42

Four Pillars to Retirement Kehoe Financial Adviso rs October 1, 2014

| Date post: | 29-Dec-2015 |

| Category: |

Documents |

| Upload: | maria-powell |

| View: | 225 times |

| Download: | 1 times |

Four Pillars to Retirement

Kehoe Financial Advisors

October 1, 2014

Steve Kehoe

Social Security

1. PastInceptionAugust 14, 1935 President Franklin Delano Roosevelt signed the Social Security Act into law.

ObjectiveThree “R”s:

1. Relief for the poor2. Recovery of the

economy3. Reform of the financial

system to prevent future depressions

2. PresentEligibility

Anyone who is:aged (age 65 or older);blind; ordisabled.

And, who:has limited income; andhas limited resources; andis a U.S. citizen or national, or in one

of certain categories of aliens

Review Social Security Statement

3. FutureA. Life Expectancy of 65

male:1940 = 77.7 years old2009 = 82.5 years old

B. Life Expectancy of 65 female:

1940 = 79.7 years old2009 = 85.2 years old

1940 1950 1960 1970 1980 1990 2000 200960

65

70

75

80

85

90

79.781.2

82.483.6 84.1 84.6 84.7 85.2

77.7 78.1 78.2 78.879.6 80.3 81

82.5

Life Expectancy at 65 years old vs. the Social Security Retirement Age

*

Female MaleRetirement Age

*Source: Center for Disease Control and Prevention,http://www.cdc.gov/mchs/hus/contenst2013.htm#018

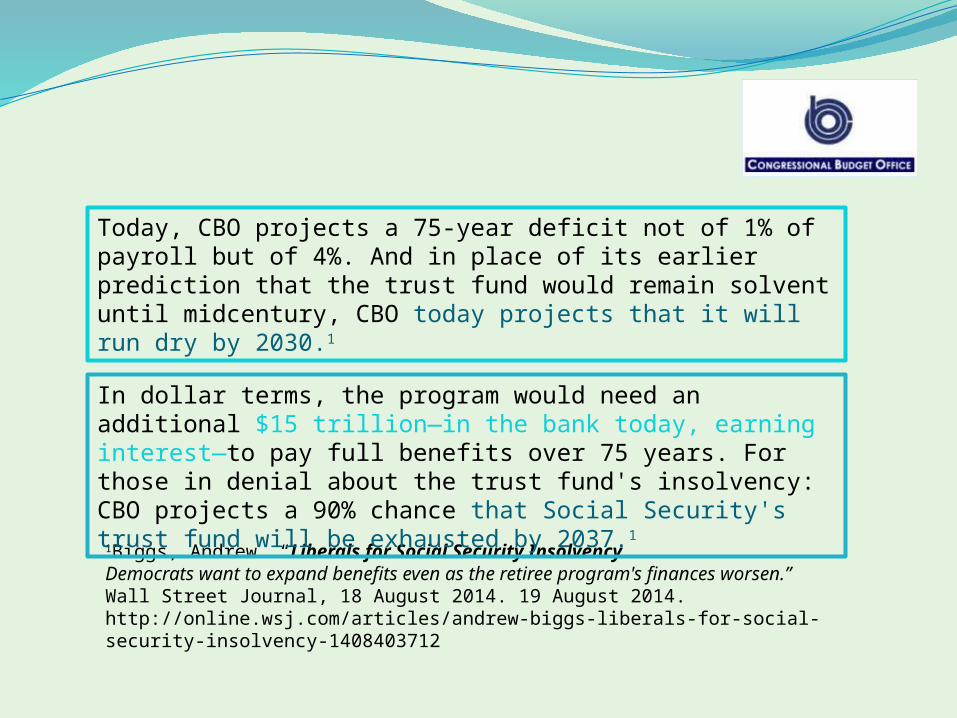

SolvencyOn July 15 the Congressional Budget Office rolled out

updated projections that show a precipitous decline in

Social Security's solvency. The program's 75-year deficit

has nearly quadrupled since 2008, and the trust fund's

exhaustion date has moved forward by nearly 20 years.

