45

Lecture 6 CHE4161 1 CHE 4161 – Environmental Management Lecture 6 • Setting a Carbon Price • Emissions Trading • Carbon Tax • Australian GHG Legislation • Carbon Capture and Storage

| Date post: | 20-Dec-2015 |

| Category: |

Documents |

| Upload: | matthew-leach |

| View: | 222 times |

| Download: | 0 times |

Lecture 6 CHE4161 1

CHE 4161 – Environmental Management

Lecture 6

• Setting a Carbon Price

• Emissions Trading

• Carbon Tax

• Australian GHG Legislation

• Carbon Capture and Storage

Lecture 6 CHE4161 2

What is a carbon price?• Goal is to create a change in an economy

• market can differentiates between goods & services based on carbon

footprints

• A carbon price can be established explicitly

• through carbon taxes or emissions trading

• or implicitly

• ie regulations, emissions standards, Best Available Control

Technology (BACT) requirements

• choice of specific policy tools depends on:

• a country’s national circumstances

• the characteristics of affected economic sectors

Lecture 6 CHE4161 3

Climate Change / Carbon Policy

• carbon price is one element of a broader climate change

policy framework

• comprehensive policy approaches should include:

• funding for research and development

• fiscal support for early large scale demonstration of near-

commercial technologies

• removal of subsidies that support carbon intensive activities

(eg fuel subsidies)

• over time national policy approaches should

• complement each other, link or converge

• to create a global mechanism which reduces emissions for

the least cost

Lecture 6 CHE4161 4

Successful Carbon Policy• will trigger the implementation of emission reduction projects and actions

throughout the economy

• lowest cost result delivered by encouraging the most economically

attractive projects to be developed first

• abatement concepts progressively move from left to right across the

abatement curve

http://www.wbcsd.org/Pages/EDocument/EDocumentDetails.aspx?ID=152&NoSearchContextKey=true

Lecture 6 CHE4161 5

Market based approach• carbon can be priced in two ways:

• fixed- price schemes, or carbon taxes

• set the price of emissions

• market decides how much it will reduce emissions

• floating price schemes

• set the quantity of emissions

• permits to emit are issued up to that amount

• permits are tradeable between businesses - market sets the price

• Various hybrid approaches combine:

• fixed prices for a period with floating later on

• floating prices at some price levels with

• a price floor or

• a price ceiling

• or both

http://www.garnautreview.org.au/update-2011/garnaut-review-2011/garnaut-review-2011.pdf

Lecture 6 CHE4161 6

The economics of a carbon price• Carbon price is initially paid by the emitter or fuel provider

• paying a tax, purchasing allowances (permits) or implementing a

required project

• Price is generally* passed through to end consumers

• Resulting in:

• increase cost of goods and services with a carbon footprint

• products with a high carbon footprint will be less competitive

• the emergence of a new cost ranking within the economy

• driving manufacturers to invest in projects to lower the footprint

• forcing the removal of some products from the market

*Special allowances are generally built into a scheme to account for industries

which are highly ‘emissions intensive’ or ‘trade exposed’ (EITE) to prevent carbon

leakage

Lecture 6 CHE4161 7

Carbon revenue

• revenue raised by a government from carbon pricing is

typically directed to the treasury as part of the overall

national budget process

• it should be used efficiently:

• to offset any net change in costs to consumers by reducing taxes

• encourage emission reduction activities

Lecture 6 CHE4161 8

The flow of carbon revenue in the economy

http://www.wbcsd.org/Pages/EDocument/EDocumentDetails.aspx?ID=152&NoSearchContextKey=true

EMISSIONS TRADING SCHEMES

ETS

Lecture 6 CHE4161 10

Emissions Trading

• a market-based tool

• markets trade ‘emissions’

• cap-and-trade schemes or

• credits that pay for, or offset GHG reductions

• a cap is set (generally by government) on allowable emissions

• emissions allowances (permits) up to the cap distributed or auctioned

• distribution of a % of ‘allowances’ (issuing free permits) is often used at the

commencement of a scheme to give a ‘soft start’

• liable entities who do not have enough allowances must either:

• reduce emissions

• buy another entities spare permits

• buy ‘credits’ (offsets)

