group’s principal products, 95% of the Group’s new business was written in JRL in the final quarter of 2016.

Both predecessor groups held a strong history in innovation and were champions of positively disrupting markets to improve customer outcomes and these values continue to underpin our future strategy.

Just will use its unrivalled intellectual property (IP) to deliver better customer outcomes in all of its markets, supported by selective diversification, to generate high-quality returns for shareholders. We will adopt a measured approach to our growth and the development of our business, focussing first on delivering the promised benefits of the merger and laying the foundations, through our strategic enablers, for our next evolution. Our execution of this strategy will evidence that we are a profitable company with a sustainable business model and will strengthen our position in the market to achieve continued profitable growth.

The Group has three areas of strategic focus:

UK retail (retirement income, lifetime mortgages, long-term care and protection) - In our UK retail business, we believe that a guaranteed income for life and access to professional advice continue to play an important part of everyone’s retirement planning, and we will be adapting and developing our individual retirement propositions and distribution capabilities to continue to support and help customers up to, at, and in-retirement.

UK Defined Benefit De-risking - In our UK DB De-risking business, we will continue to establish ourselves as the leading provider in the small to medium sector of the market, using our longevity IP and expertise to deliver better outcomes for trustees.

International (US care and South Africa retirement income) - In our international businesses we will continue to build our presence and establish the Group’s UK award-winning service in these markets.

Just Group plc SFCR 31 December 2016

7

The Group’s strategic objectives are as follows:

Strategic objectives Why this is important How this will be achieved

1. Grow our addressable markets and broaden our distribution reach Increasing our profitable sales through focussing on growing markets and broadening our distribution reach to increase access to customers.

Using our resources to influence change and positively disrupt markets to grow our addressable share is key to the success in all our businesses. In our UK Retail business, we will support growth in the addressable GIfL and LTM markets supported by the Just Group's HUB business.

Similarly, in our UK DB De-risking business, we will continue to drive growth in the medically underwritten DB de-risking market, enabling us to provide more options for pension scheme trustees and providing greater opportunity for the Company to access and underwrite in the DB market.

We will use our growing customer insight, brand, strong relationships with our distribution partners, regulators and policy makers to grow our addressable markets. We will continue to develop our propositions to win new mandates and better serve our partners across our target markets and distribution channels. This will enable us to offer more elements of the value chain to a broad range of partners, including life insurance companies, banks, workplace and retail partners as well as financial intermediaries and EBCs. We believe our product range and services, distribution capabilities and strategic enablers set us apart in our target markets and will enable us to access and serve a greater number of customers.

2. Increase profitability through superior risk selection Using our IP to identify high-value opportunities to deliver excellent outcomes for our customers and increase our profitability.

The Company generates economic value through our diversified revenue streams, which enable us to grow our business and provide attractive returns on capital. By focussing on our strategic strengths, including our longevity IP, customer insight and distribution reach, we can identify and secure the highest value opportunities in the retirement income and retirement lending markets consistent with delivering excellent value for customers and generating high-quality returns for shareholders.

We will build on the strength of our longevity IP and its use in our selection and pricing of risks in our markets, and focus on development of our customer insight to augment that IP through greater understanding of the drivers of, and actual, customer behaviour. This will enable us to target specific customer segments with the desired risk profile. At the same time we will enhance our product offering to attract customers to the Company and to enable us to capture the desired risks across the market.

3. Ensure expenses are aligned with the capital model Efficiently managing our resources in line with our capital model to deliver sustainable growth in our business.

We recognise that a priority for our business is to ensure that our growth potential is achievable and that we demonstrate our ability to sustain growth in profits by ensuring our expenses are aligned to our capital model and in line with our ambitions.

We will deliver the merger benefits communicated to the market and identify and challenge areas of the business where expenditure does not result in acceptable benefits, and manage our resource allocation effectively and in line with our longer-term priorities. We are investing in our digital and change capabilities to increase our capacity to deliver change within the Company.

Just Group plc SFCR 31 December 2016

8

Strategic objectives Why this is important How this will be achieved

4. Improve cost and efficiency of capital Using our financial and capital management framework to achieve capital self-sufficiency.

We are focussed on achieving capital self-sufficiency that will enable us to continue to invest in growing our profits and rewarding our shareholders through closely managing the cost of our capital and ensuring we are effective and efficient in how we deploy it into the business to get the greatest return. Delivering a profitable business will ensure we are able to continue to invest to maintain our market leadership in delivering excellent value and outstanding service to our target customers.

We will focus on continuing to work with the regulator on developing our Solvency II internal model and matching adjustment to ensure we achieve the optimum capital requirements for the Company. This approach will support the effective operation of our capital-efficient business model.

5. Reduce dependency on any single business line or market Selectively diversifying our business into new, complementary markets to meet the evolving retirement needs of our customers and increase our capital efficiency.

To enable us to provide excellent service to our customers by providing a complementary set of services and products in line with market developments. As customers choose to access more of their assets to support their retirement planning, we will have the capabilities required to recruit these customers and gain access to new sources of assets in our core markets. Selective diversification in these markets will also allow us to increase our capital efficiency, provide additional future profit streams for the Company and reduce our concentration risk on our core market. This limited and controlled diversification will contribute towards reducing the risks of achieving long-term sustainable growth in profits.

In line with our measured approach, our immediate focus is building on and utilising our current businesses and their capabilities, laying the foundation for future profitable growth and diversification through deploying our strategic enablers. As we move forward, we will be looking to adjacent markets that are consistent with our strategic direction and financial framework and where we can apply our capabilities to meet customer needs.

A.1.3 Material lines of business

The Group's product offering comprises the following, all of which are classified as 'Other life' products for Solvency II reporting purposes with the exception of the FPP product which is a unit-linked product:

JRL PLACL

Defined Benefit De-risking Solutions (“DB”) Solutions for pension scheme trustees to remove the financial risks of operating pension schemes and create certainty that members’ pensions will be paid in the future.

Care Plans (“CP”) A solution for people moving to residential care who want security of knowing a regular payment will be made to the care provider for the rest of their life.

Guaranteed Income for Life (“GIfL”) A solution for a person (or couple) who want the security of knowing they will receive a guaranteed income for life.

United States Care business A Care solution sold in the US by our partner Genworth is reinsured with PLACL

Flexible Pension Plan (“FPP”) A solution for a customer wanting to retain greater flexibility of their pension savings and enabling irregular withdrawals.

Protection A solution for people wanting to support a residential mortgage, for business or inheritance tax planning purposes or simply to have financial peace of mind.