Remarkably, the response by progressives is to expand Social

Security's benefits while leaving its multi-trillion-dollar

unfunded obligations largely unaddressed.1

1Biggs, Andrew. “Liberals for Social Security InsolvencyDemocrats want to expand benefits even as the retiree program's finances worsen.” Wall Street Journal, 18 August 2014. 19 August 2014.http://online.wsj.com/articles/andrew-biggs-liberals-for-social-security-insolvency-1408403712

In dollar terms, the program would need an additional $15 trillion—in the bank today, earning interest—to pay full benefits over 75 years. For those in denial about the trust fund's insolvency: CBO projects a 90% chance that Social Security's trust fund will be exhausted by 2037.1

Today, CBO projects a 75-year deficit not of 1% of payroll but of 4%. And in place of its earlier prediction that the trust fund would remain solvent until midcentury, CBO today projects that it will run dry by 2030.1

4. Summary

•Purpose of Social Security

•When to Start Social Security

•Changes to Social Security?

Tom Keller -

Investments

How Do You Invest in Retirement?

• At Retirement move all assets to 60% Stocks & 40% Bonds

• As you grow in retirement years, your allocation shifts from Equities to Bonds.

Past Investment Strategies for Retirement

What About Today?

We are a global economy now.

Interest Rates are at historic lows.

People are living longer.

What has changed the traditional strategy?

What About Today continued:

Markets have been more volatile the past 20 years.

Information is more accessible and creates immediate responses.

What can you do to have a successful Retirement Investment Plan?

Key word is:

Interest Rates will return to average numbers.

The markets

will continue

to be volatile

and patience

is more

important

than ever.

• Create a plan and keep your discipline.

You need to maintain investment earning power.

Larry Blundred

Long-Term Care

Not your typical“night out”

conversation.

Night out with

Donna – Discuss

Long-Term Care

Date Night

1. Those that have been caregivers.

2. Those that currently are caregivers.

3. Those that will be caregivers.

4. Those that will need caregivers.

Rosalynn Carter, 1997

4 Kinds of people

Addressing Long-Term Care

1) Rely Upon Family

2) Self Insure – Rely Upon Assets Accumulated

3) Long-Term Care Insurance

4) Hybrid Long-Term Care Concepts

Why Long-Term Care Matters

1.Provides Dignity Beyond $

2.Protect Assets

3.Helps Reduce Family

Disruption

4.Plans for Care of “Healthy”

Spouse

5.Supports Financial Plan

If you are not planning to rely on family or “self insure” – spending down your own assets to cover future long term care (LTC) expenses LTC insurance can be obtained through different funding instruments:

•Traditional stand-alone long-term care insurance(annual premiums – not fixed) – better known as “indemnity” plan.

Long-Term Care Policies Emergeo Nursing Home “Insurance”

o Mid ’70’s

o Insure Unknowns:

o Learning Curve for Carriers

o Today: Fewer Carriers/Steep Premiums Jumps

L: Longevity H: Our Health

Hybrid Plans EmergeLTC Benefits Funded By:

Non-qualified annuity

Life insurance (whole or universal life)

Qualified funds in traditional IRA (exception: Roth IRA)

