THE LEGACY OF DEPOSITINSURANCE: THE GROWTH, SPREAD,AND COST OF INSURING FINANCIAL

INTERMEDIARIES

Eugene N. White

Working Paper 6063

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138June 1997

I am especially grateful for helpful suggestions from Michael Bordo, Hugh Rockoff, Anna Schwartz,Larry White and the participants at the NBER Conference, "The Defining Moment: The GreatDepression and the American Economy in the Twentieth Century," and to the NBER for the supportof this research. This paper is part of NBER's research programs in the Development of theAmerican Economy and Monetary Economics. Any opinions expressed are those of the author andnot those of the National Bureau of Economic Research.

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

The Legacy of Deposit Insurance: The Growth,Spread, and Cost of Insuring Financial IntermediariesEugene N. WhiteNBER Working Paper No. 6063June 1997JEL Nos.N22, G21,G28Development of the American Economyand Monetary Economics

ABSTRACT

Without the Great Depression, the United States would not have adopted deposit insurance.

While the New Deal's anti-competitive barriers have largely collapsed, insurance has become deeply

rooted. This paper examines how market and political competition for deposits raised the level of

coverage and spread insurance to all depository institutions. A comparison of the cost of federal

insurance with a Counterfactual of an insurance-free system shows that federal insurance ultimately

imposed a higher cost but achieved political acceptance because of the distribution of the burden.

Eugene N. WhiteDepartment of EconomicsRutgers UniversityNew Brunswick, NJ 08903and [email protected]

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

One enduring legacy of the Great Depression was the creation of deposit insurance for

financial intermediaries. Deposit insurance was a real innovation in federal regulation of the

financial system. While the New Deal's anti-competitive barriers have largely collapsed, deposit

insurance has become deeply rooted.1 Coverage of the banking system has expanded steadily and

it has spread to other financial sectors. Economists have inveighed against government insurance

of financial intermediaries' liabilities; and yet even in the wake of costly insurance disasters, there

is little political interest in altering this pillar of the New Deal.

Without the Great Depression, the United States would not have adopted the New Deal

package of financial regulations that prominently featured deposit insurance. The New Deal's

regulations limiting competition had profound effects on the financial system; however these

regulations, with some exceptions, have disappeared while insurance of financial intermediaries

appears to be permanent. Insurance began with the New Deal's limited explicit guarantee of bank

deposits. This protection has grown considerably and is now granted implicitly to protect the

deposits of all large banks. Furthermore, as Table 1, shows, insurance has spread to other

financial sectors. Although some features of deposit insurance have changed recently, there is no

evidence of a rollback. With the important exceptions of mutual funds and money market mutual

funds, the insurance of financial institutions liabilities is pervasive.

There is no ready model to explain the growth and spread of federal insurance of

intermediaries. Political economy offers models of logrolling (Shattschneider, 1935) and

cascading regulation (Bernard and Leidy, 1992; Feinberg and Kaplan, 1993) that are not applicable

here. In logrolling, sectors of an industry or related industries bargain in Congress for favorable

legislation combined in one bill. Regulation "cascades" when one industry upstream secures

1

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

protection industry inducing the downstream firms to follow them later and push for their own

protection. Cascading regulation in international trade vertically moves from industry to industry.

In contrast, the spread of insurance in the financial sector from banks and thrifts to credit unions,

broker-dealers, life insurance companies and pension funds represents horizontal movement.

Although competition between types of intermediaries had increased in the 1920s, the New Deal's

regulations tried to ensure very imperfect competition between the various sectors of the financial

industry. Over time, competition within each segment and between each type of intermediary

increased. The advantages conferred on banks by deposit insurance were then eagerly sought by

uninsured intermediaries and weaker institutions pushed up the level of insurance.

In this paper, I examine how insurance spread from one group of institutions to the next

and how the level of insurance was gradually raised. Although deposit insurance has often been

discussed as an important guarantor of the stability of the banking system and hence the economy

(Friedman, 1959), the expansion of deposit insurance cannot be justified on macroeconomic

grounds. The general view today is that while the failure of individual banks might begin a panic,

a systematic collapse may be prevented by proper intervention by the Federal Reserve as the lender

of last resort (Friedman and Schwartz, 1986). Instead, it is its redistributive features that have

made insurance a permanent feature of the financial system while other New Deal regulations

disappeared. Redistribution of the costs of failures, hidden in the insurance premiums, has gained

public acceptance and allowed financial intermediaries to successfully lobby for expanded

coverage. If insurance was not necessary for securing macroeconomic stability, substantial costs

may have been incurred. I explore the cost of insurance with a Counterfactual of an insurance

free post-Great Depression financial system to assess the burden imposed by this legacy of the

2

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

New Deal.

The Origins and Establishment of Deposit Insurance

While deposit insurance today enjoys broad public support, proposals for federal insurance

before the Great Depression were viewed as special interest legislation. States had experimented

with insurance of bank liabilities before the Civil War and after the panic of 1907. These state

systems had, at best, mixed results, establishing a strong policy prejudice against federal

insurance (Golembe 1960, White 1983, Calomiris 1990, Wheelock 1992). Nevertheless, a well-

motivated lobby of predominantly rural, unit bankers was keen on securing a federal guarantee

system. Hoping to increase depositor confidence while preserving the existing banking structure,

these bankers opposed the liberalization of branching laws and other regulations, which could

have produced a more stable banking system of larger, diversified institutions (Calomiris, 1993).

Studies of the origins of deposit insurance from Golembe (1960) to Calomiris and White

(1994) emphasize that deposit insurance would have had little chance of adoption if the 1930-1933

banking collapse had not frightened the public into supporting the pro-insurance bankers' cause

in Congress. Even so, the hurtles faced by backers of deposit insurance were high. From earlier

state experiments, the problems of moral hazard and adverse selection were well known and

debated in Congress (Flood, 1991). Aware of the potential problems, the Roosevelt

administration, the bank regulatory agencies, and the larger banks were resistant to any proposal.

In the face of such opposition, credit for the adoption of deposit insurance belongs largely to Rep.

Henry Steagall (D.-Alabama), Chairman of the House Banking and Currency Committee, who

refused to permit the passage of any banking legislation unless it included an insurance system.

3

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Far from being a high-minded policy aimed at protecting the depositor, the design of the

Federal Deposit Insurance Corporation (FDIC) was the product of a lengthy legislative struggle,

pitting smaller state-chartered, often unit banks, against larger banks, often members of the Federal

Reserve System. Under the Banking Act of 1933 (often called the Glass-Steagall Act), the

Temporary Deposit Insurance Fund was organized and scheduled to begin operations on January

1, 1934. The coverage per account was set at a maximum of $2,500. All Federal Reserve

member banks were required to join. Non-member banks could receive insurance only if they

joined the Fed within two years. The last provision was resented by the non-member banks

because they would be forced to meet the higher requirements and stricter regulations imposed

on members. Banks joining the system were to pay a 0.5 percent assessment of insurable

deposits, half upon joining and half subject to call. (FDIC, 1984, p. 56-7)

When the Temporary fund was extended for a year in 1934, Steagall attempted to increase

coverage of accounts to $10,000 against Roosevelt's objection that 97 percent of depositors were

already covered. Congress raised the limit to $5,000 and postponed compulsory Federal Reserve

membership until July 1, 1937—a victory for the small banks. (Burns, 1974), The temporary

system became permanent under Title 1 of the Banking Act of 1935, which created the FDIC. All

Federal Reserve members were still required to join; but in a major concession, non-members,

while subject to approval of the FDIC, were no longer required to become members of the Fed.