• entities with extra allowances/permits can sell them or (under some

scenarios) bank them for future use

Lecture 6 CHE4161 11

Successful Emissions Trading• A successful cap-and-trade scheme relies on a strict but

feasible cap that decreases emissions over time

• If the cap is set too high

• an excess of emissions will enter the atmosphere

• the scheme will have no effect on the environment (eg EU ETS)

• A high cap can also drive down the value of allowances

• causing losses in firms that have reduced their emissions and banked

credits

• If the cap is set too low

• allowances are scarce and overpriced

Lecture 6 CHE4161 12

Successful Emissions Trading

• Some schemes have ‘safety valves’

• keep the value of allowances within a certain range

• if price of allowances gets too high

• the scheme's governing body will release additional credits to

stabilize the price

• if price gets too low

• the scheme's governing body can cancel allowances

• the price of allowances is usually a function of supply and

demand

Lecture 6 CHE4161 13

Key Principles of an ETS

• Direct investment capital towards lower CO2 emission

projects, via a market price for CO2 emissions

• Trading system should not remove that capital from the

industries or firms covered by the system

Important Design Features • The point of regulation

• Allocation of allowances

• Recognition of technologies

• Constraints and limitations

• External projects mechanisms (or offsets)

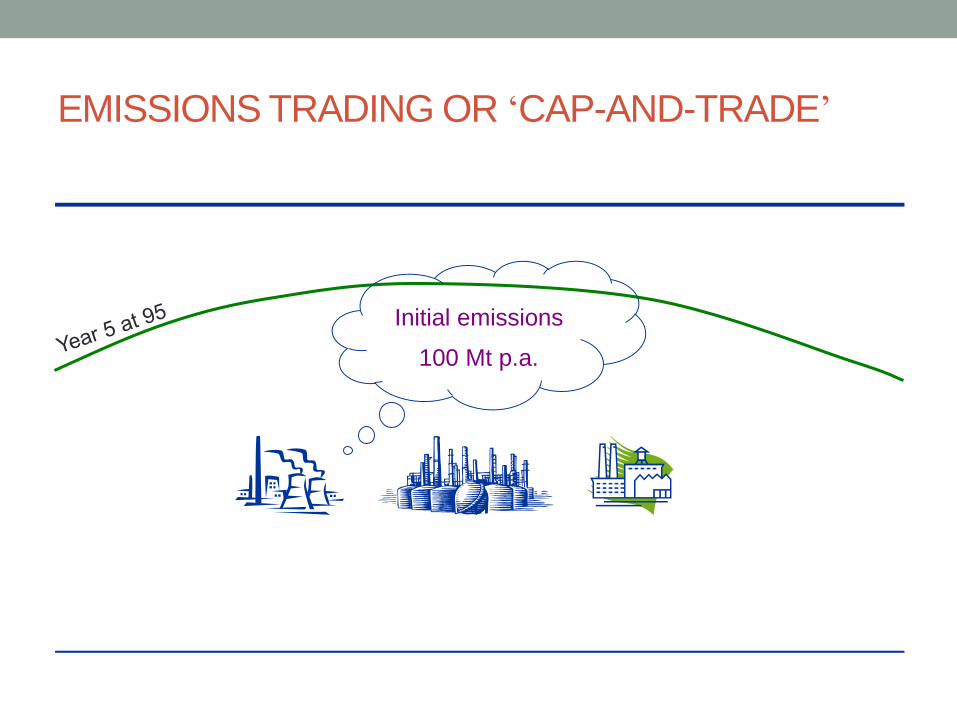

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Initial emissions

100 Mt p.a.

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Initial emissions

100 Mt p.a.

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Initial emissions

100 Mt p.a.

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Initial emissions

100 Mt p.a.

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Allowance trading between facilities

$ CO2

Initial emissions

100 Mt p.a.

Government issues

88 million allowances

into the economy

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Allowance trading between facilities

$ CO2

CCS

Project

Initial emissions

100 Mt p.a.

Government issues

88 million allowances

into the economy

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Allowance trading between facilities

$ CO2

Efficiency

Project

CCS

Project

Initial emissions

100 Mt p.a.

EMISSIONS TRADING OR ‘CAP-AND-TRADE’

