96

KESKO CMD 9 JUNE 2015

KESKO CMD9 JUNE 2015

PROGRAM

Our Strategy and Direction Mikko Helander

Changing the Scene: Back to Growth Path Jorma Rauhala

Profitable Growth from Customer Oriented Solutions Terho Kalliokoski

Combining Global Brands With Local Customer Insight Pekka Lahti

What Do You Find When You Google Kesko… Anni Ronkainen

Measuring Success – Kesko’s Financial Targets Jukka Erlund

2

3

OUR STRATEGY AND DIRECTION

MIKKO HELANDER

3

KESKO KEY FIGURES 2014

4

Net sales

Operating profit*

Equity ratio

Liquid assets

Return on capital employed*

Personnel (FTE)

* excl. non-recurring items

€9,071m

€233m

54.5%

€598m

9.9%

19,976

• K-Group’s sales €11.3bn

• 2,000 stores in eight countries

• Over 1.3 million customer visits

every day

• Personnel 45,000

FOR SHOPPING TO BE FUN

5

K-GROUP

KESKO NET SALESBY LINE OF BUSINESS 2014

6

Machinery trade 3%

Car trade 9%

Agricultural trade 4%

Sports trade 2%

Furniture trade 2%

Building and home

improvement trade 25%

Kespro 9%Grocery trade

Russia 1%

Grocery trade

Finland 44%

Grocery trade €4,754m

Home improvement and speciality goods trade €3,000m

Car and machinery trade €1,011m

KESKO NET SALES BY COUNTRY 2014

Russia 4%

Lithuania 4%

Latvia 1%

Finland 82%

Belarus 1%

Estonia 1%

Sweden 2%

Norway 5%

Over 80% of net sales

comes from Finland

7

STABLE PROFITABILITY, POTENTIAL TO IMPROVE

8

0%

1%

2%

3%

4%

5%

0

1

2

3

4

5

6

7

8

9

10

2.9

2010

8.8

3.1

2009

8.4

1.8

2008

9.6

2.3

2007

9.3

3.4

2006

8.5

3.2

2005

7.6

2.8

9.5

2014

9.1

2.6

2013

9.3

2.6

2012

9.7

2.4

2011

Net sales Operating margin, excl. non-rec. items

Net sales, € bn

STRONG OPERATIONAL CASH FLOW

0

50

100

150

200

250

300

350

400

450

500

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

9

€m

VERY STRONG CASH POSITION

• Cash position €598 million at the end of 2014

• Expected cash flow €405 million from real estate arrangement

• Strong cash position enables growth and good dividend yield

10

11

OPERATING ENVIRONMENT AND

MEGATRENDS

11

“BIG PICTURE” IN MACRO

12

• Growth of the world economy slower than before

• USA and China continue as growth drivers

• Slow economic growth in the EU area

• Inflation and interest rates remain low

BUSINESS ENVIRONMENT SLOWLY RECOVERING

Finland

• Decline of purchasing power will level off, but is not expected to improve significantly in the next few years

Skandinavia and the Baltic countries

• Steady economic growth is expected to continue

Belarus

• Consumers’ purchasing power is expected to strengthen, hyperinflation is expected to ease

13

14

OPPORTUNITIES AND RISKS IN RUSSIA

• The world’s richest country in terms of raw

material reserves

• Around 150 million consumers and 13

metropolitan cities

• As yet, political and economical risks are

greater than normal

• The economy has potential for strong growth

as soon as the political situation is normalised

15

RETAIL SALES IN RUSSIA, 2000-2014

Source: PMR Online

0

5000

10000

15000

20000

25000

30000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Non-food products Food, beverages and tobacco

