Lesson 15: Building ARMA models. Examples Umberto Triacca Dipartimento di Ingegneria e Scienze dell’Informazione e Matematica Universit` a dell’Aquila, [email protected]Umberto Triacca Lesson 15: Building ARMA models. Examples

Transcript

Lesson 15: Building ARMA models.Examples

Umberto Triacca

Dipartimento di Ingegneria e Scienze dell’Informazione e MatematicaUniversita dell’Aquila,

Umberto Triacca Lesson 15: Building ARMA models. Examples

Examples

In this lesson, in order to illustrate the time series modellingmethodology we have presented so far, we analyze some timeseries.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

By using a computer program we have generated a time seriesx .The graph of the series is presented in the following figure

Figure : A simulated time series

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

The objective is to build an ARMA model this time series.The first step in developing a model is to determine if theseries is stationary.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

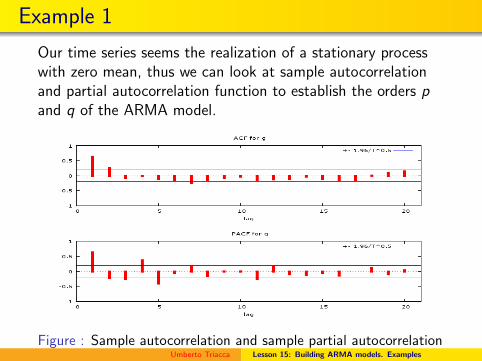

Our time series seems the realization of a stationary processwith zero mean, thus we can look at sample autocorrelationand partial autocorrelation function to establish the orders pand q of the ARMA model.

Figure : Sample autocorrelation and sample partial autocorrelationfunctions of time series xUmberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

Since the SACF cuts off after lag 2 and the SPCAF follows adamped cycle,

an MA(2) model

xt = ut + θ1ut−1 + θ2ut−2, ut ∼ WN(0, σ2)

seems appropriate for the sample data.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

Table reports the result of the ML estimation.

300 observations, Dependent Variable x

Variabile Coefficient St. error t statistic p-value

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

Now, we consider the graph of the residuals

Figure : Residuals from MA(2) model

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

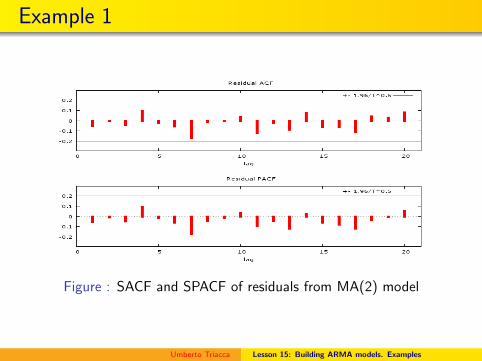

Figure : SACF and SPACF of residuals from MA(2) model

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

By analysing the SACF and SPACF of residuals presented infigure, we note that any term isn’t significant andQ25 = 16.4450 do not indicate any autocorrelation in theresiduals. They can be assimilate to a white noise process.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 1

We conclude that the MA(2) model defined by

xt = ut + 1.686ut−1 + 0.884ut−2, ut ∼ WN(0, 0.94)

appear to fit the data very well.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

Consider the montly series of the foreign exchange rate Liraper US Dollar from Jannuary 1973 until October 1989 (202observations).

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

It can be observed that the series displays a nonstationarypattern with an upward trending behavior.

Figure : Foreign exchange rate Lira per U.S. $ from Jannuary 19t3until October 1989

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

The first difference of the series seems to have a constantmean, although inspection of the graph (see Figure ) suggeststhye variance is an increasing function of time.