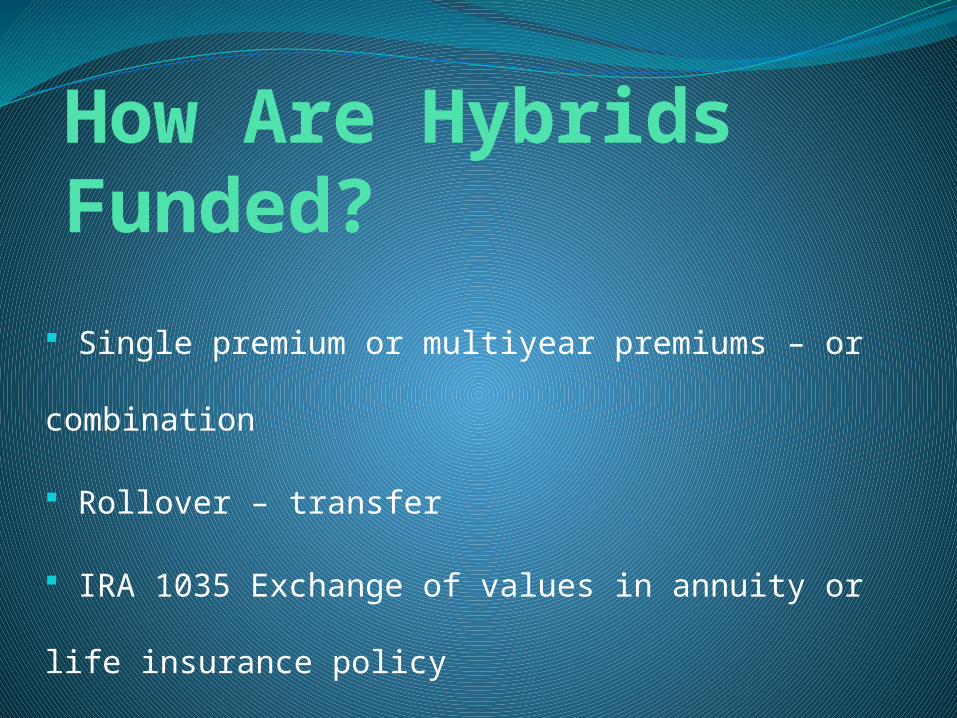

How Are Hybrids Funded?

Single premium or multiyear premiums – or

combination

Rollover – transfer

IRA 1035 Exchange of values in annuity or life

insurance policy

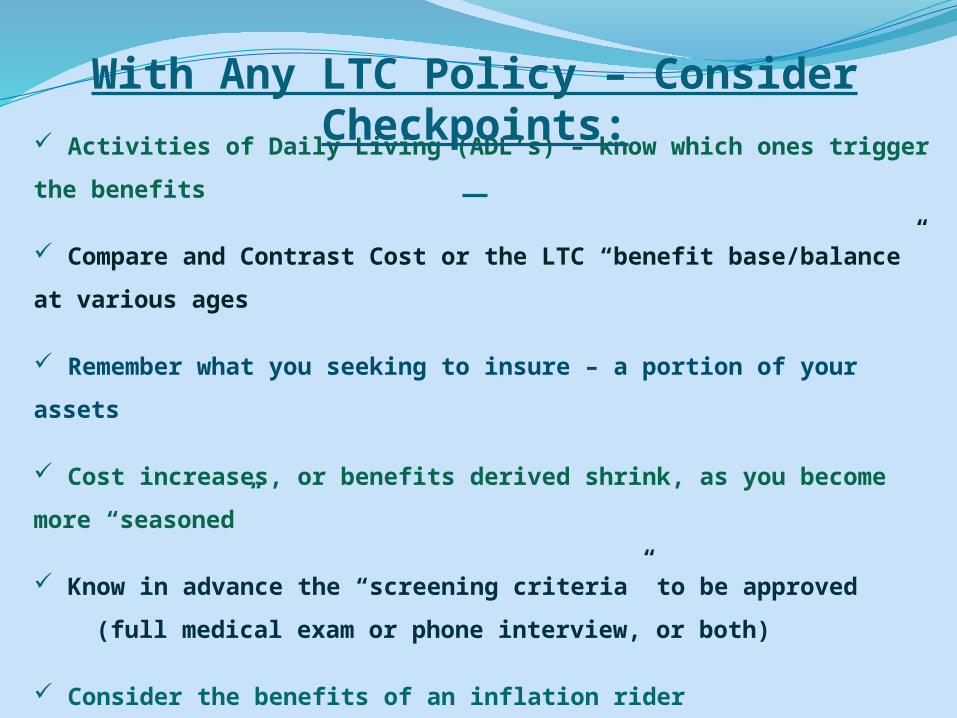

Activities of Daily Living (ADL’s) – know which ones trigger the

benefits

Compare and Contrast Cost or the LTC “benefit base/balance” at

various ages

Remember what you seeking to insure – a portion of your assets

Cost increases, or benefits derived shrink, as you become more

“seasoned”

Know in advance the “screening criteria” to be approved

(full medical exam or phone interview, or both)

Consider the benefits of an inflation rider

With Any LTC Policy – Consider Checkpoints:

Think about “worst case” “best case” scenarios in your

family situation.

Look at family longevity history

Know that LTC and health care costs rise at higher rate

than core inflation.

Know the catches (early surrender penalty … can you

get your premium back if circumstances changed?

More Considerations:

Consider what kind of care is most important to you in

relation to where you are now living, or could consider living

5, 10, 15 or 20 years from now.

Get opinions from people you know and trust, or others that

have purchased or receiving policy benefits.

