A PROJECT REPORT On “ANALYSIS OF HDFC LOANS IN BAREILLY “ For HDFC BANK Ltd. SUMMER TRAINING PROJECT UNDER THE GUIDANCE OF Akrash Mehrotra Dr. Sankalp Srivastava (Relationship Manager) (Assistant Director) HDFC BANK LTD., BAREILLY INSTITUTE OF PRODUCTIVITY & MANAGENMENT, Lucknow SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF POST GRADUATION DIPLOMA IN MANAGEMENT BY KANIKA TANDON PGDM (F/T) L209021 INSTITUTE OF PRODUCTIVITY & MANAGEMENT LUCKNOW 1 Institute of Productivity and Management

Transcript

A

PROJECT REPORT

On

“ANALYSIS OF HDFC LOANS IN BAREILLY “

For

HDFC BANK Ltd.

SUMMER TRAINING PROJECT

UNDER THE GUIDANCE OF

Akrash Mehrotra Dr. Sankalp Srivastava

(Relationship Manager) (Assistant Director)

HDFC BANK LTD., BAREILLY INSTITUTE OF PRODUCTIVITY

& MANAGENMENT, Lucknow

SUBMITTED IN PARTIAL FULFILLMENT FOR THE AWARD OF POST GRADUATION DIPLOMA IN MANAGEMENT

BY

KANIKA TANDON

PGDM (F/T)

L209021

INSTITUTE OF PRODUCTIVITY & MANAGEMENT

LUCKNOW

1Institute of Productivity and Management

2009-2011

ACKNOWLEDGEMENT

At the successful completion of summer internship program, I wish to express my true regards

to individuals who supported and directed me throughout this internship.

First of all I would like to give my gratitude and sincere regards and a note of thank to Akarsh

Mehrotra (Relationship Manager, HDFC Bank Ltd., Bareilly) for giving me this

opportunity and selecting me as summer trainee in this esteemed organization.

I would like to express my deep gratitude and regards for his valuable guidance and support

without which completion of this report would not be possible.

I would also like to give special thanks to Mr. Mukul Saxena, Mrs. Shweta Arora, (HDFC

Bank Ltd., Bareilly) for giving me their valuable time, support and inputs that helped me at

every step in this project.

I take the opportunity to acknowledge and express sincere thanks to Dr. Sankalp Srivastava

(Assistant Director, IPM Lucknow) for being constant source of inspiration to me, showing all

the patience and abundant encouragement throughout the project duration.

Lastly, I would like to thank all my friends for their support and help.

Kanika Tandon

2Institute of Productivity and Management

Declaration

I hereby declare that this Project Report entitled “ANALYSIS OF HDFC LOANS IN

BAREILLY “in HDFC BANK LTD., BAREILLY submitted in the partial fulfillment of the

requirement of Post Graduate Diploma In Management (PGDM) of INSTITUTE OF

PRODUCTIVITY & MANAGEMET, LUCKNOW is based on primary & secondary data

found by me in various departments, books, magazines and websites & collected by me in under

The project “ANALYSIS OF HDFC LAONS IN BAREILLY” gave an opportunity to get

practical experience and corporate exposure through which a lot was learned about loans. This

project is based on research in which there was a need to find out that whether people

are taking loans from HDFC or not and reasons behind both taking and not taking loans

,which age group of people are more taking, which type of loan people prefer to take,

which mode of payment they prefer one-time or EMI’s. This project helped a lot in making

people aware of loans and which type of loans people prefer more so that they could be

70Institute of Productivity and Management

benefited by it. This analysis was done on 150 individuals in Bareilly. The primary data will be

collected through questionnaire. The questionnaires consist of two parts:

First parts consist of customer demographics, which include age group, gender marital status and

Profession. This part will help in knowing which age group has more capacity according to

which market could be trapped, it will also help in knowing whether males or females are more

interested in taking loans. The second part of the questionnaire will help in knowing whether

people are aware of various loans schemes, from which institution they prefer to take loan,

people are more comfortable with EMI’s, one time payments etc. In the second part we also get

to know one important thing about customers whether they prefer loans or not and if they prefer

which type of loans they are taking etc. This project will give an idea about the current scenario

as to what customers prefer today. It will help in clearing the doubts of customers after knowing

as to why they don’t prefer loans. This way more information can be made available to them

which will increase the awareness about loans and therefore more people can enjoy the benefits

of loan.

WHY THIS PROJECT WAS UNDERTAKEN:

This report will provide different types of value addition to the organization as given below:-

Customer views on loans, which were being offered by bank according to their needs.

The facilities that the customer of loan is getting.

HDFC Bank will come to know the areas, where it needs to improve.

71Institute of Productivity and Management

The bank will also come to know what additional facilities are being provided by its competitors

on loans.

The main aim of this project is find out the market standard of HDFC’s loan when compare to its

competitors such as ICICI Bank, Axis Bank, SBI etc.

