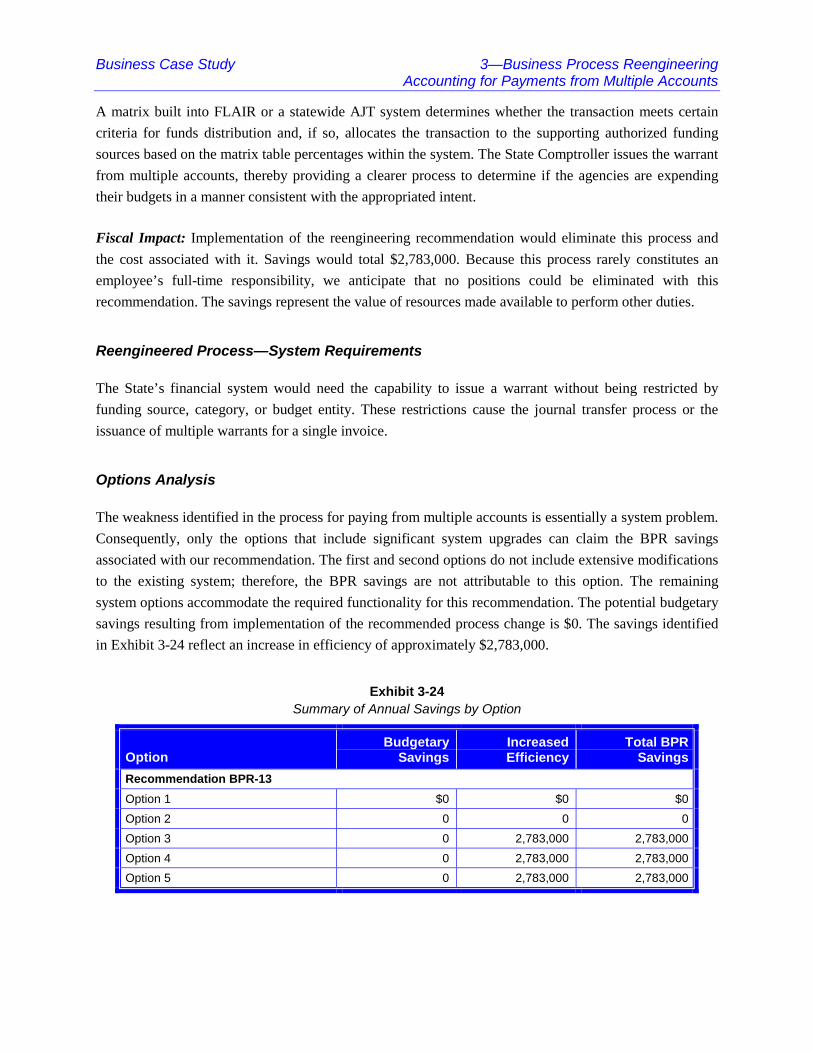

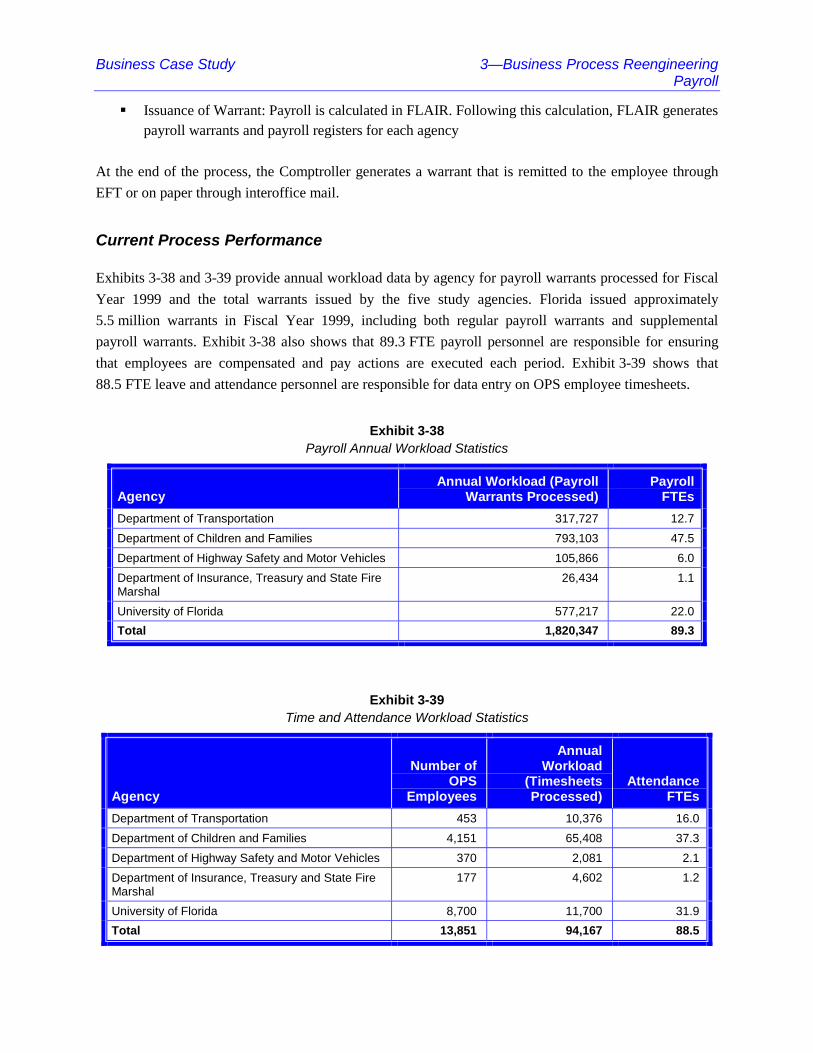

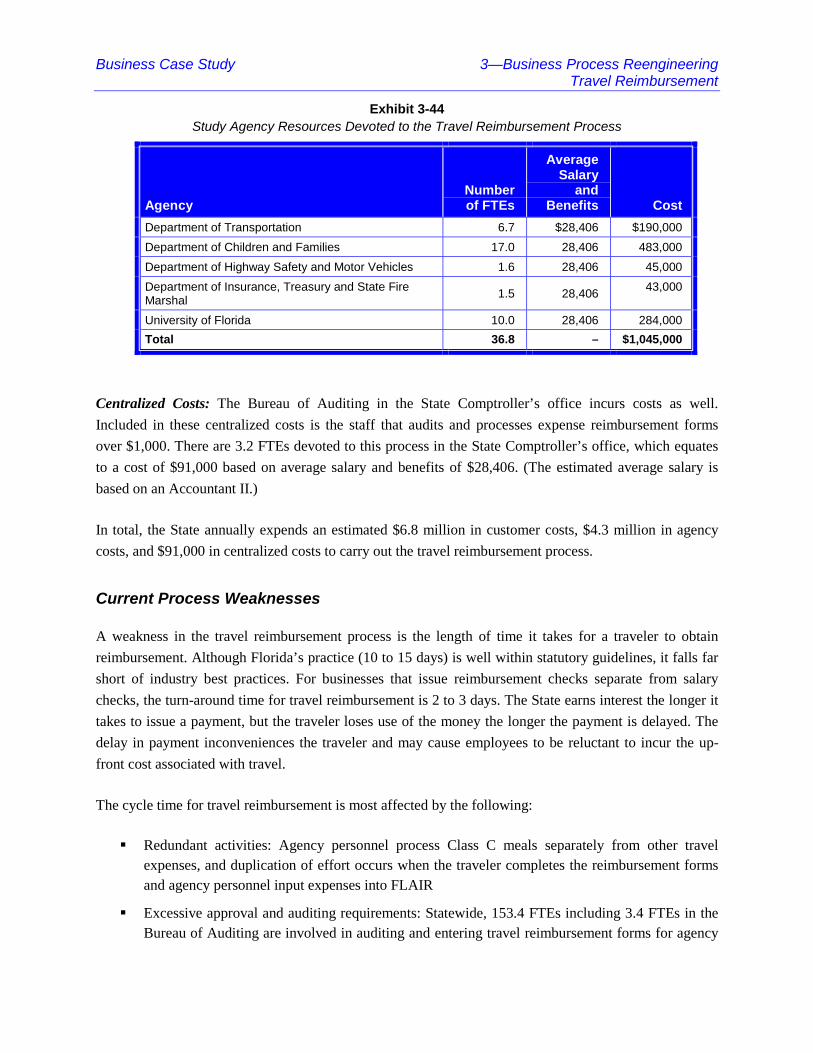

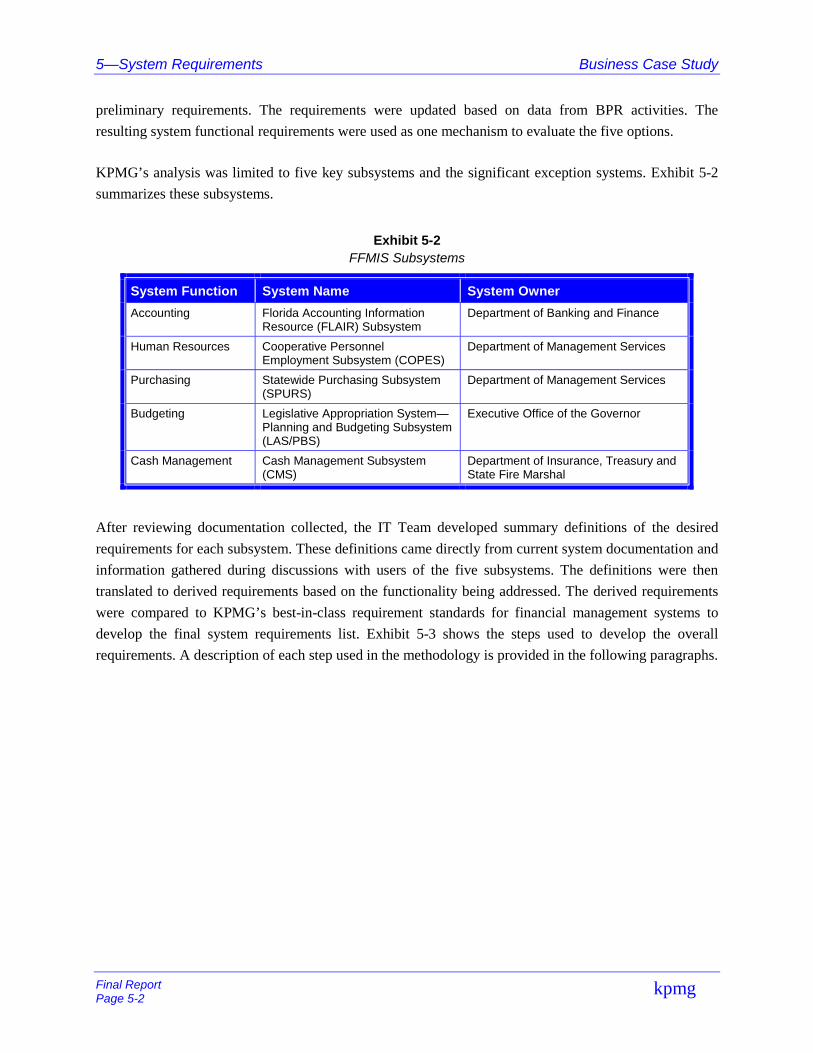

275

Business Case Study Executive Summary

Final ReportPage ES-1 kpmg

Executive SummaryThe State of Florida engaged KPMG to conduct the Modernization of State Government Financial

Management Business Practices Study (hereafter referred to as the “Business Case Study” or the

“Study”), which considered contemplated changes to the subsystems it refers to collectively as the

Florida Financial Management Information System (FFMIS). KPMG assessed the costs and risks as well

as the financial and other benefits that the State can expect from a new or enhanced financial

management system. The Study began August 2, 1999, and the final report was submitted February 15,

2000.

