25

Legal, Tax & Business Europe Legal, Tax & Business Europe David J. Smith David J. Smith , CEO , CEO Analysts & Investors, August 2001 Analysts & Investors, August 2001

| Date post: | 27-Dec-2015 |

| Category: |

Documents |

| Upload: | patience-whitehead |

| View: | 216 times |

| Download: | 0 times |

Legal, Tax & Business EuropeLegal, Tax & Business Europe

David J. SmithDavid J. Smith, CEO, CEO

Analysts & Investors, August 2001Analysts & Investors, August 2001

2

TABLE OF CONTENTSTABLE OF CONTENTS

• Overview of Overview of cluster cluster Wolters Kluwer LTBWolters Kluwer LTB EuropeEurope

• ChallengesChallenges

• Strategic Directions and DecisionsStrategic Directions and Decisions

• LTBLTB Europe’s Recipe for Growth Europe’s Recipe for Growth

• Future GoalsFuture Goals

• The Story The Story SSo o FFar and ar and NNext 12 ext 12 MMonthsonths

• SummarySummary

3

OVERVIEW OF LTBOVERVIEW OF LTB EUROPE EUROPE Consolidated ResultsConsolidated Results - EBITA Performance Improving - EBITA Performance Improving

* Linked to EUR 250 m* Linked to EUR 250 millionillion additional (Internet) product development spending additional (Internet) product development spending

HY1 HY1 20012001

(in EUR mln)(in EUR mln)

HY1 HY1 20002000

(in EUR mln)(in EUR mln)

+/-+/- Organic Organic growthgrowth

FY 2000FY 2000 FY1999FY1999 +/-+/-

Total salesTotal sales 658658 624624 5%5% 2%2% 1,3161,316 1,2161,216 8%8%

Total EBITATotal EBITA 129129 125125 3%3% (1%)(1%) 255255 277277 (8%)(8%)

Additional Internet Additional Internet investment *investment *

1010 44 1818 22

Total EBITA after Total EBITA after Internet investmentInternet investment

119119 121121 (2%)(2%) (1%)(1%) 237237 275275 (14%)(14%)

EBITA marginEBITA margin 18.1%18.1% 19.4%19.4% 18.0%18.0% 22.5%22.5%

4

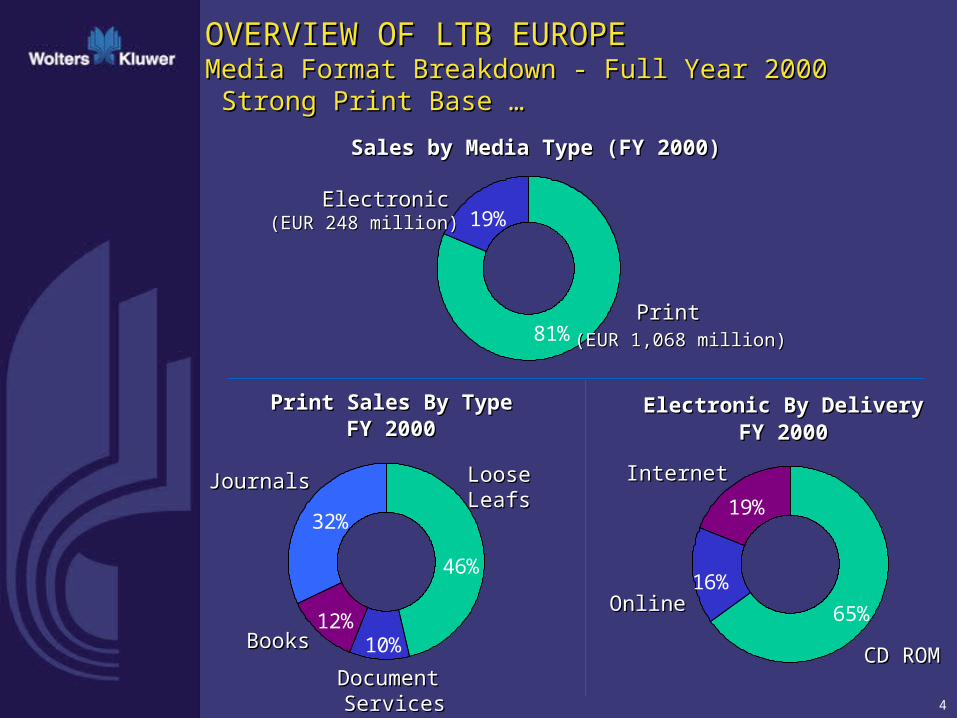

Electronic By DeliveryElectronic By DeliveryFY FY 20002000

Print Sales By TypePrint Sales By TypeFY FY 20002000

OVERVIEW OF LTB EUROPE OVERVIEW OF LTB EUROPE Media Format BreakdownMedia Format Breakdown - Full Year 2000 - Full Year 2000 Strong Print Base … Strong Print Base …

