31

Why Lease? Leasing as an alternative to debt or equity Sponsors

Why Lease? Leasing as an alternative to debt or equity

Sponsors

This presentation was prepared exclusively by Blue Sky Capital Strategies, LLC (“Blue Sky”) for the benefit and internal use of the Blue Sky client to whom it is addressed and delivered (including the client’s affiliates, the “Client”) in order to assist the Client in evaluating, on a preliminary basis, the structure and feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation may not be disclosed orused for any other purpose than our discussions without the prior written consent of Blue Sky. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by Blue Sky. This presentation does not constitute a commitment by Blue Sky to structure a transaction, arrange credit or to provide any other services.

The information in this presentation is based upon any information and forecasts supplied to us by the Client and others and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. Blue Sky’s opinions and estimates constitute Blue Sky’s current judgment and should be regarded as indicative, preliminary and for illustrative purposes only. We have relied upon and assumed, without independent verification, the accuracy and completeness of all information supplied by or on behalf of the Client, including your estimates and forecasts of future financial performance, information available from public sources or which was otherwise reviewed by us. Blue Sky does not represent or warrant the accuracy or completeness of any such information and is not responsible for losses or damages arising out of errors, omissions or changes in any of the information, market factors or any other events. This presentation does not purport to contain all of the information that an interested party may desire and, in fact, may provide only a limited view of particular transactions in particular markets. Blue Sky’s views in this presentation may change at any time and we assume no obligation to update or otherwise revise this presentation. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Client or any other entity. Blue Sky makes no representations as to the actual value of any aspect of the Client’s business, underlying assets or proceeds which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Past performance should not be taken as an indication or guarantee of future performance, and no representation or warranty, expressed or implied is made regarding future performance.

Blue Sky is an independent strategic financial advisor. It does not provide investment banking, investment advice, direct investment, broker or dealer services, tax or legal services. However, through its wide network of connections, it can provide access to the wide variety of entities that offer those and other services. Blue Sky may, from time to time, participate or invest in transactions similar to the transactions that you may engage in, perform services for or solicit business from other entities that may be similar to the services performed for you, and/or have a position or effect transactions for entities that might be competitive with your businesses.

Introduction

Blue Sky Capital Strategies, LLC (“Blue Sky”) is an international corporate finance and capital structure advisory firm with offices in New York, Chicago, DC & Michigan

We provide strategic financial advice for companies seeking to raise capital or enhance liquidity, expand funding alternatives, monetize cash flow or mitigate risk

We specialize in designing tax-efficient lease finance solutions tailored to meet the needs of capital intensive businesses and/or high yield corporate credit profiles

Senior management has over eighty years of combined leasing experience in both lessor and lessee roles, executing over $2 billion of diverse lease transactions

Blue Sky has assembled the resources with the financial, legal, tax and accounting expertise to evaluate, structure and execute broad rage of lease financings

A successful leasing program requires the participation of a broad spectrum of stakeholders including operating units, FP&A, Treasury, Tax, Legal & Procurement

