18

Level 4 Professional Accounting Technician Apprenticeship End-point assessment technical specification handbook Appendices

End Point Assessment Technical Specification Handbook 1

Level 4 Professional Accounting Technician Apprenticeship End-point assessment technical specification handbook

Appendices

1

Contents4 A. Grade descriptors: Role simulation exam (EPA1)

6 B. Assessment criteria: Reflective statement and portfolio (EPA2)

8 C. EPA2 Submission checklist

9 D. Portfolio template guidance and mapping document

13 E. Guidance: Reflective statement template

15 F. Task writing template: Reflective statement

16 G. Exemplar 1: Completed task writing template

19 H. Smart objective setting template

End Point Assessment Technical Specification Handbook 1End-point assessment technical specification handbook 2

4

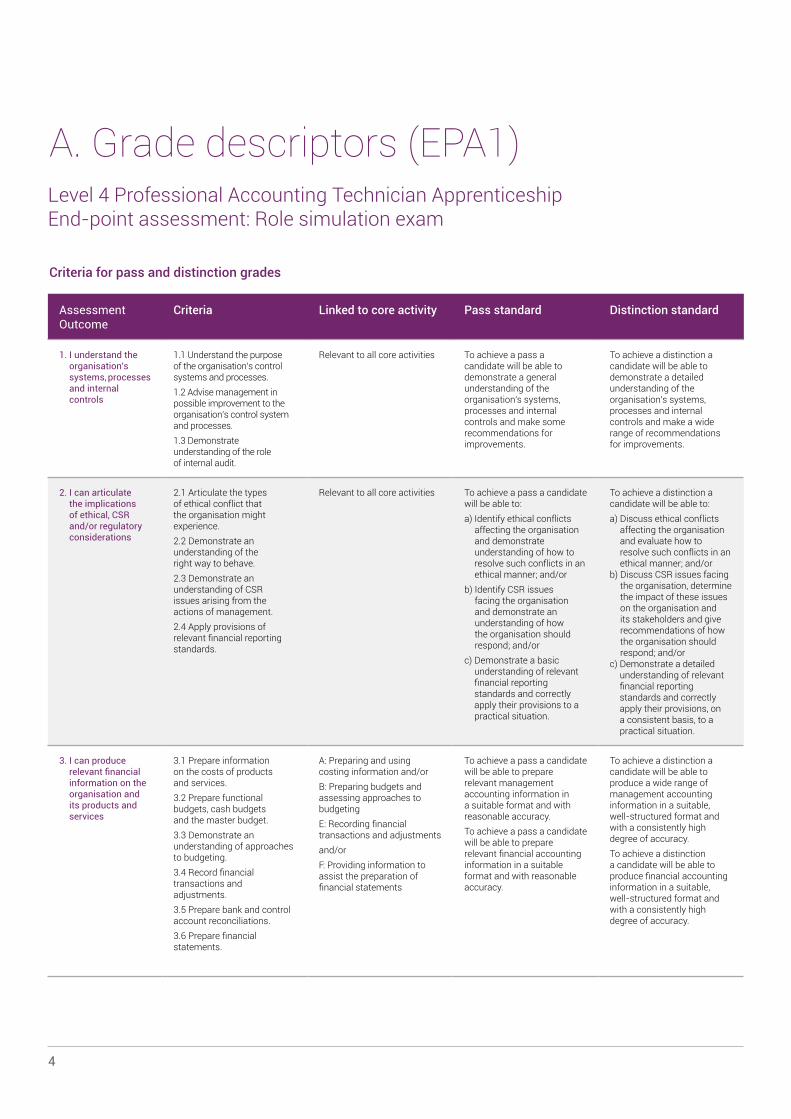

A. Grade descriptors (EPA1) Level 4 Professional Accounting Technician Apprenticeship End-point assessment: Role simulation exam

Assessment Outcome

Criteria Linked to core activity Pass standard Distinction standard

1. I understand the organisation's systems, processes and internal controls

1.1 Understand the purpose of the organisation’s control systems and processes.1.2 Advise management in possible improvement to the organisation’s control system and processes.1.3 Demonstrate understanding of the role of internal audit.

Relevant to all core activities To achieve a pass a candidate will be able to demonstrate a general understanding of the organisation's systems, processes and internal controls and make some recommendations for improvements.

To achieve a distinction a candidate will be able to demonstrate a detailed understanding of the organisation's systems, processes and internal controls and make a wide range of recommendations for improvements.

2. I can articulate the implications of ethical, CSR and/or regulatory considerations

2.1 Articulate the types of ethical conflict that the organisation might experience.2.2 Demonstrate an understanding of the right way to behave.2.3 Demonstrate an understanding of CSR issues arising from the actions of management.2.4 Apply provisions of relevant financial reporting standards.

