112

(A free translation of the original in Portuguese) Listed Company CNPJ: 89.850.341/0001-60 NIRE: 23300021118-CE Management Report 2016

(A free translation of the original in Portuguese)

Listed Company

CNPJ: 89.850.341/0001-60

NIRE: 23300021118-CE

Management Report 2016

2 Management Report 2016

BOARD OF DIRECTORS

Alexandre Grendene Bartelle

Chairman of the Board of Directors

Pedro Grendene Bartelle Vice-Chairman of the Board of Directors

Members of the Board of Directors

Maílson Ferreira da Nóbrega Oswaldo de Assis Filho

Renato Ochman Walter Janssen Neto

-----------------------------------------------------------------------------------

STATUTORY AUDIT BOARD

João Carlos Sfreddo

Chair of the Audit Board

Members of the Audit Board Eduardo Cozza Magrisso Herculano Aníbal Alves

-----------------------------------------------------------------------------------

EXECUTIVE BOARD

Rudimar Dall’ Onder Chief Executive Officer

Gelson Luis Rostirolla

Deputy Chief Executive Officer

Francisco Olinto Velo Schmitt Chief Finance Officer and Investor Relations Officer

-----------------------------------------------------------------------------------

Luiz Carlos Schneider

Accountant – CRC/CE – SEC – 70.520/O-5

3 Management Report 2016

MANAGEMENT REPORT 2016

Dear Stockholders:

In accordance with the provisions of law and the by-laws, the management of Grendene S.A. presents to you,

below, the Report of Management and the Consolidated Financial Statements prepared in accordance with

International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board

(IASB) and also based on accounting practices adopted in Brazil and the rules of the Brazilian Securities

Commission (CVM). The Company has adopted all the rules, revisions of rules and interpretations issued by IASB

which are in effect for financial statements at December 31, 2016.

4 Management Report 2016

CONTENTS

I. Message from Management 05

II. Main consolidated indicators (IFRS) 08

III. Market and macroeconomic conditions 09

IV. Economic and financial performance 10

1. Gross sales revenue 10

2. Net sales revenue 12

3. Cost of goods sold 12

4. Gross profit 13

5. Operational expenses (SG&A) 14

1. Selling expenses 14

1. Advertising expenses 14

2. General and administrative expenses (G&A) 15

6. EBIT and EBITDA 15

1. EBIT 15

2. EBITDA 16

7. Net financial revenue (expenses) 17

8. Net profit for the year 18

9. Cash generation 18

10. Net cash 18

11. Capital expenditure (Capex) 19

12. Independent auditors – CVM Instruction 381/03 20

1. Statement of justification in relation to independent auditors 20

V. Capital markets and corporate governance 21

1. Capital markets 21

2. Dividends 23

1. Dividend policy 23

2. Dividends and Interest on Equity declared 23

3. Corporate governance best practices 26

1. Commitment clause 26

2. Statement by the Executive board 26

3. Awards and recognition 27

VI. Social and environmental responsibility 29

VII. Human resources 31

VIII. Statement of value added 32

IX. Final considerations and outlook 33

X. Opinion of the Audit board Appendix I

XI. Individual and consolidated financial statements Appendix II

5 Management Report 2016

I. Message from management

Grendene reports net profit for 2016 of R$ 634 million, representing a return of 25.2% on the company’s Stockholder’s equity at the beginning of the year. Of this profit, the company has proposed a distribution of dividends and Interest on Equity totalling R$ 351.4 million, reinvesting the rest in the Company. The book value of our share thus increased in the year from R$ 8.70 to R$ 9.72. In the period since its IPO in 2004, the Company has re-invested R$ 2.2 billion which has been absorbed into its Stockholder’s equity, and increased its annual profit by R$ 400 million. In this period the Company has paid a total of dividends and Interest on Equity (including the amounts proposed for the 2016 business year) of R$ 2.4 billion.

The results have been good, but the difficulties have increased significantly, especially as from 2013 with the continuous fall in consumption of footwear in Brazil. In 2016, our fears were confirmed. It was a year of continuous economic deterioration, and great political instability. To this somber scenario in the domestic market was added an international situation that was a source of concern, with economic slowdown in numerous markets, and economies increasingly having recourse to protectionist measures, which have the effect of reducing levels of international trade.

