KPMG Highlights KPMG IN INDIA KPMG Regulatory Highlights 21 February 2014 Foreign Direct Investment 1. Multi-brand Retail Trade Relaxations With an objective of granting greater flexibility to foreign investors, in August 2013, the following relaxations were granted for permitting Foreign Direct Investment (FDI) in Multi-brand Retail Trade (MBRT): 50 per cent of total FDI, brought in the first tranche of USD 100 million to be invested in back-end infrastructure (BI) within three years, and not on the total foreign investment brought in by the foreign investor Relaxation of mandatory sourcing rule by: − Increasing the investment limit in plant and machinery by Indian micro, small and medium enterprises to USD two million, as against the earlier limit of USD one million. It has also been clarified that the above investment limit would be tested only at the time of first engagement with such unit − Sourcing from agricultural and farmer’s cooperatives would also be counted for meeting the mandatory sourcing rule The States have been given flexibility to identify smaller cities for allowing the setting up of retail stores. The current rule of permitting supermarket chains in cities with a minimum population of one million, has been done away with.

Transcript

KPMG Highlights

KPMG IN INDIA

KPMG Regulatory Highlights

21 February 2014

Foreign Direct Investment

1. Multi-brand Retail Trade

Relaxations

With an objective of granting greater flexibility to foreign investors, in August 2013, the following relaxations were granted for permitting Foreign Direct Investment (FDI) in Multi-brand Retail Trade (MBRT):

50 per cent of total FDI, brought in the first tranche of USD 100 million to be invested in back-end infrastructure (BI) within three years, and not on the total foreign investment brought in by the foreign investor

Relaxation of mandatory sourcing rule by:

− Increasing the investment limit in plant and machinery by Indian micro, small and medium enterprises to USD two million, as against the earlier limit of USD one million. It has also been clarified that the above investment limit would be tested only at the time of first engagement with such unit

− Sourcing from agricultural and farmer’s cooperatives would also be counted for meeting the mandatory sourcing rule

The States have been given flexibility to identify smaller cities for allowing the setting up of retail stores. The current rule of permitting supermarket chains in cities with a minimum population of one million, has been done away with.

In the year 2012, the Government of India (GoI) issued Press Note No. 5 (2012 Series) permitting 51 per cent FDI in MBRT. On growing industry demand, the Department of Industrial Policy and Promotion (DIPP) issued certain clarifications on some of these key issues which are summarised below:

30 per cent sourcing from Small and Medium Enterprises (SMEs)

− The 30 per cent sourcing will be reckoned only with reference to front-end stores. The MBRT entity cannot engage in any other form of distribution

− Sourcing from SMEs pertains only to manufactured and processed products, and procurement of fresh produce is not covered by this condition.

50 per cent investment in BI

− Foreign investor can invest only in greenfield assets, and acquisition of supply chain/backend assets or stakes from an existing entity would not be counted for satisfaction of this condition. Front-end retail stores must be set up as additionality and not through acquisition of existing stores

− Acquisition of equity stake of less than 100 per cent of an existing infrastructure company will not be treated as investment in BI. A company operating in wholesale cash and carry trading (WCCT) will not be considered to be providing BI

− Minimum investment of 50 per cent in BI can be made across all states, irrespective of the state where the retail store is proposed to be set up

− Franchise model is not permissible as per extant FDI Policy on MBRT. The front-end stores set up by multibrand chains will have to be ‘company owned and company operated’ only.

Investment in Front-end/BI

− Investments in multiple infrastructure companies would not be counted towards the fulfillment of 50 per cent investment in BI

− Back-end and front-end entities can be owned by separate entities, that may be 100 per cent owned by a foreign entity, as long as the investor in MBRT is able to satisfy that 50 per cent of FDI brought for MBRT has been utilised in BI as an additionality

Others

− Certificate issued by the District Industries Centre would be adequate authentication to confirm status of supplier as a ‘Small industry’

− Census data is the most authoritative source of population data, which is accepted by all the States. No other data source or self-certification would be permissible

− State laws/regulations would apply in respect of implementation of stipulations in MBRT and States can impose additional conditions if required.

− Online sales in respect of MBRT are not permitted.

