30

Financial Engineering Lecture 1

| Date post: | 19-Dec-2015 |

| Category: |

Documents |

| View: | 220 times |

| Download: | 4 times |

Financial EngineeringLecture 1

Introduction Syllabus Class Format

Part 1 - Generic Derivatives & OptionsPart 2 - Futures, Swaps, MBS

Grade Assignments/Projects Option Programs Exam-Computations Email

Derivatives are financial instruments whose price and value derive from the value of the underlying assets or other variables (ISDA)

Derivatives are a “zero sum game”

Derivatives Definition

1840s Midwest USA farmers 1848 Chicago Board of Trade (CBOT) for

grain 1874 Chicago Produce Exchange for

butter/eggs 1919 Chicago Mercantile Exchange (CME) Risk management Land options Risk management

History of Derivatives

OTC vs. Exchanges

Eurex (E-X) Chicago Board Options Exchange (CBOE) Chicago Mercantile Exchange (CME) Chicago Board of Trade (CBOT) New York Mercantile Exchange (NYMEX) Hong Kong Futures Exchange (HKFE)

Derivative Markets

Source: Bank for International Settlements

Source: WFE/IOMA Derivatives Market Survey 2012

Source: WFE/IOMA Derivatives Market Survey 2012

Source: WFE/IOMA Derivatives Market Survey 2012

Futures Options / Warrant Future options Swaps Mortgage backed securities Forward Rate Agreement Convertible bonds Real options

Derivative Instruments

Stocks (example) Bonds Indices Commodities (examples for metal and ag.) Currencies Weather Carbon emissions Radio bandwidth

Underlying Assets

Arbitrage Speculation Hedging

Derivative Uses

Derivatives Call option Put option Exercise or Strike Price Expiration, Exercise, or Maturity Date Long position Short position

Charting Derivatives

Futures & Forwards Forward Contract Futures Contract-commodities-indexes-interest rates-exchange rates

Swaps An agreement between two firms in

which each firm agrees to exchange (or Swap) the “interest rate characteristics” of two different financial instruments of identical principal.