Background

For the past two decades, the State of Florida has accomplished its budgeting, cash management,

accounting, purchasing, payroll, and human resource functions using five stand-alone, stovepipe, legacy

management information systems. Although these FFMIS subsystems have been maintained and

incrementally upgraded, the State of Florida has neither modernized nor replaced the subsystems in a

structured and coordinated manner to meet its changing and growing needs. The five functional FFMIS

subsystems and their agency “owners” are identified in Exhibit ES-1:

Exhibit ES-1FFMIS Subsystem Owners

Function Name Owner

Accounting Florida Accounting Information Resource (FLAIR)Subsystem

Department of Banking and Finance

Human Resources Cooperative Personnel Employment Subsystem(COPES)

Department of Management Services

Purchasing Statewide Purchasing Subsystem (SPURS) Department of Management Services

Budgeting Legislative Appropriation System - Planning andBudgeting Subsystem (LAS/PBS)

Executive Office of the Governor

Cash Management Cash Management Subsystem (CMS) Department of Insurance, Treasuryand State Fire Marshal

Issues and concerns with the FFMIS subsystems, including the lack of integration and incomplete

reporting capabilities, have developed over the years since the system was implemented. After several

years of research and assessment, the State decided to pursue implementation of a commercial off-the-

shelf (COTS), Enterprise Resource Planning (ERP) system to support its core business functions. The

implementation of a purchased ERP system anticipated extensive reengineering of State agencies’

business processes to ensure that the benefits of the system would be realized.

Executive Summary Business Case Study

Final ReportPage ES-2 kpmg

In 1997, a pilot project was initiated to replace the State’s COPES and payroll portions of FLAIR with a

COTS solution. In 1998, SAP R/3 was selected as the ERP package for the State. After completing the

scoping and planning phases, the State discontinued the project in March 1999. The State was concerned

about escalating cost estimates and the ability of the system to meet the State’s functional and technical

requirements. The State was also concerned about the magnitude of the projected benefits associated

with continuing its ERP implementation.

Although the pilot project was discontinued, the need to enhance or replace the FFMIS subsystems was

still apparent. With the support of newly elected Governor Jeb Bush, the Florida Legislature passed

legislation in 1999 to carry out the Business Case Study.

Vision for FFMIS

A clearly defined vision is critical for making an important decision such as the one contemplated by the

Business Case Study. One of the first steps taken by KPMG in the Study was to understand the vision

that the State of Florida has for FFMIS. KPMG interviewed stakeholders of FFMIS in senior leadership

positions at the project inception and found that the State has a clear vision for its financial management

systems. The recurring themes that together constitute the State’s vision are summarized in Exhibit ES-2.

Exhibit ES–2Vision for FFMIS

Existing FFMIS

Departmental Focus

Stovepipe System Architecture

Extensive “Dumb Terminals” and “Green Screens”

Inconsistent Chart of Accounts

Limited Integrated Performance Data

Limited Contract Management and Tracking

No CFO Drives Financial Management

No Single Source Drives FFMIS Policy

Excessive Ad Hoc Reporting

Extensive Manual Reconciliations

Four Data Centers

Limited e-commerce

Rigid Financial Policies Embedded in Statute

Focus on Expensive Preventive Controls

Future FFMIS

Statewide Enterprise Focus

Integrated System Structure

Enhanced Desktop Capabilities

Consistent and Integrated Chart of Accounts

Enhanced Integrated Performance Data

Enhanced Contract Management Support System

CFO Drives Financial Management

CFO and Governor Drive FFMIS

Standard Management and Financial Reporting

Automated Reconciliations

Consolidated Data Center Support Structure

Fully Integrated e-commerce

Flexible Financial Policies Set by Administrative Rule

Focus on Employee Efficiency with Cost-Effective Detective Controls

Business Case Study Executive Summary

Final ReportPage ES-3 kpmg

Objectives

The Study focused on providing answers to three questions critical to making the State’s vision for

FFMIS a reality:

! What should the State do to modernize its financial management systems?

! How much will it cost?

! What benefits will the State receive?

KPMG worked closely with the State to meet its objectives while ensuring the integrity and objectivity of

the analysis. The State’s Project Management Team and State’s Study Advisory Council met regularly

with KPMG to promote open, ongoing communications and Study management.

Approach

KPMG organized the Study into three major tasks:

! Business Process Reengineering (BPR)

! Information Technology (IT) Assessment and Evaluation

! Evaluation of Options

Business Processing Reengineering Task

The Business Process Reengineering task focused on assessing the benefits the State could achieve by

changing its business processes. The benefits were primarily with technology but some non-technology-

dependent opportunities were also identified. A review of every business process in State government

was not feasible within the time constraints of the Study. With the help of the State Study Team and

Study Advisory Council, KPMG selected 16 processes for analysis. These processes are listed in Exhibit

ES-3. KPMG completed high-level documentation of current activities and processes, developed

recommendations for improving these processes, and determined the impacts of the recommendations on

the five system options described below in the IT Assessment and Evaluation Task.

Executive Summary Business Case Study

Final ReportPage ES-4 kpmg

Exhibit ES-3Processes Selected for Analysis

Management Reporting Purchasing Commodities and Services

Financial Reporting Payment for Goods and Services

Accounting Reconciliation Budgeting

Accounting for Payments from Multiple Accounts Rate and Position Administration

Allocation of Common Costs Certified Forward

Flow of Federal Funds Cash Receipts and Cash Management

Payroll Accounts Receivable

Travel Reimbursement Asset Management

KPMG also worked with the State Study Team and Study Advisory Council to identify and select a

representative sample of State agencies to participate in high-level process reengineering. The five

agencies selected were:

! Department of Transportation

! University of Florida

! Department of Highway Safety and Motor Vehicles

! Department of Children and Families

! Department of Insurance, Treasury and State Fire Marshal

The results of this high-level reengineering were extrapolated to the 49 Governor, Cabinet, Legislative,

and Judicial agencies in the State of Florida. The opportunities that KPMG identified included both

technology-dependent improvements as well as improvements that the State can implement without new

technology. Our recommendations included “hard” savings (budgetary) resulting from reduced operating

costs and “soft” savings (increased efficiency) resulting from reduced staff efforts that make time

available for other higher value activities.

IT Assessment and Evaluation Task

For the IT Assessment and Evaluation Task, KPMG performed the following:

! Assessed the existing system used by the State of Florida

! Defined the five system options identified by the State for evaluation in the Business Case Study.The five options are shown in Exhibit ES-4

! Developed system requirements for existing and future technologies to use in analyzing the fivesystem options

! Evaluated the five system options

Business Case Study Executive Summary

Final ReportPage ES-5 kpmg

Exhibit ES–4Financial System Options

Option 1 As-Is Maintain the current legacy systems as-is with no major modifications or upgrades

Option 2 Enhanced Enhance current systems by adding new tools and functionality

Option 3 Custom Develop a new custom integrated information management system

Option 4 COTS Implement a commercial off-the-shelf Enterprise Resource Planning package

Option 5 Best of Breed Use some combination of the other four options

KPMG analyzed the strategic, operational, technical, and financial impact of each alternative. The

evaluation included the advantages and disadvantages associated with each system option.

Evaluation of Options Task

For the Evaluation of Options Task, KPMG prepared a Total Cost of Ownership (TCO) estimate and a

Return on Investment (ROI) analysis for a period of 15 years. The financial analysis included cost

savings identified in the BPR Task and investments required as a result of the IT Assessment and

Evaluation Task. The ROI consisted of quantitative operational improvements for the State. KPMG

analyzed various financial metrics including net present value (NPV), internal rate of return (IRR), and

payback period.

Findings—BPR Analysis and IT Assessment and Evaluation

KPMG’s BPR analysis and IT assessment and evaluation resulted in a number of findings and

recommendations for both the State’s financial management practices and for the operational support

from the respective IT staffs.

Business Process Reengineering Findings

Our analysis of the processes selected for review in the Business Case Study revealed many opportunities

for budgetary savings and increased efficiency. Some of these opportunities are a result of the State not

having taken full advantage of technology to improve its processes. Other opportunities are not

technology driven.

In total, KPMG made 46 separate recommendations, which address major weaknesses with current

processes. Among the goals are improving customer service, reducing costs, and reducing cycle times.

The recommendations cluster around several themes as follows:

! Develop an enterprisewide perspective on State government financial operations

! Expand the functionality of the financial management system

Executive Summary Business Case Study

Final ReportPage ES-6 kpmg

! Automate manual steps and reduce excess paper

! Provide better financial management information for more cost-effective decisions

! Increase the use of e-commerce

! Update and modernize policies and procedures

A sample of BPR recommendations from the Study is shown in Exhibit ES-5.

Exhibit ES-5Sample BPR Recommendations

Payroll (BPR–18) Move to a shared services concept by having severalagencies served by a single payroll unit $2,016,000

Purchasing (BPR–31) Enhance the central purchasing function at Stateagencies and DMS to focus on strategic sourcing

10,700,000

Cash Receipts andCash Management(BPR-39)

Terminate the certificate of deposit program aimed atFlorida banks and S&Ls and transfer funds to theexternally managed program

11,679,000

Cash Receipts andCash Management(BPR-40)

Reduce funds in the internal investment liquidity pooland transfer them to the externally managed funds

10,000,000

The estimated annual fiscal impact of all BPR recommendations is presented by option in Exhibit ES-6.