Source: Press Information Bureau (PIB) press release dated 6 June, 2013/Press Note 5 of 2013 dated 22 August, 2013 issued by the DIPP

2. Review of definition of ‘control’ for calculation of foreign investment in Indian companies

In August 2013, the Cabinet approved the proposal for modifying the existing definition of ‘control’ under the FDI policy. The revised definition has been aligned with the definition in Substantial Acquisition of Shares and Takeovers (SAST) Regulations (SEBI Takeover Regulations), and Companies Act, 2013. The new prospective definition of ‘control’ includes the right to appoint a majority of the directors or to control the management or policy decisions, including by virtue of their

shareholding/management rights or shareholders/voting agreements.

The definition of ‘control’ has been expanded to cover control exercisable inter-alia through management and policy decisions, shareholding, management rights and shareholder agreements.

Source: Press Note 4 of 2013 dated 22 August, 2013 issued by the DIPP

3. Relaxation of caps and routes of FDI in various sectors

The GoI also relaxed the sectoral caps and entry routes for FDI in various sectors, earlier approved in a high level meeting chaired by the Prime Minister in July, 2013. The extant and revised sectoral caps and entry routes have been tabulated below:

The GoI’s move to liberalise and grant automatic entry to minority investment by foreign investors in multiple sectors is aimed at mitigating requirement to seek prior approval and to facilitate a smoother and quicker inflow of foreign investments in these sectors.

Source: Press Note 6 of 2013 dated 22 August, 2013 issued by the DIPP

4. FDI in pharmaceutical sector

In terms of extant FDI Policy, 100 per cent foreign investment is allowed in the pharmaceutical sector under automatic route (in case of Greenfield investment) and under Government approval route (in case of Brownfield investment). In January 2014, the Government decided to continue with the extant FDI policy on the pharmaceutical sector with a condition that a non-compete clause would be allowed in special circumstances with prior approval of the Foreign Investment Promotion Board (FIPB).

Source: Press Note 1 (2014 series) issued by the DIPP dated 8 January, 2014

5. FDI in Insurance Sector

In terms of the extant FDI policy, foreign investment of up to 26 per cent is allowed in the insurance sector under the automatic route, subject to certain conditions. The GoI has clarified that cap of foreign investments in the insurance sector, apart from the Insurance company, would also apply to intermediaries such as (a) Insurance Brokers, (b) Third Party Administrators, and (c) Surveyors and Loss Assessors.

Further, the existing cap of 26 per cent would also include investment from FIIs and Non-resident Indians (NRI).

Source: Press Note 2 (2014 series) issued by the DIPP dated February 4, 2014

6. Discussion Paper on FDI in e-commerce

Presently, 100 per cent FDI in e-commerce under automatic route is permitted in Business to Business e-commerce transactions. With a view to opening up the B2C e-commerce industry to FDI, the GoI issued a discussion paper inviting comments of stakeholders for allowing FDI on Business to Consumer e-commerce earlier in January 2014.

Source: Discussion Paper on FDI in E-commerce released by DIPP in January, 2014

7. Unlisted Indian companies allowed to list and raise capital abroad

The GoI vide press release, dated September 27, 2013, permitted unlisted Indian companies to raise capital abroad, without the requirement of prior/subsequent listing in India, initially for a period of two years, subject to certain conditions. The DIPP issued a Press Note incorporating said change in the FDI policy, subject to following conditions:

Overseas listing is permitted only on exchanges in International Organization of Securities Commissions (IOSCO)/Financial Action Task Force (FATF) compliant jurisdictions or those jurisdictions with which Securities and Exchange Board of India (SEBI) has signed bilateral agreements

The Companies shall file a copy of the return which they submit to the proposed exchange/regulators also to SEBI for the purpose of Prevention of Money Laundering Act (PMLA). The Company is to also comply with SEBI’s disclosure requirements, in addition to that of the

The listing company shall be fully compliant with the FDI policy in force

The capital raised abroad may be utilised for retiring outstanding overseas debt or for operations abroad, including for acquisitions

In case the funds are not utilised abroad, such companies shall remit money back to India within 15 days and may be parked with authorised dealers notified by the Reserve Bank of India (RBI) and may be used domestically.

Source: Press Release dated September 27, 2013 and Notification No. G.S.R. 684(E) dated October 11, 2013 issued by the GoI/Press Note 7 (2013 series) issued by DIPP

8. Pricing guidelines for FDI compliant instruments with optionality clauses

In terms of extant FDI guidelines, equity shares and compulsorily convertible preference shares (CCPS)/debentures (CCD) are construed as FDI compliant instruments. The RBI has now allowed optionality clause in equity shares and CCPS/CCD to be issued to non-resident investor under the FDI scheme. This clause will oblige the buy-back of securities from the investor at the price prevailing/value determined at the time of exercise of the optionality, so as to enable the investor to exit without any assured return. The guiding principle is that the non-resident investor is not guaranteed any assured exit price at the time of making such investment/agreement and shall exit at the price prevailing at the time of exit, subject to lock-in period requirement, as applicable.