TypesInterest Rate SwapsCurrency Swaps

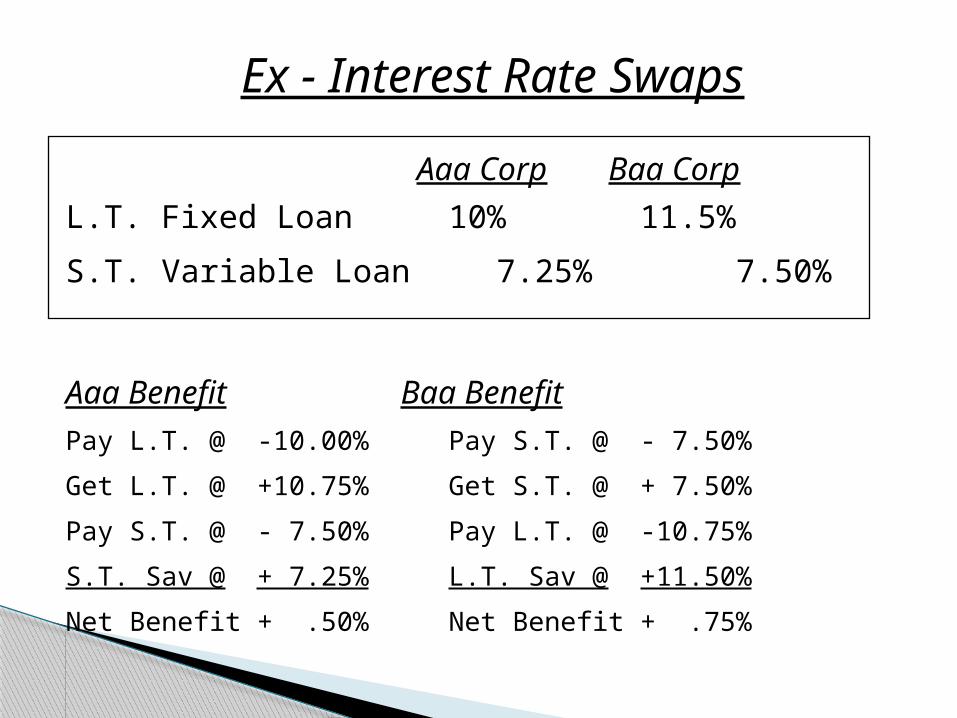

Ex - Interest Rate Swaps

Aaa Corp Baa Corp

L.T. Fixed Loan 10% 11.5%

S.T. Variable Loan 7.25%7.50%

Swap

Aaa Corp Borrows $1mil fixed loan @ 10%

BAA Corp Borrows $1mil variable loan @ 7.5%

Aaa assumes pmts on variable loan at 7.5%

Baa assumes pmts on fixed loan @ 10.75%

Aaa Benefit Baa BenefitPay L.T. @ -10.00% Pay S.T. @ - 7.50%

Get L.T. @ +10.75% Get S.T. @ + 7.50%

Pay S.T. @ - 7.50% Pay L.T. @ -10.75%

S.T. Sav @ + 7.25% L.T. Sav @ +11.50%

Net Benefit + .50% Net Benefit + .75%

Ex - Interest Rate Swaps

Aaa Corp Baa Corp

L.T. Fixed Loan 10% 11.5%

S.T. Variable Loan 7.25%7.50%

Mortgage Backed Securities FMAC GNMA

Options

Read McMillan glossary for terminology

IBMSept80CallStock = IBMExpiration Date = 3rd Friday in Sept

(Saturday)Position = Long call Strike Price = $80# of shares = 100

IBMSept80Call is selling for $5Total Cost = 5 x 100 + commissions = $500 +

Options

“In The Money” “Out of The Money”

Ex. IBMSept45Call

Options

45 50

“In The Money” “Out of The Money”

Ex. IBMSept50Put

Options

45 50

Intrinsic Value = P - E

Premium = Option price

Time Premium = O + E - P

Options

Ex. IBMSept60CallPrice = 65Call = 7Strike = 60

Intrinsic Value = 65 - 60 = 5Premium = 7Time Value Premium = 7 + 60 - 65 = 2

Options

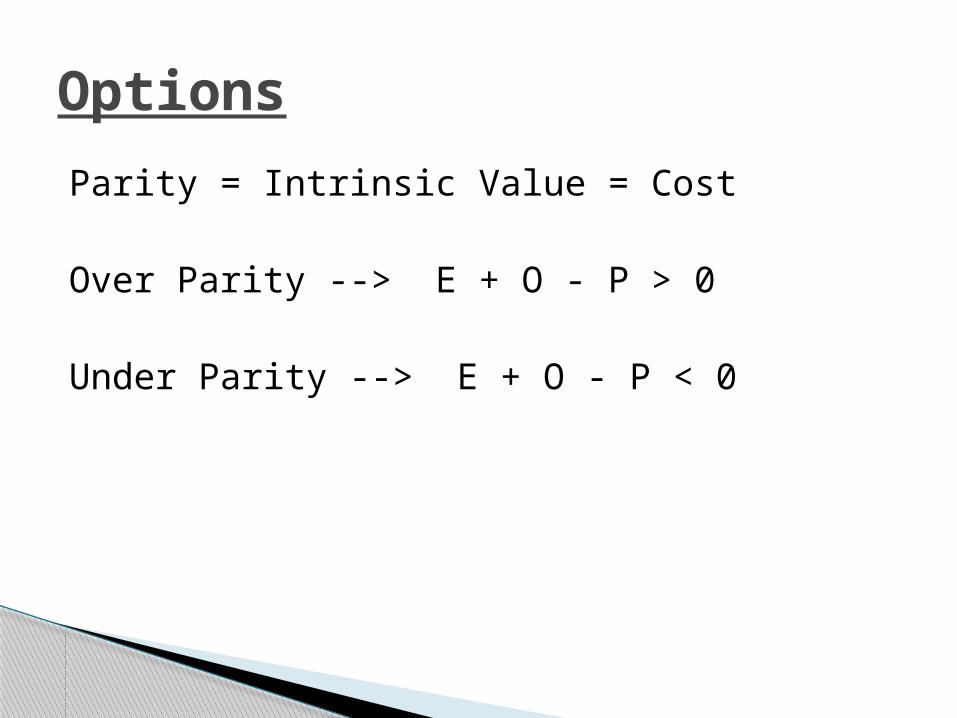

Parity = Intrinsic Value = Cost

Over Parity --> E + O - P > 0

Under Parity --> E + O - P < 0

Options

Factors in Option Price1. Stock price2. Strike price3. Time to expiration4. Volatility & distribution5. Risk free rate6. Dividends

Options

Cross Section Pricing

Intrinsic Value

Options

Option Price

Stock Price

Cross Section Pricing / Time Decay Chart

Intrinsic Value

Options

Option Price

Stock Price

Interest Rates Settlement Projects Computer software

Options