Through this project I can find out that on what grounds the loan provided by HDFC is different

from its competitors.

Project helps in creating good relationship and helps in solving the problems of the

customers.

This project helps in creating new customers and maintaining the existing customers by

providing maximum services.

PROBLEM ENVIRONMENT:

The main problem was lack of awareness about various loans schemes that the bank is offering, majority

of the people are unaware about these schemes. If the behavioral aspects of the people are taken into

account then while conducting the survey most of the people were not ready to answer the entire

questionnaire. Awareness level services offered by HDFC Bank is pitiable, respondents who had taken as

well as not taken loan are not aware about the product and services of HDFC Bank.

WHAT DOES BANK EXPECTS TO DO BY SOLVING THE PROBLEM?

The Bank expects to find out the knowledge level of customer of different loans.

The bank expects to find out which age groups of people are more interested in taking

loans.

72Institute of Productivity and Management

The bank also expects to find out in which Bank the customers prefer to take loan from.

This will help the bank in knowing the level of competition that exists.

The bank expects to find out which are the best services that they can provide to there

customers.

The company expects to find out whether the customer prefer in one time

payments or EMI’s.

73Institute of Productivity and Management

SECTION C

RESEARCH DESIGN

74Institute of Productivity and Management

Define research problem

75Institute of Productivity and Management

Design Strategy

[Type purpose, time frame, scope]

Management Decision

Data collection

Define analysis & interpretation

Research Report

RESEARCH METHODOLOGY

Research in common parlance refers to search for knowledge. Once can also define research as

a scientific and systematic search for pertinent information on a specific topic. In fact ,research

is an art an science of investigation .Redman and Moray define research as a

“systematized effort to gain knowledge” some people define research as a voyage of

discovery ,we all possess the vital instinct of inquisitiveness for when the unknown

confronts us , we wonder and our inquisitiveness makes us probe and attain full and

fuller understanding of the unknown The inquisitiveness is the mother of all the

knowledge and the method , which the man employs for obtaining the knowledge of

whatever the unknown ,can be termed as research. Research comprises defining and

redefining problems, formulating hypothesis or suggested solutions; collecting, organization and

evaluating data; making deductions and reaching conclusions, and at last carefully testing the

conclusions to determine whether they fit the formulating hypothesis. Research methodology

considers the logic behind the methods we use in the context of our study and explain why we

are using a particular method or technique and why we are not using others so that research

results are capable of being evaluated either by the researcher himself or by others. Research

methodology is a way to systematically solve the research problem. It may be understood as a

science of studying how research is done.

RESEARCH PROBLEM

The research problem was to know the position of HDFC Bank loan in Bareilly.

OBJECTIVE OF RESEARCH

To find out which type of loan for what duration is being preferred by the customer or public.

RESEARCH SUBOBJECTIVE

• To know why or why not customers/public prefer loans.

• To find out the most preferable loans taken by the customers.

76Institute of Productivity and Management

• To find what all are the requirements/services needed by the customers.

• To find out how Bank can influence a customer to take loan.

• This project helps in creating new customers and maintaining the existing customers by

providing maximum services.

• Solving the problems of the customers.

• The bank will also come to know what additional facilities that customer wants.

SCOPE OF THE STUDY

Geographical scope

Customers of Bareilly.

Duration of Study:

The study was carried out for a period of two months, from 01st May to 2nd July 2010.

RESEARCH DESIGN

Research Design is the conceptual structure within which research is conducted. It is basically

the blueprint for the collection of data, measurement of analysis of data. A Research Design is

the arrangement of conditions for collection and analysis of data in a manner that aims to

combine relevance to the research purpose with economy in procedure. A good research design

has following characteristics:

Problem Definition

Specific method of data collection and analysis

Time required for research project

My research design is of diagnostic type. Diagnostic research studies determine the

frequency with which something occurs.

77Institute of Productivity and Management

RESEARCH INSTRUMENT USED:

In this project questionnaire method is used to collect data due to following reasons:-

Written questionnaires are more cost effective as the number of research questions increases.

Questionnaires are easy to analyze. Data entry and tabulation for nearly all surveys can be

easily done with many computer software packages.

Questionnaires are familiar to most people. Nearly everyone has had some experience

completing questionnaires and they generally do not make people apprehensive.

Questionnaires reduce biasness. There is uniform question presentation and no middleman

biasness. The researchers own opinions will not influence the respondent to answer

questions in a certain manner.

There are no verbal or visual clues to influence the respondent.

Questionnaires are less intrusive.

DATA COLLECTION

The task of data collection begins after a research problem has been defined and research

design/ plan chalked out. While deciding about the method of data collection to be used for the

study, two types of data are used.

a. Primary Data

Primary data are those which are collected a fresh and for the first time and thus happen to be original in character.

