15

Leasing Market Conference Leasing Market Conference October 5, 2004 October 5, 2004 Bucharest Bucharest THE EVOLUTION OF LEASING MARKETS & THE STAGE OF ROMANIAN PRACTICE

| Date post: | 16-Dec-2015 |

| Category: |

Documents |

| Upload: | eileen-parsons |

| View: | 217 times |

| Download: | 2 times |

Leasing Market ConferenceLeasing Market Conference

October 5, 2004October 5, 2004

BucharestBucharest

THE EVOLUTION OF LEASING MARKETS & THE STAGE OF ROMANIAN PRACTICE

2

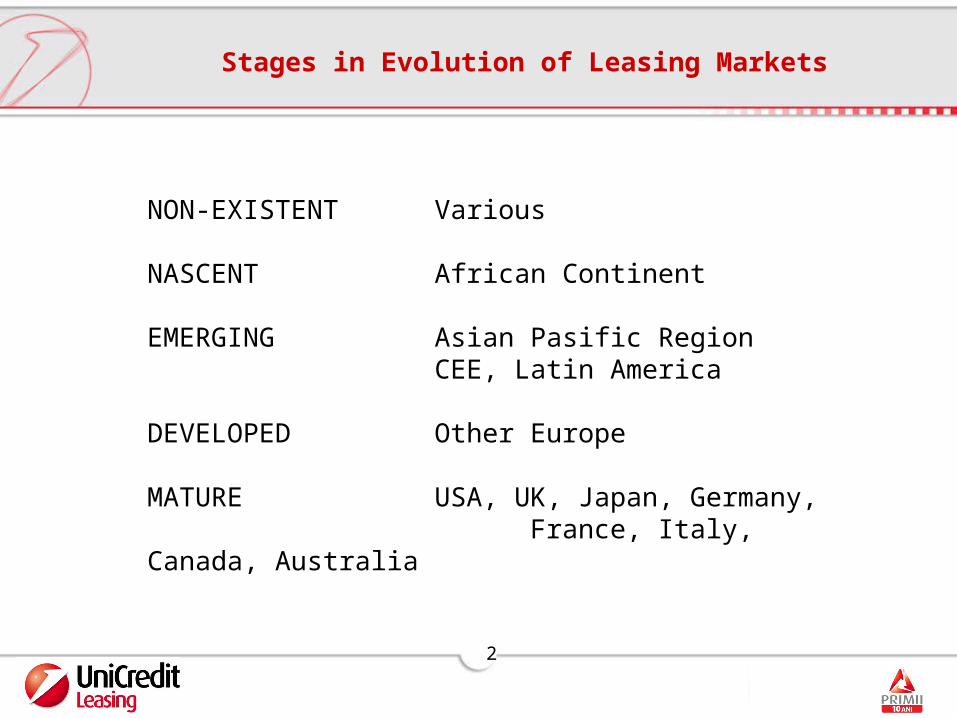

Stages in Evolution of Leasing Markets

NON-EXISTENT Various

