24

Tuesday, September 23, 2014 Augustine Doe Ron Marx Leveraging an organization’s current risk management to create a sustainable ERM program

Tuesday, September 23, 2014

Augustine Doe Ron Marx

Leveraging an organization’s current risk management to create a sustainable ERM program

AGENDAImportant considerations for ERMTransition from traditional risk management to ERM – best practicesKey enterprise risk management and monitoring toolsSustainable ERMDistilling top-tier enterprise-wide risksMapping top-tier risks on risk heat map to prioritize risk treatmentGenerating risk register to track ongoing risk management and monitoringCreating risk dashboards to monitor risk management’s performanceEstablishing risk tolerance policy to convey acceptable risk limitsDraft formal risk appetite statement to express the organization’s risk strategyQuestionsContact information

378

1011131 51719212324

2

8.3%10.6%

7.4%

Important considerations for ERM - Study

2013 Ernst & Young “Turning risks into results”* 2 0 1 1 Y T D r e p o r t e d a s o f 1 8 N o v e m b e r 2 0 1 1 .

Compound annual growth rates 2004–11* by risk maturity level

Revenue

16.8%Top 20%Middle 60%Bottom 20%

EBITDA

20.3%

9.5%

EBITDA/EV

4.1%2.5% 2.1%

• Do organizations with mature risk management practices outperform their peers financially?• Ernst & Young study suggests YES• Mature risk management drives financial results• Findings: companies with more mature risk management practices generated the highest growth

in revenue, EBITDA and EBITDA/EV

3

Total implementation timeline = 55 weeksBased on:

• $2 Billion in revenues• 40 executives interviewed during enterprise risk assessment• One internal full-time person• No mature traditional risk management program• Risk culture – perceives ERM as a checklist and an additional

cost that needs to be avoided

Important considerations for ERM - Timeline

Phase 1Identify Risks12-18 Weeks

Phase 2Assess Risks13-19 Weeks

Phase 3Monitoring/ Reporting12-18 Weeks

4

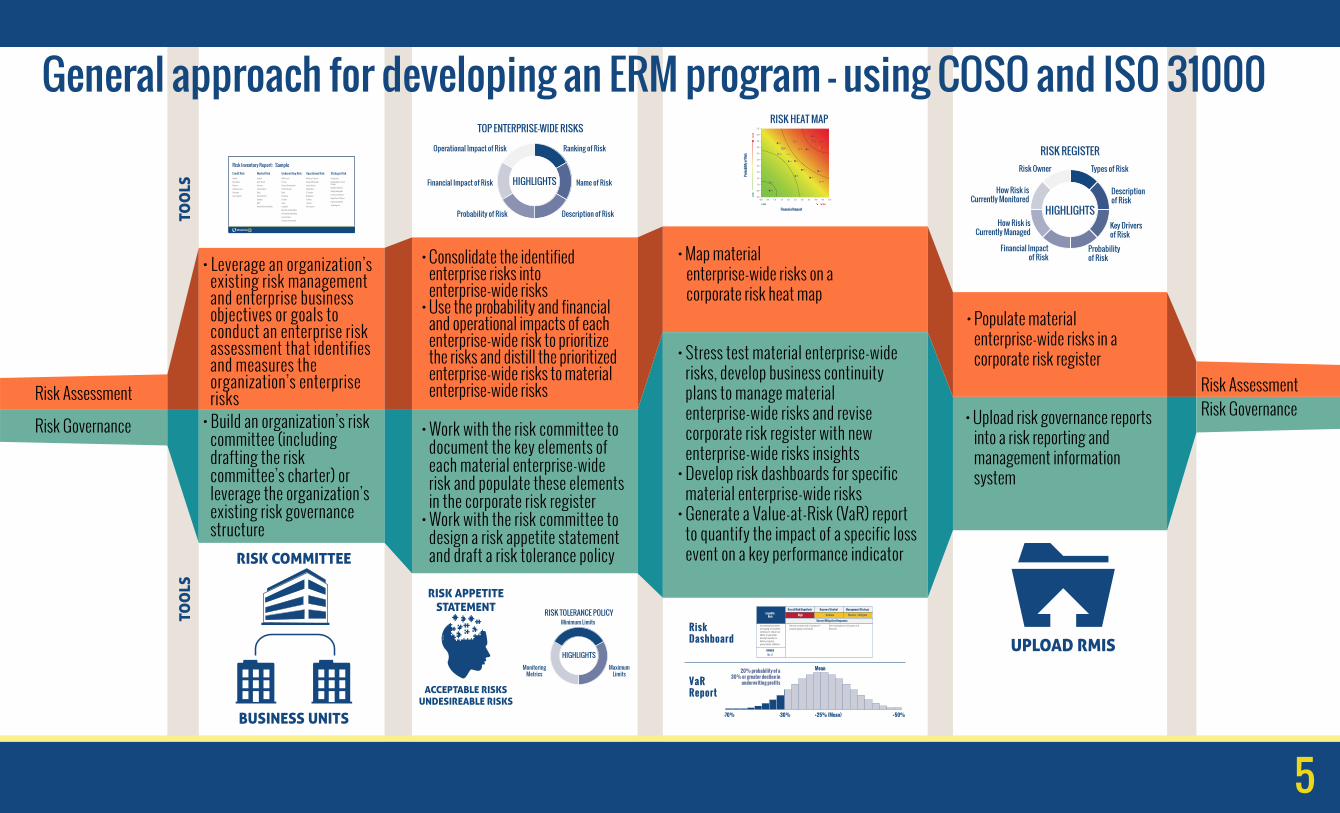

• Leverage an organization’s existing risk management and enterprise business objectives or goals to conduct an enterprise risk assessment that identifies and measures the organization’s enterprise risks

• Consolidate the identified enterprise risks into enterprise-wide risks

• Use the probability and financial and operational impacts of each enterprise-wide risk to prioritize the risks and distill the prioritized enterprise-wide risks to material enterprise-wide risks

• Work with the risk committee to document the key elements of each material enterprise-wide risk and populate these elements in the corporate risk register

• Work with the risk committee to design a risk appetite statement and draft a risk tolerance policy

• Map material enterprise-wide risks on a corporate risk heat map

• Upload risk governance reports into a risk reporting and management information system

• Populate material enterprise-wide risks in a corporate risk register• Stress test material enterprise-wide

risks, develop business continuity plans to manage material enterprise-wide risks and revise corporate risk register with new enterprise-wide risks insights