ADVANTAGES:-

get comprehensive and original information

convenient to respondents

information are primary mode

DISADVANTAGES:-

78Institute of Productivity and Management

often takes much time

info may be incomplete

need to be quite clear about what looking for

b. Secondary Data

Secondary data on the other hand are those which have already been collected by

someone else and which have already been passed on. The data is collected, formulated

and processed keeping in mind the twin object of understanding the existing social

welfare and social security scheme and to derive out the result from the employer /

employee session. Samples are chosen at random basis.

ADVANTAGES

Doesn’t interrupt program or client’s routine program

Information already exist

Less costly

DISADVANTAGES

Information may be incomplete.

Not flexible means to get data, data restricted to what already exists.

Used only primary data for which a comprehensive questionnaire was prepared and was

filled by the individuals.

PRIMARY SOURCES

PERSONAL INTERVIEWING

This method is used when we want to understand someone’s buying behavior pattern, or learn

about his or her answer to questionnaires.

SECONDARY SOURCES

Data collected through internet.

The facts sheets of different banks.

Used many website such as (HDFC BANK, ICICI BANK, SBI BANK).

79Institute of Productivity and Management

Many magazines such as outlooks, business magazines, etc

Data collected from newspaper such as business standards, economic times.

SCHEDULE METHOD

This method of data is quite popular. A questionnaire consists of a number of questions printed

in definite order on a form. The respondents’ have an answer them on there own, constructed

questionnaire containing 22 questions each related to objective of the project.

Advantages:

These responses are gathered in a standardized way, it is in close-ended and open-ended form.

Disadvantages:

Questionnaires are standardized so it is not possible to explain any points in the questions

that participant might misinterpret.

Respondents may answer superficially especially if the questionnaire takes a long time to

Complete.

Respondents may not be willing to answer the questions. They might not wish to reveal

the information or they might think that they will not benefit from responding perhaps

even be penalized by giving their real opinion.

SAMPLING DESIGN:

A sampling design is a definite plan for obtaining a sample from a given population. It refers to

the technique or the procedure the researcher would adopt in selecting items for the sample.

Simple design is determined before data are collected. The sample size should also be

ascertained before starting the research program. The larger the sample sizes the better and

accurate will be the result.

Defining the Population

The first step in good sample design is to ensure that the specification of the target

population is as clear and complete as possible to ensure that all elements within the

80Institute of Productivity and Management

population are represented. The target population is sampled using a sampling frame.

Often the units in the population can be identified by existing information; for example,

pay-rolls, company lists, government registers etc. A sampling frame could also be

geographical; for example postcodes have become a well-used means of selecting a

sample.

Sample Size = 150

For any sample design deciding upon the appropriate sample size will depend on several

key factors

(1) No estimate taken from a sample is expected to be exact: Any assumptions about

the overall population based on the results of a sample will have an attached margin of

error.

(2) To lower the margin of error usually requires a larger sample size. The amount of

variability in the population (i.e. the range of values or opinions) will also affect accuracy

and therefore the size of sample.

(3) The confidence level is the likelihood that the results obtained from the sample lie

within a required precision. The higher the confidence level that is the more certain you

wish to be that the results are not atypical. Statisticians often use a 95 per cent confidence

level to provide strong conclusions.

(4) Population size does not normally affect sample size. In fact the larger the

populations size the lower the proportion of that population that needs to be sampled to be

representative. It is only when the proposed sample size is more than 5 per cent of the

population that the population size becomes part of the formulae to calculate the sample

size.

81Institute of Productivity and Management

FIELD WORK

The field work is done in the area of HDFC BANK LTD., Civil Lines in the city

Bareilly. The questionnaires to the customers at the following places in Bareilly:

• PUBLIC SECTOR BANKS

• PRIVATE SECTOR BANKS

• GENERAL PUBLIC

SAMPLING TECHNIQUES USED

For the particular research study, used the following two types of Sampling i.e. Sampling

Techniques.

1. CONVENIENCE AND JUDGEMENT SAMPLING

2. SIMPLE RANDOM SAMPLING

1) CONVENIENCE and JUDGEMENT SAMPLING:

This method is quite helpful as one can consider the sample according to the convenience.

Under convenience sampling technique the sample units are chosen on the basis of researchers

convenience of location, travel, time, cost etc. The sampling technique used for the survey of

customer was convenience of sampling.

Advantages:

Easy to organize

Quick

82Institute of Productivity and Management

Disadvantages:

There is no guarantee that the behaviors of these people represent behaviors of other groups.

2) SIMPLE RANDOM SAMPLING

In this type of sampling, where each and every item in the population has an equal chance of

inclusion in the sample. The each item an equal probability of being selected.

Advantages:

Simple to design and interpret.

Can calculate estimate of the population and the sampling error

Analysis of data is reasonably easy

Disadvantages:

Need a complete and accurate population listing

May not be practical if the sample requires lots of small visits all over the country.

