41

The Seven Mistakes Women Make In Their Financial Planning Presented by: Joni Lindquist, MBA, CFP® KHC Wealth Management www.makinglifecount.com www.kcfinancialplanning.com

| Date post: | 15-Aug-2015 |

| Category: |

Documents |

| Upload: | joni-lindquist-mba |

| View: | 96 times |

| Download: | 3 times |

The Seven Mistakes Women Make In Their Financial Planning

Presented by: Joni Lindquist, MBA, CFP® KHC Wealth Management

www.makinglifecount.com www.kcfinancialplanning.com

Women and Money Series: Women, Work and Money Recap

Women have made strides in education levels; still trail in earnings Career interruptions, hours worked and the challenge of

work-life balance Women’s social capital not as strong Women tend not to negotiate as effectively Women need to view their human capital as critical

asset

Goal = Financial Independence

Human Capital

Financial Capital

Personal Wealth

Women at Greater Risk of Not Achieving A Financially Secure Retirement

Key Contributing Factors:

More likely than men to be single parents More likely to handle children and/or parent care-taking A high percentage of women work part-time Women’s annual income continues to lag behind men’s Women have longer life expectancies – need greater

savings

The Seven Mistakes Women Make in their Financial Planning

Don’t have a plan Taking time-outs from work Not saving enough for financial independence Investing without a plan Taking care of others first Not having adequate insurance Assuming will work longer

MISTAKE #1 : LACK OF A PLAN

Don’t Have a Plan Most people do not have a comprehensive plan Less than 1/3 of households (31%) report having a

comprehensive financial plan 44% of households report they are “on track” in saving

for retirement Those who do plan are more likely to feel “very

confident” about money factors – 52% to 32% Fewer women are confident about retirement - only 7%

are “very confident”, compared to 13% of men

Certified Financial Planner Board & Consumer Federation, 2012.

Women and Financial Planning Women are Guessing Their Retirement Savings Needs

59%

21%

6%

4%

4%

2%

3%

40%

29%

12%

5%

7%

3%

4%

Guessed

Estimated based on current living expenses

Completed a worksheet/did calculation

Read/heard that is how much is needed

Expected earnings on investments

Amount given to me by financial advisor

Other

Basis of Estimated Retirement Savings Needs Women Men

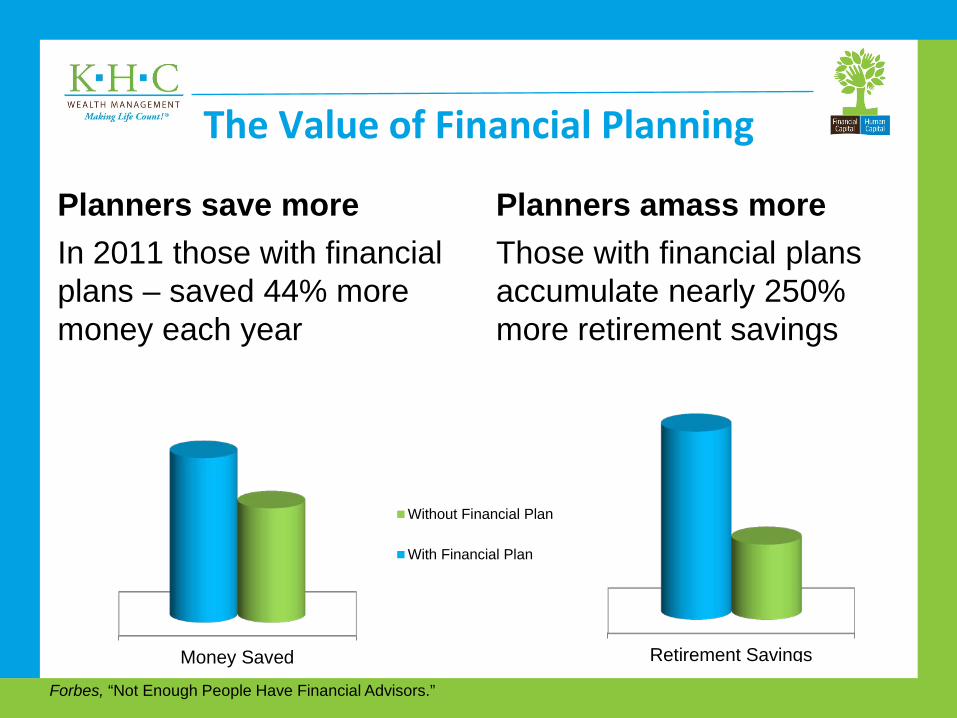

The Value of Financial Planning

The Value of Financial Planning

Planners save more In 2011 those with financial plans – saved 44% more money each year

Planners amass more Those with financial plans accumulate nearly 250% more retirement savings

Money Saved

Without Financial Plan

With Financial Plan

Retirement Savings

Forbes, “Not Enough People Have Financial Advisors.”

