14

LEBANESE SME FORUM ACCESS TO FINANCE GAPS AND RECOMMENDATIONS Beirut, Lebanon July 11, 2017

LEBANESE SME FORUM

ACCESS TO FINANCE

GAPS AND RECOMMENDATIONS

Beirut, Lebanon

July 11, 2017

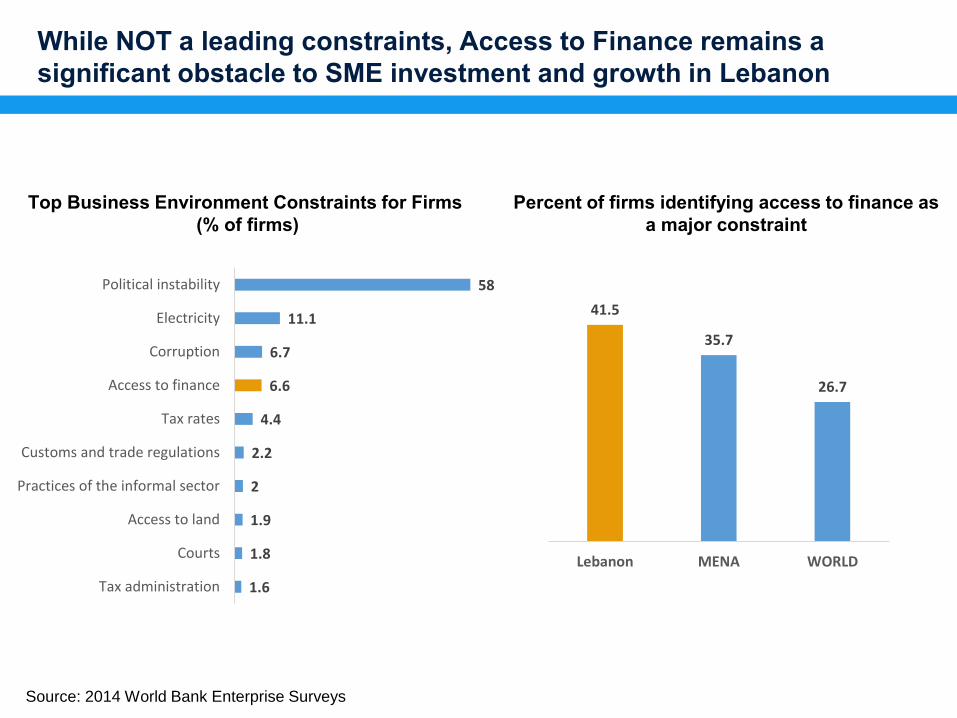

While NOT a leading constraints, Access to Finance remains a

significant obstacle to SME investment and growth in Lebanon

58

11.1

6.7

6.6

4.4

2.2

2

1.9

1.8

1.6

Political instability

Electricity

Corruption

Access to finance

Tax rates

Customs and trade regulations

Practices of the informal sector

Access to land

Courts

Tax administration

41.5

35.7

26.7

Lebanon MENA WORLD

Source: 2014 World Bank Enterprise Surveys

Top Business Environment Constraints for Firms

(% of firms)