Lifetime Mortgages (“LTM”) Solutions designed for people who want to release some of the value of their home.

Just Group plc SFCR 31 December 2016

9

A.1.4 New business sales (pro forma basis)

Following the change of accounting reference date from 30 June to 31 December, the Group’s financial period to 31 December 2016 was an 18 month period. The Group therefore reports financial performance on a statutory basis for the 18 month period to 31 December 2016. However, management consider the 2016 calendar year to be more relevant for ongoing performance measurement and have assessed performance for the 12 month period to 31 December 2016, with Partnership results included on a pro forma basis from 1 January 2016.

The table below shows sales in the 12 months to 31 December 2016:

Just Group plc

(Pro forma*)

Just

Retirement Limited

Partnership Life Assurance

Company Limited

New business sales £m £m £m

Defined Benefit De-risking Solutions (“DB”) 943.4 945.9 (2.5)

Guaranteed Income for Life Solutions (“GIfL”) 778.1 624.2 148.4

Care Plans (“CP”) 97.2 26.5 70.7

Retirement Income sales 1,818.7 1,596.6 216.6

Drawdown 25.2 25.2 -

Total Retirement sales 1,843.9 1,621.8 216.6

Protection 4.7 - 4.7

LTM loans advanced 559.3 387.6 171.7

Total new business sales 2,407.9 2,009.4 393.0

* Includes 12 months of PLACL.

New business sales Total pro forma new business sales for Just Group of £2,407.9m for the year ended 31 December 2016 included £2,009.4m for JRL and £393.0m for PLACL. These comprised: Defined Benefit De-risking sales JRL DB sales for the year ended 31 December 2016 were £945.9m. Following the Solvency II disruption, sales momentum grew through 2016 with sales in the second half of the year of £779m, which was approaching five times the £164m sales in the first half.

Prospects for growth for this proposition remain strong. The total UK market DB liabilities are anticipated to be some £2 trillion, but JRL’s primary focus is on the ‘Buy–in’ sub-sector which de-risks pensions already in payment. This category makes up 39% of the DB market liabilities, so our addressable market of pensions in payment may be around £800bn. Our proposition works for every DB scheme in the market, including those with billions of pounds of liabilities, but we focus our participations on transactions below the £250m level. Over the last few years the market value of DB de-risking transactions has been in a corridor of £8bn-£15bn per year which, given the size of the market liabilities, illustrates there is significant headroom for growth during the next decade.

It is also worth noting the emergence of a further £100bn of life company annuity back book transfers in 2016, which has created competition for already scarce de-risking capital. Altogether we expect the DB de-risking market will continue to grow, and the demand dynamics appear sustainable.

PLACL does not make DB sales following the merger, and the £2.5m in the year represents a premium adjustment. GIfL sales Total pro forma GIfL sales for Just Group totalled £778.1m.

JRL GIfL sales for the year ended 31 December 2016 were £624.2m confirming the stabilisation of the market after the introduction of Pension Freedom and Choice. It is our expectation that our addressable share of this market will grow in 2017, with increasing proportions of people buying this product on the open market.

In the short term, growth is more likely to be driven by changing distribution patterns. This should benefit us, given our focus on the products bought by customers who shop around for guaranteed income for life products on the open market where we are now the leading provider. The open market accounted for 45% of sales in 2016. There is still plenty of room for improvement before we get back to open market sales that were around 60% of the total market prior to the Pension Reforms.

Just Group plc SFCR 31 December 2016

10

PLACL GIfL sales for the year ended 31 December 2016 were £148.4m. PLACL stopped selling new GIfL contracts following the merger except for small volumes where there were contractual requirements in place. Care sales Total pro forma Care sales for Just Group totalled £97.2m.

JRL Care Plans sales were £26.5m for the year ended 31 December 2016. Care Sales are no longer a core business for JRL and future sales are written by PLACL.

PLACL Care Plan sales were £70.7m for the year ended 31 December 2016. This remains an attractive market with longer-term structural growth prospects. Drawdown sales Drawdown sales, which include Flexible Pension Plan (“FPP”) and Capped Drawdown (“CD”) sales, were £25.2m in 2016. This is in line with our expectations and reflects growth in sales of the FPP product which allows customers to take advantage of the new Pensions Freedoms. The CD product is no longer available to new customers. Protection sales Pro forma protection sales were £4.7m in 2016, all through PLACL. Lifetime mortgage loans Total pro forma LTM advances of £559.3m reflected overall UK LTM market growth in 2016, with favourable underlying dynamics.

JRL LTM advances were £387.6m for the year ended 31 December 2016. Full advantage was taken of favourable economic conditions early in the year for lifetime mortgages and then later intentionally managed back towards our target ratio of LTM to new Retirement Income liabilities. These assets provide a good match for the JRL’s liabilities, including DB De-risking solutions where the profile of liabilities can be of a longer duration than GIfL contracts due to benefit indexation.

PLACL LTM advances were £171.7m for the year ended 31 December 2016. PLACL stopped selling lifetime mortgages following the merger except where there remain contractual arrangements in place.

Just Group plc SFCR 31 December 2016

11

A.1.5 Current business performance

As noted above in section A.1.4, management consider the calendar year 2016 to be more relevant for performance measurement and assesses performance for JRL, PLACL and the Group for the 12 month period to 31 December 2016. As the acquisition was effective from the beginning of April 2016, Just Group’s statutory performance includes PLACLs performance for the 9 months to 31 December 2016.

In the table below, both periods are provided to allow cross-referencing to the 18 months statutory profit before tax analysed in sections A.2 to A.4.

Adjusted operating profit view

Just Group plc

Just Retirement

Limited

Partnership Life Assurance

Company Limited

12 months1 18 months2 12 months 18 months 12 months

£m £m £m £m

£m

New business operating profit 123.9 171.7 132.9 178.8 (9.0)

In-force operating profit 74.6 88.2 40.5 59.2 34.0

Underlying operating profit 198.5 259.9 173.4 238.0 25.0

Operating experience and assumption changes

2.6 2.5

0.9 (1.4) 4.7

Reinsurance and financing costs (40.0) (52.0) (30.5) (44.7) (9.5)

Acquisition related basis changes - - - - (45.1)

Profit on Underwriting activity - A.2 161.1 210.4 143.8 191.9 (24.9)

Investment and economic profits – A.3 96.1 93.1 34.7 37.5 63.1

Other Group companies’ operating results 2.6 5.3 - - -

Non-recurring and project expenditure (15.7) (21.1) (7.8) (14.8) (6.2)

Acquisition transaction and integration costs

(48.6) (64.1)

- - -

Amortisation costs (23.0) (24.8) - - -

Other activities – A.4 (84.7) (104.7) (7.8) (14.8) (6.2)

Profit before tax 172.5 198.8 170.7 214.6 32.0

1 Just Group figures on a calendar year basis include 12 months of JRL and 12 months of PLACL. 2 Just Group figures on a statutory basis include 18 months of JRL and 9 months of PLACL.