The permanent plan required an annual assessment on total, not just insured, deposits. This shift

was opposed by the larger banks whose shares of uninsured deposits were much greater.2

The Banking Act of 1935, based largely on the draft legislation of the FDIC staff, set a flat

annual assessment rate of one-twelfth or 0.0833 percent of a bank's total deposits, eliminating

4

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

the original capital contribution by banks. To ensure that the insurance fund was not depleted,

the FDIC was given authority to borrow up to $975 million from the Treasury. Banks contributed

premiums as a fraction of all their deposits but only received protection on deposits up to a

maximum of $5000 per account. Small banks and lower income individuals with small deposit

accounts benefitted while bigger banks with larger depositors provided a subsidy. The smaller

banks' competitive position was improved, and there was less pressure to build stronger, larger

banks.

The requirement that all Federal Reserve members join the new FDIC guaranteed that the

bigger banks, many of whom had opposed federal deposit insurance, joined the system rather than

lose the benefits of Fed membership. The non-member banks, almost all smaller state-chartered

banks, had pushed for deposit insurance. Happy with the design, they signed up immediately. In

1935, 91 percent of the 15,488 commercial banks with 86 percent of assets joined the system.

Only mutual savings bank membership was low. Of the 566 mutual savings banks, 11 percent

with 11 percent of total assets took out membership. Most mutual savings banks preferred to

remain in existing state insurance systems that offered higher levels of coverage. Nevertheless,

the nearly universal coverage of commercial banks and the subsequent disappearance of bank

failures was seen as triumph for the New Deal.

The Growth of FDIC and FSLIC Insurance

For the next fifteen years, the FDIC's insurance of commercial banks and mutual savings

banks appeared to be an unqualified success. By 1949, commercial bank membership crept up

to 95 percent, accounting for 49 percent of deposits; mutual savings bank membership increased

5

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

to 36 percent, holding 70 percent of all assets. Bank failures declined, no panics occurred, banks

were more profitable, and the insurance fund grew. At the same time, inflation had reduced the

real value of insurance. World War II inflation shrank the real value of coverage per account

from $5000 in 1934 to $2807 by 1949. Figure 1 depicts the real value of the maximum coverage

offered per account from 1934 to 1995, with the changes in the nominal levels of coverage

indicated by vertical lines. However, this decline in protection elicited no outcry by depositors for

more protection. As seen in Figure 2, the percentage of total deposits covered by FDIC insurance

had climbed from 45 percent in 1934 to 50 percent in 1950.3 The absence of big failures and the

growth of deposits kept the total insurance fund at about 1.5 percent of all insured deposits, as

shown in Figure 3, in spite of repayment of the Treasury and Federal Reserve Banks initial

contributions in 1949. (FDIC, 1984, pp. 5-7).

By any measure, the vast majority of "small depositors" were well protected by this level

of insurance, and there was no public demand for a big increase in coverage. In 1949, only 4.4

million of the 104 bank accounts were not fully protected (FDIC, Annual Report 1949). Some

of these accounts were government (293,000) and interbank deposits (127,000), which had high

average balances of $40,000 and $90,000 in contrast to the average demand deposit balance of

$1,911 and savings and time deposit balance of $824. The FDIC (Annual Report 1949) calculated

that any increase in coverage would offer little additional protection. A rise in coverage to

$10,000-which would have returned coverage to its real 1934 value-would have fully covered

another 3 million accounts or 97 percent of the total. The percentage of insured banks deposits

covered would have risen from 50 to 57 percent. An increase to $25,000 would have covered

99.5 percent of all accounts and 65 percent of all deposits.

6

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Mutual savings banks were a shrinking component of the banking industry and played no

significant role in the politics of deposit insurance. By 1949, the FDIC insured only 192 of the

531 mutual savings banks. Most of the remainder (190 of 339) were in Massachusetts and were

insured by a state fund. The FDIC-insured mutual savings banks had 12.6 million accounts in

1949 with $13 billion of deposits.4 Ninety-four percent of these accounts were fully insured, and

61 percent of all deposits were insured. While this profile looks similar to commercial banks,

mutual savings banks were not at the same risk. In commercial banks, 68 percent of all deposits

were held in the 3 percent of the accounts with over $5,000; for mutual savings banks, only 39

percent of all deposits were in the 6 percent of accounts with over $5,000. Very few accounts,

representing 3.6 percent of deposits, exceeded $10,000, whereas 57.7 percent of commercial

banks' deposits were in accounts in excess of $10,000. Mutual savings banks were not as

vulnerable as commercial banks and did not join the demand for a rise in insurance.

Demand for an increase in coverage was driven by the small banks fear of losing deposits.

Figure 4 shows the drop in fully insured accounts from 98.5 percent at the inception of insurance

to just under 96 percent by 1949. The smallest banks felt this change acutely. Table 2 shows that

in 1936 35.4 percent of banks had 90 to 100 percent of their deposits insured. The number of

banks enjoying this high level of coverage collapsed to 5.7 percent in 1949. The search for

protection by large depositors threatened smaller banks. In the 1950 Senate hearings on deposit

insurance, Sydney J. Hughes of the Industrial Bank of Commerce of New York City and member

of the Consumer Bankers Association explained that: "when a depositor's balance exceeds the

$5,000 insure maximum, he shifts the surplus to another bank and becomes one of what must be

millions of multiple deposits." (U.S. Senate, 1950, p. 90)

7

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

There were good reasons for deposits in excess of the insured maximum to worry bankers,

as one recent study suggests. Using a special sample of wealthy households from the 1992 Survey

of Consumer Finances, Kennickell, Kwast, and Starr-McCluer (1996) found that while large

depositors keep substantial shares of their assets in insured depositories, they often fail keep them

within insurance limits. According to the survey, a sizeable 17.3 percent of household deposits

were uninsured. Kennickell, Kwast, and Starr-McCluer found that any reduction or restriction in

insurance coverage would substantially increase the uninsured deposits of households and increase

the likelihood of withdrawals.5

In 1950, bills to raise the coverage were introduced by Senators John W. Bricker (R-

Ohio), Claude D. Pepper (D-Florida), Charles W. Tobey (R-New Hampshire), Hugh A, Butler

(R-Nebraska), William Langer (R-North Dakota) and Burnet R. Maybank (D-South Carolina)

who was Chairman of the Committee. All of these bills contained increases up to $15,000 and

Pepper's would have removed the limit altogether. In his plea for a rise to $10,000, Senator

Butler noted that "from my correspondence, I judge that it is primarily the smaller country banks

that are anxious for this change. It seems that under the present system a good many depositors

maintain part or all of their funds in the city banks at some distances, perhaps from their homes."

(U.S. Senate, 1950, p. 101) Ben Dubois, the Secretary of Independent Bankers Association, made

an explicit appeal to protect the small banks, stating that "the Federal Deposit Insurance

Corporation has been a powerful instrument in the perpetuation of independent banking. It has

put the small bank on a part with the large bank in the eyes of the average depositor...The

Corporation has been helpful indeed in establishment independent bank to continue in spite of the

trend toward banking concentration" (U.S. Senate, 1950, pp. 87-8).

8

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Federal regulators supported the increase but tended to cloak their support in terms of the

ideology of guaranteeing the continued protection of the small depositor. In the 1950 hearings,

there was general support from federal regulators to raise the ceiling to $10,000. The Secretary

of the Treasury John W. Snyder and the Comptroller of the Currency, Preston Delano, favored

an increase to $10,000. Delano argued that $10,000 was justified on the grounds that prices had

risen, lowering effective coverage, even though he admitted that $5000 still covered 96 percent

of accounts. The Chairman of the FDIC, Maple T. Harl also supported the increase on the

grounds that protection of the small depositor required it; but he was also clear that "the

preservation of the American banking system... As you very well know, the survival of the dual

banking system in large measure depends on Federal deposit insurance" (U.S. Senate, 1950, pp.

22-23). The Former FDIC Chairman Leo Crowley testified that he favored the increase from

$5000 to $10,000 because it would help small savers and the small banks in their home

communities.

