Nigeria Corporate Analysis | Public Credit Rating Lafarge Africa Plc Nigeria Corporate Analysis October 2017 Financial data: (USD’m Comparative) ‡ 31/12/15 31/12/16 N/USD (avg.) 193.1 253.2 N/USD (close) 197.0 305.0 Total assets 2,284.9 1,642.4 Total debt 752.7 418.1 Total capital 886.3 811.1 Cash & equiv. 83.7 63.2 Turnover 1,383.6 867.8 EBITDA 348.4 101.9 NPAT 140.6 66.7 Op. cash flow 357.6 (2.9) Market cap. ° USD925.7m Market share* c.25% ‡ Central Bank of Nigeria exchange rates. °As at 22/09/2017 @ N305.35/USD. *Estimated percentage market share of 2016 cement sales in Nigeria Rating history: Initial rating (July 2010) Long-term: A(NG) Short-term: A1(NG) Rating outlook: Stable Last rating ( October 2016) Long-term: A+(NG) Short-term: A1(NG) Rating outlook: Stable Series 1 Fixed Rate Bond: A+(NG) Series 2 Fixed Rate Bond: A+(NG) Rating Outlook: Stable Related methodologies/research: Global master criteria for rating corporate entities, updated February 2017 Glossary of terms/ratios, February 2017 Lafarge Africa Plc (“Lafarge Africa” or “LAP” or “the Group”), rating reports 2010-16; LAP bond rating report, October 2016 GCR contacts: Primary Analyst Adekemi Adebambo Senior Credit Analyst [email protected]Committee Chairperson Dave King [email protected]Analyst location: Lagos, Nigeria +234 1 462 – 2545 Website: http://www.globalratings.com.ng Summary rating rationale Lafarge Africa’s strong domestic market position is underpinned by an established international brand, effective distribution network, and operational support from its parent, LafargeHolcim. The recent completion of the new 2.5mtpa cement line at Mfamosing, Cross River State, has increased its production capacity to 14.1mtpa and further enhanced earnings potential. LAP’s cement sales volumes reduced by 16% in FY16, due to disruptions in gas supply and scarcity of foreign currency, which impeded productivity. Coupled with pricing pressures (in the first eight months of 2016), this drove an 18% decline in revenue to N219.7bn in FY16. The significant escalation in energy costs and the effect of a weaker Naira saw EBITDA margin contract sharply to 11.7% in FY16 (FY15: 25.2%), albeit this had corrected by 1H FY17. Increased productivity and operating efficiencies are expected to support an EBITDA margin of 29% for the full year. 1H FY17 cash generation rebounded N30.7bn, from the weak performance reported in FY16, to match historical trends. This was, however, offset by the accumulation of higher value inventory and debtors absorption, which drove an N8.4bn operating cash outflow (FY16: N725m outflow; five year average: N33.9bn inflow). While debt service and liquidity ratios are set to normalise by FY17, GCR will continue to monitor performance over the rating horizon, with an interest cover ratio of approximately 4x required to support stronger ratings (inter alia). In September 2016, LAP restructured USD493m (N139bn) of shareholder loans into a hybrid instrument, repayable at its discretion. Following the introduction of the dynamic Nigerian Inter-Bank Foreign Exchange Fixing (“NIFEX”) market it hedged its USD shareholder loan exposure and thus reclassified the quasi-equity to debt in 1H FY17. Borrowings therefore nearly doubled to N244.7bn in 1H FY17 (FY16: N127.5bn), with shareholder loans accounting for 52% of the total (FY16: 22%). Net gearing increased from 58% at FY14 to peak at 117% at 1H FY17 (FY16: 44%) while net debt to EBITDA deteriorated materially from 145% at FY14 to 420% at FY16, before improving to 300% in 1H FY17. LAP is planning a N131.7bn Rights Issue in 4Q FY17. Through the offer, LafargeHolcim, will subscribe to its rights by converting c.70% of dollar denominated shareholders loans into equity. According to management, the parent is also willing to extend the tenor of the remaining shareholder debt by three years. While, the high short-term debt exposure at 1H FY17 (78%) is concerning, this will be addressed by the Rights Issue, which should see net gearing and net debt to EBITDA managed to around 50% and 200% respectively. Factors that could trigger rating action may include Positive change: Upward rating migration in the medium term would depend on stabilisation/normalisation of the Group’s earnings and free cash flows, together with gearing and debt service metrics within guidance. Negative change: Slower than anticipated economic growth, delays in rolling out public infrastructure projects, foreign currency scarcity, and competitive pressures may constrain demand and/or pricing flexibility. These factors could adversely affect earnings and result in liquidity strain, increased gearing metrics and impede debt service, placing downward pressure on the ratings. Rating class Rating scale Rating Rating outlook Expiry date Long term National A+ (NG) Stable August 2018 Short term National A1(NG) Series 1 Fixed Rate Bond National A+ (NG) Stable August 2018 Series 2 Fixed Rate Bond National A+ (NG) Stable August 2018