• Develop risk dashboards for specific material enterprise-wide risks

• Generate a Value-at-Risk (VaR) report to quantify the impact of a specific loss event on a key performance indicator

• Build an organization’s risk committee (including drafting the risk committee’s charter) or leverage the organization’s existing risk governance structure

Risk Assessment

Risk Governance

Risk AssessmentRisk Governance

Credit Risk Market Risk Underwriting Risk Operational Risk Strategic RiskDefault

Downgrade

Disputes

Settlement Lag

Sovereign

Concentration

Equities

Other Assets

Currency

Concentration

Basis

Re-investment

Liquidity

ALM

Interest Rate Sensitivity

UW Process

Pricing

Reserve Development

Product Design

Basis

Frequency

Severity

Lapse

Longevity

Mortality and Morbidity

Policyholder Optionality

Concentration

Economic Environment

Monetary Controls

Financial Reporting

Legal Controls

Distribution

IT Systems

Regulatory

Training

Turnover

Data Capture

Competition

Demographic / Social Change

Negative Publicity

Rating Downgrade

Customer Demands

Regulatory / Political

Capital Availability

Technological

Risk Inventory Report: Sample

Increasing bad debts and aging receivables continue to impair our ability to generate enough liquidity to defray ongoing policyholder liabilities

Review contract with Customer Y (largest aging receivable)

Sell receivable to third party at a discount

Liquidity Risk

Overall Risk Magnitude

OWNERMr. X

Current Mitigation Responses

Degree of Control Management Strategy

High Medium Monitor / Mitigate

20% probability of a30% or greater decline in

underwriting profits

Mean

-70% -30% +25% (Mean) +50%

VaRReport

RiskDashboard

Types of RiskRisk Owner

Descriptionof Risk

How Risk isCurrently Monitored

Key Driversof Risk

How Risk isCurrently Managed

Probabilityof Risk

Financial Impactof Risk

RISK REGISTER

HIGHLIGHTSFinancial Impact

Prob

abili

ty of

Risk

0.0

0.5

0.50.0 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

HIGHLOW

HIGH

LOW

H1

H4

H2

H3

M1

M2

M4

M3

C2

C1

IT1 L1

L4

L2

L3

R1

R2

F1

F2

O1

UPLOAD RMIS

RISK APPETITESTATEMENT

ACCEPTABLE RISKSUNDESIREABLE RISKS

RISK COMMITTEE

BUSINESS UNITS

TOP ENTERPRISE-WIDE RISKS

HIGHLIGHTS Name of Risk

Description of Risk

Ranking of Risk

Financial Impact of Risk

Probability of Risk

Operational Impact of Risk

RISK HEAT MAP

RISK TOLERANCE POLICY

HIGHLIGHTS

Minimum Limits

MaximumLimits

MonitoringMetrics

TOO

LSTO

OLS

5

General approach for developing an ERM program - using COSO and ISO 31000

Risk Assessment Deliverables

Solvency Assessment DeliverablesLiquidity &Liquidity RiskManagementReport

Risk- BasedCapital Report

Risk Governance Tools

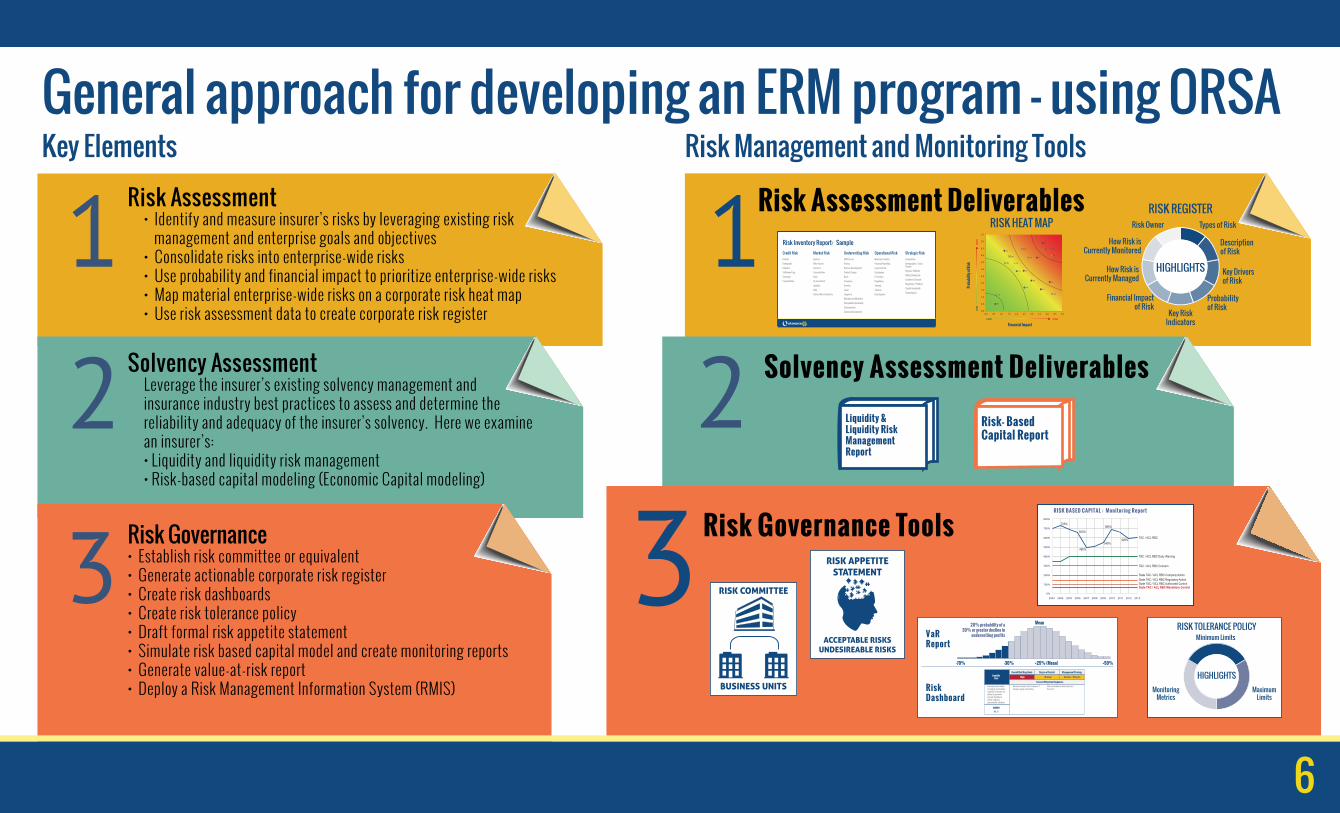

General approach for developing an ERM program – using ORSARisk Assessment

• Identify and measure insurer’s risks by leveraging existing risk management and enterprise goals and objectives