Percent of firms identifying access to finance as

a major constraint

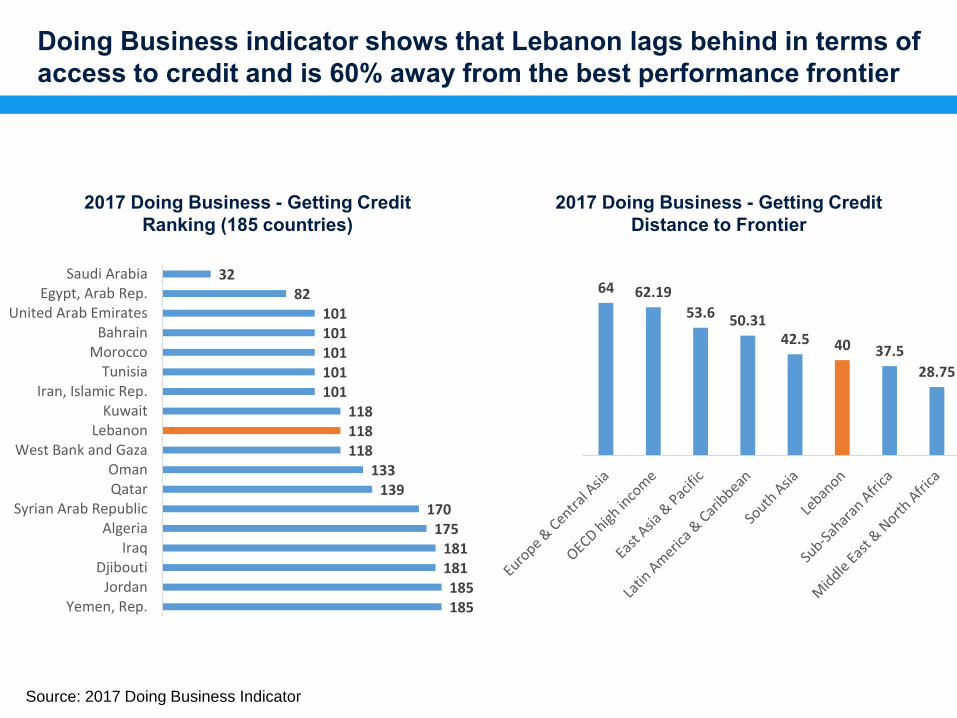

64 62.19

53.6 50.31 42.5 40 37.5

28.75

Source: 2017 Doing Business Indicator

185 185

181 181

175 170

139 133

118 118 118

101 101 101 101 101

82 32

Yemen, Rep.Jordan

DjiboutiIraq

AlgeriaSyrian Arab Republic

QatarOman

West Bank and GazaLebanon

KuwaitIran, Islamic Rep.

TunisiaMorocco

BahrainUnited Arab Emirates

Egypt, Arab Rep.Saudi Arabia

2017 Doing Business - Getting Credit

Ranking (185 countries)

2017 Doing Business - Getting Credit

Distance to Frontier

Doing Business indicator shows that Lebanon lags behind in terms of

access to credit and is 60% away from the best performance frontier

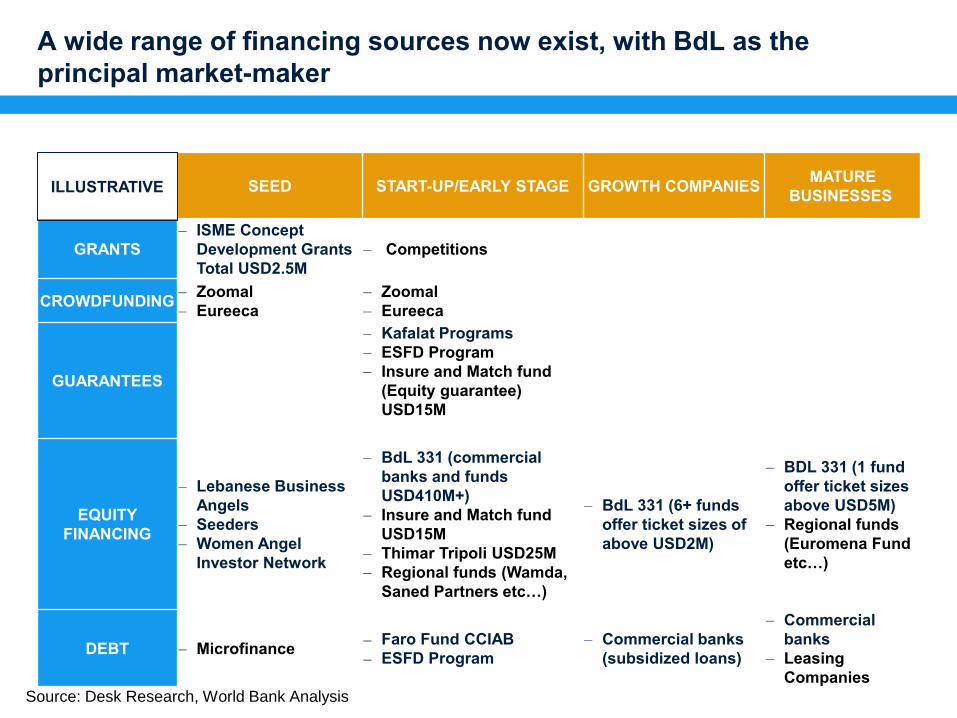

A wide range of financing sources now exist, with BdL as the

principal market-maker

Source: Desk Research, World Bank Analysis

SEED START-UP/EARLY STAGE GROWTH COMPANIES MATURE

BUSINESSES

GRANTS

– ISME Concept

Development Grants

Total USD2.5M

– Competitions

CROWDFUNDING – Zoomal

– Eureeca

– Zoomal

– Eureeca

GUARANTEES

– Kafalat Programs

– ESFD Program

– Insure and Match fund

(Equity guarantee)

USD15M

EQUITY

FINANCING

– Lebanese Business

Angels

– Seeders

– Women Angel

Investor Network

– BdL 331 (commercial

banks and funds

USD410M+)