Transcript

Nigeria Corporate Analysis | Public Credit Rating

Lafarge Africa Plc

Nigeria Corporate Analysis October 2017

Financial data:

(USD’m Comparative) ‡

31/12/15 31/12/16

N/USD (avg.) 193.1 253.2

N/USD (close) 197.0 305.0

Total assets 2,284.9 1,642.4

Total debt 752.7 418.1

Total capital 886.3 811.1

Cash & equiv. 83.7 63.2

Turnover 1,383.6 867.8

EBITDA 348.4 101.9

NPAT 140.6 66.7

Op. cash flow 357.6 (2.9)

Market cap. ° USD925.7m

Market share* c.25% ‡ Central Bank of Nigeria exchange rates.

Net interest* (8.8) (11.8) 35.2 (4.6) (10.0) 118.4

Other op. inc/exp† 1.4 1.8 29.5 (28.5) 2.2 (107.9)

Forex mvmt. (8.4) (22.7) 169.3 0.0 0.0 n.a

Combination. exp. (6.0) 0.0 (100.0) 0.0 0.0 n.a

NPBT 29.3 (22.8) (177.9) (30.2) 18.2 (160.2)

Key ratios (%)

Gross margin 30.9 18.5 14.1 28.7

EBITDA margin 25.2 11.7 9.8 23.6

Op. margin 19.1 4.5 2.7 16.7

Net int. cover (x) 5.8 0.8 0.6 2.6

*Includes interest income from short term securities and fixed bank deposits. †Includes profit/loss from disposed fixed assets, investments and associates