After the lock-in period, the non-resident investor exercising option/right shall be eligible to exit without any assured return, as under:

a) In case of a listed company, at the market price prevailing at the recognised stock exchanges

b) In case of unlisted company, at a price not exceeding that arrived at on the basis of Return on

Equity (RoE) as per the latest audited balance sheet

c) CCD/CCPS may be transferred at a price worked out as per any internationally accepted pricing

methodology, at the time of exit, duly certified by a Chartered Accountant or a SEBI registered

Merchant Banker

All existing contracts will need to comply with above conditions to qualify as FDI compliant.

9. Guidelines for calculation of total foreign investment in Indian companies, transfer of ownership and control of Indian companies and downstream investment by Indian companies

The RBI vide its Circular dated 4 July, 2013 incorporated the downstream investment regime into the Foreign Exchange Management (Transfer or Issue of Security by a Person Resident outside India) Regulations, 2000. The RBI Circular is largely in line with the downstream investment regime, as laid down in the FDI policy and permits an Indian company for the purpose of making downstream investment to bring requisite funds from abroad and/or utilise its internal accruals.

Source: RBI A.P. (DIR Series) Circular No.01 dated July 4, 2013 and A.P. (DIR series) Circular No. 42 dated September 12, 2013)

10. Purchase of shares on the recognised stock exchange under the FDI scheme in accordance with the SEBI Takeover Regulations

FIIs, Qualified Foreign investors (QFIs) and NRIs were eligible to acquire shares on the recognised stock exchange, in compliance with applicable provisions of Foreign Exchange Management Act, 1999 (FEMA). However, a non-resident was not permitted to acquire shares on the stock exchange under the FDI scheme.

RBI, as measure of liberalisation, allowed non-residents including NRIs to acquire shares of a listed Indian company on the stock exchange, through a registered broker under the FDI scheme. This is

subject to various conditions including that the non-resident investor should have already acquired and continues to hold the control, in accordance with the SEBI Takeover Regulations and other conditions with respect to payment of consideration, pricing guidelines etc.

Source: A.P. (DIR series) Circular No. 38, September 6, 2013

11. ‘Group Company’ defined in consolidated FDI policy

The term ‘group company’ was earlier not specifically defined under the FDI policy. The DIPP defined the term Group Company to mean two or more enterprises which, directly or indirectly, are in a position to:

Exercise twenty six per cent, or more of voting rights in other enterprise; or

Appoint more than fifty per cent, of the members of the board of directors in the other enterprise.

Source: Press Note 2 of 2013 dated 3 June, 2013 issued by the DIPP

12. Borrowing and Lending in Rupee - investments by person resident outside India in tax free, secured, redeemable, non-convertible bonds

FEMA restricts person resident in India, who has borrowed in Rupees from a person resident outside India, to utilise the borrowed funds from making any investment, whether by way of capital or otherwise, in any company or partnership firm or proprietorship concern or any entity, or for relending.

RBI has now permitted such resident entities/Indian companies, authorised by the GoI, to issue tax-free, secured, redeemable, non-convertible bonds in Rupees to persons resident outside India, to use such borrowed funds for the following purposes:

For on lending/re-lending to the infrastructure sector.

For keeping in fixed deposits with banks in India, pending utilisation by them for permissible end-uses.

13. Issue of Non convertible/redeemable bonus, preference shares or debentures

Under the extant FDI policy, equity shares, CCPS and CCD are treated as part of share capital for the purpose of FDI. RBI has been approving applications for the issue of non-convertible/redeemable bonus shares/debentures to shareholders from the general reserve, under the scheme of arrangement by a Court, on case to case basis.

RBI vide its circular of January 6, 2014, provided that an Indian company may issue non convertible/redeemable bonus shares/debentures to non-resident shareholders, including the depositories that act as trustees for the ADR/GDR holders, by way of distribution as bonus from its general reserves, under a Scheme of Arrangement approved by a Court in India, under the provisions of the Companies Act, as applicable, subject to no-objection from the Income-tax authorities.

