16

INSIGHTS Know Your Market The UK Retail Edible Rapeseed Oil Category March 2013

INSIGHTS

Know Your Market

The UK Retail Edible Rapeseed Oil Category

March 2013

Edible Oils – The Market Landscape

Who buys Rapeseed Oil ?

Rapeseed Oil uses

UK Grocery overview of Rapeseed Oil

Market Data Summary – UK & Scotland

Summary & Recommendations

Foreword

3

The Rapeseed industry has expanded dramatically since the first Scottish oil brand was

launched in 2008. According to the Home Grown Cereal Association Survey, around

37,000 hectares in Scotland were sown with rapeseed in 2012, up about 6% on the

previous year. Scotland’s climate helps deliver quality Rapeseed crops with consistently

high yields at a time when other countries have been suffering due to harsh winter

climates.

With at least eight oil brands being produced from rapeseed in Scotland, mostly in the

North and East with the latest launch originating from the Isle of Arran, understanding the

market size and its dynamics is important when determining the commercial opportunity.

As the market matures, providing category and consumer insight will be essential in order

to convince retail buyers of how Rapeseed Oil can maximise return on their shelf space.

This report, from Scotland Food & Drink’s INSIGHTS team, supported by Scottish

Enterprise and Highlands & Islands Enterprise, provides an overview of the Oils market

and determines the market opportunity for the growing number of Scotland’s Rapeseed Oil

manufacturers and prospective category entrants. The data available is weighted towards

Multiple Retailers, therefore does not capture speciality outlets, farm shops and Farmers

Markets. However this research does provides a robust overview of the market and

INSIGHTS estimate that this overview is representative of at least 80% of the total Oils

market.

Kenny Martin

INSIGHTS Analyst

“Success for suppliers is also becoming more dependent on a deeper

understanding of shoppers, both in terms of their specific product

categories and their brands.” IGD

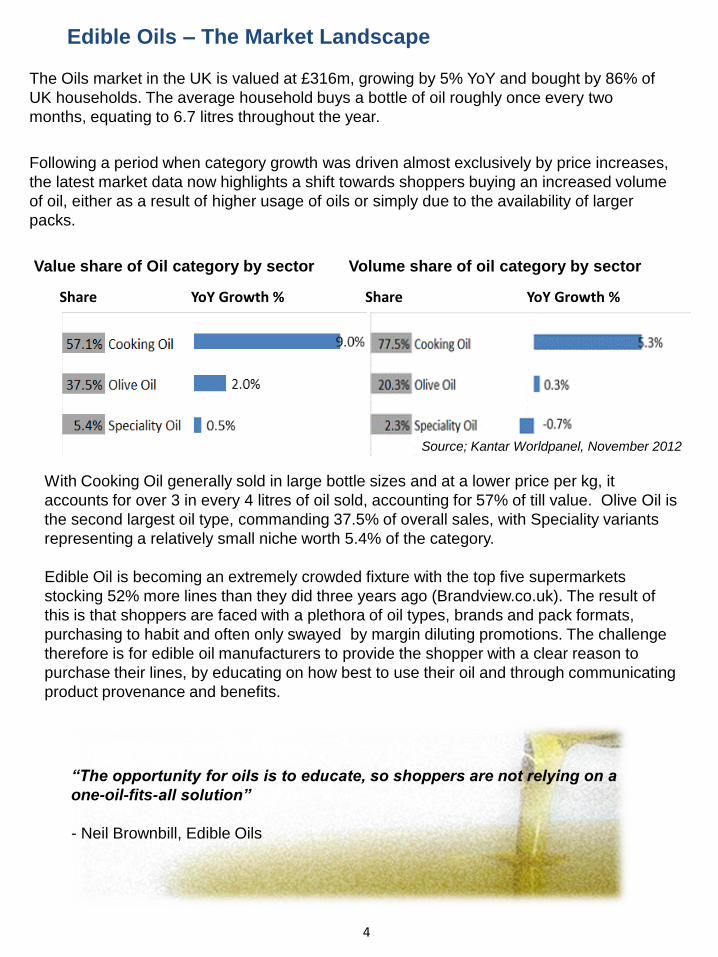

The Oils market in the UK is valued at £316m, growing by 5% YoY and bought by 86% of

UK households. The average household buys a bottle of oil roughly once every two

months, equating to 6.7 litres throughout the year.

Following a period when category growth was driven almost exclusively by price increases,

the latest market data now highlights a shift towards shoppers buying an increased volume

of oil, either as a result of higher usage of oils or simply due to the availability of larger

packs.