RUB, bn

MEGATRENDS

16

MEGATRENDS

Focused international retailers challenge local players

Consumers have ever better ability to make analytical decisions

Digital services play a key role

Ageing population, urbanisation and single household growth

Responsibility and strong brand increasingly important

17

PORTFOLIO STRATEGY

Grocery trade

• Finland

• Russia

• Kespro, horeca business

Building and home improvement trade

• Europe

Car trade

• Finland

• The Baltic countries, primarily Estonia

18

KESKO STRATEGIC GROWTH AREAS

• Good profitability achieved in all strategic growth areas

• Investments in range of €300 million / year, excluding

potential acquisitions

• Also acquisitions are considered in all three strategic

growth areas

19

INVESTING IN STRATEGICGROWTH AREAS

KEY STRATEGIC OBJECTIVES

20

• Turning the market share in the Finnish grocery trade around

• Increasing the building and home improvement trade in Europe

• Strengthening the market leadership in the Finnish car trade

• The best omni-channel customer experience in the trading sector

• One unified Kesko, harvesting synergies

21

ALL BUSINESSES WILL BE DEVELOPED FURTHER

Shoe trade

• Finland

Sports trade

• Finland and Russia

Furniture trade

• Finland and Estonia

Agricultural trade

• Finland

Machinery trade

• Finland and the Baltic countries

MAXIMISING VALUE CREATION ALSO IN OTHERBUSINESSES

• Important to have the best platform for Kesko’s small and medium sized businesses to succeed in tight competition

• All options which improve competitiveness of other businesses and retailer entrepreneurs are possible

22

REAL ESTATE ARRANGEMENT TO BE CLOSED

• Kesko has agreed to set up a joint real estate investment company with AMF

Pensionsförsäkring and Ilmarinen

• The combined fair value is €652 million and the properties owned by Kesko

Group companies account for €485 million

• Cash flow to Kesko will be around €405 million

• Closing expected to take place in June

23

24

CUSTOMER AND QUALITY –

IN EVERYTHING WE DO

24

25

GROCERY TRADE

CHANGING THE SCENE: BACK TO GROWTH PATH

JORMA RAUHALA

KESKO – QUALITY LEADER IN GROCERY

• High market share of 33% in Finland

• New customer focused strategy clearly differentiates

Kesko in the market

• already improving market share development

• Steady and strong operating profit and cash flow

• Successful business concept in Russia

• Kesko is the most responsible food retailer in the world

26

KESKO GROCERY TRADE KEY FIGURES IN 2014

27

Kespro 17%

Grocery trade

Finland 81%

Grocery trade

Russia 2%Net sales €4,754m

Operating profit €223m

Operating margin 4.7%

ROCE 22.2%

28

FINNISH GROCERY

TRADE MARKET

K-group 33.1%

Others 6.8%Suomen

Lähikauppa

6.8%

Lidl 7.6%

S-group 45.7%

Source: Nielsen

NO MAJOR CHANGES IN K-FOOD STORES’ MARKET SHARE IN 2005 – 2014

33.9 33.4 33.9 33.7 34.2 35.0 35.3 34.7 34.0 33.1

0

5

10

15

20

25

30

35

40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

29

%

Source: Nielsen

CHANGES IN THE FINNISHGROCERY TRADE MARKET

30

Quality and responsibility matters

Value for money due to weakenedpurchasing power

Servicing customers digitally

30

CUSTOMER AND QUALITY –

IN EVERYTHING WE DO

3131

STRATEGIC OBJECTIVES OF THE GROCERY TRADE

• Turning the market share in the Finnish grocery trade around

• Further improving quality and service level

• Investments to improve the K-supermarket and K-market store network

• Customer focused renewal of the K-citymarket concept

• Improving price competitiveness and price image

• Offering leading digital services in grocery

• Developed retailer business model

32

K-CITYMARKET

• The whole K-citymarket concept will be renewed and the

stores will be tailored to meet local customer needs

• In food, superiority factors are freshness, quality and

Finnish products

• Focused selection in the home and speciality goods

• Attractive partnerships including

Starbucks, Posti and K-rauta Express…

33

”Best store for the family”

K-SUPERMARKET

• ”Best in food” – tailored offering based on local customer

demand

• Opening 30 new K-supermarkets

• Focus in quality – freshness, Finnish origin, local

products, service, diversification of food culture

34

”Best in food”

K-MARKET

• Three different formats:

”Express”, ”City” and ”Province”

