ASX: LNG and OTC ADR: LNGLY Liquefied Natural Gas Limited Go East, Young Man An Alternative for Western Canada’s Potentially Stranded Gas Gastech Conference, Chiba, Japan John Baguley, Chief Technical Officer, LNG Limited Scott Atha, Director – Marketing & Commercial Strategy, Bear Head LNG Corporation 04 April 2017

Transcript

ASX: LNG and OTC ADR: LNGLY

Liquefied Natural Gas Limited

Go East, Young ManAn Alternative for Western Canada’s Potentially Stranded Gas

Gastech Conference, Chiba, Japan

John Baguley, Chief Technical Officer, LNG LimitedScott Atha, Director – Marketing & Commercial Strategy, Bear Head LNG Corporation

04 April 2017

22

Agenda

• Introduction – Go West East, Young Man

• Historical Perspective on Canadian natural gas

• Technical Considerations – unconventional gas as LNG feedstock

• Canadian Exports – the case for the West

• Canadian Exports – the case for the East

• Canadian East Coast Case Study – Bear Head LNG

33

Go East, Young Man

Magnolia LNG Bear Head LNG

Fisherman’s LandingHorace Greeley, 1811 - 1872

• Editor and Founder, New-York Tribune

• US Representative, 1848-1849

• Presidential Candidate, 1872

• Staunch liberal, yet founding member of Republican Party

• Apparent proponent of “neck beards”

“Washington is not a place to live in. The rents are high, the food is bad, the dust is disgusting and the morals are deplorable. Go West, young man, go West and grow up with the country.”