Value share of Oil category by sector Volume share of oil category by sector

4

Edible Oils – The Market Landscape

Share YoY Growth % Share YoY Growth %

With Cooking Oil generally sold in large bottle sizes and at a lower price per kg, it

accounts for over 3 in every 4 litres of oil sold, accounting for 57% of till value. Olive Oil is

the second largest oil type, commanding 37.5% of overall sales, with Speciality variants

representing a relatively small niche worth 5.4% of the category.

Edible Oil is becoming an extremely crowded fixture with the top five supermarkets

stocking 52% more lines than they did three years ago (Brandview.co.uk). The result of

this is that shoppers are faced with a plethora of oil types, brands and pack formats,

purchasing to habit and often only swayed by margin diluting promotions. The challenge

therefore is for edible oil manufacturers to provide the shopper with a clear reason to

purchase their lines, by educating on how best to use their oil and through communicating

product provenance and benefits.

“The opportunity for oils is to educate, so shoppers are not relying on a

one-oil-fits-all solution”

- Neil Brownbill, Edible Oils

Source; Kantar Worldpanel, November 2012

: INSIGHTS

5

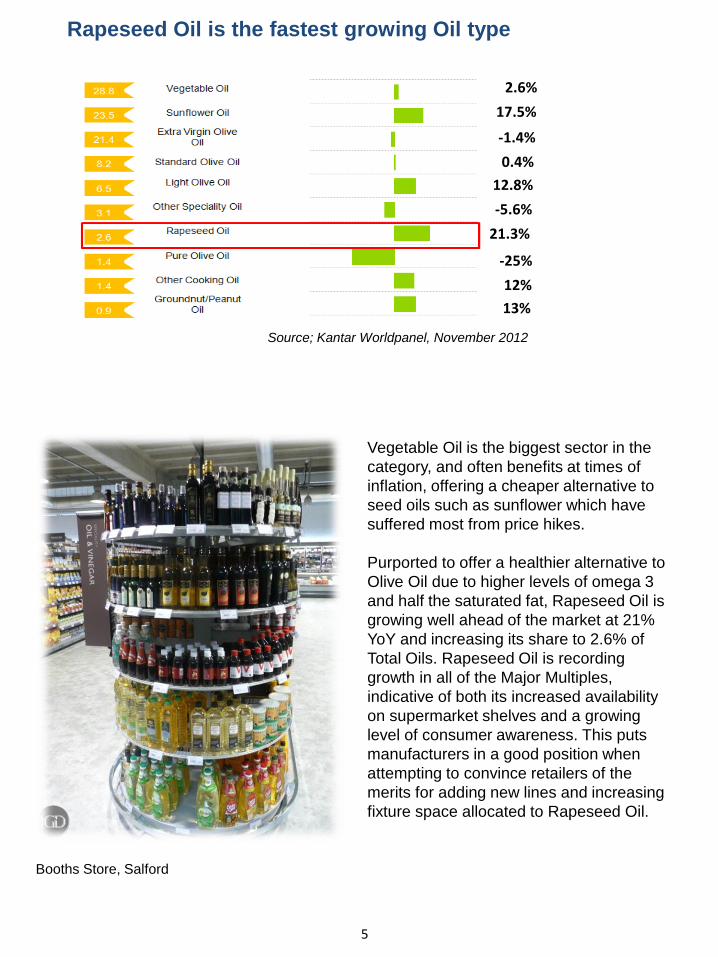

Rapeseed Oil is the fastest growing Oil type

2.6%

17.5%

-1.4%

0.4%

12.8%

-5.6%

21.3%

-25%

12%

13%

Vegetable Oil is the biggest sector in the

category, and often benefits at times of

inflation, offering a cheaper alternative to

seed oils such as sunflower which have

suffered most from price hikes.

Purported to offer a healthier alternative to

Olive Oil due to higher levels of omega 3

and half the saturated fat, Rapeseed Oil is

growing well ahead of the market at 21%

YoY and increasing its share to 2.6% of

Total Oils. Rapeseed Oil is recording

growth in all of the Major Multiples,

indicative of both its increased availability

on supermarket shelves and a growing

level of consumer awareness. This puts

manufacturers in a good position when

attempting to convince retailers of the

merits for adding new lines and increasing

fixture space allocated to Rapeseed Oil.

Source; Kantar Worldpanel, November 2012

Booths Store, Salford

6

Who Buys Rapeseed Oil ? - A shopper Profile

A Rapeseed Oil buyer is most likely to be from an older more affluent household with

66% of shoppers over the age of 55 compared to the profile of other cooking oil

products (44% being over 55).