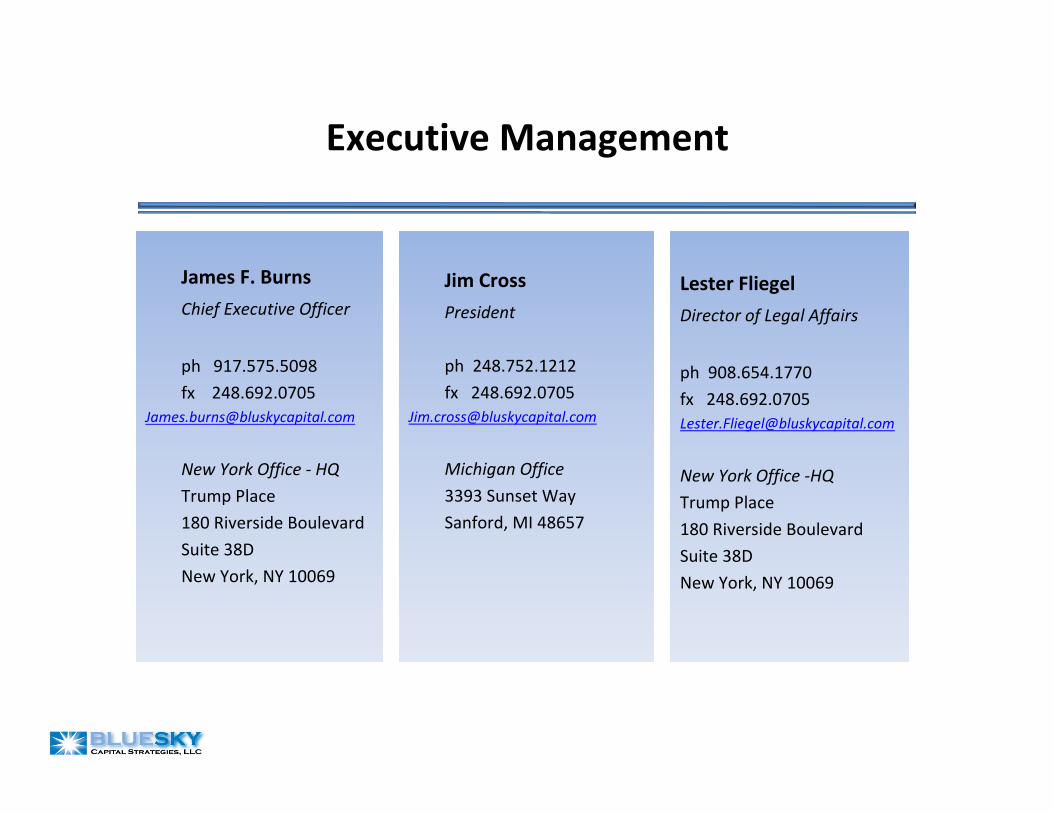

Executive Management

James F. Burns

Chief Executive Officer

ph 917.575.5098

New York Office ‐ HQ

Trump Place

180 Riverside Boulevard

Suite 38D

New York, NY 10069

Jim Cross

President

ph 248.752.1212

Michigan Office

3393 Sunset Way

Sanford, MI 48657

Lester Fliegel

Director of Legal Affairs

ph 908.654.1770

New York Office ‐HQ

Trump Place

180 Riverside Boulevard

Suite 38D

New York, NY 10069

Credit Crisis ‐ the Aftermath

Following the meltdown of financial markets, companies continue to confront significant challenges concerning access to and the availability of capital

These unprecedented events have resulted in a global repricing of risk and credit and a greater scrutiny of borrowers by lenders and investors

Many banks have shed credit relationships and existed industry sectors, limiting their balance sheet to only their most profitable customers

The impact of these changes can be measured in a number of tangible ways;I. Wider credit spreadsII. More restrictive covenantsIII. Consolidation of funding sourcesIV. Stricter underwriting practices

Last Fed Survey of loan officers reported credit remained pricey and loan terms strictwith 95% of banks keep credit standards for large & mid-size companies unchanged

Why Lease ?

Prudent fiscal stewardship mandates corporations actively pursue methods to creatively augment their borrowing capacity and diversify the liquidity

Leasing enables a company to realize economic benefits and/or achieve financial flexibility not available through conventional debt or equity alternatives

Credit crisis notwithstanding, access to and availability of capital for leasing transactions remains robust across the credit spectrum

Both single investor and leveraged lease structures provide access to incremental liquidity outside of traditional funding sources, such as “tax equity” investors

Under MACRS, a lack of currently taxable income, an AMT status or a net operating loss (“NOL”) carry-forward position each limit a company’s ability to effectively monetize the economic benefits associated with tax ownership

Leasing provides a cost effective method to offset the limitations to accessing debt financing inherent with a speculative grade credit rating

Economics behind “Buy vs. Lease”

There are some critical distinctions between owning title to an asset and simply securing the rights to use it (through a covenant of “quiet enjoyment”)

Three primary variables underpin the decision in a buy vs. lease analysis:I. Credit profileII. Tax positionIII. Residual value

In addition, the impact of soft costs embedded in a leasing agreement (such as notification and return provisions) should also be factored into the analysis

Lessees should utilize a financial modeling application such as SuperTRUMP to perform the analysis to offset Lessor’s advantages of employing similar tools

Blue Sky’s ability to market the credit story is vital for securing Lessor’s credit committee approval for the most attractive rates

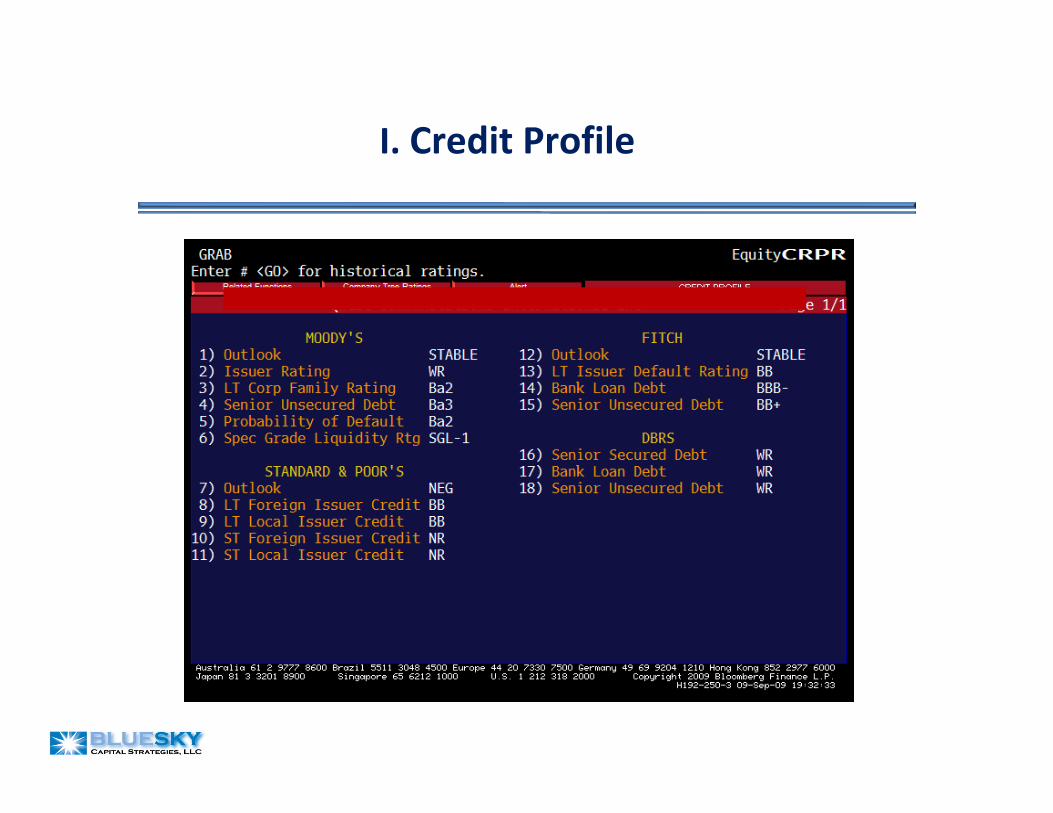

I. Credit Profile

II. Tax Considerations

Tax attributes often play a principal or determinative role in the decision to lease