– Insure and Match fund

USD15M

– Thimar Tripoli USD25M

– Regional funds (Wamda,

Saned Partners etc…)

– BdL 331 (6+ funds

offer ticket sizes of

above USD2M)

– BDL 331 (1 fund

offer ticket sizes

above USD5M)

– Regional funds

(Euromena Fund

etc…)

DEBT – Microfinance Faro Fund CCIAB

ESFD Program

– Commercial banks

(subsidized loans)

– Commercial

banks

– Leasing

Companies

ILLUSTRATIVE

Evolution of VC Landscape in Lebanon

(per year of establishment and fund size)

Figure does not include funds that stopped operating: BBF Fund in 2006 and Lebanon Growth Capital Fund in 2011. It also does not include Angel Funding: LBA - Business Angels in 2009, Seeders in 2016. It does not include funding made available by accelerators such as SPEED. Source: Funds Websites, World Bank analysis

0

10

20

30

40

50

60

70

80

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Year of Establishment

Fund Size (in USD M)

Berytech

Fund I

MEVP

Fund I BBEF

Fund

iSME

Fund

MEVP

Fund II

Berytech

Fund II

Leap Ventures

Fund IMPACT Fund

by MEVP

IM Capital

Azure Fund

Phoenician

Fund Theemar

Capital

Saned

Cedar Mundi

B&Y Ventures

This is particularly evident when looking at the evolution of the Venture

Capital landscape with 12 new funds with a total value of ~USD 410 …

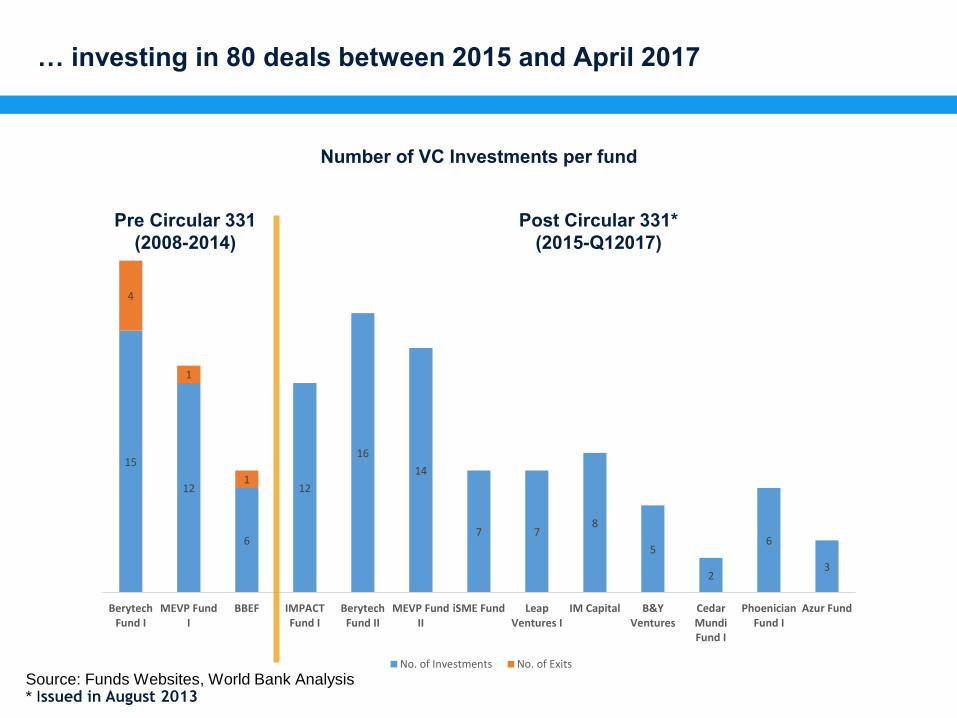

… investing in 80 deals between 2015 and April 2017

15

12

6

12

16

14

7 7 8

5

2

6

3

4

1

1

BerytechFund I

MEVP FundI

BBEF IMPACTFund I

BerytechFund II

MEVP FundII

iSME Fund LeapVentures I

IM Capital B&YVentures

CedarMundiFund I

PhoenicianFund I

Azur Fund

No. of Investments No. of Exits

Pre Circular 331

(2008-2014)

Post Circular 331*

(2015-Q12017)

