22

Life Sciences Compliance Risks - Focus on India October 2013 Yogesh Bahl Partner Life Sciences Industry Sector Deloitte Financial Advisory Services LLP

Life Sciences Compliance Risks - Focus on India

October 2013

Yogesh BahlPartnerLife Sciences Industry SectorDeloitte Financial Advisory Services LLP

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Disclosure

Information in this presentation represents the presenter’s opinions and recommendations and thus, may or may not be aligned with his or her

company’s views.

Information in this presentation is not intended to provide legal or other advice on any matter, in general or specific terms.

2

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Discussion Topics

• Market Overview

• Regulatory Environment & Compliance Issues

• Physician Code of Ethics – Interesting Excerpts

3

Market Overview

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Market Overview

5

CAGR – 17.8% from 2008 to 2016F

Source: IBEF Pharmaceutical Market March 2013

India is now among the top five pharmaceutical emerging

markets.

The front runner in a wide range of specialties involving complex drugs' manufacture, development, and technology.

Number of pharmaceutical companies are increasing their

operations in India.

Extremely fragmented market with severe price competition and government price control.

Domestic pharmaceutical market is expected to register a strong double-digit growth of

13-14 per cent in 2013.

Increasing sales of generic medicines, continued growth

in chronic therapies and a greater penetration in rural

markets.

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Product Segments

6

API is the active chemical or ingredient used in the manufacturing of a dosage form of a drug. Active pharmaceutical ingredients (APIs) is the largest segment of the Indian pharmaceuticals industry

APIs

Contract research and manufacturing services (CRAMS) is a fragmented market with more than 1000 players in IndiaCRAMS

Formulation is the process in which different chemical substances, including the active drug, are combined to produce a final medicinal product. It consists of prescription and OTC drugs

Formulation

Segments – A Sampling

Biosimilars are generic versions of the Biologics (therapies derived from living organisms or organic substances and include therapeutic proteins, DNA vaccines, monoclonal antibodies and fusion proteins, as well as new experimental modalities)

Biosimilars

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

API Market in India

7

Regulatory Changes in 2013•USFDA recent norms on Regulatory Classification of Pharmaceutical Co-Crystals•The EMA guidelines on exposure limits for production of varied medicinal products in shared facilities •The Central Drugs Standard Control Organisation (CDSCO) guidance document for the issue of Written Confirmation (WC) certificate for active substances exported to the European Union (EU) for medicinal products for human use

• The role of Indian API manufacturers in the global pharmaceutical supply chain is gradually evolving with increasing presence in synthesis and manufacture of late stage intermediates and APIs.

• Traditionally, innovators have frequently opted to perform final stages of API synthesis in-house or partner with specialized European suppliers while outsourcing early stage intermediates to Indian manufacturers. However, in recent times, the reputed track record of Indian companies in supplying quality products coupled with complex synthesis capabilities has enabled increasing participation in supply of late stage intermediates to innovator companies.

Indian API industry is now opting for environmentally- friendly production

processes.

Paradigm shift in the use of low-cost API drugs especially in innovative drugs which could further fuel the overall growth of the API market.

Producers moving away from multi- functional plants and instead of opting for specific activities at

particular sites.

API manufacturers are using various novel technologies to reduce the

processing time as well as to yield more production.

The patent expiry provides a significant opportunity for supply of

APIs to manufacturers of generic drugs.

Increased opportunities in outsourcing of bulk drugs by multinational pharmaceutical

companies.

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

CRAMS Market in India

8

• CRAMS business consists of the CMO and CRO, of which CMO constitutes a major portion (>60%) of the overall business.• CRAMS industry would continue to be dominated by the CMO segment forming larger portion of it, however we expect the share

of CMO is likely to narrow down from ~61% in 2010 to 55% in 2014E; foreseeing revival in CRO segment.• Indian CRAMS companies are the most preferred players for global pharmaceutical companies due to their product mix being

skewed towards high-end research services, biologics and complex technology services, at low cost. • Increase in cost of R&D for new chemical entities, raw materials and wage inflation are few additional factors causing pharma

companies to look out for outsourcing solutions in Indian markets.