However, it is part of our culture to face the facts head-on, and confront the challenges. We have built a good result, increasing profits, expanding margins, maintaining the return on our investments, and paying increasing dividends to stockholders. We have done this without omitting to invest in our brands, and invest in renewal of our product portfolios, while also strengthening our relationship with the channels of distribution: in other words, without omitting to strengthen our position for the future.

As a preliminary note: the results for 2015 that are the basis for our comparison this year contained adjustments. In that year, as widely reported, we made a provision for loss of the total of our investments in the furniture sector, with an accounting effect of R$ 52 million. This loss had no effect on cash flow in the year, nor in the future, and is non-recurrent.

For maximum clarity, this table shows the adjustments made in 2015:

Account lines

Consolidated result

(formal accounting) Adjustments Adjusted result

2015 % of net revenue 2015 % of net revenue

Gross profit 1,067,883 48.5% (1,887) 1,065,996 48.4%

Operational expenses (667,151) (30.3%) 55,864 (611,287) (27.8%)

EBIT 400,732 18.2% 53,977 454,709 20.7%

Net profit 551,223 25.0% 51,809 603,032 27.4%

Depreciation and amortization 53,652 2.4% (1,397) 52,255 2.4%

EBITDA 454,384 20.6% 52,580 506,964 23.0%

Our net profit in 2016 gave us a net margin of 31%, and was 5.2% higher than the adjusted net profit for 2015 (also, 15.1% higher than the unadjusted accounting profit for 2015); our 2016 adjusted net margin was 3.6 percentage points (pp) higher than in 2015 (and 6.0 pp higher than the margin based on the unadjusted accounting).

Operational cash flow in 2016 was R$ 566.5 million; and the dividends proposed represent a payout (sum of dividends and Interest on Equity, divided by accounting profit) of 53.1%, and dividend yield of 6.3%. We achieved these results in spite of falls in volume of pairs sold of 8.1% in the domestic market, and 13.0% in exports – partly compensated by a 4.1% increase in unit prices – resulting in net revenue 7.1% lower year-on-year.

On a longer view, our management has been generating value for stockholders, providing a significant return on equity, as this table shows (all amounts for profit in the table are the original accounting, with no adjustment):

6 Management Report 2016

R$ ‘000

Year

Initial Stockholders’

equity1

Net profit Dividendos Reinvestiment Return on Equity Final

Stockholders’ equity

1

2004 692,726 204,865 64,152 140,713 29.6% 733,566

2005 733,566 200,116 81,181 118,935 27.3% 847,373

2006 847,373 257,343 128,261 129,082 30.4% 998,510

2007 998,510 260,508 119,724 140,784 26.1% 1,132,718

2008 1,132,718 239,367 109,000 130,367 21.1% 1,274,080

2009 1,274,080 272,211 110,000 162,211 21.4% 1,430,569

2010 1,430,569 312,399 121,738 190,661 21.8% 1,624,542

2011 1,624,542 305,446 219,526 85,920 18.8% 1,713,743

2012 1,713,743 429,003 293,503 135,500 25.0% 1,848,309

2013 1,848,309 433,540 300,057 133,483 23.5% 1,957,295

2014 1,957,295 490,244 220,814 269,430 25.0% 2,232,649

2015 2,232,649 551,223 275,925 275,298 24.7% 2,520,866

2016 2,520,866 634,492 351,383 283,109 25.2% 2,792,976

Accumulated 4,590,757 2,395,264 2,195,493 1,241.5%

1) End-of-year stockholders’ equity, i.e. excluding dividends, etc. proposed for subsequent year.

In this 12-year period the book value per share grew from R$ 2.44 to R$ 9.72, with a compound average growth rate (CAGR) of 12.2% p.a.

Grendene’s share price was R$ 10.33 at the beginning of the period, and R$ 17.58 at the end of the period (adjusted for number of shares). With this variation and taking into account reinvestment of dividends paid, the share, GRND3, presented an average annual total return to stockholders of 10.8% p.a., less than the gain that would be indicated by the formal accounting results, but even so, more than the average total return for the Bovespa index (also based on reinvestment of the dividends), of 7.2% p.a.

In terms of brand building, we made progress with the Clube Melissa project, exceeding the initial estimate, made in 2012, of 200 stores by 2017: at the end of the year Clube Melissa had 241 franchised stores, an increase of 33 in a year of strong retraction in retailing. Also, we strengthened our traditional brands - Rider, Cartago, Ipanema, Zaxy, Grendha and Grendene Kids – with enumerable actions in marketing and communication.

