59

Legal Procurement Conference Twitter: #RLPC12

Leading global excellence in procurement and supply

Legal Procurement Conference

Twitter: #RLPC12

Leading global excellence in procurement and supply

Karl Chapman

Chief Executive Riverview Law

Twitter: @karlchapman100

Twitter: #RLPC12

Leading global excellence in procurement and supply

Redefining Legal Procurement

• Welcome • Emergency procedures • Presentations • Twitter #RLPC12 • Conference objectives:

- How the legal market is changing - What is the impact of new entrants - How will legal services will be delivered in the future - How professional buyers can add value to their organisations

Leading global excellence in procurement and supply

Redefining Legal Procurement

• Conference structure - A CIPS Perspective: Malcolm Youngson - The Legal Market: Professor Stephen Mayson - A Law Firm Perspective: Sir Nigel Knowles - Some Procurement Themes: Richard James - A Practical Example: Anne-Marie Amatt - The Panel Debate: You

Leading global excellence in procurement and supply

Malcolm Youngson

Head of Membership CIPS

Twitter: #RLPC12

Leading global excellence in procurement and supply

Professor Stephen Mayson

Director

Legal Services Institute

Twitter: #RLPC12

THE LEGAL SERVICES ACT AND ITS IMPACT

Professor Stephen Mayson

The market for legal services

• Large, valuable (c. £28bn); continuing to grow?

• Affected variously by:

– the economy and Government policy (inc. legal aid)

– ‘fragmented’ providers and ‘polarised’ legal economy

– general forces of competition

– implementation of the Legal Services Act 2007

• Therefore increasingly differentiated:

– clients/sectors; services/products; geography; access to work and routes to market; method/style of delivery and people employed; ownership

Practising solicitors

Source: The Law Society

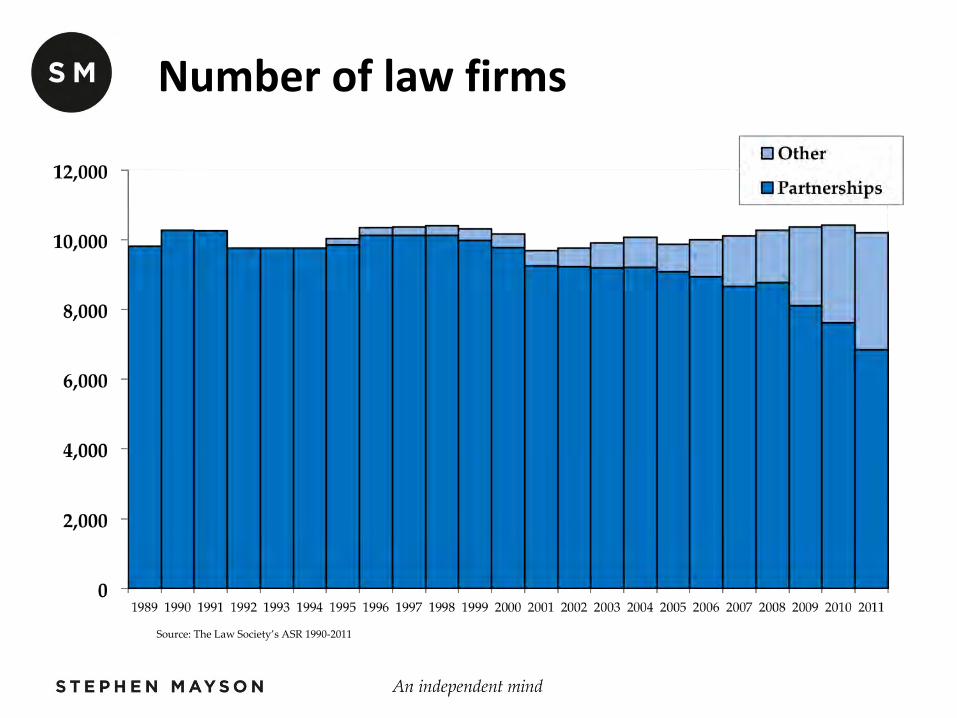

Number of law firms

Source: The Law Society’s ASR 1990-2011

Size profiles: firms 2011

Source: The Law Society’s ASR 2011

1.8%

3.2%

8.8%

41.2%

45.0%

Pressures driving change

• Complaints and restrictive regulation

• Buyer expectations, bargaining power, and cost/ funding/ value for money

• Access to work/ volume capture and distribution

• Cost-efficiency and resourcing; use of lawyers; project management;