NASCENT African Continent

EMERGING Asian Pasific RegionCEE, Latin America

DEVELOPED Other Europe

MATURE USA, UK, Japan, Germany,France, Italy, Canada, Australia

3

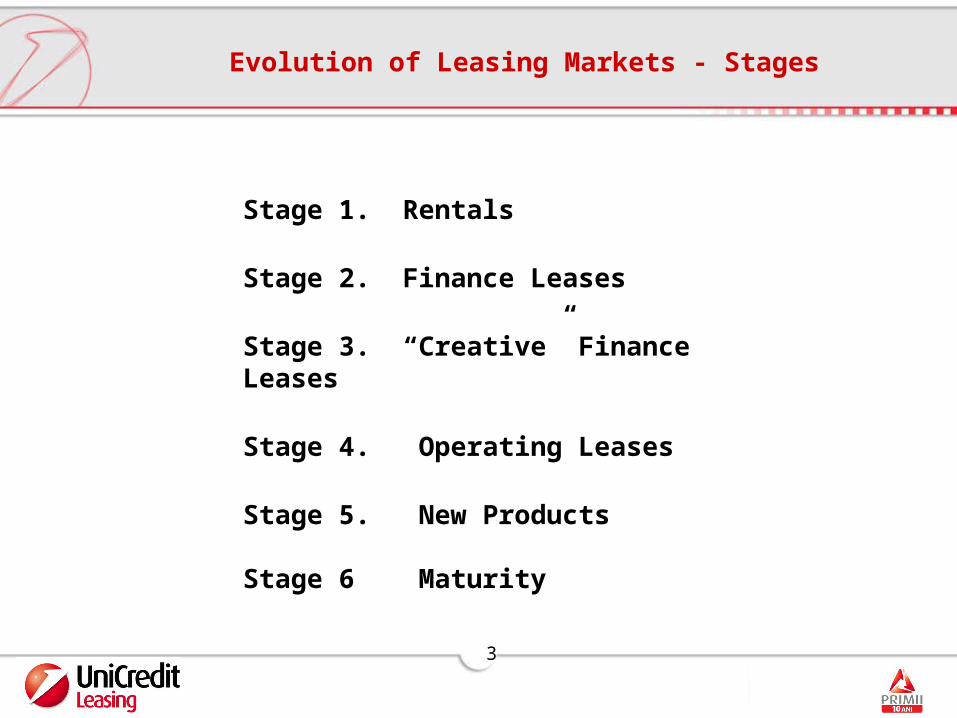

Evolution of Leasing Markets - Stages

Stage 1. Rentals

Stage 2. Finance Leases

Stage 3. “Creative” Finance Leases

Stage 4. Operating Leases

Stage 5. New Products

Stage 6 Maturity

4

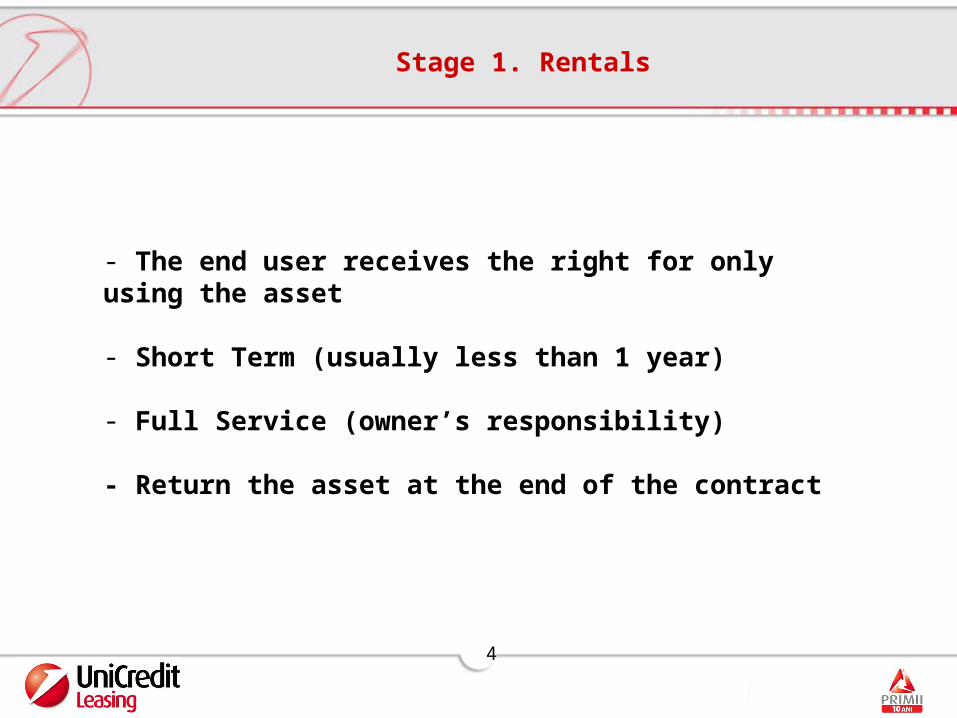

Stage 1. Rentals

- The end user receives the right for only using the asset

- Short Term (usually less than 1 year)

- Full Service (owner’s responsibility)