The basic tax benefit of leasing (for lessors) is tax deferral; the generation of tax losses in the early years, offset by tax income in the later years of equal amounts

Objective of “True” Lease: Provide financing party with right to claim tax benefits of ownership intended for use by another party so benefits can be shared through lower rentals payments which reflects a “borrowing cost” less than a market interest rate

Step 1 – identify benefitsStep 2 – structure transaction to pass benefitsStep 3 – enhance value through leverage

Taxes to model in the Buy vs. Lease analysis:o Property taxo Sales and use tax

o Federal income taxo State and local income tax

Sale-leaseback transactions for fully (tax) depreciated assets which still have significant useful lives provide effective financing option for companies with significant NOL’s

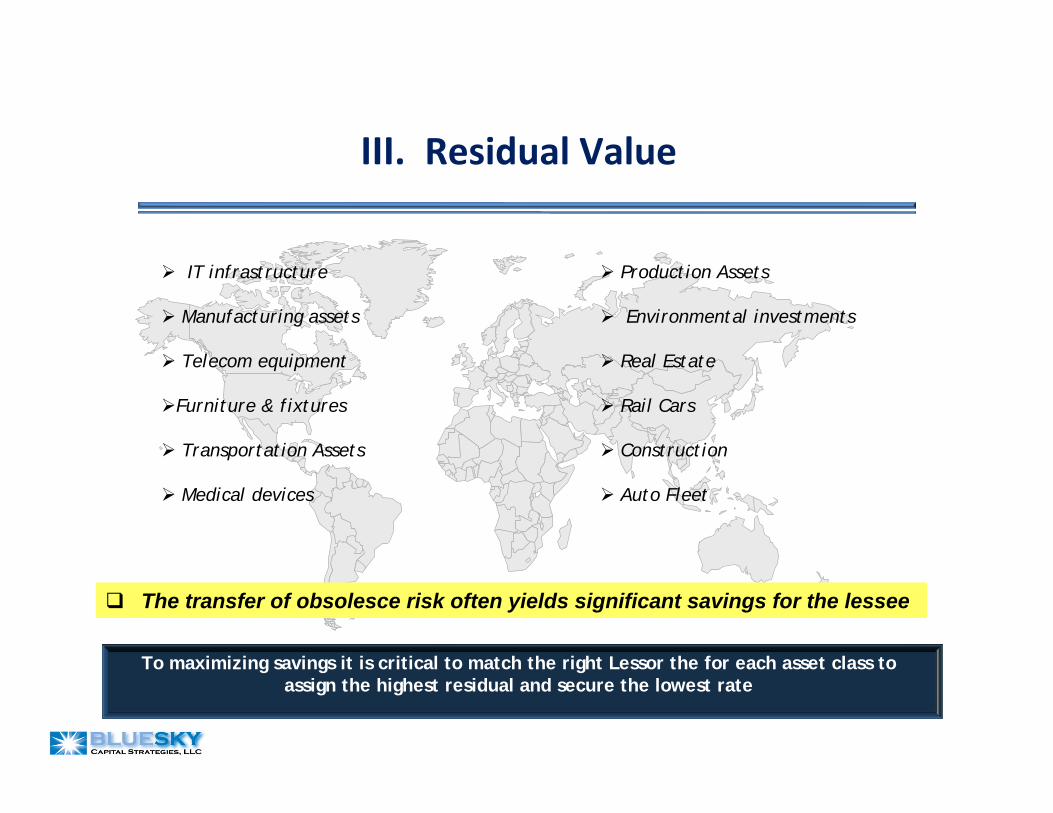

III. Residual Value

To maximizing savings it is critical to match the right Lessor the for each asset class to assign the highest residual and secure the lowest rate

The transfer of obsolesce risk often yields significant savings for the lessee

IT infrastructure

Manufacturing assets

Telecom equipment

Furniture & fixtures

Transportation Assets

Medical devices

Production Assets

Environmental investments

Real Estate

Rail Cars

Construction

Auto Fleet

Leasing 101

Leasing transactions encompass three distinct perspectives

In addition to performing the economic analysis, it’s crucial to establish the accounting, tax and legal disclosure objectives prior to deal closing

Financial Reporting (FASB)

Classifications

Capital or Operating

Statutory Reporting (IRS) True or Conditional Sale

Legal Reporting (UCC) Article 2A or Article 9

Any leasing platform should generate the documentation and audit trails required to support the various and financial reporting requirements