• Accessibility (real / virtual; physical/ remote)

• Ownership vs. management, and the quality of management; governance and risk management

• Need for capital (working capital + investment)

Impact of the LSA

• New complaints structure

– single point of access (Legal Ombudsman)

• New oversight of regulation

– separation of regulation and representation

– overarching regulator (Legal Services Board)

• Liberalisation

– allows lawyers to do things they couldn’t before

– allows ‘non-lawyers’ to do things they couldn’t before

– NOT de-regulation

Why the LSA might not be so important

• A process of continuing substitution – non-lawyers for lawyers

– IT for human beings; virtual for physical

– referrers for direct client access (cf. the Bar?)

– new providers for law firms

– external for internal (e.g. outsourcing, capital)

– corporate structures for partnerships

– professional managers for gifted amateurs

– differentiated rewards for total return

– equity for debt; capital for income

– brand for reputation?

Benefits to new entrants

• Regulated access to the legal services market – barriers to entry vs. the burden of compliance – cf. legal aid: a significant ‘market’, but brand risk?

• Ability to bundle and price services / products – attraction of criminal work, legal aid?

• Ability to innovate and control delivery – standardise and commoditise: technology and process – certainty of pricing (might not be cheaper)

• Access to returns from legal services – brand, market share and consumer loyalty; retail dominance – economies of scale – revenue and capital returns

Who’s shown an interest?

Impact on the public

• Competition for custom – loyalty to brands; complaints handling

– buying power and scale economies

• Innovation in delivery – geographical dispersion; virtual access

– more consumer-focused, user-friendly, accessible

– standardisation and commoditisation

• Bundling and one-stop shops?

• Cheaper and higher quality?

• Unregulated providers

Strategic adviser, non-executive and business coach

+44 1525 261386

+44 7860 713223

http://www.StephenMayson.com

http://www.StephenMayson.com

http://uk.linkedin.com/in/StephenMayson

http://twitter.com/StephenMayson

Leading global excellence in procurement and supply

Sir Nigel Knowles

Joint CEO and Managing Partner

DLA Piper

Twitter: #RLPC12

Leading global excellence in procurement and supply

Richard James

Senior Procurement Specialist

Proxima

Twitter: #RLPC12

The Legal Services Act What does it mean for buyers?

Richard James 17 September 2012

Agenda

• Buying Legal Services

• The Legal Marketplace in 2012

• What does the LSA mean for Buyers?

• Conclusions

About Proxima Company Profile

With over 250 procurement specialists deployed across the globe we manage procurement for a growing range of clients across several industries and across multiple geographic regions. Our relentless drive to add value for our clients is demonstrated by the longevity of many of those relationships.

24 © Proxima 2012. All rights reserved 24

Nu

mb

er o

f C

on

tra

cts

2000 2012 2005

Date of Contract Win

Proxima and Legal Services

In the last two years we have conducted a dozen exercises in the Legal Services arena for a diverse range of clients in the UK and internationally

Engagements have ranged through:

Advisory services and category strategy development

Project-based procurement

Legal panel selection and negotiation

Implementing legal engagement and supplier management processes

Buying Legal Services

© Proxima 2012. All rights reserved 25

What is different about buying Legal Services?

© Proxima 2012. All rights reserved 26

You are essentially buying “knowledge” or scarce specialist skills

Those involved are often very senior, with a high degree of subject matter expertise and inherently strong relations

The traditional time and materials cost model does not lend itself to efficiency or good cost management

The market value of these skills is often intangible or difficult to measure objectively

The outputs are often difficult to value or even to define at the outset

Value or risk is usually much higher than the fees: costs may not be high on the agenda

5 Common Mistakes, Myths or Misconceptions

© Proxima 2012. All rights reserved 27

“Show me the money”

“It’s not what you know, it’s who you know”

“You get what you pay for”

“Everyone hates lawyers”

Procurement has no right to be involved in buying legal services

The LSA: out of the frying pan…?

© Proxima 2012. All rights reserved 28

What did Procurement ever do for me?

