17

LATIN AMERICA INTEGRATING OR DIVERGING? MARIO LÓPEZ ROLDÁN HEAD OF THE INTELLIGENCE OUTREACH UNIT, CABINET OF THE SECRETARY GENERAL, OECD January 2015) Drawing by Pepe Ramírez (6 years)

| Date post: | 18-Dec-2015 |

| Category: |

Documents |

| Upload: | oswald-underwood |

| View: | 215 times |

| Download: | 1 times |

LATIN AMERICA INTEGRATING OR DIVERGING?

MARIO LÓPEZ ROLDÁNHEAD OF THE INTELLIGENCE OUTREACH UNIT, CABINET OF THE SECRETARY GENERAL, OECD

January 2015)

Drawing by Pepe Ramírez (6 years)

INTRODUCTORY WORD OF CAUTION

“Everything you say about Latin America, the opposite

is also true.”Partho Ghosh

Photo: Mirage (Google Images)

It’s so difficult to talk about Latin America as if it was a single entity or a coherent bloc. Keep this in mind.

LATIN AMERICA:A PLETHORA OF INTEGRATION INITIATIVES

70+IN 6 DECADES

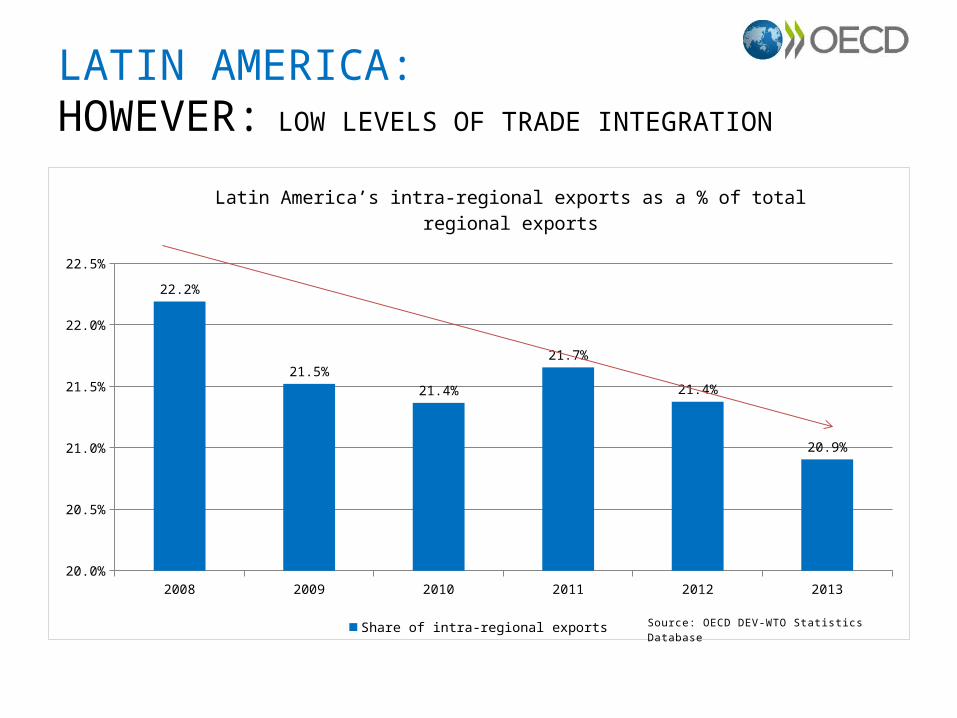

LATIN AMERICA: HOWEVER: LOW LEVELS OF TRADE INTEGRATION

2008 2009 2010 2011 2012 201320.0%

20.5%

21.0%

21.5%

22.0%

22.5%

22.2%

21.5%

21.4%

21.7%

21.4%

20.9%

Latin America’s intra-regional exports as a % of total regional exports

Share of intra-regional exportsSource: OECD DEV-WTO Statistics Database

LATIN AMERICA: COMPARATIVE TRADE INTEGRATION INDICATOR

Europe Asia Latin America Africa0

10

20

30

40

50

60

70

80

68.6

53.4

20.9

12.8

Intra-regional exports as a % of total exports

NAFTA 48%MERCOSUR 14%PACIFIC ALLIANCE 6% (2012)

Source: OECD DEV-WTO Statistics Database. 2012

Nearly 80% of Latin American exports don’t go to Latin American countries.

LATIN AMERICA: INTEGRATION TURBINES SLOWING DOWN

2010 2011 2012 20130

1

2

3

4

5

6

7

8

9

8.1

5.1

3.1

1.5

Growth of exports in volume of goods in Latin America (annual percentage change)

Source: UNCTAD secretariat calculations, based on UNCTADstat.

WHYis regional integration so low

?

Low quality and expensive logistics’ services are hindering Latin America’s trade and integration capacity

LATIN AMERICA 2014: INTEGRATION CHALLENGES

1.POOR LOGISTICS

Latin America & Caribbean Days to clear direct exports through customs

Costa

Rica

Chile

Peru

Colom

bia

Panam

a

Venez

uela

(Bol.