Sales by Media Type (Sales by Media Type (FY FY 2000)2000)

19%

81%

ElectronicElectronic

PrintPrint

12%

32%

46%

10%

JournalsJournals Loose Loose LeafsLeafs

BooksBooks

Document Document ServicesServices

19%

65%

16%

InternetInternet

CD ROMCD ROM

OnlineOnline

(EUR 248 million)(EUR 248 million)

(EUR 1,068 million)(EUR 1,068 million)

5

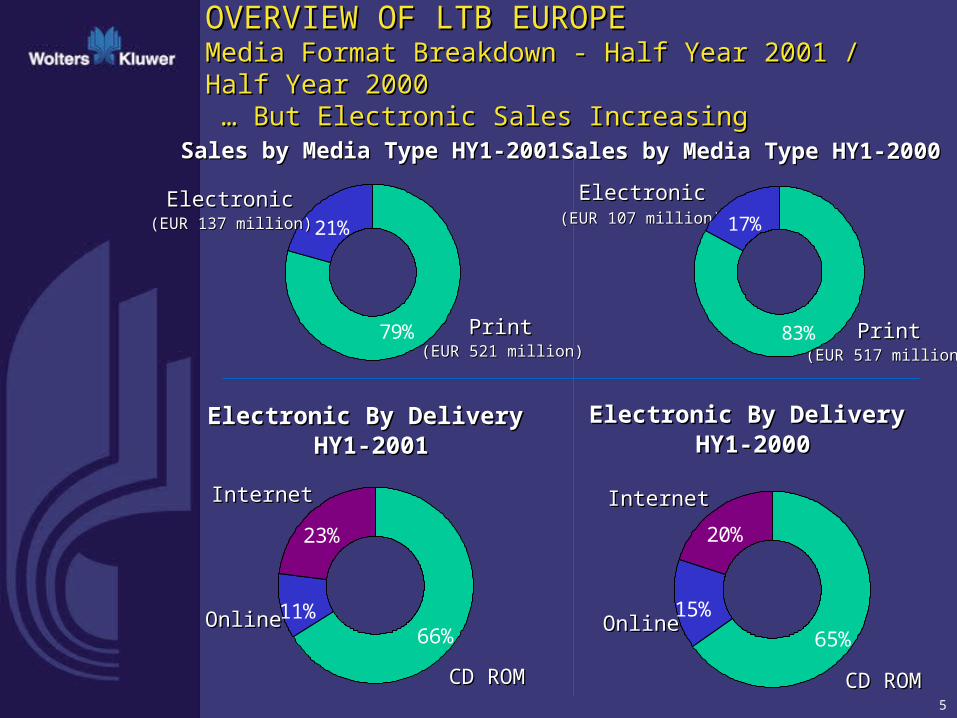

OVERVIEW OF LTB EUROPE OVERVIEW OF LTB EUROPE Media Format BreakdownMedia Format Breakdown - Half Year 2001 / Half Year 2000 - Half Year 2001 / Half Year 2000 … But Electronic Sales Increasing … But Electronic Sales Increasing

Sales by Media Type HSales by Media Type HY1-Y1-20002000Sales by Media Type HSales by Media Type HY1-Y1-20012001

Electronic By DeliveryElectronic By DeliveryHHY1-Y1-20012001

Electronic By DeliveryElectronic By DeliveryHHY1-Y1-20002000

21%

79%

ElectronicElectronic

PrintPrint

(EUR 137 million)(EUR 137 million)

(EUR 521 million)(EUR 521 million)

ElectronicElectronic

PrintPrint

(EUR 107 million)(EUR 107 million)

(EUR 517 million)(EUR 517 million)