The world has changed since 2008

The profile/challenge for Procurement has changed

Cost management as a profit driver New areas of influence – no sacred cows Increased focus on “indirects” Public and private sector profile has been raised

How Procurement reacts will determine our future role

© Proxima 2012. All rights reserved 29

Impact on the Legal marketplace

© Proxima 2012. All rights reserved

Business Failures

Mergers

But…

30

Global Expansion

The Magic Circle are still the Magic Circle PEP and margins are still high The best lawyers are still busy (and expensive)

The sands have shifted commercially

© Proxima 2012. All rights reserved 31

Discounted fees

The rise of the regions

Legal services outsourcing and offshoring

The march of the mid-tier

The Legal Services Act!

Alternative pricing • Fixed/capped fees • Contingent fees • Incentive payments • Value-based fees

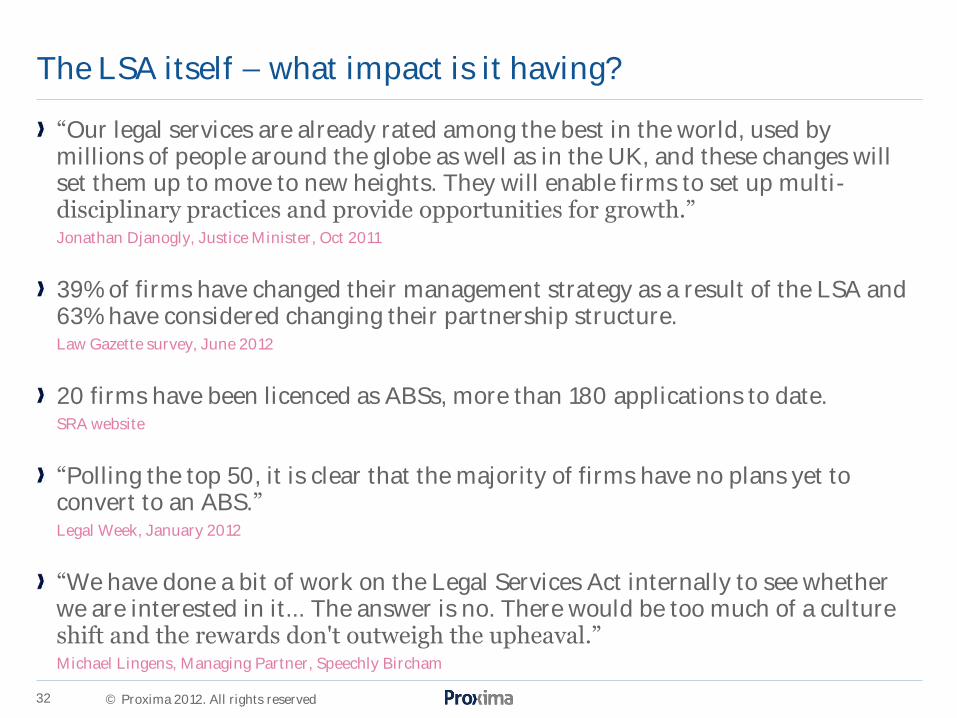

The LSA itself – what impact is it having?

“Our legal services are already rated among the best in the world, used by millions of people around the globe as well as in the UK, and these changes will set them up to move to new heights. They will enable firms to set up multi-disciplinary practices and provide opportunities for growth.” Jonathan Djanogly, Justice Minister, Oct 2011

39% of firms have changed their management strategy as a result of the LSA and 63% have considered changing their partnership structure. Law Gazette survey, June 2012

20 firms have been licenced as ABSs, more than 180 applications to date. SRA website

“Polling the top 50, it is clear that the majority of firms have no plans yet to convert to an ABS.” Legal Week, January 2012

“We have done a bit of work on the Legal Services Act internally to see whether we are interested in it... The answer is no. There would be too much of a culture shift and the rewards don't outweigh the upheaval.” Michael Lingens, Managing Partner, Speechly Bircham

© Proxima 2012. All rights reserved 32

What’s happening in practice?

© Proxima 2012. All rights reserved

Private Equity Investment

Business Partnership

Global Investment

New Investment Models

New Entrants

Expanding Operations

33

Flotation

?