Analytical Tools Used

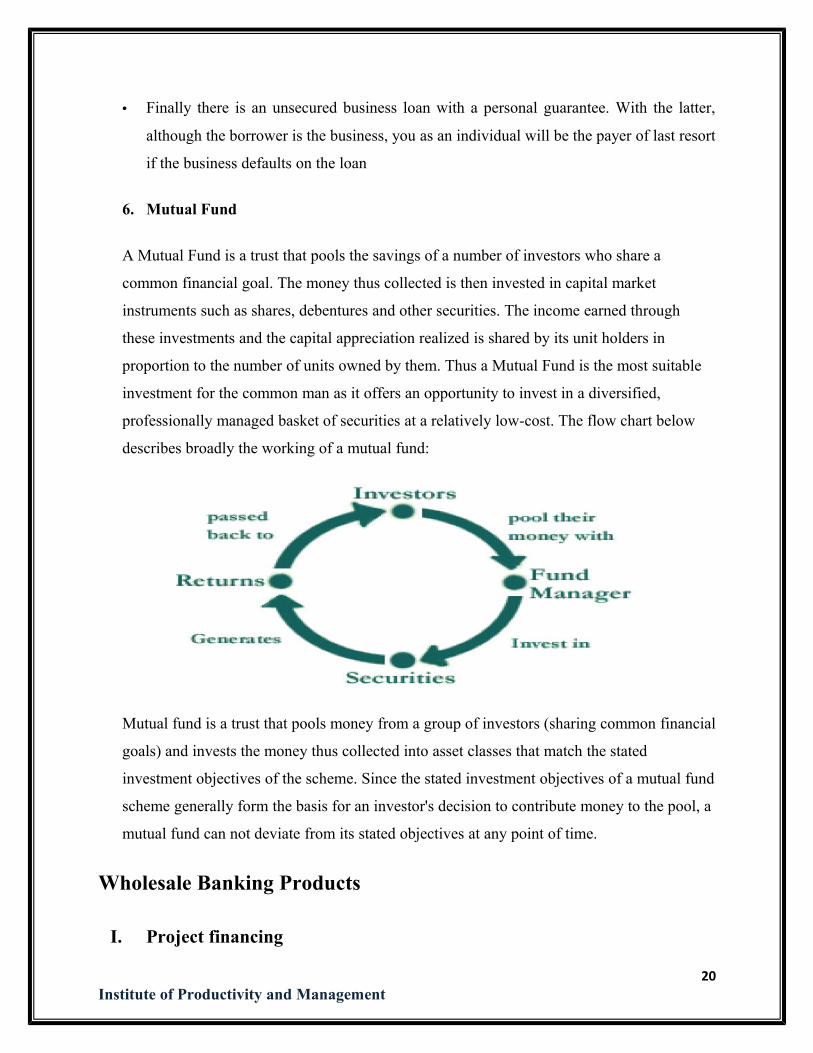

Data presented in the form of: Pie charts, percentage calculation.

LIMITATION OF THE STUDY:-

Some of the persons were not so responsive.

Since the sample for the study consist the public and customers of bank in Bareilly,

generalization may not be accurate. Further the validity and generalization of the results may

hold good only for Bareilly.

83Institute of Productivity and Management

The chance of simple random error may prove to be limitation as respondent may not to give

accurate information and even student bias while collecting the data should be considered.

Questionnaire used as the only instrument of the primary data.

SECTION D

84Institute of Productivity and Management

Data Analysis

(1)Age group?

Age group No. of Respondents Percentage

<=30yrs 36 24%

31-35yrs 52 35%

36-40yrs 26 17%

41-45yrs 15 10%

45-50yrs 12 8%

>50yrs 9 6%

Total 150 100%

85Institute of Productivity and Management

INTERPRETATION:- This chart depicts that between the age group of 31-35 are the major loan taker. This is because between this age group have lesser liability therefore are more risk taking and like to take loan to fullfill there goals in short term or as soon as possible.

(2)Gender?

Gender No. of Respondents Percentage

Male 112 75%

Female 38 25%

Total 150 100%

86Institute of Productivity and Management

INTERPRETATION:- This graph depict that 75% are male and only 25% are

female to take loan this is because majority of the female believes in saving money

or not ready to take any liability , therefore very few of the females take loan.

(3)Martial Status?

Martial Status No. of Respondents Percentage

Single 38 25%

Married 112 75%

87Institute of Productivity and Management

Total 150 100%

INTERPRETATION:- This chart depicts that married person takes more loan than single because married person want to make himself settle as soon as possible so that he can enjoy all his facility during his young age and make his old age more comfortable.

(4) Occupation/Profession?