17%

83%

23%

66%11%

InternetInternet

CD ROMCD ROM

OnlineOnline

20%

65%

15%

InternetInternet

CD ROMCD ROM

OnlineOnline

UKUKUK

UKUKBELGIUM

UKUKFRANCE

UKUKSPAIN

UKUKNETHERLANDS

UKUKITALY

UKUKCENTRAL/EASTERNEUROPE

UKUKSCANDINAVIAUKUKGERMANY

UKUKAUSTRIA

UKUKACROSS EUROPE UKUKACROSS EUROPE

OVERVIEW OF LTB EUROPEOVERVIEW OF LTB EUROPE Dense Network, Leading PositionsDense Network, Leading Positions

Reed Elsevier

Thomson

Local player

L E G E N DL E G E N D

7

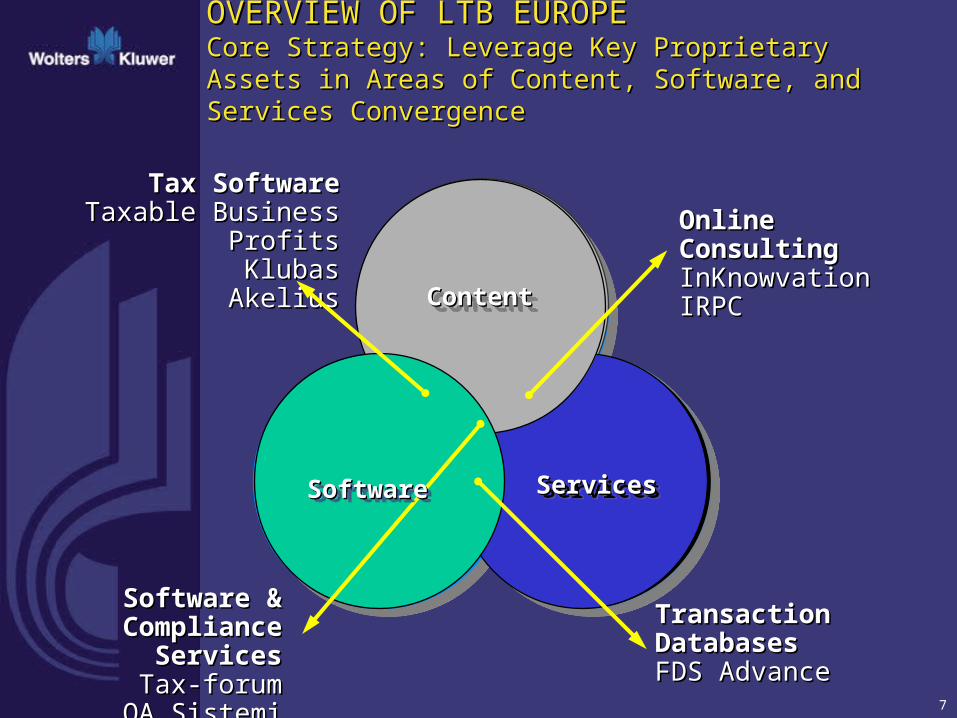

Tax SoftwareTax SoftwareTaxable Business ProfitsTaxable Business Profits

KlubasKlubasAkeliusAkelius

Transaction DatabasesTransaction DatabasesFDS AdvanceFDS Advance

Online ConsultingOnline ConsultingInKnowvationInKnowvationIRPCIRPC

Software & Software & Compliance ServicesCompliance Services

Tax-forumTax-forumOA SistemiOA Sistemi

ServicesServicesServicesServicesSoftwareSoftwareSoftwareSoftware

ContentContentContentContent

OVERVIEW OF LTB EUROPEOVERVIEW OF LTB EUROPECore Strategy: LCore Strategy: Leverageeverage Key Proprietary Assets in Areas of Key Proprietary Assets in Areas of Content, Software, and Services ConvergenceContent, Software, and Services Convergence

8

OVERVIEW OF LTB EUROPEOVERVIEW OF LTB EUROPECore Strategy: Positioning LTB Europe to move up the Value Core Strategy: Positioning LTB Europe to move up the Value ChainChain

Kluwer Fiscal GuideKluwer Fiscal Guide

La Legge (Italy)La Legge (Italy)

Nederlands Juristenblad Nederlands Juristenblad (Netherlands)(Netherlands)