Relevant to all core activities To achieve a pass a candidate will be able to:a) Identify ethical conflicts

affecting the organisation and demonstrate understanding of how to resolve such conflicts in an ethical manner; and/or

b) Identify CSR issues facing the organisation and demonstrate an understanding of how the organisation should respond; and/or

c) Demonstrate a basic understanding of relevant financial reporting standards and correctly apply their provisions to a practical situation.

To achieve a distinction a candidate will be able to:a) Discuss ethical conflicts

affecting the organisation and evaluate how to resolve such conflicts in an ethical manner; and/or

b) Discuss CSR issues facing the organisation, determine the impact of these issues on the organisation and its stakeholders and give recommendations of how the organisation should respond; and/or

c) Demonstrate a detailed understanding of relevant financial reporting standards and correctly apply their provisions, on a consistent basis, to a practical situation.

3. I can produce relevant financial information on the organisation and its products and services

3.1 Prepare information on the costs of products and services.3.2 Prepare functional budgets, cash budgets and the master budget.3.3 Demonstrate an understanding of approaches to budgeting.3.4 Record financial transactions and adjustments.3.5 Prepare bank and control account reconciliations.3.6 Prepare financial statements.

A: Preparing and using costing information and/orB: Preparing budgets and assessing approaches to budgetingE: Recording financial transactions and adjustmentsand/orF: Providing information to assist the preparation of financial statements

To achieve a pass a candidate will be able to prepare relevant management accounting information in a suitable format and with reasonable accuracy.To achieve a pass a candidate will be able to prepare relevant financial accounting information in a suitable format and with reasonable accuracy.

To achieve a distinction a candidate will be able to produce a wide range of management accounting information in a suitable, well-structured format and with a consistently high degree of accuracy.To achieve a distinction a candidate will be able to produce financial accounting information in a suitable, well-structured format and with a consistently high degree of accuracy.

Criteria for pass and distinction grades

Assessment outcome

Criteria Linked to core activity Pass standard Distinction standard

4. I can support managers to make informed decisions in the context of the business environment

4.1 Apply short-term decision-making techniques to financial data and advise managers on an appropriate course of action.4.2 Demonstrate an understanding of the limitations of decision-making techniques.4.3 Identify other factors (including ethical considerations) and further information that should be considered before making a final decision.

C: Providing and interpreting information to support short term decision making

To achieve a pass a candidate will be able to apply decision making techniques to a practical situation with minimal errors. A candidate will also demonstrate an understanding of the limitations of the technique used and/or identify other information required or factors to be considered to support the decision. A passing candidate will demonstrate some business awareness by exhibiting some understanding of the impact of the decision on the organisation and its stakeholders.

To achieve a distinction a candidate will be able to apply decision making techniques to a practical situation with no errors. A candidate will also demonstrate a detailed understanding of the limitations of the technique used and/or discuss other information required or factors to be considered to support the decision. A distinction candidate will demonstrate a high degree of business awareness by exhibiting a detailed understanding of the impact of the decision on the organisation and its stakeholders.

5 . I can analyse financial information in the context of the business environment to assist managers to evaluate performance

5.1 Analyse the organisation’s financial performance and position using financial ratios.5.2 Analyse the organisation’s performance against budget using variance analysis and KPI’s.

D: Evaluating performance using management information and financial statements.

To achieve a pass a candidate will be able to calculate appropriate financial ratios, variances or KPIs, and demonstrate some analytical skills when interpreting what these mean about the performance and financial position of the organisation in the context of the business environment.

To achieve a distinction a candidate will be able to calculate appropriate financial ratios, variance or KPIs, and demonstrate well developed analytical skills when interpreting what these mean about the financial performance and financial position of the organisation in the context of the business environment.

End-point assessment technical specification handbook 5

(continued)

6

Assessment outcome Gateway profile Ready for EPA

Assessment criteria Developed on the job experience – opportunity to rotate in different areas (Six months prior to EPA)

In current employment for a year+ in a relevant roleOn programme for at least a year.