Occupation/Profession No. of Respondents

Percentage

88Institute of Productivity and Management

Businessman 21 14%

Govt. Service 17 11%

Pvt. Service 50 33%

Professional 31 21%

Student 15 10%

Agriculture 13 9%

Others 3 2%

Total 150 100%

INTERPRETATION:-This chart depicts that Pvt. Employees and Professional take more loan because businessman has its own business so he tries to take out money from its profit. Government service people are not aware about loan schemes. While agricultural persons, students and others don’t have fixed, stable income so they try to avoid loan.

(5) Educational Qualification?

Educational Qualification No. of Respondents Percentage

89Institute of Productivity and Management

Graduation/PG 114 76%

Under graduation 24 16%

Others 12 8%

Total 150 100%

INTERPRETATION:- This chat depicts that 76% of the total sample size is graduate or post graduate. It means that they know about different types of loan schemes and know about there liabilities.

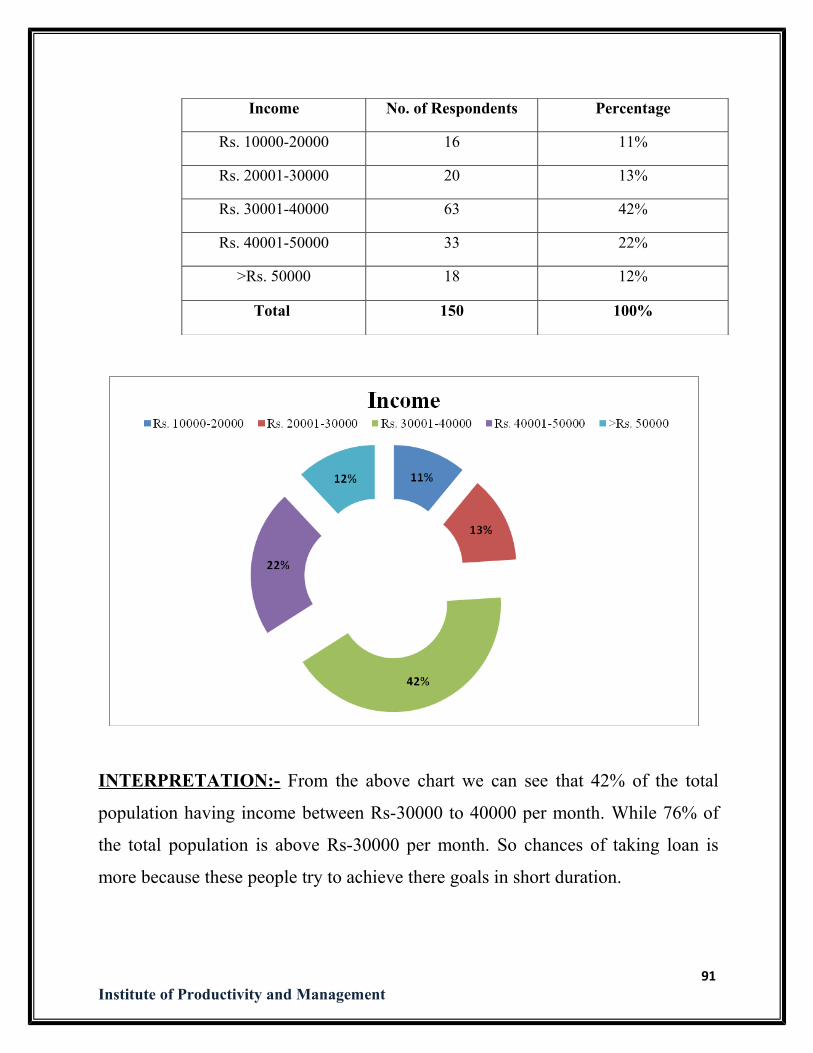

(6) Income?

90Institute of Productivity and Management

Income No. of Respondents Percentage

Rs. 10000-20000 16 11%

Rs. 20001-30000 20 13%

Rs. 30001-40000 63 42%

Rs. 40001-50000 33 22%

>Rs. 50000 18 12%

Total 150 100%

INTERPRETATION:- From the above chart we can see that 42% of the total

population having income between Rs-30000 to 40000 per month. While 76% of

the total population is above Rs-30000 per month. So chances of taking loan is

more because these people try to achieve there goals in short duration.

91Institute of Productivity and Management

(7) Prefer Loan?

Prefer Loan No. of Respondents Percentage

Yes 96 64%

No 54 36%

Total 150 100%

INTERPRETATION:- From the above chart we can see that 64% are ready to take loan or they have taken loan. While 36% do not prefer loan.

92Institute of Productivity and Management

8) Don’t Prefer Loans?

Some People don’t prefer loan because

• Want to achieve their goal by saving their money.

• Not ready to take liability on their shoulder.

• Not ready to pay interest on that amount or extra cost.

• Not ready to waste there time in paper work or any extra work related to

loan.

