82

Lebanon: Integrated Assessment of the Association Agreement with the EU With a focus on the olive oil sector

Lebanon: Integrated Assessment

of the Association Agreement

with the EU

With a focus on the olive oil sector

�

Preface

With greater implementation of trade liberlization agreements throughout the world, the interlinked issues of Trade, Environment and Poverty have become increasingly important for all countries, especially developing ones. Policies to reduce the negative impact of trade liberlization on specific groups and the environment are being developed throughout the world. Lebanon too is exploring new ways to ensure that trade liberlization does play key roles in enhancing the standard of living in rural areas and promoting environmentally friendly production practices.

In June 2002, Lebanon signed the EU-Lebanon Association Agreement (AA) and, in December the Agreement was ratified by the Lebanese Parliament. The objectives of the AA were to provide an appropriate framework for political dialogue between the parties; establish the conditions for the gradual liberalization of trade in goods, services, and capital; and promote economic, social, cultural, financial and monetary cooperation.1 An Interim Agreement entered into force in March 2003 allowing for immediate implementation of the economic and trade-related provisions of the AA while awaiting parliamentary ratification from all EU member states. The AA was then selected for integrated assessment because it remains a comprehensive agreement and all the studies conducted so far for it have assessed only its economic impacts but omitted social and environmental characteristics or probable inter-linkages between all three impact areas.

The study focuses on the olive oil subsector due to its importance for poverty reduction, employment creation, migration, trade, growth potential, the rural landscape, environmental implications such as waste generation and disposal, and because of willingness of stakeholders to provide necessary information and data. In 2002, the economic value of olive farming was estimated at US$176 million, or approximately 20 per cent of the value of Lebanese agricultural plant production (SRI, 2004). The assessment team surveyed procedures and agents involved in olive oil production in Lebanon (from farming to milling to marketing), determined baseline scenarios and areas of concern, and identified action plans to help the subsector reap all the benefits of the AA.

A number of major policies and projects are related to the current study and were consulted. These include the Strategic Environmental Assessment Project of the Ministry of Environment conducted in 2005, the World Bank country assessment strategy outlined in 1997, and the various programmes under the Association Agreement such as the quality project and the Small and Medium Enterprise (SME) project. Furthermore, a large number of pilot projects targeting the olive oil sector have also been carried out, including a study for the Ministry of Industry entitled “The Impact of the Euro-Mediterranean Agreement on the Olive Oil Industry in Lebanon” (Mirza, 2004).

1 Article 1 of the AA

��

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

The report is divided in five chapters, the first of which introduces the report and project in general. Chapter 2 briefly assesses the Lebanese socio-economic and political situation, and specifically focuses on agriculture and the olive oil sector.

Chapter 3 reviews trade liberlization policies and agreements between Lebanon and the EU as well as agreements with other countries or organizations. Chapter 4 presents the integrated assessment, forming two alternative scenarios: a baseline scenario where Lebanon does not take full advantage of the increased quota of 1,000 tonnes of olive oil to be exported duty free to the EU, and a second scenario where all necessary quality improvements are undertaken enabling these 1000 tonnes to be exported. Chapter 5 draws conclusions, makes recommendations and identifies a necessary action plan to improve the sector’s performance and increase readiness for more trade.

���

Acronyms and abbrev�at�ons

AA Association Agreement

ADP Agriculture Development Project

BOD Biological oxygen demand

CAC Codex Alimentarius Commission

CAS Central Administration of Statistics

CBA Cost benefit analysis

CBTF Capacity Building Task Force

CCIAB Chamber of Commerce, Industry, and Agriculture of Beirut and Mount Lebanon

CCT Common Customs Tariffs

CITES Convention on International Trade in Endangered Species

COD Carbon oxygen demand

DTIE Division of Technology, Industry and Economics

EC European Commission

EFTA European Free Trade Agreement

EIB European Investment Bank

ELARD Earth Link and Advanced Resources Development

ELCIM Euro-Lebanese Centre for Industrial Modernization

ENI European Neighbourhood Instrument

ENP European Neighbourhood Policy

ESCWA Economic and Social Commission for Western Asia

ESE Economic, social and environmental

ESFD Economic and Social Fund for Development

ETB Economics and Trade Branch

EU European Union

FAO Food and Agriculture Organization

FTA Free trade agreement

GAFTA Greater Arab Free Trade Area

GAP Good agricultural practices

GDP Gross Domestic Product

GHG Greenhouse gas

GMO Genetically modified organism

�v

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

GMP Good Manufacturing Practices

GOL Government of Lebanon

HACCP Hazard Analysis and Critical Control Point

IA Integrated assessment

IAP Integrated assessment project

ICU Intituto per la Cooperazione Universitaria

IOOC International Oliver Oil Council

IPM Integrated Pest Management

ISO International Organization for Standardization

LCI Living Condition Index

LCPS Lebanese Centre for Policy Studies

LIPSOS Lebanese Inter-Professional Syndicate for the Olive Sector

LOOO Lebanese Olive Oil Office

MDG Millennium Development goals

MEAs Multilateral Environmental Agreements

MOA Ministry of Agriculture

MOE Ministry of Environment

MOET Ministry of Economy and Trade

MOI Ministry of Industry

MOSA Ministry of Social Affairs

MTA Multilateral trade agreement

NGO Non-governmental organization

ODS Ozone depleting substance

O&M Operation and maintenance

OMW Olive mill wastewater

PIC Prior informed consent

POPs Persistent Organic Pollutants

RAC/CP Regional Activity Centre for Cleaner Production

SBC Secretariat of the Basel Convention

SMAP Short and Medium-term Priority Environmental Action Programme

SME Small and Medium Enterprise

SOER State of the Environment Report

SRI Stanford Research Institute (SRI International)

UN United Nations

UNCTAD United Nations Conference on Trade and Development

UNDP United Nations Development Programme

UNEP United Nations Environment Programme

USAID United Nations Agency for International Development

WTO World Trade Organization

v

Execut�ve summary

This integrated assessment of the Lebanon-EU Association Agreement (AA), which focuses on the Lebanese olive oil sector, is an all-embracing project to assess the socio-economic and environmental implications of opening up local subsectors to freer trade. The assessment was initiated in December 2004 and was headed by Lebanon’s Ministry of Economy and Trade (MOET) in collaboration with the Ministry of Environment (MOE), and with the technical assistance of the United Nations Environment Programme (UNEP). The project focused on the olive oil sector because of the important role it plays in the Lebanese economy, local communities and the environment.

The project aims to identify national priorities and outline action plans for Lebanon in line with European Neighbourhood Policy (ENP) guidelines. The report is targeted at policymakers and advocates (public sector bodies, private stakeholders, syndicates, cooperatives and NGOs) and aims to raise awareness of the importance of taking a more integrated approach to the design of trade policies. It therefore introduces a methodology and a framework to be used in planning, implementation and monitoring. The study illustrates how the IAP approach has been adapted to the Lebanese context but can be used in other sectors or planning processes.

The assessment process used scenario building to project the impacts (economic, social and environmental) of exporting the full quota of olive oil allowed under the EU-Lebanon Agreement and compared it to a “business as usual” baseline. Two scenarios were defined as follows: Scenario 1 accepted the state of the olive oil sector as it were, without policy measures to encourage increased duty-free exports to the EU; and Scenario 2 assumed that needed olive oil quality improvements were made in Lebanon to take full advantage of the 1,000-tonne quota, once farmers and millers are shown the benefits of the improvements. Quantitative analysis in the form of a “rapid” cost-benefit analysis was undertaken to assess the economic issues.

The findings clearly indicate that most Lebanese olive oil growers were not taking advantage of the duty-free export quota and that a range of necessary measures are urgently needed to achieve the benefits of the AA. In line with the Steering Committee recommendations, a list of priority action plans to enhance the quality of Lebanese olive oil and achieve the benefits of Scenario 2 is provided here. These action plans will need to be implemented to strengthen the sector before undertaking any further trade liberalization negotiations. The plans fall mainly within the scope of a sustainable regulatory framework that will create the incentive to produce extra-virgin olive oil by upgrading mill operations and promoting better agricultural practices.

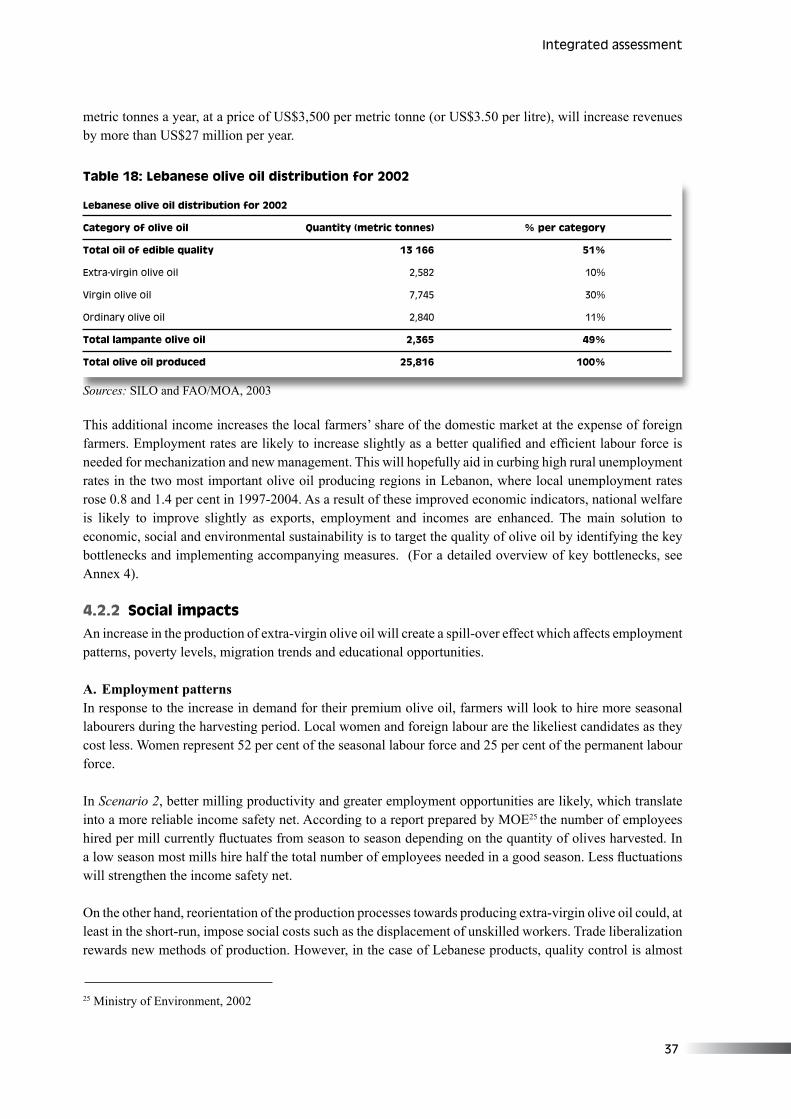

The study also shows that the economic benefits of applying the requirements for Scenario 2 are truly substantial when considering the full implications of producing extra-virgin olive oil, above and beyond fulfilling the quota. The increase in revenues from bigger exports is perhaps insignificant in absolute terms, but when compared to revenues under Scenario 1, it is relatively considerable, reaching up to 23.8 times (US$3,500,000 projected compared to 2004’s actual revenue of US$147,000).

v�

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Recommendations to improve the olive oil sector are drawn upon the identification of key bottlenecks and the views of the Steering Committee. They consist of different complementary measures to implement the action plans and successfully push reform of the sector by the EU, the Lebanese Government, the private sector and NGOs. These measures are partly in the form of continuing technical and financial assistance from the EU within the framework of the European Neighbourhood Policy (ENP), which is a commitment to enforce stakeholders’ commitment to a public-private partnership. Trade regulations such as quality standards, as well as duties and their gradual elimination, should also be communicated to all parties involved, as this ensures efficiency and lowers the incidence of rejected products. Furthermore, technical and non-trade barriers such as lengthy bureaucratic procedures should be revised and eliminated when unnecessary.

The Government of Lebanon should encourage each region in Lebanon to regionally brand its products as “unique” or “distinct” to better target niche markets (such as that of the Lebanese diaspora). The EU can encourage this endeavour by helping to create these geographic “lines” in Lebanon and also by financing the promotion of such products at European trade fairs and exhibitions. However, the major contribution should come from Lebanon’s relevant Ministries as well as the different municipalities and cooperatives concerned with olive oil production. Well within its prerogatives, the Government can create an enabling environment by improving inter-ministerial coordination. It should upgrade and certify existing testing laboratories, disseminate information to stakeholders, and build databases. It should also provide training for farmers and mill operators (such as training on good agricultural practices and good manufacturing practices), facilitate by-product management, and provide access to capital. For example, the treatment of vegetable water ought to be financed and implemented by the Government.

Centralizing decision-making on olive oil (by forming a National Olive Oil Office, for example) will go a long way in addressing all the concerns and priorities of the various stakeholders. A national policy (with respective action plans) can be formulated in which the various stakeholders are given specific responsibilities to improve the sector. The policy should be moving towards the production of better quality olive oil by decentralizing quality checks and enforcing necessary laws (on hygienic milling conditions and olive oil quality categorizing, for example).

The private sector will play a major role in achieving economies of scale, promoting fair competition, disseminating information and proposals, investing in newer technologies and production techniques, maintaining a competitive edge, coordinating with NGOs, and promoting the public-private partnership. Finally, NGOs should continue to work with the private sector to maintain efforts in raising awareness, training farmers, enhancing inter-NGO networking, disseminating information and facilitating public-private partnerships.

Lebanon’s olive oil sector is currently facing tremendous hardships in the form of high production costs, regional competition, sub-standard quality output which does not permit exports (including to Europe), and a lack of proper coordination and management by the main actors in the field. Such hardships exacerbate the already severe socio-economic concerns in the region like unemployment, poverty, a weakening quality of life and rural-urban migration. The findings of the assessment have stressed the need to strengthen the sector by implementing a number of key regulatory and policy improvements that bring the olive oil sector up to export quality standards. Many of the initiatives proposed will also have positive environmental implications and optimize the socio-economic benefits of the AA.

v��

Acknowledgements

This publication is based on the results from the Integrated Assessment and Planning (IAP) project implemented in Lebanon from January 2004. UNEP would like to begin by thanking all institutions and individuals who provided help throughout the duration of the project and also extend its deepest gratitude to the Ministry of Agriculture and the Ministry of Environment for their support and willingness to share and provide all the necessary information throughout the project.

UNEP would also like to acknowledge Joey Ghaleb, the Project Manager, for his devotion and efforts during the project, and Alissar Chaker, UNDP project manager at the Ministry of Environment and Makram Malaeb, Senior Policy Component Manager at the Ministry of Economy and Trade for all the valuable information and time they gave throughout the project.

Acknowledgements also go to individuals in the Ministry of Agriculture, particularly Myriam Eid, Agrofood production expert; Rania Bizreh at the Lebanese Chamber of Commerce; Sleiman Dagher, president of LIPSOS; Karim Hamoud, olive oil production expert at LIPSOS; Jose Antonio Villaverde, Resident Representative; Hussain Hoteit, agrofood engineer at the Instituto par la cooperazione Universitaria (ICU), and James Billing Director of the SRI in Lebanon.

UNEP also wishes to gratefully acknowledge all the people who shared ideas, time and opinions with the project team including Francisco Acosta Soto, European Union; Carol Chouchani Cherfane, ESCWA, and Lamia Chammas from the Ministry of Environment. UNEP also expresses its deepest appreciation to the millers and farmers involved in this project for their cooperation. UNEP thanks all the stakeholders for their active participation in the workshops.

An international group of experts provided important input to the project. UNEP would like to express its gratitude to members of this group: Jiri Dusik, Jan Joost Kessler, Barry Sadler and Salah el Serafy, for their time, effort, and advice, including comments on the draft version of this report.

UNEP also wishes to gratefully acknowledge the Norwegian Ministry of Foreign Affairs and the Government of the United States of America for their financial support, through the mechanism of UNEP-UNCTAD Capacity Building Task Force on Trade, Environment and Development (CBTF), which made the project in Lebanon possible. At UNEP, the project was initiated and under the overall supervision of Hussein Abaza. Maria Cecilia Pineda, Fulai Sheng and Asad Naqvi coordinated this project and provided technical support. Desiree Leon facilitated the processing of the report for editing and typesetting. Rahila Mughal provided administrative support for the project.

v���

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

UNEP’s appreciation also goes to Andrea Smith for editing the report and to Ho Hui Lin of iPublish Pte Ltd for providing editorial and typesetting services.

Notwithstanding the valuable contributions of many acknowledged here, the full responsibility for the content of this report remains with the authors.

�x

Un�ted Nat�ons Env�ronment Programme

The United Nations Environment Programme (UNEP) is the overall coordinating environmental organization of the United Nations system. Its mission is to provide leadership and encourage partnerships in caring for the environment, by inspiring, informing, and enabling nations and people to improve their quality of life without compromising that of future generations. In accordance with its mandate, UNEP works to observe, monitor, and assess the state of the global environment; improve the scientific understanding of how environmental change occurs; and in turn, determine how such change can be managed by action-oriented national policies and international agreements. UNEP’s capacity building work thus centres on helping countries strengthen environmental management in diverse areas, which include freshwater and land resource management; the conservation and sustainable use of biodiversity, marine and coastal ecosystem management; and cleaner industrial production and eco-efficiency, among many others.

UNEP, headquartered in Nairobi, Kenya, marked its first 30 years of service in 2002. During this time, in partnership with a global array of collaborating organizations, UNEP achieved major advances in the development of international environmental policy and law, environmental monitoring and assessment, and our understanding of the science of global change. This work also supports the successful development and implementation of the world’s major environmental conventions. In parallel, UNEP administers several multilateral environmental agreements (MEAs), including the Vienna Convention’s Montreal Protocol on Substances that Deplete the Ozone Layer, the Convention on International Trade in Endangered Species of Wild Fauna and Flora (CITES), the Basel Convention on the Control of Transboundary Movements of Hazardous Wastes and their Disposal (SBC), the Convention on Prior Informed Consent Procedure for Certain Hazardous Chemicals and Pesticides in International Trade (Rotterdam Convention, PIC), the Cartagena Protocol on Biosafety to the Convention on Biological Diversity, and the Stockholm Convention on Persistent Organic Pollutants (POPs).

Division of Technology, Industry and EconomicsThe mission of the Division of Technology, Industry and Economics (DTIE) is to encourage decision makers in government, local authorities and industry to develop and adopt policies, strategies, and practices that are cleaner and safer, make efficient use of natural resources, ensure environmentally sound management of chemicals, and reduce pollution and risks for humans and the environment. In addition, it seeks to enable implementation of conventions and international agreements and encourage the internalization of environmental costs. UNEP DTIE’s strategy in carrying out these objectives is to influence decision-making through partnerships with other international organizations, governmental authorities, business and industry, and NGOs; facilitate knowledge management through networks; support implementation of conventions; and work closely with UNEP regional offices. The Division, with its Director and Division Office in Paris, consists of one centre and five branches located in Paris, Geneva and Osaka.

x

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Economics and Trade Branch The Economics and Trade Branch (ETB) is one of the five branches of DTIE. Its mission is to enhance the capacities of developing countries and transition economies to integrate environmental considerations into development planning and macroeconomic policies, including trade policies. ETB helps countries develop and use integrated assessment and incentive tools for achieving poverty reduction and sustainable development. The Branch further works to improve our understanding of environmental, social, and economic effects of trade liberalization and the effects of environmental policies on trade, and works to strengthen coherence between Multilateral Environmental Agreements and the World Trade Organization. ETB also helps enhance the role of the financial sector in moving towards sustainability. Through its finance initiatives, ETB also helps enhance the role of the financial sector in moving towards sustainability.