Three Keys to a Successful Leasing Program

I. Documentation

o Delivery & Acceptance

o Events of default and remedies

o Automatic/deemed acceptance

o Notifications provisions

o Tax indemnities

o Insurance requirements

o Lessor assignments

o Early terminations / EBO points

o SLV and casualty loss tables

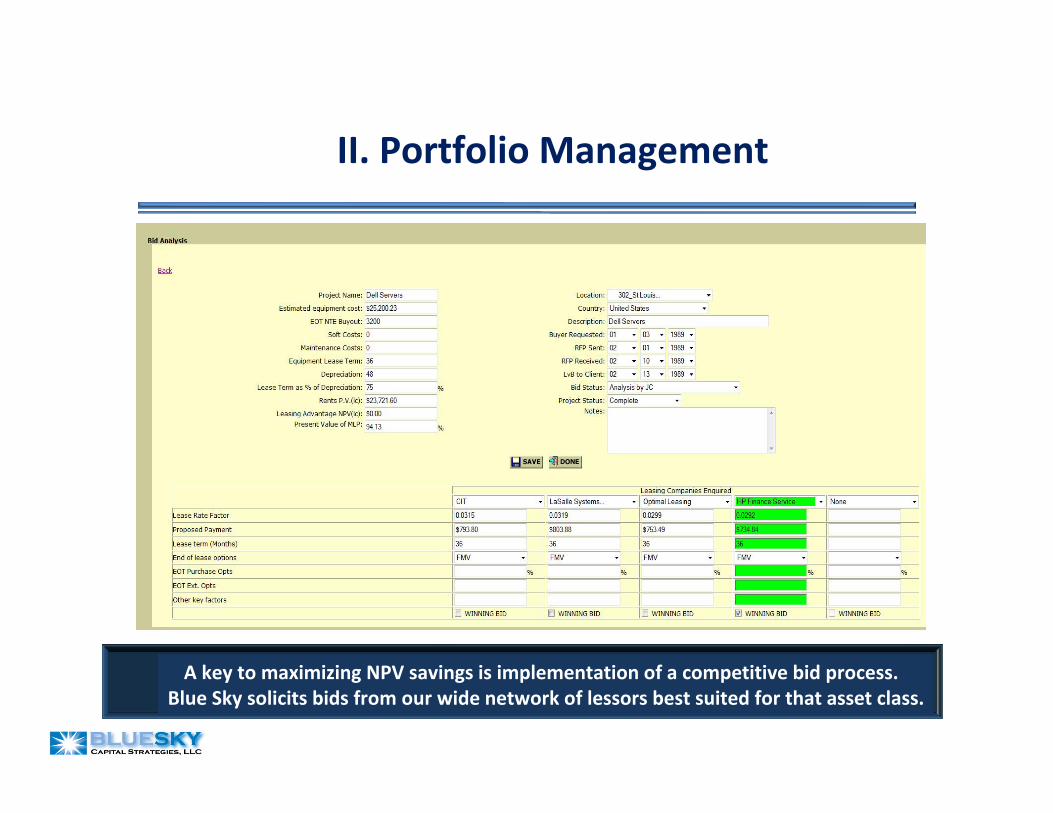

II. Portfolio Management

o Centralized lease portfolio

o Documentation repository

o Automated notices

o Financial reporting tool

o Tax reporting tool

o Bid tracking and reporting

o SARBOX reporting

o Automated G/L interface

o Treasury Workstation compatible

III. Financial Analysis

o Lease vs. Purchase analysis

o NOL, AMT, full tax pay analysis

o Linear pricing optimization

o E.B.O. and exit point modeling

o Return on time / lease to own

o IRS Tax classification test

o FASB 13 classification test

o Cash Flow Arrays

o Periodic expenses or income

The following parts must be contemplated with any Best Practices …

I. Documentation

II. Portfolio Management

A key to maximizing NPV savings is implementation of a competitive bid process. Blue Sky solicits bids from our wide network of lessors best suited for that asset class.