New business operating profit Total Just Group pro forma new business operating profit was £123.9m in the 12 months to 31 December 2016.

JRL’s new business operating profit for the 12 months to 31 December 2016 was £132.9m. Margins have improved over the period reflecting pricing changes following implementation of Solvency II, favourable mortgage yields, initial benefits from delivering the post-merger cost synergies, and our focus on profits over volumes using our IP to select higher margin new business.

PLACL’s new business operating loss for the 12 months to 31 December 2016 was £9.0m, reflecting that the company largely stopped selling GIfL business after the merger. In-force operating profit In-force operating profit for the 12 months to 31 December 2016 was £40.5m for JRL, £34.0m for PLACL, and £74.6m pro forma for the Group. This is as a result of growth in the size of the in-force business offset by the impact of lower interest rates on the returns earned on surplus assets and the effect of narrowing bond spreads which have reduced the corporate bond default margin emerging.

Just Group plc SFCR 31 December 2016

12

Underlying operating profit Underlying operating profit for the 12 months to 31 December 2016 was £173.4m for JRL, £25.0m for PLACL, and £198.5m pro forma for the Group, reflecting the new business and in-force operating profits. Underlying operating profit is the sum of the new business operating profit and in-force operating profit. This measure excludes the impact of one-off assumption changes and investment variances. Operating experience and assumption changes Operating experience and assumption changes, which include expense and mortality experience variances, for the 12 months to 31 December 2016 amounted to £0.9m for JRL, £4.7m for PLACL, and £2.6m pro forma for the Group. Reinsurance and finance costs JRL’s reinsurance and bank finance costs for the 12 months to 31 December 2016 were £30.5m, which primarily represents interest payable on £300m of Tier 2 financing. (In October 2016, £200m of the £250m bond issued to JRH was replaced with a £250m bond issue by Just Group and backed by JRL, and £50m of the bond issued to JRH remained in place).

PLACL’s reinsurance and bank finance costs for the 12 months to 31 December 2016 were £9.5m, which primarily represents interest payable on the £100m of Tier 2 financing.

Just Group’s pro forma reinsurance and finance costs for the 12 months to 31 December 2016 were £40.0m, which includes the interest payable on the Tier 2 financing comprising the £250m Just Group bonds and the £100m of PLACL bonds. Acquisition related basis changes Basis changes arising on the one-off alignment of PLACL’s reserving methodology with that of the Just Group. Changes in economic and investment conditions Changes in economic and investment conditions over the year led to a profit of £34.7m in JRL, £63.1m in PLACL, and £96.1m pro forma for the Group, mainly reflecting the impact of the significant reduction of risk-free rates during the period, and the positive impact from the difference between actual and expected investment returns earned, together with a narrowing of credit spreads, offset by property valuation movements, and by changes in future property assumptions. Other Group companies’ operating results Just Group’s other Group companies’ operating results represents the results of the Group’s non-insurance undertakings. Non-recurring and project expenditure Non-recurring and project expenditure amounted to £7.8m for JRL, £6.2m for PLACL, and £15.7m pro forma for the Group, and represented one-off regulatory, project and development costs. Acquisition transaction and integration costs Acquisition costs reflect the one-off costs incurred during the period in relation to the acquisition of Partnership Assurance Group plc, including advisory, legal and stamp duty costs. Integration costs relate to the costs arising from the integration of the Just Retirement and Partnership businesses and operations. Amortisation costs Amortisation costs relate to the amortisation of the Group’s intangible assets, including the amortisation of intangible assets newly recognised in relation to the acquisition of Partnership Assurance Group plc. Acquired in-force business and other intangibles of £169.6m were recognised on acquisition of Partnership Assurance Group plc. The acquired in-force business asset is being amortised in line with the run-off of the in-force business. Amortisation costs also includes the impairment of brand and Partnership related property lease intangible assets.

