35

www.walescooperative.org

| Date post: | 26-Jul-2015 |

| Category: |

Government & Nonprofit |

| Upload: | walescva |

| View: | 34 times |

| Download: | 0 times |

www.walescooperative.org

Who We AreWho We Are

• Set-up in 1982.

• Now the largest co-operative development agency in UK.

• Support co-operatives and social enterprises throughout Wales.

• Funded by: Welsh Government, European Union, Local Authorities & Consultancy fees.

Learning OutcomesLearning Outcomes

• To gain an overview of the legal forms available for organisations who may be considering applying for a Community Asset Transfer.

ContextContext

• Community Asset Transfers in Wales – A Best Practice Guide.

• P17 – “ When assessing whether a Stage 1 Expression of Interest application should proceed to a Stage 2 full business case, relevant criteria should include:– Governance, structure and history of

organisation….

• P18 – “The Applicant must be A Community / Town Council or a Third Sector organisation (TSO) which satisfies the following criteria:– Legal entity that is incorporated and provides

limited liability for the stakeholders involved, this would usually be in the form of a company, society or CIO (Charitable incorporated Organisation).

– It must enable the management/ownership of buildings and provision of services.

– Exist for community/social/environmental benefit.– Non-profit distributing – any surpluses must be

reinvested to further its community benefits/social aims….

– Decision making process influenced by local community.

Organisation TYPESOrganisation TYPES

The Best Practice guide refers to “Third Sector organisations” and specifically to:

– voluntary organisations– co-operatives– social enterprises

These are not legal forms

Legal FormsLegal Forms Company Limited by Guarantee Community Interest Company (C.I.C.) Charitable Company Charitable Incorporated Organisation

(CIO) Community Benefit Society Co-operative Society Company Limited by Shares Limited Liability Partnership

Unincorporated OrganisationsUnincorporated Organisations

VV

Incorporated OrganisationsIncorporated Organisations

Unincorporated OrganisationsUnincorporated Organisations These organisations do not have a separate legal

identity from its members. Examples of unincorporated organisations:

• Community Associations• Scout Groups• Tennant & Residents Associations• Unincorporated Charities

Individual members are personally responsible for any debts and contractual obligations.

IncorporationIncorporation

The organisation is legally separate from its members.Registered with an appropriate RegistryThe organisation can enter into contracts in its own nameCertain triggers will indicate it is time to incorporate – when “risks” increaseMembers’ liability is limited to the value of any guarantees they have given Directors can lose their limited liability in a few specific situations, for example wrongful or fraudulent trading