• Comprehensive renewal of the existing network

• Opening 100 new neighbourhood stores

• Expansion of new service station store concept jointly

with Neste

35

”Most service oriented neighbourhood store”

3636

• Will be based on international benchmark and best practices

• Totally different compared to current food stores in Finland

• Ease of shopping, freshness and quality are at the core of the new concept

LAUNCH OF A NEW STORE CONCEPT TO THE FINNISH GROCERY MARKET

• Changing pricing models

• Enhancing sourcing

• Increasing the share of private labels

IMPROVING OUR PRICE COMPETITIVENESS AND PRICE IMAGE

37

NUMBER ONE IN DIGITAL SERVICESIN THE GROCERY TRADE

• Targeted and personalised marketing

• Customer oriented mobile services

• Our target is a 40% market share in the online

food trade

• Already now Click & Collect service and

home delivery

• Continuously looking for new

innovative solutions

3838

39

RETAILER BUSINESS MODEL IS OUR SUCCESS FACTOR

• Retailers to develop selections and services

based on local needs

• Successful retailers to run more than one

store in the future

• New retailer model for smaller stores

STRATEGY FOR RUSSIA

• Increasing operations and improving profitability

in the St. Petersburg area

• Active in acquiring store sites

• K-ruoka is the best food store in the St. Petersburg area

• Identifying new growth possibilities in the Moscow area

and possibly in other metropolitan cities in Russia

40

41

INCREASING THEHORECA BUSINESS

• Organic growth through strong international cooperation

• Differentiating the selection with private label products

• Supporting the service counter offering of the K-food stores

• Searching for expansion alternatives in Finland and the

neighbouring areas

WE WANT TO OFFER OUR CUSTOMERS FOOD THAT IS BOTH AFFORDABLE

AND OF GOOD QUALITY

#SEKÄETTÄ

42

43

BUILDING AND HOME IMPROVEMENT TRADE

PROFITABLE GROWTH FROM CUSTOMER ORIENTED

SOLUTIONS

TERHO KALLIOKOSKI

PROFITABLE GROWTH IN BUILDING AND HOME IMPROVEMENT TRADE

• Market share in Finland over 40%

• Market #1 or #2 in Finland, Norway,

Estonia, Latvia, Lithuania and

Belarus

• Eight consecutive quarters of

improving profitability

• Strong position in B-2-B trade –

#1 in Finland, Norway and Estonia

44

0

10

20

30

40

50

60

70

2012 2013 2014

Operating profit, € million

45

300 STORES IN EIGHTCOUNTRIES

Finland€1,190m138 stores

Sweden€197m

20 stores

Norway€671m

82 stores

Russia€250m

13 stores

Belarus€125m

11 stores

Lithuania€317m

19 stores

Latvia€53m

8 stores

Estonia78 M€

8 stores

TOTAL RETAIL SALES€2,881m

46

MARKET SHARES %Belarus

€125m 6%

Russia

€250m 11%Finland

€791m 35%

Scandinavia

€625m 28%

Baltics

€443m 20%

65% OF THE BUILDING AND HOME IMPROVEMENTNET SALES COMES FROM OUTSIDE OF FINLAND

6

17

23

14

30

7

10

40

%

STRATEGIC OBJECTIVES OF THE BUILDING AND HOME IMPROVEMENT TRADE

47

• Kesko #5 in Europe – strong potential for further growth organically or

through acquisitions

• Providing excellent services from the same store network to the three

different customer segments

• A common core for all countries to ensure efficient operations

• Offering the best omni-channel digital services

ALL THREE CUSTOMER SEGMENTS ARE SERVED THROUGH THE SAME STORE NETWORK

48

Easy solutions and wide product range for each customer segments

Consumer customers

Project customers

Business customers

A COMMON CORE FOR ALL COUNTRIES TO ENSURE EFFICIENT OPERATIONS

• A common core selection at stores, which is complemented according local

customer needs

• Common operating processes, store operating models and management

practices

• Closer collaboration with international suppliers

• Increasing the proportion of own brands

• Utilizing Kesko’s entire purchasing power

49

NUMBER ONE IN DIGITAL SERVICES

• The best digital services for each customer group

• Easy to find products, extensive planning features and easy omni-channel shopping