93Institute of Productivity and Management

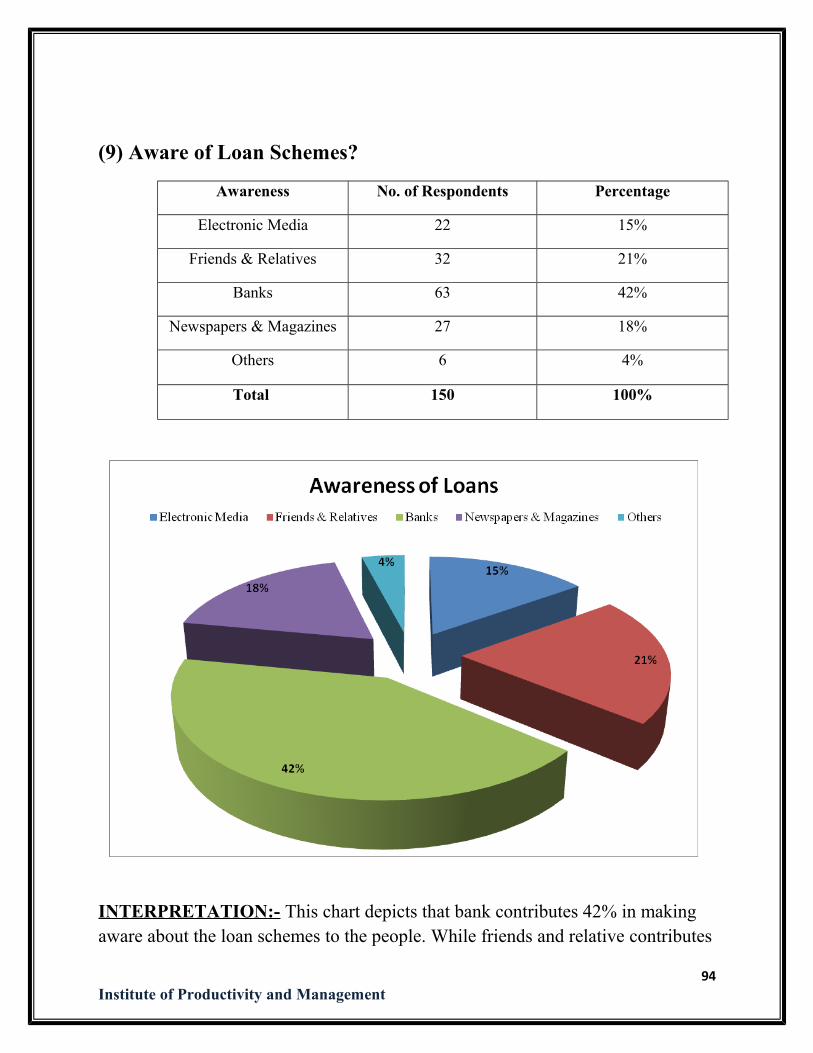

(9) Aware of Loan Schemes?

Awareness No. of Respondents Percentage

Electronic Media 22 15%

Friends & Relatives 32 21%

Banks 63 42%

Newspapers & Magazines 27 18%

Others 6 4%

Total 150 100%

INTERPRETATION:- This chart depicts that bank contributes 42% in making aware about the loan schemes to the people. While friends and relative contributes

94Institute of Productivity and Management

about 21% and news paper & magazines contributes only 18% in making aware about the loans. While electronic media and other sources contributes only 19%.

(10) Other Places Providing Loans?

Places No. of Respondents Percentages

Banks 114 76%

Financial Institutions 30 20%

Others 6 4%

Total 150 100%

INTERPRETATION:- As we know that there are various sources of taking loan but in over survey we found that 76% of the total sample like to prefer loan from

95Institute of Productivity and Management

bank and while 20% would like to take it from financial institutes and only 4% would like to take it from other sources.

(11) Banks that are most preferred by the customers for taking Loans?

Banks No. of Respondents Percentage

HDFC 47 31%

ICICI 40 27%

Kotak Mahindra 15 10%

Mahindra & Mahindra 8 5%

Public Banks 37 25%

Others 3 2%

Total 150 100%

96Institute of Productivity and Management

INTERPRETATION:- This chart depicts that population prefer for taking loan -

31% from HDFC, 27% from ICICI bank, 10% Kotak bank, 5% Mahindra &

Mahindra,25% from public bank, 2% from others.

(12) Frequency of taking Loans?

Frequency No. of Respondents Percentage

Once a year 53 36%

Every two years 35 23%

Three and above 62 41%

Total 150 100%

97Institute of Productivity and Management

INTERPRETATION:- This chart depicts that 41% of the total population would

like to take 3 to 4 time loan in a year it is personal loan which is for short duration.

It can be 15days to 91 days. While 36% percent like to take loan once in a year and

23% would like to take loan once in two year. Interest paid in loan gets tax

deduction in section 24(i).

(13) Interest Rate?