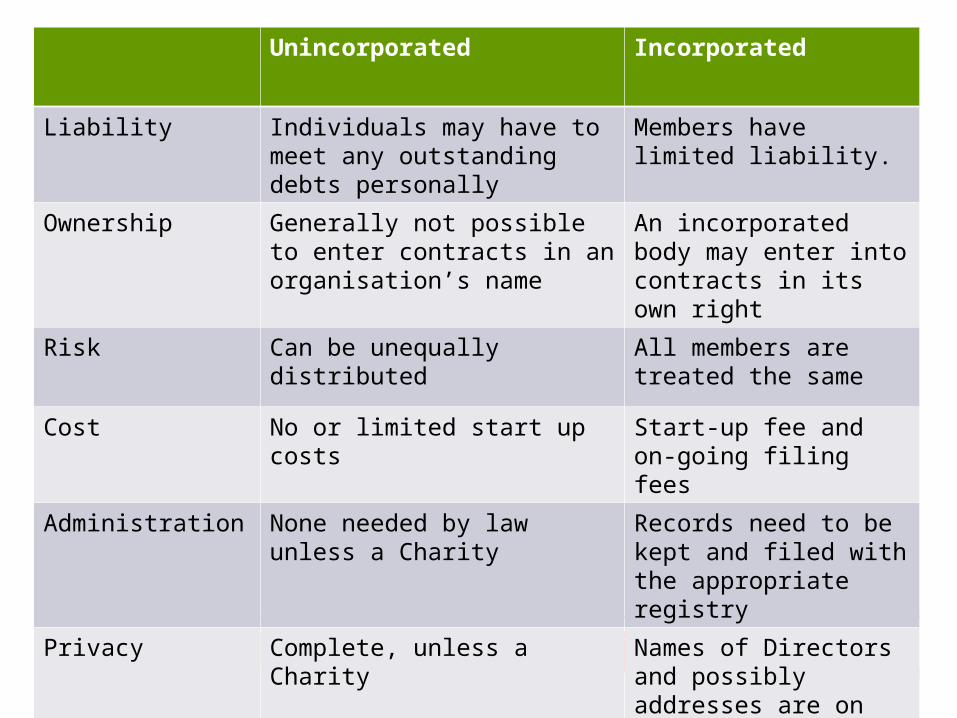

Unincorporated Incorporated

Liability Individuals may have to meet any outstanding debts personally

Members have limited liability.

Ownership Generally not possible to enter contracts in an organisation’s name

An incorporated body may enter into contracts in its own right

Risk Can be unequally distributed

All members are treated the same

Cost No or limited start up costs Start-up fee and on-going filing fees

Administration None needed by law unless a Charity

Records need to be kept and filed with the appropriate registry

Privacy Complete, unless a Charity Names of Directors and possibly addresses are on public record.

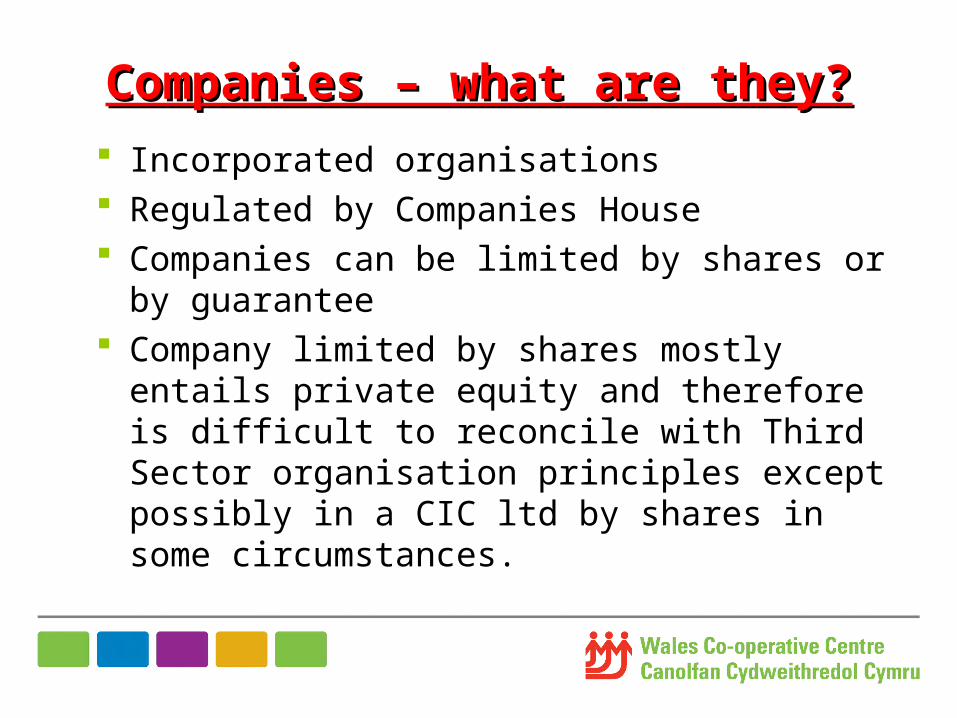

Companies – what are they?Companies – what are they? Incorporated organisations Regulated by Companies House Companies can be limited by shares or by

guarantee Company limited by shares mostly entails

private equity and therefore is difficult to reconcile with Third Sector organisation principles except possibly in a CIC ltd by shares in some circumstances.

Company Ltd by GuaranteeCompany Ltd by GuaranteePlusesPluses

Limited liability for members (usually £1) Very flexible Easiest form of company to administer Familiar legal form within the Third Sector May have social or environmental objects Must have appropriate Surplus and

Dissolution Clauses in the Articles of Association.