El Diario La Ley (Spain)El Diario La Ley (Spain)

Fiscaal Zakboek Fiscaal Zakboek (Netherlands)(Netherlands)

Kluwer law text books (Netherlands)Kluwer law text books (Netherlands)

Base de Datos Legislacion (Spain)Base de Datos Legislacion (Spain)

Juridisque Cour de Cassation (France)Juridisque Cour de Cassation (France)

Employment Case Law Index (UK)Employment Case Law Index (UK)

Lex (Poland)Lex (Poland)

Convenios Colectivos (Spain)Convenios Colectivos (Spain)

A3res (Spain)A3res (Spain) Jura@be (Belgium) (Belgium) Tutto Lavoro Windows (Italy)Tutto Lavoro Windows (Italy) Kluwer Plaza’s (Netherlands)Kluwer Plaza’s (Netherlands) AOK-line (Germany)AOK-line (Germany) Lamyline (France)Lamyline (France) Fd-centre.net (UK)Fd-centre.net (UK)

Reference Book for Reference Book for Employers (UK)Employers (UK)

Fiscal Tax Compliance Fiscal Tax Compliance (Belgium)(Belgium)

Liaisons Social / Fiscal / Liaisons Social / Fiscal / Assurances (France)Assurances (France)

Lohnbüro (Germany)Lohnbüro (Germany)

Addition of hyperlinksAddition of hyperlinks

Integration of workflow toolsIntegration of workflow tools

Libraries of integrated contentLibraries of integrated content

Addition of indexesAddition of indexes

CommentariesCommentaries

Expert analysisExpert analysis

Authored periodicalsAuthored periodicals

Public Domain Public Domain InformationInformation

Content for Content for basic researchbasic research

LowLow

ValueValue

AddedAdded

HighHigh

Primary SourcePrimary Source

MaterialMaterial

SecondarySecondary

MaterialMaterial

TertiaryTertiary

MaterialMaterial

9

1.1. Increase sales growthIncrease sales growth::

• Historically insufficient focus on innovationHistorically insufficient focus on innovation

• Sales do not mirror marketing spendSales do not mirror marketing spendinging

• Status digitiStatus digitizzation different across countriesation different across countries

• Bundled pricing models an issue in some countriesBundled pricing models an issue in some countries

CHALLENGESCHALLENGES

10

2.2. Bring costs in line with salesBring costs in line with sales

3.3. ImproveImprove strength and depth of management strength and depth of management and and ccontrolontrol

4.4. Invest in full integration of common front and Invest in full integration of common front and back office systems across Europe back office systems across Europe

CHALLENGESCHALLENGES

LTB Europe challenges require a strong LTB Europe challenges require a strong common approach to strategy and common approach to strategy and

structure at cluster level.structure at cluster level.

11

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSA Twofold ApproachA Twofold Approach

• Streamline operations and drive downStreamline operations and drive down c costsosts,, e.g. e.g.::- RRationaliationalizze locationse locations- LLimitimit personnel costspersonnel costs- Improve Improve cost of sale efficienciescost of sale efficiencies (p(printing on demandrinting on demand))

• Common skills, knowledge and measurement, e.g.:Common skills, knowledge and measurement, e.g.:- Intensify unified European management development Intensify unified European management development

programprogram- Set up benchmarksSet up benchmarks

• Structure and strategy that focus on where the money is - Structure and strategy that focus on where the money is - the customerthe customer

1. Operational Excellence1. Operational Excellence

12

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSA Twofold ApproachA Twofold Approach

• Focus on six core customer segments – deepen share of walletFocus on six core customer segments – deepen share of wallet

• Harvest/divest non-core businessHarvest/divest non-core business

• Implement matrix cluster structureImplement matrix cluster structure

• Increase organic growth Increase organic growth

2. Significant, Sustainable and Profitable Growth2. Significant, Sustainable and Profitable Growth

13

1.1. Fragmentation over 1Fragmentation over 166 customer customer segments; segments; 66 largest customer groups largest customer groups generate generate around around 7755% of sales% of sales

2.2. Several customer groups only served in Several customer groups only served in one or two countries one or two countries

3.3. Customer research, marketing and Customer research, marketing and digitization fragmented over 1digitization fragmented over 166 segments segments