It has been specifically clarified that the above general permission is only for issue of non-convertible/redeemable preference shares or debentures to non-resident shareholders by way of distribution as bonus from the general reserves and not otherwise.

1. ECB by Holding Companies/Core Investment Companies for project use in Special Purpose Vehicles

RBI vide its circular in December 2013, has permitted Holding Companies/Core Investment Companies (CICs) coming under its regulatory framework, to raise External Commercial Borrowing (ECB) under the automatic route/approval route, as the case may be, for project use in Special Purpose Vehicles (SPVs), subject to various conditions specified in the circular.

The circular interalia specifies that (i) the business activity of the SPV should be in the infrastructure sector (as defined in the ECB guidelines) (ii) the infrastructure project is required to be implemented by the SPV established exclusively for implementing the project (iii) ECB proceeds are utilised either for fresh capital expenditure (capex) or for refinancing of the existing Rupee loans (under the approval route) availed from the domestic banking system for capex as per the extant norms on refinancing (iv) ECB for SPV can be raised up to three years after the Commercial Operations Date of the SPV.

2. Revised ECB Policy for Non-Banking Finance Company – Asset Finance Companies

As a measure of liberalising the ECB policy, in July 2013, Non-Banking Finance Company – Asset Finance Companies (NBFC-AFCs) were allowed to avail of ECB under the automatic route, to finance import of infrastructure equipment for leasing to infrastructure projects, including certain additional conditions laid down in the circular.

Such ECBs (including outstanding ECBs) under the automatic route can be availed upto 75 per cent of owned funds of NBFC-AFCs, subject to a maximum of USD 200 million or its equivalent per financial year. ECBs by AFCs above 75 per cent of their owned funds will be considered under approval route.

RBI vide its Circular No. 30, dated September 4, 2013, permitted eligible borrowers to avail of ECB from the foreign equity holder under the Government approval route for general corporate purposes. The ECB’s may be raised with a minimum average maturity of seven years subject to the following conditions:

Minimum paid-up equity capital of 25 per cent should be held directly by the lender

Such ECB’s would not be used for any purpose not permitted under the extant ECB guidelines (including on-lending to their group companies/step down subsidiaries in India)

Repayment of principal to commence only after completion of minimum average maturity of 7 years. No prepayment will be allowed before maturity.