In new directions, new generations can find new opportunities

44

Canadian Natural Gas Production

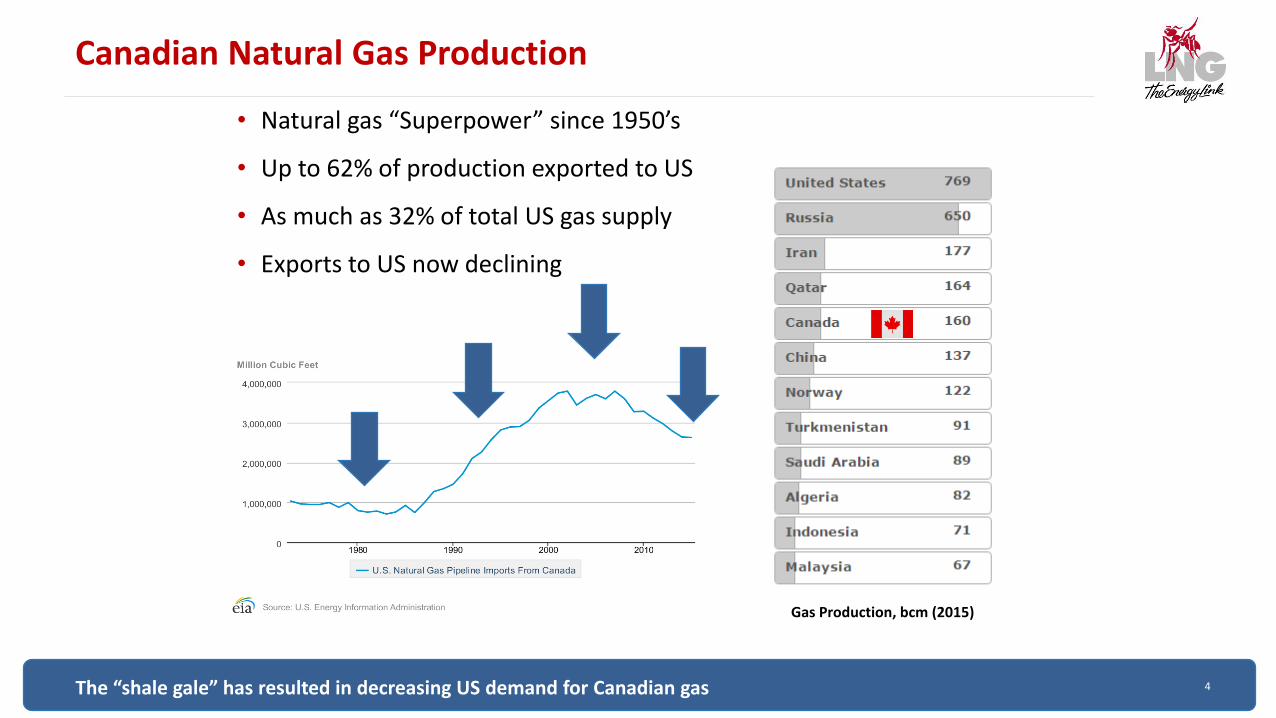

The “shale gale” has resulted in decreasing US demand for Canadian gas

Gas Production, bcm (2015)

• Natural gas “Superpower” since 1950’s

• Up to 62% of production exported to US

• As much as 32% of total US gas supply

• Exports to US now declining

55

W. Canadian Basis and pipeline export forecasts to 2030

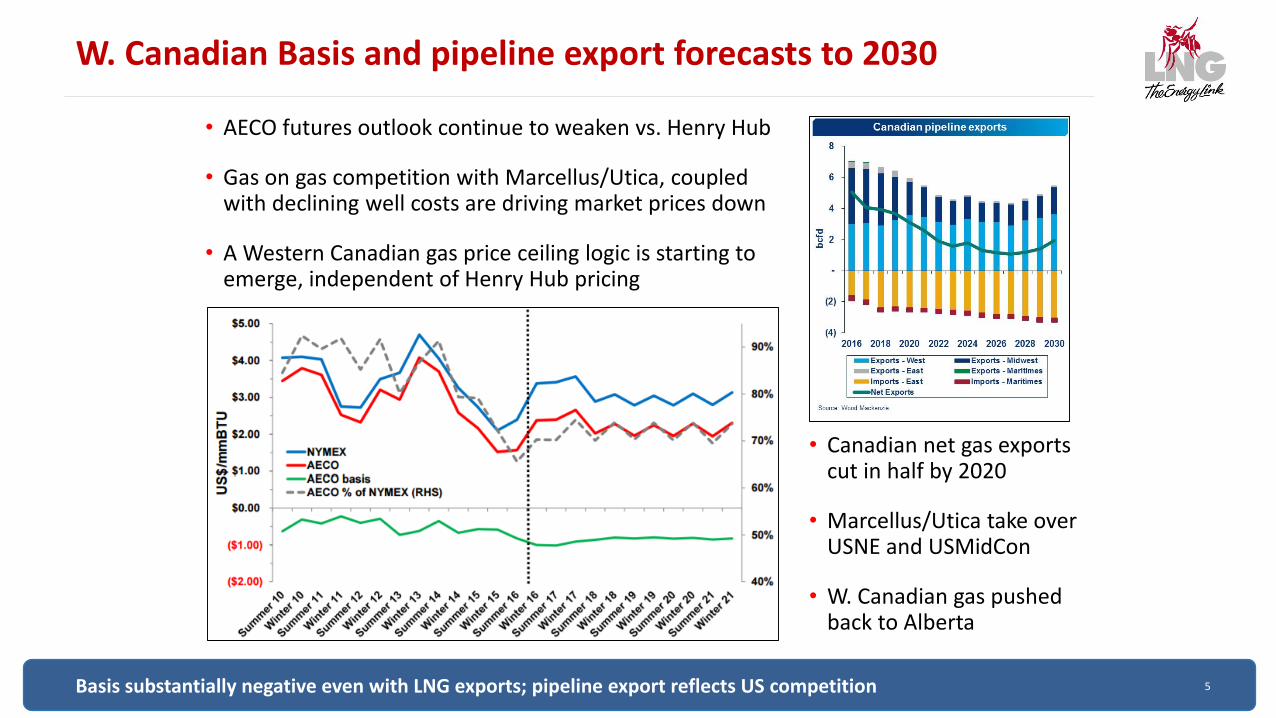

Basis substantially negative even with LNG exports; pipeline export reflects US competition