DriversDemand for new

drugs/generics and patent cliff/cost

pressures

OpportunitiesDevelopment in co- development rather than outsourcing

agreements

ChallengesUnorganised regulatory procedures, reduction

in budgets, competition from other

countries

StrengthsTechnologically

oriented, a strong man power, cost differential

benefits

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Formulations Market in India

9

CAGR – 14%CAGR – 12.2%

OpportunitiesHigh penetration in the global markets and increase of

share in Abbreviated New Drug Application (ANDA) filings are likely to power growth of the formulations

market.

Formulations Market

Chronic Therapy Acute Therapy

• Cardiovascular• Neurological• Anti-diabetes• Oncology

• Anti-infective• Gastro-intestinal• Respiratory• Analgesics/Pain

Management• Vitamins/Neutraceu

ticals

ChallengesComplex drug distribution system, diverse market and rural penetration, evolving regulatory infrastructure, brand visibility and uncertainty in pricing policies.

StrengthsIndia is almost self sufficient

in formulations and formulations is a high-margin business. external sales is coming from value-added

formulations.

TrendsPrice pressure as benefits of cheaper drugs have been

shifted to end-users and trade channels. Hence, consolidation, partnership and alliances are expected to

gather momentum in the near future.

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

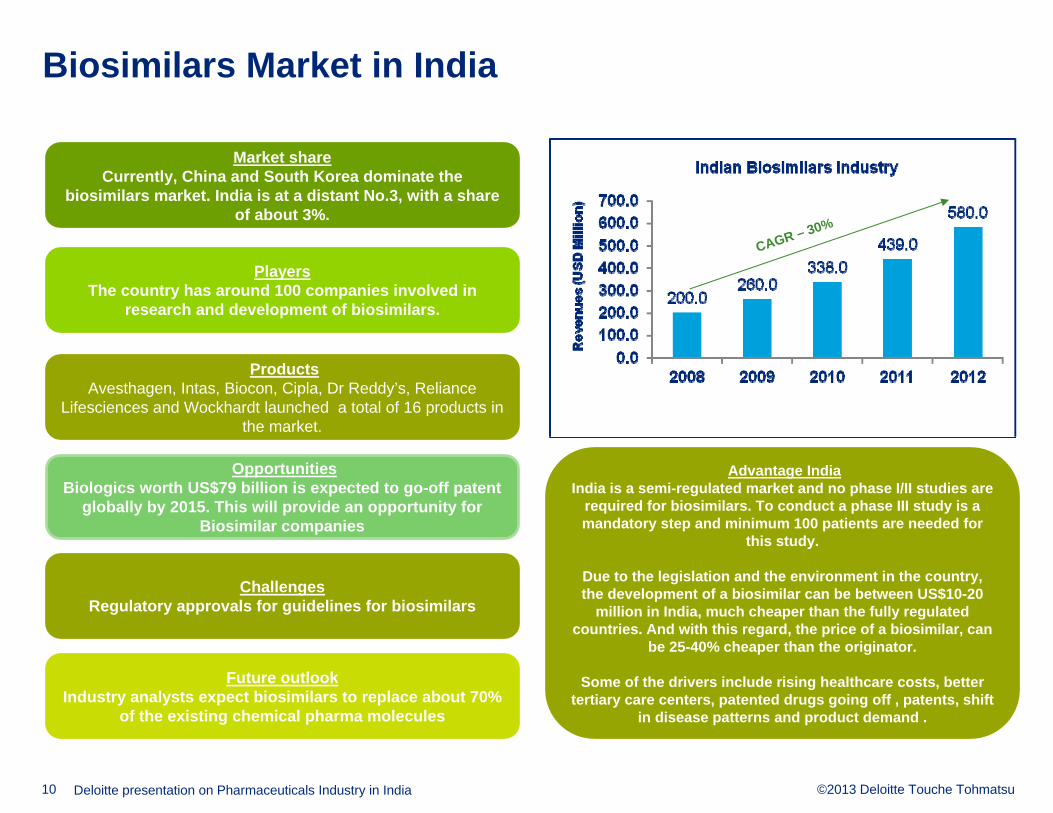

Biosimilars Market in India

10

CAGR – 30%

OpportunitiesBiologics worth US$79 billion is expected to go-off patent

globally by 2015. This will provide an opportunity for Biosimilar companies

ChallengesRegulatory approvals for guidelines for biosimilars

Advantage IndiaIndia is a semi-regulated market and no phase I/II studies are

required for biosimilars. To conduct a phase III study is a mandatory step and minimum 100 patients are needed for

this study.

Due to the legislation and the environment in the country, the development of a biosimilar can be between US$10-20

million in India, much cheaper than the fully regulated countries. And with this regard, the price of a biosimilar, can

be 25-40% cheaper than the originator.

Some of the drivers include rising healthcare costs, better tertiary care centers, patented drugs going off , patents, shift

in disease patterns and product demand .

PlayersThe country has around 100 companies involved in

research and development of biosimilars.

Market shareCurrently, China and South Korea dominate the

biosimilars market. India is at a distant No.3, with a share of about 3%.

Future outlookIndustry analysts expect biosimilars to replace about 70%

of the existing chemical pharma molecules

ProductsAvesthagen, Intas, Biocon, Cipla, Dr Reddy’s, Reliance

Lifesciences and Wockhardt launched a total of 16 products in the market.

Regulatory Environment

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Regulatory Environment in India