Initial emissions

100 Mt p.a.

Allowance trading between facilities

$ CO2

Efficiency

Project

CCS

Project

Offsets

CARBON TAX

Lecture 6 CHE4161 24

Other Mechanisms - Carbon Tax

• environmental tax levied on the carbon content of fuels

• increases the competitiveness of non-carbon energy

• revenue raised can be used to:

• fund non-carbon technologies

• offset higher prices for certain sectors of the economy (ie low income households, trade exposed industries)

• success of a carbon tax to reduce overall CO2 emissions depends on how carbon tax revenue is managed by the body collecting the revenue

• must be invested back into ‘clean’ technology, otherwise benefits of scheme are limited

• price signal not enough to drive significant reduction

Lecture 6 CHE4161 25

Carbon Tax

• an indirect tax

• a tax on a transaction

• as opposed to on income

• also called a price instrument

• sets a price for emissions

Lecture 6 CHE4161 26

Carbon Tax Vs Carbon Trading

• both have theoretical benefit to reducing emissions

• Pro’s and Con’s of specific legislation can be compared –

cannot compare ‘general’ Tax and ETS concepts

• some ETS’s have poor platforms

• some Carbon Tax schemes direct proceeds to

consolidate revenue, thus do not drive emission

reduction technologies

• Australia’s ‘Carbon Tax’ 1 July 2012 – 30 June 2014

• not a ‘Tax’

• was a ‘Fixed Price’ element of a Carbon Trading Scheme

Lecture 6 CHE4161 27

Carbon leakage

• When some manufacturers (competing in the same market)

incur the cost of carbon and others do not

• manufacturer incurring a carbon cost is penalised, b/c the

market price is set by a lower cost provider who does not

incur a carbon price

• result is “carbon leakage”

• higher cost manufacturer struggles to compete

• market share gained by producer not subject to carbon price

• no change in consumption, change in location of emissions

• emissions ‘leak’ to the country/economy without a carbon price

Lecture 6 CHE4161 28

Carbon leakageExample

• Corporation A in Australia producing widgets must pay a carbon price

for its manufacturing emissions

• Corporation B in Asia producing the same widgets, but without a

carbon price and importing them to Australia

• Corporation A closes down manufacturing in Australia and produces

product in Asia for import to Australia

• no net change in global emissions

• jobs / profit sent elsewhere

• emission ‘leaked’ (escape from pricing system for products still

consumed in Australia)

Lecture 6 CHE4161 29

The Clean Energy RegulatorEmissions Reduction Fund &

Carbon Farming Initiative

Renewable Energy Target

National Greenhouse &

Energy Reporting

Carbon Pricing Mechanism

(repealed)

Australian National Registry

of Emissions Units

Clean

Energy

Regulator

EMISSION REDUCTION

FUND

Lecture 6 CHE4161 31

Australia’s abatement task

Lecture 6 CHE4161 32

Emissions Reduction Fund

• Three elements of ERF1. Crediting emissions reduction

2. Purchasing emissions reduction

3. Safeguarding emissions reductions

• $2.55B* in 2014-15 Budget for ERF• develop bid for abatement, funding committed under contract

• payments as emissions reductions verified

• Gov’t will purchase lowest cost abatement • Eg: $35,000 Project cost for 2000 tCO2e abated