Number of VC Investments per fund

Source: Funds Websites, World Bank Analysis * Issued in August 2013

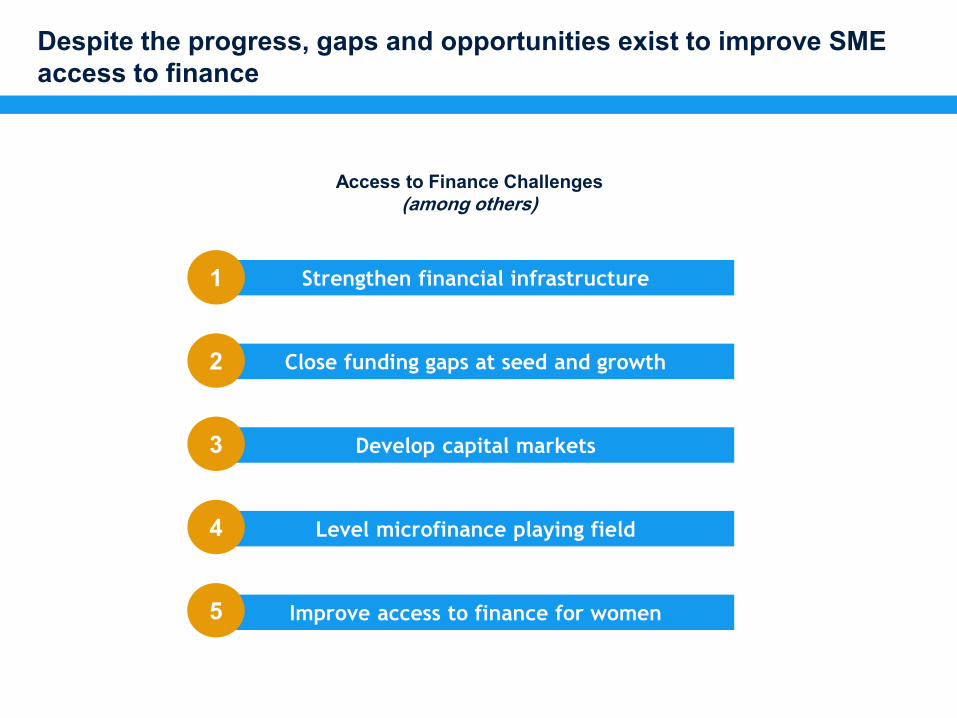

Despite the progress, gaps and opportunities exist to improve SME

access to finance

Strengthen financial infrastructure

Close funding gaps at seed and growth

Develop capital markets

Level microfinance playing field

Improve access to finance for women

Access to Finance Challenges

(among others)

1

2

3

4

5

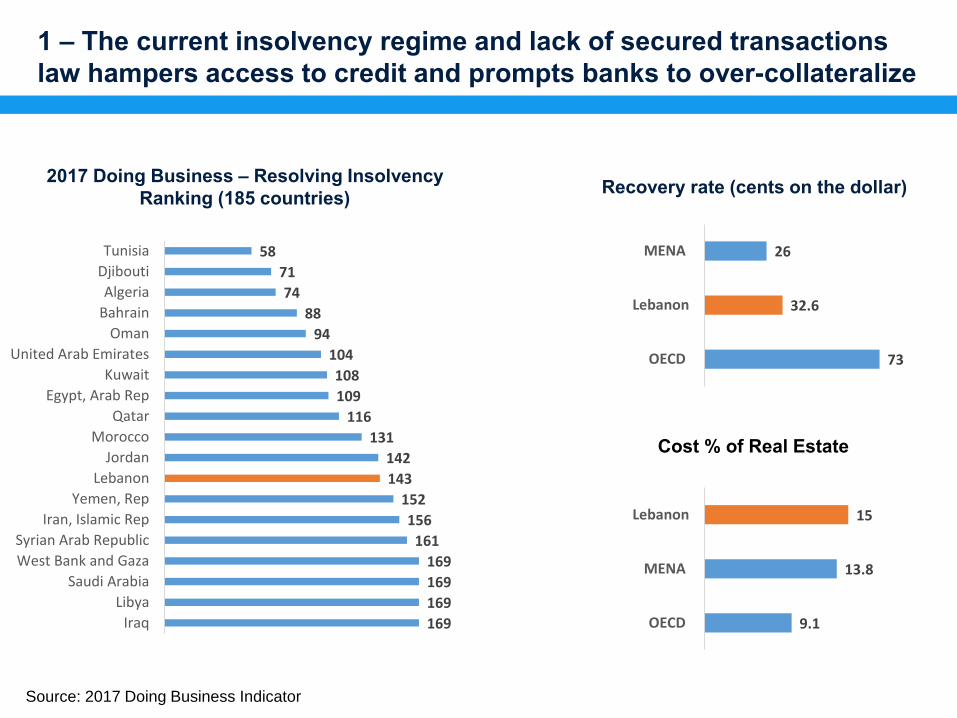

1 – The current insolvency regime and lack of secured transactions

law hampers access to credit and prompts banks to over-collateralize

2017 Doing Business – Resolving Insolvency

Ranking (185 countries) Recovery rate (cents on the dollar)