MISTAKE #2 : TAKING TIME-OUT FROM WORK

Taking Time-Out from Work

Women more likely to work part-time Career interruptions Less access to employer benefits such as retirement

plans Lower lifetime earnings Lower lifetime earnings lead to lower Social Security

benefits

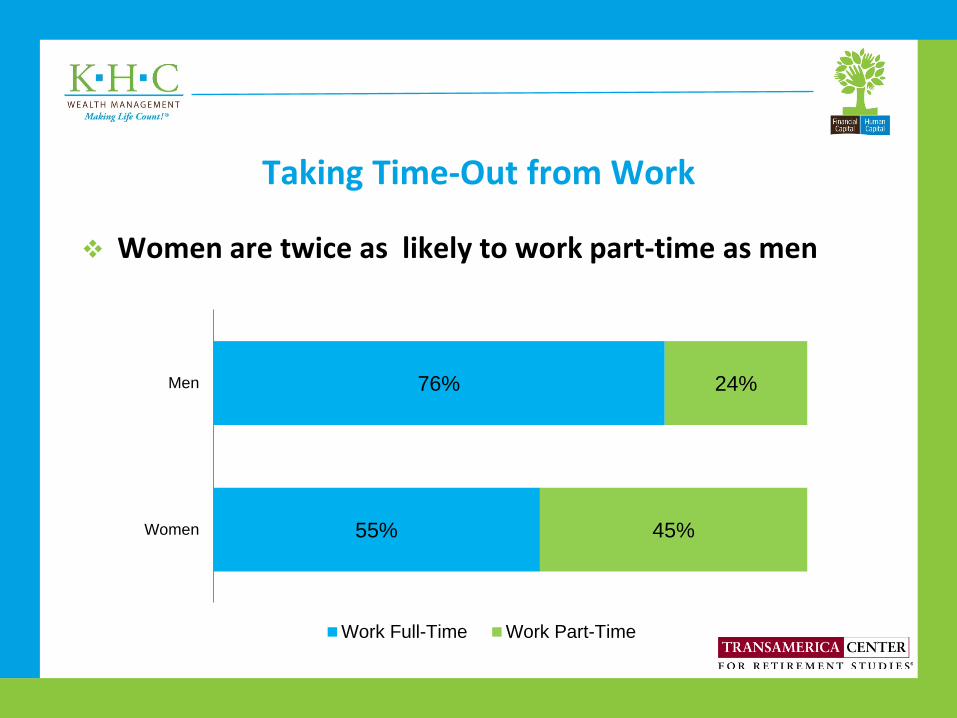

Taking Time-Out from Work

Women are twice as likely to work part-time as men

55%

76%

45%

24%

Women

Men

Work Full-Time Work Part-Time

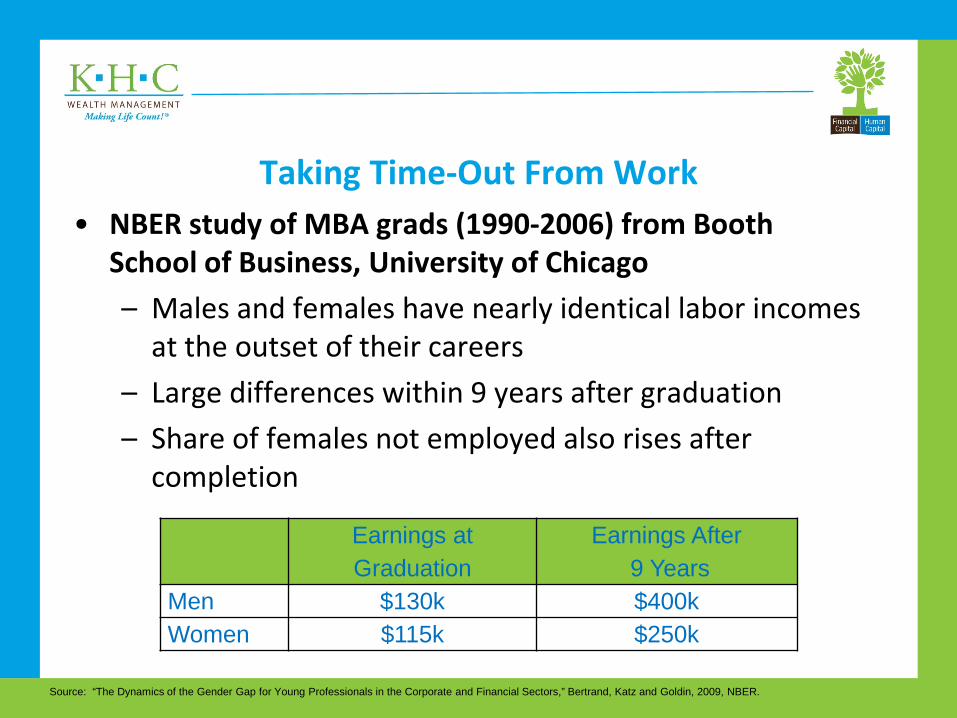

Taking Time-Out From Work • NBER study of MBA grads (1990-2006) from Booth

School of Business, University of Chicago – Males and females have nearly identical labor incomes