• Bid $17.5 / tonne CO2 abated

Lecture 6 CHE4161 33

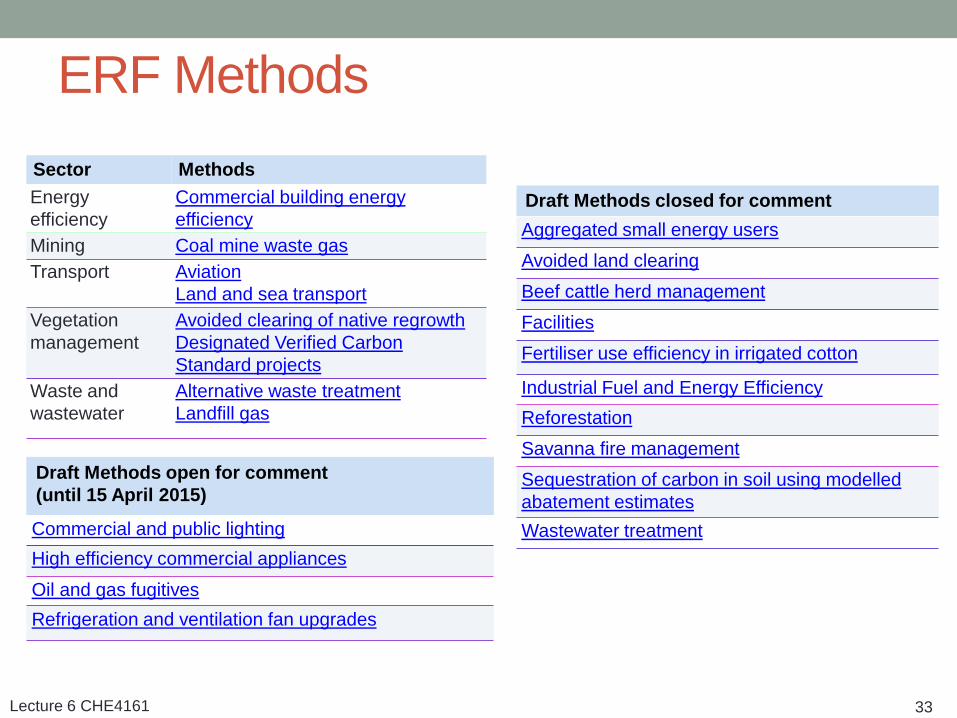

ERF Methods

Draft Methods open for comment

(until 15 April 2015)