Exhibit ES-6Summary of Fiscal Impacts by Option

OptionsBudgetary

SavingsIncreasedEfficiency Total BPR savings

Option 1 $23,691,000 $1,707,000 $25,398,000

Option 2 60,219,000 3,159,000 63,378,000

Option 3 90,776,000 6,193,000 96,969,000

Option 4 90,776,000 6,193,000 96,969,000

Option 5 90,776,000 6,193,000 96,969,000

Business Case Study Executive Summary

Final ReportPage ES-7 kpmg

IT Assessment and Evaluation Findings

KPMG found that the current FFMIS subsystems will not support the vision that the State has for its

financial management systems. The overarching concerns about Florida’s existing subsystems are shown

in Exhibit ES–7.

Exhibit ES–7Findings on Existing FFMIS Subsystems

1 Florida has created stovepipe data and technical architectural models.

2 FFMIS subsystems do not provide adequate decision-support information and functionality, resulting innumerous shadow and feeder systems.

3 Significant staffing resources are dedicated to ensuring consistency among the five FFMIS subsystems inthe form of duplicate data entry, data redundancy, and data reconciliations.

4 FFMIS processing, application, and help desk support occurs in four distinct IT organizations.

5 The lack of a unified, standard Chart of Accounts makes aggregating information across agencies extremelydifficult without extensive manual effort.

6 FFMIS subsystems are difficult, time consuming, and expensive to modify.

7 Existing State personnel policies and funding processes inhibit the recruitment and retention of skilledemployees required to support FFMIS technology.

8 FFMIS makes limited use of e-commerce.

Surveys conducted during the Study indicated that most users do not believe FFMIS can support the

future business needs of the State of Florida. Users also expressed dissatisfaction with the current

functionality in FFMIS. Targeted improvement areas from the users’ perspective focused on:

! Integration

! System flexibility

! Ad hoc reporting capabilities

! Ease of use

! Training

! Help facilities

Executive Summary Business Case Study

Final ReportPage ES-8 kpmg

Findings—Evaluation of Options

KPMG’s evaluation of the five FFMIS options covered three key areas: ability to satisfy requirements,

risks, and financial considerations.

Requirements Assessment

KPMG considered the ability of each option to meet approximately 1,500 functional and technical

requirements, which were defined for FFMIS by KPMG and State personnel. Exhibit ES-8 summarizes

the results of our requirements assessment for each option. The maximum score available was five

points. Higher scores indicate that the option is better able to meet the State’s functional and technical

requirements.

Exhibit ES-8Summary of Requirements Assessment

Category Wei

gh

tP

erce

nta

ge

As-

Is

En

han

ced

Cu

sto

m

CO

TS

Bes

t o

f B

reed

Total Functional Score 70% 1.5 2.3 3.5 2.9 3.4

Total Technical Score 30% 0.5 0.8 1.4 1.4 1.3

TOTAL SCORE 100% 2.0 3.1 4.9 4.3 4.7

As the scores indicate, a Custom solution will best meet the State’s functional and technical requirements

because it is possible with the right amount of resources and time to build exactly what the State needs.

The COTS and Best of Breed solutions can satisfy most of the State’s requirements while the As-Is and

Enhanced options fall short of meeting many of the State’s requirements.

Risk Assessment

KPMG considered the strategic, project, and continuation risk to the State for each of the options.

Exhibit ES-9 summarizes our assessment of each risk category. (Note: Lower scores indicate less risk.)

Business Case Study Executive Summary

Final ReportPage ES-9 kpmg

Exhibit ES-9Summary of Risk Assessment

Category Wei

gh

tP

erce

nta

ge

As-

Is

En

han

ced

Cu

sto

m

CO

TS

Bes

t o

f B

reed

Total Strategic Risk/Weighted Average 100% 4.8 2.8 1.3 1.2 1.3

Total Project Risk/Weighted Average 100% 0.0 2.1 4.5 3.2 3.3

Total Continuation Risk/Weighted Average 100% 3.8 3.6 3.1 2.3 2.8

Total All Risk Categories/Weighted Average 2.9 2.8 3.0 2.2 2.5

The risk analysis indicates that a Custom solution exposes the State to the greatest degree of risk. The

COTS and Best of Breed options provide the least exposure to risk.

Financial Assessment

KPMG considered the BPR savings net of the risk-adjusted implementation and ongoing operational

costs over a 15-year period for each option. In addition, financial metrics such as NPV (based on a

discount rate of 6 percent), IRR, and payback period were considered. Exhibit ES-10 summarizes the

financial impact of each option.

Executive Summary Business Case Study

Final ReportPage ES-10 kpmg

Exhibit ES-10Summary of Financial Assessment(dollar amounts are in thousands)

Options As-Is Enhanced Custom COTSBest ofBreed

Implementation Costs $ 0 $(119,222) $(563,745) $(257,960) $(281,327)

Operations Costs $(396,328) (402,065) (216,392) (277,548) (316,317)

Technology-related BPR

Savings 0 478,471 798,797 956,113 956,113

Net Fiscal Impact (Technology

Savings Only) (396,328) (42,816) 18,660 420,605 358,469

NPV on Net Savings

(Technology Savings Only) (250,806) (96,638) (166,387) 133,770 92,965

Internal Rate of Return N/A (2%) (1%) 12% 10%

Years to Payback N/A N/A 15 Years 10 Years 11 Years

Nontechnology-Related

BPR Savings 467,922 467,922 467,922 467,922 467,922

Net Fiscal Impact

(All Recommendations) $71,594 $425,106 $486,582 $888,527 $826,391

Recommendation

After comparing the five system options to the State’s vision and functional and technical requirements,

and after assessing the risk and financial impacts, KPMG believes, as shown in Exhibit ES-11, that the

Best of Breed option is the optimum choice for the State’s financial management information system.

Exhibit ES-11Minimum Requirements Analysis Ratings

(dollar amounts are in thousands)

Functionality Financial

RawScore

WeightedScore

Raw Savings(Cost)

WeightedScore Total

Option A B A + B

As-Is 2.00 40 $(396,328) - 40

Enhanced 3.10 62 (42,816) 24 86

Custom 4.90 98 18,660 28 126

COTS 4.30 86 420,606 50 136

Best of Breed 4.70 94 358,469 46 140

Business Case Study Executive Summary

Final ReportPage ES-11 kpmg

The Best of Breed option KPMG recommends would:

! Use an ERP system to replace the State’s accounting and personnel systems

! Use an ERP system to partially replace the budgeting, cash management, and purchasingsubsystems

! Allow dual-tracks for the SUS and the remainder of State government

As documented in our analysis, ERP packages (at the time of evaluation) are generally weak in certain

key areas, such as supporting the legislative approval of budget issues, supporting a web-enabled vendor

bid management system, and complying with Florida’s unique cash management practices. Accordingly,

the portions of those subsystems not replaced with an ERP system would continue to be supported by

State-developed software that would interface with the ERP solution.

In addition, the student administration systems used by the State University System (SUS) are

sufficiently self-contained and have unique requirements that must be met by the SUS Financial

Management System. If the student administration system drove the selection of an ERP package, it

could lead to selecting an ERP vendor that may not be best for the rest of State government and vice

versa. Recognizing the important differences between general government and Florida’s higher education

system, the recommendation enables a dual track software selection and implementation strategy to

accommodate, but not require, separate software packages for the State University System and the

remainder of State government. If this approach is taken, the systems would need to interface to provide

statewide management information.

KPMG believes that the Best of Breed option is the optimum practical solution to meet the functionality

required by the State of Florida. With this option, the State would be able to blend the best practices of

the industry with that of the State wherever the off-the-shelf solution does not meet a requirement.

Although KPMG recommends enhancements to the ERP solution in some specific areas, we suggest that

the State exercise care when evaluating enhancements and consider the effect that those enhancements

have on future upgrades.

To reduce the project risk of this effort, KPMG recommends that a dedicated project management office

be established—one that is consistent with the State's vision, focuses on delivering a quality product, and

is sensitive to producing a timely solution. KPMG also recommends that the Executive Office of the

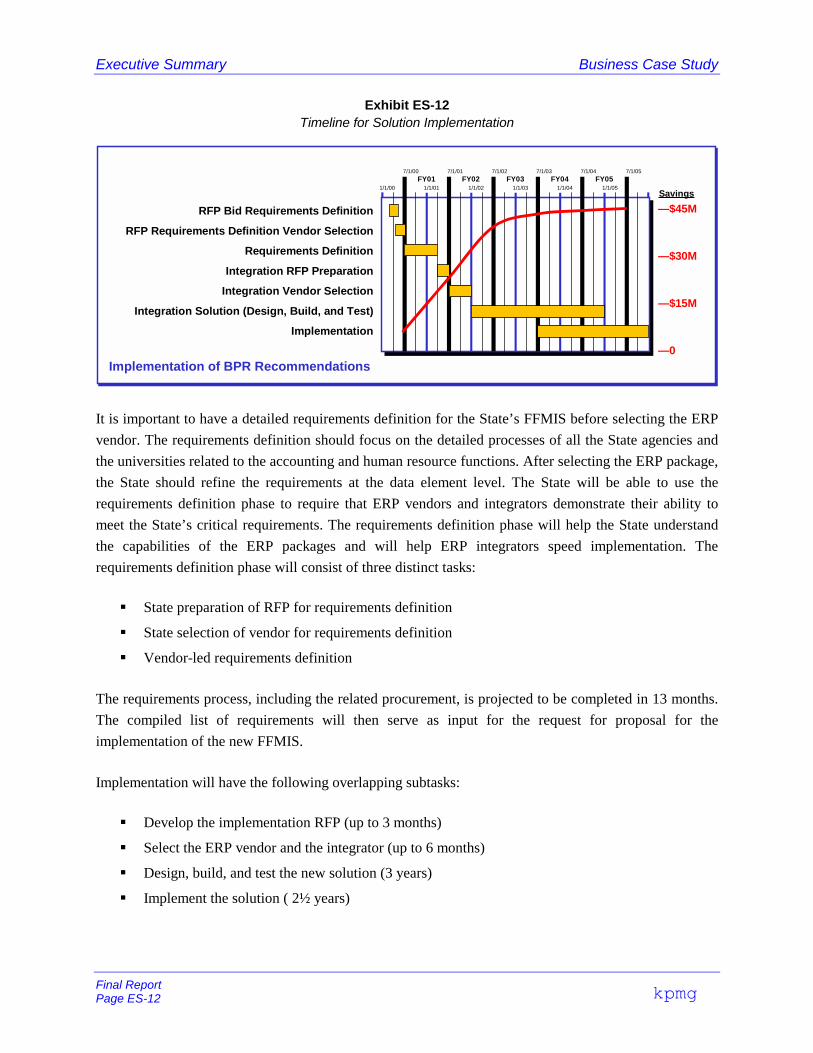

Governor take ownership of the project. Exhibit ES-12 illustrates a timeline for the implementation of the

integrated solution. We have overlaid a line on the chart to graphically represent the estimated savings

from the State’s implementation of recommendations prior to the full system implementation.

