Page 1

Taxation of Malaysia Lecture 2: Residence Status

2013

Table of Contents

Determination of residence status............................................................................................2

Section 7(1)(a)......................................................................................................................2

Section 7(1)(b)......................................................................................................................5

Section 7(1)(c)....................................................................................................................12

Section 7(1)(d)....................................................................................................................15

Section 7(1B)......................................................................................................................17

Section 8.............................................................................................................................21

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 1 | P a g e

Page 2

Taxation of Malaysia Lecture 2: Residence Status

2013

Determination of residence status

Generally, the resident status of an individual for a basis year for a year of assessment is

determined by reference to the physical presence of that individual in Malaysia and

not by his nationality or citizenship.

In certain situations, the physical presence for the basis years preceding and following a

particular year of assessment has also to be taken into consideration in determining the

residence status of an individual.

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 2 | P a g e

Section 7 and 8 deal with residence status of

individual and body of persons or companies.

Section 7(1)(a)If he is in Malaysia for a period or periods amounting to at least 182 days:

The period or periods need not be continuous He must be physically present in Malaysia

Example 1:

Explanation:

Page 3

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 3 | P a g e

Section 7(1)(a) cont’d

Example 2:

Example 3

Page 4

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 4 | P a g e

Section 7(1)(a) cont’d

Example 3 cont’d.

Explanation:

Page 5

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 5 | P a g e

Section 7(1)(b)The individual is in Malaysia for that basis year for a period of less than 182 days but that

period is linked by or to another period of 182 or more consecutive days in the

immediately preceding or following basis year respectively.

Basically this involves two periods, a shorter one of less than 182 days adjoining a

longer period of 182 or more continuous days.

However the proviso to Section 7(1)(b) grants a concession in that temporary absences

in respect of the following are ignored and the individual is deemed to be present in

Malaysia:

o Connected with his service in Malaysia and owing to service matters or attending

conferences or seminars or study abroad;

o Owing to ill-health involving himself or a seminar of his immediate family; or

o Social visits not exceeding a total of 14 days. Social visits include any form of

vacation outside Malaysia besides vacation to home country.

The provision is applicable to the “period of less than 182 days” or “period of 182 or

more consecutive days period” as the case may be, if he is in Malaysia immediately prior

to and after that temporary absence

Example 4:

Page 6

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 6 | P a g e

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 4 cont’d:

Explanation:

Example 5:

Page 7

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 7 | P a g e

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 5 cont’d:

Explanation: Kim was a non-resident in Malaysia for the basis year for the year of assessment 2011 because she was not physically present in Malaysia in 2011.

Example 6: The facts are the same as in Example 5 except that Kim returned to Malaysia on 4.1.2011.

Page 8

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 8 | P a g e

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 6: The facts are the same as in Example 5 except that Kim returned to Malaysia on 4.1.2011.

Explanation:

Page 9

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 9 | P a g e

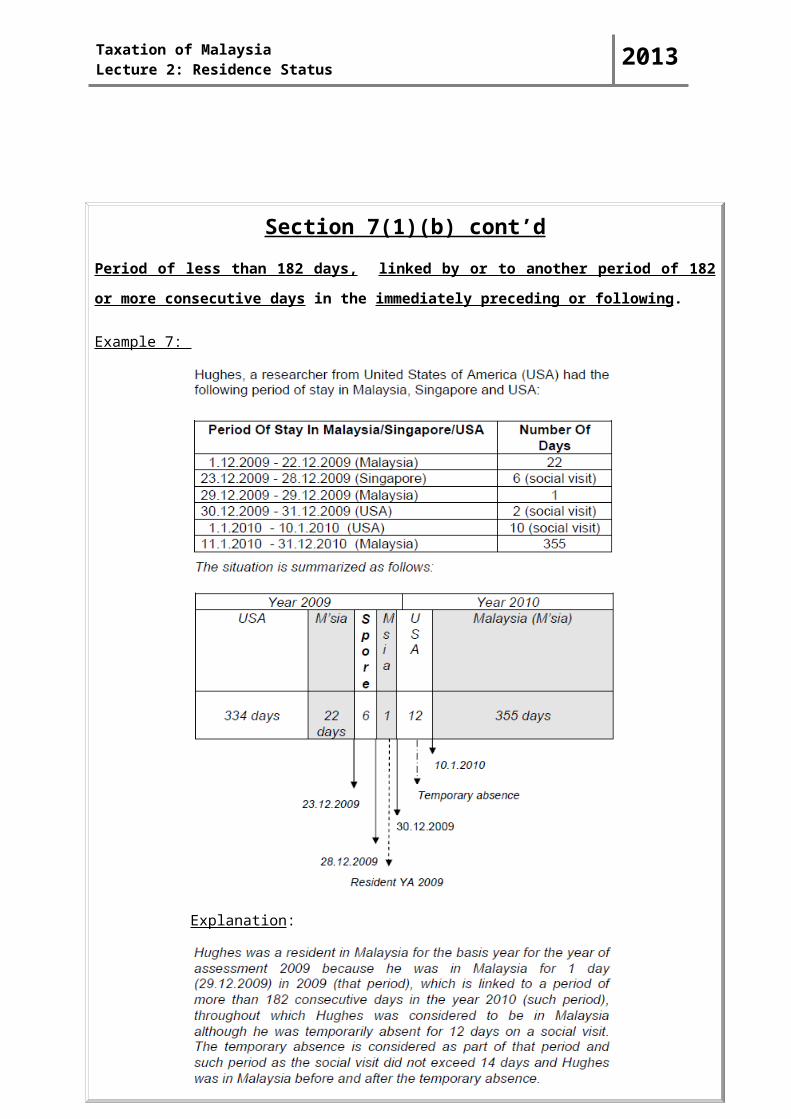

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 7:

Explanation:

Page 10

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 10 | P a g e

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 8:

Explanation:

Page 11

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 11 | P a g e

Section 7(1)(b) cont’d

Period of less than 182 days, linked by or to another period of 182 or more consecutive

days in the immediately preceding or following.

Example 9: The facts as in Example 8 except that Takayama left Malaysia on 17.12.2009 and returned to Malaysia on 1.1.2010.

Explanation:

Page 12

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 12 | P a g e

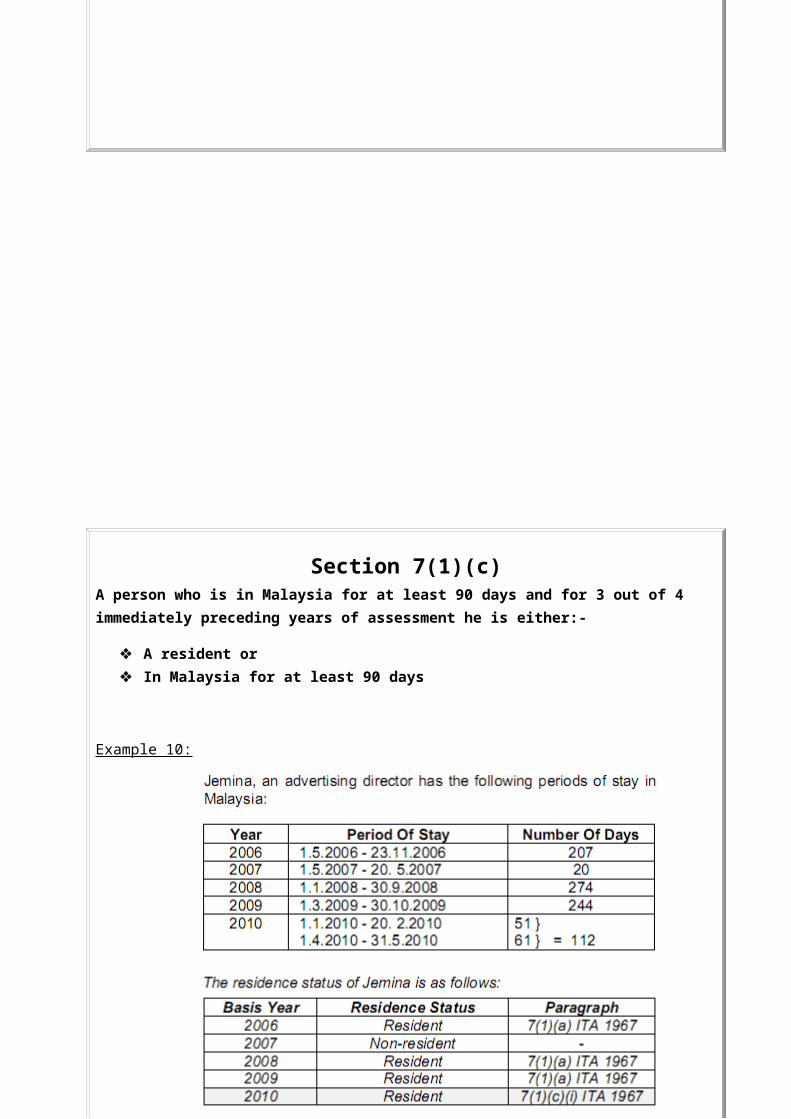

Section 7(1)(c)A person who is in Malaysia for at least 90 days and for 3 out of 4 immediately preceding years of assessment he is either:-

A resident or In Malaysia for at least 90 days

Example 10:

Explanation:

Page 13

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 13 | P a g e

Section 7(1)(c) cont’d

A person who is in Malaysia for at least 90 days and for 3 out of 4 immediately preceding years of assessment he is either:-

A resident or In Malaysia for at least 90 days

Example 11:

Explanation:

Page 14

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 14 | P a g e

Section 7(1)(c) cont’d

A person who is in Malaysia for at least 90 days and for 3 out of 4 immediately preceding years of assessment he is either:-

A resident or In Malaysia for at least 90 days

Example 12:

Explanation:

Page 15

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 15 | P a g e

Section 7(1)(d)A person will be considered a resident in any basis year as long as he is resident for:-

3 immediately preceding years of assessment; and The immediately following year of assessment.

Example 13:

Explanation:

Page 16

Taxation of Malaysia Lecture 2: Residence Status

2013

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 16 | P a g e

Section 7(1)(d) cont’d

A person will be considered a resident in any basis year as long as he is resident for:-

3 immediately preceding years of assessment; and The immediately following year of assessment.

Example 14:

Explanation:

Page 17

Taxation of Malaysia Lecture 2: Residence Status

2013

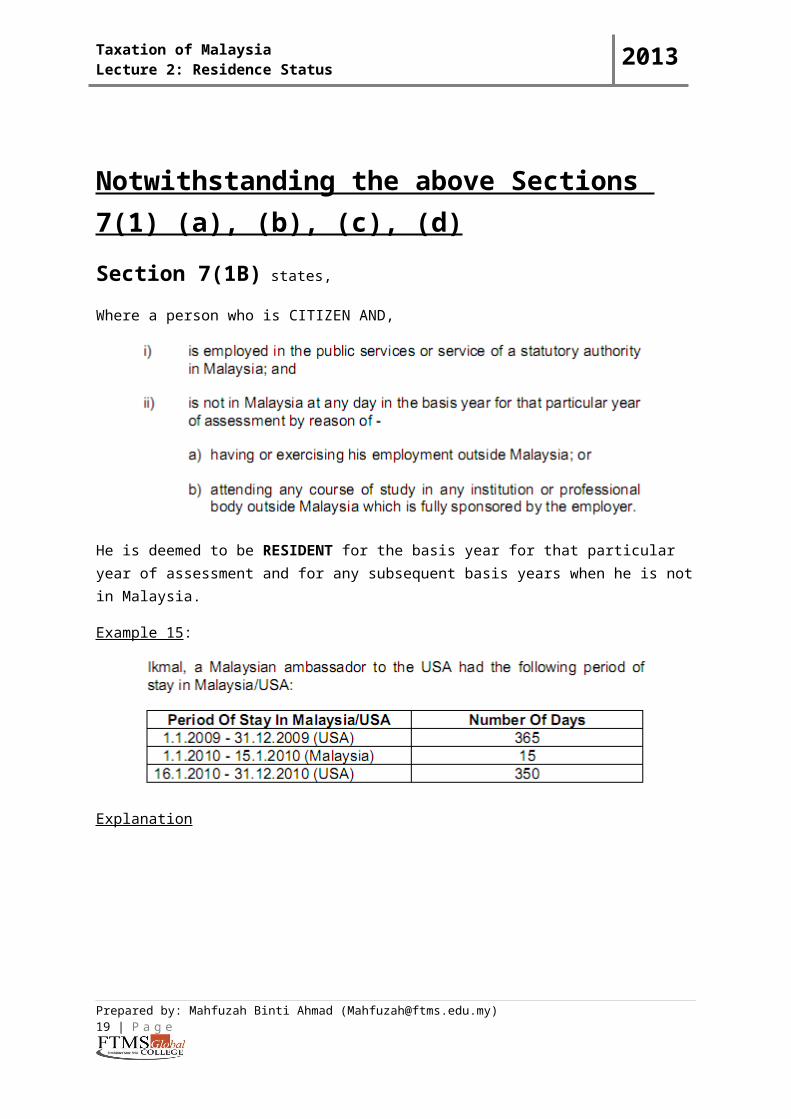

Notwithstanding the above Sections 7(1) (a), (b), (c), (d)

Section 7(1B) states,

Where a person who is CITIZEN AND,

He is deemed to be RESIDENT for the basis year for that particular year of assessment and for any subsequent basis years when he is not in Malaysia.

Example 15:

Explanation

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 17 | P a g e

Page 18

Taxation of Malaysia Lecture 2: Residence Status

2013

Example 16:

Explanation

Example 17:

Explanation

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 18 | P a g e

Page 19

Taxation of Malaysia Lecture 2: Residence Status

2013

Example 18:

Explanation

Example 19:

Explanation

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 19 | P a g e

Page 20

Taxation of Malaysia Lecture 2: Residence Status

2013

The significance impact of resident status:

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 20 | P a g e

Page 21

Taxation of Malaysia Lecture 2: Residence Status

2013

Section 8 of the ITA 1967 provides for the determination of residence status for

companies and bodies of persons (except trust bodies – subsection 61(3) of ITA covered it).

Section 8(1)(b) of the ITA 1967, a company or a body of persons carrying on a trade or

business is resident in Malaysia for the basis year for a year of assessment if at any time

during the basis year the management and control of its business or of any one of its

businesses are exercised in Malaysia.

Section 8(1)(c) of the ITA 1967, a company carrying on a business or businesses is

resident in Malaysia if at any time in the basis year for the year of assessment, the

management and control of its business or any one of its business is exercised in

Malaysia.

Residence status of a subsidiary or a branch of a foreign company in Malaysia

Foreign corporations normally extend their business activities to Malaysia by incorporating a

subsidiary in Malaysia or registering a branch in Malaysia. The residence status of

subsidiaries of foreign corporations would be determined by paragraphs 8(1)(b) and 8(1)(c)

of the ITA 1967.

Branches of foreign corporations in Malaysia are generally treated as non-residents in

Malaysia unless it can be established that the management and control of its affairs or of

its businesses or of any one of its businesses is exercised in Malaysia.

How to Define Management and Control?

Management and control refers to the controlling authority which determines the policies to

be followed by the company. The management and control is considered to be exercised

when the directors meet to conduct the company’s business/ affairs irrespective of

where the company might be incorporated.

If, at any time during the basis year for a YA, at least one meeting of the board of directors is

held in Malaysia concerning the management and control, even though all other meetings

are held outside Malaysia, then the company is resident in Malaysia for that basis year.

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 21 | P a g e

Page 22

Taxation of Malaysia Lecture 2: Residence Status

2013

The location of the trading activities or the place of physical operations may not

necessarily be the place of management and control.

For

example

:

Ching Mart Stores Inc. is a Chinese retail store dealing with luxury products in

China. The company has set up a business in Kuala Lumpur that deals with

trading activities but the management and control is exercised by the parent

company in China.

Although the physical operations of the company was carried on in Malaysia

but the management and control of the company was exercised outside

Malaysia. Therefore, the company is not a resident in Malaysia.

The appointment of a local director or local board of directors in Malaysia does not

determine the residence status of a company. If the controlling authority is exercised by

the directors who are at the company’s head office overseas, then the company is not a

resident in Malaysia. Likewise, the residence status of a director does not itself

determine the residence status of a company.

Control by the directors determines the management and control of a company . The

directors exercise their powers in the management of the company’s affairs by virtue of their

powers conferred upon them under the Articles of Association. On the other hand, control

by the shareholders is irrelevant for the determination of the management and control as

shareholders exercise their power over the company by virtue of their voting power at formal

meetings of shareholders. Company is to be treated as a taxable entity distinct from its

shareholders.

Prepared by: Mahfuzah Binti Ahmad ([email protected] ) 22 | P a g e