at the outset of their careers – Large differences within 9 years after graduation – Share of females not employed also rises after

completion

Earnings at Graduation

Earnings After 9 Years

Men $130k $400k Women $115k $250k

Source: “The Dynamics of the Gender Gap for Young Professionals in the Corporate and Financial Sectors,” Bertrand, Katz and Goldin, 2009, NBER.

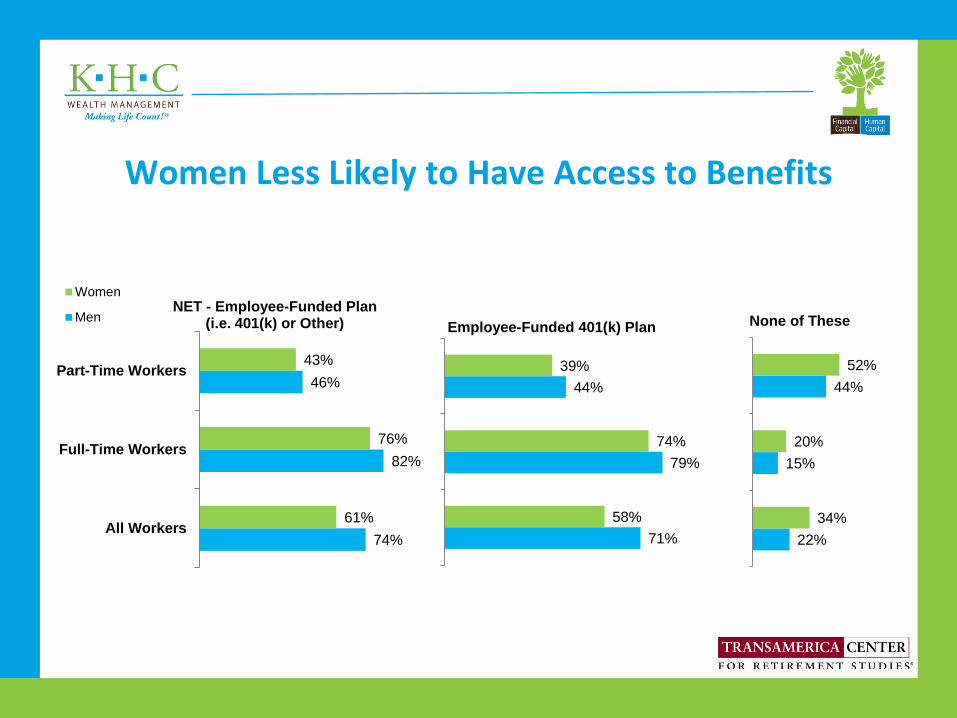

Women Less Likely to Have Access to Benefits

74%

82%

46%

61%

76%

43%

All Workers

Full-Time Workers

Part-Time Workers

NET - Employee-Funded Plan (i.e. 401(k) or Other)