• Consolidate risks into enterprise-wide risks• Use probability and financial impact to prioritize enterprise-wide risks• Map material enterprise-wide risks on a corporate risk heat map• Use risk assessment data to create corporate risk register

Key Elements Risk Management and Monitoring Tools

Credit Risk Market Risk Underwriting Risk Operational Risk Strategic RiskDefault

Downgrade

Disputes

Settlement Lag

Sovereign

Concentration

Equities

Other Assets

Currency

Concentration

Basis

Re-investment

Liquidity

ALM

Interest Rate Sensitivity

UW Process

Pricing

Reserve Development

Product Design

Basis

Frequency

Severity

Lapse

Longevity

Mortality and Morbidity

Policyholder Optionality

Concentration

Economic Environment

Monetary Controls

Financial Reporting

Legal Controls

Distribution

IT Systems

Regulatory

Training

Turnover

Data Capture

Competition

Demographic / Social Change

Negative Publicity

Rating Downgrade

Customer Demands

Regulatory / Political

Capital Availability

Technological

Risk Inventory Report: Sample

Types of RiskRisk Owner

Descriptionof Risk

How Risk isCurrently Monitored

Key Driversof Risk

How Risk isCurrently Managed

Probabilityof Risk

Financial Impactof Risk

RISK REGISTER

HIGHLIGHTS

Key RiskIndicatorsFinancial Impact

Prob

abili

ty of

Risk

0.0

0.5

0.50.0 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

HIGHLOW

HIGH

LOW

H1

H4

H2

H3

M1

M2

M4

M3

C2

C1

IT1 L1

L4

L2

L3

R1

R2

F1

F2

O1

RISK HEAT MAP

Solvency AssessmentLeverage the insurer’s existing solvency management and insurance industry best practices to assess and determine the reliability and adequacy of the insurer’s solvency. Here we examine an insurer’s:• Liquidity and liquidity risk management• Risk-based capital modeling (Economic Capital modeling)

Risk Governance• Establish risk committee or equivalent• Generate actionable corporate risk register• Create risk dashboards• Create risk tolerance policy• Draft formal risk appetite statement• Simulate risk based capital model and create monitoring reports• Generate value-at-risk report• Deploy a Risk Management Information System (RMIS)

RISK BASED CAPITAL : Monitoring Report800%

700%

600%

500%

400%

300%

200%

100%

0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

TAC / ACL RBC

725%

650%

495%

549%

685%

595%

TAC / ACL RBC Early Warning

TAC / ACL RBC Concern

State TAC / ACL RBC Company ActionState TAC / ACL RBC Regulatory ActionState TAC / ACL RBC Authorized ControlState TAC / ACL RBC Mandatory Control

RISK APPETITESTATEMENT

ACCEPTABLE RISKSUNDESIREABLE RISKS

RISK TOLERANCE POLICY

HIGHLIGHTS

Minimum Limits

MaximumLimits

MonitoringMetrics

RISK COMMITTEE

BUSINESS UNITS Increasing bad debts and aging receivables continue to impair our ability to generate enough liquidity to defray ongoing policyholder liabilities

Review contract with Customer Y (largest aging receivable)

Sell receivable to third party at a discount

Liquidity Risk

Overall Risk Magnitude

OWNERMr. X

Current Mitigation Responses

Degree of Control Management Strategy

High Medium Monitor / Mitigate

20% probability of a30% or greater decline in

underwriting profits

Mean

-70% -30% +25% (Mean) +50%

VaRReport

RiskDashboard

6

• Understand your organizational culture – culture survey• Senior management must set the tone for implementing ERM• Must measure risk in order to effectively manage and monitor it• Leverage the organization’s existing risk management and don’t

reinvent the wheel• Do not try to do too much at once – implement ERM in

reasonable phases• Have a roadmap and execute so that management stays

continuously engaged with the process

Transition from traditional risk management to ERM – best practices

7

• Top-tier enterprise-wide risks• Risk heat map• Risk register• Risk dashboards• Risk tolerance policy• Risk appetite statement• Others: Value-at-risk report,

Risk-based capital report, Risk tornado diagrams, etc.

Key enterprise risk management and monitoring toolsThe order of ERM tools creation

• Risk appetite statement• Risk tolerance policy• Risk register• Risk dashboards• Other tools: Value-at-risk report, Risk

based capital report, Risk tornado diagrams, etc.

• Risk heat map• Top-tier enterprise-wide risks

The order of how senior management uses ERM tools

8

ERM tools at-a-glance

Credit Risk Market Risk Underwriting Risk Operational Risk Strategic RiskDefault

Downgrade

Disputes

Settlement Lag

Sovereign

Concentration

Equities

Other Assets

Currency

Concentration

Basis

Re-investment

Liquidity

ALM

Interest Rate Sensitivity

UW Process

Pricing

Reserve Development

Product Design

Basis

Frequency

Severity

Lapse

Longevity

Mortality and Morbidity

Policyholder Optionality

Concentration

Economic Environment

Monetary Controls

Financial Reporting

Legal Controls

Distribution

IT Systems

Regulatory

Training

Turnover

Data Capture

Competition

Demographic / Social Change

Negative Publicity

Rating Downgrade

Customer Demands

Regulatory / Political

Capital Availability

Technological

RISK INVENTORY REPORT: SAMPLE

BUSINESS UNIT RISKBUSINESS UNIT RISKBUSINESS UNIT RISKBUSINESS UNIT RISKManagement CommitteeManagement CommitteeManagement CommitteeManagement Committee

STRUCTURE OF A RISK COMMITTEE - SAMPLE

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

IndividualBusiness Units

EXECUTIVE MANAGEMENT BOARDReports

Audits

InternalAUDIT

Department

ENTERPRISE RISK MANAGEMENT COMMITTEE

REPORTS CHECKS

Board of DirectorsRisk Elements

RISK APPETITE STATEMENT: SAMPLE

Risks that are acceptable orOn-Strategy

Market Growth We will aggressively pursue regional strategies to meet our market growth objectives (increase of 4 percent in market share) and invest in and develop key markets.