Just Group plc SFCR 31 December 2016

13

A.1.6 Other information

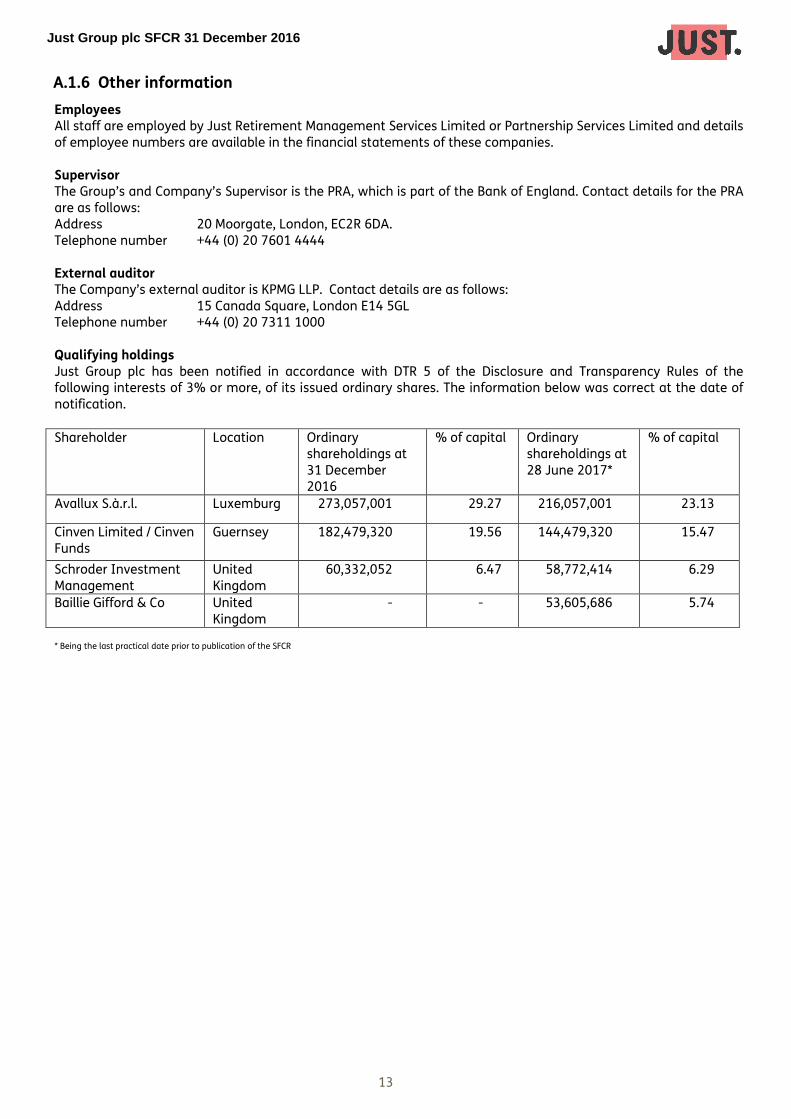

Employees All staff are employed by Just Retirement Management Services Limited or Partnership Services Limited and details of employee numbers are available in the financial statements of these companies. Supervisor The Group’s and Company’s Supervisor is the PRA, which is part of the Bank of England. Contact details for the PRA are as follows: Address 20 Moorgate, London, EC2R 6DA. Telephone number +44 (0) 20 7601 4444 External auditor The Company’s external auditor is KPMG LLP. Contact details are as follows: Address 15 Canada Square, London E14 5GL Telephone number +44 (0) 20 7311 1000 Qualifying holdings Just Group plc has been notified in accordance with DTR 5 of the Disclosure and Transparency Rules of the following interests of 3% or more, of its issued ordinary shares. The information below was correct at the date of notification.

Shareholder

Location Ordinary shareholdings at 31 December 2016

% of capital Ordinary shareholdings at 28 June 2017*

% of capital

Avallux S.à.r.l. Luxemburg 273,057,001 29.27 216,057,001 23.13

Cinven Limited / Cinven Funds

Guernsey 182,479,320 19.56 144,479,320 15.47

Schroder Investment Management

United Kingdom

60,332,052 6.47 58,772,414 6.29

Baillie Gifford & Co

United Kingdom

- - 53,605,686 5.74

* Being the last practical date prior to publication of the SFCR

Just Group plc SFCR 31 December 2016

14

A.2 Underwriting Performance

The table below presents underwriting performance consistent with IFRS statutory accounts except that a ‘normalised’ investment return has been included instead of the total investment return. Returns earned on investments are a key part of the underwriting model within long-term insurance businesses, and hence a ‘normal’ level of return has been included for the purpose of this review of underwriting performance. Variations from the normal or expected level of investment return are presented in section A.3 on Investment performance.

Following the change of accounting reference date from 30 June to 31 December, the Group and JRL's statutory reporting period for 2016 was the 18 month period to 31 December 2016, whilst PLACL’s was the 12 month period to 31 December 2016. As the acquisition was effective from the beginning of April 2016, Just Group’s statutory performance includes PLACL’s performance for the 9 months to 31 December 2016.

The Group has two lines of business for Solvency II reporting purposes as disclosed on the annexed S.05.01 template, the FPP unit-linked product with premiums of £29m representing 1.1% of the total business, and the remaining ‘Other’ life products. Given that the FPP product was in its infancy, it has not been split out separately in the table below.

Substantially all of the business written in the 18 months to 31 December 2016 was located in the United Kingdom, and hence the template S.05.02 for geographic split is not prepared.

Underwriting performance

Just Group plc 18 months to 31 Dec 20161

£m

Just Retirement Limited

18 months to 31 Dec 2016

£m

Partnership Life Assurance Company Limited

12 months to 31 Dec 2016

£m

Gross premiums written 2,693.5 2,584.9 184.9

Reinsurance premiums ceded (1,553.4) (1,498.6) (98.0)

Reinsurance recapture 1,166.9 1,166.9 -

Net premium revenue 2,307.0 2,253.2 86.9

Normalised investment return 1,522.4 1,260.1 332.5

Fee and commission income 5.6 3.1 -

Total revenue 3,835.0 3,516.4 419.4

Gross claims paid (1,204.5) (880.5) (431.5)

Reinsurers’ share of claims paid 512.4 309.3 270.8

Net claims paid (692.1) (571.2) (160.7)

Change in insurance liabilities:

Gross amount (2,687.1) (2,606.0) (240.4)

Reinsurers’ share 1,447.3 1,413.8 129.0

Reinsurance recapture (1,166.9) (1,166.9) -

(2,406.7) (2,359.1) (111.4)

Change in investment contract liabilities (15.5) (15.5) -

Acquisition costs (50.3) (52.4) (2.0)

Other operating expenses (204.6) (149.8) (64.9)

Finance costs (255.4) (176.5) (105.3)

Total claims and expenses (3,624.6) (3,324.5) (444.3)

Total Underwriting result 210.4 191.9 (24.9)

Investment performance – A.3 93.1 37.5 63.1

Other activities – A.4 (104.7) (14.8) (6.2)

Profit before tax 198.8 214.6 32.0

1 Just Group figures on a statutory basis include 18 months of JRL and 9 months of PLACL

Just Group plc SFCR 31 December 2016

15

Gross premiums written Gross premiums written are the total premiums received in relation to GIfL, DB and Care Plan contracts in the period, gross of commission paid, and amounted to £2,584.9m for JRL, £184.9m for PLACL, and £2,693.5m for the Group in the period to 31 December 2016. Net premium revenue Net premium revenue represents the sum of gross premiums written and reinsurance recapture, less reinsurance premium ceded. JRL restructured its reinsurance financing arrangements in the period, exercising its option to recapture £1,166.9m of premiums and entered into new treaties providing more extensive cover. As a result, reinsurance premiums ceded were £1,553.4m in the period to 31 December 2016. Normalised investment return The normalised investment return represents the expected return based on the opening yields on the established portfolio adjusted for investments acquired in the period and amounted to £1,260.1m for JRL, £332.5m for PLACL, and £1,522.4m for the Group for the period ended 31 December 2016. As noted above, fluctuations from expected yields due to changes in interest rates in the period and other economic factors, as captured as Investment and economic profits, are reported in the Investment performance section A.3. Net claims paid Net claims paid represents the total payments due to policyholders during the accounting period, less the reinsurers’ share of such claims which are payable back to the Group under the terms of the reinsurance treaties. Net claims paid for the period were £571.2m for JRL, £160.7m for PLACL, and £692.1m for the Group. Change in insurance liabilities Change in insurance liabilities represents the difference between the year-on-year change in the carrying value of the Group’s insurance liabilities and the year-on-year change in the carrying value of the Group’s reinsurance assets. Change in insurance liabilities was £2,359.1m for JRL, £111.4m in PLACL, and £2,406.7m for the Group for the period to 31 December 2016. The gross change in liabilities was £2,606.0m for JRL, £240.4m for PLACL, and £2,687.1m for the Group. The change in insurance liabilities net of reinsurance reflected the recapture and implementation of new reinsurance financing arrangements as noted above. Acquisition costs Acquisition costs comprise the direct costs (such as commissions) and indirect costs of obtaining new business. Other operating expenses Other operating expenses represent the operational overheads, including personnel expenses, investment expenses and charges, depreciation, reinsurance fees, operating leases and other expenses incurred in running the Group’s operations. Finance costs Finance costs represent interest payable on the deposits received from reinsurers, interest payable on subordinated debt, interest on reinsurance financing and bank finance costs, as noted in Section A.1.5.