4.4. Some segments are small, have a higherSome segments are small, have a higheradvertiadvertisising ng exposureexposure

No focus of strategyNo focus of strategyand growth prioritiesand growth priorities

No synergies;No synergies;no product exchangeno product exchange

Inefficient use ofInefficient use ofmoney and managementmoney and management

Recession Recession -- Sensitive Sensitive

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSPortfolio Review: Current SituationPortfolio Review: Current Situation

14

Portfolio is spread over many customer segmentsPortfolio is spread over many customer segmentsFullFull year 2000 sales: EUR 1.3 year 2000 sales: EUR 1.3 bbillionillion

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSPortfolio Review: Focus on Core SegmentsPortfolio Review: Focus on Core Segments

Breakdown of Sales by Customer SegmentsBreakdown of Sales by Customer Segments

23%

16%

13%9%

8%

6%

25%

Other Other Segments Segments (~10)(~10)

Health, Safety &Health, Safety &Environment (HSE)Environment (HSE)

TransportTransport

PublicPublicHRHR

LegalLegal

Fiscal / FinancialFiscal / Financial

15

Size and Size and growthgrowth

ProfitabilityProfitability

Wolters Wolters KluwerKluwer LTBE LTBE

PositionPosition

• Current market Current market sizesize

• NNumberumber of of professionalsprofessionals

• Average spend Average spend per professional per professional on publishing on publishing products products

• Expected market Expected market growth growth

• Growth of number Growth of number of professionalsof professionals

• Potential for Potential for additional services additional services (e.g.(e.g. software,software, services)services)

• Realistic Realistic EBITA EBITA marginmargin potential potential within 3 yearswithin 3 years

• Market and Market and business risks business risks (stability and (stability and predictability of predictability of income streams )income streams )

• Relative Relative mmarket arket ssharehare

• Ability to become Ability to become top-2 player within 3 top-2 player within 3 yearsyears

• Competitive Competitive strength (branding, strength (branding, content ownership)content ownership)

Importance Importance to WKto WK LTBE LTBE

• Percentage of Percentage of total country total country sales which are sales which are generated by this generated by this segmentsegment

• International International synergetic synergetic possibilitiespossibilities

NNeed to eed to HHaveave

• Regulatory/ Regulatory/ compliance compliance elementelement

• Information Information refreshment raterefreshment rate

• WK WK iinformation/ nformation/ services core to services core to customer’s customer’s businessbusiness

• Quality/reliability of Quality/reliability of information is information is essential (‘need to essential (‘need to have’)have’)

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSPortfolio Review: Selection CriteriaPortfolio Review: Selection Criteria Core Segments Core Segments

16

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSPortfolio Review: Description Core SegmentsPortfolio Review: Description Core Segments

Fiscal / FinancialFiscal / FinancialTax consultants, accountants, Tax consultants, accountants, ffinancial executives, inancial executives,

financial planners in banks and insurance, (financial planners in banks and insurance, (ppublic) tax ublic) tax auditorsauditors

LegalLegal Lawyers, notaries, magistrates, public prosecutors, Lawyers, notaries, magistrates, public prosecutors, institutional and company lawyers institutional and company lawyers

HRHR HR director/managerHR director/managerss, payroll/benefits manager, payroll/benefits managerss, training/ , training/ development managerdevelopment managerss, HR consultants, HR consultants

Public / SocialPublic / SocialLine managers in state and regional government and in Line managers in state and regional government and in municipalities, police, pedagogic professionals, social municipalities, police, pedagogic professionals, social

workers, labour union professionals workers, labour union professionals

HSEHSEManagers focused on health & safety, facilities, Managers focused on health & safety, facilities,

maintenance and environmentalmaintenance and environmental issues issues, waste contractor, waste contractorss, , HSE consultantsHSE consultants

TransportTransportGeneral transport managers, transport logistics managers, General transport managers, transport logistics managers,

engineers, product managers, sales & distribution engineers, product managers, sales & distribution personnel personnel