III. Financial Analysis

After Tax Economics• NPV savings - $123.8K

• PV of rents - $3.142M

• Implicit rate – 2.44%

• Cost of capital – 7.0%

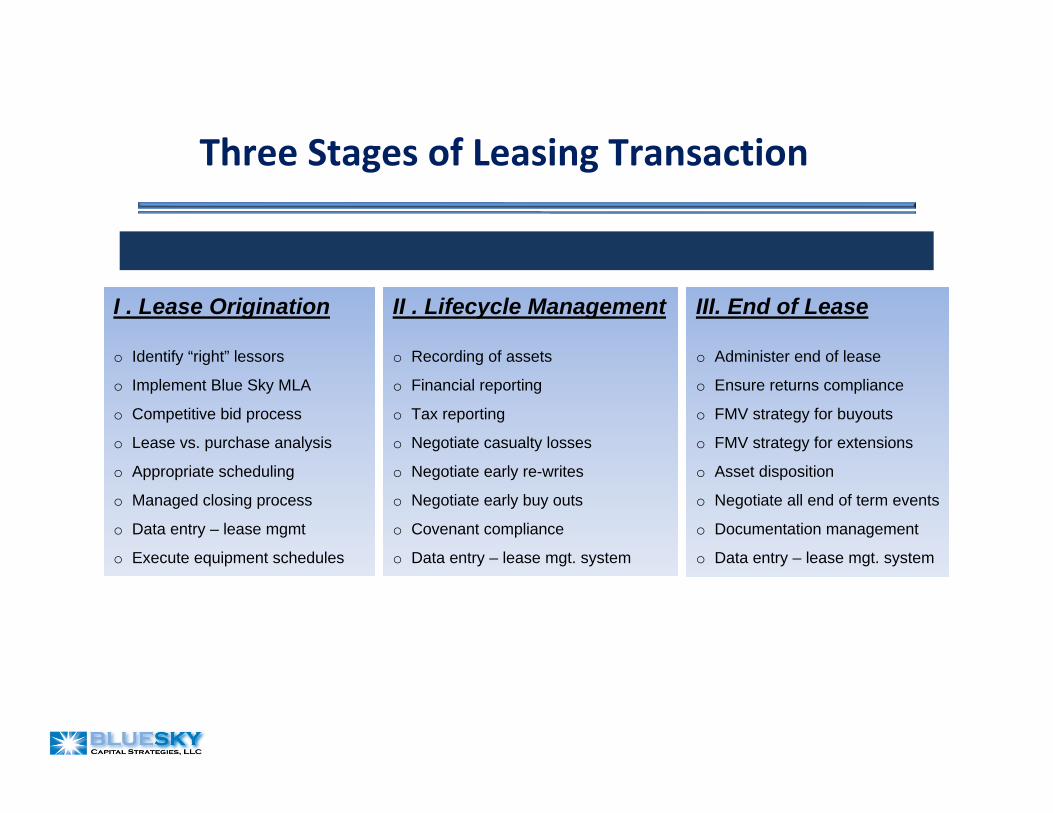

Three Stages of Leasing Transaction

I . Lease Origination

o Identify “right” lessors

o Implement Blue Sky MLA

o Competitive bid process

o Lease vs. purchase analysis

o Appropriate scheduling

o Managed closing process

o Data entry – lease mgmt

o Execute equipment schedules

II . Lifecycle Management

o Recording of assets

o Financial reporting

o Tax reporting

o Negotiate casualty losses

o Negotiate early re-writes

o Negotiate early buy outs

o Covenant compliance

o Data entry – lease mgt. system

III. End of Lease

o Administer end of lease

o Ensure returns compliance

o FMV strategy for buyouts

o FMV strategy for extensions

o Asset disposition

o Negotiate all end of term events

o Documentation management

o Data entry – lease mgt. system

Lessor Selection Process

Leasing for the U.S. is a $250B industry – There are over 1000 active lessorsChoosing the most appropriate lessors is critical