169

169

169

169

161

156

152

143

142

131

116

109

108

104

94

88

74

71

58

Iraq

Libya

Saudi Arabia

West Bank and Gaza

Syrian Arab Republic

Iran, Islamic Rep

Yemen, Rep

Lebanon

Jordan

Morocco

Qatar

Egypt, Arab Rep

Kuwait

United Arab Emirates

Oman

Bahrain

Algeria

Djibouti

Tunisia

73

32.6

26

OECD

Lebanon

MENA

9.1

13.8

15

OECD

MENA

Lebanon

Cost % of Real Estate

Source: 2017 Doing Business Indicator

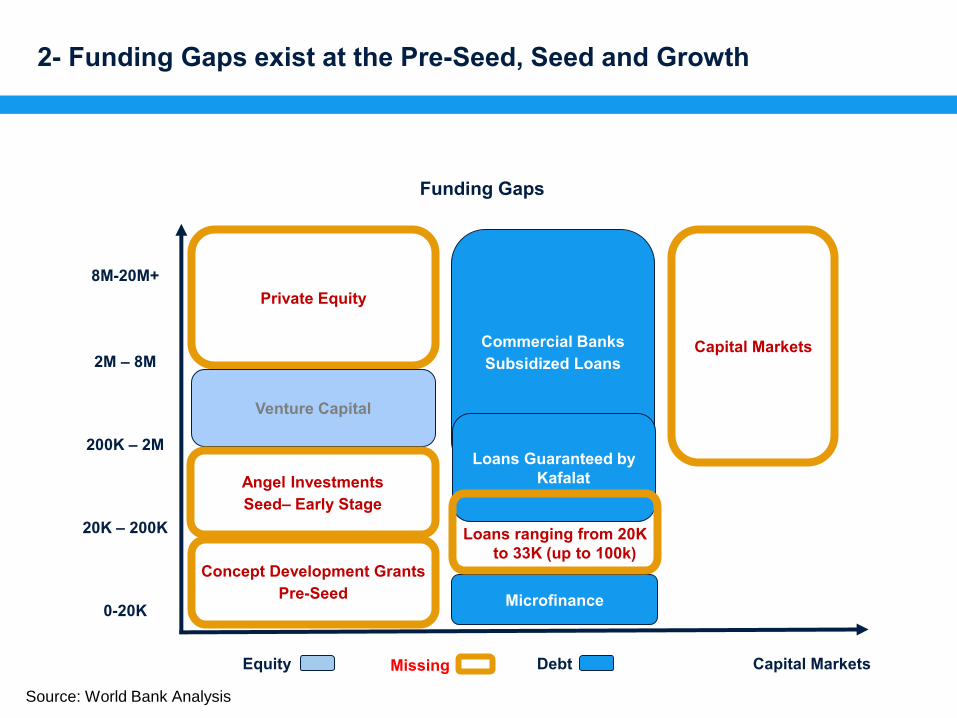

2- Funding Gaps exist at the Pre-Seed, Seed and Growth

Source: World Bank Analysis

0-20K

8M-20M+

20K – 200K

200K – 2M

2M – 8M

Commercial Banks

Subsidized Loans

Private Equity

Concept Development Grants

Pre-Seed

Venture Capital

Loans Guaranteed by

Kafalat

Microfinance

Angel Investments

Seed– Early Stage

Capital Markets

Loans ranging from 20K

to 33K (up to 100k)