Rep

. of)

Domini

can

Rep.

LAC

Mex

ico

Urugu

ayBra

zil

Argen

tina

OECD

Total

- wor

ld

Europ

e

ASEAN

South

Asia

0

10

20

30

40

50

60

70

Latin America: Ratio of Freight Costs to Tariffs (units, 2012)

Calculations based on imports from the US market. The figures show the ratio of freight cost to tariffs on imports to the region. Source: OECD’S Development Center, Latin American Economic Outlook 2014

LOGISTICS represent18 to 35% of the product’s value in LAC. (8% average in OECD countries)

Brazil and Colombia have some of the world’s highest domestic costs per container for international transport and handling.

CULTURAL CHALLENGE; PUBLIC PROCURMENT; CORRUPTION.

The number of days to clear exports from customs through Latin American borders is particularly high

LATIN AMERICA 2014: INTEGRATION CHALLENGES

2. SLOW CUSTOMS

Latin America & Caribbean Days to clear direct exports through customs

Source: World Bank Group. Enterprise Surveys 2014

Mexico

(2010)

Paragu

ay (2

010)

Venezu

ela (2

010)

Ecuad

or (2010)

Brazil (

2010)

Peru (2

010)

Jamaic

a (2010)

Surin

ame (

2010)

Bolivia

(2010)

Guyana (

2010)

Honduras (2

010)

Niger (

2009)

Tanzan

ia (2013)

Cote d'Iv

oire (2

009)

Ethiopia

(2011)

Camero

on (2009)

Mali (2

010)

Chad (2

009)

Uganda (

2013)

Kenya

(2013)

Zambia

(2013)

Mauriti

us (2009)

0

5

10

15

20

25

7

21.7

18.4 18.2

16.4 16.1

13.112.6 12.4

11.6

10.1

2.6

16.7 16.615.8

15.1

12.9

11.811.2 11.1 10.7 10.3

Days to clear direct exports through customs

SUB-SAHARAN AFRICA

135

LATIN AMERICA

157

The large majority of Latin American SMEs don’t participate in export activities.

LATIN AMERICA 2014: INTEGRATION CHALLENGES

3. LOCALLY ORIENTED SMEs

Latin America & Caribbean Days to clear direct exports through customs

Source: OECD Development Center, with Data from the World Bank, 2013. LEO 2013, p.165

América Latina Europa del Este Asia Oriental0

10

20

30

40

50

60

Pequeñas Medianas Grandes

Firms that export (directly or indirectly) by size and by region (2009-2010)

(percentage)

5%In LAC countries, SMEs account for less than

of total exports

In Italy: close to 50%In Holland: close to 45%

Only about 10-11% of Latin American SMEs export

Most of exporting SMEs in EU member states export to other EU states (76% of SMEs in EU15, 83% of SMEs in EU12).

EU INTEGRATIONENGINES

LATIN AMERICA: INTEGRATION CHALLENGES4. LOW INTEGRATION SYNERGIES THROUGH FDI

• Most FDI inflows go to services and natural resources: 64% of total FDI in 2013 (ECLAC, 2014)

• An important part of FDI in manufacturing goes to Mexico and Central America to re-export to the US.

• Trans-Latinas increasingly important but: only about 14% of FDI inflows to Latin America.

2007-2011

2012

0 10 20 30 40 50 60 70 80 90 100

10

11

9

14

22

24

40

36

4

4

10

5

5

6

Latin America and the Caribbean: origin of foreign direct investment, 2007-2011 and 2012

The Netherlands Latin America United States Other Japan Spain CanadaSource: ECLAC, 2013

LACs export specialisation still greatly focused in natural resources

With a few exceptions, Latin America has not been very successful in inserting itself into Global Value Chains (GVCs).

LATIN AMERICA 2014: INTEGRATION CHALLENGES

5. LOW INTEGRATION TO GVCs

Uruguay 2009

Argentina

Colombia

Brazil

Ecuador

Bol. Rep. Venezuela

Peru

Chile

Mexico

Latin America

Lat. Am. w/out Mex.

0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1Foodstuffs Metals and minerals Fuels Other Manufactured goods

Latin America’s Pattern of Export Specialisation

Source: OECD Development Centre, Latin American Economic Outlook 2014, Data from 2011.

Only about one fifth

ISLSVN

NORDNK

CZE FINSVK

BELAUT

SWELU

XHUN

DEUNLD CHE

FRAPOL

KOROECD

NZLITA

ESTCAN IRL

AUSJP

NGRC

ESPGBR

GBRPRT ISR

USAUSA

TURTUR

MEXCHL

0.00

0.10

0.20

0.30

0.40

0.50

0.60

2010 or latest available year Mid-1990s Mid-1980s

Latin America has made important progress combating extreme poverty and reducing inequality, but POVERTY, VULNERABILITY and INEQUALITY are still very important challenges.