Claim of competency (skills & behaviours) Sub criteria (skills and behaviours)

1. Analysis

I can produce and interpret information in order to add value to my organisation

A1 Produce accurate and reliable information that supports management decision making A2 Produce accurate and reliable information that supports evaluation of the organisation’s performance by management

A3 Interpret information to support management decision making A4 Interpret information to support evaluation of the organisation’s performance by management

2. Communication

I can select an appropriate medium and use it effectively to communicate with different stakeholders in different situations

C1 Communicate, using appropriate media and in an appropriate manner, either verbally or in writing, to peers within your immediate teamC2 Communicate using appropriate media and in an appropriate manner, either verbally or in writing, to managers within your immediate team

C3 Communicate using appropriate media and in an appropriate manner, either verbally or in writing, to internal stakeholders C4 Communicate, using appropriate media and in an appropriate manner, either verbally or in writing to external stakeholders

3. Leadership (Self-development)

I can reflect on my own performance and take action to develop my professional skills

SD1 Evaluate your own performance and identify appropriate development activities to improve your performanceSD2 Demonstrate commitment to your job by achieving work objectives

SD3 Engage with the wider accounting profession by keeping up to date with current developments

4. Planning & prioritisation

I can plan and prioritise my own workload and coordinate input from others to meet work objectives

P1 Plan and prioritise your work to meet work objectivesP2 Coordinate the input of others in order to meet work objectives

P3 Manage changing priorities in an effective manner to meet work objectives

5. Quality & accurate information

I can apply my accounting knowledge to consistently produce clear and accurate information

Q1 Produce clear and accurate information on routine tasks applicable to your role, in a consistent and timely manner

Q2 Produce clear and accurate information on non-routine tasks, in a timely manner, under guidance from your supervisor

6. Team working & collaboration

I can work effectively within a team and behave in a professional manner when collaborating with stakeholders

T1 Contribute effectively to a team to achieve the objective of the teamT2 Behave in a professional manner when collaborating with internal and external stakeholders

N/A

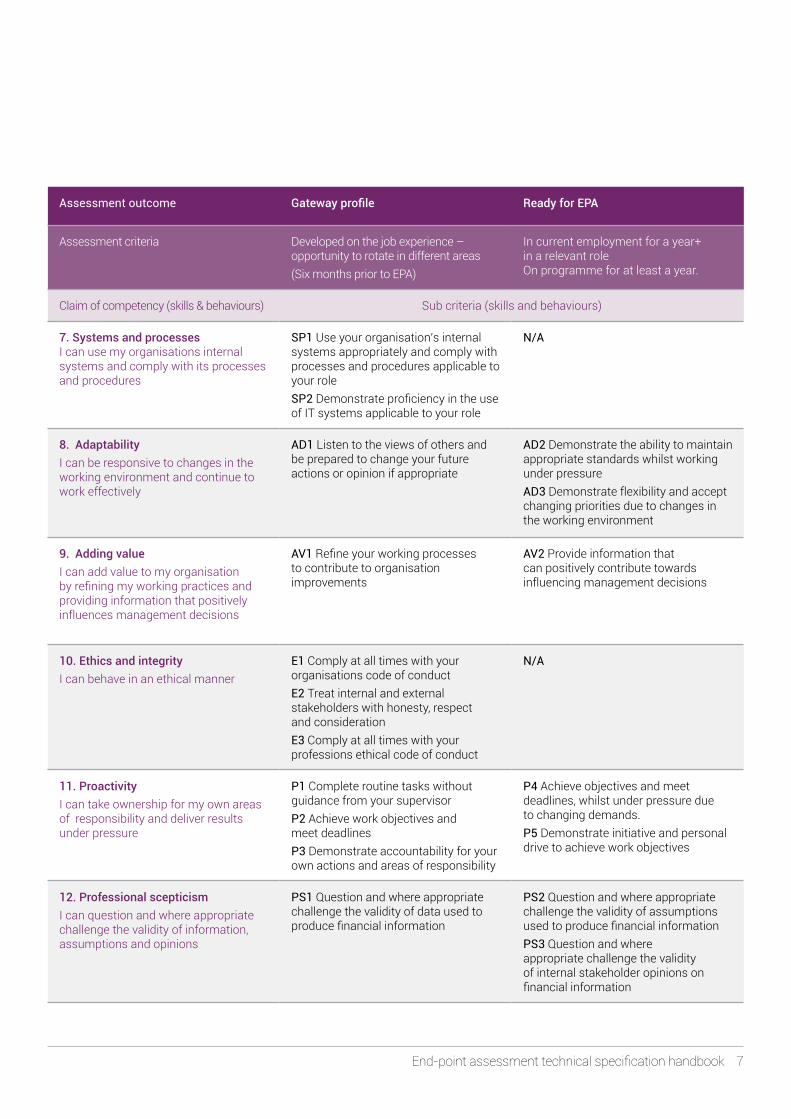

B. Assessment criteria (EPA2) Level 4 Professional Accounting Technician Apprenticeship End-point assessment: Reflective statement and portfolio

Assessment outcome Gateway profile Ready for EPA

Assessment criteria Developed on the job experience – opportunity to rotate in different areas (Six months prior to EPA)

In current employment for a year+ in a relevant roleOn programme for at least a year.