Women

Men

71%

79%

44%

58%

74%

39%

Employee-Funded 401(k) Plan

22%

15%

44%

34%

20%

52%

None of These

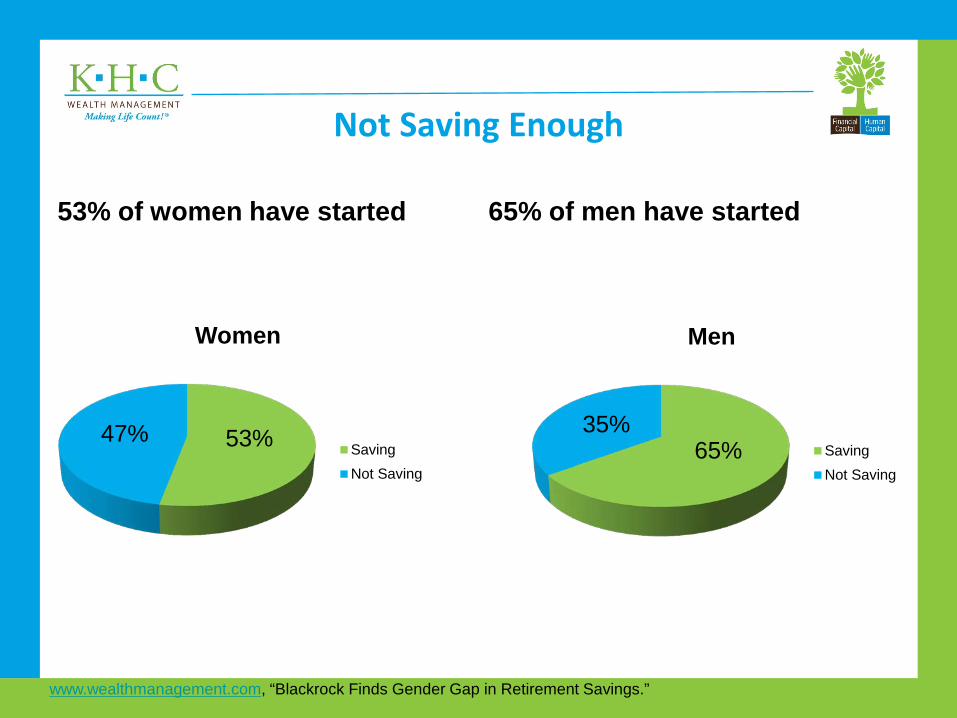

MISTAKE #3 : NOT SAVING ENOUGH

Not Saving Enough

53% of women have started 65% of men have started

53% 47%

Women

SavingNot Saving

65% 35%

Men

SavingNot Saving

www.wealthmanagement.com, “Blackrock Finds Gender Gap in Retirement Savings.”

Women’s Annual 401k Contributions Lag

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

Median Mean

6%

9.3%

8%

9.8%

WomenMen

Women Have Less in Savings

$-

$20,000

$40,000

$60,000

$80,000

$100,000

$120,000

Age 25-44 Age 54-65

$34,900

$81,300 $76,800

$118,400

WomenMen

MISTAKE #4 : INVESTING WITHOUT A PLAN

Investing without a Plan

An alarming 22% of women do not know how their assets are invested

Nearly 1/3 of women would prefer not to think about retirement investing until later

75% of women feel they do not know as much as they should about retirement planning and investing

Are women more conservative? Who cares – what matters is that the investment strategy tie in with the long-term financial plan

Women’s Investing Behavior

Women tend to trade less – and this may in fact improve their net returns compared to men In one study, men traded 45% more than women and this

reduced men’s returns by an average of 2.65% compared to 1.72% for women

Just over half (52%) of women describe themselves as “very involved” in managing/monitoring their investments

Millennial women appear more active in investing, as 31% describe themselves as active, vs. 15% for baby boomer women

MISTAKE #5 : TAKING CARE OF OTHERS FIRST

Caring for Others First

Women tend to think and plan for others before themselves Women most frequently (26%) cite their single greatest fear

about retirement as not being able to meet the financial needs of their family

An estimated 66% of caregivers are female Many parents focus on saving for college for their children

rather than saving for their own retirement.

Women need to put a priority on retirement planning; there are other options to fund college Grants, loans, scholarships, community/technical colleges

Caretaking Impacts Earnings

Caring for Others First

Care-giving reduces paid working hours for middle-aged women by 41%!