Larger banks were generally willing to support a rise but they were less enthusiastic and

were more concerned about the fact they subsidized the system. American Banking Association

officials testified in favor of $10,000 coverage but warned that any further increase would

endanger the system (U.S. Senate, 1950, p. 66). Frederick A. Potts, President Philadelphia

National Bank and a representative of the Reserve Bankers Association, testified that limited

deposit insurance was a sound idea. However, he warned that a rise in protection to $10,000

would undermine good bank management and stimulate demands for more coverage. (U.S.

Senate, 1950, pp. 80-81). The most striking testimony against the proposal came from one of the

founding fathers of the FDIC, Senator Arthur Vandenberg (U.S. Senate, 1950, p. 50-51). In a

9

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

letter, he denounced the proposed rise to $10,000 coverage, arguing that was imprudent: "There

is no general public demand for this increased coverage. It is chiefly requested by banker demand

in some quarters for increased competitive advantage in bidding for deposits." He predicted that:

"If we extend the cover to $10,000, how long will it be before we confront demands for total

coverage? Total coverage would virtually socialize out private banking system. It could involve

many of the vices which so often wrecked previous well-meaning adventures in this field."

The willingness of larger banks to support an increase in the level of coverage did not arise

out of any hope to improve their competitive position by insuring more deposits. Their position

changed very little in terms of insurance coverage after the 1950 act went into effect. At the very

beginning in 1936, large banks received very little protection, as seen in Table 3. While the more

than ten thousand banks with under $1 million in deposits had 86 percent of their deposits insured

and the banks with $1 to $5 million of deposits had 74 percent of their deposits protected by the

FDIC, the two hundred largest bank had only 28 of their deposits insured. Coverage for them

grew; yet by 1949, coverage was still only 36 percent. What concerned the larger banks was not

the fact that they still had large uninsured deposits but that they were assessed on their total, not

just their insured, deposits. To cover a much larger fraction of their deposits would have required

a huge increase in coverage that would have interested few smaller banks.

Furthermore, a big increase in coverage would have decreased the ratio of the insurance

fund to insured deposits, depicted in Figure 3, perhaps requiring an increase in assessments. The

insurance fund had grown thanks to the virtual disappearance of bank failures. The fund easily

repaid the initial contributions ($289 million) of the Treasury and the Federal Reserve Banks

(FDIC, 1984, pp. 58-60). There was concern that the assessment rate was too high, not too low,

01

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

cutting into bank profits. Although banks' net earnings rose steadily over the decade of the 1940s,

net profits had recently declined from $906 million in 1945 to $831 million in 1949. At the same

time, the FDIC assessment climbed from $86 million to $109 million, following the rise in total

deposits (FDIC, Annual Report 1949, p. 40). Cutting the assessment could easily buoy profits,

Not surprisingly, the larger banks lobbied Congress for a reduction in assessments while

they grumbled about the increase in coverage. The smaller banks returned the favor. The

Independent Bankers Association was set against any reduction in the premium and protested that

big banks had no right to complain as they had obtained the interest prohibition on demand

deposits under the New Deal. But, the end result was a compromise of an increase in coverage

and a change in assessment that satisfied both parties and ensured swift passage of the 1950 act.

Figure 2 shows that the new level of $10,000 coverage protected an additional 5 percent of

deposits. More importantly for banks concerned about protection, the shares of protected

accounts, shown in Table 3, returned to their earlier level. The more exposed banks who had lost

their high level, 90 to 100 percent, of protected deposits, regained ground lost in the previous

decade.

The larger banks also benefitted. The basic assessment rate was not reduced because the

FDIC feared this might set the stage of a depletion of the fund. Instead, it was lowered by a rebate

system. The FDIC deducted the operating expenses and insurance losses from gross assessment

income, then shared the remainder, returning 60 percent to the banks and keeping 40 percent.

As seen in Figure 5, this rule produced some fluctuation in assessment rate around 0.035 and

0.037 percent of total deposits, far below the original 0.0833 percent. Total assessments reached

in 1951 $124 million, but $70 was rebated to the banks (FDIC, Annual Report. 1951). Net profits

11

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

for 1951 were $908 million but they would have stood at only $838 million without this change.

The 1950 act was a well-crafted compromise. Insurance coverage of all deposits was on

the rise, Larger banks who had initially opposed deposit insurance now "signed on" to support

insurance thanks to the reduction in the effective assessment rate. The 1950 increase in insurance

coverage was the last time that commercial banks appear to have been the primary movers behind

insurance legislation. While commercial and mutual savings banks covered by the FDIC continued

saw the nominal coverage rise and the percentage of funds insured increase, greater competition

and inflation put more pressure on other financial intermediaries who clamored more loudly for

higher coverage.

Evaluating the Rise in Coverage for Commercial Banks

Legislation raising the level of coverage is only one factor leading to a higher level of

protection. To explain the percentage of deposits in FDIC- insured institutions that were covered

by FDIC insurance in Figure 2, four factors were considered: (1) If the real maximum deposit

insurance coverage per account is increased, the percentage of covered deposits should rise, (2)

Failures, measured either as the number of failing banks or the percentage of deposits in failing

banks, might induce depositors to shift their uninsured deposits to new accounts or banks for

complete coverage, (3) A rapid growth in deposits might decrease coverage if individuals'

balances quickly rise above insured levels, and (4) If individuals open new accounts to ensure

coverage of their deposits, the increase in the number of accounts should raise the percentage of

deposits covered.6

Data on the number of accounts was difficult to obtain, as it was only collected by the

12

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

FDIC in occasional special reports until 1981. This data is displayed in Table 4. Beginning in

1990, some data on commercial banks' accounts was collected by the FDIC.7 Accounts of all

banks appear to have grown at a very rapid rate between 1934 and the mid-1970s. The average

rate of growth exceeded the real rate of growth of the economy. Starting in the late 1970s and

certainly in the early 1980s, this growth slows down, with some years of decline. The stagnation

between 1981 and 1990 may be attributable to the high level of coverage provided by the jump

from $40,000 to $100,000 insurance and the increase in alternatives to bank deposits, such as

money market mutual funds. A continuous time series of accounts for the period 1934 to 1981

was constructed by regressing the number of accounts on time and time squared to fill in the

missing observations, but no attempt was made to fill the gap between 1981 and 1990 when the

trend growth abruptly changed.

Unit root tests and an examination of the partial autocorrelations indicated that the

percentage of insured deposits, the real insurance per account, and the measures of bank failures

needed first differencing for stationarity. It was difficult to judge whether the growth of deposits

also required first differencing, but the results were similar so only the first differenced results were

reported in Table 5. Regressions (1) and (2) are for the whole period, 1934-1994, and exclude

the variable for accounts. As hypothesized, an increase in the real value of maximum deposit

insurance coverage per account, raises the percentage of covered deposits. A rise in real

coverage of $10,000 would drive the percentage of insured deposits up by about 6 percent,

suggesting that this factor alone can only account for a modest portion of the increase. Also, as

conjectured, an increase in deposits tends to lower the percentage of covered deposits. An

acceleration in deposit growth of one percent pushed down coverage approximately 1.7 percent.

J3

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

The most notable example of this effect was during World War II, when the rapid growth of

deposits outweighed other influences and temporarily halt the upward trend in coverage. Neither

variable for bank failures helps to explain the rising coverage of deposits, probably because there

is little variation in failures. For depositors, it may have been a minor consideration given the

FDIC's practice of frequently providing full insurance to depositors whose accounts were over the

limit (FDIC, 1984).

The constructed time series on accounts was used in the regressions (3) and (4) for the

years 1934-1981. The variable does not help explain the behavior of the dependent variable.