Important progress was also made in our strategy of differentiation of products by design and innovation. Melissa continues its strategy based on three pillars: fashion, art and design – and also partnerships with renowned design names such as Karl Lagerfeld, Zaha Hadid, Gaetano Pesce and J. Maskrey. We launched products in partnership with designers including Salinas, Jeremy Scott, Vitorino Campos, Cartel 011, Fábula CSC, Cambridge Satchel Co, and Jason Wu.

Ipanema sandals are celebrating their 15th birthday, and to tell a little bit of this story, Casa Ipanema presented a

sensory, collaborative telling of the story Ipanema – 15 Anos de Bossa, remembering highlights and milestones from the brand’s history. This year it launched partnerships with leading names including Clau Cicala, Animale, Dress to and Cia Marítima. The Ipanema brand was present at Sao Paulo Fashion Week through its partnership with the brands A. Brand and Lenny Niemeyer.

The Rider brand celebrated its 30th birthday by bringing back its most important iconic product, the first vamp of

1986, with design identical to the original, and important technical alterations – with three special editions signed by Sneakersbr.

These efforts, among others, have ensured that the brands grow in the Grendene’s principal markets, and also as a percentage of Grendene’s total business, with recognition by awards in the market.

In our assessment, once again we have set the country’s economic crisis aside and achieved results that have been possible only due to the discipline and application of our management team – which has, on average, more than 20 years’ experience with the Company, with very low management-level turnover, and has provided continuous improvement in our processes – and also due to the great commitment of our 20,000 employees.

In our 46 years of existence we have won a significant leadership position in the footwear sector, and we continue to believe in the strengthening of our brands, our growth in the domestic and international markets, with confidence for the future and in our potential. The continuous and persistent gain in market share that we have

7 Management Report 2016

achieved, with robust return on equity for stockholders, provides an indication of this leadership, and of the competitive advantages that we have built.

From our calculations and assessment, we believe we achieved a small gain in market share by volume in some of our target markets, and we also improved net margin, as we had determined that we would. For the coming years, we aim to sustain this level of margins, consolidating the trend established and if possible improve it. The quality of our products, the strength of our brands and recognition by retailers and final clients, and our operational efficiency, serve as the basis for this expectation.

To achieve this regularity of results, we highlight our skill in building strong brands that have a privileged relationship with clients, and developing solid relationships with the distribution channels through a long-term process with cumulative effects. In the last 12 years, among many other efforts, we have invested approximately R$ 1.6 billion in advertising, as a means of consolidating construction of value, and in coming years we will seek this approximation with Grendene’s final clients with even greater vigor. We believe that understanding of our client’s needs is a fundamental factor for the success of our business model.

All these actions are coherent with our Values, which highlight precisely the aspects for which we have received reiterated public recognition: profitability, competitiveness, innovation, agility, ethics.

Importantly, in these 46 years we have not lacked the decisive support and trust of suppliers, clients, partners, stockholders and, especially, thousands of employees dedicated and committed to our Business Vision and Values.

To all of these, we extend our sincere thanks, and with them we share our success.

The management

8 Management Report 2016

II. Main consolidated indicators (IFRS)

R$ mn 2011 2012 2013 20141 2015

1 2016

Change 16/15

CAGR2

16/11

Gross revenue from sales 1,831.6 2,324.5 2,711.4 2,719.4 2,630.0 2,483.0 (5.6%) 6.3%

Domestic market 1,489.9 1,845.4 2,146.9 2,077.7 1,899.2 1,870.3 (1.5%) 4.7%

Exports 341.7 479.1 564.5 641.7 730.8 612.7 (16.2%) 12.4%

Net revenue 1,481.1 1,882.3 2,187.3 2,232.4 2,201.1 2,045.1 (7.1%) 6.7%

Cost of goods sold (840.5) (1,000.2) (1,193.6) (1,206.8) (1,135.1) (1,048.6) (7.6%) 4.5%