For more information on the general programme of the Economics and Trade Branch, please contact:

Hussein AbazaChief, Economics and Trade Branch (ETB)Division of Technology, Industry and Economics (DTIE)United Nations Environment Programme (UNEP)11-13 Chemin des Anemones1219 Chatelaine/GenevaTel : 41-22-917 81 79Fax : 41-22-917 80 76http://www.unep.ch/etb

x�

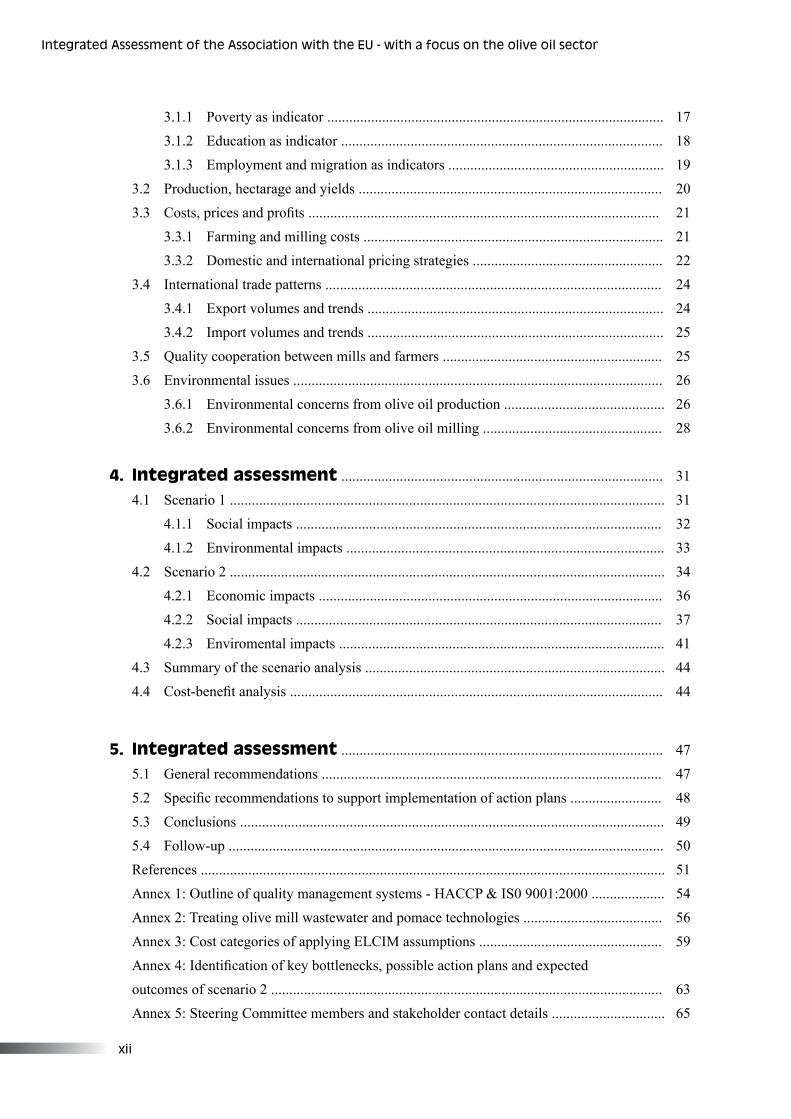

Table of contents

Preface ..................................................................................................................................... i

Acronyms and abbreviations ...................................................................................... iii

Executive summary .......................................................................................................... v

Acknowledgements .......................................................................................................... vii

United Nations Environment Programme ........................................................... ix

Table of contents ............................................................................................................... xi

List of tables ......................................................................................................................... xiii

List of figures ....................................................................................................................... xiii

List of boxes ......................................................................................................................... xiv

Map ............................................................................................................................................. xiv

1. Introduction .................................................................................................................... 1

1.1 About this report ............................................................................................................. 1

1.2 Background to the project .............................................................................................. 1

1.2.1 Project objectives ............................................................................................... 2

1.2.2 Assessment team ................................................................................................ 3

1.3 Development of methodology ....................................................................................... 4

1.3.1 Scenario analysis ................................................................................................ 4

1.3.2 Cost-benefit analysis .......................................................................................... 4

1.4 Lebanon: A brief introduction ........................................................................................ 5

1.4.1 Agriculture and the agri-food industry in Lebanon ............................................ 5

2. Trade liberalization in Lebanon ........................................................................... 9

2.1 Lebanese-EU AA ........................................................................................................... 10

2.2 European Neighbourhood Policy (ENP) ........................................................................ 12

2.3 Other trade agreements .................................................................................................. 13

3. Overview of olive oil production in Lebanon .............................................. 15

3.1 Socio-economic characteristics of olive producers ........................................................ 16

x��

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

3.1.1 Poverty as indicator ............................................................................................ 17

3.1.2 Education as indicator ........................................................................................ 18

3.1.3 Employment and migration as indicators ........................................................... 19

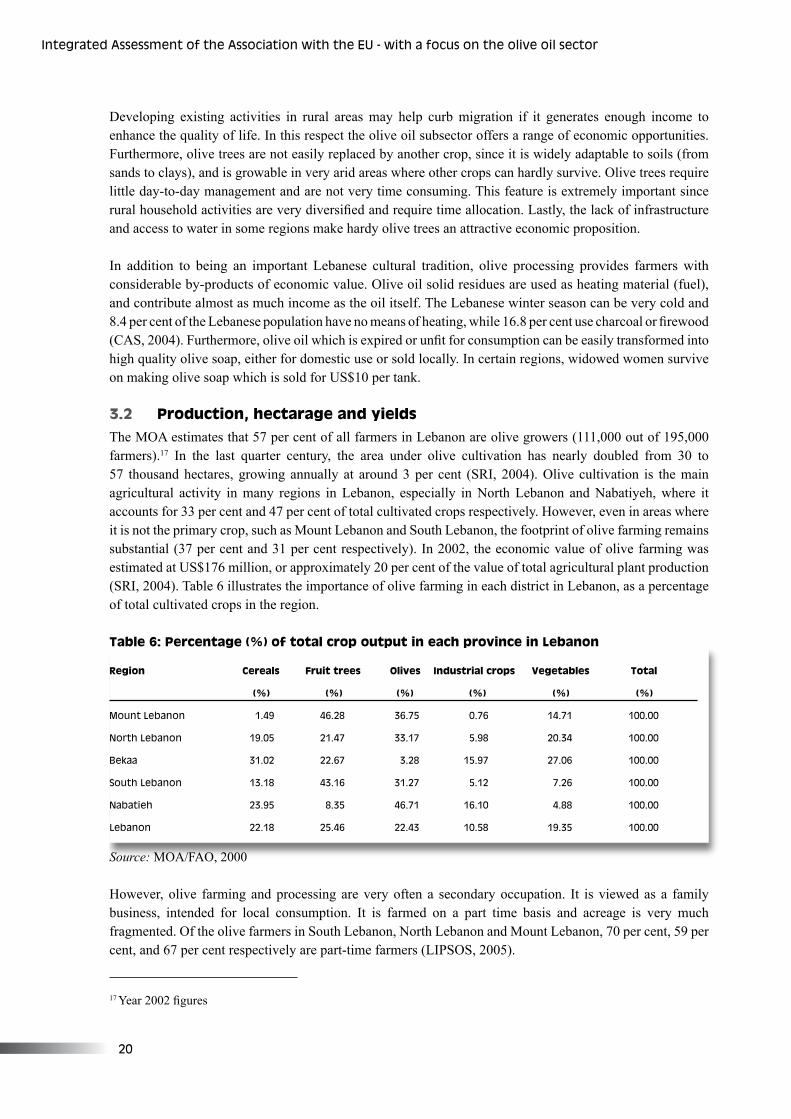

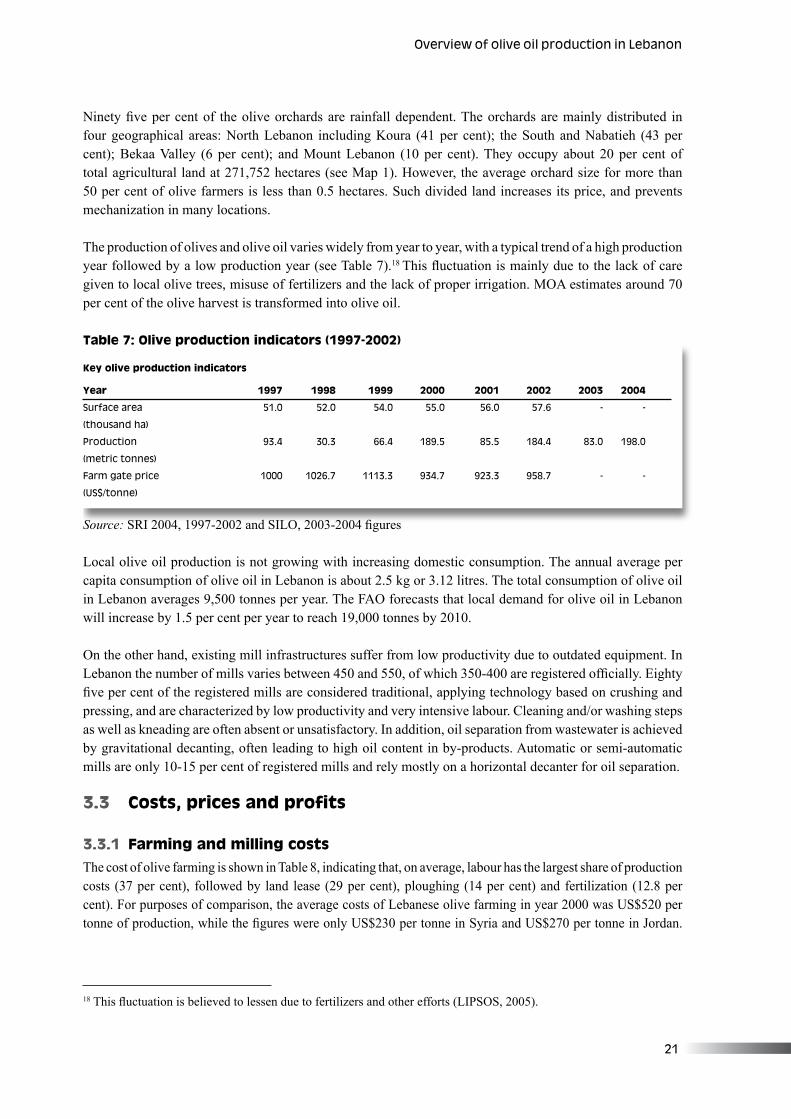

3.2 Production, hectarage and yields ................................................................................... 20

3.3 Costs, prices and profits ................................................................................................ 21

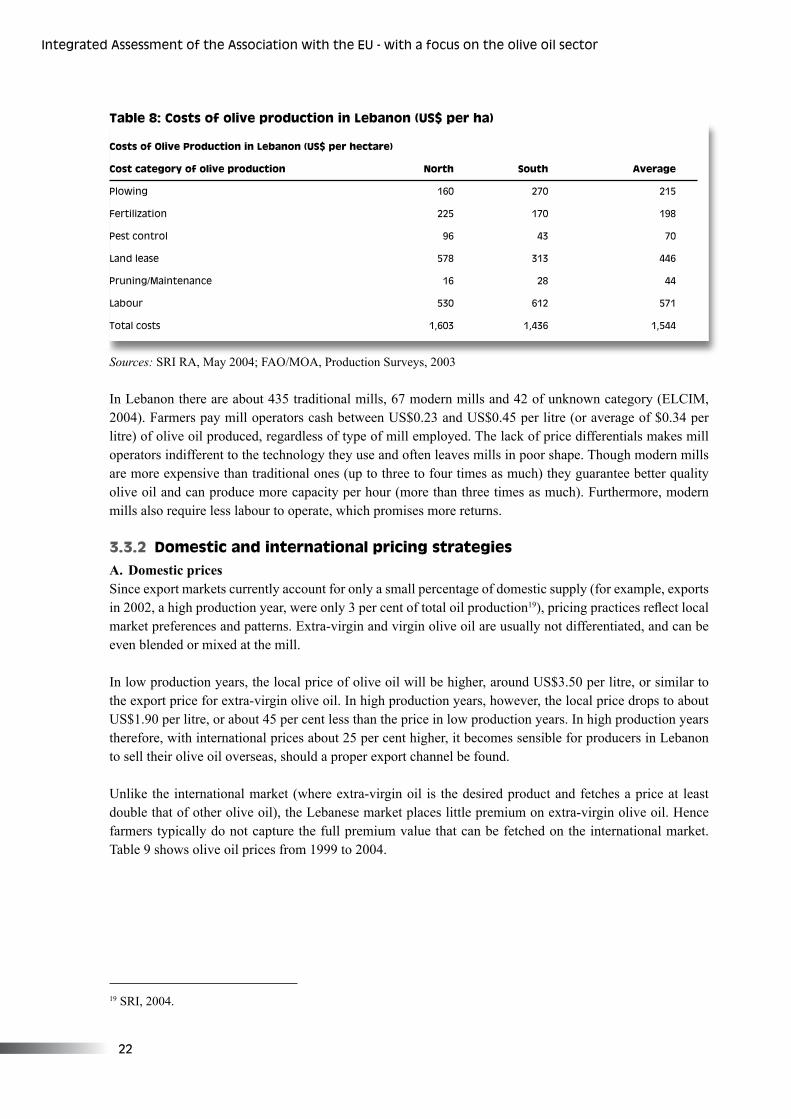

3.3.1 Farming and milling costs .................................................................................. 21

3.3.2 Domestic and international pricing strategies .................................................... 22

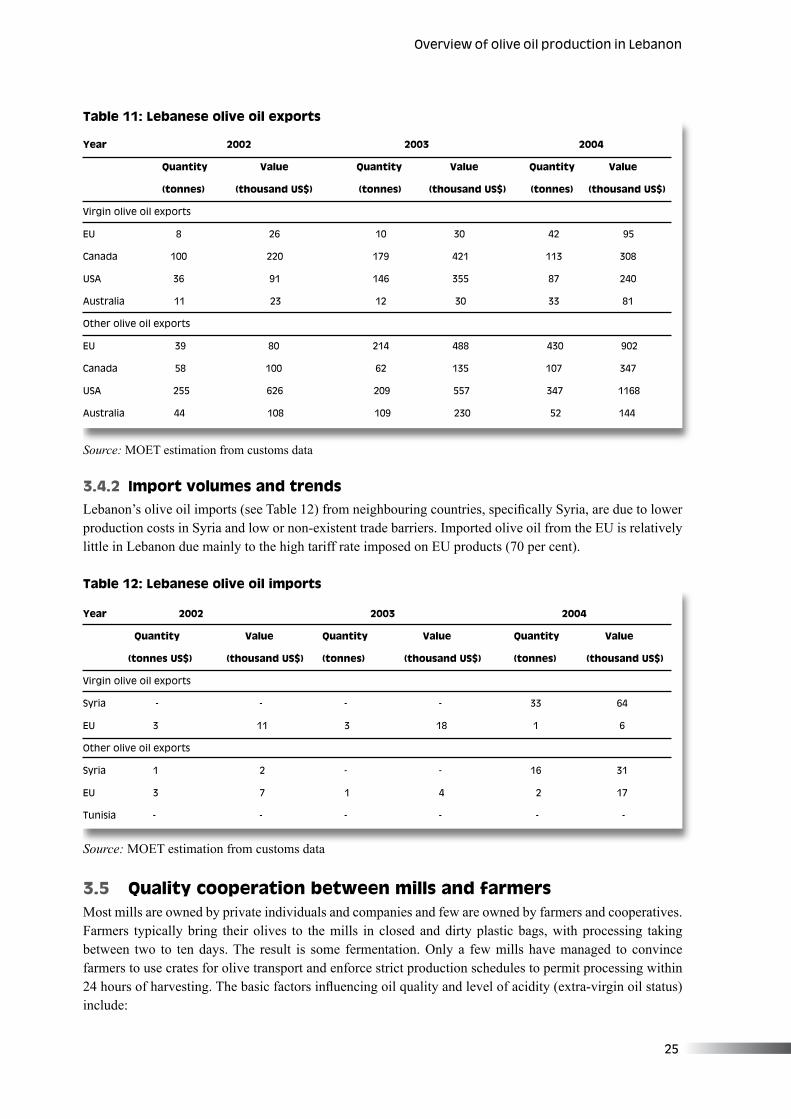

3.4 International trade patterns ............................................................................................ 24

3.4.1 Export volumes and trends ................................................................................. 24

3.4.2 Import volumes and trends ................................................................................. 25

3.5 Quality cooperation between mills and farmers ............................................................ 25

3.6 Environmental issues ..................................................................................................... 26

3.6.1 Environmental concerns from olive oil production ............................................ 26

3.6.2 Environmental concerns from olive oil milling ................................................. 28

4. Integrated assessment ........................................................................................ 31

4.1 Scenario 1 ....................................................................................................................... 31

4.1.1 Social impacts .................................................................................................... 32

4.1.2 Environmental impacts ....................................................................................... 33

4.2 Scenario 2 ....................................................................................................................... 34

4.2.1 Economic impacts .............................................................................................. 36

4.2.2 Social impacts .................................................................................................... 37

4.2.3 Enviromental impacts ......................................................................................... 41

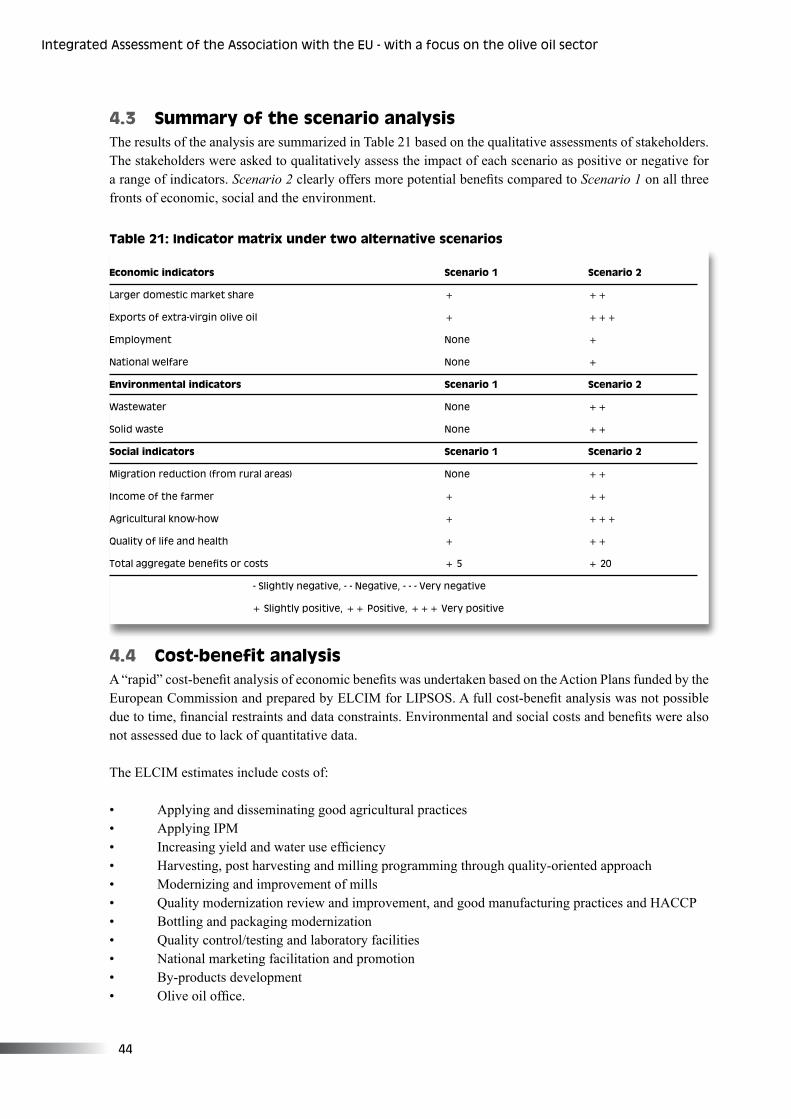

4.3 Summary of the scenario analysis .................................................................................. 44

4.4 Cost-benefit analysis ...................................................................................................... 44