• Canadian net gas exports cut in half by 2020

• Marcellus/Utica take over USNE and USMidCon

• W. Canadian gas pushed back to Alberta

• AECO futures outlook continue to weaken vs. Henry Hub

• Gas on gas competition with Marcellus/Utica, coupled with declining well costs are driving market prices down

• A Western Canadian gas price ceiling logic is starting to emerge, independent of Henry Hub pricing

66

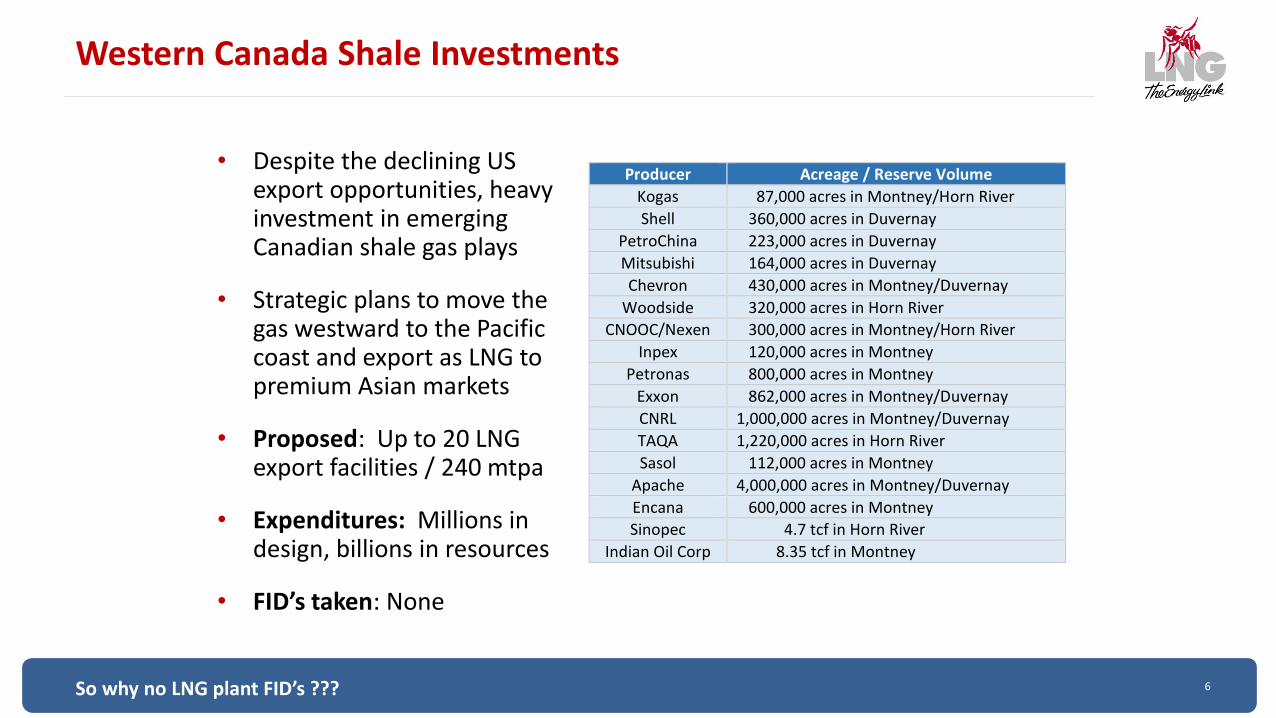

Western Canada Shale Investments

• Despite the declining US export opportunities, heavy investment in emerging Canadian shale gas plays

• Strategic plans to move the gas westward to the Pacific coast and export as LNG to premium Asian markets

• Proposed: Up to 20 LNG export facilities / 240 mtpa

• Expenditures: Millions in design, billions in resources

• FID’s taken: None

So why no LNG plant FID’s ???