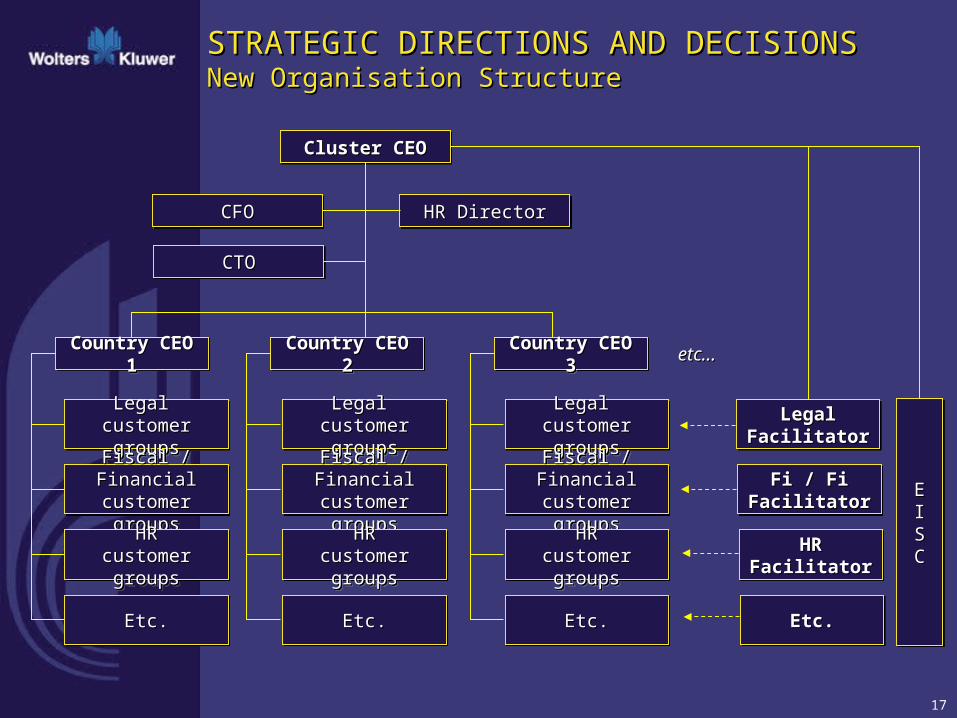

17

Legal Legal FacilitatorFacilitator

Legal Legal FacilitatorFacilitator

etc…etc…

EEIISSCC

EEIISSCC

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSNew Organisation StructureNew Organisation Structure

Cluster CEOCluster CEOCluster CEOCluster CEO

CFOCFOCFOCFO

CTOCTOCTOCTO

HR DirectorHR DirectorHR DirectorHR Director

Country CEO 1Country CEO 1Country CEO 1Country CEO 1

Legal Legal customer groupscustomer groups

Legal Legal customer groupscustomer groups

Fiscal / FinancialFiscal / Financialcustomer groupscustomer groupsFiscal / FinancialFiscal / Financialcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

Etc.Etc.Etc.Etc.

Fi / FiFi / Fi FacilitatorFacilitator

Fi / FiFi / Fi FacilitatorFacilitator

HRHRFacilitatorFacilitator

HRHRFacilitatorFacilitator

Etc.Etc.Etc.Etc.

Country CEO 2Country CEO 2Country CEO 2Country CEO 2 Country CEO 3Country CEO 3Country CEO 3Country CEO 3

Legal Legal customer groupscustomer groups

Legal Legal customer groupscustomer groups

Fiscal / FinancialFiscal / Financialcustomer groupscustomer groupsFiscal / FinancialFiscal / Financialcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

Etc.Etc.Etc.Etc.

Legal Legal customer groupscustomer groups

Legal Legal customer groupscustomer groups

Fiscal / FinancialFiscal / Financialcustomer groupscustomer groupsFiscal / FinancialFiscal / Financialcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

HRHRcustomer groupscustomer groups

Etc.Etc.Etc.Etc.

18

STRATEGIC DIRECTIONS AND DECISIONSSTRATEGIC DIRECTIONS AND DECISIONSMissionMission

"To be on the mind of each of our target "To be on the mind of each of our target

customers, on their computer screen, laptop, customers, on their computer screen, laptop,

mobile; in their briefcase, drawer, desktop; with mobile; in their briefcase, drawer, desktop; with

smart content, superior services and support, smart content, superior services and support,

making their job easier, more effective and making their job easier, more effective and

profitable"profitable"

19

LTB EUROPE’S RECIPE FOR GROWTHLTB EUROPE’S RECIPE FOR GROWTH

Growth tactic LTB Europe 1. Natural growth

Each segment is growing; in some cases e.g. HSE at above average rate Market size valued at € 9-12 billion, and growing

2.