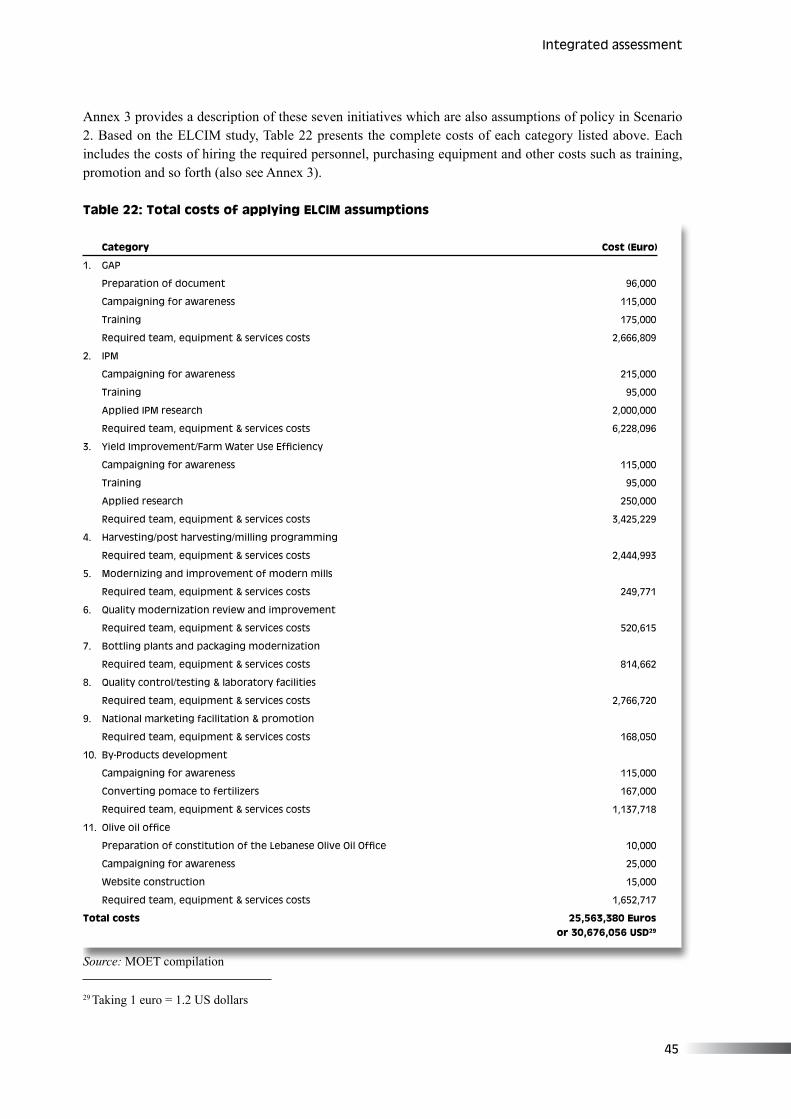

5. Integrated assessment ........................................................................................ 47

5.1 General recommendations ............................................................................................. 47

5.2 Specific recommendations to support implementation of action plans ......................... 48

5.3 Conclusions .................................................................................................................... 49

5.4 Follow-up ....................................................................................................................... 50

References ............................................................................................................................... 51

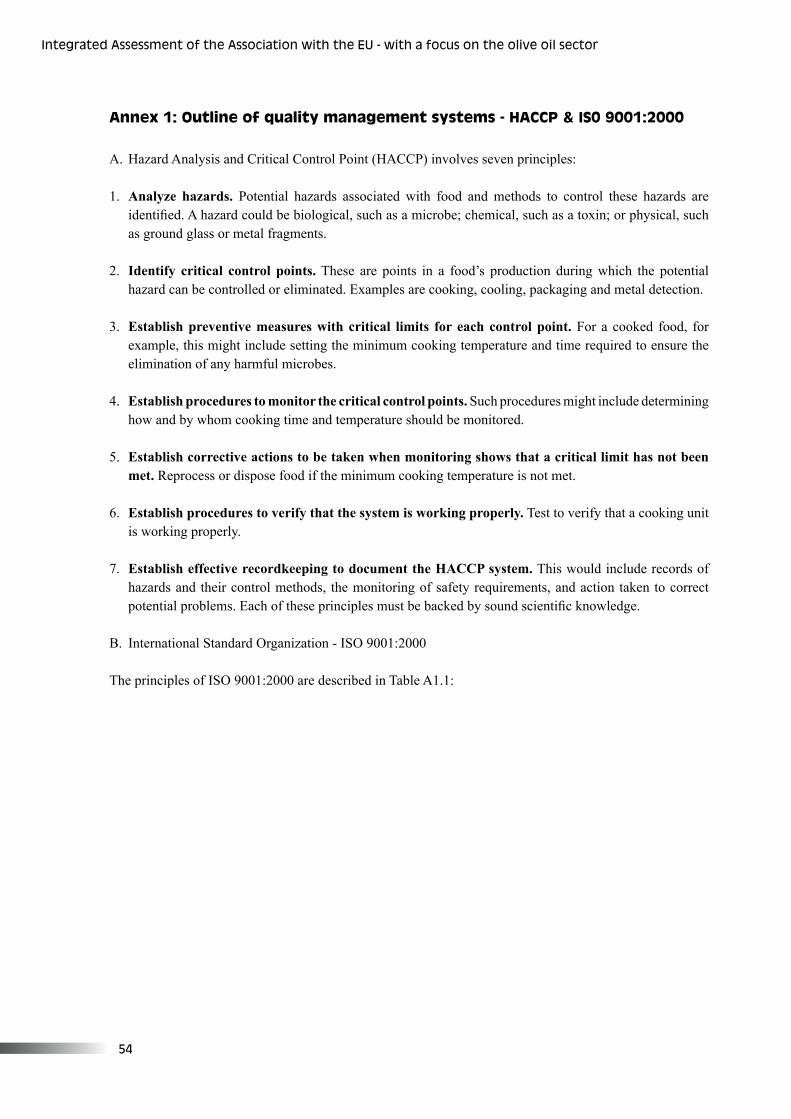

Annex 1: Outline of quality management systems - HACCP & IS0 9001:2000 .................... 54

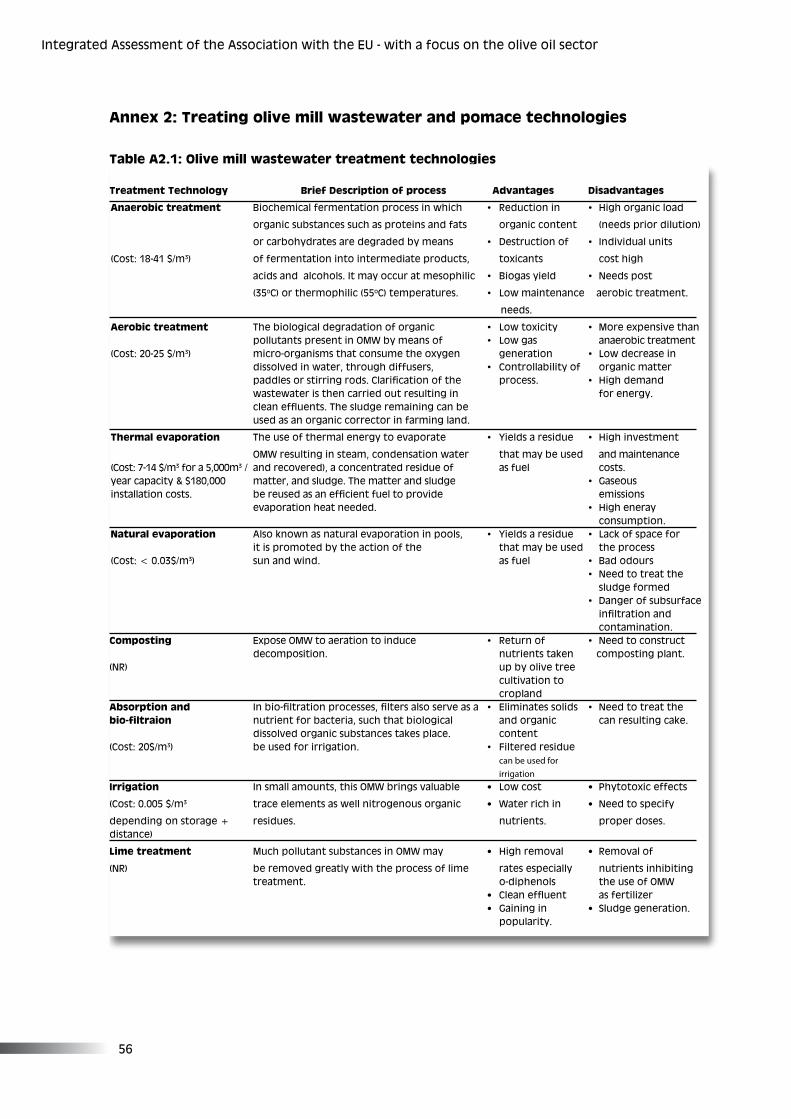

Annex 2: Treating olive mill wastewater and pomace technologies ...................................... 56

Annex 3: Cost categories of applying ELCIM assumptions .................................................. 59

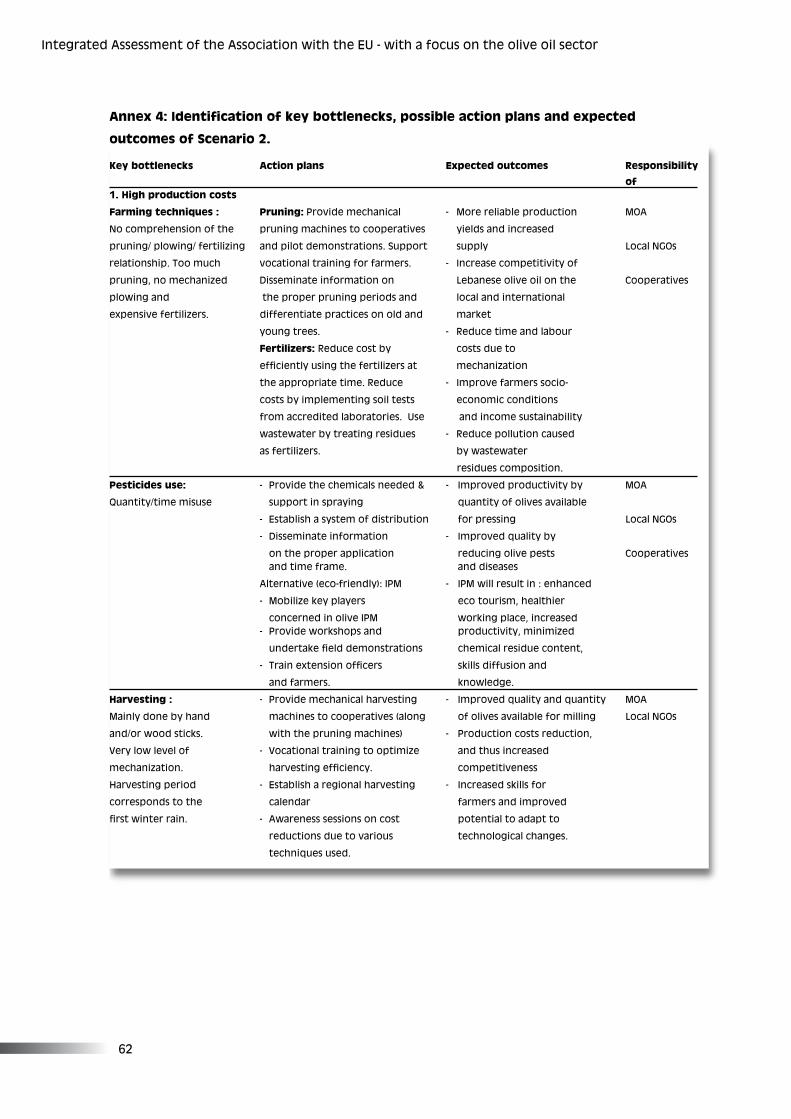

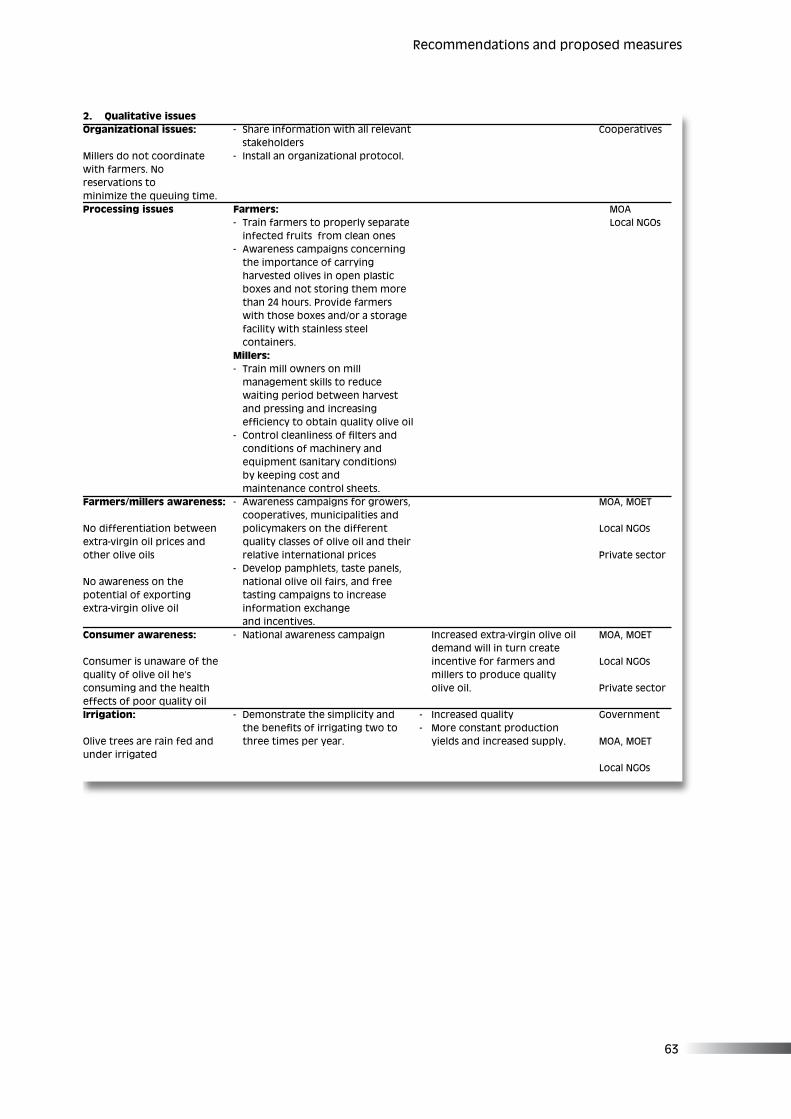

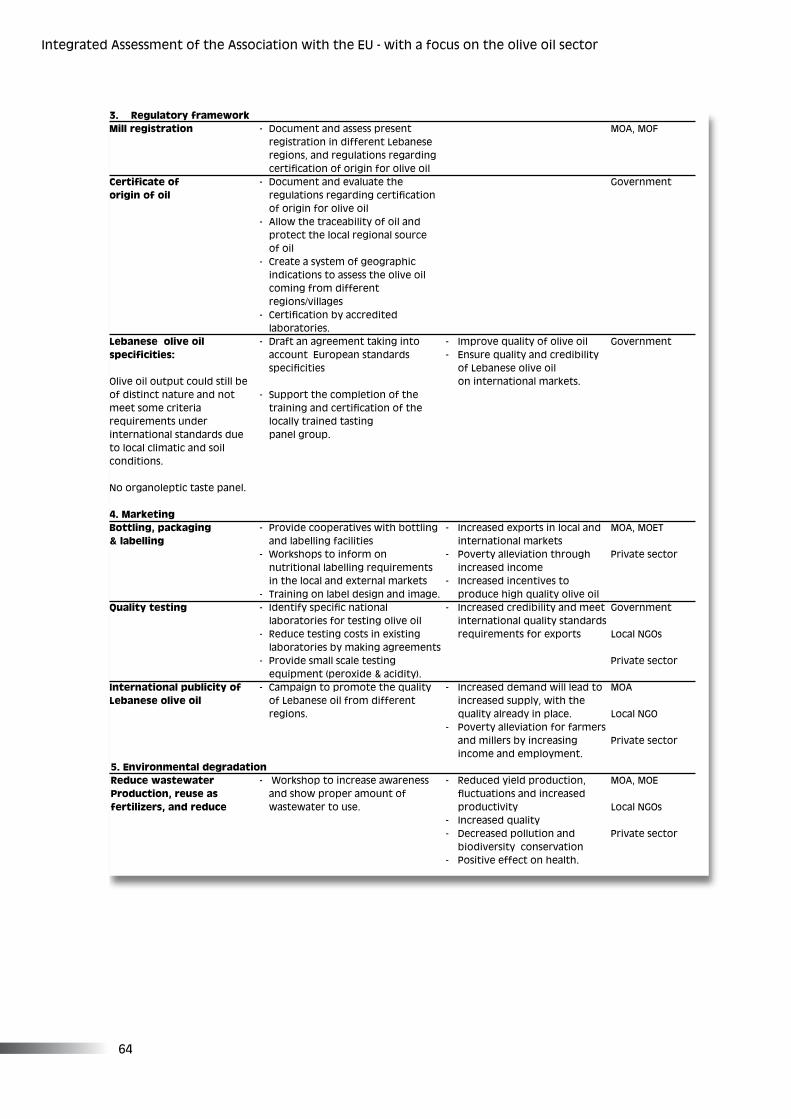

Annex 4: Identification of key bottlenecks, possible action plans and expected

outcomes of scenario 2 ........................................................................................................... 63

Annex 5: Steering Committee members and stakeholder contact details ............................... 65

x���

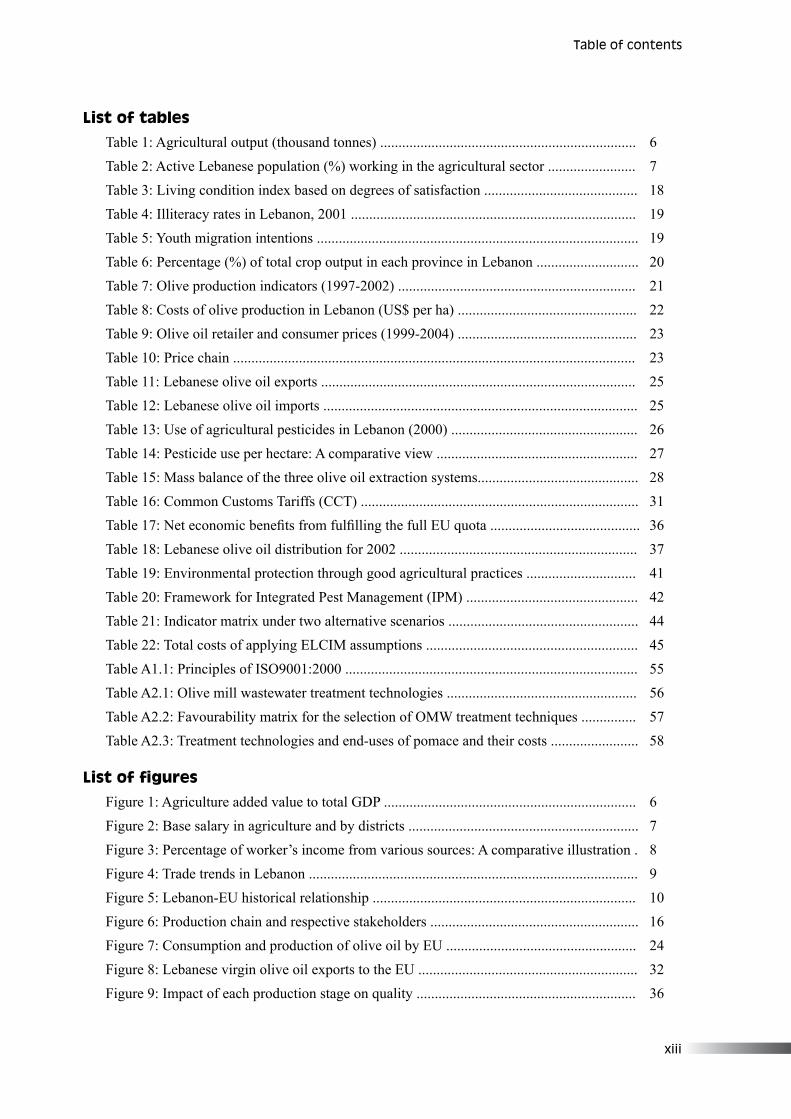

List of tables

Table 1: Agricultural output (thousand tonnes) ...................................................................... 6

Table 2: Active Lebanese population (%) working in the agricultural sector ........................ 7

Table 3: Living condition index based on degrees of satisfaction .......................................... 18

Table 4: Illiteracy rates in Lebanon, 2001 .............................................................................. 19

Table 5: Youth migration intentions ........................................................................................ 19