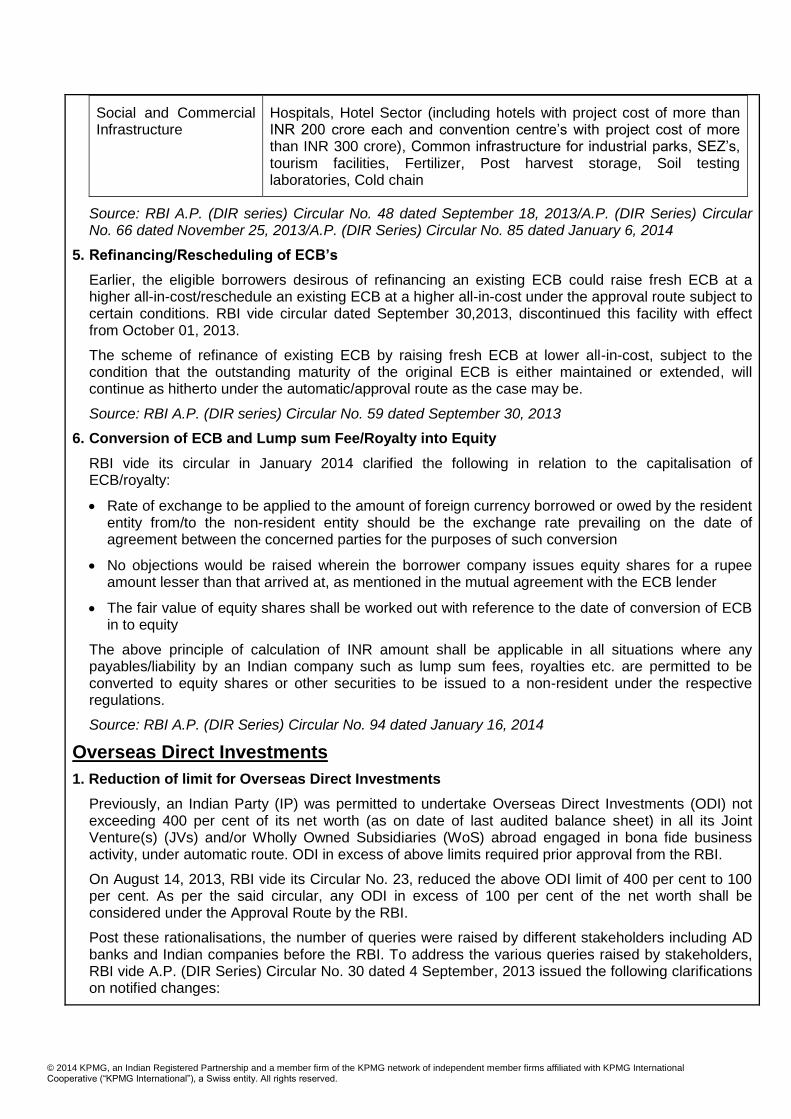

As per the extant ECB guidelines, ECB can be raised for investment in infrastructure sector. The RBI vide circulars in September 2013 and January 2014, expanded the definition of ‘Infrastructure’, as below:

Sectors Sub-sectors

Energy Electricity generation/transmission/distribution, Oil pipelines, Oil/Gas/Liquefied Natural Gas (LNG) storage facilities, Gas Pipelines (includes city gas distribution network)

Communication Mobile telephony services, Cellular services, Fixed network telecommunication, Telecommunication towers

Transport Railways, Road and bridges, Ports, Inland waterways, Airport (Including ‘Maintenance, Repairs and Overhaul’ (MRO) which shall also be treated as a part of airport infrastructure), Urban public transport

Water and Sanitation Water supply pipelines, Solid waste management, Water treatment plants, sewage projects, Irrigation, Storm water drainage system

Hospitals, Hotel Sector (including hotels with project cost of more than INR 200 crore each and convention centre’s with project cost of more than INR 300 crore), Common infrastructure for industrial parks, SEZ’s, tourism facilities, Fertilizer, Post harvest storage, Soil testing laboratories, Cold chain

Source: RBI A.P. (DIR series) Circular No. 48 dated September 18, 2013/A.P. (DIR Series) Circular No. 66 dated November 25, 2013/A.P. (DIR Series) Circular No. 85 dated January 6, 2014

5. Refinancing/Rescheduling of ECB’s

Earlier, the eligible borrowers desirous of refinancing an existing ECB could raise fresh ECB at a higher all-in-cost/reschedule an existing ECB at a higher all-in-cost under the approval route subject to certain conditions. RBI vide circular dated September 30,2013, discontinued this facility with effect from October 01, 2013.

The scheme of refinance of existing ECB by raising fresh ECB at lower all-in-cost, subject to the condition that the outstanding maturity of the original ECB is either maintained or extended, will continue as hitherto under the automatic/approval route as the case may be.

6. Conversion of ECB and Lump sum Fee/Royalty into Equity

RBI vide its circular in January 2014 clarified the following in relation to the capitalisation of ECB/royalty:

Rate of exchange to be applied to the amount of foreign currency borrowed or owed by the resident entity from/to the non-resident entity should be the exchange rate prevailing on the date of agreement between the concerned parties for the purposes of such conversion

No objections would be raised wherein the borrower company issues equity shares for a rupee amount lesser than that arrived at, as mentioned in the mutual agreement with the ECB lender

The fair value of equity shares shall be worked out with reference to the date of conversion of ECB in to equity

The above principle of calculation of INR amount shall be applicable in all situations where any payables/liability by an Indian company such as lump sum fees, royalties etc. are permitted to be converted to equity shares or other securities to be issued to a non-resident under the respective regulations.

1. Reduction of limit for Overseas Direct Investments

Previously, an Indian Party (IP) was permitted to undertake Overseas Direct Investments (ODI) not exceeding 400 per cent of its net worth (as on date of last audited balance sheet) in all its Joint Venture(s) (JVs) and/or Wholly Owned Subsidiaries (WoS) abroad engaged in bona fide business activity, under automatic route. ODI in excess of above limits required prior approval from the RBI.

On August 14, 2013, RBI vide its Circular No. 23, reduced the above ODI limit of 400 per cent to 100 per cent. As per the said circular, any ODI in excess of 100 per cent of the net worth shall be considered under the Approval Route by the RBI.