Risks that are undesirable or Off-strategy

Reputation and brand image

We will avoid any situation and action resulting in a negative impact on our reputation, if and when an undesirable situation arises, manage it aggressively to protect our reputation and brand image.

Financial Derivatives We will limit our use of derivative instruments to "plain vanilla" swaps and options entered into with counterparties rated "AA" or better.

Strategic risk parameters Investment Limits We will limit capital expenditures and investments in mergers and acquisitions to an amount that allows the com-pany to achieve its annual free cash flow target of $330 million.

Financial risk parameters Target debt rating We will seek to maintain an enterprise-level debt rating of "A" or better.

Self sustaining growth In seeking new business, we will maintain our working capital ratio between 1 and 1.5 percent.

Operational risk parameters Loss Exposure We will manage our operational activities and exposures to avoid an event resulting in a loss to pre-tax operating margin of more than $25 million.

Geographical Independence

A single geographical location will not account for more than 20 percent of our total loans.

Financial Strength We will maintain an EBIT/Interest ratio between 4 and 5 percent.

Our Assertions Description of Risk Liquidation Value Policy Minimum Policy Maximum Monitoring Metrics

Borrower carrying more overall debt $5,000,000 to $15,000,000 2% monthly prime portfolio and 5% monthly subprime portfolio

4% monthly prime portfolio and 8% monthly subprime portfolio

Borrower debt to equity ratio

Subprime borrower default $5,000,000 to $15,000,000 10% monthly subprime portfolio 20% monthly subprime portfolio Monthly subprime default rate per 1,000 subprime loans

Borrower amount higher as a percentage of home valuations

$5,000,000 to $15,000,000 5% monthly sum of prime and subprime 7% monthly sum of prime and subprime Percentage difference in loan and home valuation

Particular lender noncompliance $5,000,000 to $15,000,000 Cost of fines $5,000,000Cost of fines $2,500,000 Total value of noncompliance fines

Mortgage origination fraud $1,000,000 to $5,000,000 Loss due to fraud $500,000 Loss due to fraud $2,500,000 Average loss due to origination fraud

Little or no documentation on borrower $1,000,000 to $5,000,000 20 incidents per month 30 incidents per month Number of no documentation incidents per month

Depreciating housing market $1,000,000 to $5,000,000 3% decline in home values 4% decline in home values Percentage decline in home values over a given period

Borrower concentration $625,000 to $1,000,000 20% California, 30% Florida 15% New York

30% California, 35% Florida, 20% New York

Percentage of loan portfolio by geographical region

Prime borrower default $500,000 to $1,000,000 4% monthly prime portfolio 6% monthly prime portfolio Monthly prime default rate per 1,000 prime loans

Borrower paying low minimum payments $500,000 to $1,000,000 2% monthly prime portfolio and 5% monthly subprime portfolio

4% monthly prime portfolio and 10% monthly subprime portfolio

Monthly percent of prime or subprime borrowers paying minimum payments

Inability to resell loans in secondary market $500,000 to $1,000,000 1% annual prime portfolio and 2% annual subprime portfolio

2% annual prime portfolio and 4% annual subprime portfolio

Annual percent of prime or subprime loans of borrowers with less than 5% equity

High interest rates $500,000 to $1,000,000 1% basis points on prime and 2% basis points on subprime 4% basis points on subprime

Basis points changes in prime or subprime rates2% basis points on prime and

RISK TOLERANCE REPORT: SAMPLE

Risk Category

Risk Description

Risk Drivers

Risk Probability

Risk Treatment

Risk Monitor

Risk Owner

Human Capital 5 = Certain $15,000,000$5,000,000

Head of Human Resources (SVP, HR)

Head of Compliance (SVP, Compliance)

Head of Finance (CFO)

Head of Clinicians (Chief Clinical Officer)

Head of Legal (SVP & General Counsel)

$5,000,000$1,000,000

$5,000,000$1,000,000

$5,000,000$1,000,000

$1,000,000$500,000

4 = Likely

4 = Likely

3 = Possible

3 = Possible

Regulatory Compliance

Financial

Clinical

Legal

Disparity between employee base salary and marketplace base salary

Potential HIPAA non-compliance

Decreasing revenue

Delivery of quality care

Sentinel events

(1) Freezes in merit raises(2) Amount of merit raises(3) Increasing employee cost of healthcare

benefits

(1) Laptop encryption not conforming to HIPAA standards

(2) Patient health information and files not conforming to HIPAA standards

(3) Sales, Marketing and certain employees exempted from ZIX

(1) Increased discounting of programs during marketing

(2) Failure to obtain insurance contracts(3) Increasing bad debts

(1) Failure of clinical staff to embrace treatment model

(2) Increasing acuity and complexity of patients

(3) Quality of physician pool

(1) Acuity of patients(2) Patient suicides(3) Patient drug overdose

(1) Targeted pay increases and job leveling roll-out(2) Rebid healthcare benefits in 20XX (3) Voluntary turnover rate(4) Number of exit interviews that cite compensation as key

(1) Log and track areas of non-compliance and pursue corrective actions

(2) Enforce annually required HIPAA training of all employees(3) Number of resolved non-compliance issues logged in the

compliance log(4) Amount and types of citations received as a result of

(1) Track and discuss with programs with lower than budgeted revenues how to improve revenues

(2) Increase collections training for Finance and Admissions(3) Bad debts expense as a % of revenue(4) Program allowances or discounts from revenue

(1) Use clinical treatment tool to educate and train clinical staff(2) Educate Admissions staff on how to screen-out

acute patients (3) Percentage of staff that completes clinical treatment training(4) Number of new sentinel event incidents

(1) Monitor and respond to sentinel events reported in the incident report system

(2) Create new clinical management interventions (3) Number of sentinel events per program per month,

quarter or year(4) Frequency and cost of sentinel-related litigation

RISK REGISTER: SAMPLE RISK BASED CAPITAL MONITORING REPORT: SAMPLE

800%

700%

600%

500%

400%

300%

200%

100%

0%

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

TAC / ACL RBC

725%

650%

495%

549%

685%

595%

TAC / ACL RBC Early Warning

TAC / ACL RBC Concern

State TAC / ACL RBC Company ActionState TAC / ACL RBC Regulatory ActionState TAC / ACL RBC Authorized ControlState TAC / ACL RBC Mandatory Control