Claim of competency (skills & behaviours) Sub criteria (skills and behaviours)

7. Systems and processesI can use my organisations internal systems and comply with its processes and procedures

SP1 Use your organisation’s internal systems appropriately and comply with processes and procedures applicable to your roleSP2 Demonstrate proficiency in the use of IT systems applicable to your role

N/A

8. AdaptabilityI can be responsive to changes in the working environment and continue to work effectively

AD1 Listen to the views of others and be prepared to change your future actions or opinion if appropriate

AD2 Demonstrate the ability to maintain appropriate standards whilst working under pressureAD3 Demonstrate flexibility and accept changing priorities due to changes in the working environment

9. Adding valueI can add value to my organisation by refining my working practices and providing information that positively influences management decisions

AV1 Refine your working processes to contribute to organisation improvements

AV2 Provide information that can positively contribute towards influencing management decisions

10. Ethics and integrity I can behave in an ethical manner

E1 Comply at all times with your organisations code of conduct E2 Treat internal and external stakeholders with honesty, respect and considerationE3 Comply at all times with your professions ethical code of conduct

N/A

11. ProactivityI can take ownership for my own areas of responsibility and deliver results under pressure

P1 Complete routine tasks without guidance from your supervisorP2 Achieve work objectives and meet deadlinesP3 Demonstrate accountability for your own actions and areas of responsibility

P4 Achieve objectives and meet deadlines, whilst under pressure due to changing demands. P5 Demonstrate initiative and personal drive to achieve work objectives

12. Professional scepticismI can question and where appropriate challenge the validity of information, assumptions and opinions

PS1 Question and where appropriate challenge the validity of data used to produce financial information

PS2 Question and where appropriate challenge the validity of assumptions used to produce financial informationPS3 Question and where appropriate challenge the validity of internal stakeholder opinions on financial information

End-point assessment technical specification handbook 7

8

C. EPA2 Submission checklist Reflective statement and portfolio

Submission checklist

The apprentice has met the following criteria:

Completed mapping against the assessment criteria and sub criteria (Appendix B).

Identified tasks that can be accurately categorised as one of the core activities and is relevant to the Level 4 Professional accounting technician apprenticeship standard.

Provided current and valid evidence (within the last six months) for claimed skill(s) and behaviour(s)

Provided an evidence-based justification (explanation) for competence against EACH of the 12 competencies as defined by the sub criteria in the assessment criteria.*

In each task identified at least one lesson learned that is supported by the justification and evidence in the portfolio

In each statement described at least one change that would be made for a future activity

* Where an asterisk is provided, only one reasoned, evidence-based justification for competence is needed for EACH skill and behaviour.

Claim of competency Task template1, 2, 3 ,4 or 5

Assessment criteria – sub criteria (Skills & behaviours evidenced)

Portfolio evidence

Analysis T1, T2 Y Y Y Y N/A Induction day presentation

Example 1 2 3 4 5

1. Analysis N/A

2. Communication N/A

3. Leadership (Self-development)

N/A N/A

4. Planning & prioritisation N/A N/A

5. Quality & accurate information

N/A N/A N/A

6. Team working & collaboration

N/A N/A N/A

7. Systems & processes N/A N/A N/A

8. Adaptability N/A N/A

9. Adding value N/A N/A N/A

10. Ethics & integrity N/A N/A

11. Proactivity

12. Professional scepticism N/A N/A

End Point Assessment Technical Specification Handbook 9

D. Portfolio template guidance Throughout your apprenticeship, you will be required to demonstrate that you have met the skills and behaviours detailed in the Level 4 Professional accounting technician apprenticeship standard.

You must provide evidence from the last six months to demonstrate that these skills and behaviours have been met. This can be taken from your training log or can include actual work product, emails, written statements, excerpts from your performance appraisals and professional discussions.

Your portfolio will be marked by independent assessors so it is important that the evidence you submit is traceable in case your work is selected for review.

Where possible, we would recommend that the evidence you put forward maps across the different skills and behaviours detailed in the assessment criteria and standard.