Table 6: Percentage (%) of total crop output in each province in Lebanon ............................ 20

Table 7: Olive production indicators (1997-2002) ................................................................. 21

Table 8: Costs of olive production in Lebanon (US$ per ha) ................................................. 22

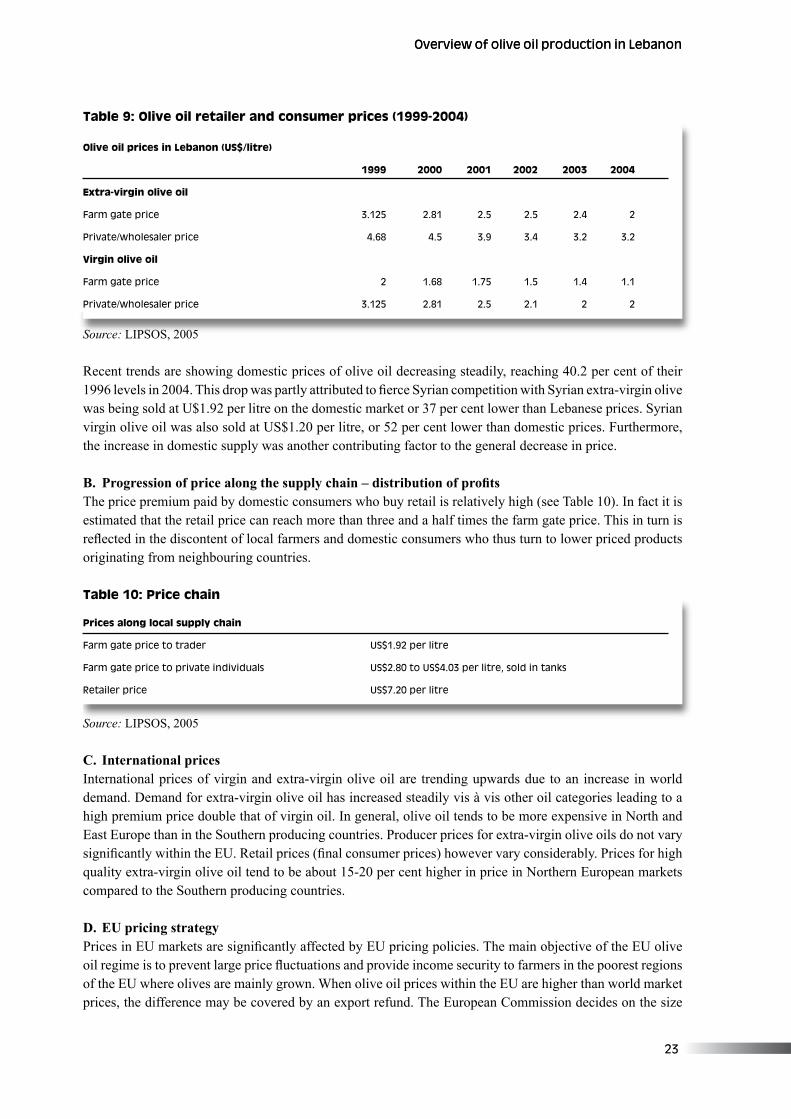

Table 9: Olive oil retailer and consumer prices (1999-2004) ................................................. 23

Table 10: Price chain .............................................................................................................. 23

Table 11: Lebanese olive oil exports ...................................................................................... 25

Table 12: Lebanese olive oil imports ...................................................................................... 25

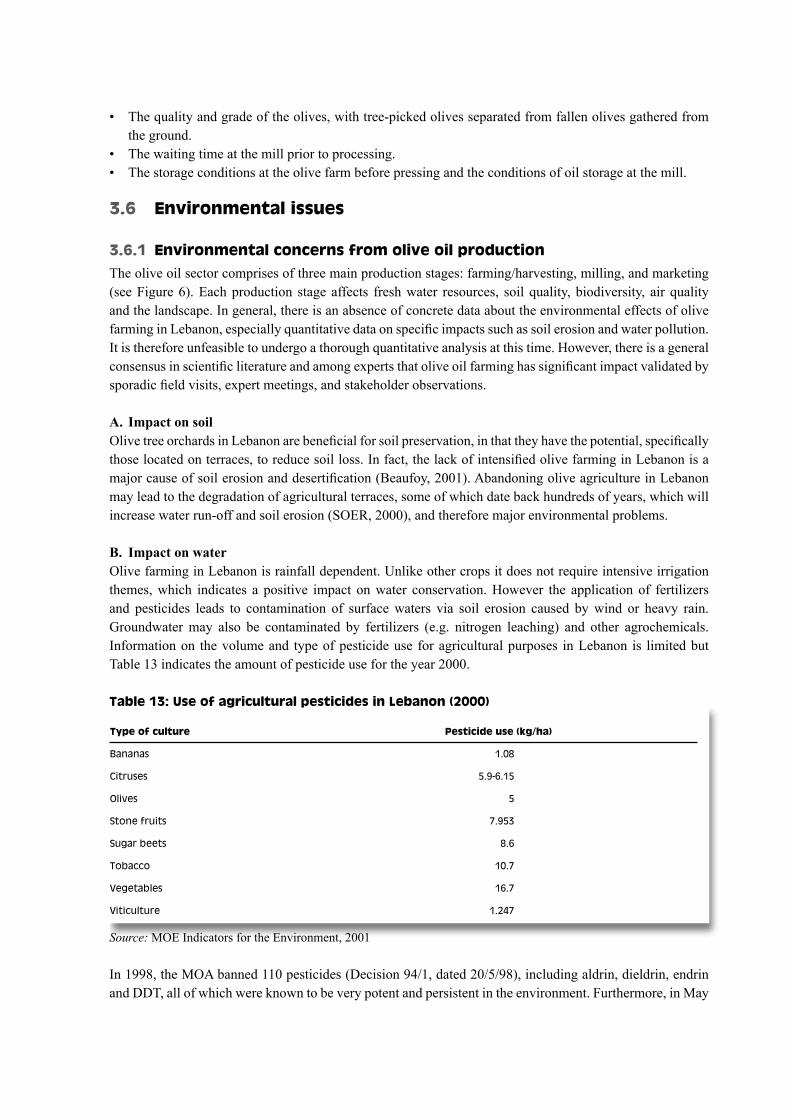

Table 13: Use of agricultural pesticides in Lebanon (2000) ................................................... 26

Table 14: Pesticide use per hectare: A comparative view ....................................................... 27

Table 15: Mass balance of the three olive oil extraction systems............................................ 28

Table 16: Common Customs Tariffs (CCT) ............................................................................ 31

Table 17: Net economic benefits from fulfilling the full EU quota ......................................... 36

Table 18: Lebanese olive oil distribution for 2002 ................................................................. 37

Table 19: Environmental protection through good agricultural practices .............................. 41

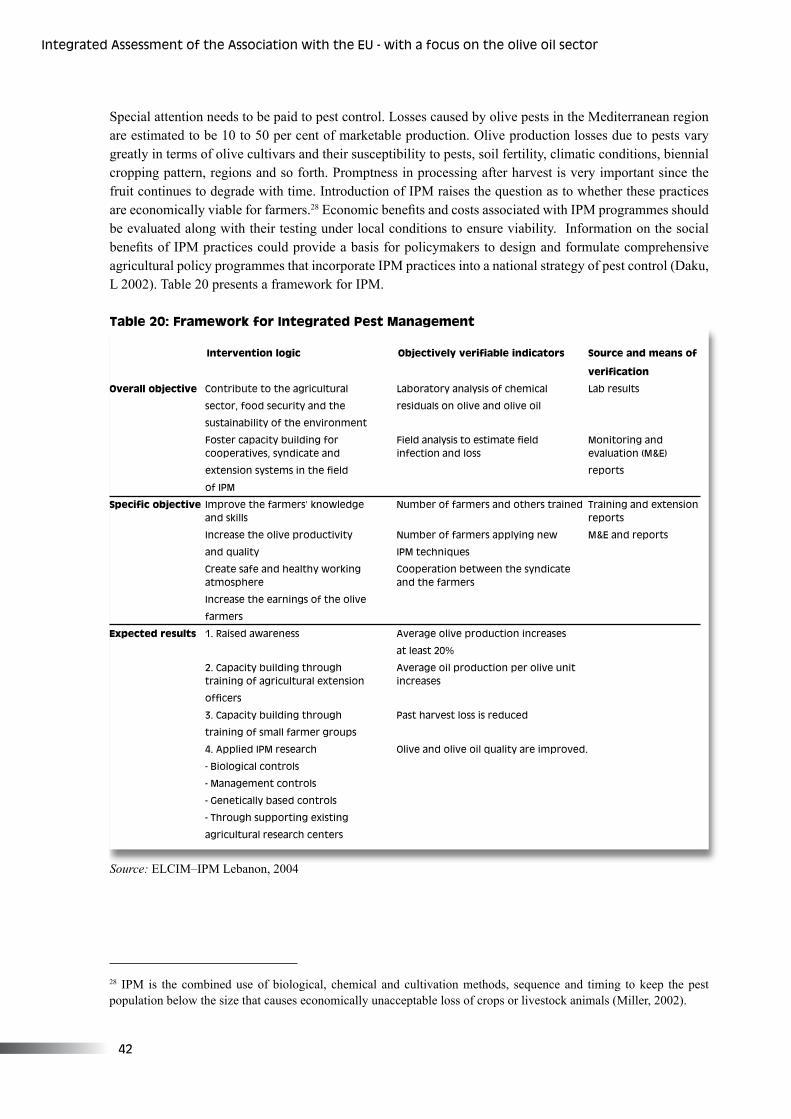

Table 20: Framework for Integrated Pest Management (IPM) ............................................... 42

Table 21: Indicator matrix under two alternative scenarios .................................................... 44

Table 22: Total costs of applying ELCIM assumptions .......................................................... 45

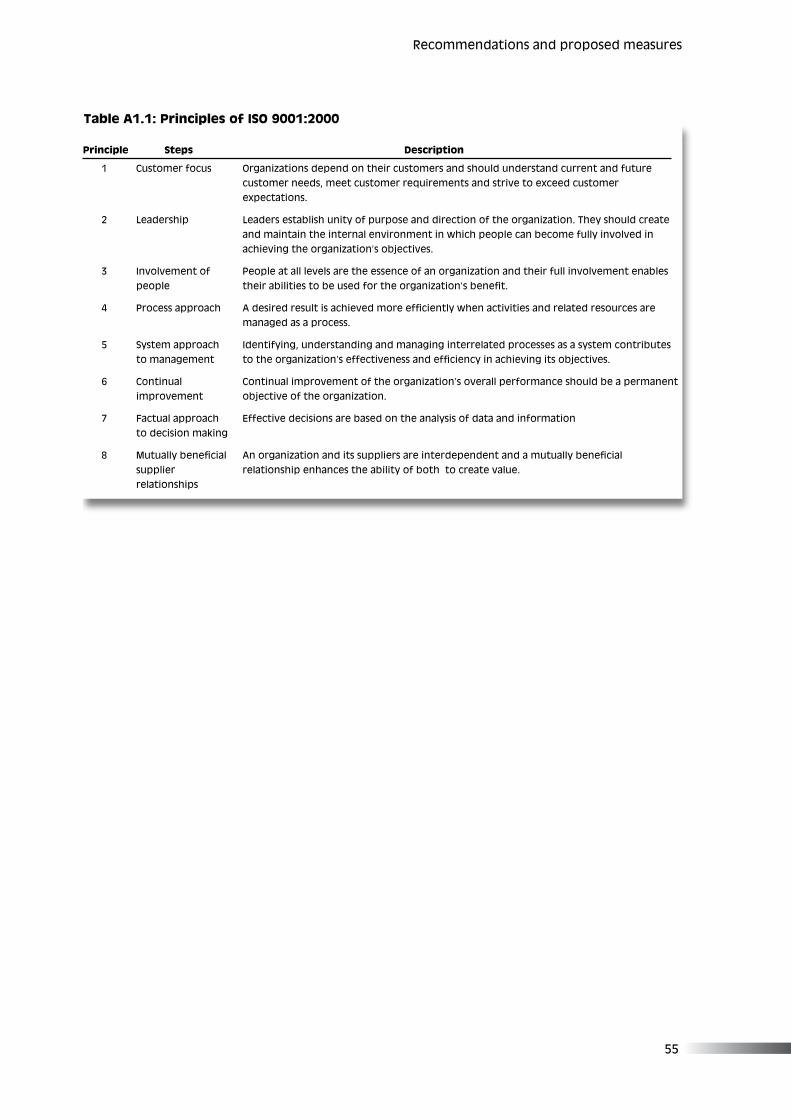

Table A1.1: Principles of ISO9001:2000 ................................................................................ 55

Table A2.1: Olive mill wastewater treatment technologies .................................................... 56

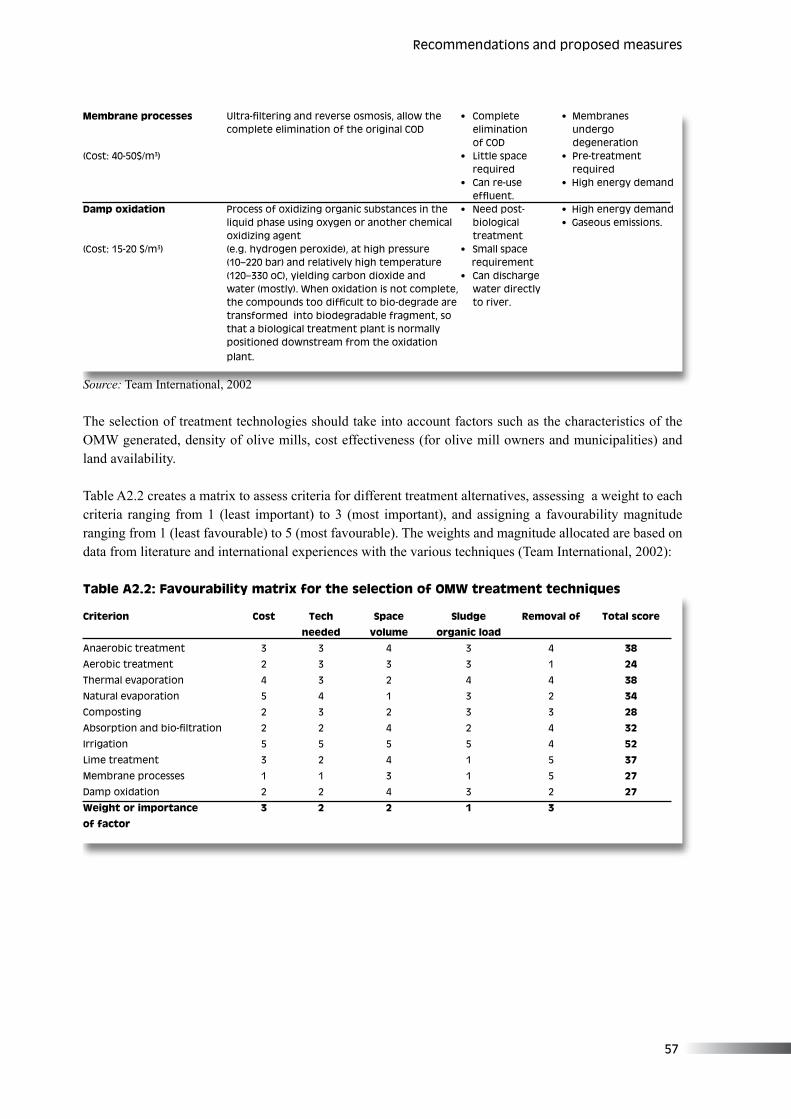

Table A2.2: Favourability matrix for the selection of OMW treatment techniques ............... 57

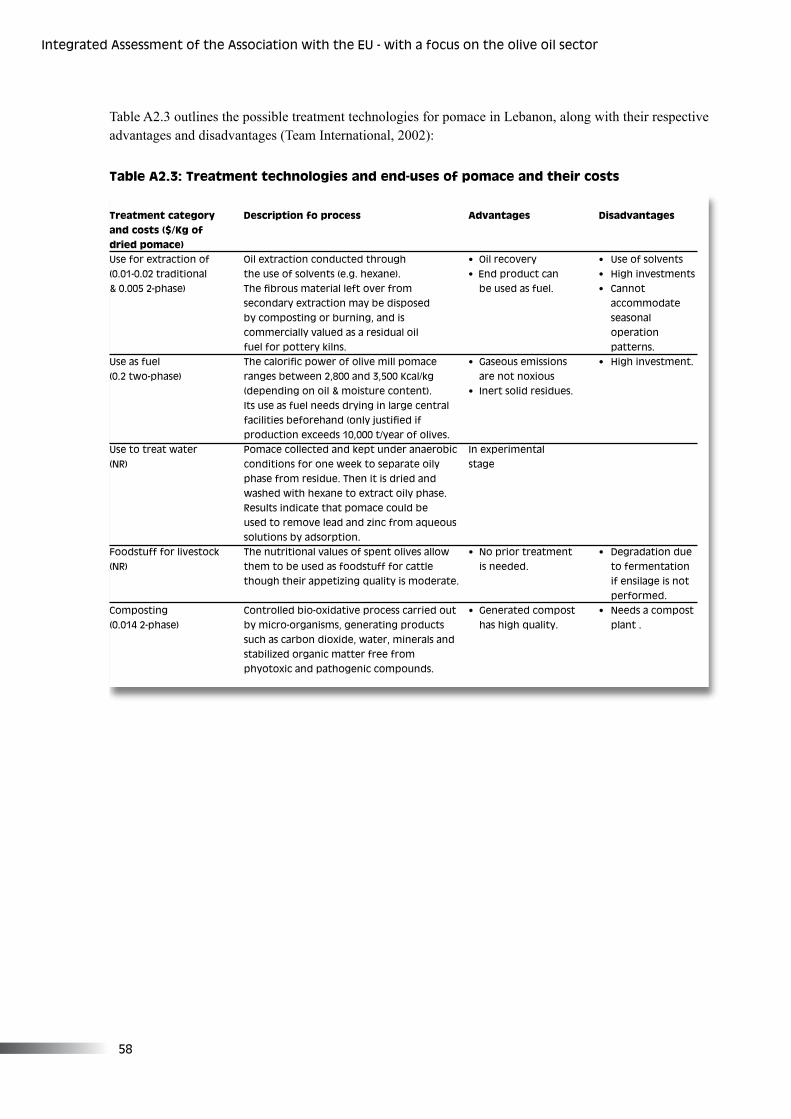

Table A2.3: Treatment technologies and end-uses of pomace and their costs ........................ 58

List of figures

Figure 1: Agriculture added value to total GDP ..................................................................... 6

Figure 2: Base salary in agriculture and by districts ............................................................... 7

Figure 3: Percentage of worker’s income from various sources: A comparative illustration . 8

Figure 4: Trade trends in Lebanon .......................................................................................... 9

Figure 5: Lebanon-EU historical relationship ........................................................................ 10