The Rapeseed Oil shopper is twice as likely to be retired as other Speciality Oil

buyers. Therefore any press activity focussed on the promotion of Rapeseed Oil or

specific brand communications should be targeted towards the more affluent and

55+ demographic.

7

Over the last few years there has been a

surge in artisanal, British, “Cold Pressed"

Rapeseed Oils. Many consumers are

drawn by the subtle and nutty taste which

many first encounter at food festivals and

Farmers Markets, so selling or sampling

product through this channel is a worthy

way of driving product trial amongst the

target consumer. For the “foodies”,

Rapeseed Oil has a flashpoint that allows

for high temperature cooking and roasting,

so it’s good for roasting potatoes, even for

using as a butter substitute in baking and

as an alternative to Olive Oil and the

plethora of Salad Dressings available on

shelves.

How chefs are using Rapeseed Oil

Consumers have become more aware of the health,

versatility and taste attributes of Rapeseed Oil

thanks to food writers and the adoption of it by TV

chefs such as Nigella Lawson, James Martin and

Jamie Oliver.

“We should embrace it as enthusiastically as

Olive Oil”

- Ollie Dabbous, Michelin Star Chef

Rapeseed Oil Uses

Ollie Dabbous combines it with home-made apple vinegar for dressings and uses it

to toast barley and roast winter fruits.

Tristan Welch uses it to fry home-made crisps before dinner at Launceston Place

and also whisks it into a sea-beet pesto to serve with salt marsh lamb.

Darron Bunn bases all the dressings and vinaigrettes on Rapeseed Oil and uses it

to complement fois gras at Quaglino's.

Former MasterChef winner Mat Follas who is now at the helm of Wild Garlic in

Dorset makes a duck-egg and rapeseed mayonnaise.

A total of 26 Rapeseed Oil brands registered sales over the last year, highlighting the

degree of category fragmentation, with a high number of low share regional brands.

Compared to other ambient categories this is a particularly high number of brands

especially taking into account the relatively small category size. The total number of

producers in the UK is estimated to be close to 70.

Over the last year a total of 38 branded SKU’s have registered sales, this does not

include Retailers’ Own-Label lines. Pricing ranges from 18p to £1.16 per 100ml,

highlighting the range of Rapeseed Oil available.