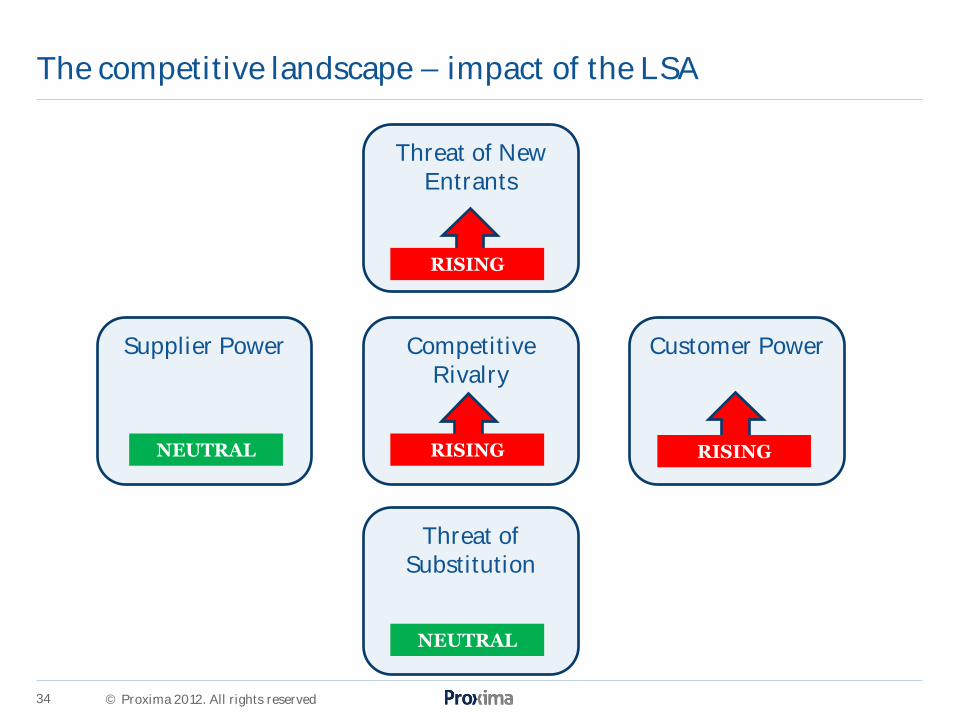

The competitive landscape – impact of the LSA

© Proxima 2012. All rights reserved 34

Supplier Power

NEUTRAL

Threat of Substitution

NEUTRAL

Competitive Rivalry

RISING

Customer Power

RISING

Threat of New Entrants

RISING

The competitive landscape – high street

© Proxima 2012. All rights reserved 35

Supplier Power

NEUTRAL

Threat of Substitution

MODERATE

Competitive Rivalry

RISING

Customer Power

VERY HIGH

Threat of New Entrants

INTENSE

The competitive landscape – mid-tier corporate

© Proxima 2012. All rights reserved 36

Supplier Power

NEUTRAL

Threat of Substitution

NEUTRAL

Competitive Rivalry

VERY HIGH

Customer Power

VERY HIGH

Threat of New Entrants

MODERATE

The competitive landscape – Magic/Silver Circle

© Proxima 2012. All rights reserved 37

Supplier Power

NEUTRAL

Threat of Substitution

NEUTRAL

Competitive Rivalry

RISING

Customer Power

MODERATE

Threat of New Entrants

NEUTRAL

Relationships are a value driver, not a threat

© Proxima 2012. All rights reserved 38

Love your enemy

Seek and you will find

Fear not, for I am with you

Know your enemy

Be proactive: Drive the relationship and

outcomes you need

So what does it mean for buyers?