H1 National healthcareR1 Potential HIPAA non-complianceF1 National healthcare regulationC1 Healthcare reform

Financial Impact

Very High Risk Medium Risk

Moderate Risk

LEGEND: Financial Impact LEGEND: Probability of Risk

High Risk

Prob

abili

ty of

Risk

0.0

0.5

0.50.0 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

HIGHLOW

HIGH

LOW

H1

H4

H2

H3

M1

M2

M4

M3

C2

C1

IT1 L1

L4

L2

L3

R1

R2

F1

F2

O1

L1 Specific economic conditionIT1 Inadequate IT systemsM1 RBC levelsL3 Pricing / reserving issues

1 <$500,0002 $500,000 to $1,000,0003 $1,000,000 to $5,000,0004 $5,000,000 to $15,000,0005 Over $15,000,000

1 Rare2 Unlikely3 Possible4 Likely5 Almost Certain

F2 LitigationM2 Unfunded mandates / cost shiftingL2 Adequacy of insurance coveragesO1 InvestmentsH2 Reputational risksM3 Provider contractingM4 Poor economyH3 Succession planning for senior managementR2 Fluctuation of asset valuesL4 Unanticipated substantial increase in Workers’

Compensation reserves

C1 PandemicsH4 Employee voluntary turnover

RISK HEAT MAP: SAMPLE

VALUE AT RISK REPORT: SAMPLE

20% probability of a30% or greater decline in

underwriting profits

(%) Change in Underwriting Profits

Mean

-70% -30% +25% (Mean) +50%

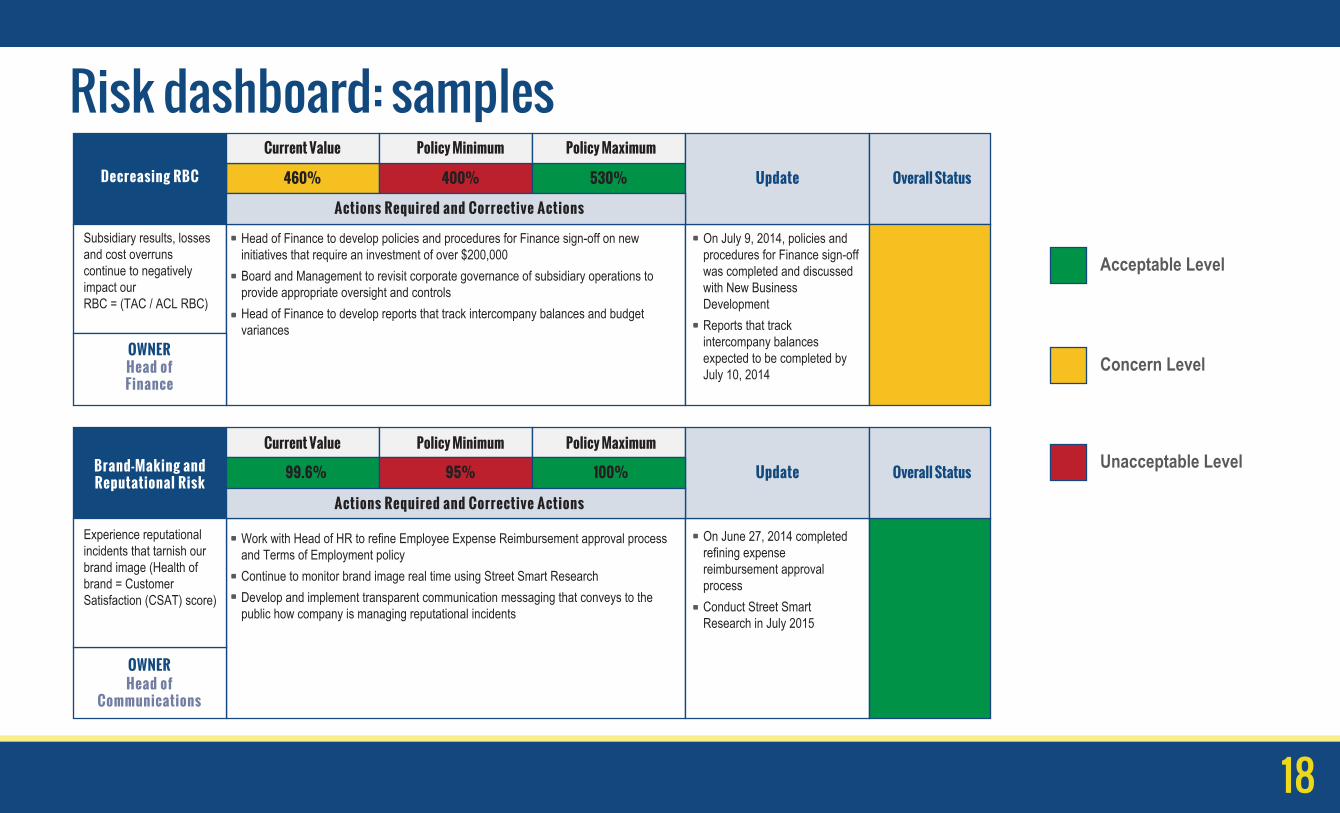

RISK DASHBOARD: SAMPLES

Increasing bad debts and aging receivables continue to impair our ability to generate enough liquidity to defray ongoing policyholder liabilities

Review contract with Customer Y (largest aging receivable)

Strategies agreed, any required funding in place and mitigation underway

Strategies agreed, any required funding in place and mitigation in early stages

Strategies in development, any required funding not yet in place as of yet, limited mitigation in process

Sell receivable to third party at a discount

Update

Liquidity Risk

Overall Risk Magnitude

OWNERMr. X

Current Mitigation Responses

Degree of Control Management Strategy

Future Mitigation Strategy Overall StatusHigh Medium Monitor / Mitigate

Hazards or catastrophic/ other events threaten the company’s ability to sustain operations and perform critical business functions or provide services to internal or external customers

Implementing enhanced supplier/vendor risk mgmt. processes (D&B Supplier Risk Mgmt. tool)

Additional updates from Mr. X

Update

Business ContinuityRisk

Overall Risk Magnitude

OWNERMrs. Y

Current Control Responses

MitigationP&C, General Liability, Crime and Fiduciary renewals bound 3/31/20XX

Significant improvements achieved in BI, Contingent BI, Flood, Earthquake and Wind coverage and sub-limits