Executive Summary Business Case Study

Final ReportPage ES-12 kpmg

Exhibit ES-12Timeline for Solution Implementation

RFP Bid Requirements Definition

RFP Requirements Definition Vendor Selection

Requirements Definition

Integration RFP Preparation

Integration Vendor Selection

Integration Solution (Design, Build, and Test)

Implementation

Implementation of BPR Recommendations

1/1/00 1/1/01 1/1/02 1/1/03 1/1/04 1/1/05

7/1/00 7/1/01 7/1/02 7/1/03 7/1/04 7/1/05

FY01 FY02 FY03 FY04 FY05

Savings

—$45M

—$30M

—$15M

—0

It is important to have a detailed requirements definition for the State’s FFMIS before selecting the ERP

vendor. The requirements definition should focus on the detailed processes of all the State agencies and

the universities related to the accounting and human resource functions. After selecting the ERP package,

the State should refine the requirements at the data element level. The State will be able to use the

requirements definition phase to require that ERP vendors and integrators demonstrate their ability to

meet the State’s critical requirements. The requirements definition phase will help the State understand

the capabilities of the ERP packages and will help ERP integrators speed implementation. The

requirements definition phase will consist of three distinct tasks:

! State preparation of RFP for requirements definition

! State selection of vendor for requirements definition

! Vendor-led requirements definition

The requirements process, including the related procurement, is projected to be completed in 13 months.

The compiled list of requirements will then serve as input for the request for proposal for the

implementation of the new FFMIS.

Implementation will have the following overlapping subtasks:

! Develop the implementation RFP (up to 3 months)

! Select the ERP vendor and the integrator (up to 6 months)

! Design, build, and test the new solution (3 years)

! Implement the solution ( 2½ years)

Business Case Study Executive Summary

Final ReportPage ES-13 kpmg

The implementation process is projected to require approximately 4 years to complete. For simplicity, we

assumed that accounting and human resource modules of the chosen ERP vendor will be built once and

will be implemented in phases. With this approach, implementation for the initial phase of agencies will

begin in 3½ years. With proper planning, control, and approval, the State could begin implementing the

solution in selected agencies 6 to 9 months earlier than presented in our timeline. Thus, implementation

in the first agencies could be completed in less than 3 years.

Executive Summary Business Case Study

Final ReportPage ES-14 kpmg

This page intentionally left blank

Business Case Study 1—Objectives and Approach

Final ReportPage 1-1 kpmg

1. Objectives and Approach1.1 Objectives

The State of Florida’s objectives in the Modernization of State Government Financial Management

Business Practices Study are:

To develop a business case study for enhancing or replacing the State’s current financial

management systems while simultaneously changing the State’s associated financial

management business practices.

The decisions that Florida must make based on this Study are both significant (in dollars and time to

implement) and complex (in the number of agencies and processes it impacts). Furthermore, these

decisions will receive extensive scrutiny by both internal and external stakeholders of the State. The

underlying analysis governing this Study must be widely viewed as independent and objective. In reality,

the future of the Florida Financial Management Information System (FFMIS) modernization rests on this

Study’s credibility.

KPMG worked closely with the State’s leaders to meet their objectives while ensuring the integrity and

objectivity of this analysis:

! The State and KPMG agreed up front on the Study’s approaches and methodologies

! The State’s Project Management Team and Advisory Council met regularly with the KPMGStudy Team to promote open, ongoing communications and study management

! The Study effort was organized to provide decision-useful results

1.2 Business Case Study Approach

To achieve the State’s objectives, KPMG conducted a Business Case Study to provide a recommendation

for reengineering selected State business processes in tandem with enhancing or replacing the State’s

current financial management systems. Our recommendations are based on a comprehensive assessment

of costs and benefits and include a strategy for rollout and funding, an estimate for the time to implement,

and direction on system ownership.

1—Objectives and Approach Business Case Study

Final ReportPage 1-2 kpmg

The Study compares five options identified by the State as shown in Exhibit 1-1.

Exhibit 1-1Options

Option 1 As-Is Maintain the current systems as-is with no major modifications or upgrades

Option 2 Enhanced Enhance current systems by adding new tools and functionality

Option 3 Custom Develop a new custom integrated information management system

Option 4 COTS Implement a commercial off-the-shelf Enterprise Resource Planning package

Option 5 Best of Breed Use some combination of the other four options

KPMG considered the strategic, operational, technical, and financial impacts of the five options and

prepared a 15-year total cost of ownership (TCO) estimate and a return on investment (ROI) analysis.

We organized the Study into seven tasks as shown in Exhibit 1-2.

Exhibit 1-2KPMG Approach

BusinessProcess

ReengineeringTask 3

IT Assessmentand

EvaluationTask 4

Evaluationof

OptionsTask 5

FinalizeBCS

MethodologyTask 2

InitiateStudy

Task 1

PrepareFinal

ReportTask 8

Finalize BCSand Prepare

RecommendationTask 7

DraftInterimReportTask 6

Our amended timeline for the Study is presented in Exhibit 1-3.

Business Case Study 1—Objectives and Approach

Final ReportPage 1-3 kpmg

Exhibit 1-3Amended Timeline

1. Initiate Study

2. Finalize Business Case Study Methodology

3. Conduct BPR Assessment

4. Evaluate System Options

5. Conduct Business Case Study

6. Brief Steering Committee

7. Finalize BCS and Prepare Recommendations

8. Prepare Final Report

BIWEEKLY STATUS REPORTS

Kick Off Meeting August 2, 1999

Report on PreliminaryAnalysis and Results

October 15, 1999

Draft Final ReportJanuary 21, 2000

Final Report withRecommendationsFebruary 15, 2000

Up to 3 Briefingsas requested

Presentation to Senior State Officials

December 15, 1999

To evaluate the five options, we organized the Study into three major components grouped in the center

of Exhibit 1-2:

! Business Process Reengineering (BPR)

! Information Technology (IT) Assessment and Evaluation

! Evaluation of Options

After initiating the Study, KPMG met with the State management representatives to finalize the Study

methodology and assumptions. Our experience has shown that it is critical for KPMG and the State’s

Study Management Team to reach consensus on key issues that will influence the success of this project.

During the Finalize BCS Methodology Task, we reached consensus on the methodologies and approaches

for the BPR, IT Assessment and Evaluation, and Evaluation of Options tasks. This included determining

the processes to be modeled, specific agencies to be evaluated, and agreements on various financial and

operational criteria and assumptions. This task provided the basis for the activities to be performed in

Tasks 3, 4, and 5. We made numerous data and record requests on which to base our analysis. A list of the

documents and key information reviewed is included in Appendix E.

1—Objectives and Approach Business Case Study

Final ReportPage 1-4 kpmg

For the BPR Task, KPMG:

! Reviewed the State’s goals and underlying business strategies

! Developed a high-level process flow model of 15 selected business processes

! Identified opportunities for improvements in the current performance of selected businessfunctions, processes, overall business process integration, and the Chart of Accounts used by thefive FFMIS subsystems

! Quantified the current performance of selected business processes and compared them to thereengineering improvements

! Made recommendations for business process reengineering

! Determined the strategic impact and economic benefits of selected business processimprovements

! Coordinated the business process reengineering with the evaluation of system options

For the IT Assessment and Evaluation Task, KPMG evaluated the five options, in three steps:

! Assessed the existing FFMIS

! Developed system requirements including existing and future technologies for our analysis of thefive system options

! Defined the five options for which we prepared implementation cost estimates and operationalcost estimates

For the Evaluation of Options Task, KPMG prepared a TCO estimate and a ROI analysis for an average

5-year implementation period and an average 10-year operational period. The TCO estimate for each

option included the following cost factors:

! Required hardware (that is, production, testing, training, and user “sandbox”)

! Software (system software and utilities, core application software, and applicable third-partysoftware)

! Database

! Network and connectivity requirements

! Desktop

! Peripherals

! Interfaces

! Hardware and software maintenance

! State staff (that is, project management team, core project team, technical team, and users)

Business Case Study 1—Objectives and Approach

Final ReportPage 1-5 kpmg

! Consultants (that is, process reengineering, common data conversion, system configuration, andimplementation)

! Training

! Operations support (that is, technical and help desk support)

! Overhead allocations

KPMG analyzed the TCO during the following stages, as applicable to each option:

! Planning—Costs to develop the To-Be vision and detailed requirements

! Evaluation—Costs incurred in the selection process for the application software, hardware, andconsultants, and during the contract negotiation process

! Implementation—Costs incurred for sizing and placement of technology infrastructure, data andprocess design, data cleansing, migration and reconciliation, integration with legacy and third-party applications, customizations, testing, development of new processes and relateddocumentation, and change management

! Operation—Costs to support the application software and hardware after they have beenimplemented and for supporting existing hardware and software during any transition period

! Upgrades—Cost to upgrade (that is, resizing infrastructure, customizations, testing new releases,and retraining)

The financial analysis included cost savings identified in the BPR Task and investments required from the

IT Assessment and Evaluation Task. ROI analysis consists of those benefits that support the State’s

strategy, vision, and direction such as:

! Reducing waste, fraud, and abuse in State government

! Supporting the ability to move to improved performance-based budgeting

! Improving the sharing of information between government agencies and between the governmentand the public

! Realizing e-commerce savings to the government and public

KPMG analyzed various tangible ROI metrics including net present value, internal rate of return, and

payback period. KPMG then prepared a summarized analysis of the strategic, operational, technical, and

financial impacts of each alternative. The evaluation included the advantages and disadvantages

associated with each system option. KPMG considered the functional and technical requirements;

strategic, project, and continuation risks; the costs of operations and implementation; and other BPR

savings for each option. We have recommended one option for the State of Florida to pursue, which is

presented in Section 7 of this report.