Producer Acreage / Reserve Volume

Kogas 87,000 acres in Montney/Horn River

Shell 360,000 acres in Duvernay

PetroChina 223,000 acres in Duvernay

Mitsubishi 164,000 acres in Duvernay

Chevron 430,000 acres in Montney/Duvernay

Woodside 320,000 acres in Horn River

CNOOC/Nexen 300,000 acres in Montney/Horn River

Inpex 120,000 acres in Montney

Petronas 800,000 acres in Montney

Exxon 862,000 acres in Montney/Duvernay

CNRL 1,000,000 acres in Montney/Duvernay

TAQA 1,220,000 acres in Horn River

Sasol 112,000 acres in Montney

Apache 4,000,000 acres in Montney/Duvernay

Encana 600,000 acres in Montney

Sinopec 4.7 tcf in Horn River

Indian Oil Corp 8.35 tcf in Montney

77

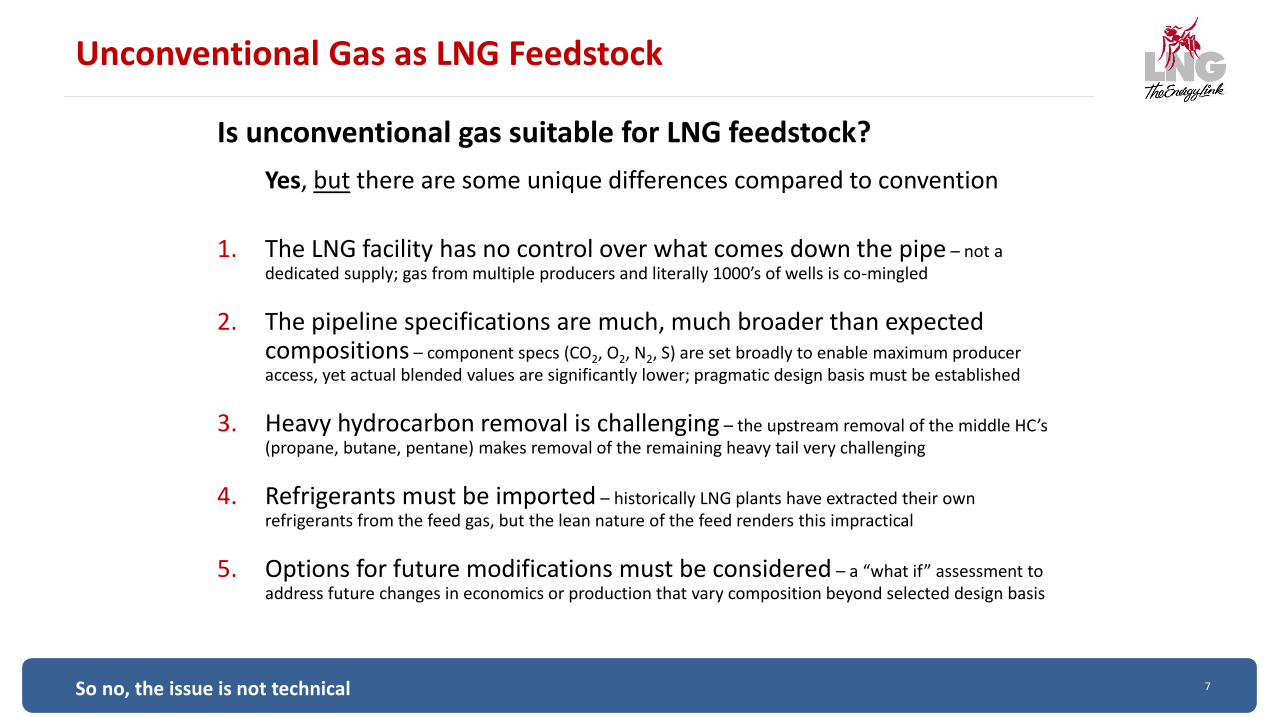

Unconventional Gas as LNG Feedstock

Is unconventional gas suitable for LNG feedstock?