In total the cost of caregiving in lost wages and Social Security benefits equals $324,044

Family Caregiver Alliance, “Women & Caregiving: Facts & Figures.” Updated 2015.

MISTAKE #6 : INADEQUATE INSURANCE

Inadequate Insurance

Life Insurance Lack of coverage – for major bread-winner; for household Under-insured

Disability Insurance

Lack of coverage Under-insured Over-estimating eligibility for Social Security Disability Benefits

Gaps in Life Insurance

The number of people with life insurance dropped to 70% from 78% in 2004 Millennials are less likely to have life insurance than boomers Consumers over-estimate the cost of life insurance

Those with life insurance may be under-insured 40% of Americans with life insurance don’t think they have

enough The average gap is up to $320,000 – need $540,000; only have

$220,000 Work with a financial professional to understand need

Life Insurance and Market Research Association

Lack of Disability Insurance

Disability is much likelier to happen than people expect Just over 25% of today’s 20 year olds will become disabled

before they retire One in eight workers will be disabled for five or more years Over 37 million Americans are classified as disabled in 2012

Yet, most of us (65%) think we have 2% chance or less of

becoming disabled

Council for Disability Awareness

Effect of Not Having Disability Insurance

Disability prevents people from earning a living, creating financial hardship Medical problems contribute to 62% of all personal bankruptcies 65% of Americans say they could not cover normal living

expenses even for a year if employment income lost

Council for Disability Awareness

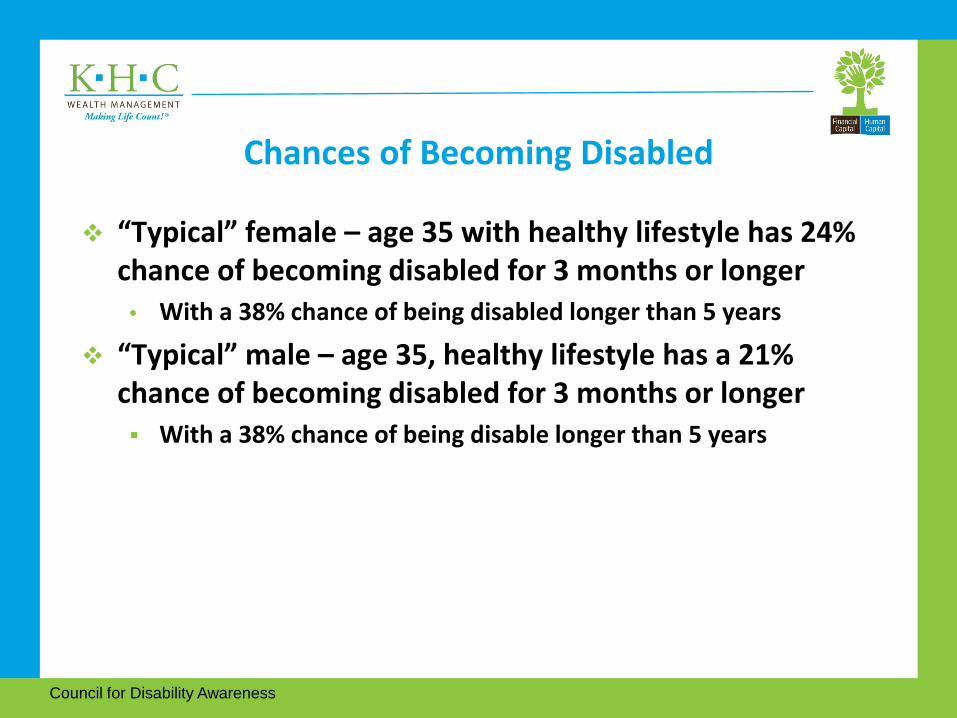

Chances of Becoming Disabled

“Typical” female – age 35 with healthy lifestyle has 24% chance of becoming disabled for 3 months or longer

• With a 38% chance of being disabled longer than 5 years

“Typical” male – age 35, healthy lifestyle has a 21% chance of becoming disabled for 3 months or longer With a 38% chance of being disable longer than 5 years