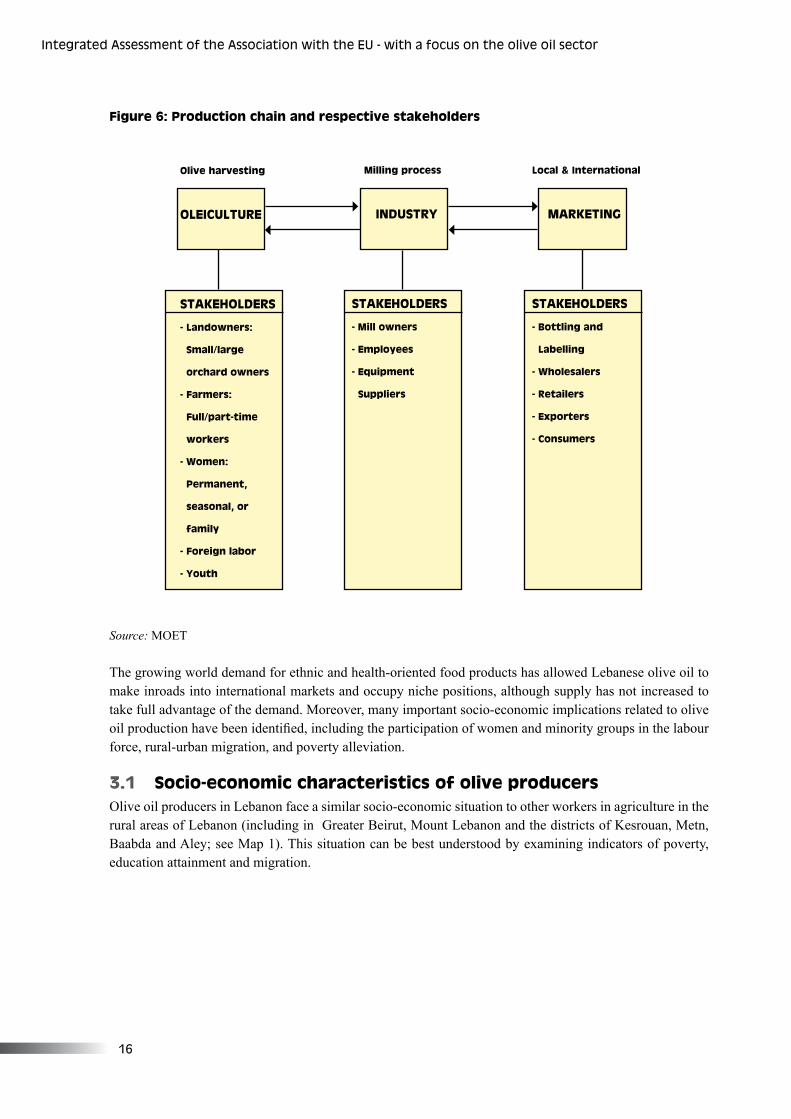

Figure 6: Production chain and respective stakeholders ......................................................... 16

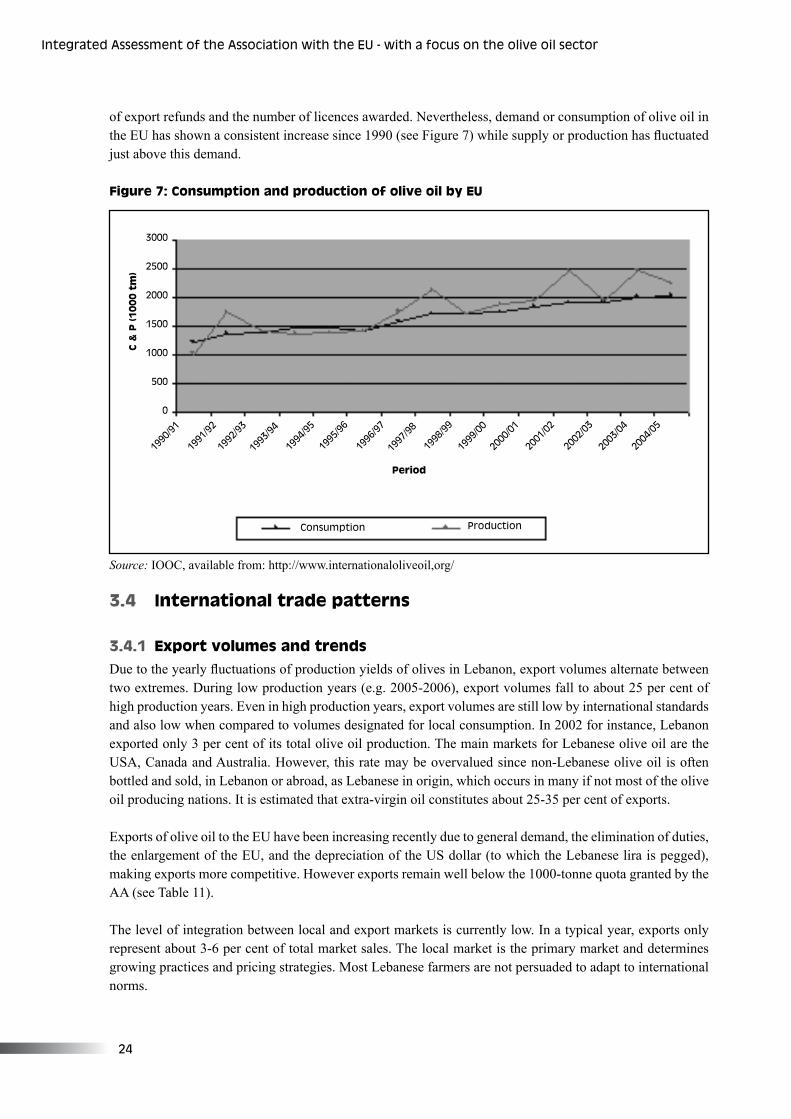

Figure 7: Consumption and production of olive oil by EU .................................................... 24

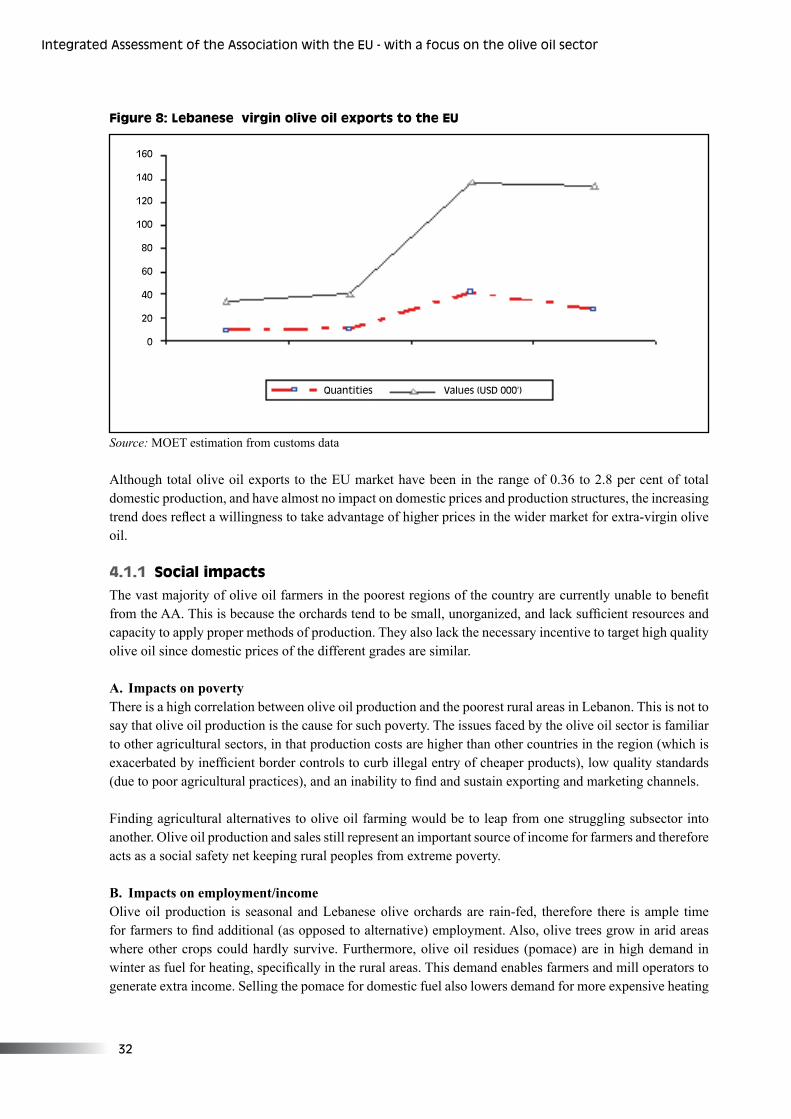

Figure 8: Lebanese virgin olive oil exports to the EU ............................................................ 32

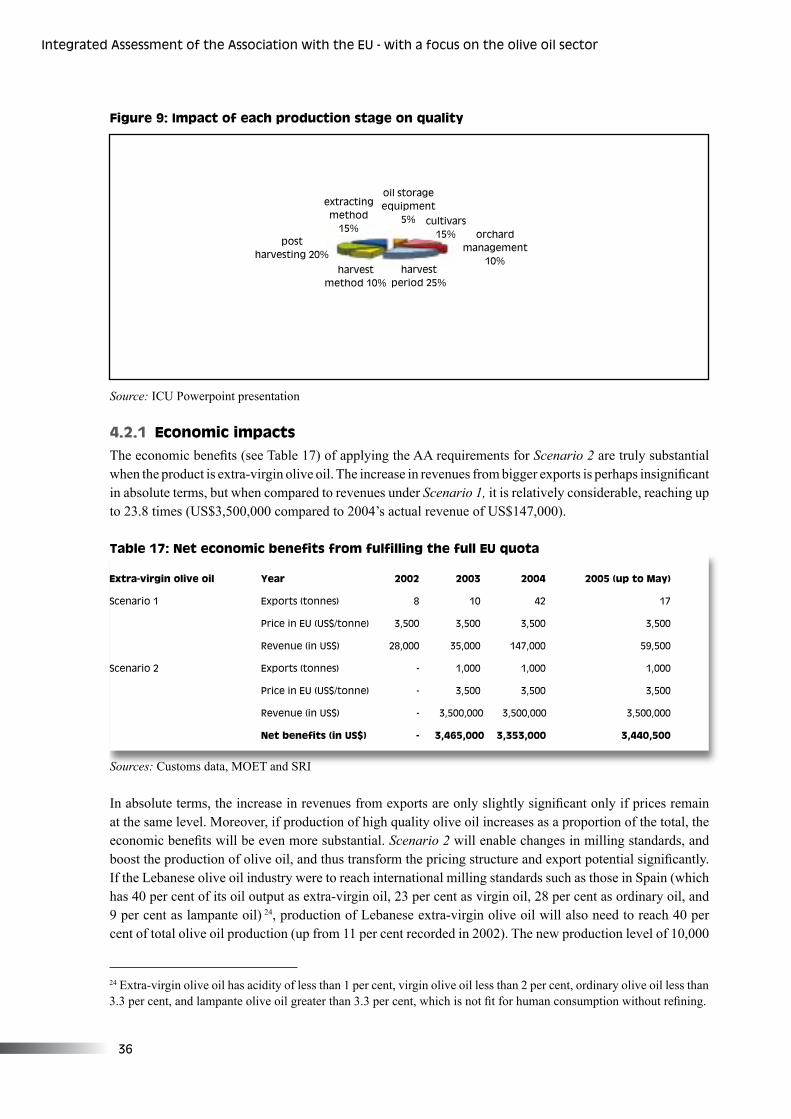

Figure 9: Impact of each production stage on quality ............................................................ 36

Table of contents

x�v

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

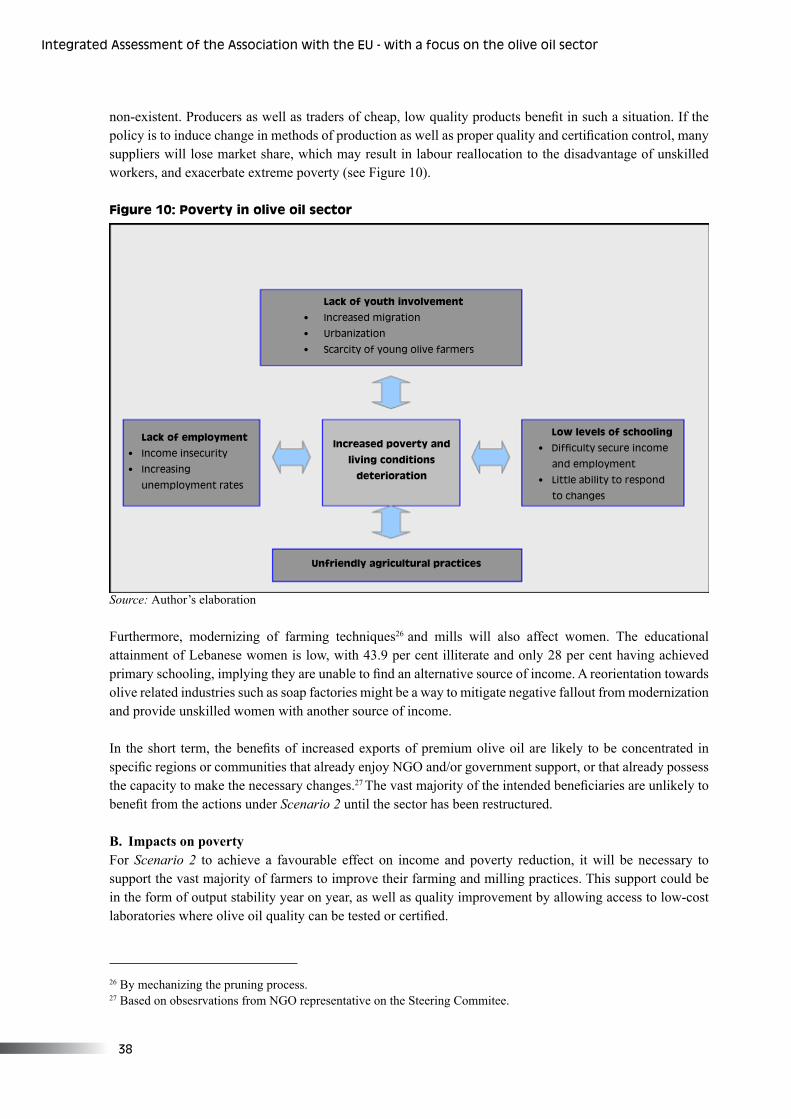

Figure 10: Poverty in the olive oil sector ................................................................................. 38

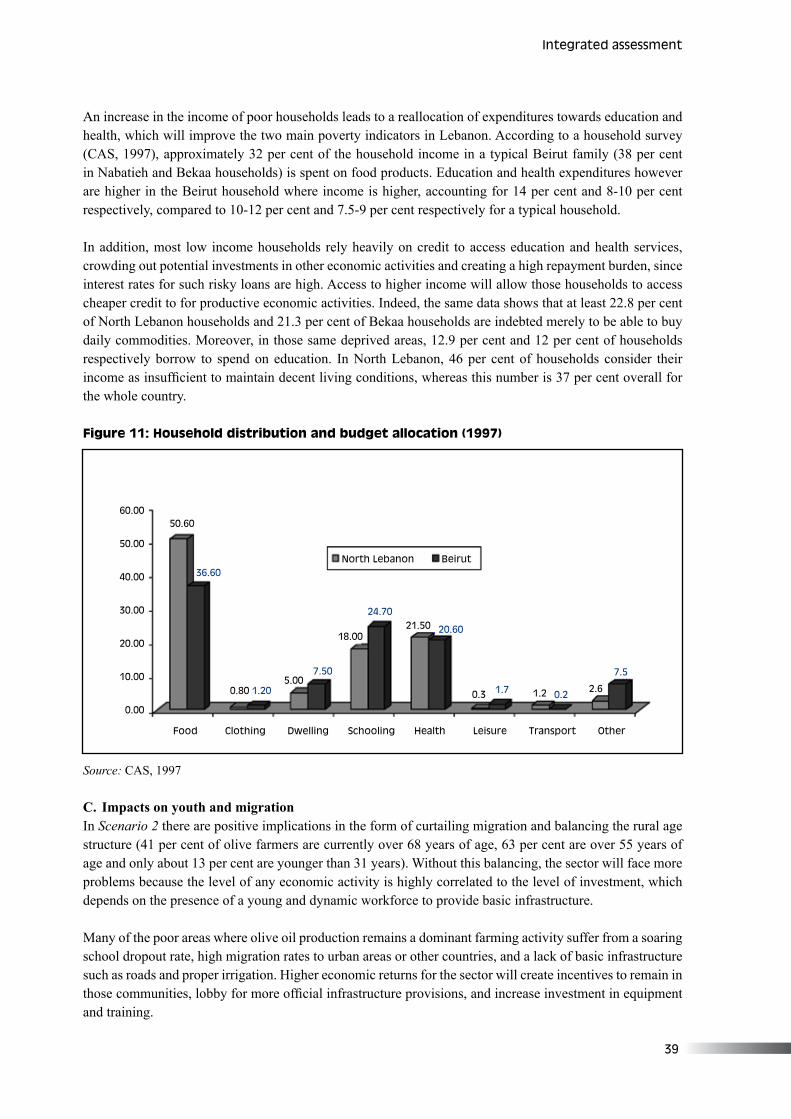

Figure 11: Household distribution and budget allocation ........................................................ 39

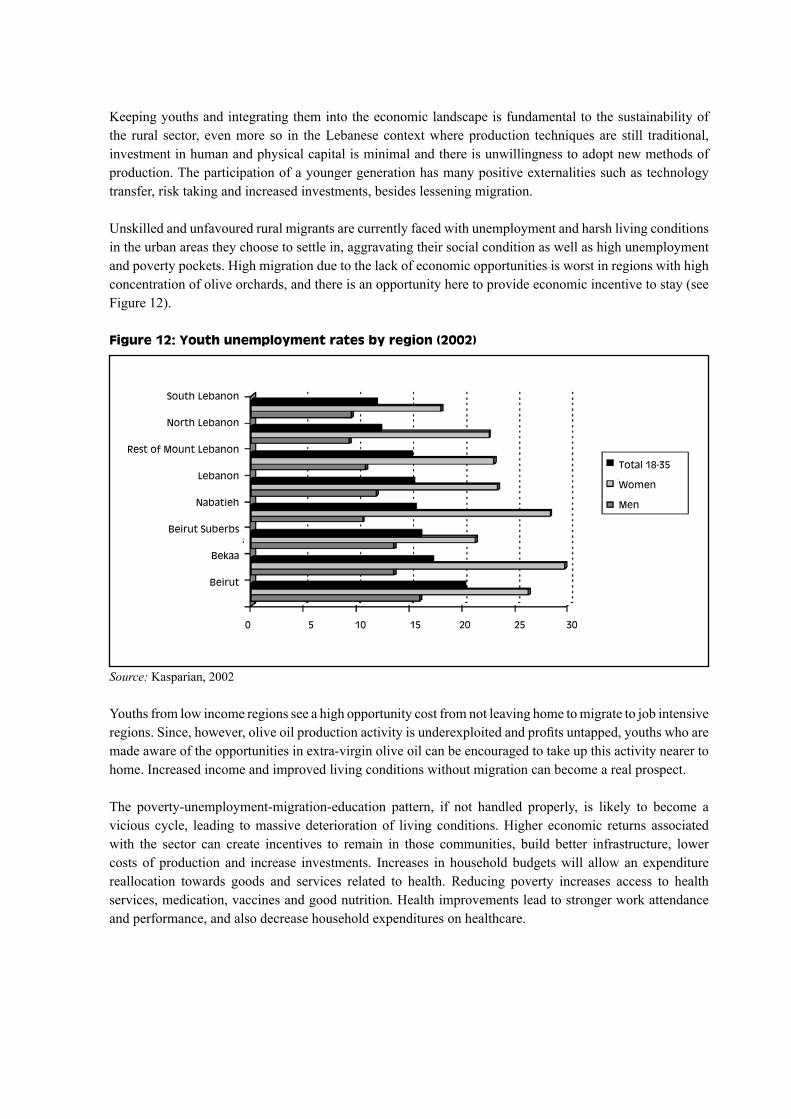

Figure 12: Youth unemployment rates by region (2002) ......................................................... 40