© Proxima 2012. All rights reserved 39

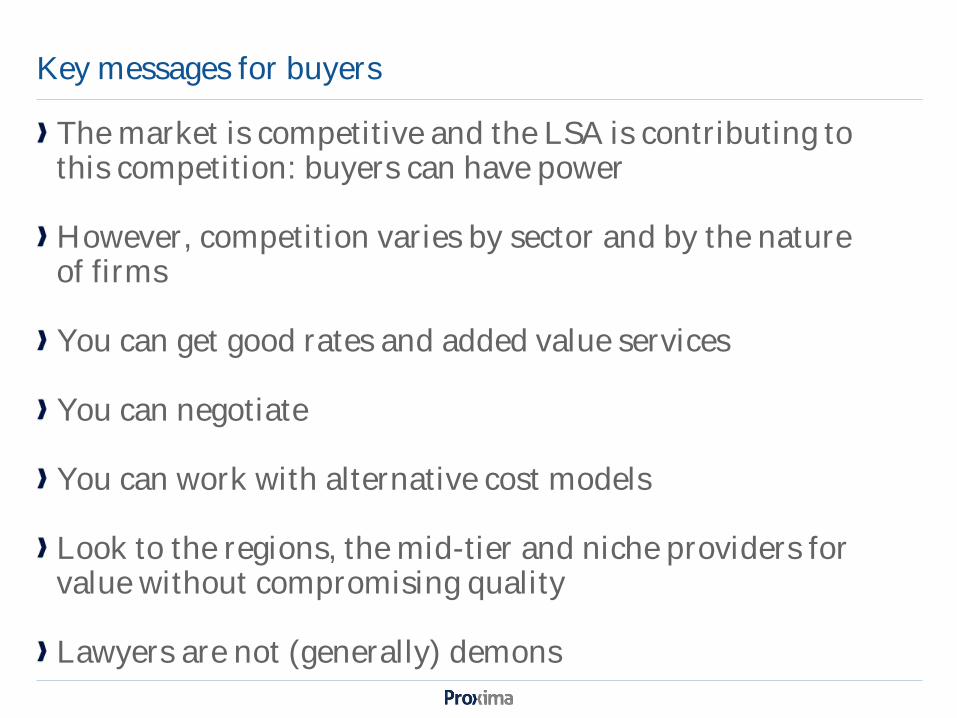

Key messages for buyers

The market is competitive and the LSA is contributing to this competition: buyers can have power However, competition varies by sector and by the nature of firms You can get good rates and added value services You can negotiate You can work with alternative cost models Look to the regions, the mid-tier and niche providers for value without compromising quality Lawyers are not (generally) demons

