37

The Griffith Insurance Education Foundation INFORM+INSPIRE Life Insurance and Annuities R. B. Drennan, PhD Temple University August 20, 2011

| Date post: | 30-Dec-2015 |

| Category: |

Documents |

| Upload: | kaden-landry |

| View: | 32 times |

| Download: | 0 times |

The Griffith Insurance Education Foundation

INFORM+INSPIRE

Life Insurance and Annuities

R. B. Drennan, PhDTemple UniversityAugust 20, 2011

2

Life Numbers…

How long will you live?

What is “life expectancy”?

Males/Females Today: M / F

Life Expectancy At Birth

Year Female Male

1850 40.5 38.3

1900 51.1 48.3

1950 71.7 66.0

The Griffith Insurance Education Foundation

3

Mortality: Nature of the Loss (Premature Death)Meaning-- “Death with outstanding

unfulfilled financial obligations” Costs

Loss of earnings to family (Human Life Value) Final expenses (Liquidity Issue) Non-economic costs

Emotional loss, role models

Causes of death among young (~20) CA, S, OA, C

The Griffith Insurance Education Foundation

4

Life Numbers…

Probability of death for 20-35 year-old: In U.S.:

X out of 1,000

$100,000 of LI coverage: F * S .001 * $100,000 = $____ $1 per $1000 of face amount Price for pure protection

The Griffith Insurance Education Foundation

5

Term Life Insurance Pricing

time

$orp(l)

mortality curve (~term)

100x

The Griffith Insurance Education Foundation

6

Term Versus Permanent Pricing

time

$orp(l)

overpayment

underpaymentlevel

premium

mortality curve (~term)

100x

The Griffith Insurance Education Foundation

7

Life Insurance Products Traditional

Term Life Whole Life Endowment Annuities

Non-Traditional Universal Life Variable Life Variable Universal Life Variable Annuities

The Griffith Insurance Education Foundation

8

Life Insurance Rate (Price) Development Mortality Experience and Rating Factors

Age (group 20 and 60 year-olds?) Male / Female Smoker / Non-Smoker Race? Unique Factors: Hobbies, Job, Foreign Residence

Loading (Net Rate vs Gross Rate) Expenses Taxes Contingencies Profit

Interest (Long-term contract)

The Griffith Insurance Education Foundation

9

Objectives in Insurance Prices (Rates) Adequate

The payments generated by a block of policies plus any investment return on same must be sufficient to cover current / future benefits and costs

Equitable (not “unfairly” discriminatory) Refers to setting premiums commensurate with expected

losses and expenses; also suggests no cross subsidization. Sets a floor.

Not Excessive Sets a ceiling Competition Regulation (FL catastrophes)

The Griffith Insurance Education Foundation

10

Solvency Policing

Statutory Accounting ( A = L + Surplus ) Minimum Capital and Surplus Requirements Annual and Quarterly Financial Statements Audited Statements Required Statements Signed by an Actuary Company Examinations

Every 3 to 5 years Coordinated within zones

The Griffith Insurance Education Foundation

11

Solvency Policing Investment Restrictions

Type, quality, and quantity Insurers typically match assets and liabilities

Minimum Reserve Requirements

Solvency Monitoring Insurance Regulatory Information System (IRIS) FAST – Financial Analysis Solvency Tools Risk-Based Capital Requirements Ratings (Best, S&P, Weiss)

Holding Company Issues

The Griffith Insurance Education Foundation

12

Consumer Protection Product and Price

Rate criteria (not inadequate, not excessive, not “unfairly” discriminatory)

Types of rating laws Prior approval MLR in health insurance

Policy forms (products)

Underwriting

Agents and Brokers

The Griffith Insurance Education Foundation

Consumer Protection

Unfair Trade Practices Rebating, Twisting vs. Replacement

Market Conduct Examinations Policy Forms - Contracts

Definition of key terms Grace period Incontestability Clause Surrender values Reinstatement

The Griffith Insurance Education Foundation

14

Annuities

•Oscar Wilde:–“…It is better to have a permanent income than to be fascinating.”

The Griffith Insurance Education Foundation

15

The Risk We’ve worked and saved $1 million The Risk: We might live a (really) long

time and outlive our assets W.B.’s goal: In most countries:

65-year-old men and women can expect to live to 81 and 85

1/3 women and 1/5 men born today will live beyond 90

The Griffith Insurance Education Foundation

16

How Long Will Retirement Assets Last?