However, this should not be taken as evidence that account-creating activity of depositors had no

effect on coverage. The correlation between the number of accounts and the percentage of

coverage deposits from 1934 to 1981 is high, 0.93, reflecting a common trend. In the regression,

the percentage of insured deposits is first differenced, but the application of this procedure to

accounts is first differencing a variable, many of whose observations are fitted to the trend, thus

rendering it relatively weak in the regression. While the quality of the data on accounts does not

permit very robust tests of the effects of individual account-creating activity, qualitative evidence

implicates account creation an important factor from the beginning of the FDIC until at least the

mid-1970s.

Although account creation may have been more important, the regressions only identify

the FDIC's increased coverage per account in 1950, 1966, 1969, 1974, and 1980 as a key factor.

The first increase in real coverage in 1950 was the product of lobbying by the unhappy sectors of

commercial banking. Afterwards it was not the needs of the commercial banks but rather their

rivals that pushed for expanded coverage.

P1

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Raising Deposit Insurance in 1966 and 1969: the role of the S&Ls

S&Ls originally had little interest in deposit insurance. They were very cautious about

advocating any guarantee system and probably would never had supported one if commercial

banks had not obtained the FDIC (Ewalt, 1962). S&Ls were given the opportunity to obtain

federal deposit insurance at the same time as Congress established the FDIC. The National

Housing Act (1934) established the Federal Savings and Loan Insurance Corporation, almost as

an afterthought, to provide a full set of institutions to S&Ls to parallel those for banks.8 Many

thrifts had found it advantageous to join the Federal Home Loan Bank system. The purchase of

shares in one of the 12 regional Federal Home Loan Banks gave them access to FHLB credit

facilities but did not impose any additional regulations on them (Grossman, 1992). Many fewer

took out charters to become federal mutual savings and loan associations. Supervised by the

FHLBB and narrowly constrained in lending, a federal charter appeared relatively unattractive to

most S&Ls. Although federally chartered S&Ls were required to join the FSLIC, members of the

FHLB system were not so obliged. This regulation contrasted insurance for banks where all

Federal Reserve members—national banks and state banks—were required to obtain FDIC

insurance. Thus, by 1940, half of all S&Ls had joined a FHL Bank; but only 20 percent took out

federal charters. Unlike the banks, where deposit insurance was almost universal from the outset,

only 30 percent of the S&Ls with 50 percent of assets (See Figure 6) had obtained FSLIC

insurance by 1940.

The initial responses of banks and S&Ls to deposit insurance reflected their different

experiences during the Great Depression and the costs and benefits of insurance they faced. Both

industries suffered severe withdrawals of deposits between 1929 and 1933. Commercial banks

15

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

lost 17 percent of their deposits and S&Ls 28 percent. S&Ls were forced to endure a larger

contraction, but it was more orderly. Between 1929 and the end of 1933, the number of banks

fell from 24,504 to 14,440; yet S&Ls only declined from 12,342 to 10,596. Unlike the banks who

had to wait for state and then federal bank holidays to refuse customers payment, the S&Ls had

a right to put depositors "on notice" and refuse to meet demands for withdrawals until loan

repayments came in. Thus, S&Ls had a device to ward off the runs that devastated the banks and

saw less advantage to insurance that required acceptance of more federal regulation. In addition,

FSLIC insurance came at a higher price. The FSLIC premium was 0.125 percent of deposits,

whereas FDIC insurance was 0.0833 percent. The FSLIC rate was only reduced to the FDIC level

in 1951 (Grossman, 1992).

After World War II, the thrifts were one of the fastest growing groups of financial

intermediaries. The New Deal conferred a variety of advantages on thrifts, whose share of all

financial intermediaries assets rose from 6 percent in 1950 to 13 percent in 1970. Although

imperfect substitutes for commercial banks' demand deposits, which paid no interest, S&Ls'

interest-bearing passbooks were attractive to small savers and competed with banks' time deposits.

By 1950, 50 percent of S&Ls with 80 percent of all assets had joined the system (see Figure 6).

However, unlike the banks, FSLIC-insured institutions had almost all their accounts insured. In

1941, 86 percent of all savings capital (deposits) in S&Ls were insured, rising to 94 percent by

1947. This high level of insurance is attributable to the predominance of small savers with

balances averaging well below $1000 (FHLBB, Annual Report 1947). This nearly complete

coverage helps to explain why the insured S&Ls did not participate in the 1950 deposit insurance

debate. Ten years later, conditions had changed dramatically. When S&Ls' surging inflow of

16

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

savings deposits came to an abrupt halt in the credit crunch of 1966, they became interested in

deposit insurance. The similarity of coverage among thrifts assured a fairly uniform view of the

desirability of increased insurance in contrast to the wide divergence of opinion among banks.

Neither banks nor S&Ls saw the erosion in the real value of deposit insurance per account

as a threat. The decline in real deposit insurance in Figure 1 was slight compared to what

happened before the 1950 increase. Furthermore, total coverage of deposits, shown in Figure 2,

was fairly stable. However, there was a significant drop in the number of fully insured accounts

that especially affected small banks. Although coverage dropped for most classes of banks, the

three smallest categories of banks in Table 3 show very large declines in coverage of deposits

between 1951 and 1966. Inflation and the shift between groups make comparisons between years

difficult, yet the danger posed by this decline in coverage is clear in Table 2. Here, the percentage

of commercial banks with 90 to 100 percent of their deposits insured by the FDIC dropped from

23.2 percent in 1951 to 9.9 percent in 1964. Thus, a small but significant fraction of the banking

industry was feeling increasingly exposed.

By the mid-1960s, banks and thrifts were also worried that interest rate restrictions

reduced their ability to attract deposits. While banks had been subject to Regulation Q interest

rate ceilings since 1935, FHLB member thrifts were constrained by FHLBB rules, which imposed

a variety of restrictions on the "dividends" paid on savings account (FHLBB, Annual Report

1965). In 1965, the limit on the interest charged on bank's time deposits stood at 5.5 percent, yet

very few S&Ls could offer rates in excess of 5 percent. In this year, market rates moved above

the ceilings and both banks and thrifts began to lose funds.9 Thrifts experienced a 4 percent fall

in funds available for new investment, followed by a 28 percent fall in 1966, when savings inflows

17

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

and loan repayments fell off. The big demand for advances from the FHLBB, led the Board to

ration lending to S&Ls who then slashed mortgage lending by one third. In response, the Board

adopted a more flexible dividend policy; and by the end of 1966 over 20 percent of S&L deposits

were paying 5.25 percent (FHLBB, Annual Report. 1966).

Interest rate regulations needed some unification to preserve the system. The Treasury and

the FDIC proposed that the Federal Home Loan Bank Board be given more supervisory authority

and power to set maximum interest and dividend rates. Many S&Ls were not enthusiastic about

the prospect of new FHLBB regulation, but they were willing to countenance more control if it

would ensure that deposit inflows resumed. Of considerable concern to the S&Ls was that savers

were showing great reluctance to hold deposits in excess of the $10,000 level of coverage. One

Board study showed that there was an "artificial bulge" in S&L's account at the $10,000 level,

indicating that people were limiting their deposits (Congressional Record. August 23, 1966).

Efforts to raise insurance predated the 1966 credit crunch, but demands more urgent now.

Hearings in Congress were held in 1963 to consider a rise in insurance coverage to $25,000 for

banks and S&Ls. Over the next three years, Congressmen wrangled over the level of coverage

and whether the FHLBB should be granted additional regulatory powers. In Congressional

hearings, there was no protest by the FHLBB, the Board of Governors of the Federal Reserve or

the FDIC about the increase in insurance. They were much more concerned about the effects of

changing the supervisory practices. Rep, Wright Patman (D-Tex), chairman of the House

Banking and Currency Committee, vigorously argued for a simple increase in coverage. He

brushed aside arguments that individuals could easily secure coverage by creating multiple

accounts and claimed that the current $10,000 maximum coverage encouraged everyone from

18

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

businessmen to widows to firemens' funds to put their money in out-of-town banks once the

ceiling was reached in local banks. Patman slammed the big banks for pressuring their

correspondent banks to block an increase in insurance, portraying them as predators anxious to

drive the S&Ls out of business (Congressional Record. August 23, 1966).