Just Group plc SFCR 31 December 2016

16

A.3 Investment Performance

A.3.1 Income and expenses by asset class

Investment performance

Just Group plc 18 months to 31 Dec 20161

£m

Just Retirement Limited

18 months to 31 Dec 2016

£m

Partnership Life Assurance Company Limited

12 months to 31 Dec 2016

£m

Interest income

Bond interest 453.7 323.1 168.6

Cash interest 3.9 2.0 0.3

Mortgage interest 327.3 225.9 50.6

Collateral interest 0.2 0.1 -

Rental income 0.3 0.8 -

Intra-group income - 18.5 -

785.4 570.4 219.5

Fair value movements

Bonds 527.6 300.4 306.6

Mortgages 544.7 532.4 207.9

Reassurance (153.9) (25.1) (272.4)

Derivatives (66.6) (61.2) (65.5)

Other (20.4) (19.3) (0.5)

831.4 727.2 176.1

Total net investment return 1,616.8 1,297.6 395.6

Less: Normalised return included in underwriting result

(1,523.7)

(1,260.1)

(332.5)

Investment variance 93.1 37.5 63.1

1 Just Group figures on a statutory basis include 18 months of JRL and 9 months of PLACL

Interest income Interest income relates mainly to corporate bonds and rolled-up mortgage interest in the period during which there was strong growth in the asset portfolio from underlying business growth. Fair value movements The current period saw a substantial fall of 143bps in gilt rates, largely following the Brexit vote, which generated £300.4m of gains on bonds in JRL, £306.6m in PLACL, and £527.6m for the Group. There was also a £532.4m positive movement in fair value of mortgages in JRL, £207.9m in PLACL, and £544.7m for the Group, mainly caused by the further falls in interest rates which led to increases in the value of the lifetime mortgages. The reassurance fair value movement represents the amount of the increase in the reinsurance financing liabilities, which is driven by changes in the valuation interest rate. The fall in interest rates has resulted in the unfavourable valuation adjustment in the liabilities, partly offset by a change in the value of the reinsurance recoverable.

Just Group plc SFCR 31 December 2016

17

The fair value movement in derivatives includes £71.4m of realised losses on positions that have been closed out in the period. Following the implementation of Solvency II, the interest rate risk changed from being an upward rate risk to a downward rate risk as this increases balance sheet values, and correspondingly, the Solvency Capital Requirement. The unrealised gain of £4.8m represents offsetting movements across the various derivative types, reflecting the following experience:

Favourable on interest rates swaps as interest rates have declined, particularly following the Brexit vote.

Favourable on inflation swaps as longer-term inflationary pressures have built following the weakening of Sterling.

Unfavourable on FX swaps as the Group’s hedged currency denominated assets have increased in value in Sterling terms.

Investment expenses

Investment expenses in the period were £8.0m in JRL, £5.5m in PLACL, and £9.8m for the Group.

A.3.2 Gains and losses recognised directly in equity There were no gains or losses recognised directly in equity in the period.

A.3.3 Investments in securitisation

There are no investments in securitisations.

A.4 Performance of other activities

Just Group plc

Just Retirement

Limited

Partnership Life Assurance

Company Limited

18 months 18 months 12 months

£m £m

£m

Other Group companies’ operating results 5.3 - -

Non-recurring and project expenditure (21.1) (14.8) (6.2)

Acquisition integration costs (40.7) - -

Acquisition transaction costs (23.4) - -

Amortisation and impairment of intangible assets

(24.8) - -

Other activities (104.7) (14.8) (6.2)

Other Group companies’ operating results includes income on internal debt issued by JRL less holding company expenses and losses in the professional services companies.

Non-recurring and project expenditure includes one-off regulatory project and development costs.

Acquisition transaction costs of £23.4m reflect the one-off costs incurred during the period in relation to the acquisition of Partnership Assurance Group plc. These costs include advisory, legal and stamp duty costs.

Acquisition integration costs of £40.7m relate to the cost arising from the post-merger integration of the Just Retirement and Partnership businesses and operations. The restructuring changes made to date have already delivered approximately £30m of synergies on an annualised basis.

Amortisation costs relate to the amortisation of the Group’s intangible assets, including the amortisation of intangible assets newly recognised in relation to the acquisition of Partnership Assurance Group plc by JRP Group plc.

Just Group SFCR Report 31 December 2016

18

Chapter B contents

B. System of Governance ................................................................................................................................................. 19 B.1 General information on the system of governance ........................................................................................... 19

B.1.1 Governance in the Just Group ......................................................................................................................... 19 B.1.2 Governance structure in Just Retirement Limited and Partnership Life Assurance Company Limited ............................................................................................................................................................................. 22 B.1.3 Allocation of responsibilities to functions..................................................................................................... 23 B.1.4 Changes in the system of governance .......................................................................................................... 24 B.1.5 Assessment of adequacy .................................................................................................................................. 24 B.1.6 Remuneration policy .......................................................................................................................................... 25 B.1.7 Material transactions ........................................................................................................................................ 28 B.1.8 Intra-group outsourcing arrangements........................................................................................................ 28

B.2 Fit and proper requirements .................................................................................................................................... 28 B.2.1 Requirement applicable to Directors ............................................................................................................. 29 B.2.2 Assessing fitness and propriety....................................................................................................................... 31

B.3 Risk management system including the own risk and solvency assessment ............................................. 31 B.3.1 Risk governance and management framework .......................................................................................... 31 B.3.2 Integration of risk management into the decision making processes .................................................. 33 B.3.3 Determination of own solvency needs .......................................................................................................... 33 B.3.4 Internal model Governance ............................................................................................................................. 33 B.3.5 ORSA management ............................................................................................................................................ 33 B.3.6 ORSA process ....................................................................................................................................................... 34

B.4 Internal control system ............................................................................................................................................ 35 B.4.1 Internal control system description ............................................................................................................... 35 B.4.2 Roles and responsibilities of the Compliance function .............................................................................. 36

B.5 Internal audit function .............................................................................................................................................. 37 B.5.1 Internal audit function description ................................................................................................................ 37 B.5.2 Independence and objectivity of internal audit .......................................................................................... 38

B.6 Actuarial function ....................................................................................................................................................... 38 B.7 Outsourcing .................................................................................................................................................................. 39

B.7.1 Group Outsourcing Policy .................................................................................................................................. 39 B.7.1 Principal outsourced activities ......................................................................................................................... 39

B.8 Any other information ............................................................................................................................................... 39

Just Group SFCR Report 31 December 2016

19

B. System of Governance (Unaudited)

This section sets out information regarding the System of Governance in place in the Just Group plc, which applies to the UK regulated entities in the Group, including the JRL and PLACL subsidiaries.