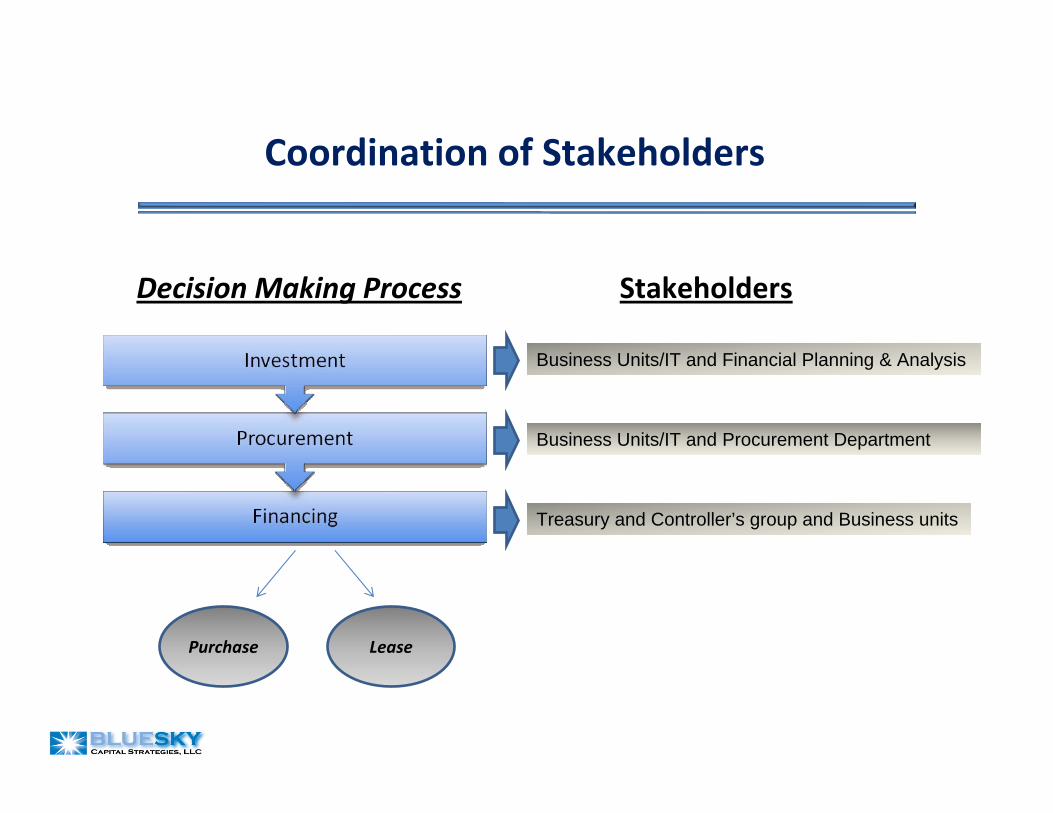

Coordination of Stakeholders

Decision Making Process

Business Units/IT and Financial Planning & Analysis

Business Units/IT and Procurement Department

Treasury and Controller’s group and Business units

Purchase Lease

Stakeholders

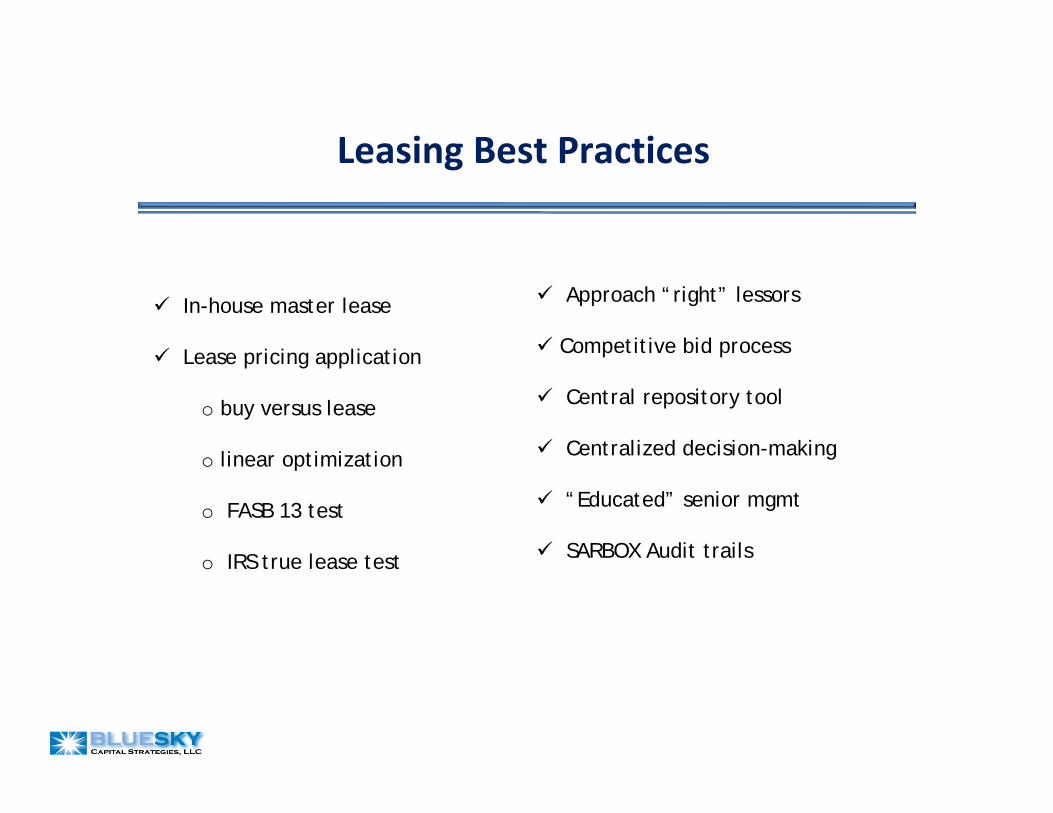

Leasing Best Practices

In-house master lease

Lease pricing application

o buy versus lease

o linear optimization

o FASB 13 test

o IRS true lease test

Approach “right” lessors

Competitive bid process

Central repository tool

Centralized decision-making

“Educated” senior mgmt

SARBOX Audit trails

Advantages of Lease Finance

A leasing program should be tailored to support the company’s internal and external financial objectives and supplement funding within existing covenants