Yes, but there are some unique differences compared to convention

1. The LNG facility has no control over what comes down the pipe – not a dedicated supply; gas from multiple producers and literally 1000’s of wells is co-mingled

2. The pipeline specifications are much, much broader than expected compositions – component specs (CO2, O2, N2, S) are set broadly to enable maximum producer access, yet actual blended values are significantly lower; pragmatic design basis must be established

3. Heavy hydrocarbon removal is challenging – the upstream removal of the middle HC’s (propane, butane, pentane) makes removal of the remaining heavy tail very challenging

4. Refrigerants must be imported – historically LNG plants have extracted their own refrigerants from the feed gas, but the lean nature of the feed renders this impractical

5. Options for future modifications must be considered – a “what if” assessment to address future changes in economics or production that vary composition beyond selected design basis

• Challenge 2 First Nations, Community & Special Interest Concerns – effective and collaborative consultation is vital

• Challenge 3 Project Cost Concerns – remote sites, challenging terrain, limited regional infrastructure, marine access, logistics for large construction workforces and materials delivery, limited craft labor pool, climatic challenges (rain, fog, wet snow), labor camps and temporary facilities, provincial taxes

Regional & environmental concerns may be overcome for some projects, yet cost issues will remain

1010

Canadian Exports – The Case for the East

Intended as a Complementary Solution to Canadian West Coast opportunities

Major Advantages:

• Regulatory Climate

• Regional Community Support

• First Nations Support

• Labour Market

• Site Access

• Regional Infrastructure

• Plant & Marine Siting

• Seismic Zones

• Pipeline Route

• Regional Synergy

• Investment Capital & Cash Flow

1111

Canadian Exports – The Case for the East

Nova Scotia shipping distances to Europe, Eastern SA and Western India < BC or USGC ; only E. Asia significantly longer

Challenges:

• Gas Supply – while the gas can travel west or east, the existing 14,000 km of TransCanada

mainlines will need to be extended by an additional 1600 km to reach the East Coast

• Pipeline Transport Costs – the Canadian NEB recently approved reduced TC mainline tolling

rates, and increased usage can yield even lower costs

• Momentum – companies who invested literally billions into the problematic west coast solution

will need to convince increasingly skeptical management to change direction 180 degrees

• USGC Competition – the US is emerging as a low cost provider; Canadian projects must deliver

a “cost stack” (i.e. gas + transport + capex + opex + equity + financing) at or below USGC rates

• Onward Shipping Distances – shipping to east / southeast Asia is at a greater distance than

from the West Coast. Conversely, shipping to Europe, E. South America and western parts of Asia are shorter. Cross-basis swaps can potentially ease the impact. Interestingly, Eastern Canada shipping distances to E. South America are also shorter than those from the USGC

Overall: Compelling advantages to “Going East” at lower delivered cost

1212

Canadian East Coast: The Bear Head LNG Project

Often considered the world’s “Second Best LNG Plant Site”

The proposed 8-12 mtpa Bear Head LNG project at Port Tupper, Cape Breton Island, Richmond County, Nova Scotia demonstrates many of the advantages of “Going East”:

• Located on a heavy industrial estate

• 327 acres can accommodate up to 6 x 2 mtpa mid-scale trains

• Initially planned as import terminal

• Site clearing & grading, roads, drainage, fencing, LNG tank foundations

Bear Head LNG Site

Oil TerminalPaper Mill

Power Plant Town of Port Tupper

1313

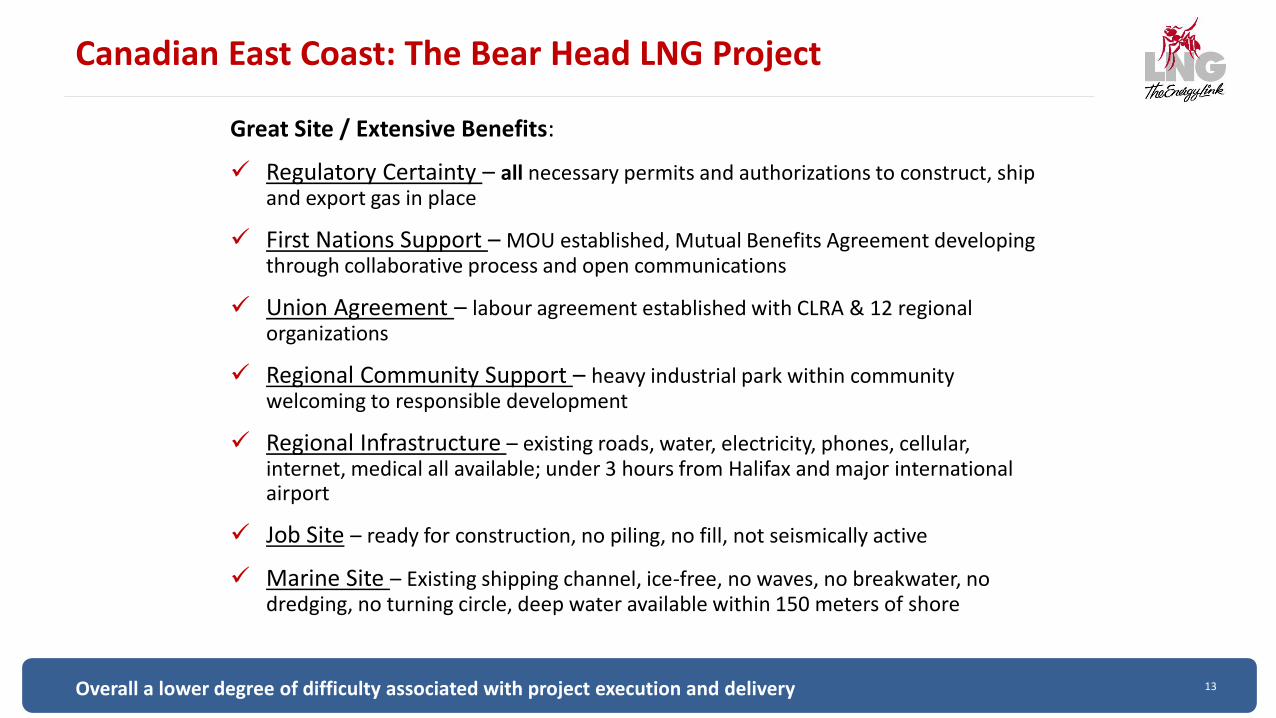

Canadian East Coast: The Bear Head LNG Project

Overall a lower degree of difficulty associated with project execution and delivery

Great Site / Extensive Benefits:

Regulatory Certainty – all necessary permits and authorizations to construct, ship and export gas in place

First Nations Support – MOU established, Mutual Benefits Agreement developing through collaborative process and open communications

Union Agreement – labour agreement established with CLRA & 12 regional organizations

Regional Community Support – heavy industrial park within community welcoming to responsible development

Regional Infrastructure – existing roads, water, electricity, phones, cellular, internet, medical all available; under 3 hours from Halifax and major international airport

Job Site – ready for construction, no piling, no fill, not seismically active

Marine Site – Existing shipping channel, ice-free, no waves, no breakwater, no dredging, no turning circle, deep water available within 150 meters of shore