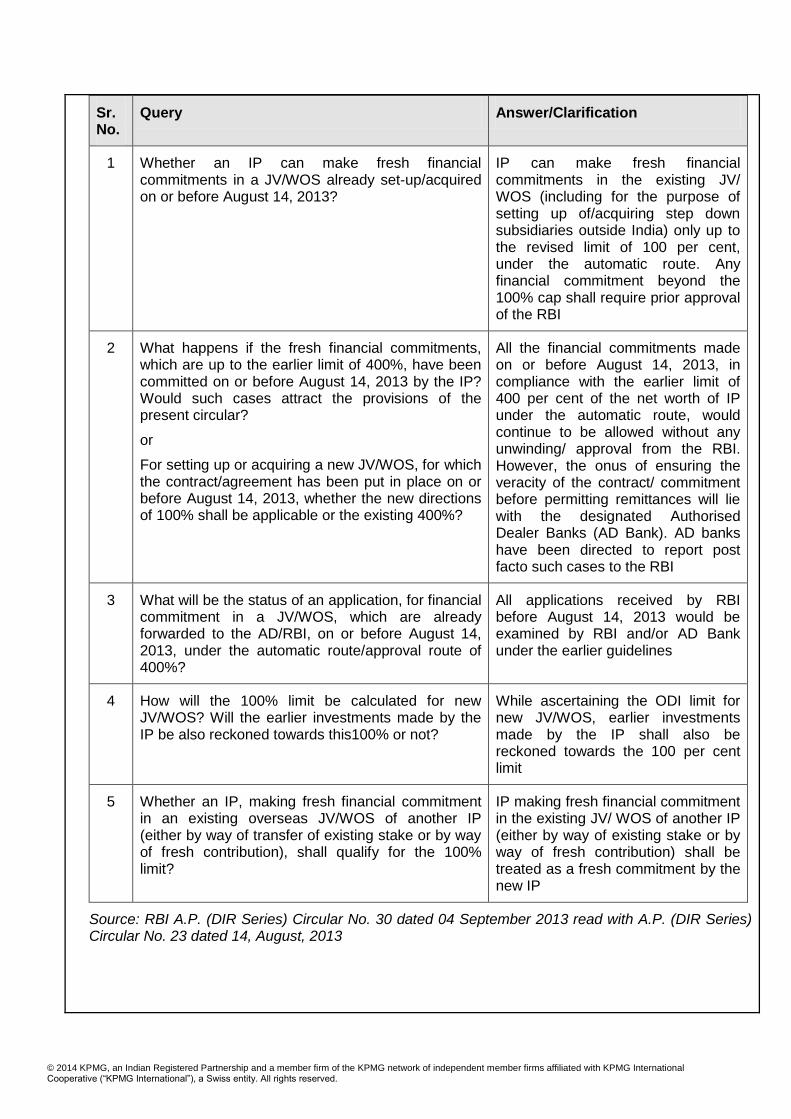

Post these rationalisations, the number of queries were raised by different stakeholders including AD banks and Indian companies before the RBI. To address the various queries raised by stakeholders, RBI vide A.P. (DIR Series) Circular No. 30 dated 4 September, 2013 issued the following clarifications on notified changes:

1 Whether an IP can make fresh financial commitments in a JV/WOS already set-up/acquired on or before August 14, 2013?

IP can make fresh financial commitments in the existing JV/ WOS (including for the purpose of setting up of/acquiring step down subsidiaries outside India) only up to the revised limit of 100 per cent, under the automatic route. Any financial commitment beyond the 100% cap shall require prior approval of the RBI

2 What happens if the fresh financial commitments, which are up to the earlier limit of 400%, have been committed on or before August 14, 2013 by the IP? Would such cases attract the provisions of the present circular?

or

For setting up or acquiring a new JV/WOS, for which the contract/agreement has been put in place on or before August 14, 2013, whether the new directions of 100% shall be applicable or the existing 400%?

All the financial commitments made on or before August 14, 2013, in compliance with the earlier limit of 400 per cent of the net worth of IP under the automatic route, would continue to be allowed without any unwinding/ approval from the RBI. However, the onus of ensuring the veracity of the contract/ commitment before permitting remittances will lie with the designated Authorised Dealer Banks (AD Bank). AD banks have been directed to report post facto such cases to the RBI

3 What will be the status of an application, for financial commitment in a JV/WOS, which are already forwarded to the AD/RBI, on or before August 14, 2013, under the automatic route/approval route of 400%?

All applications received by RBI before August 14, 2013 would be examined by RBI and/or AD Bank under the earlier guidelines

4 How will the 100% limit be calculated for new JV/WOS? Will the earlier investments made by the IP be also reckoned towards this100% or not?