Enhance Capital Structure

Lower cost of capital

Preserve liquidity

Transfer obsolescence risk

Enhance financial flexibility

Supplement funding sources

Support Financial Metrics

Equity analysts

Rating agencies

Bank lenders

Bond holders

Senior management

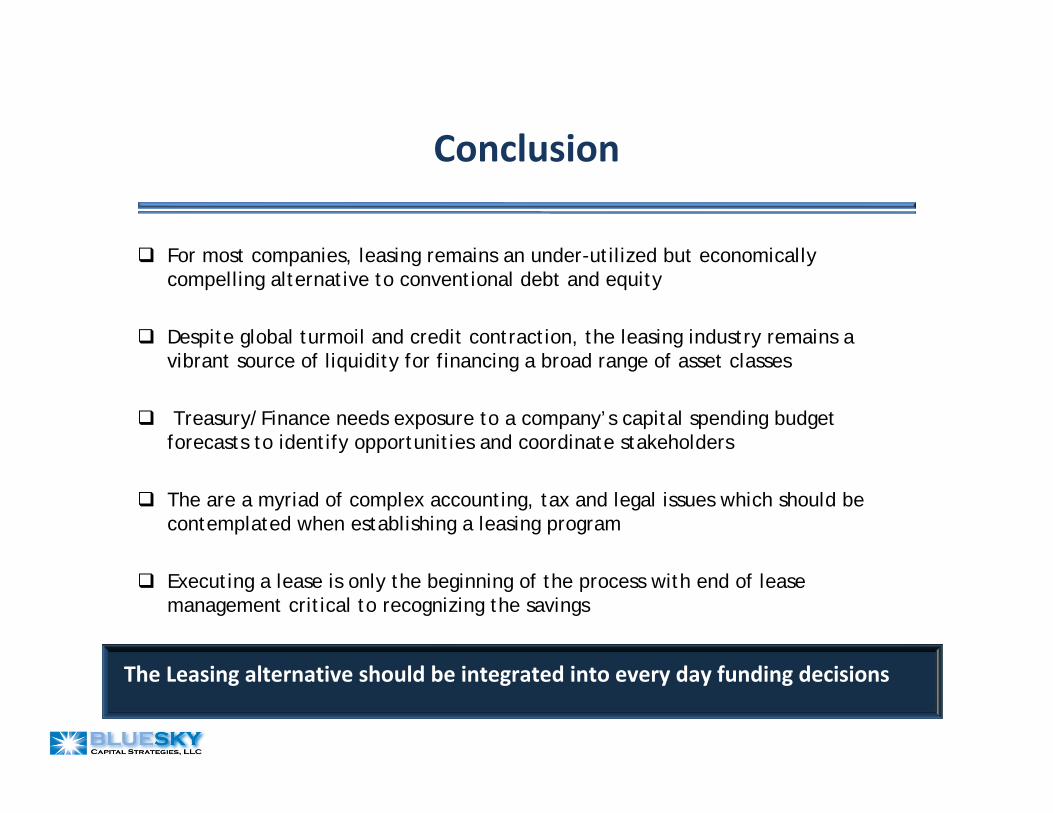

Conclusion

For most companies, leasing remains an under-utilized but economically compelling alternative to conventional debt and equity

Despite global turmoil and credit contraction, the leasing industry remains a vibrant source of liquidity for financing a broad range of asset classes

Treasury/Finance needs exposure to a company’s capital spending budget forecasts to identify opportunities and coordinate stakeholders

The are a myriad of complex accounting, tax and legal issues which should be contemplated when establishing a leasing program

Executing a lease is only the beginning of the process with end of lease management critical to recognizing the savings

