31

Benjamin Leavenworth Honorary Consul of Chile Federal Reserve Bank of Philadelphia September 18, 2009 Chile’s economic and trade policies 0

| Date post: | 28-Mar-2016 |

| Category: |

Documents |

| Upload: | global-interdependence-center |

| View: | 217 times |

| Download: | 5 times |

Benjamin LeavenworthHonorary Consul of Chile

Federal Reserve Bank of PhiladelphiaSeptember 18, 2009

Chile’s economic and trade policies

0

HAPPY BIRTHDAY199 YEARS TODAY!!

Chile: Location

2

Chile: Shape

3

Chile: Diversity

4

5Sources: World Bank, EIU, IMF, INE,, Central Bank of Chile

Chile - Basic Data 2008Population: 16.6 M

Urban Population 85.6%Annual rate of growth 1.2%Literacy rate 96.3%

Area 290,000sq.miles

GDP (2008) US$ 169,57 BGDP Growth (2008) 3.2%GDP average 1990/2008 5.36%GDP per capita (nominal/2008) US$10,814GDP per capita(PPP-2008) US$14,688

Annual inflation (2008) 7.1%July -0,4%Inflation accumulated 2009 -1,2%

Unemployment 2008 average 7.8% 2009 average April/June 10.7%

Fiscal surplus 2008 as % of GDP 5.2% (US$8.8 B)

Average annual GDP growth 1990 – 2008Selected economies (%)

Source: International Monetary Fund, IMF (www.imf.org)6

Source: Institute for Management Development (www.imd.ch)8

Source: World Economic Forum (www.weforum.org)9

Index of Economic Freedom - 2009

Source: Index of Economic Freedom 2009, The Heritage Foundation

(1)(6)

(11)(19)

(25)

(40)(49)

(64)

(132)(138)

(105)

10

Corruption perception index

• 1 Denmark 9,4• 1 Finland 9,4• 1 New Zealand 9,4• 4 Singapore 9,3• 4 Sweden 9,3• 6 Iceland 9,2• 7 Netherlands 9,0• 7 Switzerland 9,0• 9 Canada 8,7• 9 Norway 8,7• 11 Australia 8,6• 12 Luxembourg 8,4• 12 United Kingdom 8,4• 14 Hong Kong 8,3

• 15 Austria 8,1• 16 Germany 7,8• 17 Ireland 7,5• 17 Japan 7,5• 19 France 7,3• 20 USA 7,2• 21 Belgium 7,1• 22 Chile 7,0• 25 Uruguay 6,7• 46 Costa Rica 5,0• 61 Cuba 4,2• 68 Colombia 3,8• 72 Brazil 3,5• 72 Mexico 3,5• 72 Peru 3,5

Source: Transparency International(www.transparency.org), 2007

11

Chile: Poverty and Indigence(Percentage of total population)

38.6

32.9

27.623.2 21.7 20.2 18.7

13.7139 7.6 5.8 5.8 5.6 4.7 3.2

0

10

20

30

40

50

1990 1992 1994 1996 1998 2000 2003 2006Years

%

PovertyIndigence

Source : Ministry of Planning, CASEN survey12

Development Strategy

Economic reforms

Liberalization of prices and markets

Privatization of public enterprises

Consensus on key role of private sector in the productive process

Openness to foreign Investments

Low external tariffs: (Nominal : 6%, Global Effective: 0.4%, US Effective: 0,1%)

Government policies focused on:

Maintaining stable, clear and non discriminatory rules

Reducing poverty

Preserving macroeconomic stability

13

Sound and consistent Macroeconomic Policies

Monetary policy based on inflation targeting framework aimed at keeping annual inflation at 3 % on average within a policy period of two years, with a tolerance range of +/- 1%. Independent Central Bank.

Flexible exchange rate.

Strict fiscal discipline. Rule of structural fiscal surplus of 0.5 % of GDP.

14

Foreign Investment as engine for growth

Chile welcomes foreign investments as they are a very important component of the economic model. Key role in underpinning Chile’s growth.

Chile needs to bring in investments to increase the accumulation of capital, expand economic activity, generate employment and to receive transfers of new technologies.

Political and economic stability, as well as a friendly and neutral foreign investment regime, have attracted large inflows of FDI since 1990.