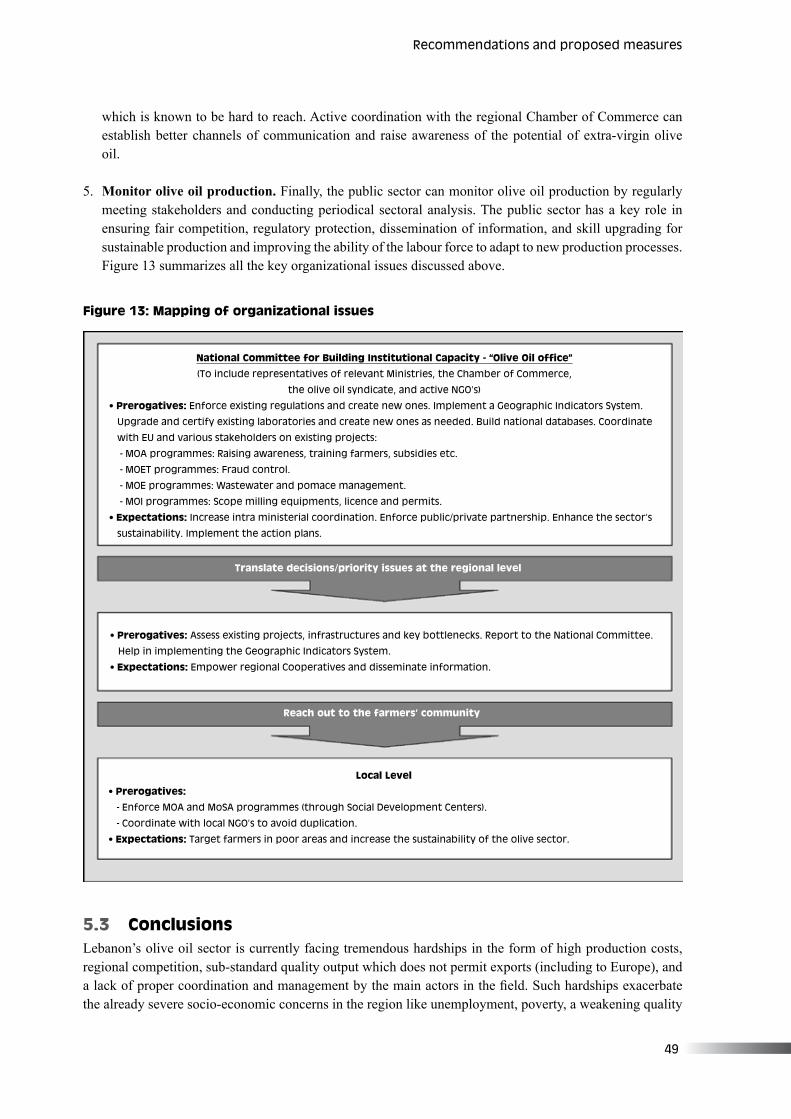

Figure 13: Mapping of organizational issues ........................................................................... 49

List of boxes Box 1: Project on integrated management of olive oil production waste ............................... 29

Box 2: Case study: Impacts of olive oil processing in the Hasbaya region ............................ 34

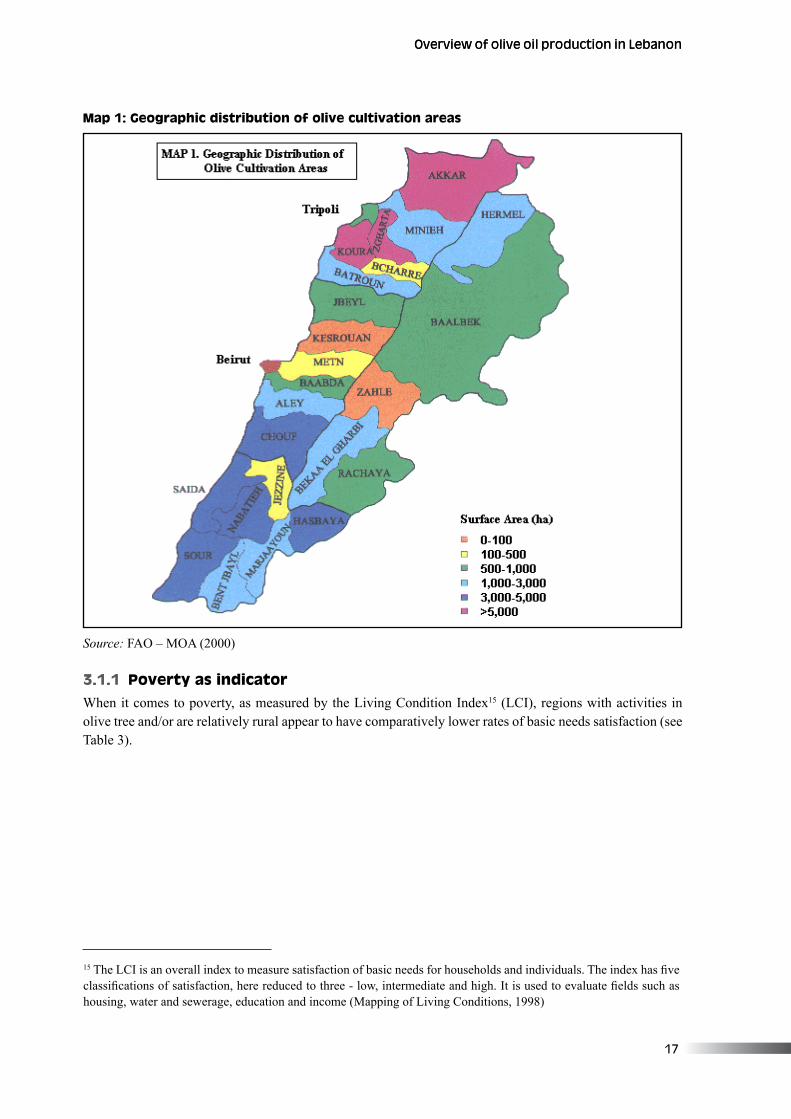

Map Map 1: Geographic distribution of olive cultivation areas ..................................................... 17

�

�. Introduct�on

1.1 About this report This report presents the results of an integrated assessment of the impacts of trade liberalization on Lebanon’s olive oil sector, specifically the projected effect of the Euro-Mediterranean Association Agreement (AA) between the EU and Lebanon signed in 2002. The AA permits 1,000 tonnes of duty-free olive oil to be exported from Lebanon to the EU, but Lebanon has so far not taken full advantage of this market opportunity. In order to do so, Lebanon needs to improve product quality, reduce production costs and sustain output volume and consistency. The aim of the report is thus to present an analysis of the situation and outline a clear set of policy recommendations and measures necessary to strengthen the olive oil sector, and improve the quality and quantity of olive oil produced including exports.

The report is divided into 5 chapters. Chapter 1 introduces the project and provides a brief background of the Lebanese socio-economic and political situation with detailed focus on agriculture and the olive oil sector. Chapter 2 discusses Lebanon’s approach to trade liberalization and reviews the agreements between Lebanon and the EU as well as relevant agreements with other countries or organizations. Chapter 3 presents an overview of Lebanon’s olive oil subsector and describes the production chain from farming to processing to marketing. Chapter 4 discusses the results of the integrated assessment and Chapter 5 outlines recommendations and measures to be undertaken to improve the sector’s performance and increase readiness for more trade liberalization. Finally, some general conclusions and suggestions for follow-up are summarized.

The report is targeted at policymakers and advocates (public sector bodies, private stakeholders, syndicates, cooperatives and NGOs) to raise awareness of an integrated approach to the design of trade policies that takes into account key social and environmental issues in addition to economic concerns.

1.2 Background to the projectThe project was initiated in December 2004 by the Ministry of Economy and Trade (MOET) in collaboration with the Ministry of Environment (MOE) and United Nations Environment Programme (UNEP). In June 2002, Lebanon signed the EU-Lebanon Association Agreement (AA) and, in December the Agreement was ratified by the Lebanese Parliament. The objective of the AA was to provide an appropriate framework for political dialogue with Europe; establish the conditions for the gradual liberalization of trade in goods, services, and capital; and promote economic, social, cultural, financial and monetary cooperation.1 An Interim Agreement entered into force in March 2003 allowed for the immediate implementation of economic and trade-related provisions of the AA while awaiting parliamentary ratification from all EU member states. The AA was selected for integrated assessment because it was created as an comprehensive agreement and allows study of economic, social and environment impacts and inter-linkages beyond all earlier studies.

1 Article 1 of the AA.

�

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

The project focused on the olive oil sector because of the important role it plays in the Lebanese economy, local communities and the environment, including poverty reduction, employment generation, migration, magnitude of trade, growth potential, the rural landscape, and environmental implications such as waste generation and disposal. Moreover, the keen willingness of stakeholders in the olive oil industry to provide necessary information and available data smoothed the way for an assessment. In 2002, the economic value of olive farming was estimated at US$176 million, or approximately 20 per cent of the total value of Lebanese agricultural plant production (SRI, 2004). The procedures and agents involved in olive oil production in Lebanon (from farming to milling to marketing) were surveyed to identify areas of concern and accordingly, action plans.

A number of major policies and projects are related to the current study and were studied. These included the Strategic Environmental Assessment Project of the Ministry of Environment (MOE) conducted in 2005, the World Bank country assessment strategy outlined in 1997, and the various programmes under the Association Agreement. Furthermore, a large number of pilot projects targeting the olive oil sector have also been carried out, for example a study for the Ministry of Industry (MOI) entitled, “The Impact of the Euro-Mediterranean Agreement on the Olive Oil Industry in Lebanon” (Mirza, 2004).

The Euro-Lebanese Centre for Industrial Modernization (ELCIM) also undertook an evaluation of necessary action plans to improve quality of olive oil, disseminate better farming practices (including the introduction of Integrated Pest Management) and enhance marketability of Lebanese olive oil. This study also features a comprehensive inventory of the costs involved in implementing such action plans. Moreover, the Stanford Research Institute (SRI) conducted a rapid appraisal of the olive oil sector in Lebanon (SRI, 2004), and unveiled ways to produce a higher proportion of extra-virgin olive oil. SRI is also intensively involved in various projects to improve olive oil quality, and enhance its marketability and export potential.

Furthermore, a Lebanese National Agricultural Policy termed the “Green Plan” was initiated in 1995 to provide assistance to farmers and rural communities in agricultural land development and in rural road construction, in line with environmental protection. On one hand, land development activities were undertaken through cost sharing arrangements with the farmer who would complete a land reclamation and assistance application and pay a percentage contribution before start-up of works. On the other hand, agricultural roads executed by the Green Plan were usually short roads that improved access of rural communities to their land.

The contribution of the current IAP project over previous studies is that it takes a holistic approach to the assessment of the olive oil sector by integrating socio-economic implications with environmental ones as the consequences of opening up trade through the AA.

1.2.1 Project objectives• Identify national priorities and action plans to increase exports under the AA• Propose complementary measures to support implementation of action plans• Promote cooperation between relevant government entities• Enhance active stakeholder participation • Develop a country-specific methodology that can be replicated in other sectors or planning processes.

�

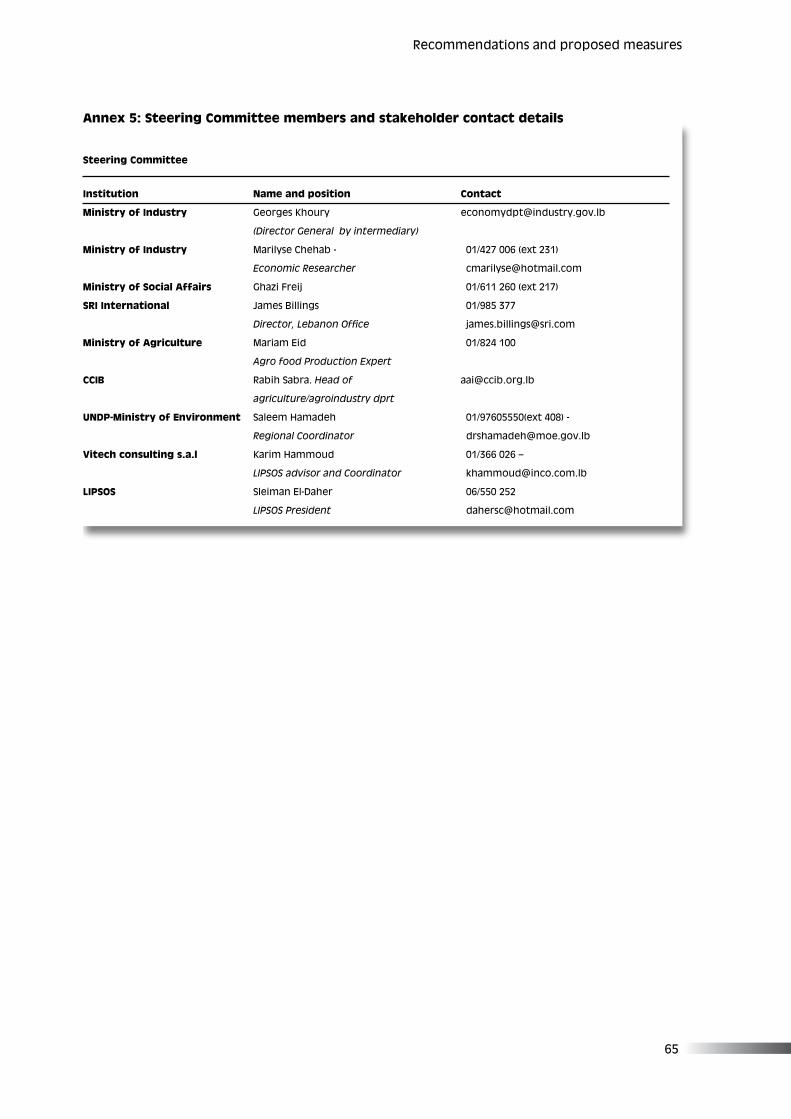

1.2.2 Assessment teamThe assessment team was led by MOET in collaboration with MOE, and with technical support from UNEP. A Steering Committee was established to coordinate the work and two workshops were held to permit thorough and on-the-ground understanding of the sector as a whole.

Members of the Steering Committee were as follows:

• Georges Khoury, Director General by intermediary, Ministry of Industry • Marilyse Chehab, Economic Researcher, Ministry of Industry • Ghazi Freij, Ministry of Social Affairs • James Billings, Director, Lebanon Office SRI International • Mariam Eid, Agro-food production expert, Ministry of Agriculture • Rabih Sabra, Head of agriculture/agroindustry department, CCIB • Saleem Hamadeh, Regional Coordinator, UNDP-Ministry of Environment • Karim Hammoud, SILO advisor and coordinator Vitech consulting s.a.l • Sleiman El-Daher, President SILO.

A multi-disciplinary team comprising of a wide range of stakeholders was established, and included representatives from the following organizations and institutions:

• Association of Lebanese Industrialists - Saad Ouyeenni • Central Administration of Statistics (CAS) - Ziad Abdallah • Chamber of Commerce, Industry and Agriculture of Beirut

o Rabih Sabra, Head of Agriculture/Agro Industry Departmento Rania Bizri, Economic Researchero Nassima Ghanem, Head of Library and Documentation Departmento Albert Nasr, EU Experto Hana Haidar, EU Database

• Cortas Trader - Raja Cortas • Economic and Social Fund for Development (ESFD)

o Lara Abou Saifan, Communication and Public Relations Officer o Racha Chahine o Hassam Omar

• European Commission Delegation - Fransisco Acosta, Economic and Political Coordinator• Instituto par la cooperazione Universitaria (ICU; Italian NGO)

o Jose Antonio Villaverde, Resident Representative o Hussain Hoteit, Agrofood Engineer

• Ministry of Agriculture - Myriam Eid • Ministry of Environment

o Saleem Hamadeh, Regional Coordinatoro Alissar Chaker, Project Managero Lamia Chamas

• Ministry of Industry o Georges Khoury, Acting Director General o Marilyse Chehab, Economic Researcher

Introduct�on

�

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

• Ministry of Social Affairs o Joumana Kalot, NGO Liaison Officer o Hachem el Hussein, Technical Expert o Mazhar Haraké, Project Managero Ghazi Freij

• Rene Moawad Foundation o Fady Yarak, Executive Director o Delphine Copain

• Lebanese Interprofessionnal Syndicate of Olive Oil (SILO) - Sleiman El-Daher, SILO President• SRI International - James Billings, Director, Lebanon Office• Syndicate of Agro-Food - George Nasraoui • Vitech Consulting s.a.l - Karim Hammoud, SILO Advisor and Coordinator.

1.3 Development of methodologyThis study is an ex ante assessment of the projected impacts of increasing olive oil exports under the EU-Lebanon AA, which permits Lebanon to export 1,000 tonnes of extra-virgin olive oil to the EU duty-free while allowing the country to impose a 70 per cent tariff rate on EU olive oil.

Lebanon does not currently take full advantage of the terms offered under the AA, exporting only 27 tonnes to the EU in 2005.2 In order to achieve the maximum increase in exports, certain policy measures will need to be implemented. A scenario analysis was carried out to determine the projected impacts (economic, social and environmental) of exporting the full quota of olive oil allowed under the EU-Lebanon Agreement and compared it to a “business as usual” baseline. Due to limited data availability, both qualitative and quantitative techniques were used in the analysis. A rapid cost-benefit analysis was also performed to assess the economic impacts using quantitative data found in the action plans funded by ELCIM.3

1.3.1 Scenario analysisTwo scenarios were defined as follows:

• Scenario 1 accepted the state of the olive oil sector as it currently stands, without policy measures to encourage increased duty-free exports to the EU.

• Scenario 2 assumed that needed olive oil quality improvements are made in Lebanon to take full advantage of the 1,000-tonne quota, once farmers and millers are shown the benefits of the improvements.

The scenario analysis was based on qualitative data compiled from comprehensive stakeholder consultations, focus group meetings, fieldwork and literature reviews.

1.3.2 Cost-benefit analysis A ‘rapid’ cost benefit analysis was carried out to assess the economic impacts using quantitative data from the ELCIM study which outlined 7 action plans to improve the quality and export potential of Lebanon’s olive oil.

2 For comparison, Lebanon exported 42 tonnes of virgin olive oil to the EU in 2004. 3 Daher S., Dragotta A., Gabr M. and Hammoud K. (2004) prepared these action plans for the Lebanese Inter-Professional Syndicate for the Olive Sector (LIPSOS). They were funded by The European Commission Delegation. These actions plan will be referred to as “ELCIM”.

�

1.4 Lebanon: A brief introduction Lebanon is a relatively small country with a diverse population of about 4 million inhabitants (including 17 different ethnic and religious communities). It is a Republic with 3 branches of government: the Legislative, the Executive, and the Judiciary with positions distributed among the different religious and sectarian groups (Euro-Med Partnership, 2002).

The Lebanese civil war spanned a period of 15 years (1975-1990), damaging the socio-economic conditions of Lebanese citizens and destroying most of the country’s infrastructure. Since the cessation of war in 1990, substantial progress has taken place in rehabilitating and expanding war-torn physical infrastructure. All major public services are operating again (although not very efficiently), including basic education and health care. Internal security is also restored. A sound banking system and a resilient small and medium-scale manufacturing sector have facilitated this economic recovery. Family remittances, banking services, exports and international aid are the main sources of foreign exchange.

The Government of Lebanon (GOL), however, still faces serious challenges. It has funded reconstruction by borrowing heavily, mostly from domestic banks. Debt stands currently at over US$37 billion, or over 167 per cent of annual GDP. In the meantime, it has not managed to privatize many of its inefficient public sector services. The servicing of the public debt and the relatively large portion of the national budget allocated to salaries and wages, along with known geo-political realities, have taken its toll on unemployment. Significant poverty and income disparities exist as the society is increasingly split between the very rich and the poor. According to the World Bank’s crude Living Condition Index which measures the degree of satisfaction with basic needs, 32 per cent of Lebanese households were at the low end of the index, 42 per cent were at the intermediate level while 26 per cent were at the high end.4 A UN study calculated that 35 per cent of the population lacked basic needs, i.e. they lived below a poverty line of minimum living standards.5 There are an estimated one million poor in Lebanon today, of whom 75 per cent are urbanized. Economic growth and reconstruction have favoured some regions, notably parts of the Beirut region, at the expense of large parts of the country. Growth has also favoured the services sectors over the more traditional labour-intensive activities in agriculture and industry.

Unemployment, officially given as 8 per cent, is at least double this figure according to some studies, and is highest amongst the young.6 Tight monetary policy, a narrow tax base and economic recession have led to declining real incomes of many salary earners. Illiteracy rates range from 11 per cent to 15 per cent (see forward to Table 4) in the more disadvantaged areas of the Bekaa, and South and North Lebanon, and is most grave amongst women (Kasparian, 2002).

Public welfare programmes and social safety nets, largely non-existent in Lebanon, are narrowly based, and often subject to mismanagement. Remittances from expatriates go some way to alleviating the situation amongst underprivileged communities. There is no national health care policy. The system favours equipment, curative and tertiary services driven by the supply of an abundant private sector, rather than primary health care and prevention (Euro-Med Partnership, 2002).