Interest Rate No. of Respondents Percentage

Fixed 40 27%

Floating 65 43%

Special Interest rate schemes 45 30%

Total 150 100%

98Institute of Productivity and Management

INTERPRETATION:- This chart shows that 43% would like to take floating

interest, 27% prefer fixed interest and while 30% prefer special interest rate

scheme on their loans.

(14) Term Loan?

Term No. of Respondents Percentage

Short-term 71 47%

Medium-term 31 21%

Long-term 48 32%

Total 150 100%

99Institute of Productivity and Management

INTERPRETATION:- This chart shows as that 47% prefer short term loan (less than 1year), while 32% prefer long term loan (more than 5 year), 21% prefer medium term loan.

(15) Duration of Payment?

Duration of Payment No. of Respondents Percentage

EMI’s 64 43%

One time Payment 17 11%

NPDC’s 33 22%

Six months installments 21 14%

Three months installments 13 9%

Others 2 1%

Total 150 100%

100Institute of Productivity and Management

INTERPRETATION:- From the above chart we can see that 43% population like

to have EMI facility. While 22% like to have NPDC, 11% prefer onetime payment

system, 14% prefer six months installments system, and 9% prefer three months

installments system, only 1% prefers other modes of making payments. This chart

conclude that maximum number of people prefer installment system.

(16) Customer of HDFC bank?

Customer of HDFC bank No. of Respondents Percentage

Yes 87 58%

No 63 42%

Total 150 100%

101Institute of Productivity and Management

INTERPRETATION:- This chart depicts that 58% are the customers of the bank

while 42% are not the customers of bank but in future they will become the

customer of the bank.

If No, Why?

• Branch is not near to there location.

• They think that private bank charges are higher than public bank.

• Few people have certain fixed mentality that private bank can run any time.

102Institute of Productivity and Management

• Private Banks have very strict rules for loans and account.

(17) Awareness of HDFC Loans?

Awareness of HDFC loans

No. of Respondents Percentage

Yes 108 72%

103Institute of Productivity and Management

No 42 28%

Total 150 100%

INTERPRETATION:- From the above chart we can see that 72% are aware

about different types of loan and schemes that HDFC bank gives. While 28% are

unaware about the loans and schemes that HDFC offers.

If No, Why?

• They are not interested in taking loans

104Institute of Productivity and Management

• They are not interested in taking loan from private banks because they due

to high interest rates.

• Lots of furred can be done with the customers.

• HDFC Bank is not flexible according to the customers need and wants.

(18) Type of Loan?

105Institute of Productivity and Management

Type No. of Respondents Percentage

Two-wheeler 20 13%

Car Loan 29 19%

Gold Loan 3 2%

Commercial-vehicle Loan 15 10%

Personal Loan 12 8%

Educational Loan 17 11%

Working capital finance 6 4%

Home Loan 31 21%

Loan against property 13 9%

Others 4 3%

Total 150 100%

106Institute of Productivity and Management

INTERPRETATION:- This chart depicts that 13% likes two-wheeler loans, 19%

likes car loans, 2% like gold loan, 10% likes commercial-vehicle loan, 8%like

personal loan, 11% likes educational loan, 4% likes working capital loan, 21%

likes home loan, 9% likes loan against property, 3% likes other types of loan.

107Institute of Productivity and Management

(19) Why Customers choose HDFC for taking Loans?

• It is easy to take loan from HDFC bank

• Bank believes on its ethics and commitment.

• Less fraud records with customers.

• Best schemes available.

• Easily convertibility between fixed interests to floating interest.

• Fewer charges charged to the customers in comparison to the other private

banks and financial institutions.

108Institute of Productivity and Management

(20) Factors that customer keep in mind while choosing Loans?

Factors No. of Respondents Percentage

A trusted name 27 18%

Accessibility 19 13%

Easy policies 48 32%

Friendly services & responsiveness

56 37%

Total 150 100%

INTERPRETATION:- This chart shows that 18% believes on trust name, 13%

believes on accessibility 32% believes on policies and 37% believes on friendly

services and responsiveness.

109Institute of Productivity and Management

(21) Timely giving information regarding change in services & interest rate on certain policies?

Information No. of Respondents Percentage

Timely information given 106 71%

Not updated 44 29%

Total 150 100%

INTERPRETATION:- This chart shows that 71% are happy that they are

informed timely about the changes made in their loan contracts. While due some

problems 29% are not been able to get properly informed about the changes in

their loan contracts.

110Institute of Productivity and Management

(22) Satisfaction of customers?

Satisfaction of customers No. of Respondents Percentage

Highly satisfied 64 43%

Satisfied 54 36%

Dissatisfied 17 11%

Highly dissatisfied 11 7%

Can’t say 4 3%

Total 150 100%

INTERPRETATION:- This chart depicts 43% customers are highly satisfied,

36% are satisfied, 11% are dissatisfied, 7% are highly dissatisfied and 3% are

average it means they can’t say any.