Figure : First difference of the foreign exchange rate Lira per USdollar

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

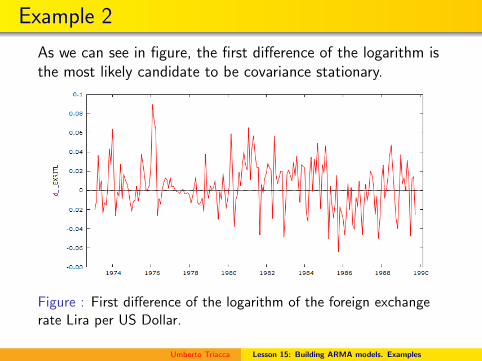

As we can see in figure, the first difference of the logarithm isthe most likely candidate to be covariance stationary.

Figure : First difference of the logarithm of the foreign exchangerate Lira per US Dollar.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

Now, we examine the autocorrelation and partialautocorrelation functions of the logarithmic change in theforeign exchange rate Lira per US Dollar.

Figure : SACF and SPACF for the logarithmic change in theforeign exchange rate Lira per US Dollar.

Examination of the two graphs suggests that an AR(1) modelcan be appropriate. In particular, the SPACF is such thatφ11 = 0.3607 and cuts off to -0.0022 abrutly (i.e.φ22 = −0.0022. Thus the SPACF is suggestive of an AR(1)model.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

An AR(1) model is fitted by using the exact maximumlikelihood estimation. The parameter estimates aresummarized in the following table

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

Sample 1973:02–1989:10. Dependent Variable: First differenceof log of the foreign exchange rate Lira per US Dollar

Coefficient Std. error t statistic p-value Variance innov.

0,381412 0,0652368 5,8466 0,0000 0,000543700

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

The AR(1) model fit indicates a highly significant parameterφ1 with estimate φ1 = 0, 381.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

The Q statistic (Q20 = 16, 5014) and the graphs of the SACFand SPACF of residuals (see Figure )indicate that theautocorrelations of the residuals are not statistically significant.

Figure : SACF and SACFP of residuals from the model AR(1)

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 2

Thus we conclude that the AR(1) model

xt = 0.381xt−1 + ut

where ut ∼ WN(0, 0.00054) and xt is the first difference of logof the foreign exchange rate Lira per US Dollar, fits the datawell.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

We consider the log of GNP deflator series in USA observedon the period 1955:1- 2000:4. The objective is to build anARMA model for this time series.

Umberto Triacca Lesson 15: Building ARMA models. Examples

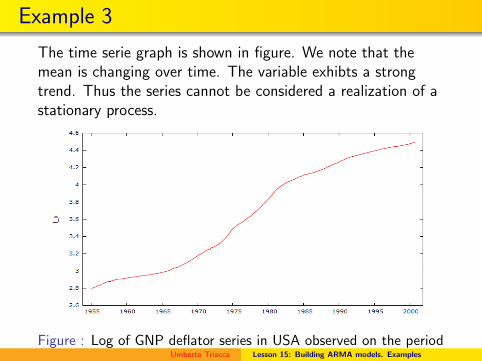

Example 3

The time serie graph is shown in figure. We note that themean is changing over time. The variable exhibts a strongtrend. Thus the series cannot be considered a realization of astationary process.

Figure : Log of GNP deflator series in USA observed on the period1955:1 - 2000:4 Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

In order to make stationary the series, we consider the firstdiffereces.

Figure : Graphical plot of the first difference of log of GNPdeflator series

Umberto Triacca Lesson 15: Building ARMA models. Examples

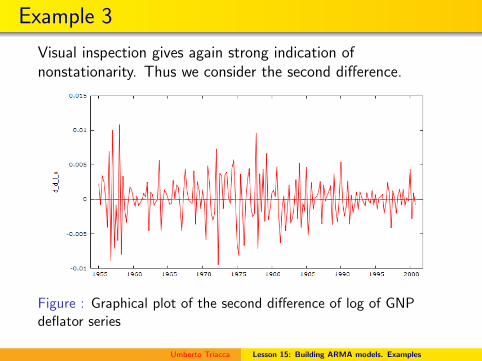

Example 3

Visual inspection gives again strong indication ofnonstationarity. Thus we consider the second difference.