End-point assessment technical specification handbook 9

10

D. P

ortfo

lio m

appi

ng d

ocum

ent

Num

ber o

f fil

e at

tach

men

ts

Evid

ence

I’ve

use

d to

su

ppor

t my

refle

ctiv

e st

atem

ents

(For

mat

of e

vide

nce)

Anal

ysis

Com

mun

icat

ion

Lead

ersh

ipPl

anni

ng &

pr

iorit

isat

ion

Qua

lity

& ac

cura

te

Info

rmat

ion

Team

w

orki

ng &

co

llabo

ratio

n

Syst

ems

& Pr

oces

ses

Adap

tabi

lity

Addi

ng v

alue

Ethi

cs &

in

tegr

ityPr

oact

ivity

Prof

essi

onal

sc

eptic

ism

1Pr

esen

tatio

n at

in

duct

ion

day

(PD

F fo

rmat

)

✓✓

✓✓

✓

2Au

dit J

ob x

xx

(app

rais

al fo

rm

from

Oct

16)

3 4 5 6 7 8 9 10

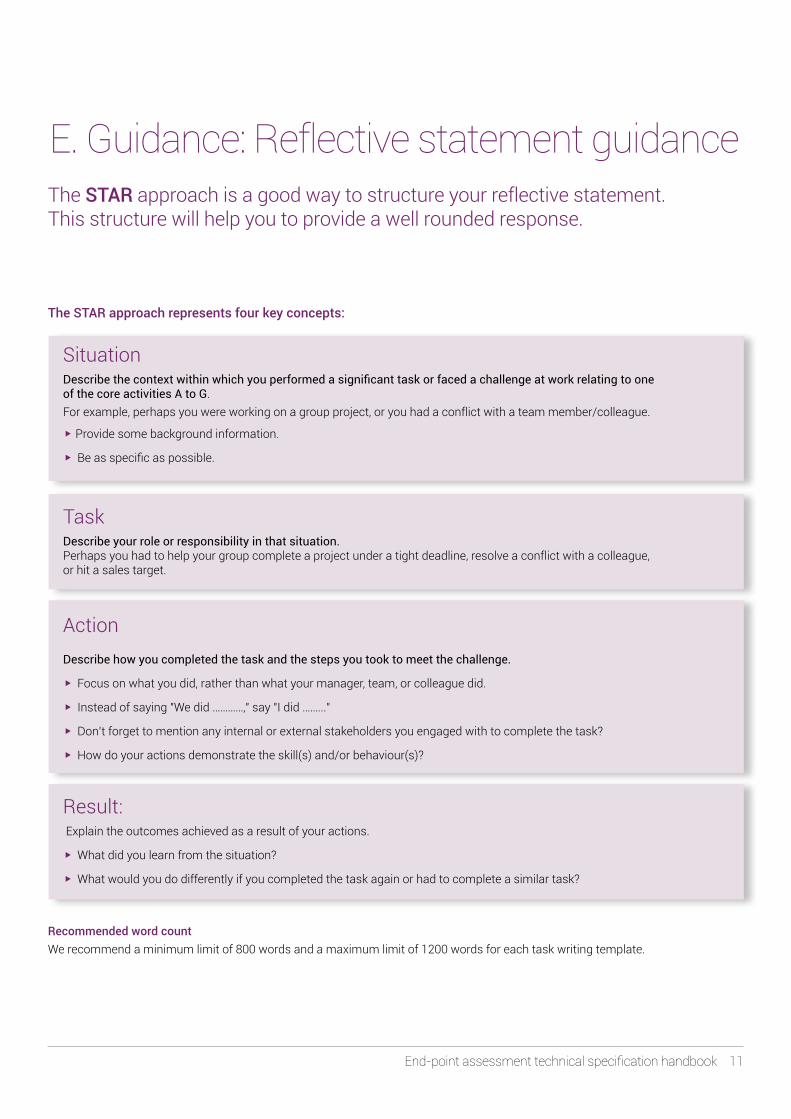

E. Guidance: Reflective statement guidanceThe STAR approach is a good way to structure your reflective statement. This structure will help you to provide a well rounded response.

SituationDescribe the context within which you performed a significant task or faced a challenge at work relating to one of the core activities A to G.For example, perhaps you were working on a group project, or you had a conflict with a team member/colleague.

w Provide some background information.

w Be as specific as possible.

TaskDescribe your role or responsibility in that situation.Perhaps you had to help your group complete a project under a tight deadline, resolve a conflict with a colleague, or hit a sales target.

Action Describe how you completed the task and the steps you took to meet the challenge.

w Focus on what you did, rather than what your manager, team, or colleague did.

w Instead of saying "We did …………," say "I did ……..."

w Don’t forget to mention any internal or external stakeholders you engaged with to complete the task?

w How do your actions demonstrate the skill(s) and/or behaviour(s)?

Result: Explain the outcomes achieved as a result of your actions.

w What did you learn from the situation?

w What would you do differently if you completed the task again or had to complete a similar task?

Recommended word countWe recommend a minimum limit of 800 words and a maximum limit of 1200 words for each task writing template.