1—Objectives and Approach Business Case Study

Final ReportPage 1-6 kpmg

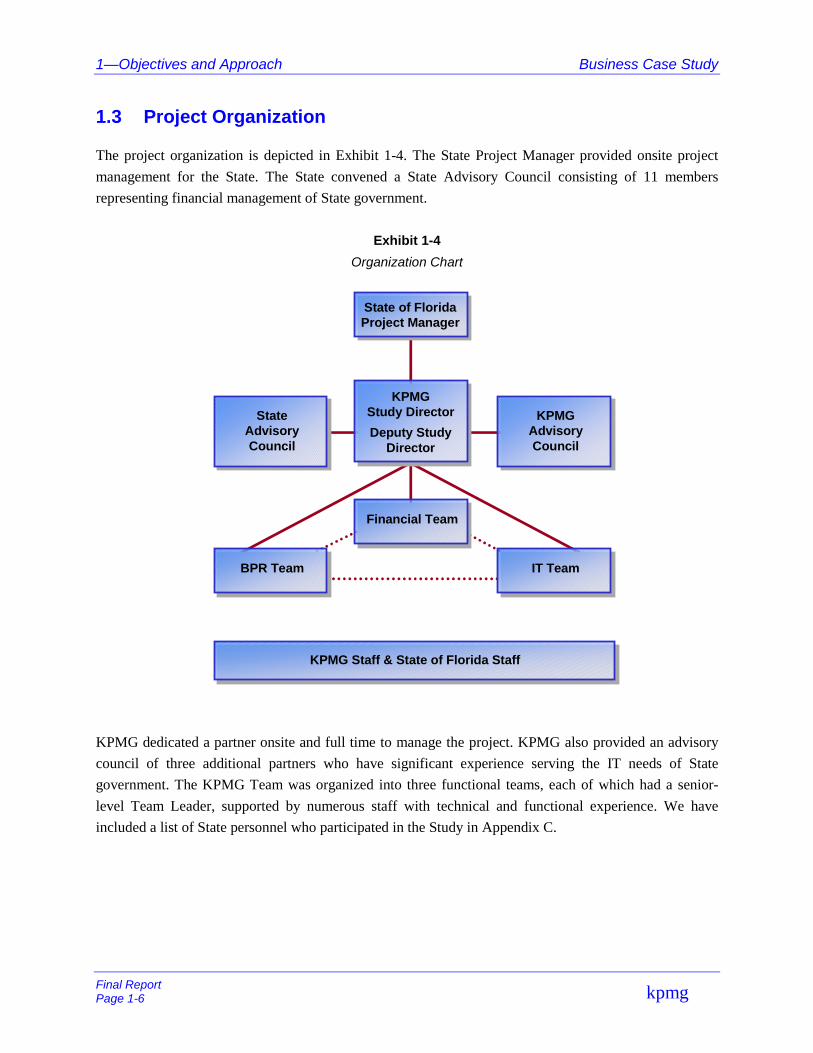

1.3 Project Organization

The project organization is depicted in Exhibit 1-4. The State Project Manager provided onsite project

management for the State. The State convened a State Advisory Council consisting of 11 members

representing financial management of State government.

Exhibit 1-4

Organization Chart

KPMG dedicated a partner onsite and full time to manage the project. KPMG also provided an advisory

council of three additional partners who have significant experience serving the IT needs of State

government. The KPMG Team was organized into three functional teams, each of which had a senior-

level Team Leader, supported by numerous staff with technical and functional experience. We have

included a list of State personnel who participated in the Study in Appendix C.

State of FloridaProject Manager

KPMGStudy Director

Deputy StudyDirector

Financial Team

StateAdvisoryCouncil

KPMGAdvisoryCouncil

BPR Team IT Team

KPMG Staff & State of Florida Staff

Business Case Study 1—Objectives and Approach

Final ReportPage 1-7 kpmg

1.4 Communication

Both KPMG and the State’s Study Management Team recognized that effective lines of communication

are essential to the success of the Study. To ensure effective communications, an official Communications

Plan for the Study was developed. The purpose of this Plan was to summarize the process for creating

effective lines of communication both to and from the Study team. Ultimately, the goal was to enlist the

support and commitment necessary for the success of the Study, as well as the acceptance and adoption of

the Study’s recommendations. The Plan identified more than 500 stakeholders in the Study. The

stakeholders were informed of the Study’s purpose and have received regular updates on the Study’s

progress.

1.5 Report Organization

The Business Case Study final report is organized as follows:

! Section 1, Objectives and Approach, identifies the State of Florida’s objective in undertaking theModernization of State Government Financial Management Business Practices Study. ThisSection also outlines the approach that the State and KPMG adopted to achieve the objective

! Section 2, Current Environment, describes the existing management information system and itsfive subsystems

! Section 3, Business Process Reengineering, lists the 16 major financial processes analyzed anddescribes the current process and our recommendations for reengineering them

! Section 4, IT Assessment, identifies the elements analyzed to gain an understanding of and todocument the FFMIS subsystems

! Section 5, System Requirements, delineates the key technical and business requirements

! Section 6, Options Analysis, provides KPMG’s in-depth analysis of the five options, includinggeneral assumptions and criteria

! Section 7, Recommendation, presents KPMG’s evaluation of the five options. This Sectiondescribes a vision for the State’s technology infrastructure; compares the functionality, risk, andfinancial impact of each option; and presents its recommendation

The appendices contain the following information:

! Appendix A, Innovative Practices, details the results of research conducted on key processimprovement strategies successfully used by companies and government agencies

! Appendix B, Risk Multiplier, presents the risk-adjusted contingency rate used to account forperceived risk of additional project expense for each of the five options analyzed

1—Objectives and Approach Business Case Study

Final ReportPage 1-8 kpmg

! Appendix C, List of Participants, identifies the personnel and organizations that participated inthe Study

! Appendix D, Cost Detail, presents the BPR savings associated with each of the five options, aswell as the total costs of operation for each option

! Appendix E, Research Documents, lists the documentation used during the Study

! Appendix F, Preliminary Implementation Plan, provides a sample high-level project plan for therecommended option

! Appendix G, High Level Infrastructure Schematic, depicts the infrastructure for four of theoptions analyzed

Business Case Study 2—Current Environment

Final ReportPage 2-1kpmg

2. Current Environment2.1 Overview

In 1980, the Florida Legislature enacted the Florida Fiscal Accounting Management Information System

(FFAMIS) Act (Chapters 215.90-215.96, Florida Statutes). The Act’s purpose was to design and

implement a management information system through a unified approach with the following goals:

! Strengthening and standardizing management and accounting procedures

! Strengthening internal controls

! Enabling the preparation of objective, accurate, and timely fiscal reports

! Reporting on the stewardship of officials who are responsible for public funds or property

! Providing timely and accurate information for decision making

Since its enactment in 1980, the FFAMIS Act has been modified 12 times. In 1997, the name of the Act

(Chapter 215.93, Florida Statutes) changed to the Florida Financial Management Information System

(FFMIS) Act. Exhibit 2-1 shows the five functional subsystems of FFMIS.

Exhibit 2-1Five Functional Subsystems of FFMIS

System Function System Name System Owner

Accounting Florida Accounting InformationResource Subsystem

FLAIR Department of Banking and Finance

Human Resources Cooperative PersonnelEmployment Subsystem

COPES Department of ManagementServices

Purchasing Statewide PurchasingSubsystem

SPURS Department of ManagementServices

Budgeting Legislative AppropriationSystem—Planning andBudgeting Subsystem

LAS/PBS Executive Office of the Governor

Cash Management Cash Management Subsystem CMS Department of Insurance, Treasuryand State Fire Marshal

The subsystems of FFMIS underwent extensive modifications between their respective development,

pilot, and implementation dates. Exhibit 2-2 reflects those dates.

2—Current Environment Business Case Study

Final ReportPage 2-2

kpmg

Exhibit 2-2FFMIS Development, Pilot, and Implementation Dates

Subsystem

InitialDevelopmentDate

PilotImplementationDate

ImplementationDate

FLAIR July 1980 July 1982 July 1986

COPES July 1980 July 1981 July 1982

SPURS October 1985 May 1988 May 1988

LAS/PBS July 1982 July 1983 July 1983

CMS July 1982 July 1982 July 1982

The FFMIS subsystems have many users statewide. Exhibit 2-3 summarizes the approximate number of

current subsystem users.

Exhibit 2-3Approximate Number of FFMIS Subsystem Users

Subsystem Number of Users (approximate)

FLAIR 14,300

COPES 4,000

SPURS 6,400

LAS/PBS 486

CMS 30

Business Case Study 2—Current Environment

Final ReportPage 2-3kpmg

2.2 FLAIR

FLAIR is a double-entry, computer-based general ledger accounting subsystem consisting of four

components:

! Departmental Accounting System—Maintains agency accounting records and is used at the endof each fiscal year to prepare financial statements in accordance with Generally AcceptedAccounting Principles

! Central Accounting System—Maintains cash basis records and is used by the Comptroller toensure that expenditures are made in accordance with the legislative appropriations

! Payroll Accounting—Processes the State’s payroll

! Information Warehouse—A reporting system that allows users to access the Central AccountingSystem information and limited Departmental Accounting System information from FLAIR

The Department of Banking and Finance is the functional owner of FLAIR. While all agencies and

universities use FLAIR for their primary accounting functions, numerous other specialized accounting

systems are used by State agencies in addition to FLAIR.

FLAIR has been expanded and enhanced many times during the past 17 years. The most recent

expansions were the implementation of the Purchasing Card (PCard) in July 1997 and Electronic Data

Interchange (EDI) of invoices in July 1998. During Fiscal Year 2000, the Department of Banking and

Finance will focus on short-term enhancements that emphasize electronic commerce.

The State has the following projects planned or currently underway for FLAIR:

! Vendor History on the Web—Vendors will be able to access their payment history directly fromthe web site thus reducing vendor interaction and encouraging electronic fund transfer (EFT)

! Electronic Invoicing Through the Internet—This application allows invoices to be input via theInternet and processed through the invoice tracking system. Ideally, this application will allowvendors to query the statuses of their invoices through the Internet

! Electronic Routing of Earnings Statements to Department of Banking and Finance Employees—This project provides the earning statements of employees on the Internet

! EFT to Miscellaneous Deduction Vendors—This application provides the capability to transfermiscellaneous payroll deductions to vendors electronically

2—Current Environment Business Case Study

Final ReportPage 2-4

kpmg

2.3 COPES

COPES is the statewide online personnel subsystem used by all State agencies (excluding the State

University System, Auditor General, Legislature, and the Board of Regents) to maintain human resource

records for approximately 140,000 employees. This subsystem includes functions for maintenance of

employee and position data, including funding sources and percentages and salary lapse; recruitment and

examination; time reporting; and collective bargaining. The Department of Management Services is the

functional owner of COPES.