Risk Transfer

Degree of Control Management Strategy

Future Mitigation Strategy Overall StatusHigh Medium Mitigate / Transfer

Annual Voluntary Turnover Rate (%) Risk: Employee Voluntary Turnover

60% 50% 40% 30% 20% 10% 0% Base Value = 30%, Total # of Employees = 4,500

Employee base salary 2655 45

Management of employees 2025 1305

Work/Life balance 1260

Tenure 1868 1125

Employee performance 1575 1260

Job characteristics 1395 1305

Developmental opportunities 1418 1328

1710

RISK TORNADO DIAGRAM: SAMPLE

9

Sustainable ERMLeverage your risk management knowledge and experience to move ERM forward

Distill many, many risks to arrive at your organization’s top-tier risks

• You have overall knowledge of the organization• You are the repository for exposure information and loss data• Gain knowledge of your business continuity, emergency response

and disaster recovery• You have the ability to prioritize risk based on probability and impact• You have the contacts throughout the organization

10

Distilling risks to arrive at top-tier enterprise-wide risks

• Risk assessment questionnaire• Consolidating risks• Determining enterprise-wide risks• Prioritizing enterprise-wide risks based on probability and impact• Arrive at top-tier enterprise-wide risks

11

Ranking Description of Risk Probability Financial Impact

1 Ineffectively managed subsidiary results cause liquidity pressures 5 5

2 Experience reputational incidents that tarnish brand image 4 5

3 Data loss at parent and subsidiaries exposes Company XYZ to privacy breaches 4 4

4 Decreasing RBC may affect Company XYZ’s solvency 4 3

5 The increased risk of underwriting health insurance in the post-ACA market environment may negatively impact Company XYZ’s financial strength and liquidity

3 4

Company XYZ’s top-tier enterprise-wide risks

12

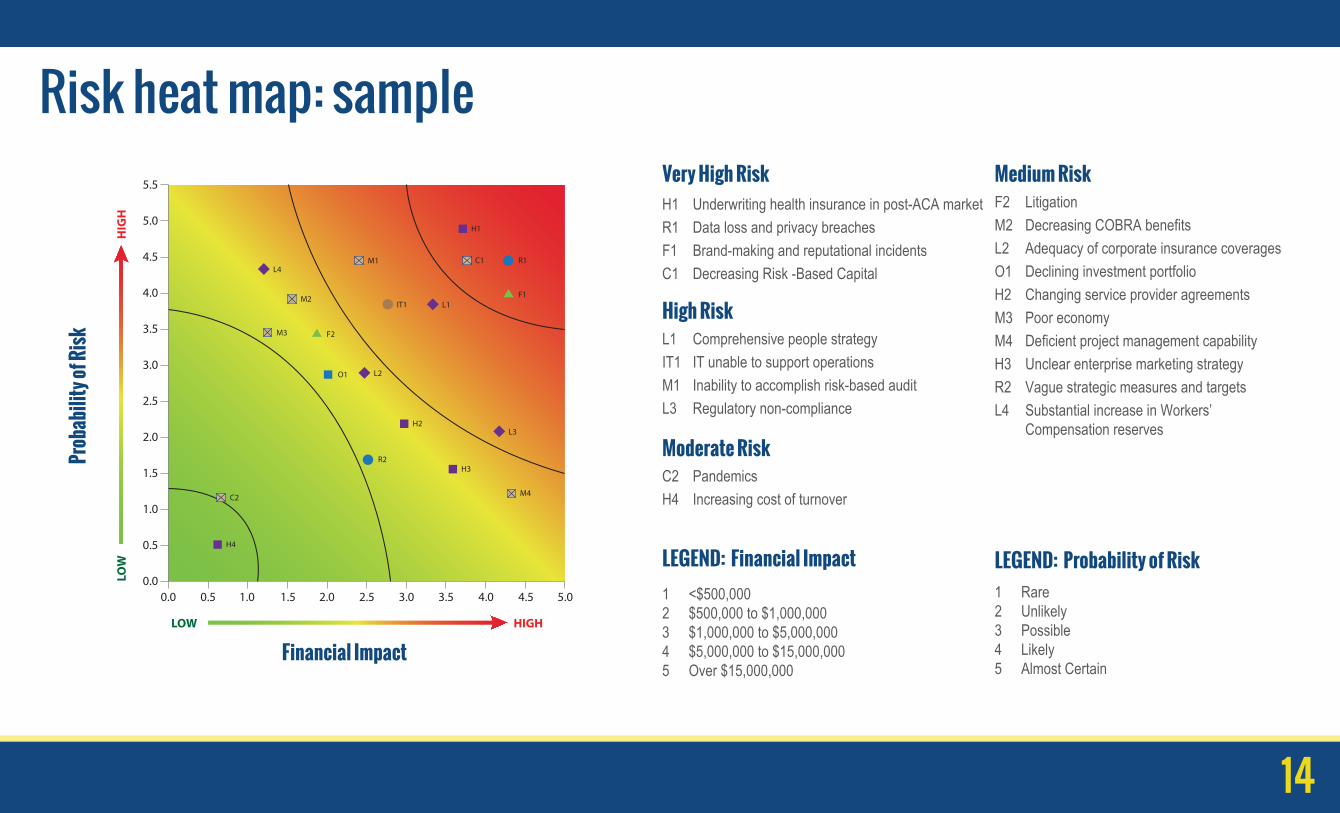

Mapping top-tier enterprise-wide risks on risk heat map toprioritize risk treatment

• Use Excel and PowerPoint• Use Riskonnect and other GRC softwares

13

H1 Underwriting health insurance in post-ACA marketR1 Data loss and privacy breachesF1 Brand-making and reputational incidentsC1 Decreasing Risk -Based Capital

Financial Impact

Very High Risk Medium Risk

Moderate Risk

LEGEND: Financial Impact LEGEND: Probability of Risk

High Risk

Prob

abili

ty of

Risk

0.0

0.5

0.50.0 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

HIGHLOW

HIGH

LOW

H1

H4

H2

H3

M1

M2

M4

M3

C2

C1

IT1 L1

L4

L2

L3

R1

R2

F1

F2

O1

L1 Comprehensive people strategyIT1 IT unable to support operationsM1 Inability to accomplish risk-based auditL3 Regulatory non-compliance

1 <$500,0002 $500,000 to $1,000,0003 $1,000,000 to $5,000,0004 $5,000,000 to $15,000,0005 Over $15,000,000