End-point assessment technical specification handbook 11

The STAR approach represents four key concepts:

12

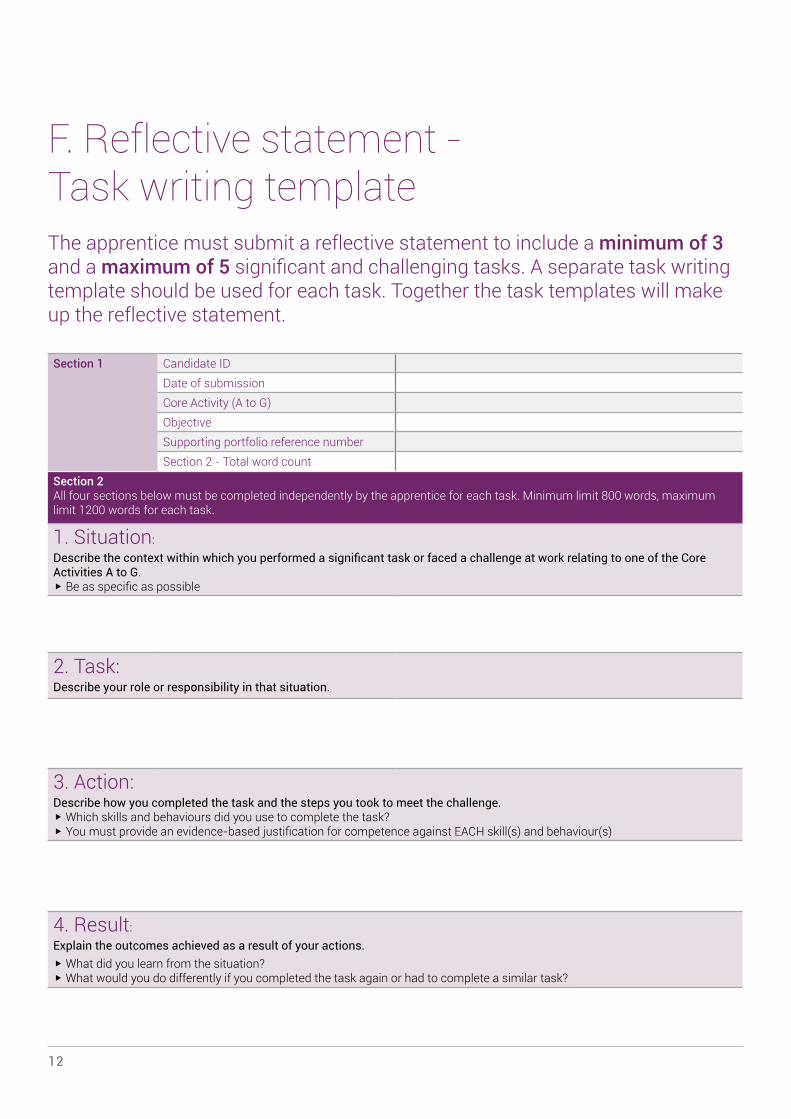

F. Reflective statement - Task writing templateThe apprentice must submit a reflective statement to include a minimum of 3 and a maximum of 5 significant and challenging tasks. A separate task writing template should be used for each task. Together the task templates will make up the reflective statement.

Section 1 Candidate IDDate of submissionCore Activity (A to G)ObjectiveSupporting portfolio reference numberSection 2 - Total word count

Section 2 All four sections below must be completed independently by the apprentice for each task. Minimum limit 800 words, maximum limit 1200 words for each task.

1. Situation: Describe the context within which you performed a significant task or faced a challenge at work relating to one of the Core Activities A to G. w Be as specific as possible

2. Task: Describe your role or responsibility in that situation.

3. Action: Describe how you completed the task and the steps you took to meet the challenge. w Which skills and behaviours did you use to complete the task?w You must provide an evidence-based justification for competence against EACH skill(s) and behaviour(s)

4. Result: Explain the outcomes achieved as a result of your actions. w What did you learn from the situation?w What would you do differently if you completed the task again or had to complete a similar task?

G. Exemplar 1 Completed task writing template Section 1 Candidate ID

Date of submissionCore Activity (A to G) AObjectiveSupporting portfolio evidenceSection 2 - Total word count 1095 words

Section 2 All four sections below must be completed independently by the apprentice for each task. Minimum limit 800 words, maximum limit 1200 words for each task.

1. Situation: Describe the context within which you performed a significant task or faced a challenge at work relating to one of the core Activities A to G.

I was part of the finance team assigned to produce the 2018/2019 budget. The team included three accounting apprentices (including me) two assistant accountants and the planning manager who had ultimate responsibility for the budget process. The process started in April 2018 and was to be completed by mid-June.

The company produces budgets annually using incremental budgeting and a participative budget approach.