From 1974 Chile has received US$ 65 billion as FDI. About 87 % of the total arrived since 1990.

15

1974-2008 Share (%) 2004-2008 Share (%)

USA 16,860 24.43 1,234 7.31

Spain 14,342 20.78 4,586 31.97

Canada 12,755 18.48 4,631 36.30

UK 5,667 8.21 4,596 8.11

Australia 3,069 4.45 834 27.17

Japan 2,239 3.24 517 23.09

Others 14,093 20.42 3,036 21.54

Total 69,023 100 15,297 100

FDI in Chile by Countries of Origin

Source: Foreign Investment Committee

Million dollars

16

Chile: Importance of Trade

As Chile has a relatively small economy it was decided more than three decades ago to open it to international trade. Model of an open economy and foreign trade oriented.

Chile is highly dependent on foreign trade: exports plus importsof goods represents approximately 74 % of GDP in 2008.

Foreign trade is an essential component of its strategy of economic development (economic growth, employment and reduction of poverty).

17

Chile: Trade Policy

Active policy of trade liberalization through three different channels:

Unilateral liberalization (1975-2002): Chile reduced unilaterally its trade tariffs and today has a flat tariff of 6 %. Effective tariff of 0.4 %.

Multilateral level: Chile participates actively at the WTO and supports a world trade system governed by fair, transparent and non discriminatory rules.

Bilateral and regional agreements: Very active policy of FTA negotiations since 90’s. These agreements grant preferential access to markets of special interest and ensure a framework of stability.

18

Chile has preferential access to a market of 4 billion peoplein 56 countries

United StatesUnited States

Central America:Central America:

‐‐ Costa RicaCosta Rica

‐‐ El Salvador El Salvador

‐‐ HondurasHonduras

CanadaCanada

PanamaPanama

CubaCuba

EU (25 members)EU (25 members)

VenezuelaVenezuela

MERCOSUR:MERCOSUR:

BrazilBrazil

UruguayUruguay

ParaguayParaguay

ArgentinaArgentina

ColombiaColombia

EcuadorEcuador

PeruPeru

SingaporeSingapore

EFTA:EFTA:

JapanJapan

ChinaChina

IndiaIndia

Brunei DarussalamBrunei Darussalam

Source: Ministry of Foreign Affairs of ChileSource: Ministry of Foreign Affairs of Chile

New ZealandNew Zealand

P4:P4:

AustraliaAustralia

SwitzerlandSwitzerlandNorway Norway

LiechtensteinLiechtenstein

IcelandIceland

In forceIn force

TurkeTurkeyy

GuatemalGuatemalaa

MexicoMexico

SignedSigned

MalaysiaMalaysia

VietnamVietnam

RussiaRussia

Under negotiation:Under negotiation:(Vietnam, (Vietnam, MalaysiaMalaysia, , ThailandThailand))