• All stores will offer Click&Collect service

• 82 K-rauta and Rautia stores already implemented in Finland

• 20 K-rauta stores in Sweden

• Kesko's building and home improvement online store

50

51

NEW CUSTOMER ORIENTED CONCEPTS

51

NEW K-RAUTA EXPRESS CONCEPT

• A concept for locations with large flows of customers to offer fast and

easy shopping

• Satellite store in a shopping centre, city centre or in connection with a

K-citymarket

• The first store to open in August at the Forum shopping centre in

Helsinki

52

NEW CELLO HOME & SEASONCONCEPT

• Increasing the attractiveness of the K-rauta chain

• The concept will offer inspiring home

improvement and seasonal products

• The concept is built around the Cello brand

53

KESKO BUILDING AND HOME IMPROVEMENT ONLINE STORE

54

• The changing market situation demands also a pure play online store

• Comprehensive assortment for home and family needs across chain

boundaries. Kesko's product offering as well as partnerships

• The cornerstones are

• the building and home improvement trade product lines

• the store network as collection points

FOR SHOPPINGTO BE FUN

55

56

CAR TRADE

COMBINING GLOBAL BRANDS WITH LOCAL CUSTOMER INSIGHT

PEKKA LAHTI

THE CAR TRADE IS ONE OF KESKO’S THREESTRATEGIC GROWTH AREAS

• VV-Auto’s market share in the Finnish passenger car and van trade

has risen from 15% to 21% within ten years

• Throughout recent years, Volkswagen has been the best selling car

brand in Finland and Audi has been number one in its competitive

segment

• VV-Auto’s retail net sales have quadrupled within ten years from 100

million to 400 million

• VV-Auto’s profitability has remained at a good level despite the

difficult market situation

5757

CAR AND MACHINERY TRADE 2014

58

Konekesko

Baltics €96m 9%

VV-Auto

€756m 75%

Konekesko

Finland €161m 16%Net sales €1,011m

Operating profit €30m

Operating margin 2.9%

ROCE 18.3%

Car trade operating profit €30 million, 4.0%

Volkswagen 12.3%

Toyota 11.9%

Skoda 9.2%

Volvo 7.3%

Ford 7.0%

Nissan 6.1%

Audi 6.0%

Kia 5.7%

Seat 1.7%

Others 32.8%

PASSENGER CAR MARKET IN FINLAND

59

• Average CO2 emissions of passengercars in 2014: 128 g/km

• Diesel cars 40%, petrol cars 60%

• Only 200 electric cars

• Golf segment 50% of total market

• Increasing segment, SUV 20%of total market

• Average age of registered carsin Finland 13.5 years

Market Share in 2014

Source: TraFi (Finnish Transport Safety Agency)

PASSENGER CARS, FIRST REGISTRATIONS

0

20000

40000

60000

80000

100000

120000

140000

160000

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

60

Source: TraFi (Finnish Transport Safety Agency)

61

STRATEGIC OBJECTIVES OF THE CAR TRADE

• Co-operation with Volkswagen AG: Volkswagen aims to be the biggest car

manufacturer by 2018. Volkswagen is the biggest R&D investor in the world

• VV-Auto will focus on Volkswagen Group's car brands

• Sales growth and growing market share in Finland and in the Baltics

• Increasing retail sales by investing in new sales and service channels

• Developing customer loyalty with new finance and service models

• The best omnichannel customer experience in car trade

62

LOCAL CUSTOMERINSIGHT CASES

62

CASE AUDI: LOCAL INSIGHT AND CUSTOMER LOYALTY PROGRAMS BRING RESULTS

63

• CRM marketing increases customer loyalty

and brings more sales

• CRM marketing is automated and

systematised messages sent to customers

during customer life cycle

• Customers that were targeted by Audi CRM

marketing had substantially higher repurchase

likelihood

87% higher

repurchase

likelihood

CASE: SERVICE ONLINE BOOKING CREATINGCUSTOMER VALUE

64

• Online vehicle authentication produces matching

service packages and prices according to the

vehicle’s service history, maintenance program

and kilometers

• Results after beta phase:

• 15% of the bookings coming online

• 20% of the sales is upselling additional services

65

GREAT SUCCESS IN TWO DIFFERENTU.S. BASED CRM AWARDS

September 2014: Infor Excellence in Action Awards – Customer Excellence

November 2014: Loyalty 360 CX Awards – 360 degree Award

THANK YOU

66

What do you find when you Google Kesko?