Gain market share through higher productivity, rapid cycle times

Higher innovation spend Ongoing cost reductions, rationalizations aiming at keeping cost base competitive Increased use of common technology for cost and rapid product cycle time: e.g. Sigmalink and European Internet Centre Increase marketing & sales power

3.

Hold proprietary product & services

Focus on regulatory/compliance businesses with own product & services and high need-to-have factor

20

LTB EUROPE’S RECIPE FOR GROWTHLTB EUROPE’S RECIPE FOR GROWTH

Growth tactic LTB Europe 4. Further develop “distribution”

channels Migration to electronic distribution

increasing

5.

Open new markets

Geographically looking to ‘hole fill’ in key segments, by acquisition, alliance or organically

6.

Expand the pond/move to adjacent segments

Looking at core customer needs and providing new services

7.

Build new competencies and skills to enter new markets

Building skills in workflow software to meet large growing need of professionals to use time effectively.

21

FUTURE GOALS FUTURE GOALS

• Increased wallet share of core Increased wallet share of core customer customer segments to achieve segments to achieve an average an average sales sales growth of 7% per annumgrowth of 7% per annum

• Rank 1Rank 1stst / 2 / 2ndnd in chosen customer segments in chosen customer segments

• Create a structure, reporting and measurement system and Create a structure, reporting and measurement system and rerennuumemeration packageration package centered centered on on these these customer segmentscustomer segments

• Stabilize and increase profitabilityStabilize and increase profitability,, leading to EBITA margin of leading to EBITA margin of more than 20%more than 20%

• Create operational comparability and excellence Create operational comparability and excellence

• Further prepare digitFurther prepare digitizedized content in core segments through content in core segments through common technology as a platform for “smartcommon technology as a platform for “smart” ” contentcontent..

22

THE STORY SO FAR AND NEXT 12 MONTHSTHE STORY SO FAR AND NEXT 12 MONTHS

SO FAR:SO FAR:

• Have set up the basic structureHave set up the basic structure

• Have acquired a number of workflow software companies in Have acquired a number of workflow software companies in core areascore areas

• Have identified key markets and begun process of divestingHave identified key markets and begun process of divesting

• Have made progress with building of common European Have made progress with building of common European Internet Platform Internet Platform

• CostCost--saving plans already underwaysaving plans already underway..

23

THE STORY SO FAR AND NEXT 12 MONTHS THE STORY SO FAR AND NEXT 12 MONTHS

NEXT 12 MONTHS:NEXT 12 MONTHS:

• Redefine managerial competency needs and establish Redefine managerial competency needs and establish management development program management development program

• Further turn structures to customer centric approach Further turn structures to customer centric approach

• Leverage skills, knowledge and products across Europe in key Leverage skills, knowledge and products across Europe in key customer customer segmentssegments

• Increase innovation initiatives Increase innovation initiatives

• Set up focused acquisition program Set up focused acquisition program

• Set up Set up bbenchenchmmarksarks;; operational management accounts operational management accounts

• Further improve cost controls Further improve cost controls

• Upgrade Upgrade CRM CRM systemssystems

• Use common technology approach to continued digitUse common technology approach to continued digitizatization of ion of content in core content in core customer customer segmentssegments..

24

SUMMARYSUMMARY

• Culture change; innovation and growthCulture change; innovation and growth

• Cost controlsCost controls

• Driving up through value chainDriving up through value chain

• Customer centricCustomer centric

Legal, Tax & Business EuropeLegal, Tax & Business Europe

David J. SmithDavid J. Smith, CEO, CEO

Analysts & Investors, August 2001Analysts & Investors, August 2001

![Presentation to Investors and Analysts [Company Update]](https://static.documents.pub/doc/80x56/577c7d531a28abe0549e52b6/presentation-to-investors-and-analysts-company-update.jpg)

![Investors' and Analysts' Meet [Company Update]](https://static.documents.pub/doc/80x56/577c7ac51a28abe054963435/investors-and-analysts-meet-company-update.jpg)

![Investors & Analysts Presentation [Company Update]](https://static.documents.pub/doc/80x56/577c7c231a28abe0549972fe/investors-analysts-presentation-company-update.jpg)