Congress navigated through the complex, competing interests in writing the Interest Rate

Control Act of 1966. The act extended Regulation Q to thrifts, but gave them a favorable

differential. Thrifts were allowed to pay 3/4 of one percent in interest more than banks, in the

hope of channeling funds back to the mortgage market. Congress also gave more supervisory

authority to the FHLBB. The legislators settled on increasing deposit insurance for persons

holding accounts in banks and thrifts to $15,000, a relatively low number as far as many thrifts

were concerned. Following the 1950 deal, the 1966 package provided a sweetener for the larger

banks in the form of an increase in the assessment rebate to 66 2/3 percent. Although interest rate

flexibility was clearly of greatest concern to intermediaries, the rise in insurance did help. No data

exists on insurance coverage among thrifts, but the level of insured deposits rose for all sizes of

banks in Table 3.

These adjustments to the New Deal system did little to alleviate the underlying problems.

Once again in 1969-1970, tighter monetary policy pushed market rates above the Regulation Q

ceilings. S&Ls saw virtually no net inflow of new funds while commercial banks lost funds,

contrasting the 1966 experience when S&Ls were in greater distress. S&Ls were in better shape

thanks to the favorable differential in interest rate ceilings. Still, there were gaps in the interest

rate controls. A substantial number of mutual savings banks in the Northeast who were not

members in the Federal Reserve or the FDIC avoided the controls, as did non-FSLIC member

19

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

thrifts. These institutions' higher rates were drawing funds away. Congress responded to the

complaints of controlled banks and thrifts by extending Federal authorities' control of all

institutions in states where over 20 percent of savings were held by non-federally regulated

institutions (FHLBB, Annual Report 1969).

With no debate, Congress also raised deposit insurance coverage for banks and thrifts on

December 23, 1969 from $15,000 to $20,000.10 This hike halted the new decline in fully insured

accounts depicted in Figure 4. The real value of nominal coverage of $20,000 was now higher

than it had ever been (Figure 1), reaching approximately $7,000 in 1934 dollars. The percentage

of insured accounts and deposits of FDIC institutions were at all time highs of 99.1 and 63.1

percent (Figure 2), with institutions of all sizes (Table 3) benefitting from the increase. By 1969

there were only 208 noninsured commercial banks and nondeposit trust companies and 166 mutual

savings banks, virtually all of the latter being located in Massachusetts and covered by its deposit

insurance system. (FDIC, Annual Report. 1969). In the thrift industry, over 70 percent of the

S&Ls with over 90 percent of assets were covered by 1969. Deposit insurance coverage in the

1960s had grown considerably for the banks and thrifts, well beyond the initial intentions of the

New Deal.

The Spread of Insurance

Greater interest rate volatility and increased competition in the 1960s created difficulties

for all financial intermediaries. Facing these new challenges, credit unions, broker-dealers,

pension funds, and insurance companies sought the benefits of government provided insurance for

their liabilities. As they held relatively modest or no funds on deposit and no claim could be made

20

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

that insurance would serve to prevent a panic, the history of these intermediaries demonstrates

how, even in the absence of concern about macroeconomic instability, new classes of

intermediaries were successful in lobbying Congress to expand insurance far beyond its New Deal

boundaries.

Designed to assist the small saver, credit unions grew rapidly in the postwar period. The

Federal Credit Union Act of 1934 made federal credit union charters available, as an alternative

to state charters, and they soon dominated the industry. The number of all credit unions—federal

and state—more than doubled from 10,571 in 1950 to 23,656 in 1970, with deposits climbing

from $880 million to $15.5 billion.11 Like the S&Ls, credit unions were initially reluctant to press

Congress to create institutions for them. But, competition from federally assisted and protected

banks and thrifts coupled with increased financial difficulties led the credit unions to aspire for

parity with banks and thrifts. Between 1934 and 1969, over 5,600 federal credit unions were

liquidated.12 Failures were increasing and in 1969, 274 federal credit unions were closed, 35 of

them at a loss of $95,000 to their members. Some assistance for failing firms came from credit

union leagues, bailing out another 280 other credit unions; but these private reserve funds were

very small. Failures induced Massachusetts in 1961 and later Wisconsin and Rhode Island to

create state funds; but they were restricted to state chartered credit unions, a small fraction of the

industry (Congressional Record. September 2, 1970).

Prompted by the credit crunches of 1966 and 1969, credit unions pressed for lending and

insurance institutions to parallel the Federal Reserve, the FHLB system, the FDIC and the FSLIC.

In 1970, Congress obliged them with the Federal Credit Union Act, creating the National Credit

Union Administration (NCUA), an analog to the Federal Reserve and FHLBB. While this bill was

21

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

making its way through Congress, an amendment was added to create a system of insurance for

credit unions.13 The amendment was initially sponsored by several Senators and there was no

apparent opposition from either banks or thrifts. A simple rational was given by one sponsor,

Senator Wallace F. Bennett (R.-Utah), who pointed out that federally chartered credit unions

were the only depository institutions not covered by a federal insurance program. The Senator

admitted that the absence of insurance posed no threat to the stability of the financial system and

that the losses of credit unions had been small, Insurance coverage for credit unions was almost

a matter of pure competitive equity.

Established in 1970, the National Credit Union Share Insurance Fund (NCUSIF) gave the

credit unions an insurance system. At the same coverage per account of $20,000 as the FDIC and

the FSLIC of $20,000, the 22 million credit union members, who had an average of $650 on

deposit, gained ample protection. Like the FDIC and the FSLIC, the NCUSIF was mandatory for

federally chartered credit unions and optional for state institutions. Administered by the NCUA,

the fund charged an annual premium of 0.0833 on the aggregate of members' accounts and

creditor obligations. Adoption of federal insurance was not initially universal. Many state-

chartered credit unions did not want to accept the federal regulations necessary to obtain NCUSIF

insurance. At the behest of these institutions, more states created their own insurance funds. In

1981 when California established the California Credit Union Share Guaranty Corporation, there

were sixteen state funds, covering 3,150 credit unions with $12 billion of deposits (NCUA,

Annual Report 1982), However, in the wake of widespread failures banks, S&Ls and credit

unions in the 1980s, there was a flight to the NCUSIF, which afforded greater protection. In

1981, NCUSIF-insured credit unions held 82 percent of all credit union shares. By 1985 this

22

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

figure jumped to 92 percent, rising to a nearly universal 99 percent in 1995 with the demise of the

state insurance plans (NCUA, Annual Reports. 1989, 1995).

In the same year that credit unions secured federal protection for their depositors,

customers of broker-dealers received guarantees for their funds on deposit—protection that the

original New Deal had never countenanced. The Securities Exchange Act of 1934 tried to protect

customers from brokers' dishonesty but not their incompetence. Protection from the

incompetence was the responsibility of the relevant self-regulatory organization (SRO)--the New

York Stock Exchange or the NASD. These organizations could intervene and transfer customer

accounts from a weak to a strong member firm, liquidate failing members or merge weak firms

with stronger ones (Teweles and Bradley, 1987).

The rising volume of activity on the exchanges during the 1960s' bull market put an

enormous strain on brokerages' ability to handle the complex paperwork that accompanied every

transaction. The number of "fails" or failures to deliver security certificates or complete

transactions produced a "back office" crisis. Many firms were swamped by business and could not

manage their operations well. Firms used customers' free credit balances for any business purpose,

including trading or underwriting, putting these funds on deposit at risk. When Ira Haupt and

Company foiled in 1963, as a result of a huge default on commodity contracts, the NYSE stepped

in and assisted with the firm's liquidation (Teweles and Bradley, 1987). Anticipating more

problems, the NYSE created a Special Trust Fund of $10 million and a $15 million line of credit

in 1964 to assist troubled members and protect customers (Sowards and Mofsky, 1971). AMEX

followed the NYSE's lead and by 1968 all the exchanges had established special funds. (Sobel,

1972 and U.S. Senate, Report No. 91-1218, 1970).