National Pharma Policy 2011 bring greater transparency in pricing of essential drugs

12

Essentiality of drugs

• Essentiality of drugs is determined by inclusion of the drug in the National List of Essential Medicines (NEDL)

• Promote rational use of medicines based on cost, safety and efficacy

Market-based pricing

• Cost based pricing is complicated and time consuming in comparison to market based pricing

• Market based pricing is expected to create greater transparency in pricing information would be available in public domain

Price control of finished medicines only

• Only finished medicines are to be considered essential which would prevent price control of APIs which are not necessarily used for essential drugs

Policy support

• Reduction in approval time for new facilities. E.g. NOC for export license issued in two weeks compared to 12 weeks earlier.

• MOUs with USFDA, WHO, Health Canada, etc. to boost growth of the Indian Pharma sector by benefiting from their expertise.

• Government of India plans to set up a US$640 million VC fund to boost drug discovery and strengthen the pharma infrastructure.

• Pharma Vision 2020 by the government’s Department of Pharmaceuticals aims to make India a major hub for end-to-end drug discovery.

• Zero duty for technology upgrades in the pharmaceutical sector through the Export Promotion Capital Goods (EPCG) Scheme

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Regulatory Bodies and Regulations

13

Central Drugs Standard Control Organization (CDSCO), Ministry of Health & Family Welfare, Government of India provides general information about drug regulatory requirements in India.

CDSCO

Drugs (Price Control) Order 1995 and other orders enforced by National Pharmaceutical Pricing Authority (NPPA), Government of India.NPPA

The Drugs & Cosmetics Act, 1940 regulates the import, manufacture, distribution and sale of drugs in India.

D & C Act, 1940

Regulatory Resources – A Sample

Schedule M of the D&C Act specifies the general and specific requirements for factory premises and materials, plant and equipment and minimum recommended areas for basic installation for certain categories of drugs.

Schedule M

Source: Indian Pharmaceutical Association

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Challenges for the Industry

14

Infrastructure development

Quality Management

Drug price control

Effects of the new product patent

Conformance to global standards

Regulatory reforms

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Compliance-Relevant Developments

- US FDA tightens regulatory enforcement on drug companies in India; focus on cGMP

- Anticorruption Legislation

- Clinical trials

- Increase in complaints involving ties between doctor and pharmaceutical companies

- The government is considering a 'Uniform Code of Pharmaceutical Marketing Practices' to deal with the alleged nexus between regulatory, doctors and drug companies

- Compulsory Licensing – R&D Strategy, Commercial Strategy, and Intellectual Property ramifications