Council for Disability Awareness

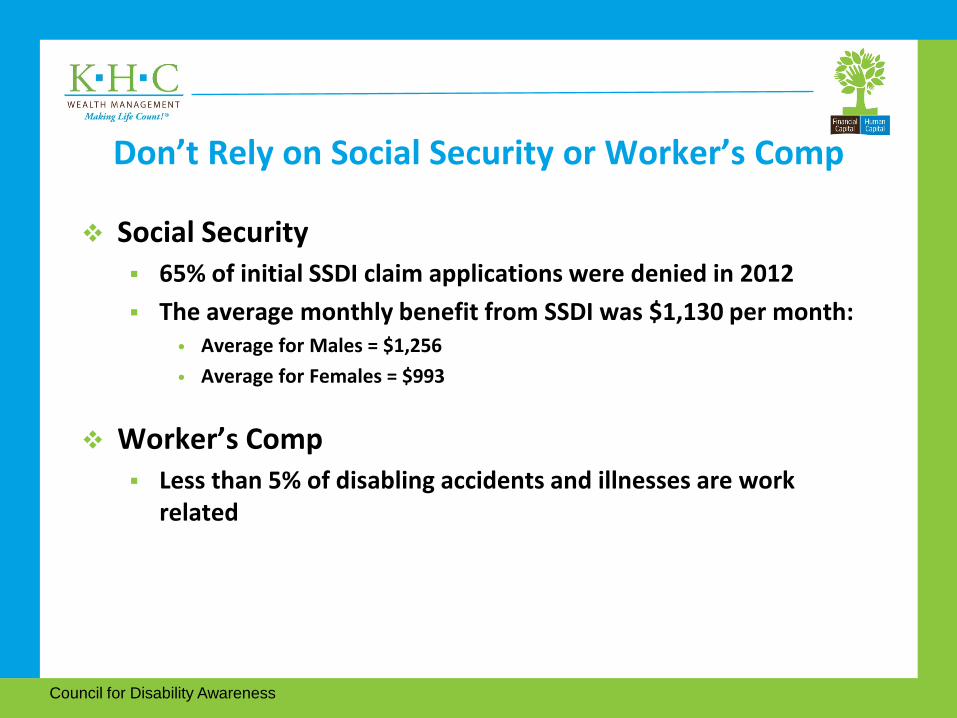

Don’t Rely on Social Security or Worker’s Comp

Social Security 65% of initial SSDI claim applications were denied in 2012 The average monthly benefit from SSDI was $1,130 per month:

• Average for Males = $1,256 • Average for Females = $993

Worker’s Comp Less than 5% of disabling accidents and illnesses are work

related

Council for Disability Awareness

MISTAKE #7: ASSUMING YOU CAN WORK LONGER

Assuming You Will Work Longer

People end up retiring sooner than expected

Finding work after retirement is more difficult than expected

Women don’t have back-up plans

Assuming You Will Work Longer

Nearly half of workers (49%) find themselves retiring sooner than planned

Employee Benefits Research Institute, March 2014.