While ascertaining the ODI limit for new JV/WOS, earlier investments made by the IP shall also be reckoned towards the 100 per cent limit

5 Whether an IP, making fresh financial commitment in an existing overseas JV/WOS of another IP (either by way of transfer of existing stake or by way of fresh contribution), shall qualify for the 100% limit?

IP making fresh financial commitment in the existing JV/ WOS of another IP (either by way of existing stake or by way of fresh contribution) shall be treated as a fresh commitment by the new IP

2. Clarifications on revised guidelines of Liberalised remittance scheme

Considering the macroeconomic situation of the economy, RBI on August 14, 2013 vide Circular No. 24 notified a reduction in the remittance limits made by Resident Individuals under the Liberalised remittance scheme (LRS) scheme, from USD 200,000 to USD 75,000 per financial year.

In response to the queries raised by various stakeholders relating to these changes in the LRS Scheme, RBI vide its Circular dated 4 September, 2013 interalia clarified that LRS can be used to acquire both unlisted and listed shares of an overseas company and resident individuals are permitted to make remittances for acquiring immovable property within the annual limit of USD 75,000 for those contracts, which were entered into on or before the date of the circular, i.e., August 14, 2013.

The RBI has decided not to treat/reckon the renewal/rollover of an existing/original guarantee, which is part of the total financial commitment of the Indian party, as a fresh financial commitment, provided that:

the existing/original guarantee was issued in terms of the then extant/ prevailing FEMA guidelines

there is no change in the end-use of the guarantee

there is no change in any of the terms and conditions, including the amount of the guarantee except the validity period

the reporting of the rolled over guarantee would be done as a fresh financial commitment in Part II of Form ODI, as hitherto

if the Indian party is under investigation by any investigation/enforcement agency or regulatory body, the concerned agency/body shall be kept informed about the same.

In case the above conditions are not met, the Indian party shall obtain a prior approval of the RBI for a rollover/renewal of the existing guarantee through a Banker.

1. Third party payments for Export/Import Transactions

Normally, the payment for import/export has to be paid/received from the overseas supplier/buyer named in the underlying documents i.e., Export Declaration Form (EDF) or Bill of entry, as the case may be. With a view to liberalise the above procedure, the RBI allowed third party payments in respect of export/import transactions, subject to meeting various conditions specified in the circular.

1. SEBI (Foreign Portfolio Investors) Regulations, 2014

SEBI notified the SEBI (Foreign Portfolio Investors) Regulations, 2014 on 7 January, 2014. The key highlights of the said regulations are as indicated below:

Existing FIIs, Sub-Accounts and QFIs shall be merged into a new investor class termed as Foreign Portfolio Investors (FPIs)

SEBI has delegated the registration of FPIs to approved Designated Depository Participants (DDPs) subject to compliance with know your client (KYC) requirements

FPI shall be required to seek registration in any one of the following categories:

− ‘Category I FPI’ which shall include Government, Government related foreign investors etc.

− ‘Category II FPI’ which shall include appropriately regulated broad based funds, appropriately regulated entities, broad based funds whose investment manager is appropriately regulated, university funds, university related endowments, pension funds etc.

− ‘Category III FPI’ which shall include all others not eligible under Category I and II FPI

The above categorisation has been devised based on the risks associated with each category and differ in terms of KYC requirements

All existing FIIs and Sub Accounts may continue to buy, sell or otherwise deal in securities under the FPI regime until the lapse of the current registration

All existing QFIs may continue to buy, sell or otherwise deal in securities till the period of one year from the date of notification of this regulation

Investment conditions under the FPI regulations largely continue as per the current SEBI (FII) Regulations.

Source: SEBI Notification No. LAD-NRO/GN/2013-14/36/12 dated 7 January, 2014

2. SEBI (Listing of Specified Securities on Institutional Trading Platform) Regulations, 2013

SEBI vide its notification in October 2013 notified the SEBI (Listing of Specified Securities on Institutional Trading Platform) Regulations, 2013. The move is aimed at providing easier exit options to informed investors (such as Angel Investors, Venture Capital Funds and Private Equities).