111Institute of Productivity and Management

Conclusion

The project opportunities provided was market segmentation and identifying prospective

customers in potential geographical location and convincing them to take loan so that new

business opportunities of the bank can be explored. Through this project, it could be concluded

that people are not much aware about the various products of the bank.

As we know that HDFC bank is the oldest and number one bank in giving loan. As the survey

was done in Bareilly I have found that age above 31 are the most loan takers because they want

to fulfill there life goals in less time and they prefer floating rate of interest and they also prefer

EMI facility for paying back the loan. There are various other people who are ready for taking

loan but they need some awareness from the bank. The bank provides various types of loans

according to the needs of the customers. Bank should conduct some seminars, contest, etc for

making aware about the different types of loans, special interest rate schemes and some exciting

offers. This will help the bank in increasing customers and creating the good relationship with

existing customers.

So, at last the conclusion is that there is tough competition ahead for the company from its

major competitors in the banking sector.

Last but not the least I would like to thank HDFC Bank for giving me an opportunity to work in

the field of Finance. I hope the company finds my analysis relevant.

112Institute of Productivity and Management

Suggestions

Finally some recommendations for the bank are as fallows:-

To make people aware about the benefit of becoming HDFC Bank’s Customer following

activities of advertisement should be done through:

• Print Media.

• Hoarding & Banners.

• Stalls in Trade Fares

• Distribution of leaflets containing details information.

Minimum balance for savings account should be reduced from Rs 5000, so that people

who are not financially strong enough can maintain their account properly.

Make people understand about the various benefits of its products by conducting some

seminars.

Bank should organize the program in the society, so that people will be aware about the

bank and different products of the bank.

It should maintain the image of transparency and should also create trust among all the

present customers.

The younger people of age group <=30 will be a key new customer group into the

future, so making greater efforts with these people who show some interest in

various schemes in banks.

Launch innovative schemes in the market to attract the customers.

113Institute of Productivity and Management

Questionnaire

Q1) Age group?

A) <=30 yrs B) 31-35 yrs C) 36-40 yrs

D) 41-45 yrs E) 45-50 yrs F) >50 yrs

Q2) Gender?

A) Male B) Female

Q3) Marital status?

A) Single B) Married

Q4) What is your Occupation/Profession?

A) Businessman B) Govt. service C) Private sector

D) Student E) Professionals F) Agriculture

G) others

Q5) What is your Educational Qualification?

A) Graduation/PG B) Under Graduate C) Others

Q6) What is your income?

A) Rs.10000-20000 B) Rs. 20001-30000 C) Rs. 30001-40000D) Rs.40001-50000 E) >Rs. 50000

Q7) Do you prefer loan?

A) Yes B) NoQ8) Why don’t you prefer Loan?

Q9) How you get aware about various Loan Schemes?

A) Electronic Media B) Friends & Relatives C) Banks

114Institute of Productivity and Management

D) Newspapers & Magazines E) Others

Q10) From where do you prefer to take Loan?

A) Banks B) Financial Institutions C) Others

Q11) Which Bank you prefer taking loan from?

A) HDFC B) ICICI C) Kotak Mahindra D) Mahindra & Mahindra E) Public Banks F) Others

Q12) Frequency of taking Loans?

A) Once a year B) every two-three years C) three & above year

Q13) Which interest rate do you prefer taking?

A) Fixed B) Floating C)special interest rate Scheme

Q14) Which term of loan you prefer?

A) Short-term B) Medium-term C) Long-term

Q15) Which is preferable duration for payment?

A) EMI’s B) one time payment C) NPDC’s D) six months installments E) three months installments

F) Others

Q16) Are you customer of HDFC?

A) Yes B) No

If No than why?

Q17) Are you aware of HDFC Loans?

115Institute of Productivity and Management

A) Yes B) No

If No than why?

Q18) Which type of loan you have taken from HDFC/ planning to take?

A) Two-wheeler Loan B) Car loan C) Gold loan D) Commercial vehicle loan E) Personal loan F) Educational Loan

G) Working capital finance H) Home loan I) Loan against Property

J) Others

Q19) Why you have chosen HDFC for taking Loans?

Q20) Factors that you keep in mind while choosing the loan?

A) A trusted name B) Accessibility C) Easy PoliciesD) Friendly services & responsiveness

Q21) Timely giving information regarding change in services & interest rate on certain policies?

A) Timely information given B) Not updated

Q22) Are you satisfied with the bank/loan you have chosen?

A) Highly satisfied B) satisfied C) DissatisfiedD) Highly dissatisfied E) Can’t say

Name:-________________________

116Institute of Productivity and Management

Annexure

117Institute of Productivity and Management

Bibliography

Books:

• Marketing Research & Research Methodology: - C.R. Kothari.