- Return the asset at the end of the contract

5

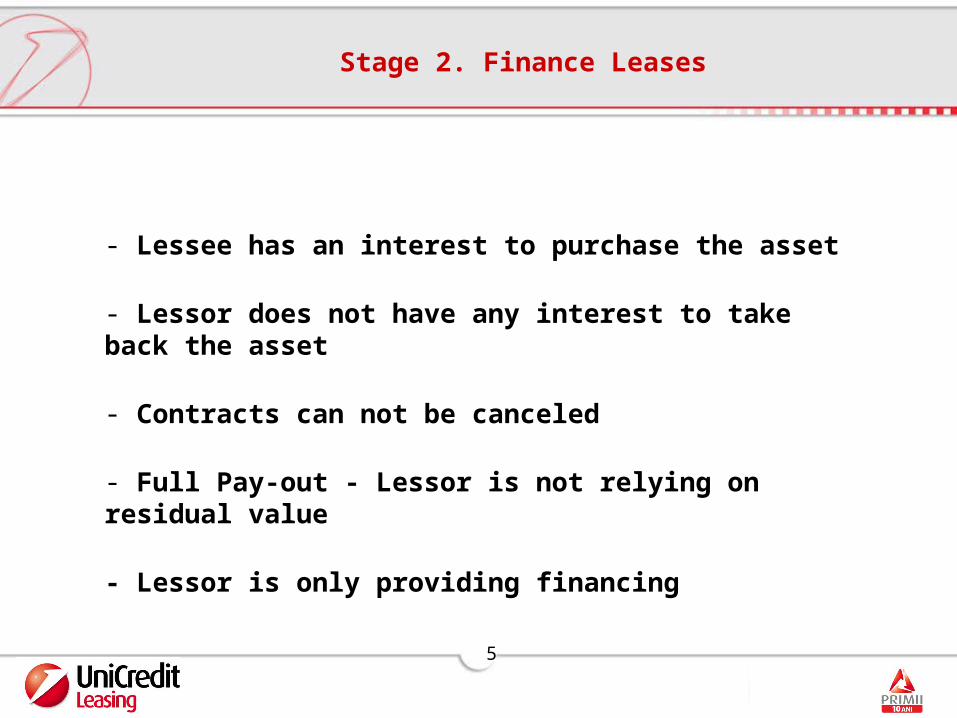

Stage 2. Finance Leases

- Lessee has an interest to purchase the asset

- Lessor does not have any interest to take back the asset

- Contracts can not be canceled

- Full Pay-out - Lessor is not relying on residual value

- Lessor is only providing financing

6

Stage 3. “Creative” Finance Leases

- Increasing competition

- Structuring the leases (more suitable to business cash flow)

- Formation of in-house lessors (sales aid - captive leases)

- Value of the equipment and residual value start to be considered

- Rental wars and commissions more present- increasing competition

- Largest growth takes place during this stage

7

Stage 4. Operating Leases

- Full service- Fleet Management

- Asset is usually returned - Lessor has asset risk

- Sophisticated Lessee and Expertised Lessor

- Developing secondary markets

- Demand from multinational lessees

8

Stage 5. New Products

- Venture Leasing – Greenfield Investments

- Securization

- Cross border Transactions – Airplanes, ships

- Strong network, logistics and legal-fiscal infrastructure

9

Stage 6. Maturity

- M&A - Consolidation – Big become bigger

- Focus on alliances- joint ventures

- Intense Competition & Lower Margins

- Highlighting the Value Added

10

Highlights

- The above stages refer globally to the market and not necessarily to the players

- A company could remain in finance leasing for its entire life – but it is expected to be a niche company in maturity stage (ex. Financial Lease could remain the only product even in maturity stage)

- Different products could be in different stages

11

Infrastructure Supporting Leasing

I. LEGAL - Ownership Title - Not as a burden for lessor - Expedient repossesion and recovery - Clear description of rights and responsabilities II. TAX & ACCOUNTING - IAS 17 Interest; expense for lessee, revenue for lessor - Depreciation in lessee’s hands in financial leasing in lessor’s hands in operational leasing preferably over the lease term

III. REGULATORY - Lessors to be regulated - Minimum capital requirements

12

Romanian Practice

- Starts to develop in 1994, recent modifications in law in 1999

- No need for operating licence

- It seems that a yearly volume of about at least EUR 1 billion

- Financial Lease is the most common product (several tries existed for operational lease but ceased due to the low sustainability)

- Captives were established especially for the vehicle market

13

Future Expectations for Romania

- Captive leasing companies will focus more on operating leasing. Profit margins will be increased, the future sales will be secured due to unexcercised buy option, fleet management services will be fashion,

- Market will start to consolidate, M&A are expected to follow, small and independent lessors will dissappear or in short term focus on operating leases,

- Banks are interested to develop their own leasing facilities due to lending limits, banking lessors focus only on financial leasing,

- Margins will decrease more and volumes are becoming more and more important, ROL lending will be made by banking lessors