ThailandThailand

19

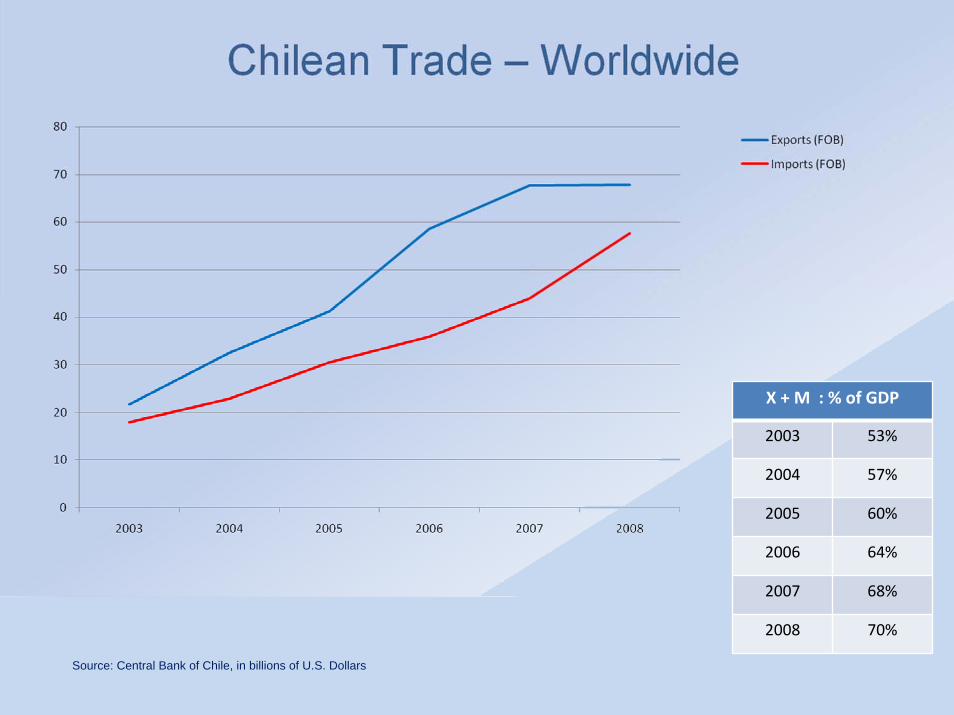

Source: Central Bank of Chile, in billions of U.S. Dollars

X + M : % of GDP

2003 53%

2004 57%

2005 60%

2006 64%

2007 68%

2008 70%

Source: Central Bank of Chile, in millions of U.S. Dollars

21

Historical Market Participation(average 2000-2008)

Source: Central Bank of Chile

Pre-Crisis Situation

• Fiscal regulations1. Fiscal savings: we are net creditors2. Sovereign funds: we accumulated 28% of GDP over a five-yearperiod3. Fiscal responsibility rule: stabilizes future social spending and public investments

• Accumulation of International Reserves1. US$24 billion, double the reserves accumulated five years ago

• Flexible exchange rate1. It adjusts to external shocks

• Inflation targets1. Help to stabilize the cycle and minimize the costs of maintaining low and stable inflation (credibility)

• Bank supervision1. Preventative supervision that includes the evaluation of financial institution management and solvency

23

To a large extent, we have been able to amortize external shocks thanks to our expansive macroeconomic policies

• Timely reaction to liquidity problems in late 20081. Central Bank2. Government

• Fiscal policy:1. Fiscal packet2. Pro- credit Initiative3. Pro-employment Accord4. May 21st announcements

• Monetary policy:Aggressive reduction of the Central Bank’s interest rate

24

Chile and The United States

Free Trade Agreement

January 1, 2004

25

Source: Central Bank of Chile, in millions of U.S. Dollars 26

Main Exports to the US (2008)

Source : Central Bank of Chile

* Share of total copper exports to the world: 55.9%

PPrroodduuccttss mm.. $$ %% Copper and articles 2.781 37.50*

Salmon 792 10.1

Gold 427 5.5

Grapes 349 4.5 Wood and articles of

wood 243 3.1

Wines 199 2.6

Iod 128 1.6

Blueberries 104 1.3

Molybdenum 96 1.2

Fresh Cherries 63 0.8

Avocados 61.2 0.8

27

Main Imports from the US (2008)

Source : Central Bank of Chile

PPrroodduuccttss mm.. $$ %% Mineral Fuel, Oil, etc 3.673 33.6

Vehicles and tractors 545 5

Polyethylen 157 1.4

Wheat 150 1.4

Vehicles 97 0.9

Sodium Hydroxide (caustic soda) 80 0.7

28

Trade facts

• 2007 Chile with only 16 million inhabitants, imported more US goods than big countries like:

- Russia and Pakistan (150 million each) or Indonesia (240 million) - Egypt and Turkey (more than 50 million each) - Colombia (over 40 million) and Argentina (almost 40 million), etc.

• 10% of Chile’s trade with the U.S. goes through the Tri-State region: approx 1 billion.

• Several thousand jobs generated locally.

Conclusion: Free Trade has worked for Chile!!

![The Leavenworth echo (Seattle, Wash) 1904-06-17 [p ]chroniclingamerica.loc.gov/lccn/sn87093039/1904-06-17/ed-1/seq-1.pdfVol. I. No. 22. Leavenworth, Wash., Friday, June 17, 1904. LEAVENWORTH](https://static.documents.pub/doc/80x56/5caaa65688c993135e8c13a6/the-leavenworth-echo-seattle-wash-1904-06-17-p-i-no-22-leavenworth-wash.jpg)