COPESView provides a snapshot of COPES and is updated daily with downloads from COPES. Users

can create and run reports using tools such as Impromptu. COPESView can be accessed via the State’s

intranet.

During the past 10 years, significant modifications to COPES occurred when more than 40,000

employees of the Department of Children and Families and the Department of Health agencies were

added to COPES. During the past 3 years, enhancements to COPES have been on hold because the

Human Resources and Payroll project that was piloting a replacement to the current Human Resources

and Payroll subsystems.

The State has the following projects planned or currently underway for COPES:

! COPES DIRECT—A web site is under development to make COPES information available viathe State’s intranet to aid in paper reduction, training, and better communication to COPES users.Browser-based transactions and reports are also being developed. Most of these transactionsprovide functionality that does not exist in the mainframe environment

! Employee DIRECT—This web site links areas of interest to employees in one location. Theemployees’ personal and leave information will be available for them to review. Whereappropriate, employees will be provided the capability to update their personal information suchas telephone numbers and emergency contact information. Various statewide forms will beavailable electronically. A solution will also be developed to provide employees’ earningsstatements electronically

! COPES Security System—The COPES security system was developed with physical securityfeatures (that is, the actual workstation on which the user enters data must be known to thesecurity system and is validated when the user signs on). Today’s mobile workforce would bebetter served by changing the security system to one that requires user IDs and passwords forauthenticating a user

Business Case Study 2—Current Environment

Final ReportPage 2-5kpmg

2.4 SPURS

SPURS is the automated commodity procurement (purchasing) subsystem for the State of Florida.

SPURS provides purchasing information for decision making by customers, management, and legislators,

and provides operational systems for effective and efficient purchasing operations by State agencies. The

subsystem is used by the Executive Branch agencies of State government for the creation of requisitions,

purchase orders, vendor bid lists and mailing labels, and a variety of other standard purchasing functions.

The Department of Management Services is the functional owner of SPURS.

SPURSView provides a “snapshot” copy of SPURS. Users perform queries and reporting from the

Internet and intranet.

The Vendor Bid System (VBS) allows an agency user to advertise its bids and requests for proposals on

the Internet and publish the documents on the Internet. VBS notifies registered vendors of the bids via

e-mail.

Over the last decade, a number of important modifications and enhancements were made to SPURS

including:

! System Security—A new security system was developed and implemented in the CommodityProcurement component of SPURS

! FLAIR/SPURS Financial Interface—SPURS interfaces online in real time with FLAIR forvendor updates, account code validation, and fund encumbrance additions, updates, and deletions.In addition, users can inquire on fund encumbrances and account balances

The State has the following projects planned or currently underway for SPURS:

! Electronic Commerce—This initiative includes a web-based electronic requisition component,EDI of purchase orders from the mainframe to approved trading partners, and VBS enhancements

! Other SPURS Mainframe Applications Development—Modifications will be made to theStatewide Vendor File to provide additional Certified Minority Vendor information

! Agency Implementations—Tentative plans call for the addition of two agencies during FiscalYear 2000: the Office of the Auditor General, and Office of Program, Policy Analysis, andGovernment Accountability

2—Current Environment Business Case Study

Final ReportPage 2-6

kpmg

2.5 LAS/PBS

LAS/PBS is the State’s automated budgeting and appropriation subsystem. This subsystem is used by all

branches of State government for developing, preparing, analyzing, and evaluating State agency budget

requests. The Executive Office of the Governor and the Office of Policy and Budgeting use LAS/PBS to

develop the Governor’s budget recommendations and to allocate and control the appropriations. The

legislative appropriations committees use the subsystem to create the appropriations bills, including the

proviso and other controlling language used to document the legislative intent and create a basis to enable

the agencies to manage their agencies consistent with such legislative intent. The budgeting and

appropriating process produces the General Appropriations Act and its supplements. The Executive

Office of the Governor is the functional owner of LAS/PBS.

During the mid- to late-1980s, modifications and enhancements were made to LAS/PBS including the

following:

! LAS merged with PBS to form the current LAS/PBS

! The Virtual Storage Access Method files were replaced with Software AG’s ADABAS databasemanagement system, and its fourth-generation language, Natural, became the primaryprogramming language

During the last decade, a number of important enhancements were made to LAS/PBS including the

following:

! The Systems Design and Development section enhanced LAS/PBS by developing auxiliarysystems in Lotus Notes and Visual Basic that increase functionality

! Heavily used modules in LAS/PBS have been rewritten to operate as much like a personalcomputer as possible. Pop-up windows and hierarchical help are provided. Both application-leveland field-level help have been added

! LAS/PBS is mission critical and therefore provides for Direct Access Storage Device mirroring,hot-site backup, 24x7 vendor and staff support, and disaster recovery

The State has the following projects planned or currently underway for LAS/PBS:

! Multitier client/server

! Relational database management systems

! Network-based computing

! Graphical user interfaces

! Local area networks, Internet/intranet, Groupware, and e-mail

Business Case Study 2—Current Environment

Final ReportPage 2-7kpmg

2.6 CMS

Owned by the Department of Insurance, Treasury, and Fire Marshal, CMS is a collection of 13 systems.

These systems facilitate the Treasurer’s responsibilities for monitoring cash levels and activities in State

bank accounts, receipt and disbursements of funds, investment of available balances, performance of

related accounting functions, and cash management operations and consultations.

During the last decade, a number of important enhancements and modifications were made to CMS

including the following:

! The Treasurer purchased an IBM AS/400 mid-range computer

! A client/server-based front end was developed for the interactive portions of the applications

! The original COBOL programs were migrated to the AS/400 and they continued to be used forovernight processing

! The Treasurer updated its PC operating system to Windows 95

! Seventy percent of the Treasurer’s processing is now in an interactive mode, while 30 percent isbatch processing using COBOL

The State has the following projects planned or currently underway for CMS:

! During Fiscal Year 2000, the Treasurer will establish an interactive web site on an AS/400 server.The web site will include interactive capabilities for general and administrative functions relativeto activities of the Treasurer

! Automation of the receipt and verification of incoming Automated Clearing House (ACH)Payments will replace the use of telephone and facsimile with electronic means to notify agenciesof incoming ACH payments, automate FLAIR verification, and pass on other income, such asaddenda data that is received with payments

Other current initiatives include the development of electronic data exchange, enhancement of

communications and functionality, a return items application, and consolidation of revolving accounts

transactions and statements.

2—Current Environment Business Case Study

Final ReportPage 2-8

kpmg

This page intentionally left blank.

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-1

kpmg

3. Business Process Reengineering3.1 Overview

The BPR analysis of the State of Florida’s financial management processes identified several

recommendations for improvement. If implemented, these recommendations would increase the

availability of financial management information through more user-friendly processes, reduce the time

needed to carry out financial management processes, and increase efficiency. When the estimated fiscal

impacts of all the recommendations are taken together, the estimated annual savings totals $97 million.

This includes $91 million in anticipated budgetary reductions and $6 million in increased efficiencies.

The BPR analysis was undertaken in the context of assessing five options for addressing the State of

Florida’s need for an automated financial management system. The five options are shown in Exhibit 3-1.

Exhibit 3-1Options

Option 1 As-Is Maintain the current legacy systems as-is with no major modifications or upgrades

Option 2 Enhanced Enhance current systems by adding new tools and functionality

Option 3 Custom Develop a new custom integrated information management system

Option 4 COTS Implement a commercial off-the-shelf Enterprise Resource Planning package

Option 5 Best of Breed Use some combination of the other four options

Although some of the recommendations for reengineering the State’s financial management processes can

be implemented with the current automated system (Option 1), most of the recommendations require

either a significant upgrade of the current system or its replacement. Of the $91 million in annual

budgetary savings, only $24 million can be achieved if no change in the automated system is undertaken.

An additional $36 million in annual savings can be achieved with Option 2, but only with Options 3, 4,

and 5 can all $91 million in budgetary savings be achieved.

The remainder of this section includes a discussion of the background, assessment of current processes,

reengineering themes, and fiscal impact that resulted from the BPR analysis.

Background

The purpose of a financial management system is to automate an organization’s financial management

processes. Maximum benefit is derived from the automated system if the processes are efficient and if

they make use of the automated system’s fullest capabilities. To understand the customer service and

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-2

kpmg

fiscal impact of a decision to keep, upgrade, or replace the State of Florida’s financial management

system, we have undertaken a BPR analysis of selected financial management processes. The purpose of

this analysis is to identify better ways to carry out financial management processes and to document the

expected impacts on quality, service, and costs.

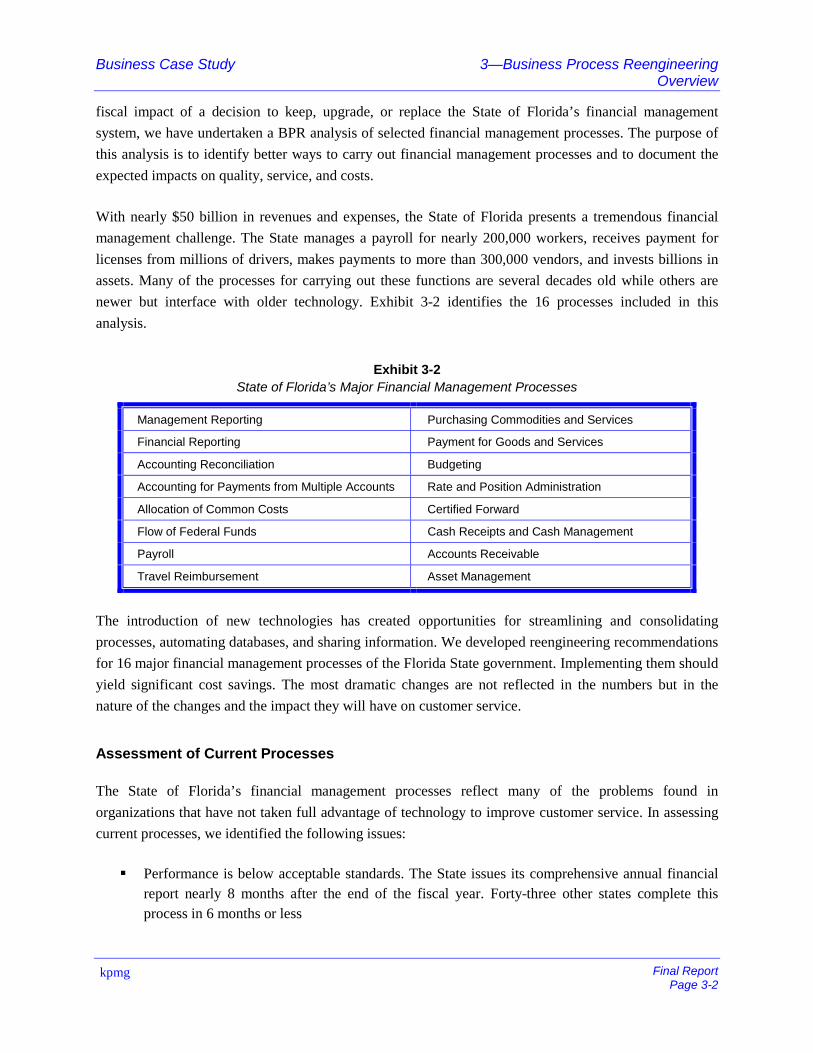

With nearly $50 billion in revenues and expenses, the State of Florida presents a tremendous financial

management challenge. The State manages a payroll for nearly 200,000 workers, receives payment for

licenses from millions of drivers, makes payments to more than 300,000 vendors, and invests billions in

assets. Many of the processes for carrying out these functions are several decades old while others are

newer but interface with older technology. Exhibit 3-2 identifies the 16 processes included in this

analysis.