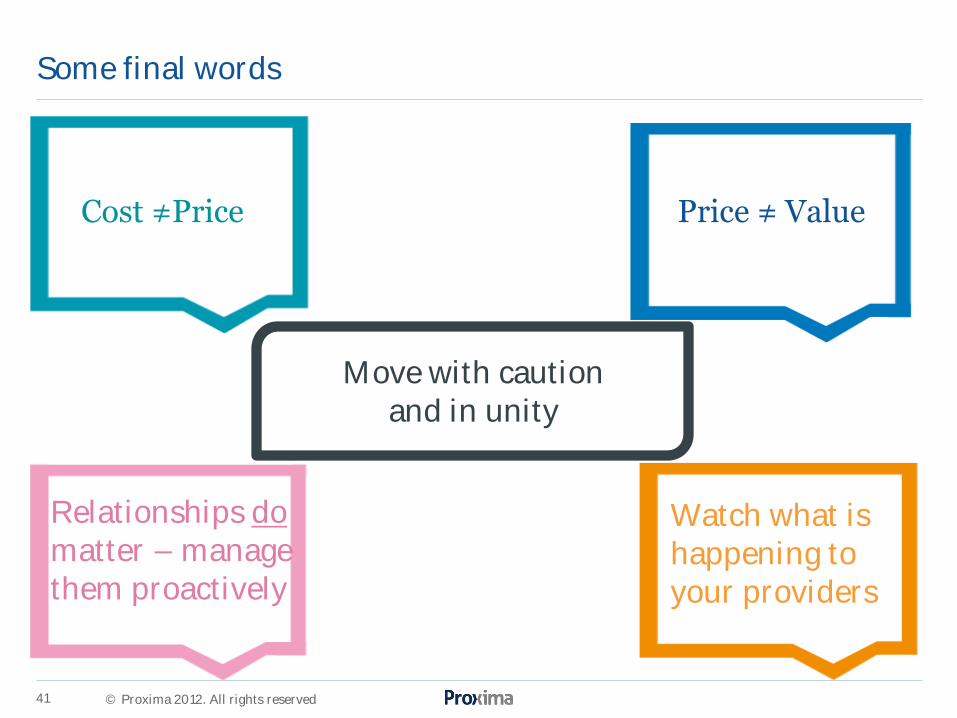

Some final words

© Proxima 2012. All rights reserved 41

Price ≠ Value

Relationships do matter – manage them proactively

Watch what is happening to your providers

Cost ≠Price

Move with caution and in unity

Leading global excellence in procurement and supply

Anne-Marie Amatt

Senior Category Manager

E.ON UK

Twitter: #RLPC12

Wednesday, 19 September 2012

Anne-Marie Amatt Professional Services Category Manager

THE DEVELOPMENT OF A LEGAL CATEGORY

• Start of the Journey

• Approaching the category

• Building Relationships • Tackling the spend • Changing Market Place

OVERVIEW OF THE LEGAL CATEGORY

PROFESSIONAL SERVICES CATEGORY

45

CONSULTANCY LEGAL

FINANCIAL SERVICES

IN HOUSE LEGAL TEAM

•DON’T HAVE TO USE US

46

•DON’T WANT US

•DON’T NEED US

Stakeholder Maps

Speak to suppliers

Investigate the market

Analysis of spend

Offer a Service

Demonstrate value

Listen and be flexible

APPROACHING THE CATEGORY

Legal Spend

£

48

BUILDING RELATIONSHIPS

ACCEPTANCE

49

ACCESS HOURLY RATES APPROPRIATE

LEVEL USED

FIXED RATES

COMMERCIAL APPROACH

LAW FIRM AGREEMENT

CONTRACT MANAGEMENT

RISK SHARE

ADDED VALUE CAPTURED

BLENDED RATES

APPROPRIATE TIME APPLIED

TACKLING THE SPEND

SPEND SUPPLIER

TENDER

Tendering the Legal Spend

19 September 2012, E.ON, Page 50

Value

Spend

Supplier

Down

2009 • Property Tender • Litigation Tender

2010

• Employment • Environment • Barristers • Law Firm Agreement/Legal Team Guidelines

2011 • Commercial Projects • Scottish Property Tender • Contract Management

2012 • E Auctions • Property / Planning Tender • Panel Review – 2013 Strategy Sign off

19 September 2012, E.ON, Page 51

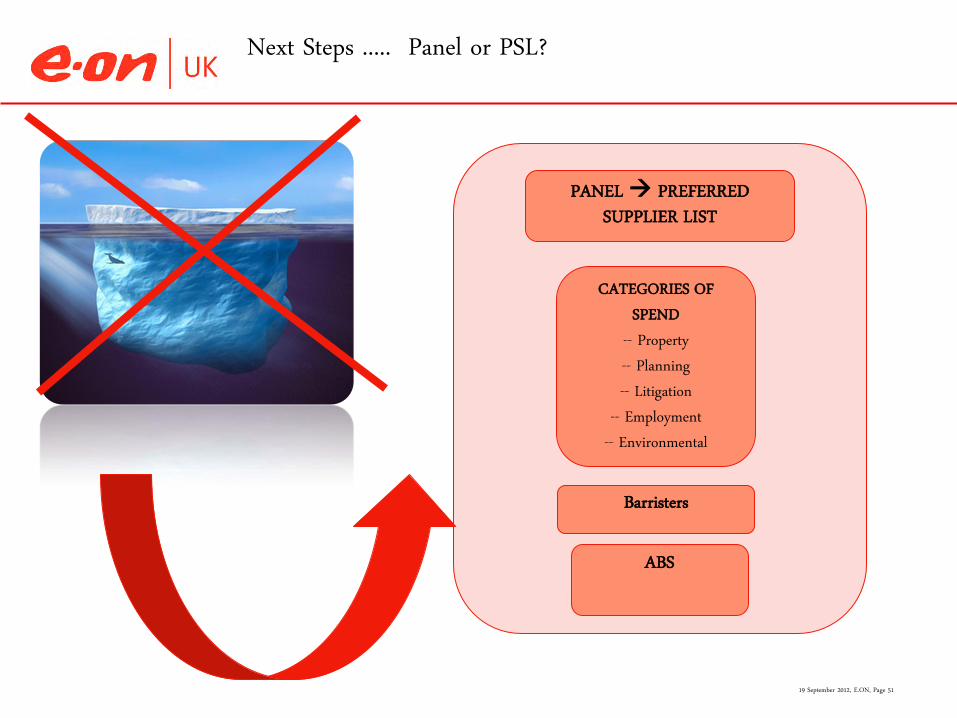

Next Steps ..... Panel or PSL?