The Griffith Insurance Education Foundation

17

Life Insurance vs. Annuities

Think of as opposite of LI Life insurance addresses the risk of dying too

soon—mortality risk Annuities address the risk of living “too

long”—longevity risk

The Griffith Insurance Education Foundation

18

Life Insurance vs. Annuities Over 50% of Life Insurer premiums today

are for annuities instead of LI—why the shift from when they were only 25%?

Basic Idea is: For every $100,000, 65-year-old can receive ~$700 in monthly income ($8,400 per year), for life.

Now, women receive more or less than men? And why?

The Griffith Insurance Education Foundation

19

Annuities Defined Life Annuity

In return for a single premium or a series of premiums

Provides a series of periodic payments to a named person

Starting at a specified date (now or later) For life

…People always live forever when there is any annuity to be paid to them. Jane Austen

The Griffith Insurance Education Foundation

20

Purpose of Annuities Purpose: to provide an income that cannot

be outlived Insurer takes on longevity risk and investment risk Annuitant / Payee takes on risk of dying too soon

Live to 104, good deal; Die in 6 months, not so good

Insurer not so concerned with poor health of applicants for annuities

The Griffith Insurance Education Foundation

21The Griffith Insurance Education Foundation

One Product, Two Stages: A Deferred Stage, Then an Immediate Stage

Annuitization (conversion from

deferred to immediate stage)

Source: Black and Skipper, Life & Health Insurance, 13th edition, (Upper Saddle River, NJ: Prentice-Hall, 2000) p. 165.

22

Annuities—Mechanics Longevity risk is pooled by insurer

Insurer can predict the approximate number of annuitants who will be alive at the end of each year

Some individuals will live long / short The unliquidated contributions of those who die

early can be used to provide payments to those who live a long time – benefit of survivorship

Some people uncomfortable with big “forfeit”—to be discussed shortly. Thus, few people annuitize, and even fewer annuitize without some form of minimum guarantee

The Griffith Insurance Education Foundation

23

Annuity Settlement Options Cash option—lump sum or in installments for a period

of time Life annuity (no refund) – provides life income while

annuitant alive; payments end at death Highest periodic income But potential for big forfeiture