The Leasing alternative should be integrated into every day funding decisions

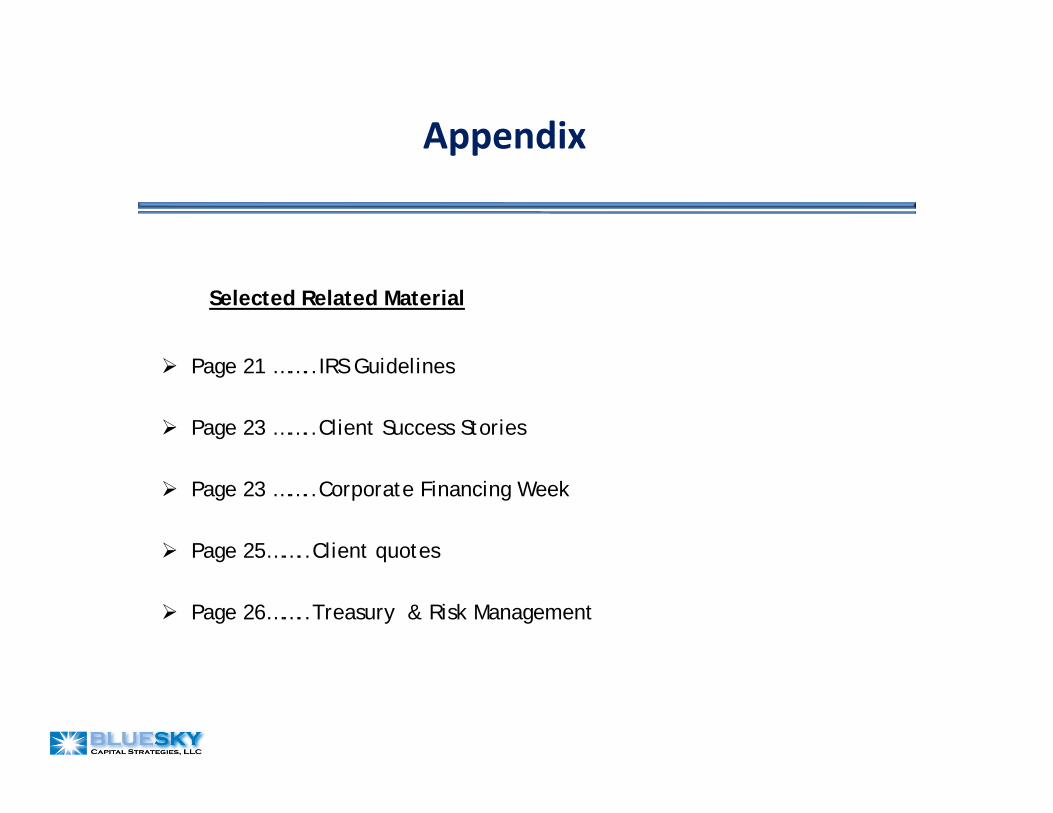

Appendix

Selected Related Material

Page 21 ……..IRS Guidelines

Page 23 ……..Client Success Stories

Page 23 ……..Corporate Financing Week

Page 25……..Client quotes

Page 26……..Treasury & Risk Management

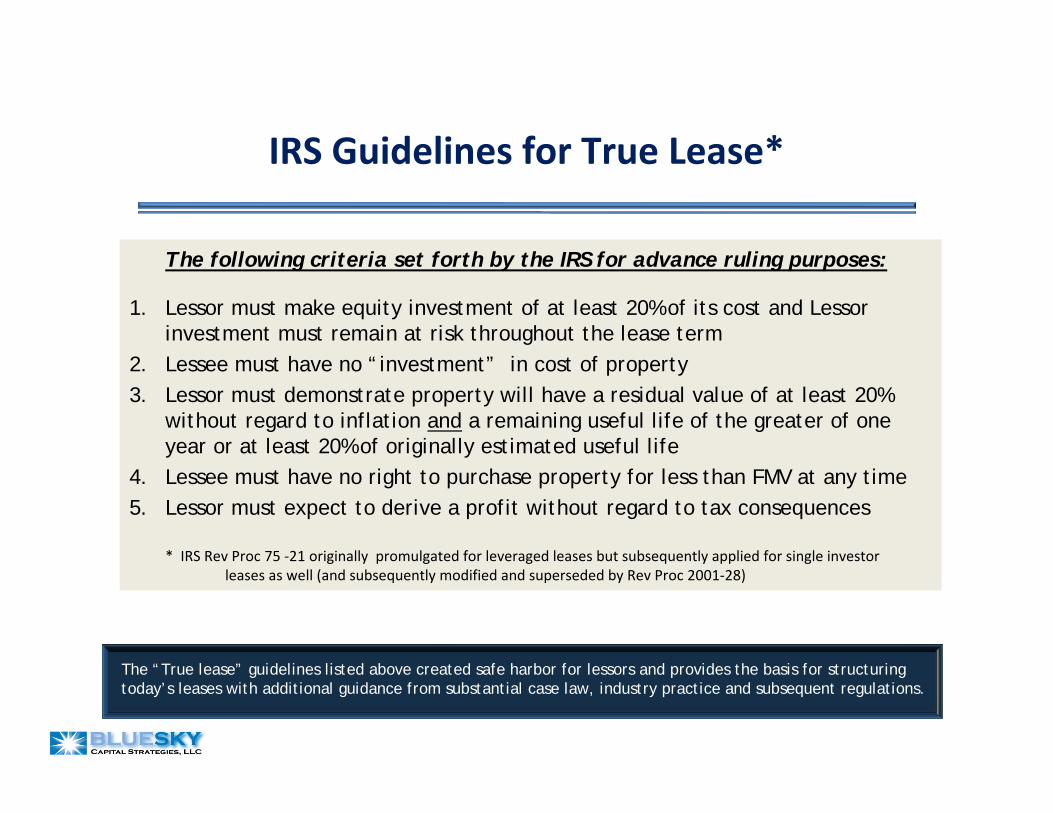

IRS Guidelines for True Lease*

The following criteria set forth by the IRS for advance ruling purposes:

1. Lessor must make equity investment of at least 20% of its cost and Lessor investment must remain at risk throughout the lease term

2. Lessee must have no “investment” in cost of property3. Lessor must demonstrate property will have a residual value of at least 20%

without regard to inflation and a remaining useful life of the greater of one year or at least 20% of originally estimated useful life

4. Lessee must have no right to purchase property for less than FMV at any time5. Lessor must expect to derive a profit without regard to tax consequences

* IRS Rev Proc 75 ‐21 originally promulgated for leveraged leases but subsequently applied for single investor leases as well (and subsequently modified and superseded by Rev Proc 2001‐28)

The “True lease” guidelines listed above created safe harbor for lessors and provides the basis for structuring today’s leases with additional guidance from substantial case law, industry practice and subsequent regulations.

IRS Guidelines for a Conditional Sales Contact*

Does not qualify for “true lease” designation if one or more of the following;

a) Any portion of the periodic lease payment are made to an equity position in the asset to be acquired by the lessee

b) Lessee automatically acquires title upon payments of stated amount of required “rentals”

c) Total amount of lessee payments for a relatively short period of use constitutes an inordinately large proportion of the total due to secure title

d) The agreed “rental” payments materially exceed the current fair rental valuee) Property may be acquired under a purchase option at a price which is nominal in

relation to the value of the property at the time when the option may be exercised, as determined at the time or entering the original agreement

f) Some portion of the periodic payment is specifically designated as interest

* IRS Revenue Ruling 55‐540, 1955‐2 CB39, ‐ “Guides to be used in determining the treatment, for Federal income tax purposes, of leases of equipment used in trade or business of the lessee.”

*

Client Success Stories

Automotive Manufacturer – 2001 – 2003 savings of $3.5 Million

Automotive Supplier – 2004 savings of $1.8 Million

Automotive Supplier – 2003 – 2008 $2.25 Million

Digital Satellite Radio Provider ‐ 2006 – 2008 savings of $5.958 Million

Client Quotes

“Blue Sky’s software systems, processes and controls provide the assurance that we are in total control of our global lease portfolio. Lease vs. purchase analysis is one of the most critical elements in our leasing processes and Blue Sky’s expertise in this area is invaluable. With Blue Sky’s best practices and negotiations we have realized over $1 million in savings over hundreds of lease originations and terminations. We now have years of valuable data points on leasing and a centralized data repository to efficiently make decisions on equipment leasing. “

Peter RapinTreasurer, Tax & Risk Management

“ Blue Sky has consistently delivered the most cost effective lease financing options available. Despite challenging credit conditions, Blue Sky has been able to identify and deliver cost-effective lease financing and expand our access to incremental liquidity. It’s the most comprehensive, “turn key” set of lease management services and tools I’ve worked with. I’d recommend Blue Sky’s Lease Management Services to any CFO or Treasurer who are interested in processes, controls and proactive portfolio management to realize the benefits of equipment leasing. “

Kevin K. JoyceDirector, Treasury