15

Physician’s Code of Ethics

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Medical Counsel of India – Code of Medical Ethics Excerpts

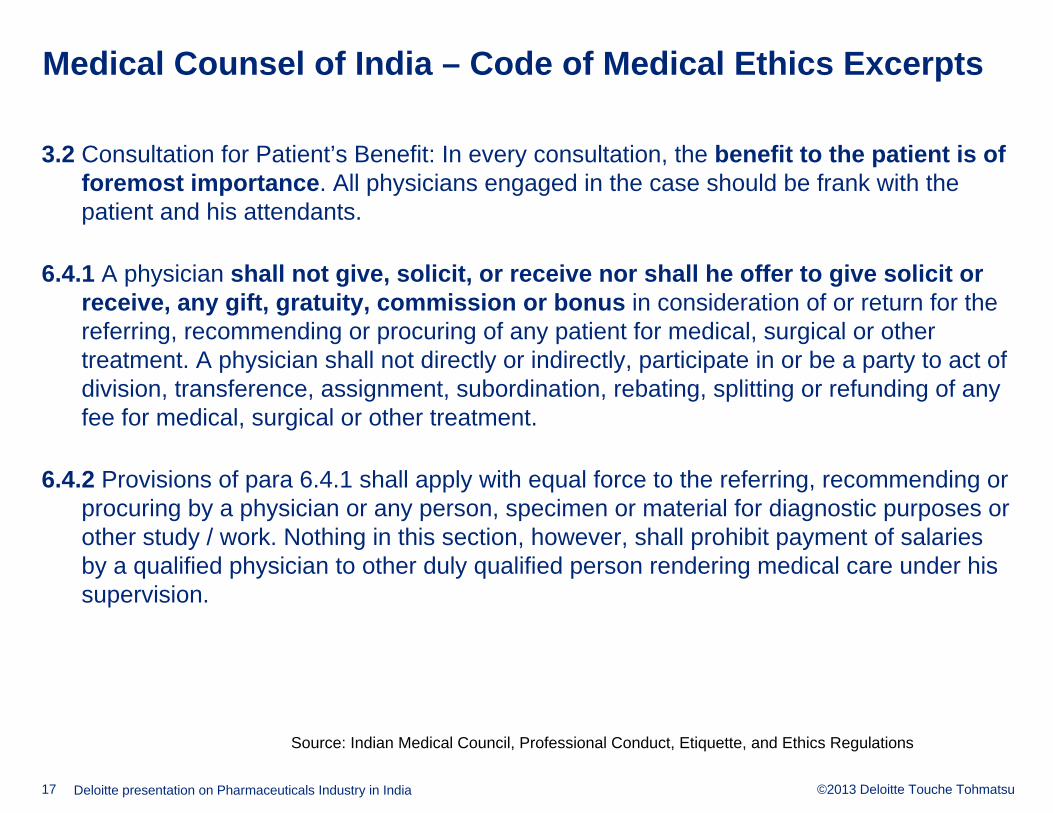

3.2 Consultation for Patient’s Benefit: In every consultation, the benefit to the patient is of foremost importance. All physicians engaged in the case should be frank with the patient and his attendants.

6.4.1 A physician shall not give, solicit, or receive nor shall he offer to give solicit or receive, any gift, gratuity, commission or bonus in consideration of or return for the referring, recommending or procuring of any patient for medical, surgical or other treatment. A physician shall not directly or indirectly, participate in or be a party to act of division, transference, assignment, subordination, rebating, splitting or refunding of any fee for medical, surgical or other treatment.

6.4.2 Provisions of para 6.4.1 shall apply with equal force to the referring, recommending or procuring by a physician or any person, specimen or material for diagnostic purposes or other study / work. Nothing in this section, however, shall prohibit payment of salaries by a qualified physician to other duly qualified person rendering medical care under his supervision.