8

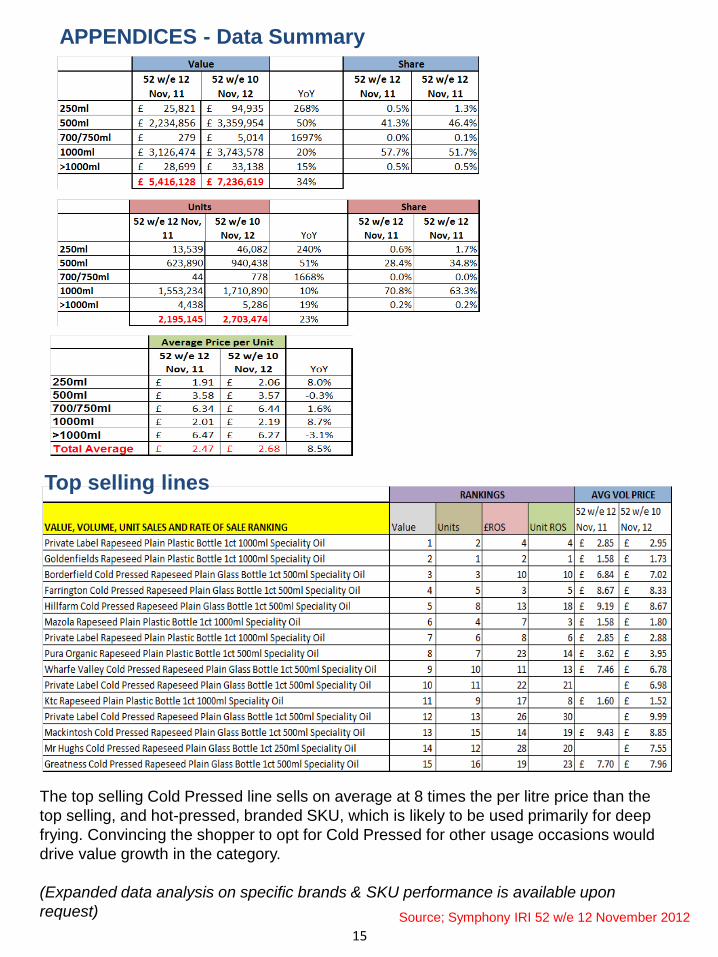

Rapeseed Oil in UK Grocery

Fast-Facts

• £7.2m UK market value, growing at 34% YoY

• 2.7m bottles sold a year, growing by 23% YoY

• 1 litre bottles account for 51.7% of sales value

and 70% of units, and are priced at the

cheaper end of the category

• 500ml commands 46.4% share of value from

just 1 in 3 bottles sold, so tend to be

positioned at higher price points

• 500ml driving category growth with sales

growing by 50% on last year - See appendix for data

Source; Symphony IRI 52 w/e 12 November 2012

Waitrose were the pioneers of Rapeseed Oil, listing a line back in 2005, and it

currently sells both national and regional lines. Following critics and writers

banging the Rapeseed drum, M&S opted to list what they describe as “one of the

more subtle ones we tasted”. Since listing a Northumbrian product, M&S has seen

a steady growth in Rapeseed Oil rate of sale. Speciality Retailers such as

Selfridges and Fortnum & Mason have also listed Cold Pressed Rapeseed Oils,

including Scottish variants.

Most of the large retailers have launched their own premium positioned Cold

Pressed products over the last year. The advent of this indicates their faith in the

strength of the category, this can be viewed as both a supply opportunity and also

a threat to those brands currently in or planning to enter the market place.

Nevertheless this highlights the importance for brands to invest in marketing to

drive consumer loyalty and differentiate themselves from the growing number of

competitors, including Retailers themselves.

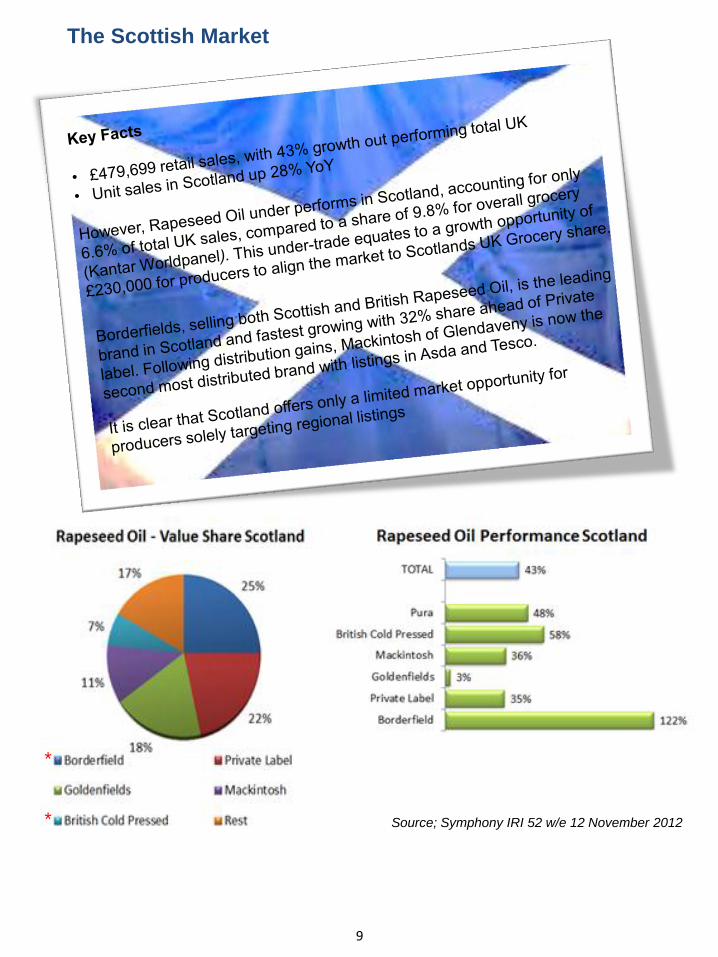

The Scottish Market

9

Source; Symphony IRI 52 w/e 12 November 2012

*

*

Sainsb

ury's Ely, C

amb

ridgesh

ire

Availability in Scottish Grocery Retail

11

Source; Symphony IRI 52 w/e 12 November 2012

54% of Scots think that it is

important that food of Scottish

provenance is available at

their local supermarket *, so

producers should initially focus

on negotiating local/regional

listings. Rapeseed Oil brands

are generally listed on a

regional basis by retailers, with

the exception of Borderfields

and Goldenfields.

*Source: YouGov SixthSense Food

Provenance Survey (11-19 June

2012)

However if brands are able to

differentiate themselves in

terms of taste profile, this

would enable them to

challenge this barrier to

access a broader national

coverage.

UK Brand performance

• Own Label has 28% share of sales value for the category, with brands accounting

for £5.2m, equating to an average brand market value of £208,913.

• Goldenfields, originating from Belgium, is the leading brand in the category, which

retails at £1.79. Sold in PET 1 litre bottle the brand is listed nationally in Morrisons

and 88% of Waitrose stores.