Anni Ronkainen

“EVERYTHING THAT CAN BE DIGITAL WILL BE.”

Jeff Dachis, Razorfish

THE CHANGED CONSUMER

THE WORLD IS CHANGING AT AN INCREASING SPEEDThe average age of S&P 500 companies has gone from67 to 15 years since 1920

DIGITAL TECHNOLOGYDRIVESTHE CHANGE

10 DEVICESCONNECTED TO THE INTERNET

COMPANIES HAVE TWO OPTIONS:• Make digital technology a competitive advantage

• Make digital technology a competitive disadvatage

IT WILL BE MOREAND MOREDIFFICULT TO REACH YOURCUSTOMERS

CONSUMERS AREABLE TO MAKE VERYANALYTICAL BUYINGDECISIONS

WEBROOMING

VS. SHOWROOMING

360°360°

KESKO’S OBJECTIVE IS TO OFFER BEST CLASSDIGITAL SERVICES

78

OMNI-CHANNEL

CUSTOMER

INTERACTION

INNOVATIVE

E-COMMERCE

SOLUTIONS

TARGETED AND PERSONALISED MARKETING

CUSTOMER

ORIENTED MOBILE

SERVICES

79

CUSTOMER LOYALTY SYSTEM WILL BE REVISED TO MAKE IT EVEN MORE ATTRACTIVE

80

THANK YOU!80

81

MEASURING SUCCESS –FINANCIAL TARGETS

JUKKA ERLUND

81

NET SALES – BACK TO GROWTH

82

0

2000

4000

6000

8000

10000

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Finland Other countries

+5.8%+11.1%

+9.3%+3.3%

-11.9%+3.9%

+7.8% +2.4%-3.8%

€m

-2.6%

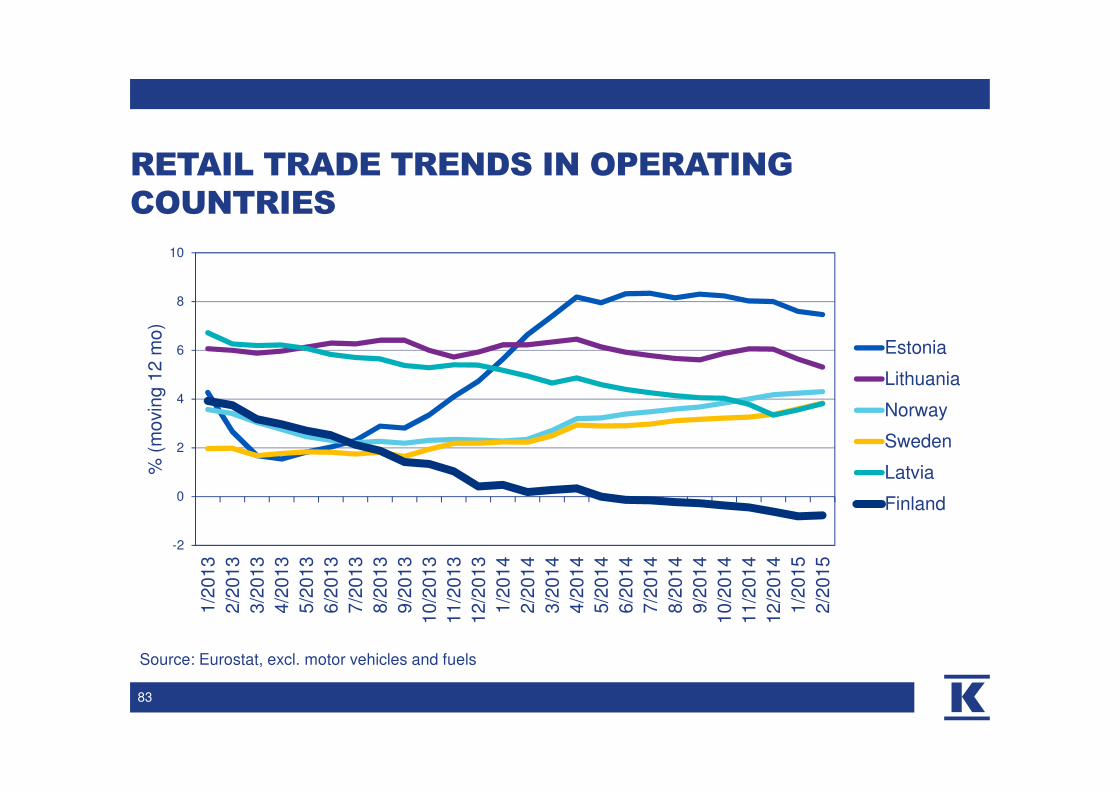

RETAIL TRADE TRENDS IN OPERATING COUNTRIES