23

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

When the bull market broke in 1969 and prices and volume fell, many brokerages held

large inventories. Falling revenues and costly inventory losses led 129 NYSE member firms to

be liquidated, merged, or acquired and another 70 required some assistance from the Exchange.

The Special Fund ran out of funds in the summer of 1970 and was unable to pay out customers'

accounts in foiled brokers. In this emergency, the NYSE transferred $30 million from its building

fund to its Special Fund. However, it was clear that if a large brokerage went under, the resources

of the Special Fund would be inadequate (Sobel, 1975). The free credit balances—in effect, the

funds customers held on deposit with broker-dealer firms—stood at $3 billion in 1970 for NYSE

member firms. In addition, broker-dealers had custody of the $50 billion of customer securities

(U.S. Senate, Report No. 91-1218, 1970). Although there were no runs on brokerages, the

exchanges appeared unable to provide sufficient protection on their own. Insurance equivalent

to FDIC and the FSLIC was viewed as a reasonable solution by the securities industry and the

public. (Seligman, 1982). The House Report on insurance legislation was explicit: "Failures may

lead to loss of customers' funds and securities with an inevitable weakening of confidence in the

U.S. securities markets. Such lessened confidence has an effect on the entire economy....The need

is similar in many respects to that which prompted the establishment of the Federal Deposit

Insurance Corporation and the Federal Savings and Loan Insurance Corporation" (U.S. House of

Representatives Report, No. 91-1613, 1970, p. 2). This misreading of history put macroeconomic

stability as the prime reason for insurance, when special interests in the financial industry always

had the keenest interest in the establishment of insurance funds.

A proposal was put before Congress to establish a Securities Investor Protection

Corporation (SIPC) to act as an FDIC or FSLIC for the securities industry. The bill had the

24

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

support of the SEC, the Department of the Treasury and Congress' Joint Securities Industry Task

Force. An old New Dealer, Emmanuel Celler (D.-N.Y.) questioned the intention of insuring all

firms registered with the SEC without any inspection or further regulation. These qualms were

repeated by other congressmen; but like the bill for credit unions, the idea of insuring customer

accounts had wide support in Congress (Congressional Record. December 1, 1970).

Congress passed the Securities Investor Protection Act (SIPA) in December 1970. This

act created the SIPC, which was charged to administer a fund providing protection up to a

maximum of $50,000 for both cash and securities with a limit of $20,000 for cash. This insurance

was mandatory for broker-dealers registered with the SEC, making coverage nearly universal from

the outset. All SIPC members were assessed 3/16 of 1 percent per year of gross revenues from

the securities business for the SIPC fund (Matthews, 1994). If needed the corporation could

borrow up to $1 billion from the U.S. Treasury with the approval of the SEC (Seligman, 1982).14

Under SEC oversight, the SIPC has no authority to examine or inspect its members, Instead the

securities exchanges and the NASD are the examining authorities for its members, and the SIPA

gave the SEC additional authority to adopt rules relating to the acceptance, custody and use of

customers' securities, deposits and credit balances.15

The examples of insurance for credit unions and broker-dealers reflect the low tolerance

for even small losses to the customers of financial intermediaries and the drive for equal

competitive advantage. Although concern about the effects of failures on the stability of the

financial system were often discussed, it motivated few of the participants in the legislative

process. The spread of insurance to non-depository intermediaries, where a financial panic or run

is not a concern, highlights this fact. Both pension funds and insurance companies responded to

25

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

the favorable political circumstances to demand insurance. Underfunding of private defined-

benefit pension plans left workers without pensions when their employers went bankrupt. The

Pension Benefit Guaranty Corporation (PBGC) was established by Title IV of the Employee

Retirement Income Security Act (ERISA) in 1974 to protect retirement incomes from defined

benefit pension plans. Financed by premiums collected from companies, the PBGC's coverage of

pensions reached over one third of work force by 1995 (PBGC, Annual Report, 1995). While

insurance of pensions became a federal responsibility, the guarantee of life insurance became a

state responsibility as the federal government had never ventured to regulate life insurance. Before

1970, only New York had a guarantee system to protect policy holders. A rise in failures of life

insurance companies prompted the National Association of Insurance Commissioners to

recommend a model guarantee system to state legislatures in 1970. Although the plans varied

from state to state, funds guarantee insurance in all 50 states (Brewer and Mondschean, 1993).

By the early 1970s, financial pressures had pushed the insurance of liabilities beyond the

banking system to the securities, pension and insurance industries. There was no anticipation that

the FDIC, FSLIC, NCUSIF, SIPC, PBGC, or state insurance systems could fall into trouble. In

fact, the spread of insurance helped to prompt new demands from depositories for increased

protection.

The 1974 Increase in Insurance

In 1973, Fernand St. Germain (D.-R.I.) offered a bill to increase deposit insurance from

$20,000 to $50,000 and provide 100 percent insurance for all government deposits, amending the

FDIC Act and the National Housing Act, and the Federal Credit Union Act. Where did this

26

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

demand for more protection come from? Once again, there was no cry by the public for increased

protection. As seen in Figure 1, inflation had reduced the real value of insurance after the 1969

increase, but a $50,000 increase would have been a huge increase in real coverage. Total FDIC

coverage of deposits in Figure 2 had sagged a bit, but it was slight for all sizes of banks in Table

3,

The interest group at work behind this new proposal was the thrift industry, although some

banks were also eager for higher levels of coverage. An appeal was made to raise coverage to

$50,000 to achieve parity with the securities industry—even though the brokerage accounts only

had insurance of $20,000 for cash. Frank Willie, Chairman of the FDIC took the view of the small

banks in testifying that more insurance was required because "depositors seem to believe that their

money is safest in the largest institutions....a depositor is more likely to put funds exceeding the

insured limit in a large commercial bank than a small one." (U.S. House of Representatives,

Hearings 1973 p. 14). In addition, he pointed out that more insurance would reduce the flight of

funds from depository institutions to non-deposit institutions and markets.

The thrifts appeared to be especially eager to attract state and local deposits and were

relentless in their Congressional testimony about the need for 100 percent insurance government

deposits (U.S. House of Representatives, Hearings 1973). The representative of the U.S. Savings

& Loan League described the cumbersome process of depositing county or state funds into

multiple accounts, none exceeding the $20,000 limit, to ensure full protection. In addition, many

states required that bonds be used to collateralize deposits, with requirements varying from one

locality to the next. Donald P. Lindsay of the National League of Insured Savings Associations

gave an example from the King Country treasurer of Washington State who kept 552 S&L

27

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

passbook accounts to ensure that county funds were fully protected. He also gave the example

of a city treasurer in Washington State who mistakenly calculated the FSLIC coverage within one

S&L and lost funds. The National Association of Mutual Savings Banks supported 100 percent

insurance of government deposits, hoping for more business (U.S. House of Representatives,

Hearings. 1973). The Vice President of the Credit Union National Association, William D. Heier,

supported the St. Germain bill. Since the Federal Credit Union Act prohibited federal credit

unions from receiving funds from state and local governments, he proposed an amendment to

allow credit unions to receive such funds.

While Willie favored higher individual coverage, he resisted full coverage for government

deposits. The Chairman of the FDIC pointed out that public depositors losses had been very

small and they had recovered 99 percent of funds from failed banks. He was concerned that this

innovation would imperil the insurance fund. An increase in coverage of all deposits to $50,000

would have caused the ratio of the insurance fund to insured deposits to fall from 1.28 to 1.13

percent. Willie did not find this alarming, except when coupled with 100 percent insurance for

public units. The full coverage for public units would have driven the coverage of the insurance

fund to 1.04 percent. At such a level, the fund might be easily exhausted if large banks continued

to fail. l6 In contrast, Thomas R. Bomar, head of the FHLBB, was more sanguine and fully

supported the position of the thrift industry, testifying that the FSLIC fund would not be put at

risk by 100 percent insurance of government deposits (U.S. House of Representatives, Hearings.