• Borderfields is the leading UK brand and also the fastest growing, offering “British”

and “Scottish” variants, listed nationally in Asda, Sainsburys, Morrisons and Tesco.

• All Rapeseed Oil brands are in unit sales growth with the exception of Goldenfields,

indicating a willingness for shoppers to spend on more premium Rapeseed Oil as

product awareness grows

12

Source; Symphony IRI 52 w/e 12 November 2012

With so many brands competing for a share of what is a limited Rapeseed Oil market,

sustainable brand growth will only be achievable through category growth. In order to do

this, it would require a producer, or a group of them to amass a sufficient budget

principally to build category awareness and trial.

13

Cold Pressed Rapeseed Oil has the opportunity to capture a larger share of the

Edible Oils market. Without investment to allow for overall category growth,

Rapeseed Oil producers will always vie for share of a very limited market. Therefore

there is a requirement for joined up Category Marketing to develop overall

awareness and generate consumer trial in order to drive market growth, allowing for

all Scottish Rapeseed Oil producers to flourish.

The Category Development Levers

As Olive Oil prices continue to rise, Cold Pressed Rapeseed Oil is in a strong position to

emerge as a natural alternative for shoppers. Currently the Rapeseed Oil market is

limited to only £7.2m in UK Retail spread across numerable brands, with almost 20%

being standard hot pressed 1 litre PET originating from Belgium.

Encouraging consumer trial and repeat purchase will require a step up in building the

awareness of benefits and uses of Cold Pressed Rapeseed Oil versus alternative

variants, particularly amongst the older, more up market female.

Category Marketing Investment is the key

To achieve sustainable growth, investment will be paramount to allow for category

growth the numerous small producers to flourish. Without this, brands will be forced into

pricing and promotion tactics which might achieve short term share steal, leading to at

category deflation in the long term. Inevitably some producers will be then be squeezed

out by retailers as Buyers seek to manage the plethora of brands and optimise ranges

to offer their shopper a unique product range, which will limit the opportunity for

producers to be listed across grocery.

Following category investment, it is important that Scottish producers are able

differentiate themselves from other regions and brands by communicating what makes

them, their sourcing, taste profile, nutritional profile or manufacturing process different or

better than the rest. By doing so this allows for the positioning of Producers to

communicate specific benefits, allowing them to target listings beyond default regions,

offering the potential for Scottish Rapeseed Oil to be listed in stores beyond our border.

Finally, Brand level activity should then focus efforts on the merits and values of their

individual provenance and unique taste attributes to differentiate themselves from other

producers on the fixture. Currently, packaging and design coupled with discounting are

the key mechanisms to driving purchase choice.

Currently the lead brand is arguably devaluing the market, in terms of packaging and

price position. Category level marketing will encourage those consumers currently

buying Rapeseed Oil purely for frying to trade up to Cold Pressed products offering a

broader usage repertoire, which presents significant opportunity to drive category value.

With Rapeseed Oil under trading in Scotland, there is a clear opportunity to develop the

category based on communication pillars of premium, provenance and health benefits.

However, for the industry to progress, efforts must be focussed on driving the Rapeseed

sector within the overall Edible Oils category. Investment should not be focussed solely

on the individual capabilities of one single producer, but on how together Scotland’s

Rapeseed Oil producers can evolve together as part of a dynamic sector within the

Edible oil category.

Summary & Recommendations

14

APPENDICES - Data Summary

15

Source; Symphony IRI 52 w/e 12 November 2012

Top selling lines

The top selling Cold Pressed line sells on average at 8 times the per litre price than the

top selling, and hot-pressed, branded SKU, which is likely to be used primarily for deep

frying. Convincing the shopper to opt for Cold Pressed for other usage occasions would

drive value growth in the category.

(Expanded data analysis on specific brands & SKU performance is available upon

request)

Web : www.scotlandfoodanddrink.org/insights

Andrew Niven INSIGHTS Manager

Kenny Martin INSIGHTS Analyst

Scotland Food & Drink,

No.3, The Royal Highland Centre,

Ingliston,

Edinburgh,

EH28 8NB

Tel: 0131 335 0940

Twitter: @Insight2Go

Know Your Market

A View of the UK Rapeseed Oil Category

![Injection Spray Comparison of Diesel Fuel and Cold Pressed ... · Table 1. Important Fuel Properties of Rapeseed oil (RSO), [3] Due to the distinctly higher kinematic viscosity of](https://static.documents.pub/doc/80x56/5f2f6e59efac49651049b9e3/injection-spray-comparison-of-diesel-fuel-and-cold-pressed-table-1-important.jpg)