5/2015 Jukka Erlund

83

Source: Eurostat, excl. motor vehicles and fuels

-2

0

2

4

6

8

10

1/2

013

2/2

013

3/2

013

4/2

013

5/2

013

6/2

013

7/2

013

8/2

013

9/2

013

10/2

013

11/2

013

12/2

013

1/2

014

2/2

014

3/2

014

4/2

014

5/2

014

6/2

014

7/2

014

8/2

014

9/2

014

10/2

014

11/2

014

12/2

014

1/2

015

2/2

015

% (

movin

g 1

2 m

o)

Estonia

Lithuania

Norway

Sweden

Latvia

Finland

CONSUMER CONFIDENCE IN FINLAND

84

0

2

4

6

8

10

12

14

16

1/0

0

7/0

0

1/0

1

7/0

1

1/0

2

7/0

2

1/0

3

7/0

3

1/0

4

7/0

4

1/0

5

7/0

5

1/0

6

7/0

6

1/0

7

7/0

7

1/0

8

7/0

8

1/0

9

7/0

9

1/1

0

7/1

0

1/1

1

7/1

1

1/1

2

7/1

2

1/1

3

7/1

3

1/1

4

7/1

4

1/1

5

Expectations for own finances

Expectation, 21st century average

Source: Statistics Finland

NET SALES – GROWTH DRIVERS

• Customer focused strategies and concept renewals

• Investments to new store openings

• Customer oriented omni-channel services

• Potential acquisitions in three strategic growth areas

85

213273

315

217155

268 279230 239 233

-100

0

100

200

300

400

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Operating profit excl. non-recurring items Non-recurring items