Relatively Simple and Cheap to set up. Could apply for charitable status

Company Ltd by Company Ltd by GuaranteeGuaranteeMinusesMinuses

No regulation of social purpose No statutory “Asset Lock” (unless

charitable when change to dissolution provisions requires charity commission consent)

Community Interest Community Interest CompaniesCompanies

Legal form specifically for social enterprises CICs can be limited by guarantee or by

shares Bolting on social purposes to company

structure Must have a community interest statement Feature a statutory asset lock Intended to make both public and

commercial funding more accessible Establish a clear social enterprise 'brand' Regulated by the CIC Regulator

Community Interest Community Interest CompanyCompany

PlusesPluses Specifically designed for social enterprises All the freedoms and flexibilities of a

normal company in terms of trading The social purpose is regulated Can provide equity with shares always at

face value (par) and a cap on aggregate dividend

Community Interest Community Interest Company Company MinusesMinuses

Each share in a CIC Ltd by shares normally carries one vote (as opposed to one member, one vote)

More regulation Cannot also apply to be a charity CIC’s do not get any charity tax reliefs even if

the objects seem to be charitable in nature.

Hay Community Enterprise Hay Community Enterprise CICCIC

• “Commercial trading enterprise”• Democratically controlled by

members. • CIC status means that the assets of

the enterprise are locked-in and cannot be sold. All profits can only be used to further the interests of the enterprise and for social, community or environmental benefit.

• It is available to hire for community events, shows, exhibitions, sales and public or private functions. Holiday accommodation to let.

Registered SocietiesRegistered Societies

Incorporated organisations Regulated by Financial Conduct Authority (FCA) Designed specifically for co-operatives and community

benefit societies Co-operative Societies are run for mutual member benefit Community Benefit Societies are run for the benefit of a

wider community rather than just the members Limited by shares – but different from company shares Exemptions from Financial Services and Markets Acts

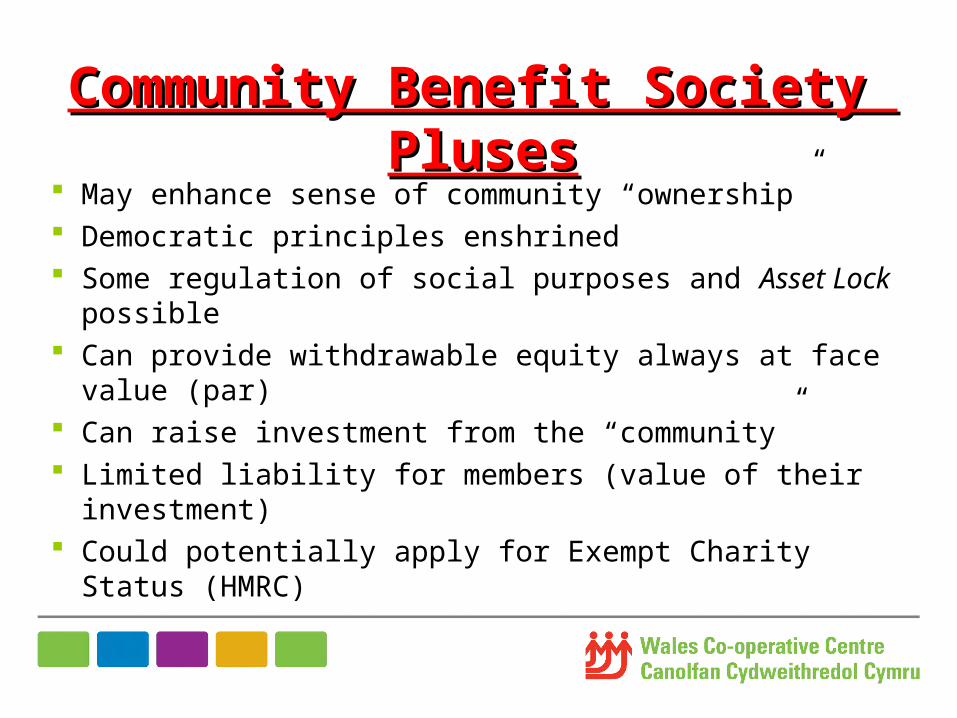

Community Benefit Society Community Benefit Society PlusesPluses

May enhance sense of community “ownership” Democratic principles enshrined Some regulation of social purposes and Asset Lock

possible Can provide withdrawable equity always at face value

(par) Can raise investment from the “community” Limited liability for members (value of their

investment) Could potentially apply for Exempt Charity Status

(HMRC)