2. Task: Describe your role or responsibility in that situation.

I was tasked to work with three of the support service managers to assist them in producing their departmental budgets. I had to issue the budget instructions, co-ordinate the production of the budgets and review the proposed budgets for next year against the current year’s budget and actuals. Following the review, I needed to discuss the budget with the department manager and suggest possible changes. The final part of the process was to produce a report incorporating a recommendation as to whether the budgets should be accepted and to present this at a team meeting.

3. Action: Describe how you completed the task and the steps you took to meet the challenge. w Which skills and behaviours did you use to complete the task?w You must provide an evidence-based justification for competence against EACH skill(s) and behaviour(s)

My first step was to prepare the budget instruction including a timetable for completion (EVIDENCE: budget instructions and timetable– P1, P2, SP1). I then emailed each of the managers with the details and also advised them that I would be available to discuss any issue that arise during the process (EVIDENCE: copy of email – C3). I immediately received an email from the marketing manager who said he would not be able to complete the budget on time as he was out of the office for the month prior to the submission date - on holiday for two weeks and then at an overseas conference for two weeks. I knew that this would cause an issue as it would hold up completion of the master budget. I therefore made an appointment to meet the marketing manager and offered to provide assistance to his deputy to enable completion of the budget. I suggested that he could give final approval to the figures by email. (EVIDENCE: record of conversation signed by marketing manager – C3, AD2, AD3, SD2, P3, T2, PR4, PR5).

During the time period, I answered a number of email queries raised by the individual managers about different aspects of the process. I thought some of the questions were fairly straight forward and was surprised the managers had raised them but I replied in a courteous manner and gave them the information they required. (EVIDENCE: copy of emails – C3, E2).

End-point assessment technical specification handbook 13

14

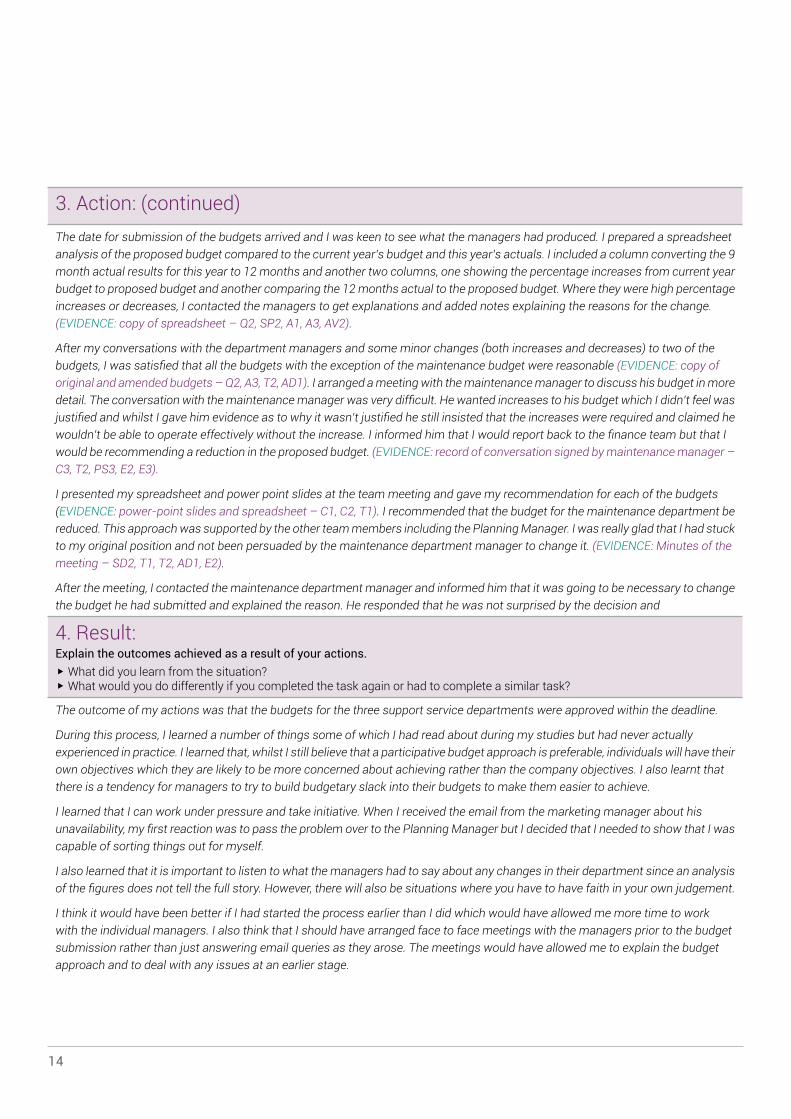

3. Action: (continued)The date for submission of the budgets arrived and I was keen to see what the managers had produced. I prepared a spreadsheet analysis of the proposed budget compared to the current year’s budget and this year’s actuals. I included a column converting the 9 month actual results for this year to 12 months and another two columns, one showing the percentage increases from current year budget to proposed budget and another comparing the 12 months actual to the proposed budget. Where they were high percentage increases or decreases, I contacted the managers to get explanations and added notes explaining the reasons for the change. (EVIDENCE: copy of spreadsheet – Q2, SP2, A1, A3, AV2).