14

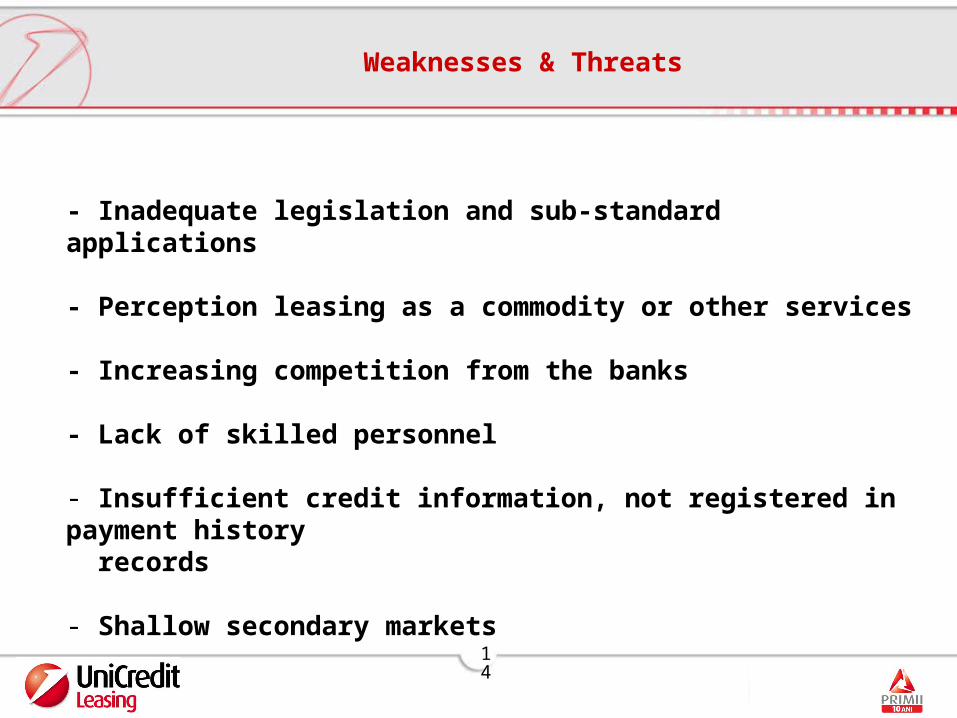

Weaknesses & Threats

- Inadequate legislation and sub-standard applications

- Perception leasing as a commodity or other services

- Increasing competition from the banks

- Lack of skilled personnel

- Insufficient credit information, not registered in payment history records

- Shallow secondary markets

15

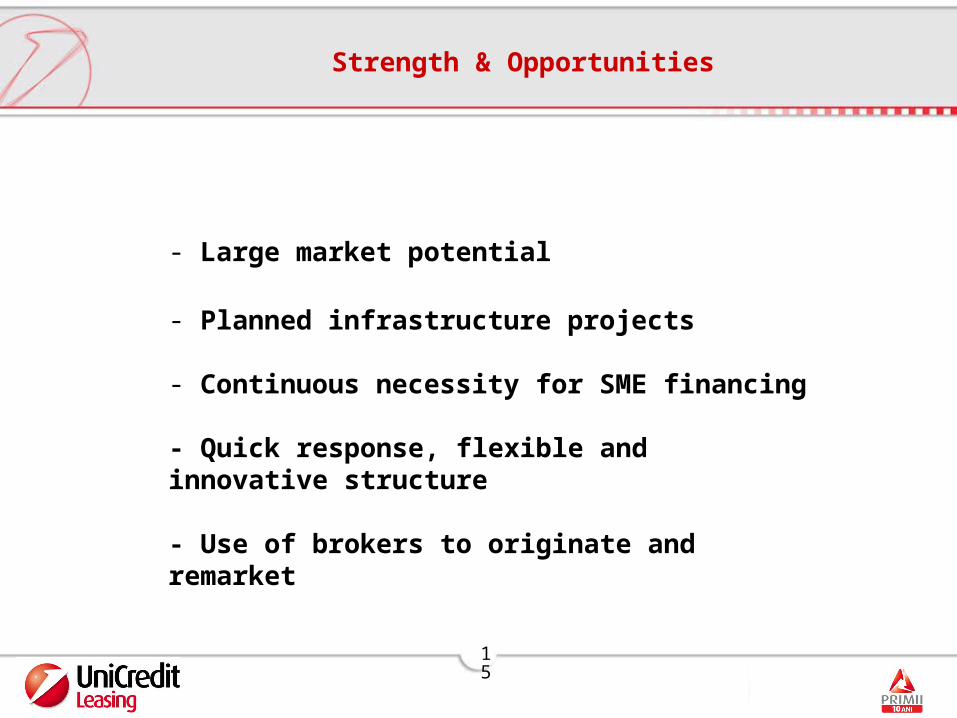

Strength & Opportunities

- Large market potential

- Planned infrastructure projects

- Continuous necessity for SME financing

- Quick response, flexible and innovative structure

- Use of brokers to originate and remarket