Debt Equity Capital Markets Missing

Funding Gaps

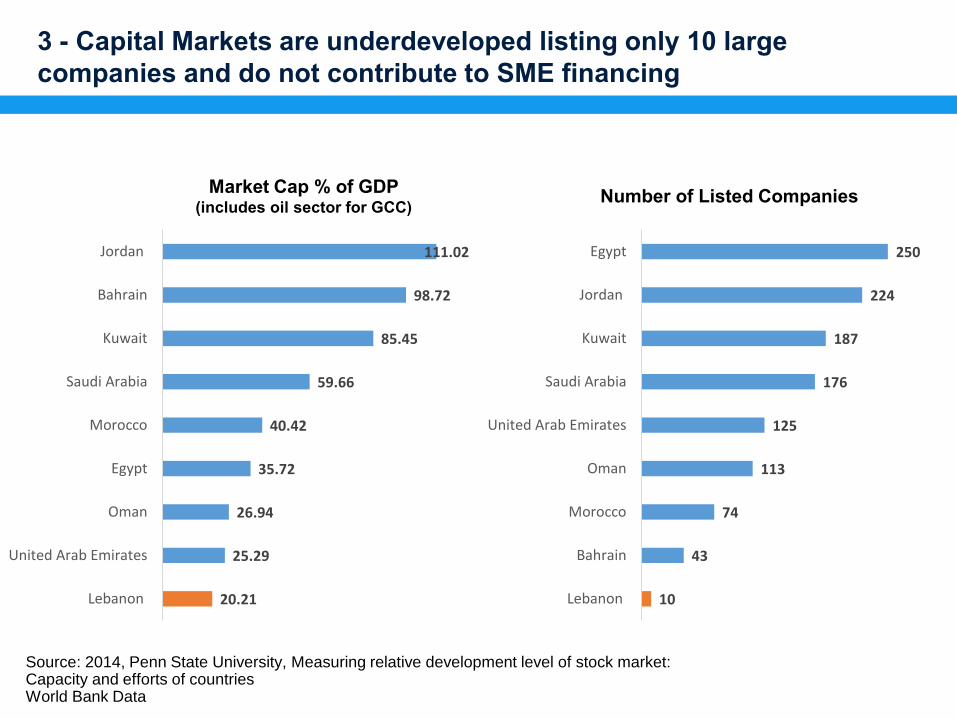

3 - Capital Markets are underdeveloped listing only 10 large

companies and do not contribute to SME financing

Source: 2014, Penn State University, Measuring relative development level of stock market: Capacity and efforts of countries World Bank Data

20.21

25.29

26.94

35.72

40.42

59.66

85.45

98.72

111.02

Lebanon

United Arab Emirates

Oman

Egypt

Morocco

Saudi Arabia

Kuwait

Bahrain

Jordan

Market Cap % of GDP (includes oil sector for GCC)

10

43

74

113

125

176

187

224

250

Lebanon

Bahrain

Morocco

Oman

United Arab Emirates

Saudi Arabia

Kuwait

Jordan

Egypt

Number of Listed Companies

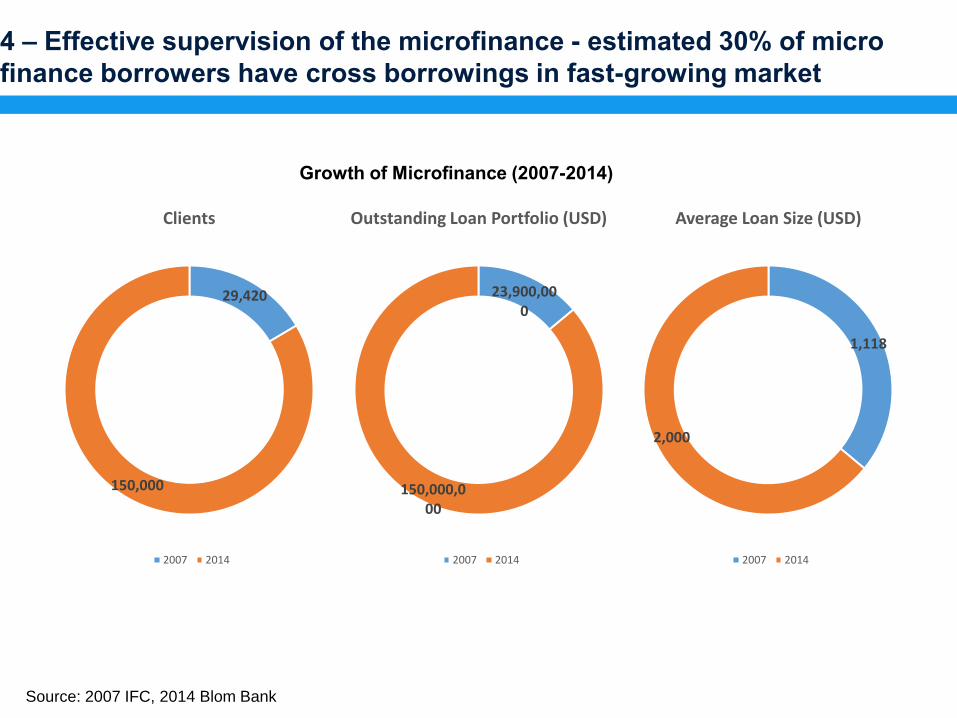

4 – Effective supervision of the microfinance - estimated 30% of micro

finance borrowers have cross borrowings in fast-growing market

Source: 2007 IFC, 2014 Blom Bank

29,420

150,000

Clients

2007 2014

23,900,00

0

150,000,0

00

Outstanding Loan Portfolio (USD)