1414

Canadian East Coast: The Bear Head LNG Project

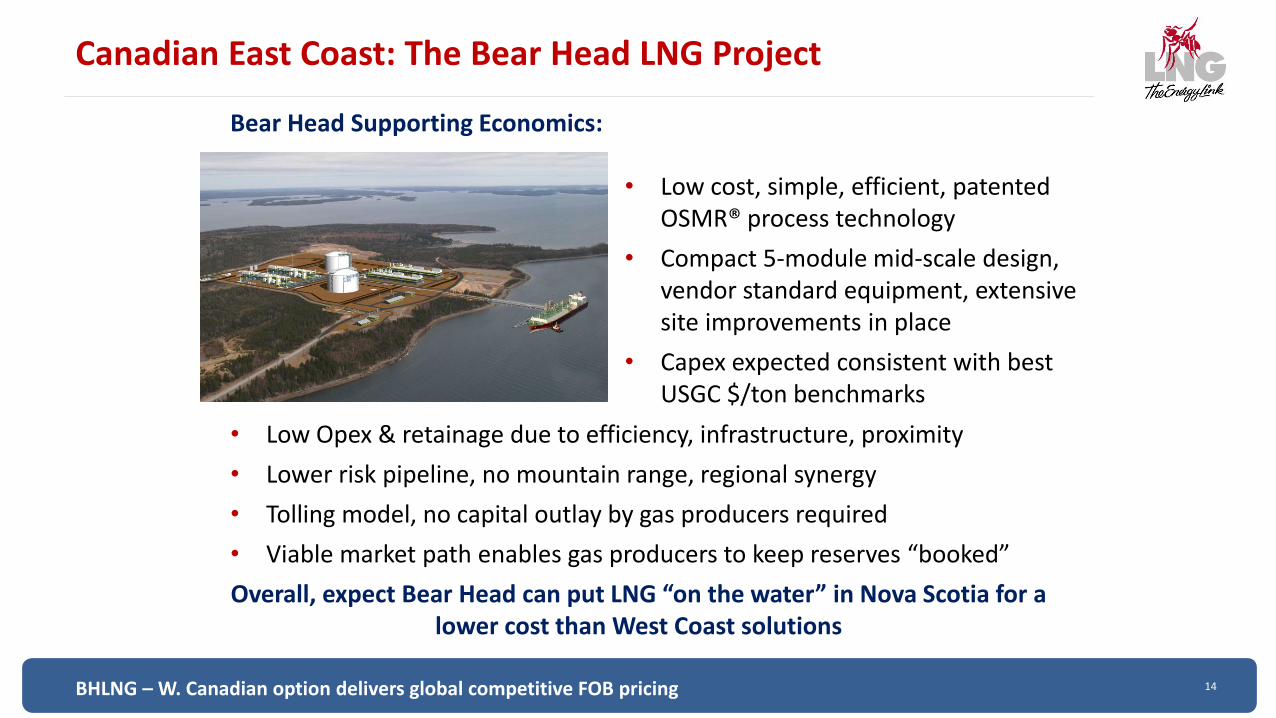

BHLNG – W. Canadian option delivers global competitive FOB pricing

Bear Head Supporting Economics:

• Low Opex & retainage due to efficiency, infrastructure, proximity

• Lower risk pipeline, no mountain range, regional synergy

• Tolling model, no capital outlay by gas producers required

• Viable market path enables gas producers to keep reserves “booked”

Overall, expect Bear Head can put LNG “on the water” in Nova Scotia for a lower cost than West Coast solutions

• Low cost, simple, efficient, patented OSMR® process technology

• Compact 5-module mid-scale design, vendor standard equipment, extensive site improvements in place

• Capex expected consistent with best USGC $/ton benchmarks

1515

Conclusion

Despite extensive efforts, millions in design works and billions in resource acquisition, a West Coast export solution for increasingly stranded Western

Canada natural gas has proven elusive.

By following the 1860’s advice of Horace Greely and looking in a fresh direction, Western Canada gas producers can now contemplate a viable

complementary monetization solution – this time by looking East.