1973).

In spite of the growing demands from many parts of the financial industry for more and

more insurance, some sectors resisted. One official of the American Bankers Association, H.

28

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Phelps Brooks, Jr. president of the Peoples National Bank of Chester, South Carolina made their

case: "Full insurance coverage of public accounts will open the door to pressure for 100 percent

insurance of all accounts. Account holders with quasi-public responsibility could well ask why

their savings or checking accounts above $20,000 are any less important than Government

funds...When the county sewer district promptly receives 100 percent of its deposits upon closing

of the institution, the officials at the local private hospital will certainly feel entitled to special

consideration. Then other depositories with large accounts would not understand why their

accounts are not fully covered." Brooks concluded that 100 percent coverage would have

detrimental effects on the sound management of depository institutions (U.S. House of

Representatives, Hearings. 1973, p. 114).

Faced with these strongly held conflicting positions, Congress passed compromise

legislation in 1974. Insurance on accounts of individuals and businesses was lifted to $40,000,

while government deposits guarantee was hiked to $100,000. This legislation applied to

commercial banks, mutual savings banks, and thrifts. SIPC protection was raised to $100,000 in

cash and securities, with a $40,000 maximum for cash. The result was a dramatic rise in real

protection as seen in the data for the FDIC. The real value of insurance rose in Figure 1, as did

the total coverage of deposits in Figure 2. All sizes of banks, except the very largest, as seen in

Table 3, achieved much higher rates of protection for their deposits and accounts. Five years of

legislation, beginning in 1970, had spread insurance to institutions beyond the banking system and

dramatically raised the level of insurance for all accounts. Until the S&L crisis broke, a further

increased in insurance appeared unlikely.

29

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

$100,000 Insurance and Too-Big-To-Fail

The collapse of the S&L industry has been extensively chronicled (Barth, 1991; Kane,

1989; and White, 1991). By the end of the 1970s, the income and net worth of the thrift industry

was plummeting. Measured by book value in, net worth of the thrift industry fell from 5.7 to 4.0

percent between 1977 and 1982, but any market value method showed the industry as whole to

be insolvent by about $100 billion. The FSLIC possessed only $6.5 billion of reserves and could

have paid off only a fraction of the deposits of insolvent thrifts. The housing industry did not want

massive S&L closures and the Reagan administration had no desire to see a doubling of the federal

deficit. A militant S&L lobby pressured the FSLIC into a policy of forbearance—putting off any

serious attempt to discipline or close thrifts. With generous PAC money, the thrifts also helped

to persuade Congress to give it another chance to recover.

The results of intense lobbying by the thrifts and other financial institutions were the

Depository Institutions Deregulation and Monetary Control Act of 1980 (DIDMCA) and the

Garn-St, Germain Act of 1982. All financial institutions, banks and thrifts, began a phased

eliminated of interest rate ceilings over the next six years. The 1982 Act authorized banks and

thrifts to offer money market deposit accounts to compete with money market mutual funds.

Furthermore, S&Ls were given a whole new range of powers. They were released from their

traditional portfolio constraints and permitted to increase consumer loans, commercial real estate

mortgages and business loans. In addition to this legislation, the FHLBB diluted capital

requirements.

Congress did not openly discuss the issue of deposit insurance. There was considerable

opposition to any further protection. Federal bank regulators strongly opposed an increase in

30

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

coverage, emphasizing that it would cause some institutions to take more risks. Instead, the

increase in coverage was added quietly and quickly to DIDMCA in a House-Senate conference

session to placate the thrifts who feared the impact of interest rate deregulation (Litan, 1994).

The 1980 act raised federal deposit insurance coverage on individual accounts from

$40,000 to $100,000 for banks, thrifts, and credit unions. Customer accounts for broker-dealers

were now insured for up to a maximum of $100,000 in cash and $500,000 for both cash and

securities. The result of this legislation was a big increase in the real value of insurance per account

(Figure 1) to approximately three times the level of 1935. The percentage of insured deposits was

racheted up (Figure 2); and, as Table 3 shows, the leap from $40,000 to $100,000 brought a much

higher rate of protection for all classes of banks.

Deposit insurance was locked firmly in place, yet since 1980, there has been no further

increase in deposit insurance. As of 1996, it has been sixteen years since there was any nominal

increase in coverage. Unlike the end of two period s of similar length, 1934-1950and 1950-1966,

there is no swelling demand for a new rise. The real value of insurance per account has declined

with inflation, but it is still more than 50 percent higher than the 1934 level, Some constraints

have been placed on insurance. There been some additional limits placed on the coverage of

accounts to limit the creation of joint and multiple accounts to expand coverage.17 Following the

1986 increase in the minimum capital ratio to 6 percent (White, 1992), the Federal Deposit

Insurance Corporation Improvement Act of 1991 mandated the creation of risk-based insurance

premiums in an attempt to control the problem of moral hazard.

While the high real level of coverage may have reduced the demand for insurance, there

are other important factors at work, most notably, the "too-big-to-fail" policy providing de facto

31

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

100 percent insurance. Deposit insurance was a useful instrument for guaranteeing relatively

small deposits. The advent of very large denomination, uninsured certificate of deposits allowed

banks greater ability to manage their liabilities. But, it left them subject to the judgment of the

money market. Rumors of insolvency panicked large CD holders into a run on Continental Illinois

in 1984. The Federal Reserve and the FDIC intervened to protect all depositors, large and small,

because they feared that losses would precipitate runs on other banks, generating a system-wide

crisis. The bailout of Continental Illinois certified the too-big-to-fail policy that had been evoked

in the early 1970s in the case of selected banks, like Franklin National (Sprague, 1986). Although

initially aimed at only the money center banks, the doctrine was extended in varying degrees to

other big banks (Boyd and Gertler, 1993). This subsidization of risk taking by large banks

produced an incentive to grow. When combined with the reduction in geographic barriers to

branching and holding companies, a merger and acquisition wave began in the 1980s. The

winnowing of weak institutions in the bank and thrift crises of the decade and this consolidation

of the banking industry has reduced the lobbies that previously pushed for higher coverage while

leaving deposit insurance firmly in place.

Conjecture and Conclusion

In the public's eye, deposit insurance was is still considered to be one of the great successes

of the New Deal. While many economists no longer hold it in such high regard, any serious

rollback is politically inconceivable. Public acceptance of deposit insurance for banks and thrifts,

even with numerous costly failures, has enabled these intermediaries to obtain higher levels of real

coverage and made it easier for other institutions to press their claim for insuring their liabilities,

32

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

A reasonable policy question is whether the cost of deposit insurance exceeded the cost of bank

failures in the absence of deposit insurance, following the Great Depression. This Counterfactual

is potentially complex, and I will only consider here the case with the available complete data for

the FDIC.

The New Deal greatly altered the structure of the financial system. The constraints that

were placed on banks allowed other intermediaries to capture what potentially would have been

banking business. Thus, the size of the banking sector is smaller than it would have been in the

absence of the New Deal. Similarly, the regulations on bank portfolios altered the liquidity and

risk of banks, affecting the probability of bank failure. Any attempt at constructing what the

banking system would have looked like and how many failures would have occurred in the absence

of the New Deal requires grand simplifying assumptions. Aware of these difficulties, I offer here

a simple, suggestive Counterfactual where macroeconomic policy continued to be generally

stabilizing after World War II, preventing any new great depression.