After my conversations with the department managers and some minor changes (both increases and decreases) to two of the budgets, I was satisfied that all the budgets with the exception of the maintenance budget were reasonable (EVIDENCE: copy of original and amended budgets – Q2, A3, T2, AD1). I arranged a meeting with the maintenance manager to discuss his budget in more detail. The conversation with the maintenance manager was very difficult. He wanted increases to his budget which I didn’t feel was justified and whilst I gave him evidence as to why it wasn’t justified he still insisted that the increases were required and claimed he wouldn’t be able to operate effectively without the increase. I informed him that I would report back to the finance team but that I would be recommending a reduction in the proposed budget. (EVIDENCE: record of conversation signed by maintenance manager – C3, T2, PS3, E2, E3).

I presented my spreadsheet and power point slides at the team meeting and gave my recommendation for each of the budgets (EVIDENCE: power-point slides and spreadsheet – C1, C2, T1). I recommended that the budget for the maintenance department be reduced. This approach was supported by the other team members including the Planning Manager. I was really glad that I had stuck to my original position and not been persuaded by the maintenance department manager to change it. (EVIDENCE: Minutes of the meeting – SD2, T1, T2, AD1, E2).

After the meeting, I contacted the maintenance department manager and informed him that it was going to be necessary to change the budget he had submitted and explained the reason. He responded that he was not surprised by the decision and

4. Result: Explain the outcomes achieved as a result of your actions. w What did you learn from the situation?w What would you do differently if you completed the task again or had to complete a similar task?

The outcome of my actions was that the budgets for the three support service departments were approved within the deadline.

During this process, I learned a number of things some of which I had read about during my studies but had never actually experienced in practice. I learned that, whilst I still believe that a participative budget approach is preferable, individuals will have their own objectives which they are likely to be more concerned about achieving rather than the company objectives. I also learnt that there is a tendency for managers to try to build budgetary slack into their budgets to make them easier to achieve.

I learned that I can work under pressure and take initiative. When I received the email from the marketing manager about his unavailability, my first reaction was to pass the problem over to the Planning Manager but I decided that I needed to show that I was capable of sorting things out for myself.

I also learned that it is important to listen to what the managers had to say about any changes in their department since an analysis of the figures does not tell the full story. However, there will also be situations where you have to have faith in your own judgement.

I think it would have been better if I had started the process earlier than I did which would have allowed me more time to work with the individual managers. I also think that I should have arranged face to face meetings with the managers prior to the budget submission rather than just answering email queries as they arose. The meetings would have allowed me to explain the budget approach and to deal with any issues at an earlier stage.

H. SMART objective setting templateThe template below may be used to define and record specific, measurable, achievable, realistic, and time-based objectives. The objectives must relate to at least three of the core activities. Each objective can relate to one or more core activity. We recommend that objective setting takes place at least 6 to 9 months prior to attempting the EPA.

End-point assessment technical specification handbook 15

During the on programme phase, the employer (workplace mentor) should discuss and agree a number of SMART objectives with the apprentice. Followed up by an action /development plan of the tasks the apprentice is required to perform to meet each objective.

The objectives should provide sufficient opportunity for the apprentice to engage in a minimum of 3 to 5 significant and challenging tasks which the apprentice will produce a reflective statement on and submit to CIMA as part of their end-point assessment. Across the 3 to 5 tasks the apprentice must demonstrate all skills and behaviours as defined by the sub criteria in the assessment criteria.

Core activity: A: Preparing and using costing information

Key component

Specific What is the specific task?

MeasurableWhat are the standards or parameters?

AchievableIs the task feasible? What challenges may be faced?

Realistic What resources are needed to complete the task?

Time-BoundStart and end dates?

SMART objective:

16

End-point assessment technical specification handbook 17

© 2018 Association of International Certified Professional Accountants. All rights reserved. Association of International Certified Professional Accountants is a trademark of the Association of International Certified Professional Accountants and is registered in the United States, the European Union and other countries. The Globe Design is a trademark owned by the Association of International Certified Professional Accountants.

aicpa.orgaicpa-cima.com cgma.org cimaglobal.com

June 2018ISBN XXXXXXXXX