TARGETING PROFIT IMPROVEMENT

86

€m

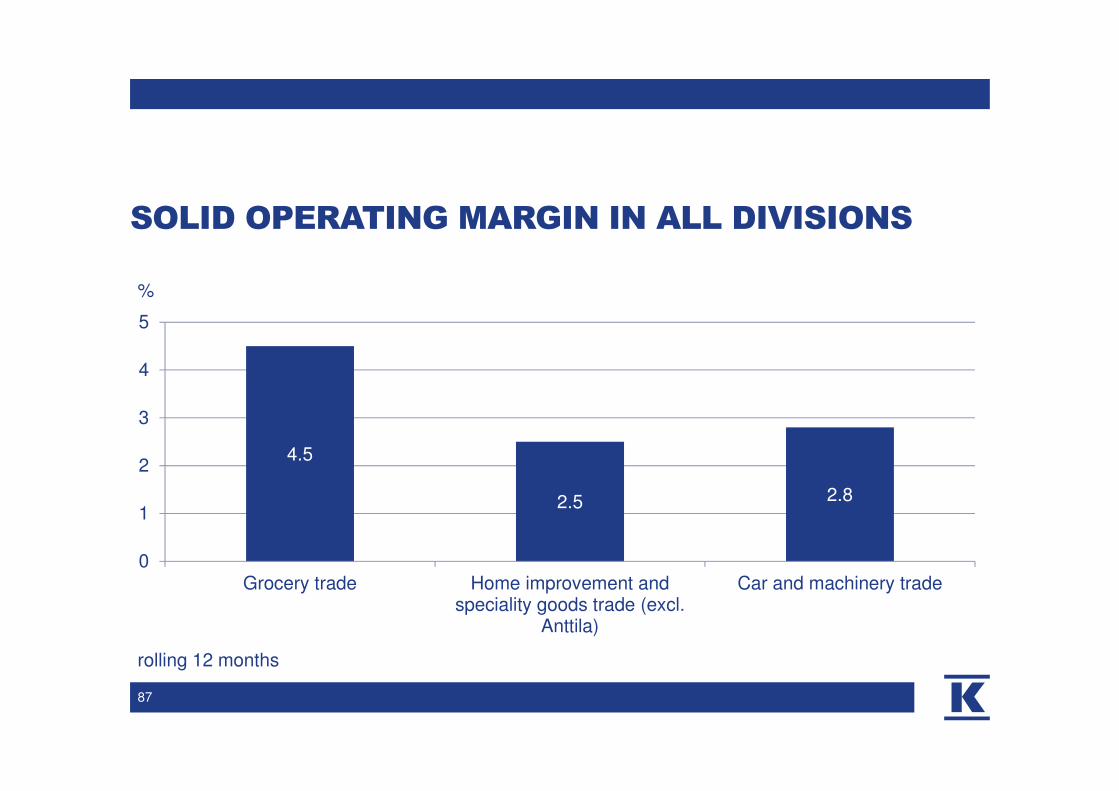

SOLID OPERATING MARGIN IN ALL DIVISIONS

4.5

2.5 2.8

0

1

2

3

4

5

Grocery trade Home improvement andspeciality goods trade (excl.

Anttila)

Car and machinery trade

87

%

rolling 12 months

IMPROVING PROFITABILITY

• Profitable growth in three strategic areas

• Divestment of Anttila

• Improving cost efficiency

• Enhanced sourcing operations

• Efficient support functions and synergies in core processes

• The objective is to achieve cost savings of at least €50 million in

fixed costs by the end of 2016

88

FIXED COSTS, € MILLION

536

494

73

219

125

Personnel costs

Rents and store site costs

ICT-costs

Marketing and loyalty costs

Other costs

89

Total €1,449 million, excl. Anttila

Rolling 12 months, € million

ROCE AND ROEEXCL. NON-RECURRING ITEMS

9.6

12.4

14.7

10.2

7.4

14.013.1

9.09.8 9.9

14.0

10.510.0

14.6

8.1

3.8

8.7 8.8

6.97.7 7.6

12.0

0

2

4

6

8

10

12

14

16

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 target

ROCE ROE

90

0

50

100

150

200

250

300

350

400

450

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Capital expenditure in store sites Acquisitions Other capital expenditure

average

CAPITAL EXPENDITURE BACK TO NORMAL LEVEL

91

€m

• Capex approximately €300 million per annum excluding acquisitions

• Majority of capital expenditure for grocery trade growth

• Itäkeskus shopping centre, €100 million

• Growth investments also in building and home improvement trade

and car trade

92

CAPITAL EXPENDITURE

FINANCIAL TARGETS

• Return on capital employed 14%

• Return on equity 12%

• Interest bearing net liabilities / EBITDA < 2.5

93

DIVIDEND HISTORY

1.10

1.501.60

1.00 0.90

1.301.20 1.20

1.401.50

0

1

2

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

94

€

DIVIDEND POLICY UNCHANGED

5/2015

95

• Kesko Corporation distributes at least 50% of its earnings per share

excluding non-recurring items as dividends, taking however the

company's financial position and operating strategy into account

• Currently balance sheet is overly strong and is targeted to be more

efficient

• BoD’s will make the dividend proposal for the AGM taking into account

the progress of strategy implementation

96