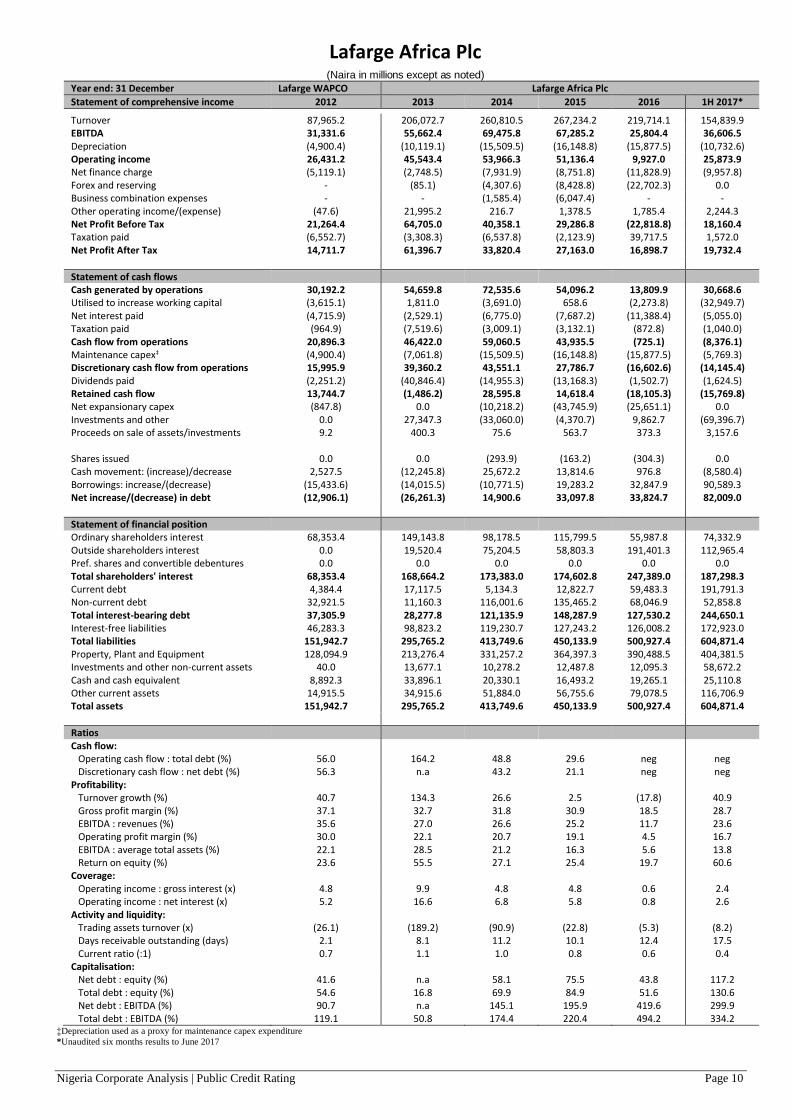

LAP’s cement volumes decreased by 16% in FY16 and

combined with the impact of pricing pressures in Nigeria

and South Africa, revenue fell by 18% to N219.7bn in

FY16, representing 63% of forecast. Fuel costs spiked to

N21.2bn in FY16 (FY15: N9.3bn) and absorbed 10% of

revenue compared with 4% in FY15. In addition, fixed

production costs6 more than trebled to N26.9bn in FY16

(and absorbed 12% of revenue from just 3% in FY15). As

a result, gross margin contracted to a review period low of

18.5% in FY16 (budget: 33.7%), from 30.9% in FY15

while gross profit halved to N40.7bn. Positively, there has

been increased stability in gas supply since September

2016, and most plants can operate on gas, coal and/or

Nigeria Corporate Analysis | Public Credit Rating Page 6

alternative fuels. A 16MW lignite-fired coal power plant is

being built at Ashaka, with commissioning expected for

2018. Combined, selling and administrative costs absorbed

14% of revenue (FY15:12%). The EBITDA margin

declined to an all-time low of 11.7% in FY16 (FY15:

25.2%; five-year average: 25.2%) stemming largely from

pressures from the gross margin line. Consequently,

operating profit plunged to cN10bn, representing less than

20% of initial expectation.

Cement demand was sluggish in Nigeria during 1H FY17

based on the challenging operating environment and delay

in passing the national budget. According to management,

national cement consumption contracted by 28% in 2Q

FY17 y/y, due to prevailing economic realities which

impacted negatively on end-user demand. Consequently,

LAP’s domestic cement sales volumes was 2.5mt in 1H

FY17, compared with 3.1mt in 1H FY16. This was offset

by price increases in Nigeria, which supported 44% y/y

growth in LAP’s revenue to N154.8bn in 1H FY17. Despite

the lower volumes, production costs rose by 20% y/y to

N110.bn in 1H FY17, mainly due to impact of currency

devaluation on maintenance costs, fixed and variable

production costs, as well the increase in the price of gas.

The strong turnover growth bolstered the gross margin to

28.7% (1H FY16: 14.1%), while a correction in the

EBITDA margin to 23.6% (1H FY16: 9.8%) saw a 246%

increase in EBITDA to N36.6bn. Although depreciation

costs increased by 40% y/y, the higher EBITDA margin

and overhead cost rigour supported a 12 percentage-point

correction in the operating margin to 16.7%, leading to a

considerable rise in operating profit to N25.9bn (1H FY16:

N2.9bn; 1H FY15: N32.6bn). Domestic earnings are

typically firmer in the last quarter of the year, due to

increased construction activities in the dry season, which

suggests that FY17 financial performance could supersede

FY15, barring exogenous shocks.

Gross interest costs rose by 45% to N15.5bn in FY16,

mainly due to the impact of cessation of interest

capitalisation on newly commissioned 2.5mtpa line at

UniCem and impact of devaluation in Naira value on USD-

denominated finance costs. Overall, net interest costs rose

by 35% to N11.8bn in FY16. Gross and net interest cover

reduced below 1x due to the depressed operating income,

reflecting marked deterioration in debt serviceability. Net

interest cover rose to 2.6x in 1H FY17 (1H FY16: 0.6x)

despite the 68% increase in net interest expenses, albeit

continuing to track below historical levels. UniCem

accounted for 49% and 53% of gross finance costs in FY16

and 1H FY17 respectively. With the project completed,

gross debt for Nigeria is anticipated to taper below N200bn

at FY17.