The Key eligibility criteria for listing are as indicated below:

The company has not completed more than 10 years from incorporation

Revenue has not exceeded INR 100 crore in any previous financial year

Paid up capital of the company has not exceeded INR 25 crore in any of the previous financial years

No regulatory action has been taken against the company, its promoter or director, by prescribed regulatory authorities within a period of 5 years prior to the date of application for listing

The company shall satisfy any one of the following criteria:

− Investment of atleast INR 50 lakhs in equity shares of the company by AIF, VCF, other SEBI approved investors or specified angel investor

− Company has received finance (no minimum threshold specified) from a scheduled bank for its project financing/working capital requirement atleast before 3 years and the same has been fully utilised

− Investment of atleast INR 50 lakhs in equity shares of the company by registered Merchant Banker/Qualified Institutional Buyer which shall be locked in for 3 years from date of listing

− a specialised international multilateral agency or domestic agency or a public financial institution has invested in the equity capital of the company (no minimum threshold specified).

Separately, SEBI has also issued guidelines to stock exchanges in this regard. The SEBI has asked the stock exchanges to execute a listing agreement with SMEs seeking listing on ITP in line with the Model listing agreement and implement the consequential amendments, if any (like changes in bye laws etc.) for the implementation of the Regulations.

Source: SEBI Notification No. No. LAD-NRO/GN/2013-14/27/6720 dated 8 October, 2014/SEBI Circular No. CIR/MRD/DSA/33/2013 dated October 24, 2013

3. Consultation paper on draft SEBI (Real Estate Investment Trusts) Regulations, 2013

With a view to reviving an over five-year old proposal of Real Estate Investment Trust (REIT) to attract

real estate investors, SEBI issued the draft revised regulations inviting public comments. REITs would allow property developers to monetise their developed, revenue-generating assets by off-loading them in a separate listed entity. As per the consultation paper, the REIT shall be set up as a Trust and shall not launch any schemes and the REIT will also have parties such as trustee (registered with SEBI), sponsor, manager and principal valuer. The Consultation Paper also deals with various aspects relating to Offer of units to the public and listing of units, key eligibility criteria for Sponsor and Manager of REIT, Eligible Investors, Investment conditions and dividend policy, Borrowings and deferred payments etc.

Source: SEBI Press Release dated 10 October 2013 vide PR No. 101/2013

4. SEBI amendments to Securities Contracts (Regulation) Act, 1956

SEBI relaxed certain provisions under Securities Contracts (Regulation) Act, 1956 (SCRA) to boost the interest of investors by allowing them to include preferential clauses like right of first refusal (ROFR), tag-along, drag-along and call-put option in the share purchase agreements/Articles of Association subject to certain conditions. SEBI has permitted the following contracts to be entered without obtaining its approval:

Contract for pre-emption including ROFR or tag-along or drag along rights contained in shareholders’ agreement or articles of association of companies or other body corporate

Contracts for purchase or sale of securities pursuant to exercise of an option (essentially call option - put option) contained in shareholders agreements or articles of association subject to conditions

The aforesaid notification specifically provides that:

− all the aforesaid permissible contracts shall be in accordance with the provisions of the Foreign Exchange Management Act, 1999 and rules and regulations made thereunder

− The provisions of this notification shall not affect or validate any contract which has been entered into prior to the date of this notification.

5. SEBI (Investment Advisers) Regulations, 2013

SEBI (Investment Advisers) Regulations, 2013(Investment Advisors Regulation), came into effect from 20 April, 2013 and are applicable to every person providing investment advice to any person for consideration (including non-cash benefit) and would be required to obtain registration under this Regulation. Investment advice inter-alia includes advice relating to investing in, purchasing, selling, financial planning or otherwise dealing in securities or investment products, through any means of communication (including oral) for the benefit of the client.

Exemption has been provided to any fund manager of a mutual fund, AIF or any other intermediary or entity registered with the Board, and to any person providing investment advice exclusively to clients based out of India. Exemption is also provided in respect of the insurance agents/brokers, pension advisor, distributor of mutual funds, SEBI registered portfolio managers, stock brokers, professionals providing investment advice incidental to their professional service (e.g. Law-firms, Chartered Accountants) etc. from registration.

Investment Advisors are also required to comply with capital adequacy norms (Body corporates - minimum net-worth of INR 25 lakh and Individuals/Partnership Firm - minimum net tangible assets of INR 1 lakh).

Source: SEBI Notification No. LAD-NRO/GN/2012-13/31/1778 dated 21 January, 2013

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we

endeavour to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue

to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

The KPMG name, logo and “cutting through complexity“are registered trademarks of KPMG International Cooperative (“KPMG International”), a Swiss entity.