Details of the structure of the Company's “administrative, management or supervisory body” (defined as including the Board, subsidiary boards and Board sub-committees) are provided. The roles, responsibilities and governance of key functions (defined as the Risk, Compliance, Internal Audit and Actuarial functions) are also provided. Other components of the system of governance are also outlined, including the risk management system and internal control system implemented across the business.

B.1 General information on the system of governance

B.1.1 Governance in the Just Group

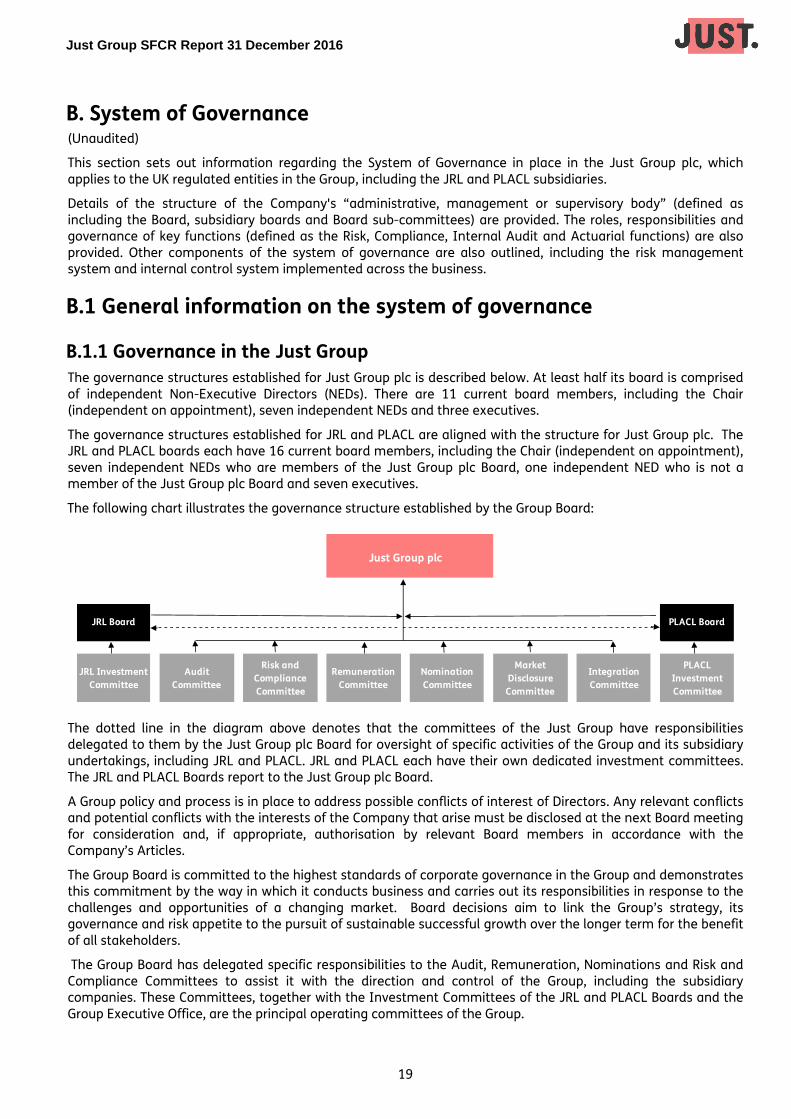

The governance structures established for Just Group plc is described below. At least half its board is comprised of independent Non-Executive Directors (NEDs). There are 11 current board members, including the Chair (independent on appointment), seven independent NEDs and three executives.

The governance structures established for JRL and PLACL are aligned with the structure for Just Group plc. The JRL and PLACL boards each have 16 current board members, including the Chair (independent on appointment), seven independent NEDs who are members of the Just Group plc Board, one independent NED who is not a member of the Just Group plc Board and seven executives.

The following chart illustrates the governance structure established by the Group Board:

The dotted line in the diagram above denotes that the committees of the Just Group have responsibilities delegated to them by the Just Group plc Board for oversight of specific activities of the Group and its subsidiary undertakings, including JRL and PLACL. JRL and PLACL each have their own dedicated investment committees. The JRL and PLACL Boards report to the Just Group plc Board.

A Group policy and process is in place to address possible conflicts of interest of Directors. Any relevant conflicts and potential conflicts with the interests of the Company that arise must be disclosed at the next Board meeting for consideration and, if appropriate, authorisation by relevant Board members in accordance with the Company’s Articles.

The Group Board is committed to the highest standards of corporate governance in the Group and demonstrates this commitment by the way in which it conducts business and carries out its responsibilities in response to the challenges and opportunities of a changing market. Board decisions aim to link the Group’s strategy, its governance and risk appetite to the pursuit of sustainable successful growth over the longer term for the benefit of all stakeholders.

The Group Board has delegated specific responsibilities to the Audit, Remuneration, Nominations and Risk and Compliance Committees to assist it with the direction and control of the Group, including the subsidiary companies. These Committees, together with the Investment Committees of the JRL and PLACL Boards and the Group Executive Office, are the principal operating committees of the Group.

Just Group plc

- - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - - -

JRL Investment

Committee

Audit

Committee

Risk and

Compliance

Committee

Remuneration

Committee

Nomination

Committee

Market

Disclosure

Committee

Integration

Committee

PLACL

Investment

Committee

JRL Board PLACL Board

Just Group SFCR Report 31 December 2016

20

The Chief Executive Officer (CEO) operates a Group Executive Office to support him in the performance of his duties, including the Group’s financial performance and capital position, the capital strategy and approach to Solvency II, the Group’s risk management and Own Risk & Solvency Assessment (ORSA), regulatory issues, assets and liability management oversight and the Group’s strategy and development.