LAP reported a significant N22.7bn foreign exchange loss

in 2016, largely the impact of adverse currency movement7

realised on repaying a portion of UniCem’s USD

denominated loans. After accounting for other income, a

7 exacerbated by impact of the 45% devaluation in Naira value

pre-tax loss of N22.8bn was reported in FY16 compared

with a profit of N29.3bn in FY15. The Group reported a

post-tax profit of N16.9bn in FY16, supported by N39.7bn

deferred tax credits from UniCem. After accounting for a

much lower interim tax credit of N1.6bn, net income

increased by an annualised 134% to N19.7 in 1H FY17 (1H

FY16: net loss of N30.2bn), at a 13% net margin (FY16:

8%).

Cash flow Table 9: Working capital (N'bn) FY15 FY16 1H FY17

Inventories 33.0 44.5 57.2

Trade receivables 7.4 7.6 22.1

Trade payables (56.4) (60.4) (42.9)

Operating working capital (15.9) (8.2) 36.4

Other receivables 9.7 17.0 27.3

Prepayments 6.6 9.9 10.1

Other payables and accruals (24.2) (55.3) (82.8)

Current tax payable (0.4) (0.8) (1.0)

Non-operating working capital (8.2) (29.2) (46.4)

Net working capital asset/(liability) (24.1) (37.4) (10.0)

Net working capital movement 0.7 (2.3) (32.9)

Cash generation continues to trend with EBITDA, barring

deviations attributed to one-off restructuring costs, write-

offs and adjustments for fair value and unrealised foreign

currency movements. Cash generation fell sharply in FY16,

registering at N13.8bn (FY15: N54.1bn), which was starkly

at odds with a strong historical trend. Enhanced

profitability saw a correction to N30.7bn in 1H FY17 (1H

FY16: N14.8bn). Working capital requirements have

fluctuated widely over the five and a half years under

review, reflecting the increase in capacity, reorganisation,

and evolving market conditions. That said, pressures

particularly intensified during 1H FY17, with an

unprecedented increase in working capital of N32.9bn (1H

FY16: N2bn decrease). This was partly due to a ramp up of

inventories (both from production and consumables)

attributed to newly commissioned capacity. This was

further exacerbated by slow market uptake of cement

produced, with note also taken of the increased value of

inventories on hand due to the distortive effect of currency

movements. Further distortion came from the inclusion of

advance payments to suppliers related to the UniCem

expansion project. An untapped letter of credit (1H FY17:

N8bn; FY16: N5.6bn; FY15: N4.2bn) related to the Ashaka

project is included in other receivables. The project was

temporarily suspended due to security challenges in North-

Eastern Nigeria.

Historically, trade debtors have had little impact on

working capital movements, as 90% of LAP’s customers

pay before delivery while the other 10% have varying terms

of trade but are usually allowed a 30-day credit period.

However, due to effect of economic recession, customers

that used to pay months in advance, reduced payment

timelines. Trade receivables increased by N14.5bn in 1H

FY17, albeit that trade debtors turnover remained below 20

days. LAP settled around N6bn in outstanding technical

Nigeria Corporate Analysis | Public Credit Rating Page 7

fees during 1H FY17 and N17.3bn in trade creditors while

other payables also increased by N23bn. The net increase

of N5.4bn in creditors was completely offset by the

movement in inventory and debtors’ balances.

The moderate cash generated in FY16 was largely

consumed by the combined interest and tax outlay of

N12.3bn and a N2.3bn, inventory-driven increase in

working capital. Accordingly, LAP reported an operating

cash outflow of N725m in FY16, which was followed by a

much larger interim out flow of N8.4bn in IH FY18.

While no quantified guidance is given regarding LAP’s

dividend policy, management indicated that the dividend

cover is set after taking into account operational and

expansionary capital expenditure requirements as well as

planned investments. The Board proposed a dividend

payment of N1.05 per share on the 2016 results (2015

results: N3 per share), which represented 34.7% (2015:

50%) of net profits. As a result of foreign exchange

liquidity challenges, outstanding dividend balances due to

LafargeHolcim increased from N3.4bn in FY15 to N18.9bn

in 1H FY17 (FY16: N13.2bn). According to management,

around N15bn of the outstanding amount was settled during

3Q FY17.

Since FY14, capex spend has related largely to the

construction of the 2.5mtpa plant at Mfamosing while the

balance was spent on maintenance capex across other

operations. Total capex registered at N41.5bn in FY16

(FY15: 60bn) before tapering to N5.8bn in 1H FY17.