0%

5%

10%

15%

20%

25%

30%

35%

Before age 60 Between ages60-64

Age 65 Age 66-69 Age 70 & older

9%

18%

23%

11%

22%

35%

32%

11%

7% 9%

Workers planning to retire

Workers actually retiring

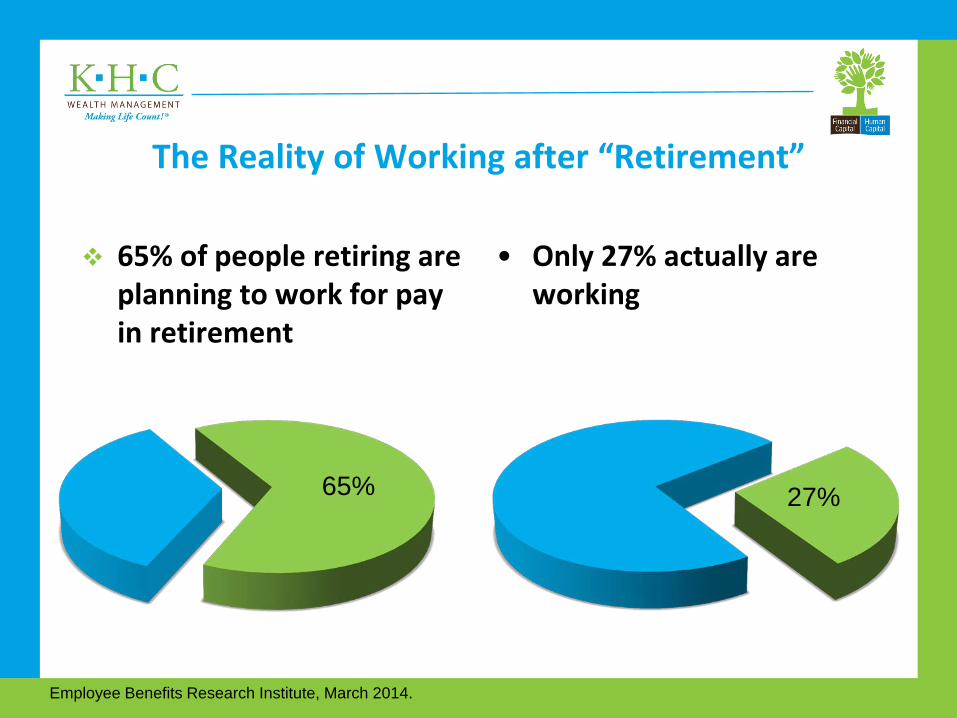

The Reality of Working after “Retirement”

65% of people retiring are planning to work for pay in retirement

• Only 27% actually are working

Employee Benefits Research Institute, March 2014.

65% 27%

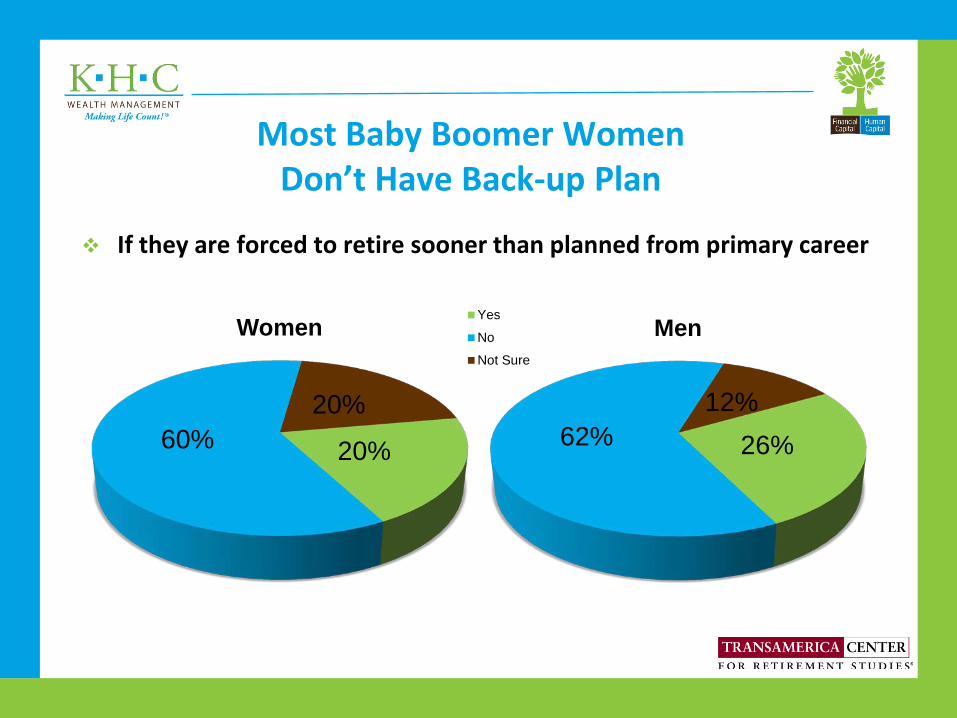

Most Baby Boomer Women Don’t Have Back-up Plan

If they are forced to retire sooner than planned from primary career

20% 60% 20%

Women

26% 62% 12%

Men Yes

No

Not Sure

SEVEN TIPS TO DEVELOP A SUCCESSFUL FINANCIAL PLAN

Seven Tips for Developing a Successful Plan 1) Develop a written plan – don’t guess!

Work with a Certified Financial Planner (CFP®) practitioner Clarify goals, take action, monitor Adjust as life changes

2) When making decisions about reducing work hours, understand and plan for the financial trade-offs

Adjust goals, prioritize Build expense plans

3) Within your plan, set savings target and save at this level

Seven Tips for Developing a Successful Plan

4) If employer has retirement plan, participate. Make retirement a priority over college funding.

There are other ways to pay for college; there are no other ways to pay for retirement

5) Get engaged and educated about investments

6) Ensure you have adequate life and disability insurance

7) Have a backup plan