The Group Executive Office comprises the Executive Directors Rodney Cook, David Richardson and Simon Thomas, and Jane Kennedy (Chief Operating Officer) and Alex Duncan (Chief Risk Officer) from the Group’s senior management. The Group Executive Office meets weekly to discuss and approve operational matters and is supported by the following management committees: UK Corporate Senior Management Team (SMT), UK Retail SMT, UK Retirement Lending SMT, Owned Distribution SMT, International SMT, Asset and Liability Committee, Insurance Committee, Regulatory Oversight Committee, Product and Proposition Committee, Operational Risk Committee and Retail Funds Committee.

In addition to its principal operating committees, the Just Board has established a Market Disclosure Committee and an Allotment Committee, which meet whenever necessary. The Market Disclosure Committee oversees the disclosure of information by Just Group plc to meet its obligations under the Market Abuse Regulation and the UK Listing Authority Disclosure and Transparency Rules (DTR), and to ensure that decisions in relation to those obligations can be made quickly. The Committee’s role is to determine whether information is inside information, when such information needs to be disclosed and whether any announcements are required. Other responsibilities include reviewing and approving announcements concerning developments in Just’s business and monitoring compliance with the Group’s DTR disclosure controls and procedures. Its members comprise Tom Cross Brown (Chairman), Chris Gibson-Smith, Keith Nicholson, Rodney Cook, David Richardson and Simon Thomas.

The Allotment Committee has responsibility for overseeing the allotment and listing of new ordinary shares in the Just Group plc in accordance with the Company’s executive incentive plans and employee share plans. Its members comprise any two Directors, one of whom must be a non-executive Director.

Every Board Committee has written terms of reference setting out its duties, reporting responsibilities and authorities which are reviewed annually. Committee terms of reference are subject to periodic updating to reflect any changes in legislation, regulation or best practice.

The five main Board Committees comprise Non-Executive Directors of the Company who were appointed by the Board following review and recommendation by the Nominations Committee. The Chairman of each Committee reports on the proceedings of the previous Committee meeting at the next scheduled Board meeting. The Group Company Secretary is the Secretary of every Committee. Group Audit Committee The Audit Committee’s role is to assist the Boards with the discharge of their responsibilities in relation to financial reporting, internal and external audits, and controls, including reviewing the Group’s and principal subsidiaries’ annual financial statements, reviewing and monitoring the scope of the annual audit and the extent of the non-audit work undertaken by external auditors, advising on the appointment of external auditors and reviewing the effectiveness of the internal audit activities, internal controls and risk management systems in place within the Group. The Audit Committee will normally meet not less than four times a year and is chaired by Paul Bishop. Its other members are Steve Melcher, Keith Nicholson and Clare Spottiswoode. Group Remuneration Committee The Remuneration Committee recommends what policy the Group should adopt on executive remuneration and, within the terms of the Directors’ Remuneration Policy approved by the shareholders at the AGM in May 2017, determines the remuneration benefits, pension rights and compensation payments for all Solvency II staff, the Chairman, the Executive Directors of the Company, the Chief Actuary, the Company Secretary, the members of the Executive Committee and any other employees of the Group for when the Committee determines it will have oversight as agreed by the Board from time to time. The Remuneration Committee will also generate an annual remuneration report to be approved by the members of the Group at the AGM. The Remuneration Committee will normally meet not less than twice a year and is chaired by Ian Cormack. Its other members are Chris Gibson-Smith, Michael Deakin, and Steve Melcher. Group Nominations Committee The Nominations Committee assists the Boards in determining their composition and make-up. It is also responsible for periodically reviewing the Boards’ structure and identifying potential candidates to be appointed as Directors, as the need may arise. The Committee also determines succession plans for the Chairman and the

Just Group SFCR Report 31 December 2016

21

CEO. It will normally meet not less than twice a year and is chaired by Chris Gibson-Smith. Its other members are Paul Bishop, Ian Cormack, Tom Cross Brown, Keith Nicholson and Michael Deakin. Group Risk and Compliance Committee The Risk and Compliance Committee is principally responsible for assisting the Boards and other members of the Group in the discharge of their risk and regulatory oversight responsibilities. The Committee reviews and challenges the overall effectiveness of the Group’s regulatory systems and controls, risk management and future developments. It also provides advice on regulatory and risk strategies including oversight of current risk exposures. The Committee will normally meet not less than four times a year and is chaired by Keith Nicholson. Its other members are Ian Cormack, Tom Cross Brown, Chris Gibson-Smith, Steve Melcher and Clare Spottiswoode. Investment Committee The Investment Committees of the Boards of Just Retirement Limited and Partnership Life Assurance Company Limited assist their respective Boards in achieving its investment objectives, in line with the Group’s risk appetite. The Investment Committees are responsible for reviewing and overseeing the implementation of the life companies’ investment policies, including the performance of the investment portfolio, recommending the appointment and assessing the performance of the external investment managers, and the effectiveness of reporting procedures. The Investment Committees will normally meet not less than four times a year and are chaired by Michael Deakin. Their other members are Paul Bishop and Tom Cross Brown. Just Group plc Board The Group Board is responsible for the proper management of the Just’s strategy and direction, including its risk appetite. It also oversees the activities and direction of Just Retirement Limited, Partnership Life Assurance Company Limited and Just Retirement Money Limited, and the Group’s other operating subsidiaries. There are eleven Board members: the Chairman (independent on appointment), three Executive and seven Non-Executive Directors who are considered to be independent. Keith Nicholson is the Senior Independent Non-Executive Director.

The Board believes that documented roles and responsibilities for Directors, with a clear division of key responsibilities between the Chairman and the CEO, are essential elements in the Group’s governance framework and facilitate the effective operation of the Board. As noted above, Independent NEDs make up at least half of the Directors on the Just Group Board excluding the chairman. There is a separate NED chairman for each of the key Committees.