Life annuity w/ guaranteed payments Usually 5, 10, 15 or 20 years

In general, monthly benefit is related to risk borne by annuitant versus insurer

The Griffith Insurance Education Foundation

24The Griffith Insurance Education Foundation

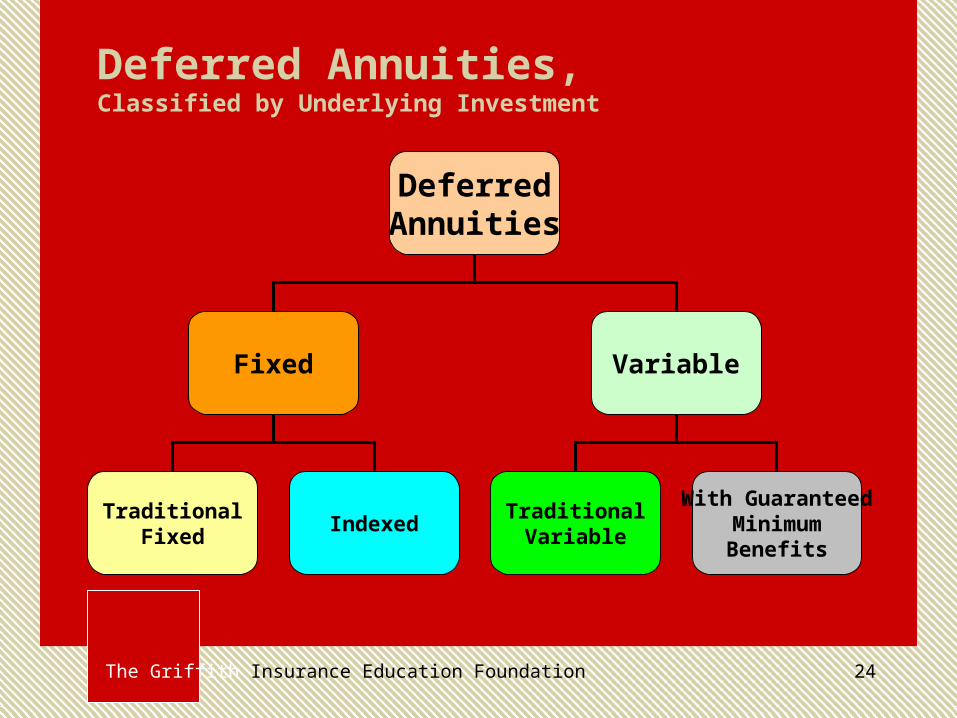

Deferred Annuities,Classified by Underlying Investment

DeferredAnnuities

Fixed Variable

TraditionalFixed

IndexedTraditional

Variable

With GuaranteedMinimumBenefits

Fixed Annuities

Traditional Fixed Guaranteed ROR at the time of purchase No investment risk for the purchaser More safety Tradeoff – ROR is very modest

The Griffith Insurance Education Foundation

Fixed Annuities

Indexed Annuities Splits the difference between a fixed and

variable annuity Fixed guaranteed minimum ROR Variable ROR tied to S&P Market Index

or some other barometer of investment growth

Can participate in the market while still protecting their principal

The Griffith Insurance Education Foundation

Variable Annuities

Traditional Variable Ties the growth of the annuity to stock

and mutual funds No guarantees offered by the insurer

The Griffith Insurance Education Foundation

Variable Annuities

Variable with Living Benefit Option Guaranteed minimum benefits Guaranteed benefits for life Guaranteed minimum ROR Opportunity for a portion of their funds to

be invested at a potentially higher ROR

The Griffith Insurance Education Foundation

Individual Annuity Sales – 2001-2010

The Griffith Insurance Education Foundation

30The Griffith Insurance Education Foundation

Annuity Regulation

Currently, Who RegulatesWhat?

31The Griffith Insurance Education Foundation

States Regulate Fixed and Variable Annuities

• Annuities are insurance products because,in their immediate annuity stage, they involve “life contingencies”

• This means the benefit depends on how long someone lives

• As insurance products, they are regulated by the states

• State regulation of annuities covers • Minimum reserves• Contract provisions• Market conduct standards

32The Griffith Insurance Education Foundation

Currently, the SEC Regulates Variable Annuities

The SEC considers a variable annuity an investment, not an insurance product

•Because the annuity owner retains the investment risk (unlike a fixed annuity, in which investment risk is transferred to the insurance/annuity company)

•SEC regulation is in addition to state securities regulation, but states typically copy SEC requirements

•SEC regulation of annuities covers • Market conduct standards

33The Griffith Insurance Education Foundation

Who Regulates Indexed Annuities?

• Indexed annuities are fixed annuity products • When interest is credited, the credit is determined by the

annuity company.• The determination uses a formula that the company can

change.• The formula uses an external index, often the S&P 500

• As fixed annuity product, they’re currently regulated by the states

• Even though indexed annuities • Determine investment growth by reference to a

stock market index, and• May be sold partly on the “upside potential,”

they’re not currently regulated by the SEC This issue is a matter of debate – Rule 151(a)

34The Griffith Insurance Education Foundation

“Suitability” Issue

• It involves matching• The customer’s characteristics, future plans for the

policy and related financial matters, the customer’s circumstances, and

• A policy’s characteristics

• Ideally, the policy should also be better suited for the customer’s needs than alternative financial products and/or arrangements.

35The Griffith Insurance Education Foundation

Who Decides What’s Suitable? Two Philosophies

• Let the buyer decide what’s suitable for him/herself

• Provide full and clear disclosure of all relevant information related to an annuity

• Put the “burden” on the seller to sell only products that are suitable for the buyer

• Specify types of information the seller must take into account

• Require that the insurer review prospective sales for suitability

36The Griffith Insurance Education Foundation

Summary of Annuities

• Annuities are financial products that many people find hard to understand

• Regulators have been concerned that some people are buying annuities that are unsuitable for them – particularly variable annuities

• Indexed annuities are still regulated by the states but have been proposed to be regulated by the SEC

• Suitability standards are inconsistent from one jurisdiction to another

• Regulation will differ depending on which suitability model is relied on

37The Griffith Insurance Education Foundation

Life Insurance and Annuities

Thank you For more information contact:

The Griffith Insurance Education Foundation623 High StreetWorthington, Ohio 43085

Phone: 614-880-9870Email: [email protected]