LATIN AMERICA 2014: INTEGRATION CHALLENGES

6. POVERTY & INEQUALITY

Source: 67% = World Bank Group, Shifting Gears to Accelerate Shared Prosperity in Latin America and the Caribbean, World Bank Document No. 78507, June 2013. Graph: OECD Factbook 2014, p. 65

67%Trends in income inequality Gini coefficient in the mid-80s, mid-90s and around 2010s

RATIO OF AVERAGE INCOME OF RICHEST 10% TO THE POOREST 10%• Chile: 27 times (OECD)• Mexico: 31 times (OECD)• Argentina: 31 times (UNDP)• Brazil: 50 times (OECD)• Bolivia: 93 times (UNDP)• OECD average 10 times (OECD)

LIVE IN POVERTY OR VULNERABILITYEARNING LESS THAN $10 A DAY (WB)

Shan

ghai

-C...

Sing

apor

eHo

ng K

ong-

...Ch

ines

e Ta

ipei

Kore

aM

acao

-Chi

naJa

pan

Liech

tens

tein

Switz

erla

ndNe

ther

land

sEs

toni

aFi

nlan

dCa

nada

Pola

ndBe

lgiu

mGe

rman

yVi

et N

amAu

stria

Aust

ralia

Irela

ndSl

oven

iaDe

nmar

kNe

w Z

eala

ndCz

ech

Repu

...Fr

ance

OEC

D av

erag

eUn

ited

Kin.

..Ice

land

Latv

iaLu

xem

bour

gNo

rway

Port

ugal

Italy

Spai

nRu

ssia

n Fe

d...

Slov

ak R

epu.

..Un

ited

Stat

esLit

huan

iaSw

eden

Hung

ary

Croa

tiaIsr

ael

Gree

ceSe

rbia

Turk

eyRo

man

iaBu

lgar

iaUn

ited

Arab

...Ka

zakh

stan

Thai

land

Chile

Mal

aysia

Mex

icoM

onte

negr

oUr

ugua

yCo

sta

Rica

Alba

nia

Braz

ilAr

genti

naTu

nisia

Jord

anCo

lom

bia

Qat

arIn

done

siaPe

ru

350.00

400.00

450.00

500.00

550.00

600.00

650.00

Mean score at the same level as the OECD average

Mean score

Education plays a key role in integration: THE HYDRA OF LAC

LATIN AMERICA 2014: INTEGRATION CHALLENGES

7. EDUCATION

Source:

LOW QUALITY EDUCATION SYSTEMS: 8 LAC countries among the last in PISA.

WEAK HIGHER EDUCATION: No Latin American university among the world’s top 100.

LAC INTEGRATION IN CURRICULA: Low presence of LAC Integration in higher, postgraduate and MBAs education programmes.

A LATIN AMERICAN “ERASMUS”: Latin America needs to develop stronger exchange programmes for students geared towards promoting LAC economic integration.

Student performance in PISA 2012 (mathematics)

Let’s not forget these three key factors:

GEOGRAPHY: A huge region: Distance from Mexico City to Buenos Aires = Paris to Kathmandu; 106 hours drive from Brasilia to Bogota.

IDEOLOGY

MIRAGE:

CULTURE:

LATIN AMERICA 2014: INTEGRATION CHALLENGES8. GEOGRAPHY, IDEOLOGY, CULTURE & LAW

RULE OF LAW: ONE OF THE CENTRAL CONCERNS FOR BUSINESS IN THE REGION.

THE MARKET ORIENTED VS. STATE ORIENTED BLOCS DISCUSSION CAN BE DECEIVING

SIZE OF STATE IN THE ECONOMY:Public spending: Brazil 40% of GDP;Argentina 44%.

Canada 40%; the UK 48%;Denmark about 60%;EU about 50% (average).

LATIN AMERICA: TO CONCLUDE:SIX GOOD NEWS FOR INTEGRATION

The region is expected to invest at least US$1.5 trillion in infrastructure projects over the next decade (IDB)

The come back of Bachelet to Chile is starting to build a link between Mercosur and Pacific Alliance.

FDI by Trans-Latinas is growing strongly and most of these investments go to countries of the region.

In contrast with developed economies, most adults in Latin America believe their children will have a better life than theirs.Expectations count!

Mexico’s success approving 11 structural reforms is having positive spillovers in other LAC countries where similar reforms are on track.

OECD growing engagement with the region in a myriad of policy areas through inclusive initiatives that bring the different blocs together..

LATIN AMERICA

INTEGRATING OR DIVERGING?

Probably none of the above!

THANK YOU.

MARIO LÓPEZ ROLDÁNHEAD OF THE INTELLIGENCE OUTREACH UNIT, CABINET OF THE SECRETARY GENERAL, OECD

Drawing by Pepe Ramírez (6 years)