Exhibit 3-2State of Florida’s Major Financial Management Processes

Management Reporting Purchasing Commodities and Services

Financial Reporting Payment for Goods and Services

Accounting Reconciliation Budgeting

Accounting for Payments from Multiple Accounts Rate and Position Administration

Allocation of Common Costs Certified Forward

Flow of Federal Funds Cash Receipts and Cash Management

Payroll Accounts Receivable

Travel Reimbursement Asset Management

The introduction of new technologies has created opportunities for streamlining and consolidating

processes, automating databases, and sharing information. We developed reengineering recommendations

for 16 major financial management processes of the Florida State government. Implementing them should

yield significant cost savings. The most dramatic changes are not reflected in the numbers but in the

nature of the changes and the impact they will have on customer service.

Assessment of Current Processes

The State of Florida’s financial management processes reflect many of the problems found in

organizations that have not taken full advantage of technology to improve customer service. In assessing

current processes, we identified the following issues:

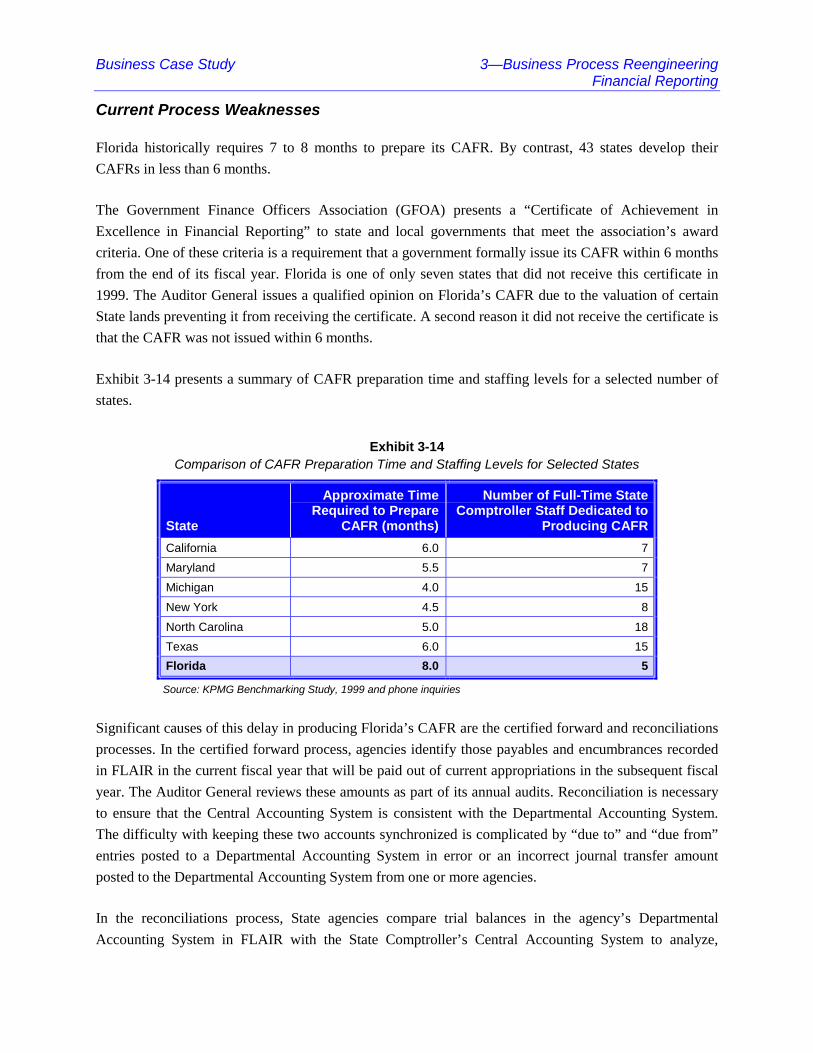

! Performance is below acceptable standards. The State issues its comprehensive annual financialreport nearly 8 months after the end of the fiscal year. Forty-three other states complete thisprocess in 6 months or less

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-3

kpmg

! System capabilities do not meet customer needs. The clearest evidence is that agencies havepurchased or developed numerous supplemental systems to overcome limitations in systemfunctionality. An agency may have one or more of the following modules supplementing thestatewide accounting systems: grants management, accounts receivable, cash receipts, journaltransfer, project cost, position control, reconciliation, leave and attendance, payroll tracking, andcertified forward. In many cases, agencies download data from the Florida AccountingInformation Resource (FLAIR) subsystem to PC-based spreadsheets and databases to analyze andreport financial information

! Key steps in the process are not automated. Entry of travel vouchers and positive pay timekeeping, purchasing, and vendor payments are initiated using paper processes. The centralizeddata entry is redundant in the preparation of manual forms

! Selected policies place a tremendous burden on staffing resources with little added value. Assetmanagement, certified forward, financial reporting, and rate and position administration require alarge staff. The experiences of other states and large corporations show that the goals of theseprocesses can be achieved using more streamlined and efficient processes

! Key building blocks of the financial management system impede efficient operations. FLAIRincludes two ledger systems: Central Accounting System (Comptroller Records/Cash Basis) andDepartmental Accounting System (Agency Record/Accrual Basis). This fact by itself creates theneed for a reconciliation process. In addition, a significant amount of work—checking,reconciling, verifying, and ad hoc reporting—is caused by variations among agencies in the Chartof Accounts

The impact of these shortcomings in the current processes is manifested through an unacceptably high

cost for managing the State’s financial resources.

Reengineering Themes

The reengineered processes address major weaknesses with current processes. Among the goals are

improving customer service, reducing costs, and reducing cycle times. The recommendations cluster

around several themes. These themes and the reengineering recommendations associated with them are

summarized as follows:

! Develop an enterprisewide perspective on State government financial operations

– Establish a statewide single Chart of Accounts

– Consolidate central and department accounting into one enterprisewide accounting system

– Establish an enterprisewide policy for accounts receivable and a database capable ofenforcing a “clean hands” law

– Establish a semi-monthly payroll statewide

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-4

kpmg

– Consolidate payroll support functions into five shared service cluster units

! Expand the functionality of the financial management system

– Modify the system to enable disbursements against more than one account

– Automate the process of calculating and reporting indirect (common) costs

– Develop a grants management system and automate the process of matching federal fundsreceipts

! Automate manual steps and reduce excess paper

– Introduce electronic auditing of invoices and exception reporting for in-depth audits

– Fold most supplemental warrants into the regular payroll warrant and issue only one pay stub

– Decentralize data entry for employees entering time and travelers seeking reimbursement

– Automate the interface between the accounting system and the budget system

! Provide better financial management information for more cost-effective decisions

– Use better financial management information, shift up to $1 billion in assets from the internalprogram to the higher yielding external program

– Create a statewide financial information data warehouse for the collection and reporting offinancial management information

! Increase the use of e-commerce

– Decentralize purchasing and verification of receipt of goods and services to the lowestpossible level within service delivery units

– Decentralize and automate the payment process

– Require that all vendors doing business with the State have e-commerce capabilities (onlineinvoicing and payment) by 2002

– Establish online automated reconciliation with banks

– Require that all travel reimbursement be remitted through electronic funds transfer

! Update and modernize policies and procedures

– Raise the definition of a capital asset to $5,000 for tracking purposes and reduce thefrequency of physical inventory

– Make the acceptance of debit cards a statewide standard

– Terminate the certificate of deposit program aimed at Florida banking institutions

– Eliminate the detailed certified forward process—review obligations by exception rather thancomprehensively and estimate year-end obligations

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-5

kpmg

– Make salary rate a direct function of salary appropriations to simply calculation of ratethroughout the year

– Remove travel parameters from the Florida Statutes and place them in administrative rules

Except for the last set of recommendations under the theme “Update and modernize policies and

procedures,” most of the recommendations do not require legislative action beyond the authorization for

funds to replace or upgrade the Florida Financial Management Information System (FFMIS).

Fiscal Impact

Taken together, the fiscal impact of all the reengineering recommendations is significant. Fiscal impacts

are labeled in two ways—budgetary savings and increased efficiency. Budgetary savings reflect the

potential for reductions in full-time equivalent (FTE) positions and consequently reductions or redirection

of budgetary resources. Increased efficiency reflects a reduction in the labor necessary to carry out a

process, but that reduction is either too small or spread across so many staffs that FTE reductions are not

expected to result. Exhibit 3-3 presents the total fiscal impact of all the Business Case Study

recommendations. The fiscal impact of the recommendations has been presented separately for Option 1

and Option 2. The fiscal impact of the recommendations is the same for Option 3, 4 and 5 and is

presented once at the end of Exhibit 3-3.