1.4.1 Agriculture and the agro-food industry in Lebanon Agriculture in Lebanon plays an important (albeit declining) role in the Lebanese economy, contributing 5.8 per cent of GDP (MOET, 2002), employing about 6.7 per cent of the total labour force (USJ, 2002)

4 Ministry of Social Affairs – UNDP Lebanon, 1998.5 ibid.6 CAS, 1997.

Introduct�on

�

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

% of GDP

�.�0

�.�0

�.�0

�.00

�.80

�.�0

�.�0

�997 �998 �999 �000 �00� �00�

Nature of crop product �997 �998 �999 �999 �99� �99�

Cereals 88.� �0�.� 9�.7 ��0.� �7�.0 ���.9

Legum�nous �0.� �0.� ��.8 ��.0 ��.� ��.�

vegetables

Vegetables ����.7 ����.� ���0.0 ��07.7 �07�.9 ��0�.�

Plants for ��9.7 ���.0 �8�.� ���.� �0.9 ��.�

manufactur�ng

Fru�ts ��0�.� 98�.7 �0��.0 899.� 8��.� 8��.�

Ol�ves 9�.� �0.� ��.� �89.� 8�.� �8�.�

Others ��.8 - - �9.� ��.� �9.8

Total ��00 �87� �8�9.� �78�.� ��0�.7 ����.�

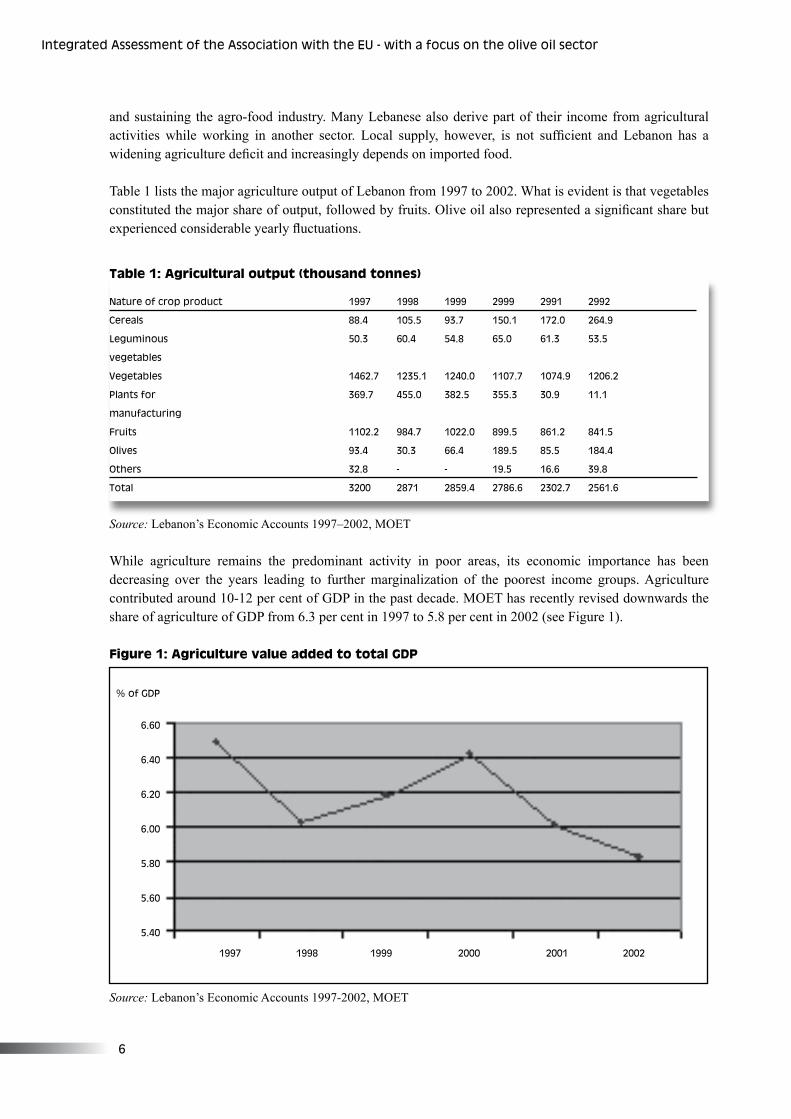

and sustaining the agro-food industry. Many Lebanese also derive part of their income from agricultural activities while working in another sector. Local supply, however, is not sufficient and Lebanon has a widening agriculture deficit and increasingly depends on imported food.

Table 1 lists the major agriculture output of Lebanon from 1997 to 2002. What is evident is that vegetables constituted the major share of output, followed by fruits. Olive oil also represented a significant share but experienced considerable yearly fluctuations.

Table 1: Agricultural output (thousand tonnes)

Source: Lebanon’s Economic Accounts 1997–2002, MOET

While agriculture remains the predominant activity in poor areas, its economic importance has been decreasing over the years leading to further marginalization of the poorest income groups. Agriculture contributed around 10-12 per cent of GDP in the past decade. MOET has recently revised downwards the share of agriculture of GDP from 6.3 per cent in 1997 to 5.8 per cent in 2002 (see Figure 1).

Figure 1: Agriculture value added to total GDP

Source: Lebanon’s Economic Accounts 1997-2002, MOET

7

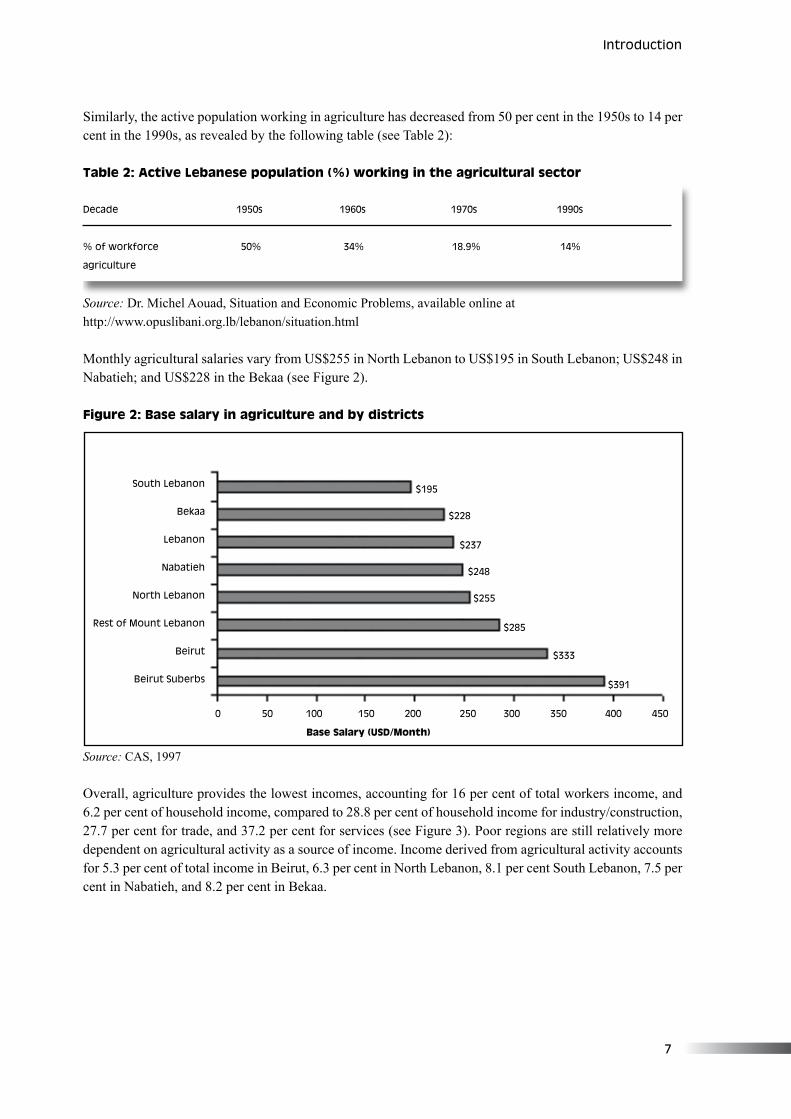

Similarly, the active population working in agriculture has decreased from 50 per cent in the 1950s to 14 per cent in the 1990s, as revealed by the following table (see Table 2):

Table 2: Active Lebanese population (%) working in the agricultural sector

Source: Dr. Michel Aouad, Situation and Economic Problems, available online at http://www.opuslibani.org.lb/lebanon/situation.html

Monthly agricultural salaries vary from US$255 in North Lebanon to US$195 in South Lebanon; US$248 in Nabatieh; and US$228 in the Bekaa (see Figure 2).

Figure 2: Base salary in agriculture and by districts

Source: CAS, 1997

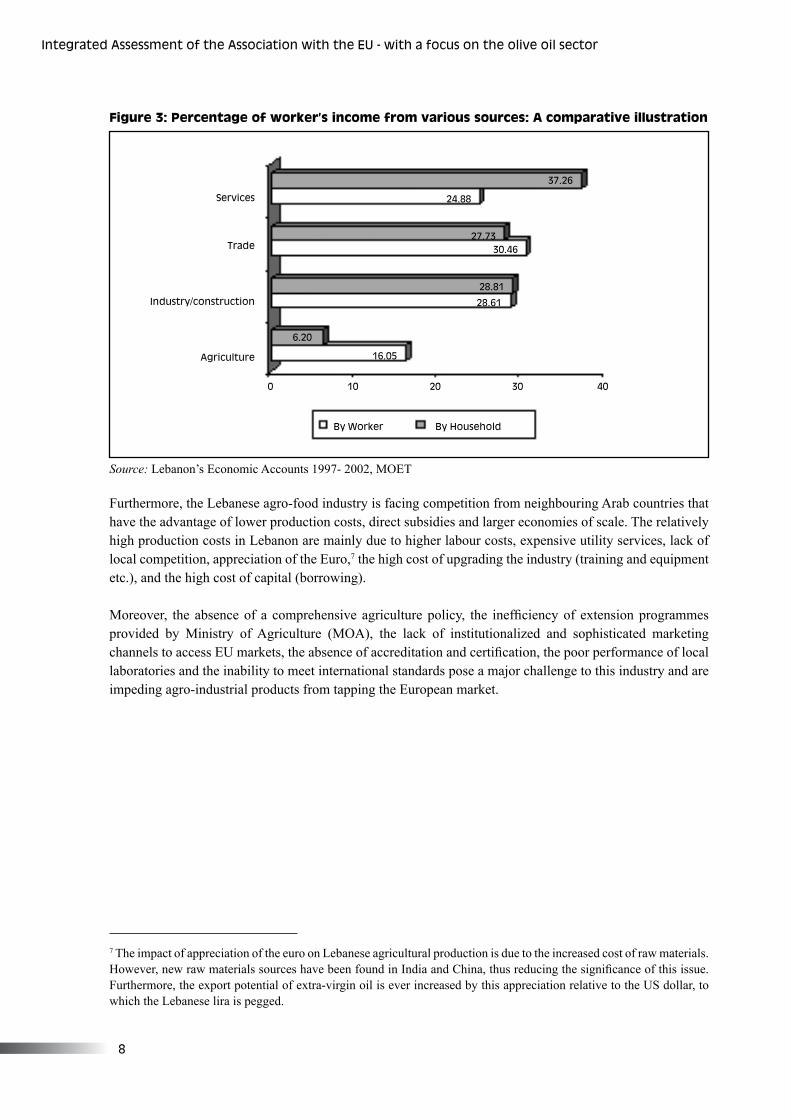

Overall, agriculture provides the lowest incomes, accounting for 16 per cent of total workers income, and 6.2 per cent of household income, compared to 28.8 per cent of household income for industry/construction, 27.7 per cent for trade, and 37.2 per cent for services (see Figure 3). Poor regions are still relatively more dependent on agricultural activity as a source of income. Income derived from agricultural activity accounts for 5.3 per cent of total income in Beirut, 6.3 per cent in North Lebanon, 8.1 per cent South Lebanon, 7.5 per cent in Nabatieh, and 8.2 per cent in Bekaa.

Decade �9�0s �9�0s �970s �990s

% of workforce �0% ��% �8.9% ��%

agr�culture

South Lebanon

Bekaa

Lebanon

Nabat�eh

North Lebanon

Rest of Mount Lebanon

Be�rut

Be�rut Suberbs

$�9�

$��8

$��7

$��8

$���

$�8�

$���

$�9�

0 �0 �00 ��0 �00 ��0 �00 ��0 �00 ��0

Base Salary (USD/Month)

Introduct�on

8

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Figure 3: Percentage of worker’s income from various sources: A comparative illustration

Source: Lebanon’s Economic Accounts 1997- 2002, MOET

Furthermore, the Lebanese agro-food industry is facing competition from neighbouring Arab countries that have the advantage of lower production costs, direct subsidies and larger economies of scale. The relatively high production costs in Lebanon are mainly due to higher labour costs, expensive utility services, lack of local competition, appreciation of the Euro,7 the high cost of upgrading the industry (training and equipment etc.), and the high cost of capital (borrowing).

Moreover, the absence of a comprehensive agriculture policy, the inefficiency of extension programmes provided by Ministry of Agriculture (MOA), the lack of institutionalized and sophisticated marketing channels to access EU markets, the absence of accreditation and certification, the poor performance of local laboratories and the inability to meet international standards pose a major challenge to this industry and are impeding agro-industrial products from tapping the European market.

Serv�ces

Trade

Industry/construct�on

Agr�culture

�7.��

��.88

�7.7� �0.��

�8.8�

�8.��

�.�0

��.0�

By Worker By Household

0 �0 �0 �0 �0

7 The impact of appreciation of the euro on Lebanese agricultural production is due to the increased cost of raw materials. However, new raw materials sources have been found in India and China, thus reducing the significance of this issue. Furthermore, the export potential of extra-virgin oil is ever increased by this appreciation relative to the US dollar, to which the Lebanese lira is pegged.

9

�. Trade l�beral�zat�on �n Lebanon

��,000.000

�0,000,000

8,000,000

�,000,000

�,000,000

�,000,000

-�997 �998 �999 �000 �00� �00� �00� �00� �00�

Total exports Total �mports

9,�9�,9�� 9,��9,8�9

7,��8,�98

�,���,77�

7,�9�,07�

�.�0�,���7,0��,�9�7,���,�7�

���,�8� ��0,9�9 �7�,777 7��,��� 889,�99 �,0��,�9��,���,9�� �,7�7,0�9 �,879,7��

�.��7,9�0

The Lebanese Government is a strong advocate of trade liberalization. A number of trade agreements have been agreed bilaterally and regionally, for example the Association Agreement with Europe (AA), the European Neighbourhood Policy and the Greater Arab Free Trade Area (GAFTA), as well as multilateral mechanisms such as the expected accession to the World Trade Organization (WTO) in 2006.

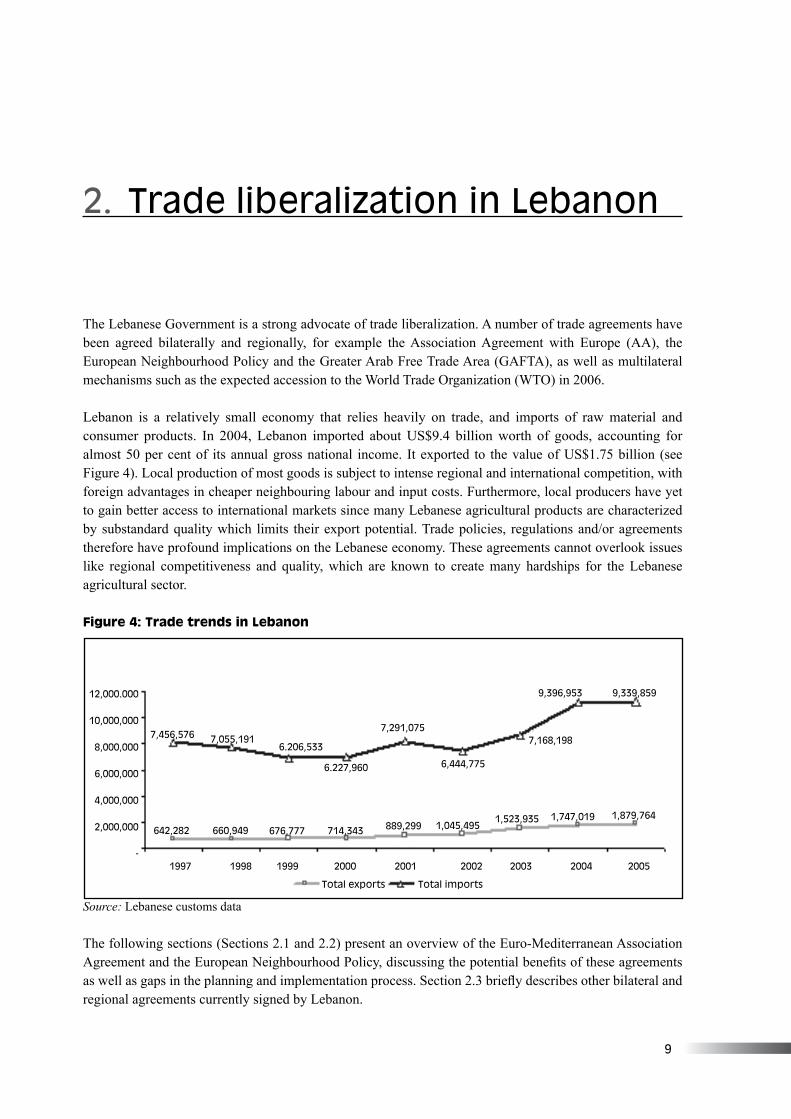

Lebanon is a relatively small economy that relies heavily on trade, and imports of raw material and consumer products. In 2004, Lebanon imported about US$9.4 billion worth of goods, accounting for almost 50 per cent of its annual gross national income. It exported to the value of US$1.75 billion (see Figure 4). Local production of most goods is subject to intense regional and international competition, with foreign advantages in cheaper neighbouring labour and input costs. Furthermore, local producers have yet to gain better access to international markets since many Lebanese agricultural products are characterized by substandard quality which limits their export potential. Trade policies, regulations and/or agreements therefore have profound implications on the Lebanese economy. These agreements cannot overlook issues like regional competitiveness and quality, which are known to create many hardships for the Lebanese agricultural sector.

Figure 4: Trade trends in Lebanon

Source: Lebanese customs data

The following sections (Sections 2.1 and 2.2) present an overview of the Euro-Mediterranean Association Agreement and the European Neighbourhood Policy, discussing the potential benefits of these agreements as well as gaps in the planning and implementation process. Section 2.3 briefly describes other bilateral and regional agreements currently signed by Lebanon.

�0

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Source: Author’s elaboration

Under the AA, the liberalization of trade of European imports to Lebanon will occur after 5 years from signing (beginning in 2007) and will take 12 years for total liberalization to come into force (in 2014). On the other hand, Lebanon has managed to ensure duty-free protection for its own agricultural products entering EU markets (with the exception of a small list of products still under quotas or tariffs).9 Lebanon will still impose a 70 per cent tariff on olive oil and 15 per cent on other oils derived from olives. Other highlyprotected items are meat and fruits (50 per cent tariff) and milk and fresh cheese (30 per cent).

Within the interim period, this asymmetric liberalization in favour of Lebanese commodities should confer higher comparative advantages on the olive oil sector. However Lebanon has so far not been able to capture these advantages due to the absence of conformity with international quality standards and the inability to increase and sustain production. This reality is not only true of the olive oil sector, but also most agricultural sub-sectors. To increase exports, Lebanon will need to improve product quality, reduce production costs to compete regionally and sustain output. The potential benefits of tariff reduction include:

• A reduction in transaction costs due to reduction and harmonization of tariffs and regulations across all EU countries.

• Upgrading of domestic quality, sanitary and labelling requirements in order to comply with export requirements of the EU.

• Access to a larger pool of countries.

1995

Barcelona

Conference

• Assoc�at�on

Agreement

s�gnature

• Ratification by

the Lebanese

Parl�ament

2002 2003

�-year Inter�m

Agreement

�n effect

• EU enlargement

• European

Ne�ghbourhood

Pol�cy

2004

Launched negot�at�ons

and act�on plan for ENP

�n Lebanon

2005

8 In the Declaration, the Euro-Med countries agreed to establish a comprehensive partnership through strengthened political dialogue, development of economic and financial cooperation, and greater emphasis on social, cultural and human dimensions.9 EU maintains high tariff rates on three “sensitive” items: cut flowers and flower buds; sugar beet and chemical sucrose; and wine of fresh grapes.