According to management, capex spend will be around

N27bn in FY17, and of this, N17.8bn pertains mainly to the

Ashaka coal fired power plant and UniCem (crusher, line 2

and evacuation road) while N9bn is maintenance and

development capex. The investment inflow of N9.9bn

reported in FY16 is a net movement in receivables due from

related companies (UniCem and NCH). A significant

N69.4bn net investment outflow was reported in 1H FY17

and relates mainly to movement in deferred tax assets and

intercompany receivables. As capex has been mainly

funded by debt, LAP’s net debt increased by a cumulative

N148.9bn in the 30-month period to 1H FY17.

Funding and gearing profile

Underpinned by business combination and capacity

expansion, LAP’s asset base increased fourfold from

N151.9bn at FYE12 to 604.8bn at 1H FY17 (FYE16:

N500.9bn). As is typical of the industry, the Group

evidences a capital-intensive balance sheet, with property,

plant and equipment (“PPE”) having averaged 77% of total

assets over the review period. PPE rose significantly from

N331.3bn in FY14 to N404.4bn in 1H FY17 following the

completion of new 2.5mtpa line. Inventories accounted for

10% of total assets in 1H FY17 (FY16: 9%; five-year

average: 8%). Debtors and prepayments have constituted

around 5% of the asset base since FY13, but increased to

10% of total assets at 1H FY17 (FY16: 7%). Cash balances

have accounted for a stable 4% of the asset base since FY15

and remained robust at N25bn at 1H FY17 (FY16:

N19.2bn). The remainder of the asset base comprised long

term intercompany receivables and deferred tax assets.

For most of the review period, equity has accounted for the

significant portion (over 40%), of funding. Net foreign

currency loans totalled USD595m at July 2016 (USD510m

shareholder loans and USD85m external loans). During 2H

FY16, LAP restructured USD493m (N139bn) of

shareholder loans into a quasi-equity instrument, repayable

at LAP’s discretion (and reported under ‘non-controlling’

interests in the AFS). The loans bear an average interest rate

of 6% p.a. Following the introduction of a dynamic

‡Depreciation used as a proxy for maintenance capex expenditure

*Unaudited six months results to June 2017

Nigeria Corporate Analysis | Public Credit Rating Page 11

This page is intentionally left blank

Nigeria Corporate Analysis | Public Credit Rating Page 12

SALIENT POINTS OF ACCORDED RATINGS

GCR affirms that a.) no part of the rating was influenced by any other business activities of the credit rating agency; b.) the rating was based solely on the merits of the rated entity, security or financial instrument being rated; c.) such rating was an independent evaluation of the risks and merits of the rated entity, security or financial instrument; and d.) The Issuer and Bonds ratings expire in August 2018. Lafarge Africa Plc participated in the rating process via face-to-face management meetings, teleconferences and other written correspondence. Furthermore, the quality of information received was considered adequate and has been independently verified where possible. The credit rating/s has been disclosed to Lafarge Africa Plc with no contestation of the ratings. The information received from Lafarge Africa Plc and other reliable third parties to accord the credit rating included: - the 2016 audited annual financial statements and audited comparative results for the preceding four years, - 2017 budget for Nigerian operations - unaudited management accounts to June 2017, - a completed rating questionnaire containing additional information on Lafarge Africa Plc, - breakdown of facilities available and related counterparties The ratings above were solicited by, or on behalf of, the rated client, and therefore, GCR has been compensated for the provision of the ratings.

ALL GCR CREDIT RATINGS ARE SUBJECT TO CERTAIN LIMITATIONS, TERMS OF USE OF SUCH RATINGS AND DISCLAIMERS. PLEASE READ THESE LIMITATIONS, TERMS OF USE AND DISCLAIMERS BY FOLLOWING THIS LINK:HTTP://GLOBALRATINGS.COM.NG/UNDERSTANDINGRATINGS. IN ADDITION, RATING SCALES AND DEFINITIONS ARE AVAILABLE ON GCR’S PUBLIC WEB SITE AT HTTP://GLOBALRATINGS.COM.NG/RATINGS-INFO. PUBLISHED RATINGS, CRITERIA, AND METHODOLOGIES ARE AVAILABLE FROM THIS SITE AT ALL TIMES. GCR'S CODE OF CONDUCT, CONFIDENTIALITY, CONFLICTS OF INTEREST, COMPLIANCE, AND OTHER RELEVANT POLICIES AND PROCEDURES ARE ALSO AVAILABLE FROM THE UNDERSTANDING RATINGS SECTION OF THIS SITE.