1 Rare2 Unlikely3 Possible4 Likely5 Almost Certain

F2 LitigationM2 Decreasing COBRA benefitsL2 Adequacy of corporate insurance coveragesO1 Declining investment portfolioH2 Changing service provider agreementsM3 Poor economyM4 Deficient project management capabilityH3 Unclear enterprise marketing strategyR2 Vague strategic measures and targetsL4 Substantial increase in Workers’

Compensation reserves

C2 PandemicsH4 Increasing cost of turnover

Risk heat map: sample

14

Generating risk register to track ongoingrisk management and monitoring

• Create Key Risk Indicators and risk metrics• Link each top-tier risk to a Key Performance Indicator (KPI)• Appoint risk owners – makes management more accountable• Develop an actionable risk register – actions required and dates

15

Ranking Description

1

2

3

4

5

Key Drivers of Risk Probability Financial ImpactKey Performance andRisk Indicators (KPIs & KRIs) Actions Required Owner

Head ofActuary

Head of IT

Head ofCommunications

Head ofFinance

Head ofHuman

Resources

5 = Certain $15,000,000$5,000,000

$5,000,000$1,000,000

$5,000,000$1,000,000

$5,000,000$1,000,000

$1,000,000$500,000

4 = Likely

4 = Likely

3 = Possible

3 = Possible

(1) Adverse selection(2) Competition(3) Premium constraints

(2) Employee security practices(3) Hackers

(1) Vendor security

(1) Lack of effective controls around employee agreements(2) Ineffective governance structure

(3) Talent acquisition and recruitment plans

(3) Major adverse event

(1) Subsidiary results(2) Subsidiary losses and cost overruns(3) Investment portfolio variability

(1) Unclear compensation program(2) Employee relations/engagement

(1) Monthly loss ratio analysis(2) Monthly claims trend analysis

(1) Number of vendors reviewed by security per month(2) Number of employee non-compliance with IT security practices per month

(1) Customer satisfaction (CSAT) score(2) Employee satisfaction (ESAT) score

(1) Quarterly ratio (%) of TAC/ ACL RBC(2) Month end budget variance

(1) Current month employee turnover (voluntary)(2) Revenue per employee

(1) Review reinsurance annually for adequacy of coverage(2) Report to board new business and renewal quotes

(1) Implement security management and controls by 20XX(2) Implement software that monitors emails real time by 20XX

(1) HR report to Board unique employee agreements(2) Continue to monitor CSAT and ESAT scores and implement corrective measures

(1) Purchase catastrophic reinsurance by 20XX(2) Finance sign-off on all major projects

(1) Beginning 20XX establish process for approving positions(2) Acquire new talent

Risk register: sample

Increased risk of underwriting health insurance in post -ACA market

Data loss that exposes company to privacy breaches

Brand-making and reputational incidents that impact brand health

Decreasing risk-based capital that may impact liquidity

Lack comprehensive people strategy

16

Creating risk dashboards to monitor risk management’sperformance

• KRIs and KPIs for board-level reporting• Risk metrics for executive-level reporting• Current value, target minimum and target maximum

17

Acceptable Level

Concern Level

Unacceptable Level

Decreasing RBC

Brand-Making andReputational Risk

OWNERHead ofFinance

Actions Required and Corrective Actions

Update Overall Status460% 400% 530%

OWNERHead of

Communications

Update Overall Status99.6% 95% 100%

Risk dashboard: samples

Current Value Policy Minimum Policy Maximum

Current Value Policy Minimum Policy Maximum

Actions Required and Corrective Actions

Subsidiary results, losses and cost overruns continue to negatively impact our RBC = (TAC / ACL RBC)

Experience reputational incidents that tarnish our brand image (Health of brand = Customer Satisfaction (CSAT) score)

Work with Head of HR to refine Employee Expense Reimbursement approval process and Terms of Employment policyContinue to monitor brand image real time using Street Smart ResearchDevelop and implement transparent communication messaging that conveys to the public how company is managing reputational incidents

•

••

Head of Finance to develop policies and procedures for Finance sign-off on new initiatives that require an investment of over $200,000Board and Management to revisit corporate governance of subsidiary operations to provide appropriate oversight and controlsHead of Finance to develop reports that track intercompany balances and budget variances

• On July 9, 2014, policies and procedures for Finance sign-off was completed and discussed with New Business DevelopmentReports that track intercompany balances expected to be completed by July 10, 2014

•

•

On June 27, 2014 completed refining expense reimbursement approval processConduct Street Smart Research in July 2015