2007 2014

1,118

2,000

Average Loan Size (USD)

2007 2014

Growth of Microfinance (2007-2014)

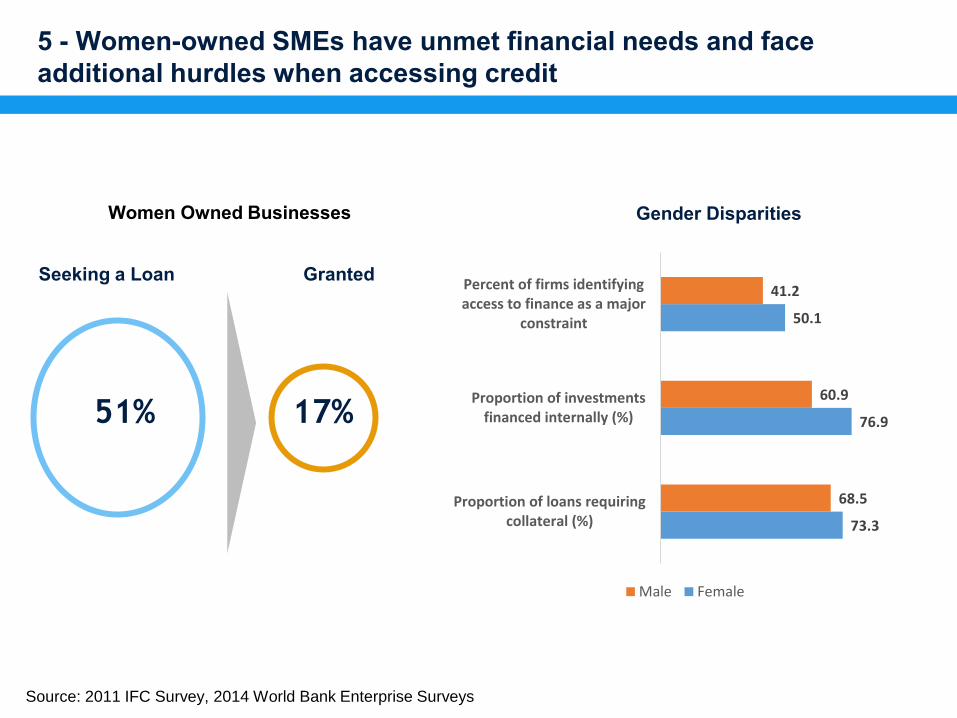

5 - Women-owned SMEs have unmet financial needs and face

additional hurdles when accessing credit

17% 51%

Seeking a Loan Granted

Source: 2011 IFC Survey, 2014 World Bank Enterprise Surveys

Women Owned Businesses Gender Disparities

73.3

76.9

50.1

68.5

60.9

41.2

Proportion of loans requiringcollateral (%)

Proportion of investmentsfinanced internally (%)