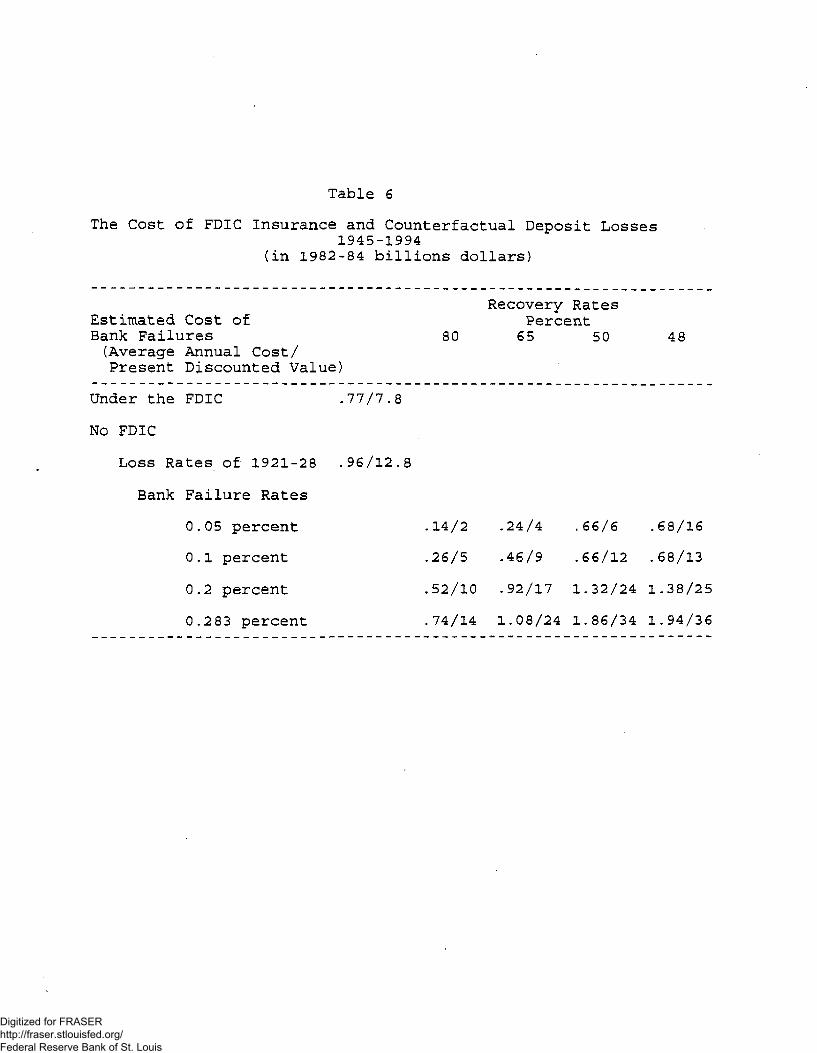

First, I estimated the real cost of bank losses under the FDIC from 1945 to 1994. The

cost here is taken to be the administrative and operating expenses of the FDIC plus the losses from

bank failures. To estimate the latter, I considered the losses from the three types of FDIC

interventions: deposit payoffs, deposit assumptions, and assistance transactions. For payoffs, I

took the estimated losses (disbursements less recoveries) plus the deposits not reimbursed by the

FDIC (estimated by the total deposits times fraction of uninsured deposits).18 For assumptions

and assistance transactions, the estimated losses to the FDIC were used. The total losses for each

year were converted into real dollars, employing the consumer price index where 1982-1984 is the

base year. As presented in Table 6, the total cost of resolving bank failures with the FDIC was

33

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

$39 billion for 1945-1994 or an annual cost of $770 million. The present discounted value of the

cost of bank failures from the beginning of the postwar era, 1945, was $7.8 billion. This starting

date was selected to omit the chaos and clean up of the thirties.

What the bank failures would have looked like in the absence of the New Deal is difficult

to estimate. Banking and Monetary Statistics (1943) reported the estimated losses to depositors

for all bank failures from 1921 to 1941. The average annual loss rate on total bank deposits for

1921-1928, the nearest period of stability without insurance, was 0.1032 percent. If we assume

that the structure of the banking system after 1945 remained essentially the same as it was in the

1920s and the shocks to the economy were the same, then we could use the loss rate to estimate

the losses to depositors in the absence of the FDIC. Multiplying the loss rate times the real

deposits of insured banks for each year of 1945-1994, yields a potential annual loss of $960 million

or a present discounted value of $12.8 billion. There is also reason to think that this is a high

estimate because the banking system was undergoing a shake out in the 1920s, as many small

banks were disappearing. The Great Depression accelerated this process and eliminated virtually

any bank showing signs of weakness. The recession of 1936-37 would have produced a further

winnowing of banks. Furthermore, the New Deal halted the process of merger and consolidation

that had started in the 1920s. This development would have certainly continued more vigorously

in the post-World War II period in the absence of New Deal banking regulation. Both the

destruction of weak banks and the formation of larger banks would have produced a stronger

banking system with fewer losses.

An alternative approach to estimating the losses to depositors in the absence of the FDIC

is to using varying bank failure rates and recovery rates. The percentage of deposits in suspending

34

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

banks to total deposits for the period 1921-1928 was 0.291 percent. For a slightly longer period

for just national banks, 1907-1929, it was 0.283. Table 6 offers four possible failure rates.

Beginning in 1907, the Comptroller of the Currency (U.S. Comptroller of the Currency, Annual

Reports and see Calomiris and White, 1994) produced detailed records of the recoveries and

losses for national banks. No single detailed source exists for state chartered banks. The recovery

rates used are the percentage paid out on proved claims three years after suspension. After three

years, recoveries are very low. The average recovery rate for suspended national banks from

1907 to 1927, weighted by bank deposits, was 48 percent.19 The recovery rate for the FDIC on

its disbursements for failed banks from 1934 to 1994 was 65 percent (FDIC, Annual Report.

1994). Whether the FDIC was more efficient than the receivers under the national banking system

or the nature of the failures or economic conditions were different is difficult to determine. Rather

than hazard a guess, Table 6 offers several recovery rates, ranging from 20 to 80 percent and

including the FDIC and national bank suspension rates.

Table 6 provides a range of Counterfactual estimates. If banks in the post-1945 period

continued to fail at the same rate as national banks had in 1921-1927 and had the same low

recovery rate, depositors might have been hit with losses of $1.86 billion per year, much more than

under the FDIC. However, this estimate is certainly an upward bound. If failure rates were lower

and recovery rates were higher-both plausible facts with a stronger banking system-then costs

to depositors would have been similar or even lower than under the FDIC. For a broad range of

estimates, it appears that the FDIC did not reduce costs and may have raised them.

Unfortunately, given the absence of comparable data, it was not possible to conduct this exercise

for the FSLIC. However, the sheer magnitude of the S&L disaster of the 1980s relative to the

3?

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

calm of the 1920s strongly suggests that the FSLIC imposed very high costs compared to an

uninsured system.

Even given the tenuous nature of these estimates, it is hard to escape the conclusion that

deposit insurance did not substantially reduce the aggregate losses from bank failures and may

have raised them. What it did do was to alter the distribution of losses. Instead of a small number

of depositors bearing the losses of a relatively small number of banks, costs were distributed to

all depositors and hidden in the premia levied on the banks. While these costs remained large in

aggregate, they appeared to have vanished to the individual depositor. The change in the

distribution of the costs of failure made the FDIC a widely accepted program and has ensured the

continuance of deposit insurance into the next century.

32

Digitized for FRASER http://fraser.stlouisfed.org/ Federal Reserve Bank of St. Louis

Notes

1. For complete descriptions of the New Deal's banking regulations and their evolution over timesee Golembe (1986), Macey and Miller (1992), and White (1992).

2. In 1936, the 10,014 batiks with deposits of under $1 million had 85 percent of their depositsinsured, while the 209 largest banks with deposits over $25 million had only 28 percent of theirdeposits covered. See Table 2.