17

Source: Indian Medical Council, Professional Conduct, Etiquette, and Ethics Regulations

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Medical Counsel of India – Code of Medical Ethics Excerpts (cont)6.8.1a) Gifts: A medical practitioner shall not receive any gift from any pharmaceutical or

allied health care industry and their sales people or representatives.

b) Travel facilities: A medical practitioner shall not accept any travel facility inside the country or outside, including rail, air, ship , cruise tickets, paid vacations etc. from any pharmaceutical or allied healthcare industry or their representatives for self and family members for vacation or for attending conferences, seminars, workshops, CME programme etc as a delegate.

c) Hospitality: A medical practitioner shall not accept individually any hospitality like hotel accommodation for self and family members under any pretext.

d) Cash or monetary grants: A medical practitioner shall not receive any cash or monetary grants from any pharmaceutical and allied healthcare industry for individual purpose in individual capacity under any pretext. Funding for medical research, study etc. can only be received through approved institutions by modalities laid down by law / rules / guidelines adopted by such approved institutions, in a transparent manner. It shall always be fully disclosed.

18

Source: Indian Medical Council, Professional Conduct, Etiquette, and Ethics Regulations

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

Medical Counsel of India – Code of Medical Ethics Excerpts (cont)6.8.1e) Medical Research: A medical practitioner may carry out, participate in, work in research

projects funded by pharmaceutical and allied healthcare industries. A medical practitioner shall:

(iv) Ensure that the source and amount of funding is publicly disclosed at the beginning itself.

(vii) Ensure that while accepting such an assignment a medical practitioner shall have the freedom to publish the results of the research in the greater interest of the society by inserting such a clause in the MoU or any other document / agreement for any such assignment.

f) Maintaining Professional Autonomy: In dealing with pharmaceutical and allied healthcare industry a medical practitioner shall always ensure that there shall never be any compromise either with his / her own professional autonomy and / or with the autonomy and freedom of the medical institution.

19

Source: Indian Medical Council, Professional Conduct, Etiquette, and Ethics Regulations

©2013 Deloitte Touche TohmatsuDeloitte presentation on Pharmaceuticals Industry in India