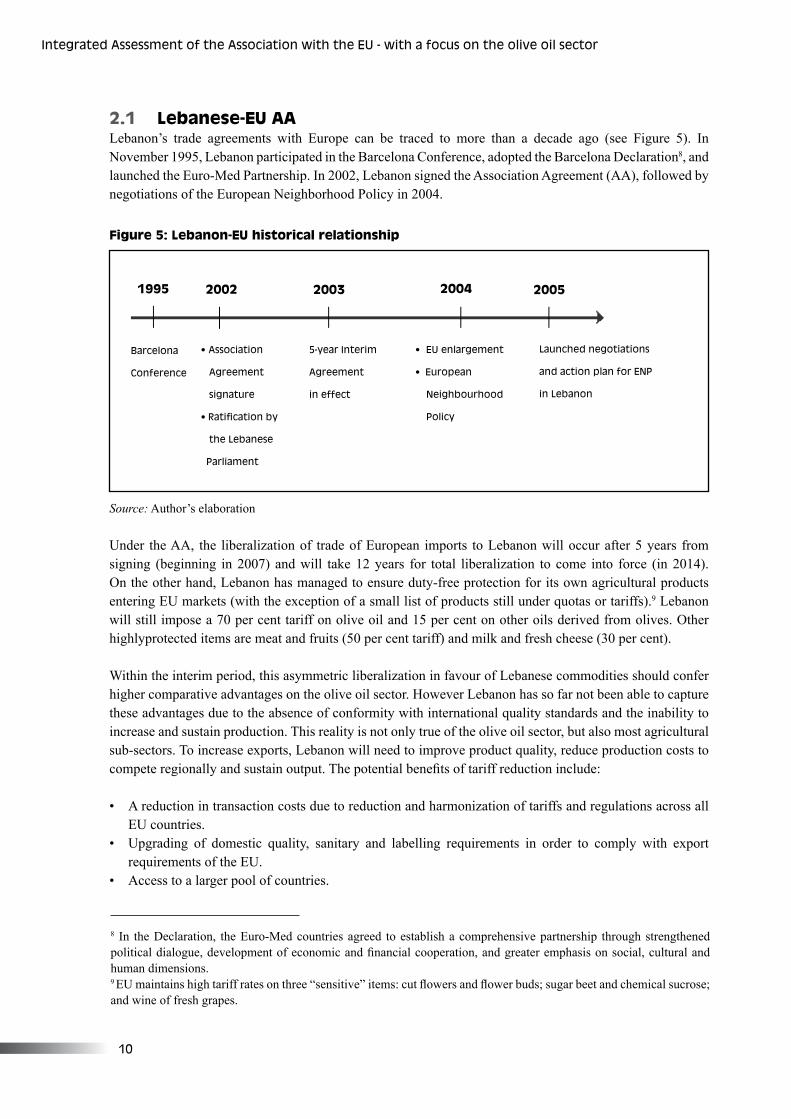

2.1 Lebanese-EU AA Lebanon’s trade agreements with Europe can be traced to more than a decade ago (see Figure 5). In November 1995, Lebanon participated in the Barcelona Conference, adopted the Barcelona Declaration8, and launched the Euro-Med Partnership. In 2002, Lebanon signed the Association Agreement (AA), followed by negotiations of the European Neighborhood Policy in 2004.

Figure 5: Lebanon-EU historical relationship

��

For the Lebanese economy, the AA constitutes an important milestone in the development of a more dynamic trade and economic partnership with the EU. The agreement will help Lebanon realize a greater part of its export potential. Furthermore, Lebanon will benefit from technology transfer and EU know-how resulting from foreign direct investments as well as from technical and financial cooperation projects. The agreement is expected to help strengthen the Lebanese economy and serve as a catalyst for reform.

The implementation phase of the AA has increasingly involved key stakeholders through a series of mise-à-niveau workshops and projects aimed at maximizing the benefits of trade liberalization. The projects address the quality of exported goods, consumer protection, intellectual property rights, upgrading, small and medium enterprise, and rules of origin aimed at facilitating trade.

For olive oil, the AA should increase the incentive of farmers, mill operators and traders to meet international standards and compete in foreign markets. There is now greater potential for high quality Lebanese olive oil to enter niche markets in Europe and other regions in the world (North America and Australia). Because trade liberalization is unilateral, Lebanon should take this opportunity to develop its olive oil sector. From olive growers to millers, wholesalers, retailers, exporters, and consumers, the AA is an opportunity for a new production dynamic with good agricultural practices, pricing incentives, and local and regional economic development.

Improving the quantity and quality of olive oil supply will require the labour force to be educated on better agricultural practices, technology where applicable (e.g. pruning machinery), and coordination between farmers and mill operators. Socially, the AA offers a multifaceted framework for social and cultural cooperation. It aims at promoting social security, healthcare systems and the empowerment of women. The projects major issue addressed in the AA is the improvement of labour relations and work conditions. Moreover, many EU funded projects aim at improving poverty reduction in Lebanon’s most deprived regions, which will contribute to improving living conditions in rural areas.

Environmentally, the AA seeks to protect water quality in the Mediterranean Sea and manage water resources. The agreement entails specific policies oriented towards improving wastewater treatment facilities, reducing industrial pollution, raising environmental awareness and developing a sound environmental policy.

Throughout the negotiation process of the AA, the Government of Lebanon engaged the main agro-food stakeholders through regular consultations as well as direct involvement in the negotiation process. Moreover, the Government now promotes the agro-food sector in foreign markets through export fairs and involves delegations in events aimed at facilitating market access to Lebanese products.

However, the following gaps in the planning process have been identified:

• When assessing the impact of trade liberalization on the economy, the social and environmental dimensions were overlooked, resulting in an absence of accompanying measures to address those concerns.

• Follow-up consultations with the private sector are not regular.

• The dissemination of information needs to be improved, including a need to clarify the EU regulations on agro-food export for producers.

• There is an absence of monitoring and assessment of the initial impact of trade liberalization on the agro-food industry.

Trade l�beral�zat�on �n Lebanon

��

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

• Regulatory and lengthy bureaucratic procedures have led to delays in technical assistance aimed at facilitating trade through upgrading programmes.

• There is a lack of financial incentives and other necessary measures to address private sector requirements, hindering the efficiency of the AA policy.

2.2 European Neighbourhood Policy (ENP) The enlargement of the EU (with the entry of ten new countries in May 200410) created opportunities, posed challenges and affected Europe’s geopolitical relations with its neighbours, including Lebanon. There was no doubt that enlarging the EU would increase diversity and bring with it a different outlook on important issues such as labour market policies and trade agreements (with non-EU members). This would necessitate an efficient decision-making and governance mechanism that would ensure that “more” did not mean “less”. Hence the ENP was developed to address this new reality and build upon existing cooperation with Mediterranean partners. The EU has proposed a new and developed mechanism to govern its relations with its immediate ring of neighboring countries, and is also offering a stake in its internal market in return for closer integration and harmonization.

The ENP policy, first outlined by the European Commission in its Communication on Wider Europe in March 2003, demonstrates the high priority that the EU accords to future relations with its neighbours. Substantially increased financial assistance and a single dedicated European Neighbourhood and Partnership Instrument support implementation of this policy. The ENP’s objective (implemented through country Action Plans) is to share the benefits of the enlargement with neighbouring countries for the benefit of all parties concerned. It is designed to prevent the emergence of new dividing lines between the enlarged EU and its neighbours and offer greater political, security, economic and cultural cooperation.11 The Lebanese Government has officially welcomed the ENP for deepening of bilateral and regional integration.

The method to implement the ENP is to define with each partner country a national set of priorities, whose fulfillment will bring them closer to the EU without offering membership. These priorities are incorporated in jointly agreed Action Plans. These action plans build on mutual commitment to common values such as the rule of law, good governance, the respect of human rights, and the promotion of market economy and sustainable development. Engagement is introduced progressively and is conditional on mutually agreed targets for reform. Action Plans are revised approximately every 3 years and progress is monitored through a set of benchmarking indices, to ensure consistent approaches.

While the historic relationship between Lebanon and the EU has been strengthened by the AA, the ENP will bring about considerable value in all aspects of sustainable development. The ENP stands to offer Lebanon an even larger window of opportunities. It is expected to:

• Offer a higher stake in the EU internal market• Upgrade the scope and the intensity of political cooperation• Harmonize economic legislation and eliminate all trade barriers• Increase financial support, including infrastructure investment support through the European Investment

Bank (EIB)• Provide technical assistance

10 Poland, Czech Republic, Slovakia, Hungry, Latvia, Lithuania, Estonia, Cyprus, Malta and Slovenia. 11 Available from: http://europa.eu.int/comm/world/enp/policy_en.htm.

��

• Develop the transport, energy and information society sectors and networks• Strengthen cooperation in science and technology.12

The Mesures d’Accompagnement (MEDA) programme is the main financial assistance instrument for Mediterranean partner countries to implement the Partnership and Action Plans. As of 2007, a new financial instrument will be created amalgating all existing instruments. The new European Neighborhood Instrument (ENI) will build on existing cross-border programmes such as partnership, multi-annual programming and co-financing. Its main elements will be the promotion of sustainable development; coordinating action against common challenges such as environment, public health and the prevention and fight of organized crime; ensuring efficient and secure common borders; and promoting exchanges. The planning process for ENP is in its early stages at the time of writing.

2.3 Other trade agreements Two other major trade agreements are important to Lebanon:

• Greater Arab Free Trade Area (GAFTA). GAFTA was launched to promote a free trade area among 17 Arab countries, and was implemented in January 2005. All other non-trade barriers (administrative, quotas and monetary) are eliminated through the GAFTA agreement. Agro-food products are duty-free, but must meet standards of quality, certification and administration required of GAFTA. Lebanese exports to the EU (through the AA) are heavily influenced by the implications of trade liberalization with GAFTA. The competition faced by domestic producers of olive oil is crippling, and therefore weakens the capacity and incentive to export to the EU. The need to survive has led domestic producers to undertake severe cost minimizing strategies, often undercutting the quality of the olive oil and thus the credentials to enter the highly taste and certification-conscious EU markets.

• World Trade Organization (WTO). In February 1999, the Lebanese Government submitted its application for accession to the WTO. Since then MOET has led the negotiations by formulating a masterplan for accession and establishing a department to supervise the process expected to take shape at end of 2006.

12 Available from: http://www.dellbn.cec.eu.int/en/pev/information.htm.

Trade l�beral�zat�on �n Lebanon

��

�. Overv�ew of ol�ve o�l product�on �n Lebanon

The olive oil sector was selected for analysis because it remains an important economic and cultural, not to mention traditional, activity in many regions in Lebanon. Each region in Lebanon prides itself on indigenous olive trees and therefore a distinct type of olive oil. The environment (soil, altitude, climate and cultural practices) also produces special characteristics and tastes distinct to each region. Farmers favour olive tree growing because it does not require much management and day-to-day care once the seedlings are established, and also no irrigation since most areas under cultivation are rain-fed. Therefore, olive oil production is often associated with regions with poor access to water.13

Olive oil in Lebanon is mostly a family run and seasonal business, contributing a considerable proportion of household family activity and income. Families take great pride when they sell their olive oil, when the oil is processed into soap bars, or when the pomace14 is sold for heating purposes. The production process has three stages: olive farming/harvesting, milling and marketing. Figure 6 illustrates the olive oil supply chain.

13 Irrigation schemes are recommended as the dry season is getting longer. 14 Residue from the milling process.

��

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Figure 6: Production chain and respective stakeholders

Source: MOET

The growing world demand for ethnic and health-oriented food products has allowed Lebanese olive oil to make inroads into international markets and occupy niche positions, although supply has not increased to take full advantage of the demand. Moreover, many important socio-economic implications related to olive oil production have been identified, including the participation of women and minority groups in the labour force, rural-urban migration, and poverty alleviation.

3.1 Socio-economic characteristics of olive producers Olive oil producers in Lebanon face a similar socio-economic situation to other workers in agriculture in the rural areas of Lebanon (including in Greater Beirut, Mount Lebanon and the districts of Kesrouan, Metn, Baabda and Aley; see Map 1). This situation can be best understood by examining indicators of poverty, education attainment and migration.

Olive harvesting

OLEICULTURE

STAKEHOLDERS

- Landowners:

Small/large

orchard owners

- Farmers:

Full/part-time

workers

- Women:

Permanent,

seasonal, or

family

- Foreign labor

- Youth

Milling process

INDUSTRY

STAKEHOLDERS

- Mill owners

- Employees

- Equipment

Suppliers

Local & International

MARKETING

STAKEHOLDERS

- Bottling and

Labelling

- Wholesalers

- Retailers

- Exporters

- Consumers

�7

Map 1: Geographic distribution of olive cultivation areas

Source: FAO – MOA (2000)

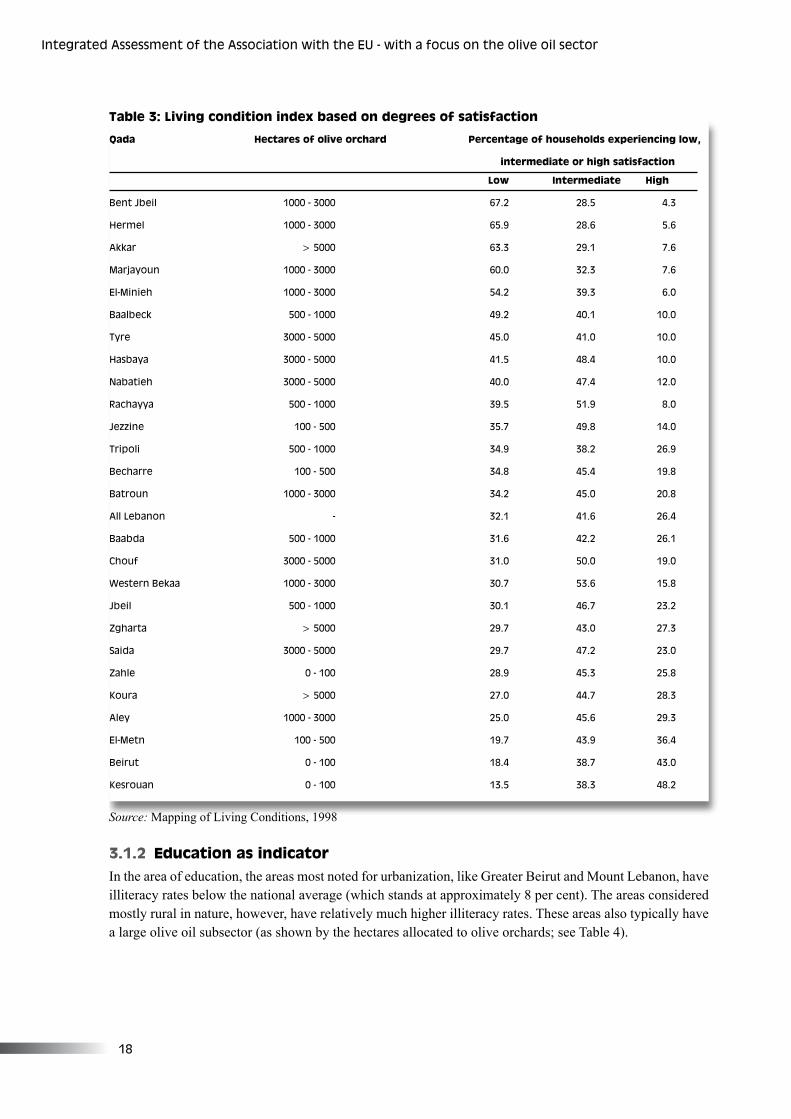

3.1.1 Poverty as indicatorWhen it comes to poverty, as measured by the Living Condition Index15 (LCI), regions with activities in olive tree and/or are relatively rural appear to have comparatively lower rates of basic needs satisfaction (see Table 3).

15 The LCI is an overall index to measure satisfaction of basic needs for households and individuals. The index has five classifications of satisfaction, here reduced to three - low, intermediate and high. It is used to evaluate fields such as housing, water and sewerage, education and income (Mapping of Living Conditions, 1998)

Overv�ew of ol�ve o�l product�on �n LebanonOverv�ew of ol�ve o�l product�on �n Lebanon

�8

Integrated Assessment of the Assoc�at�on w�th the EU - w�th a focus on the ol�ve o�l sector

Qada Hectares of olive orchard Percentage of households experiencing low,

intermediate or high satisfaction

Low Intermediate High

Bent Jbe�l �000 - �000 �7.� �8.� �.�

Hermel �000 - �000 ��.9 �8.� �.�

Akkar > �000 ��.� �9.� 7.�

Marjayoun �000 - �000 �0.0 ��.� 7.�

El-M�n�eh �000 - �000 ��.� �9.� �.0

Baalbeck �00 - �000 �9.� �0.� �0.0

Tyre �000 - �000 ��.0 ��.0 �0.0

Hasbaya �000 - �000 ��.� �8.� �0.0

Nabat�eh �000 - �000 �0.0 �7.� ��.0

Rachayya �00 - �000 �9.� ��.9 8.0

Jezz�ne �00 - �00 ��.7 �9.8 ��.0

Tr�pol� �00 - �000 ��.9 �8.� ��.9

Becharre �00 - �00 ��.8 ��.� �9.8

Batroun �000 - �000 ��.� ��.0 �0.8

All Lebanon - ��.� ��.� ��.�

Baabda �00 - �000 ��.� ��.� ��.�

Chouf �000 - �000 ��.0 �0.0 �9.0

Western Bekaa �000 - �000 �0.7 ��.� ��.8

Jbe�l �00 - �000 �0.� ��.7 ��.�

Zgharta > �000 �9.7 ��.0 �7.�

Sa�da �000 - �000 �9.7 �7.� ��.0

Zahle 0 - �00 �8.9 ��.� ��.8

Koura > �000 �7.0 ��.7 �8.�

Aley �000 - �000 ��.0 ��.� �9.�

El-Metn �00 - �00 �9.7 ��.9 ��.�

Be�rut 0 - �00 �8.� �8.7 ��.0

Kesrouan 0 - �00 ��.� �8.� �8.�

Table 3: Living condition index based on degrees of satisfaction

Source: Mapping of Living Conditions, 1998

3.1.2 Education as indicatorIn the area of education, the areas most noted for urbanization, like Greater Beirut and Mount Lebanon, have illiteracy rates below the national average (which stands at approximately 8 per cent). The areas considered mostly rural in nature, however, have relatively much higher illiteracy rates. These areas also typically have a large olive oil subsector (as shown by the hectares allocated to olive orchards; see Table 4).

�9

Mohafazat Men (%) Women (%) Total (%) Hectares of olives orchards

Rest of mount Lebanon �.7 �.� �.� 0 to �000

Be�rut �.� �.7 �.7 0 to �00

Be�rut suburbs �.9 8.� �.� 0 to �00

Lebanon (Average) �.� �0.9 8.0 -

South Lebanon 7.� ��.� �0.0 �00 to �000

Bekaa �.8 ��.� �0.� �00 to �000

North Lebanon 7.8 ��.0 �0.9 �,000 to > �,000

Nabat�eh 7.8 ��.0 ��.9 �,000 to �,000

Men (%) Women (%) Total (%)

Nabat�eh �9.� ��.� ��.�

South Lebanon �0.� ��.� ��.�

Rest of Mount Lebanon �7.� ��.� ��.�

Bekaa ��.� ��.� �9.0

Be�rut �7.� �7.0 �9.�

Be�rut Suburbs �0.� ��.� ��.�

Total ��.� ��.� �7.�

16 Kasparian, 2003.

Table 4: Illiteracy rates in Lebanon, 2001 (10 years of age and more)

Source: USJ, 2002

3.1.3 Employment and migration as indicatorsThe national unemployment rate in Lebanon is 8 per cent. Official unemployment rates in Northern Lebanon, Southern Lebanon, Nabatieh and the Bekaa are 11.10 per cent, 7.40 per cent, 6.30 per cent and 10.10 per cent respectively (CAS, 1998) and are the highest in the country. Unofficially, however, all unemployment rates are thought to be at least twice their official estimates.

Migration patterns, on the other hand, are closely linked to employment opportunities, as people move to the cities to find work and improve their financial situation. Table 5 shows the results of a survey (USJ, 2002) undertaken in the various regions of Lebanon on the intentions of the youth to migrate. Migration intentions, the survey showed, were high throughout the country, and not only in rural regions, but even in the relatively better off areas of Beirut, and Mount Lebanon. Poverty and unemployment opportunities in rural regions have exacerbated rural-urban migration and poverty belts around cities, especially Beirut. Overcrowded, these urban areas become over-supplied with job-seeking individuals and thus the migration intentions of youths (to other countries) remain high.

Table 5: Youth migration intentions

Source: Kasparian, 2002