Take your time. Because you are making a decision based

upon unknowns, explore how the decision and the investment

fits your overall financial plan and situation.

Finally:

Conclusion No “Silver Bullets”

Everyone’s situation and LTC needs are

different

Process – “Plan Centric”

Always Have “Unknowns”

Health Care Issues Remain

Industry Adapts – New Options (Hybrids)

Questions?

Kevin Webb

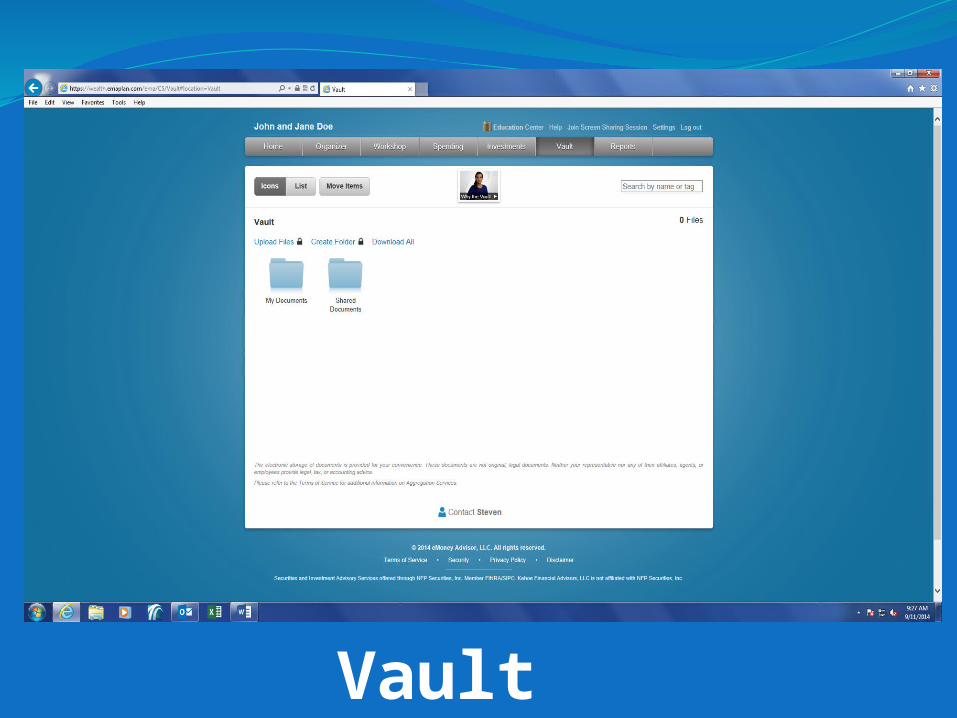

E-Money

Home Page Features

Spending Tab

Investment Tab

Vault Tab

Reports Tab 5 Year Cash Flow

Security:

•Non transactional

•Account locks for 10 minutes after 3 unsuccessful login attempts, blocking programmed hackers information on the site is encrypted with 256-bit encryption, the highest level currently available today

•3rd party sites are hired to try to hack into the software daily

Benefits:

•Saves time by signing on to one website to view all

your financial accounts

•Allows for better decision making by viewing the

interplay of all the accounts together

•Workshops help users follow progress toward

major goals, such as retirement, in real-time

Securities and Investment Advisory Services offered through NFP Advisor Services, LLC (NFPAS), member FINRA/SIPC. NFPAS is not affiliated with Kehoe Financial Advisors.

The Kehoe Team

![1 Copyright © [2005]. Roger L. Costello, Timothy D. Kehoe. All Rights Reserved. REST (Representational State Transfer) Roger L. Costello Timothy D. Kehoe.](https://static.documents.pub/doc/80x56/5514616a550346414e8b592c/1-copyright-2005-roger-l-costello-timothy-d-kehoe-all-rights-reserved-rest-representational-state-transfer-roger-l-costello-timothy-d-kehoe.jpg)

![Kehoe, Rubin, Kehoe, August 29, 2014 - Maryland Judiciarymdcourts.gov/opinions/cosa/2014/0040s13.pdf · “[a] process by which a river or stream shifts its location, causing the](https://static.documents.pub/doc/80x56/5f03ece67e708231d40b72e1/kehoe-rubin-kehoe-august-29-2014-maryland-aoea-process-by-which-a-river.jpg)