Community Benefit Society Community Benefit Society MinusesMinuses

Unfamiliar legal form Legislation still lags behind that of

companies Cost of registration can be higher There must be three members

Charitable StatusCharitable StatusTo be a charity an organisation must:-

Be set up with purposes which are exclusively charitable

Carry out these purposes for the public benefit when you run your charity

Charities can be unincorporated or incorporated

Advantages of charitable Advantages of charitable statusstatus

Various tax advantages e.g. corporation tax exemption, National Non-Domestic Rates (NNDR) reliefs, stamp duty exemption

Well- regarded Charities can claim Gift Aid on donations

made by UK tax payers. Some funders can/will only fund charities May be more attractive from a commercial

sponsor perspective.

Disadvantages of charitable Disadvantages of charitable statusstatus

Heavily regulated by the Charity Commission

There are restrictions on trading as Charities

Employees cannot normally serve on boards

Charities and TradingCharities and TradingThere are exemptions which allow charities to trade:-

Primary purpose trade where the trade is the direct provision of the charity’s objects

Ancillary trade where the trade contributes indirectly to the charity’s objects

Non primary-purpose trading (25% of income up to income of £200k, max £50K)

A trading subsidiary could be set up if income from non primary-purpose trading are likely to exceed the Inland Revenue threshold

The Charity must not subsidise the subsidiary

Incorporated Charitable Incorporated Charitable FormsForms

• Charitable Company Ltd by Guarantee

• Charitable Incorporated Organisation

• Community Benefit Society that has Exempt Charity status

Charitable Companies Ltd by Charitable Companies Ltd by GuaranteeGuarantee

• A company ltd by Guarantee is set up with appropriate Articles of Association

• The company then applies for charitable status

Charitable Companies Ltd by Charitable Companies Ltd by GuaranteeGuarantee

PlusesPluses• A very familiar legal form within the Sector• Tried and tested• Has the advantage of charitable status and the

advantages of being a company e.g. funders / lenders can take a charge on an asset.

• It may be more appropriate for larger –scale organisations than the CIO form.

• A company can be in place fairly promptly and can work towards charitable status.

Charitable CompanyCharitable CompanyMinusesMinuses

Dual registration and regulation – Companies House and Charity Commission

Administratively more onerous and higher accountancy fees

The Charitable Incorporated The Charitable Incorporated Organisation - CIOOrganisation - CIO

A new incorporated form for a charity, not a company

Only has to register with the Charity Commission and not Companies House

Can enter into contracts in its own right and trustees will normally have limited/no liability for CIO debts

Foundation and Association models available Process for direct conversion of charitable

companies is not yet available

CIO CIO PlusesPluses

Provides a single incorporated structure for charities

Only one regulator – the Charity Commission

Easier accounts, filing, reporting Simpler constitutional form Smaller CIOs can prepare receipts and

payments accounts, while smaller charitable companies must prepare accounts on the accruals basis

CIOCIOMinusesMinuses

New, untested form Registration time Designed for small to medium charities and

may not be appropriate for those charities looking to grow.

CIO legislation makes no provision for the maintenance of a public register of charges - a lender / funder will not be able to obtain the protection of registering a charge at Companies House.

There is a completely new legal regime for CIOs, and grey areas may emerge.

Life Leisure Trust (trading as Life Leisure Trust (trading as Aneurin Leisure)Aneurin Leisure)

• Clear charitable objects encompassing recreation, arts, culture and heritage.

• Multiple sites including sport centres, theatres, libraries, parks.

• “Trading” is likely to be mainly primary purpose or ancillary.

• Clear advantages of being a charity e.g. rate relief etc.

Thank YouThank You

Any questions?Any questions?