The Chairman is responsible for the effective leadership and governance of the Board but takes no part in the day-to-day running of the business. His key responsibilities include: • Leading the Board effectively to ensure it is primarily focused on strategy, performance, value creation and

accountability • Ensuring the Board determines the significant risks the Group is willing to embrace in the implementation of

its strategy • Leading the succession planning process and chairing the Nominations Committee • Encouraging all Directors to contribute fully to Board discussions and ensuring that sufficient challenge

applies to major proposals • Fostering relationships within the Board and providing a sounding board for the CEO on important business

issues • Identifying development needs for the Board and Directors • Leading the process for evaluating the performance of the Board, its Committees and individual Directors • Ensuring effective communication with major shareholders The CEO is responsible for leadership of the Group’s business and managing it within the authorities delegated by the Board. His key responsibilities include: • Proposing and developing the Group’s strategy and significant commercial initiatives • Leading the executive team in the day-to-day running of the Group • Ensuring the Group’s operations are in accordance with the business plan approved by the Board, the Board’s

overall risk appetite, the policies established by the Board, and applicable laws and regulations • Representation of the Group’s interests in the UK and abroad • Maintaining dialogue with the Chairman on important business and strategy issues • Recommending budgets and forecasts for Board approval

Just Group SFCR Report 31 December 2016

22

• Providing recommendations to the Remuneration Committee on remuneration strategy for Executive Directors and other senior management

• Leading the communication programme with shareholders and ensuring the appropriate and timely disclosure of information to the stock market

The NED’s constructively challenge and help develop the Group’s strategy. In addition to this, Paul Bishop, Ian Cormack and Keith Nicholson respectively chair the Board’s Audit, Remuneration, and Risk and Compliance Committees, while Michael Deakin chairs the Investment Committees of Just Retirement Limited and Partnership Life Assurance Company Limited. As the Senior Independent Director, Keith Nicholson provides a sounding board for the Chairman, deputises for the Chairman in his absence and serves as an intermediary for the other Directors when necessary.

Decisions on operational matters are delegated to the Executive Directors under documented policies and procedures. In advance of scheduled Board meetings, each Director receives documentation providing updates on the Group’s strategy, finances, operations and development, and which have reference to a formal schedule of matters reserved for Board approval which includes: • The Group’s business strategy and risk appetite • Business strategy plans and objectives, budgets and forecasts • Extension of the Group’s activities into new business or geographic areas • Changes in capital structure and any form of fundraising • Major changes to the Group’s corporate structure, including reorganisations, acquisitions, disposals and

major capital projects • The Group’s systems of internal control and risk management • Changes to the membership of the Board • Interim and annual financial statements • Dividend policy The schedule of matters reserved for Board approval is reviewed annually.

Non-Executive Directors’ appointments are subject to review every three years. Their letters of appointment set out the expected time commitment, recognising the need for availability in exceptional circumstances, and the Board is informed of any subsequent changes in their other significant commitments. None of the Executive Directors holds a Non-Executive Directorship in a FTSE 100 company. All Directors’ appointments are subject to annual re-election by shareholders.

B.1.2 Governance structure in Just Retirement Limited and Partnership Life Assurance Company Limited The governance structures established for Just Retirement Limited and Partnership Life Assurance Company Limited are aligned with the structure for Just Group plc. Each legal entity within the Group has its own Board responsible for taking key decisions regarding the conduct of its business and its responses to the challenges and opportunities presented by changing markets, as well as alignment of the entity’s strategy with that of the Group as a whole.

At least half of the Board of any regulated subsidiary of Just Group plc must be comprised of Independent NEDs. The Just Group plc Chairman is also the JRL and PLACL Chairman. The Board of Just Group plc decided that Just Retirement Solutions (JRS), Just Retirement Money Limited (JRML) and Partnership Homes Loans Limited (PHLL) should have a separate Chairman to mitigate against potential conflicts of interest with JRL and PLACL. Just Retirement South Africa (JRSA) also has a separate Chairman to reflect the market in which it operates.

The Boards of JRL and PLACL include an independent NED who is not a member of the Just Group plc Board or any other subsidiary boards.

The remit of each Board is defined in Terms of Reference, which set out its principal role and scope of responsibilities. Certain decisions are listed in a document as being reserved for decision by the Board of Just Group plc, notably where consistency of strategy, policies, processes and procedures are appropriate.

Just Group SFCR Report 31 December 2016

23

Each Board is responsible for:

Continually gaining insight into the company and its environment

Clarifying priorities for management and the company and defining how the Board expects these priorities to be achieved

Holding management to account and seeking assurance that these priorities and expectations are being delivered

Each Board is supported in its decision making by legal entity specific reports provided by the Audit, Remuneration, Nominations and Risk and Compliance Committees of the Group. The Investment Committees are directly committees of the Just Retirement Limited and Partnership Life Assurance Company Limited Boards.

As a regulated entity in another territory, JRSA has in place its own Committee Structure. This includes a Remuneration Committee, a Treating Customers Fairly Committee and an Actuarial, Audit and Risk Committee.

B.1.3 Allocation of responsibilities to functions

In order that the Group can be run effectively, responsibility and accountability is delegated to specific individuals. The Group CEO is responsible for apportionment and oversight. In addition, the CEO provides oversight to those who are apportioned responsibilities through the performance management framework. The allocation of responsibilities is covered in the Just Group Governance Map.

Executive Committees

DCEO Deputy Chief Executive Officer GDS Group Director Strategy MDUKC Managing Director UK Corporate Business

GFCO Group Chief Financial Officer GCDIO Group Chief Digital Information Officer MKUKR Managing Director UK Retail Business

GCOO Group Chief Operating Officer GMDD Group Marketing and Distribution Director MDUKLTM Managing Director UK LTM

GCRO Group Chief Risk Officer GBDD Group Business Development Officer GMDD Group Marketing & Distribution Director

Management committees

CSMT UK Corporate SMT (Deputy CEO) INT SMT International SMT (EDBD) PPC Product and Proposition Committee (GMDD)

RSMT UK Retail SMT (UKMDR) ALCO Asset and Liability Committee (DCEO) OpRisk Operational Risk Committee (GCRO)

RLSMT UK Retirement Lending SMT (UKMDRL) InsCom Insurance Committee (Deputy CEO) RFC Retail Funds Committee (UKMDR)

ODSMT Owned Distribution (JRS) SMT (GMDD) ROC Regulatory Oversight Committee (GRAD)

Executive Committees Committees are in place to support Executives in meeting their accountabilities because they will require advice, assistance and challenge in meeting these accountabilities from people across the business. A committee is a permanent, regular and formal meeting that brings together different disciplines or business area experts, to help to shape decisions within executive accountabilities. Each committee has clearly defined authority to support decisions related to a designated area and all minutes are recorded formally.

Group Executive Office Members: CEO, DCEO, GCFO, GCOO, GCRO In attendance: GDS Agenda specific: GCDIO, GMDD, GCRD, GBBD Matters: Group financial performance, group capital position / strategy & SII, Group risk (ORSA), regulatory issues, asset & liability oversight, Group strategy and Group Development.

Group Executive Office Members: CEO, DCEO, GCFO, GCOO, GCRO In attendance: GDS Agenda specific: GCDIO, GMDD, GCRD, GBBD Matters: Group financial performance, group capital position / strategy & SII, Group risk (ORSA), regulatory issues, asset & liability oversight, Group strategy and Group Development.