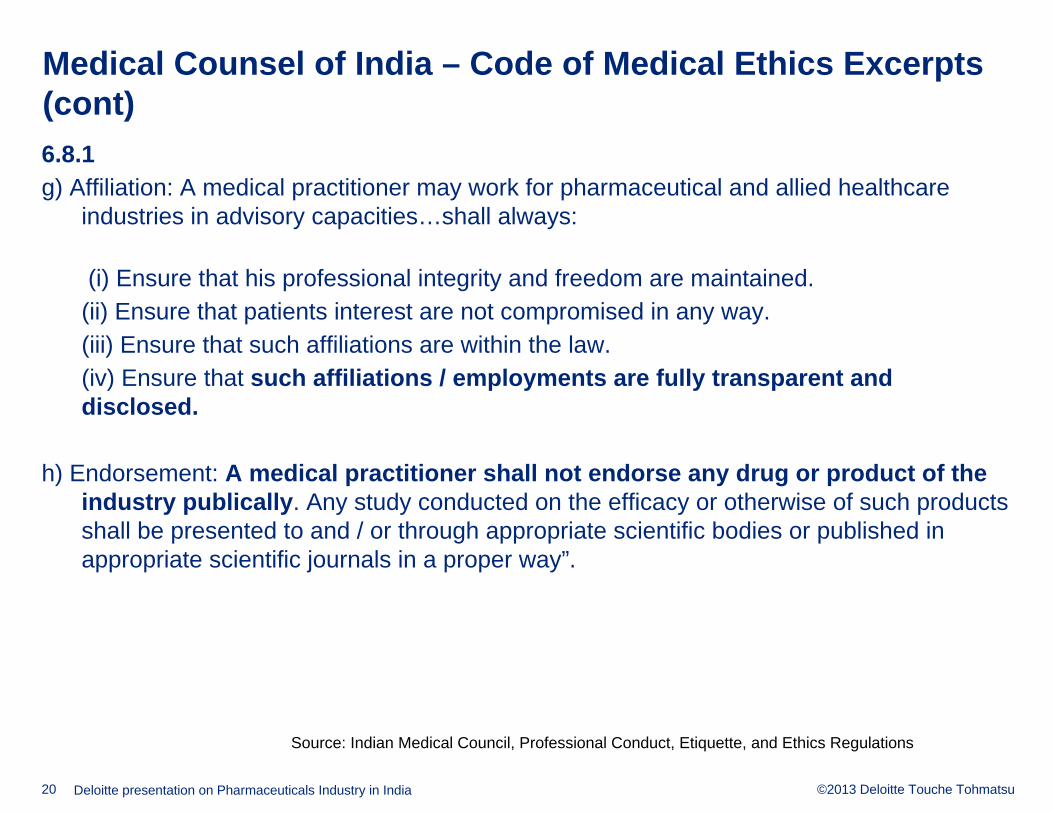

Medical Counsel of India – Code of Medical Ethics Excerpts (cont)6.8.1 g) Affiliation: A medical practitioner may work for pharmaceutical and allied healthcare

industries in advisory capacities…shall always:

(i) Ensure that his professional integrity and freedom are maintained.(ii) Ensure that patients interest are not compromised in any way.(iii) Ensure that such affiliations are within the law.(iv) Ensure that such affiliations / employments are fully transparent and disclosed.

h) Endorsement: A medical practitioner shall not endorse any drug or product of the industry publically. Any study conducted on the efficacy or otherwise of such products shall be presented to and / or through appropriate scientific bodies or published in appropriate scientific journals in a proper way”.

20

Source: Indian Medical Council, Professional Conduct, Etiquette, and Ethics Regulations

Contact Information

Yogesh BahlPartnerDeloitte Financial Advisory Services LLPT: +917.306.7882E: [email protected]

Yogesh helps companies mitigate enterprise risks, investigate financial crimes, and manage commercial disputes. Yogesh has advised multinational companies on risk, contract and accounting issues involving a broad range of products within the pharmaceutical, medical device, biotechnology and consumer sectors. Yogesh has also been engaged as an expert and an arbiter with respect to litigation involving intellectual property, breach of contract and industry practice issues. Yogesh is currently focused on helping companies develop various tools and analytics to manage third party risks. Yogesh has also advised a number of companies in various industries on compliance issues, preventing and detecting fraud, managing third party risk. In addition, he has strong experience with the financial structure and provisions of joint venture, co-development, co- promotion, and cross-licensing deals. Yogesh has earned his MBA in Finance and Statistics and his BS in Accounting and International Business from NYU’s Stern’s School of Business. Yogesh is also a Certified Public Accountant.

©2013 Deloitte Touche Tohmatsu

Dhruv PhophaliaSenior Director Deloitte Touche Tohmatsu India Private Limited T: +91 (22) 6185 5208E: [email protected]

Dhruv is a Senior Director (Partner) at Deloitte Touche Tohmatsu India Private Limited. Dhruv focuses on the life sciences industry in India and has advised various life sciences clients in the U.S., and India on a wide range of areas such as compliance and risk management, anti-fraud programs and controls, anti- corruption consulting, investigations and cross-border disputes/arbitrations.Before relocating to India , Dhruv worked with Deloitte in the United States for over 12 years where he led and managed engagements for a number of Fortune 500 companies. He has led and managed a number of high profile engagements in India, Southeast Asia, Europe, and United States of America for domestic and international clients representing a wide range of industries including life sciences, technology media and telecommunications, manufacturing, construction, financial services, and oil and gas. Previously, Dhruv was also involved in setting up Deloitte’s forensic and dispute consulting business in India.

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

This material has been prepared by Deloitte Touche Tohmatsu India Private Limited (“DTTIPL”), a member of Deloitte Touche Tohmatsu Limited, on a specific request from you and contains confidential information. The information contained in this material is intended solely for you thereby, any disclosure, copy or further distribution of this material or the contents thereof may be unlawful and is strictly prohibited.

©2013 Deloitte Touche Tohmatsu

Source for quantitative information:IBEF Pharmaceutical Market Report March 2013