Figure : Graphical plot of the second difference of log of GNPdeflator series

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

The second difference seems the realization of a stationaryprocess with zero mean, thus we can look at sampleautocorrelation and partial autocorrelation function of thesecond difference, to establish the orders p and q of the ARMAmodel. Figure shows the graphs of SACFs and SPACFs.

Figure : Graphical plot of the of SACF and SPACFof the seconddifference of log of GNP deflator series

In this case, it is very difficult to identify the orders p and q ofthe ARMA model by using the correlogram and the partialcorrelogram.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Additional information can be obtained by inspecting theoutcomes of the AIC and BIC criteria.

From AIC values it is concluded that the ARMA(1,2) model ismost suitable for our time series. From BIC values, however,the MA(1) is judged to be better suited.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

The fact that AIC and BIC provided different indications aboutthe best fitting models is not surprising because BIC penalizeslarger models more than AIC.

Thus BIC tends to produce more parsimonious best-fittingmodels than AIC.

Umberto Triacca Lesson 15: Building ARMA models. Examples

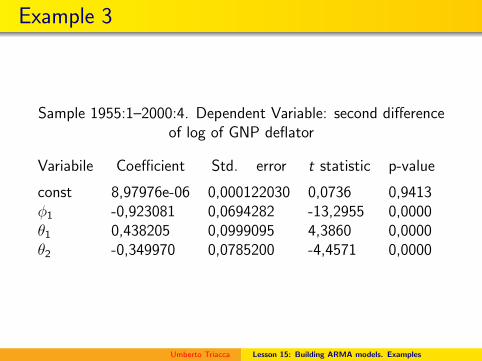

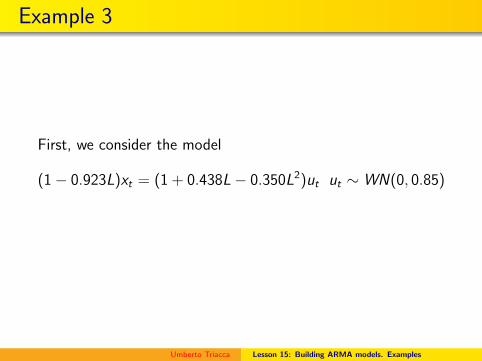

Example 3

Since computing time is inexpensive we can estimate bothmodels. Table 1 shows the results of fitting an ARMA(1,2) forthe second difference of log of GNP deflator.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Sample 1955:1–2000:4. Dependent Variable: second differenceof log of GNP deflator

Variabile Coefficient Std. error t statistic p-value

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Now, we can look at sample autocorrelation and partialautocorrelation functions of residuals of the model ARMA(1,2)to establish if this ARMA model is a good model for the data.

Figure : SACF and SACFP of residuals from the model ARMA(1,2)

These graphs are very similar to the correlograms of a whitenoise process. There is only a SACF coefficient and only aSACFP which are significant. We consider it as a result ofpure chance.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

The QK -statistic computed with K = 20 lags is equal toQ20 = 16.2932, whereas the critical value isχ2

1−0.05,17 = 27.5871.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Umberto Triacca Lesson 15: Building ARMA models. Examples

The correlograms and the Box-Pierce statistics(Q20 = 21.6819) indicate that the residuals behave as whitenoise processes.

Figure : SACF and SACFP of residuals from the model MA(1)

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Thus we conclude that also the model

xt = (1 − 0.466L)ut ut ∼ WN(0, 0.89),

fits the data well.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Let us look at the forecasting performace of the two models.In particular, we forecast the future values of our time series,log(yt), from 2001:1 to 2001:4.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Given these results we may conclude that the performance oftwo models is very similar. Which model should be prefered?

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

It is usual to choose a parsimonious model, that is a modelthat describes all of the features of the data of interest usingas few parameters as possible.

Umberto Triacca Lesson 15: Building ARMA models. Examples

Example 3

Thus we choose the MA(1) model

xt = (1 − 0.466L)ut ut ∼ WN(0, 0.89),

Umberto Triacca Lesson 15: Building ARMA models. Examples