Percent of firms identifyingaccess to finance as a major

constraint

Male Female

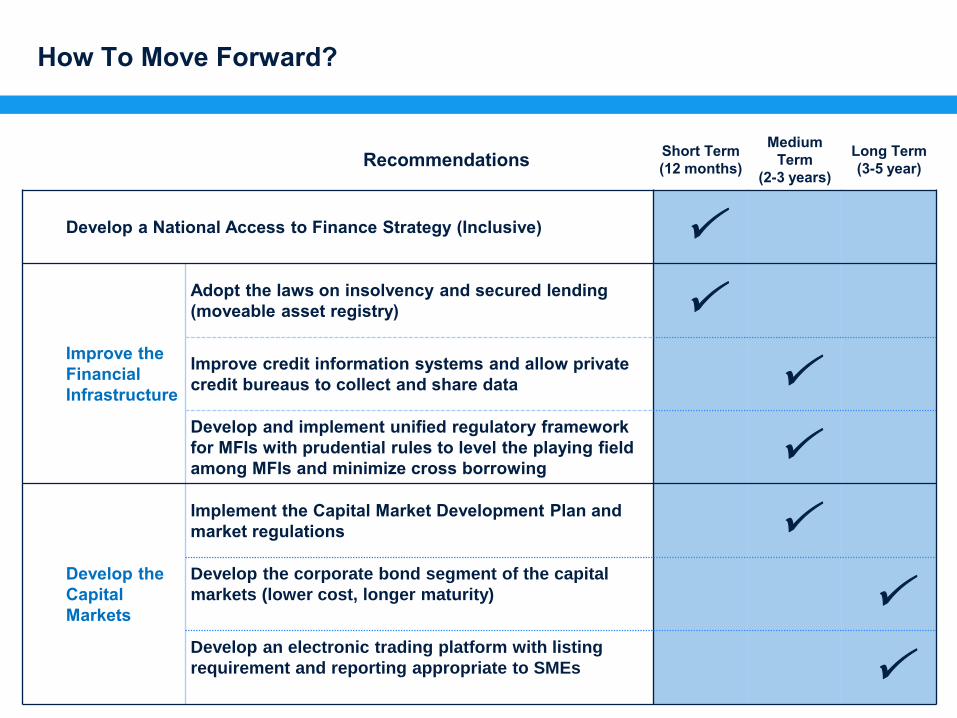

How To Move Forward?

Recommendations Short Term

(12 months)

Medium

Term

(2-3 years)

Long Term

(3-5 year)

Develop a National Access to Finance Strategy (Inclusive)

Improve the

Financial

Infrastructure

Adopt the laws on insolvency and secured lending

(moveable asset registry) Improve credit information systems and allow private

credit bureaus to collect and share data Develop and implement unified regulatory framework

for MFIs with prudential rules to level the playing field

among MFIs and minimize cross borrowing

Develop the

Capital

Markets

Implement the Capital Market Development Plan and

market regulations Develop the corporate bond segment of the capital

markets (lower cost, longer maturity)

Develop an electronic trading platform with listing

requirement and reporting appropriate to SMEs

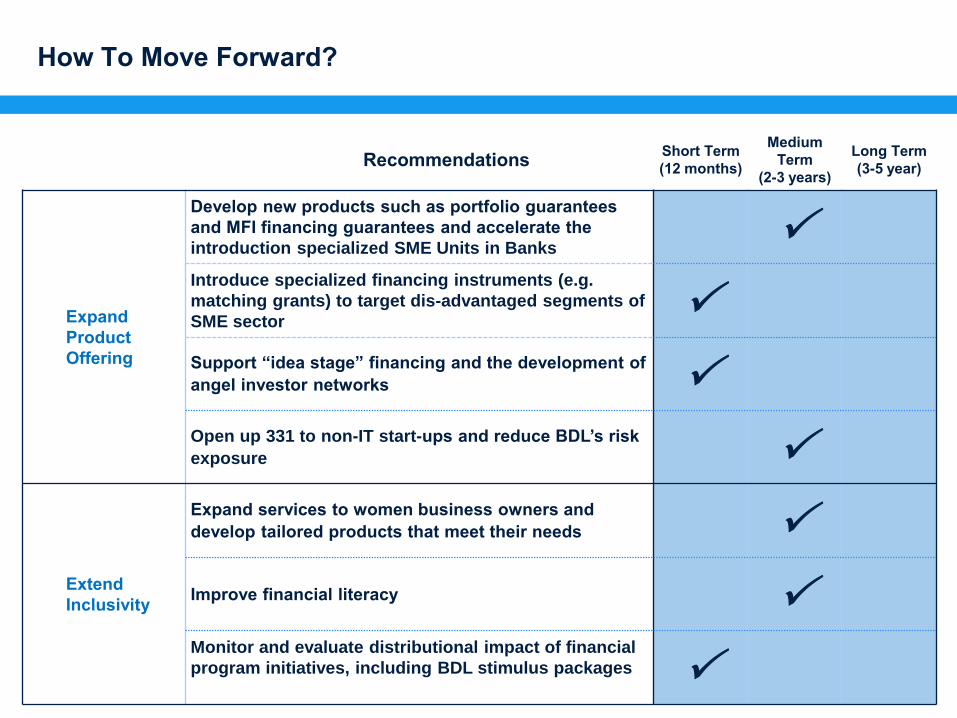

How To Move Forward?

Recommendations Short Term

(12 months)

Medium

Term

(2-3 years)

Long Term

(3-5 year)

Expand

Product

Offering

Develop new products such as portfolio guarantees

and MFI financing guarantees and accelerate the

introduction specialized SME Units in Banks

Introduce specialized financing instruments (e.g.

matching grants) to target dis-advantaged segments of

SME sector

Support “idea stage” financing and the development of

angel investor networks Open up 331 to non-IT start-ups and reduce BDL’s risk

exposure

Extend

Inclusivity

Expand services to women business owners and

develop tailored products that meet their needs

Improve financial literacy Monitor and evaluate distributional impact of financial

program initiatives, including BDL stimulus packages