Commercial and public lighting

High efficiency commercial appliances

Oil and gas fugitives

Refrigeration and ventilation fan upgrades

Draft Methods closed for comment

Aggregated small energy users

Avoided land clearing

Beef cattle herd management

Facilities

Fertiliser use efficiency in irrigated cotton

Industrial Fuel and Energy Efficiency

Reforestation

Savanna fire management

Sequestration of carbon in soil using modelled

abatement estimates

Wastewater treatment

Sector Methods

Energy

efficiency

Commercial building energy

efficiency

Mining Coal mine waste gas

Transport Aviation

Land and sea transport

Vegetation

management

Avoided clearing of native regrowth

Designated Verified Carbon

Standard projects

Waste and

wastewater

Alternative waste treatment

Landfill gas

Lecture 6 CHE4161 34

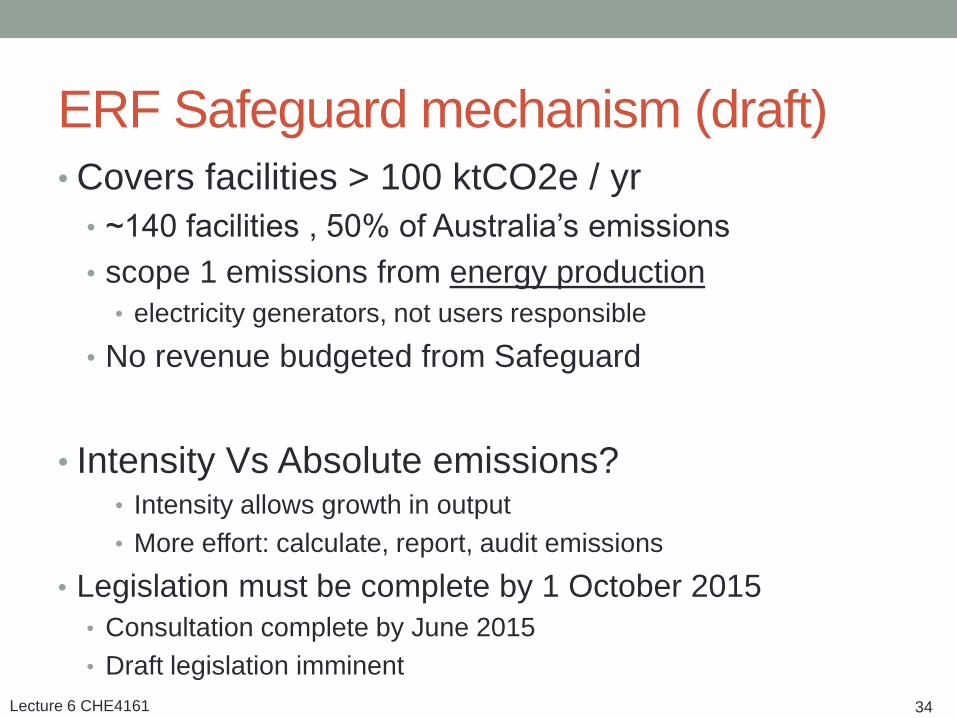

ERF Safeguard mechanism (draft)• Covers facilities > 100 ktCO2e / yr

• ~140 facilities , 50% of Australia’s emissions

• scope 1 emissions from energy production

• electricity generators, not users responsible

• No revenue budgeted from Safeguard

• Intensity Vs Absolute emissions?• Intensity allows growth in output

• More effort: calculate, report, audit emissions

• Legislation must be complete by 1 October 2015

• Consultation complete by June 2015

• Draft legislation imminent

Lecture 6 CHE4161 35https://www.tai.org.au/downloads/tug-of-war.pdf

CARBON CAPTURE & STORAGE

Lecture 6 CHE4161 37

Technologies for reducing CO2 emissions

http://www.iea.org/publications/freepublications/publication/etp2010.pdf

Lecture 6 CHE4161 38

Man-made carbon ‘sinks’ (CCS)• Carbon Capture and Storage (or sequestration)

• capturing CO2 emissions

• transporting to a storage site

• injecting into an underground geological formation

• allows fossil fuel combustion without emissions

• GHG emissions injected into:

• Aquifers

• Depleted oil reservoirs

• EU CCS video

Lecture 6 CHE4161 39

Sinks – manmade: carbon sequestration

Lecture 6 CHE4161 40

Sources which CCS might be relevant for

http://www.ipcc.ch/publications_and_data/ar4/wg3/en/ch4s4-3-6.html

Lecture 6 CHE4161 41

CCS

• http://www.afr.com/p/national/carbon_capture_and_storag

e_no_easy_Qi2ViTwWPWoiKUGoVIw6EN

• Carbon capture and storage no easy task

• PUBLISHED: 18 JUL 2013 00:27:00 | UPDATED: 19 JUL

2013 11:42:12

Lecture 6 CHE4161 42

Full scale CCS plants

Currently 4 operational commercial-scale CCS plants

globally:

http://www.ccsassociation.org/faqs/viability-and-timescale-of-developing-ccs/

Salah: Algeria, Sahara Dessert: • operational since 2004

• > 1 million tonnes of CO2 / yr

Snøvit plant: northern Norway• operational since 2008

• ~ 700,000 tonnes of CO2 / yr

(full production)

Sleipner: North Sea, Norway• operational since 1996

• >1 million tonnes of CO2 / yr

Weyburn: Canada: • operational since 2005

• 26 million tonnes (net) over project

lifetime

Lecture 6 CHE4161 43

CCS in Australia• CCS demonstration projects underway in Australia

• November 2008, the Australian Government developed the

Offshore Petroleum and Greenhouse Gas Storage Act 2006

legislation

• enable CCS activities in Commonwealth offshore waters

• Vic, Qld and SA have CCS legislation

• Legislation is being developed by NSW and WA

• Further info at Dept Resources, Environment & Tourism website

• Article on why CCS is lapsing

Lecture 6 CHE4161 44

CCS in Australia

Lecture 6 CHE4161 45

Other references• General GHG Information

• The Greenhouse Gas Protocol (GHG Protocol) is the most widely used international

accounting tool for government and business leaders to understand, quantify, and

manage greenhouse gas emissions.

• http://www.ghgprotocol.org/

• GHG Myths Vs Realities Report:

• www.euractiv.com/25/images/Climate_change_myths.pdf

• McKinsey & Company

• www.mckinsey.com

• Pathways to a low carbon economy

• www.mckinsey.com/globalGHGcostcurve

• The McKinsey Quarterly is the business journal of McKinsey & Company

• http://www.mckinseyquarterly.com/home.aspx

• wbcsd energy & climate

• www.wbcsd.org/web/energy.htm