•

•

•

•

18

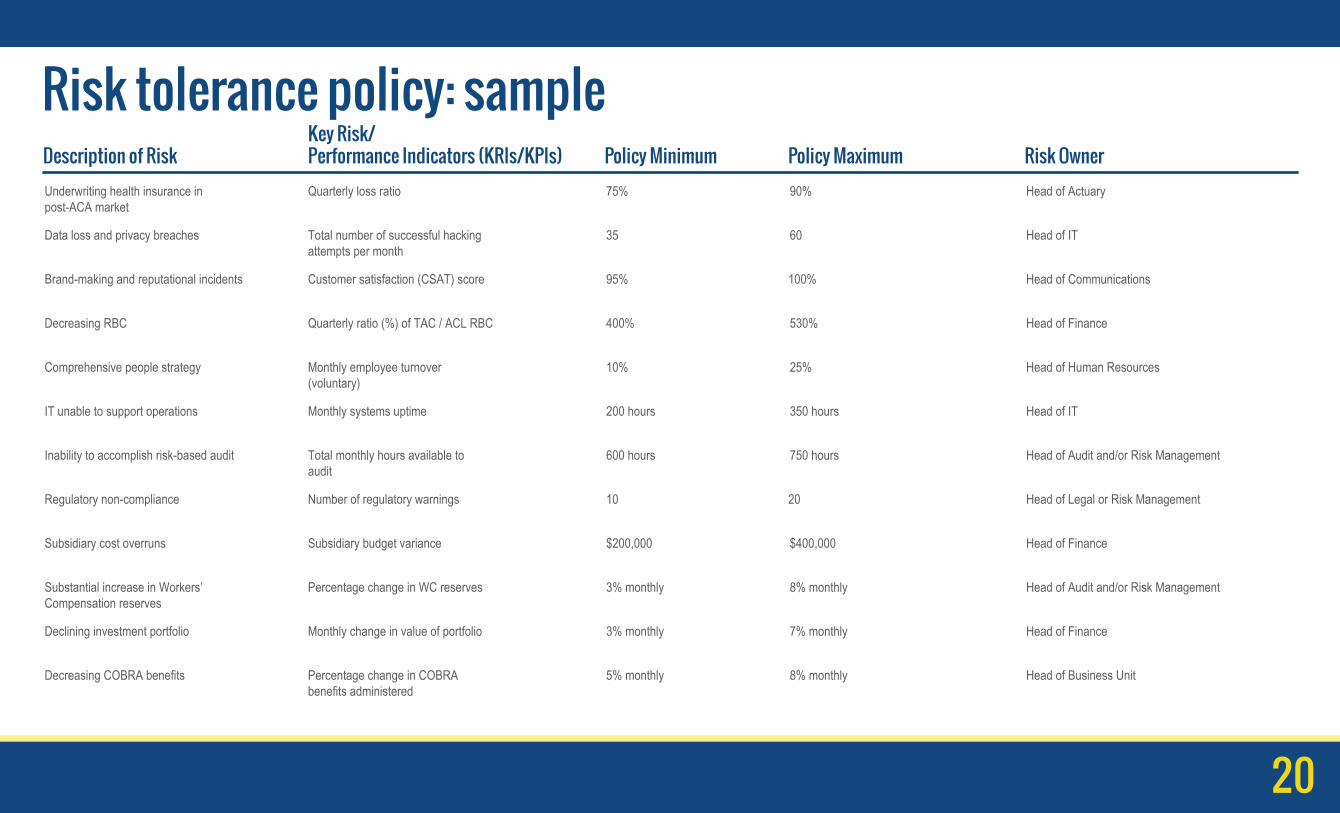

Establishing risk tolerance policy to convey acceptablerisk limits

• Meet with risk owners and determine the minimum and maximum limits for each KRI, KPI and risk metrics

• Determine appropriate corrective actions needed to normalize KRIs, KPIs and risk metrics

19

Description of RiskKey Risk/Performance Indicators (KRIs/KPIs) Policy Minimum Policy Maximum Risk Owner

Underwriting health insurance inpost-ACA market

Quarterly loss ratio 75% 90% Head of Actuary

Data loss and privacy breaches Total number of successful hackingattempts per month

35 60 Head of IT

Brand-making and reputational incidents Customer satisfaction (CSAT) score 95% 100% Head of Communications

Decreasing RBC Quarterly ratio (%) of TAC / ACL RBC 530%400% Head of Finance

Comprehensive people strategy Monthly employee turnover(voluntary)

10% 25% Head of Human Resources

IT unable to support operations Monthly systems uptime 200 hours 350 hours Head of IT

Inability to accomplish risk-based audit Total monthly hours available toaudit

600 hours 750 hours Head of Audit and/or Risk Management

Regulatory non-compliance Number of regulatory warnings 10 20 Head of Legal or Risk Management

Subsidiary cost overruns Subsidiary budget variance $200,000 $400,000 Head of Finance

Substantial increase in Workers’Compensation reserves

Percentage change in WC reserves 3% monthly 8% monthly Head of Audit and/or Risk Management

Declining investment portfolio Monthly change in value of portfolio 3% monthly 7% monthly Head of Finance

Decreasing COBRA benefits Percentage change in COBRAbenefits administered

5% monthly Head of Business Unit8% monthly

Risk tolerance policy: sample

20

• General counsel involvement in risk appetite statement• Guiding statement• Risk appetite elements• Risk assertions• Listing additional support

Draft formal risk appetite statement to express theorganization’s risk strategy

21

Risk Elements Our Assertions Additional Support

Formal risk appetite statement: sampleGuiding Statement

Brand-making and reputation

Contribution to Surplus

Network Provider Penetration

Operational Risk Parameters

Human Resources Risk Parameters

Capital Adequacy

22

This Formal Risk Appetite Statement is drafted solely for the purpose of providing Company XYZ, its subsidiaries and affiliates guidance on how to manage enterprise-wide risks. No statements made herein bind Company XYZ, its subsidiaries and affiliates to any contemplated contracts or agreements. Company XYZ, its subsidiaries and affiliates reserve the right to change any statements made herein with or without notice to any third parties.

Company XYZ is an insurance company that exists for the benefit of its policyholders. We protect our brand, maintain adequate capital, run sustainable subsidiary and affiliate operations, carry-out core operations and leverage our market share to ensure we return value to our policyholders.

Brand protection and enhancements: We strive to proactively avoid any situation or action that has the potential to unnecessarily impair our brand and reputation. This involves ensuring our employees, business partners and policyholders are committed to our values and that their actions and behaviors reflect these values. We believe this is what would allow us to take appropriate actions to preserve the strength of our brand and reputation in the areas of corporate compliance, customer privacy, corporate information security, governance and positive public image.

Risk-based capital: We will strive to grow to an RBC level appropriate to the risk of our core operations to ensure our sustainability in our market.(1) Controlled subsidiaries: Controlled subsidiaries are expected to manage their businesses and operations with the best interest of the shareholder and other appropriate stakeholders in mind. This expectation includes analysis and understanding of the risks associated with business initiatives to be undertaken by the controlled subsidiary. Further, controlled subsidiaries should comply with defined agreements (e.g. inter-company agreements, dividend policies, etc.) and governance processes as established with their shareholder.(2) External Portfolio risk: Must contemplate the risk profile of our controlled subsidiaries, the risk profile of our core business and Company XYZ's capital position.

Income/earnings: In order to remain viable in our market, we target an annual operating margin of 5% across all core operations. Product segments (both core and non-core) are expected to have a positive contribution to RBC.

Provider reimbursements: We will maintain adequate market share to provide the best value to our policyholders. We target no less than 50% of aggregate California health care providers' private payer revenue.

Contract management and bid and proposal review: No projects or bids will be pursued without appropriate review and analysis based on defined governance processes, which should include an assessment of material risks and financial impact.

Human Capital: We will ensure Company XYZ has identified key talent and leadership to develop new leaders through defined succession plans and development. We will maintain the resources and tools to attract, develop and retain the employees necessary to fulfill our mission.

Vision andMission Statements

Employee Expenses Reimbursement Policies Employment Policies

Investment Policy Intercompany Agreements and Dividend Policies with Subsidiaries

Human Resources Policies

QUESTIONS

23

Augustine [email protected](949) 466-6968

CONTACT INFORMATION

Ron [email protected](858) 552-3710

24