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-6

kpmg

Exhibit 3-3Summary of Business Process Reengineering Savings by Process

Net Budgetary Savings Net Increased Efficiency

ProcessTechnologyDependent Other

TechnologyDependent Other Total Savings

Option 1: As-Is

Management Reporting $0 $0 $0 $0 $0

Financial Reporting 0 (100,000) 0 0 (100,000)

Reconciliation 0 0 0 0 0

Accounting Payments for Multiple Accounts 0 0 0 0 0

Allocation of Common Costs 0 0 0 0 0

Flow of Federal Funds 0 0 0 0 0

Payroll 0 0 0 0 0

Travel Reimbursement 0 3,482,000 0 0 3,482,000

Purchasing Commodities and Services 0 0 0 0 0

Payment for Goods and Services 0 0 0 0 0

Budgeting 0 0 0 0 0

Rate and Position Administration 0 0 0 0 0

Certified Forward 0 3,125,000 0 3,125,000

Cash Receipts and Cash Management 0 14,656,000 0 0 14,656,000

Accounts Receivable 0 0 0 193,000 193,000

Asset Management 0 2,528,000 0 1,514,000 4,042,000

Option 1: As-Is Total $0 $23,691,000 $0 $1,707,000 $25,398,000

Option 2: Enhanced

Management Reporting $0 $0 $0 $0 $0

Financial Reporting 56,000 (100,000) 90,000 0 46,000

Reconciliation 0 0 145,000 0 145,000

Accounting Payments for Multiple Accounts 0 0 0 0 0

Allocation of Common Costs 0 0 0 0 0

Flow of Federal Funds 0 0 0 0 0

Payroll 6,038,000 0 0 0 6,038,000

Travel Reimbursement 0 3,482,000 0 0 3,482,000

Purchasing Commodities and Services 16,910,000 0 0 0 16,910,000

Payment for Goods and Services 1,500,000 0 0 0 1,500,000

Budgeting 0 0 1,217,000 0 1,217,000

Rate and Position Administration 0 0 0 0 0

Certified Forward 0 3,125,000 0 3,125,000

Cash Receipts and Cash Management 10,000,000 14,656,000 0 0 24,656,000

Accounts Receivable 0 0 0 193,000 193,000

Asset Management 0 2,528,000 0 1,514,000 4,042,000

Option 2: Enhanced Total $34,504,000 $23,691,000 $1,452,000 $1,707,000 $61,354,000

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-7

kpmg

Exhibit 3-3 (continued)Summary of Business Process Reengineering Savings by Process

Net Budgetary Savings Net Increased Efficiency

ProcessTechnologyDependent Other

TechnologyDependent Other Total Savings

Option 3: Custom, Option 4: COTS, andOption 5: Best of Breed

Management Reporting $0 $0 $0 $0 $0

Financial Reporting 56,000 (100,000) 90,000 0 46,000

Reconciliation 2,848,000 0 145,000 0 2,993,000

Accounting Payments for Multiple Accounts 0 0 2,783,000 0 2,783,000

Allocation of Common Costs 2,324,000 0 0 0 2,324,000

Flow of Federal Funds 303,000 0 0 0 303,000

Payroll 8,054,000 0 0 0 8,054,000

Travel Reimbursement 3,260,000 3,482,000 0 0 6,742,000

Purchasing Commodities and Services 22,335,000 0 0 0 22,335,000

Payment for Goods and Services 17,905,000 0 0 0 17,905,000

Budgeting 0 0 1,217,000 0 1,217,000

Rate and Position Administration 0 0 73,000 0 73,000

Certified Forward 0 3,125,000 0 3,125,000

Cash Receipts and Cash Management 10,000,000 14,656,000 0 0 24,656,000

Accounts Receivable 0 0 0 193,000 193,000

Asset Management 0 2,528,000 178,000 1,514,000 4,220,000

Option 3: Custom, Option 4: COTS, andOption 5: Best of Breed Total

$67,085,000 $23,691,000 $4,486,000 $1,707,000 $96,969,000

A summary by option of the fiscal impact of the BPR recommendations is shown in Exhibit 3-4.

Exhibit 3-4Summary of Fiscal Impacts by Option

Net Budgetary Savings Net Increased Efficiency

OptionsTechnologyDependent Other

TechnologyDependent Other

TotalSavings

Option 1 – As Is $ 0 $ 23,691,000 $ 0 $ 1,707,000 $ 25,398,000

Option 2 – Enhance 34,504,000 23,691,000 1,452,000 1,707,000 61,354,000

Option 3 – Custom 67,085,000 23,691,000 4,486,000 1,707,000 96,969,000

Option 4 – COTS 67,085,000 23,691,000 4,486,000 1,707,000 96,969,000

Option 5 – Best of Breed 67,085,000 23,691,000 4,486,000 1,707,000 96,969,000

Business Case Study 3—Business Process ReengineeringOverview

Final ReportPage 3-8

kpmg

Savings can be achieved through reengineering the State’s financial management processes. The largest

saving, however, is expected to result from implementing Options 3, 4, and 5. These options represent a

comprehensive change in the underlying automated system that supports financial management in the

State of Florida.

Business Case Study 3—Business Process ReengineeringMethodology

3.2 Methodology

This section presents the methodology used for designing reengineered financial management processes

for the State of Florida. The methodology consisted of three components:

! Process identification

! Process analysis

! Extrapolation

Process is defined as a series of steps or activities that enable an organization to meet a customer need.

These steps may cross organizational boundaries and usually involve the customer as well. To conduct the

process analysis, we assess the current process, which is sometimes called the As-Is process. Current

processes are usually defined from the organizational perspective and limited by organizational

boundaries. The result of the process analysis is the development of a reengineered process, which is also

known as the To-Be process. Reengineered processes are usually defined from the customer’s

perspective.

Processes begin with a customer request or need and end when that request or need is fulfilled. Customers

of Florida’s financial management processes include customers internal to State government as well as

external individuals and businesses.

Process Identification

Florida State government has numerous financial management processes. Some processes such as the

certified forward process require a small amount of time from a large number of people, while other

processes such as payroll and purchasing require a large amount of time from a centralized staff dedicated

to the process. For this analysis, we focused on the major processes that have a significant impact on costs

or decision making. Furthermore, the analysis focuses on processes that require the use of an automated

financial management system. The three major steps used in identifying the processes included the

following:

! Identify what customers need and request

! Identify the customers

! Identify the roll played in the process by FFMIS

For the first step, KPMG identified customer needs that are fulfilled by financial management processes.

Although customers want different kinds of financial and program performance information, the process

of obtaining that information is still the same from the customer’s point of view. The customer makes a

Business Case Study 3—Business Process ReengineeringMethodology

request; then, someone in the organization queries one or more databases, manipulates numbers, and

produces a report. Although the actual steps that the agency staff follow may differ according to the

agency or nature of the information request, all of these steps can be seen as one process. A summary of

customer-oriented financial management needs is provided in Exhibit 3-5.

Next, we identified the customers. The customers are the internal employees or organizational units or

external individuals or businesses that rely upon a financial management process to meet a particular

need. Most of the processes that we identified have multiple customers. Column 2 of Exhibit 3-5 provides

a listing of the customers by category of need.

Finally, we note the role that FFMIS plays in supporting the process. The level of support for financial

management processes can vary. Some processes such as those for reporting management information,

rely almost exclusively on FFMIS; others such as budget formulation include many steps that may not

interface with FFMIS or any of its subsystems.

Exhibit 3-5Summary of Customer Needs

Needs Fulfilled Through FFMIS Who Needs It?

To know how money is spent Citizens, Legislators, Governor, CabinetAgencies, Department Heads, Unit Managers,Grantors, Creditors

To know the status of their investments Citizens, Legislators, Governor, CabinetAgencies, Department Heads, Unit Managers,Grantors, Creditors

To obtain/make appropriations for the next year Legislators, Governor, Cabinet Agencies,Department Heads

To manage end of year spending Governor, Cabinet Agencies, Department Heads

To receive non-tax revenue and to make it available forexpenditure

Governor, Unit Managers, Cabinet Agencies,Department Heads

To monitor the deployment of human resources Governor, Unit Managers, Cabinet Agencies,Department Heads

To monitor and record purchases of commodities andservices

Legislature, Governor, Unit Managers, CabinetAgencies, Department Heads

To collect on overdue receivables Legislature, Governor, Cabinet Agencies,Department Heads, Unit Managers

To receive reimbursement, salary and benefits andrelated information

Employees

To pay an amount owed to a vendor Legislature, Governor, Cabinet Agencies,Department Heads, Unit Managers

Business Case Study 3—Business Process ReengineeringMethodology

Through the process described above, we identified the following processes for analysis:

! Management reporting: Reporting of a wide range of financial management information primarilyto State managers

! Financial reporting: Developing the annual Comprehensive Financial Management Report(CAFR)

! Accounting reconciliation: Reconciling central accounts with agency accounts

! Accounting for payments from multiple accounts: Recording disbursements that should be paidagainst more than one account

! Allocation of common costs: Calculating and reporting of indirect costs to federal grantingagencies

! Flow of federal funds: Managing federal grant funds

! Payroll: Recording employee time and paying salaries

! Travel reimbursement: Reimbursing employees for expenses covered by the travel policy

! Purchasing commodities and services: Procuring commodities from vendors

! Payment for goods and services: Paying vendors for commodities purchased

! Budgeting: Tracking budgetary decision making and monitoring compliance

! Rate and position administration: Monitoring personnel expenditures

! Certified forward: Managing end-of-year spending

! Cash receipts and cash management: Receiving funds and making them available

! Accounts receivable: Collecting on overdue receivables

! Asset management

Through the process identification, two processes were not included and two were combined. We did not

include the administration of training because of the low impact that a new financial management system

would have on it. We also eliminated recruitment and hiring because FFMIS plays a small part in that

process. Receiving and purchasing were combined into one process—purchasing.

The process analysis consisted of two parts: the analysis of the current process and the development of a

prototype reengineered process.

Business Case Study 3—Business Process ReengineeringMethodology

Current Process Analysis

Analysis of current processes included the following steps:

! Develop high-level process maps

! Identify technology required to carry out the process

! Gather process metrics

! Identify cost components

! Identify strengths and weaknesses

The high-level process maps illustrate the major steps in a process and identify the organizational entities

that participate in the process. These maps usually include the customer to ensure that the customer’s

relationship to the process is documented. The maps also indicate where technology plays a role in

facilitating the process.

Different process metrics or measures of process performance are used in the process analysis. Among the

process metrics used is cycle time—the time that lapses from the point that the customer need is identified

or a request is made to the time that the need or request is fulfilled. Another common metric is process

time—the actual time it takes to carry out the process excluding waiting time between steps. Other key

process metrics are accuracy or error rates and customer satisfaction.

Cost is an important component of any process analysis. The cost analysis focuses on costs at three

levels—customer costs, agency costs, and centralized costs. The customer costs are costs associated with

initiating a process, such as completing a travel reimbursement voucher or recording time worked. Based

on this definition not all processes have customer costs.

Agency and centralized costs refer to the labor cost required to carry out the process. In the purchasing

process, for example, agency costs reflect the salaries of staff dedicated to processing purchase orders at

the agency level. Centralized costs are labor costs as well, but refer to costs incurred by agencies that have