CATEGORIES OF SPEND

-- Property -- Planning -- Litigation

-- Employment -- Environmental

PANEL PREFERRED SUPPLIER LIST

Barristers

ABS

THE CHANGING MARKET PLACE

ECONOMY

TOO MANY LAWYERS CONSOLIDATION OF LAW FIRMS

LEGAL SERVICES ACT

Beat Hess...General Counsel of Shell: “Every day has been Xmas for decades, the party is now over”

The changing face of legal services in the UK – Legal Services Act (LSA) and Alternative Business Structures (ABS)

Opportunity for the smart buyer.....UTILISATION

BUYING SMART

CHANGES TO E.ON – NEW MARKETS

Travel Policy changed use of low cost airlines

New entrants to our market place

THE TOP TEN – The Lawyer UK200 2011

Firm Revenue (£M) PEP (£000) Equity Partners Profit Margin

Clifford Chance 1,219 1,005,000 379 31% Linklaters 1,200 1,225,000 442 43% Freshfields 1,140 1,308,000 416 48% Allen & Overy 1,120 1,100,000 398 38% DLA Piper 604.9 564,000 201 19% Hogan Lovells 582 740,000 250 32% Norton Rose 488 445,000 277 25% Herbert Smith 465 900,000 131 25% Slaughter and May 448 1,930,000 122 52% Eversheds 354 555,000 132 21%

Source: The Lawyer

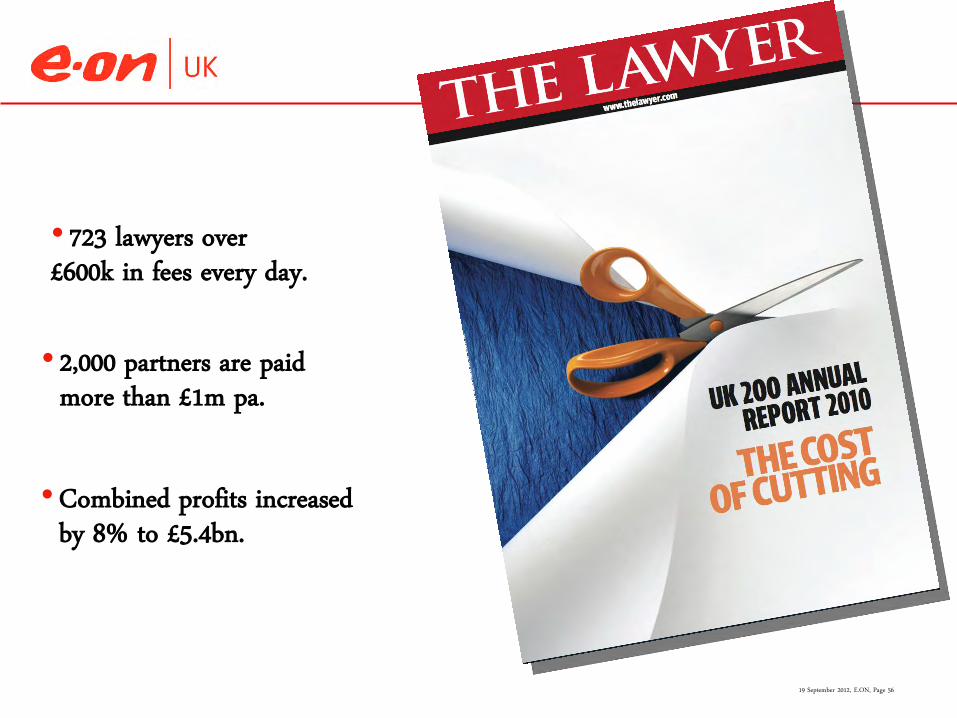

• 723 lawyers over £600k in fees every day.

19 September 2012, E.ON, Page 56

• 2,000 partners are paid more than £1m pa.

•Combined profits increased by 8% to £5.4bn.

Leading global excellence in procurement and supply

Panel Debate

Malcolm Youngson Head of Membership

CIPS

Twitter: #RLPC12

Leading global excellence in procurement and supply

Conference Close

Karl Chapman CEO

Riverview Law

Twitter: #RLPC12