Gross profit 640.6 882.1 993.7 1,025.6 1,066.0 996.5 (6.5%) 9.2%

Operational expenses (453.3) (519.3) (594.5) (625.7) (611.3) (596.9) (2.3%) 5.7%

EBIT 187.3 362.8 399.2 399.9 454.7 399.6 (12.1%) 16.4%

EBITDA 216.2 394.5 435.9 447.3 507.0 457.5 (9.8%) 16.2%

Net financial revenue (Exp.) 153.0 132.5 103.6 135.1 184.3 268.5 45.7% 11.9%

Net Profit 305.4 429.0 433.5 493.7 603.0 634.5 5.2% 15.7%

R$ 2011 2012 2013 2014 2015 2016 Change

16/15 CAGR

2

16/11

Average price 12.20 12.56 12.54 13.27 14.58 15.18 4.1% 4.5%

Domestic market 13.85 13.21 12.96 13.60 14.12 15.13 7.2% 1.8%

Exports 8.04 10.56 11.17 12.29 15.91 15.33 (3.6%) 13.8%

Exports (US$) 4.80 5.40 5.18 5.22 4.78 4.39 (8.2%) (1.8%)

R$ 2011 2012 2013 2014 2015 2016 Change

16/15 CAGR

2

16/11

Basic profit per share 1.0157 1.4266 1.4421 1.6328 1.8342 2.1101 15.0% 15.7%

Diluted profit per share 1.0123 1.4195 1.4367 1.6293 1.8305 2.1058 15.0% 15.8%

Dividend per share 0.7300 0.9760 0.9985 0.7351 0.9177 1.1686 27.3% 9.9%

Million of pairs 2011 2012 2013 2014 2015 2016 Change

16/15 CAGR

2

16/11

Volumes 150.1 185.0 216.2 204.9 180.4 163.6 (9.3%) 1.7%

Domestic market 107.6 139.7 165.7 152.7 134.5 123.6 (8.1%) 2.8%

Exports 42.5 45.3 50.5 52.2 45.9 40.0 (13.0%) (1.2%)

Margin, % 2011 2012 2013 20141 2015

1 2016

Change p.p.

3 16/15

Change p.p.

3 16/11

Gross 43.3% 46.9% 45.4% 45.9% 48.4% 48.7% 0.3 p.p. 5.4 p.p.

EBIT 12.6% 19.3% 18.3% 17.9% 20.7% 19.5% (1.2 p.p.) 6.9 p.p.

EBITDA 14.6% 21.0% 19.9% 20.0% 23.0% 22.4% (0.6 p.p.) 7.8 p.p.

Net 20.6% 22.8% 19.8% 22.1% 27.4% 31.0% 3.6 p.p. 10.4 p.p.

R$ 2011 2012 2013 2014 2015 2016 Change

16/15 CAGR

2

16/11

US dollar at the end of the year 1.8758 2.0435 2.3426 2.6562 3.9048 3.2591 (16.5%) 11.7%

US dollar – average 1.6750 1.9546 2.1576 2.3536 3.3315 3.4901 4.8% 15.8%

Note:

1) Adjusted numbers, excluding the non-recurring effect – A3NP.

2) CAGR: Compound annual growth rate.

3) p.p.: percentage points.

9 Management Report 2016

III. Market and macroeconomic conditions

The economic context developed in 2016 not much differently from 2015: very adversely. The bill for the fiscal misadjustments finally arrived and had to be paid: consumption was strongly hit by unemployment, fall in personal income, and even delays in payment of local government workers in some states. With interest rates continuing to be high, high unemployment – some 13 million Brazilians without jobs – will continue to have a negative effect on consumption in 2017. The high leverage of Brazilian individuals, families and companies – with record applications by companies for judicial recovery, and default by individuals – indicate only a slow, timid recovery in 2017.

In 2016 we faced our third consecutive year of decline in the consumption and output of footwear: a return to the levels of 2011. Even so, in 2016 we delivered a slightly higher volume of pairs than in 2011 (164 million pairs in 2016, vs. 150 million pairs in 2011), but – in an indication of how much we have progressed in efficiency of our operations – we made more than double the profit (R$ 634mn this year, vs. R$ 305mn in 2011).

Unemployment has affected propensity to consume since 2015; we expect it now to stabilize in the first half of 2017, and the beginnings of a reaction in the second half of the year. We can, indeed, report that early 2017 is already better than early 2016, in terms of demand in the market – attenuating our expectations for this year.

We have no doubt that 2017 will once again be a difficult year. In our assessment it will be some time before we see an effect on consumption from: reduction of interest rates and inflation; reduction of individuals’ and companies’ indebtedness; and the government’s continuing fiscal adjustment. We believe, indeed, that the path of the public debt continues to be a fundamental uncertainty – as also does the reform of the social security system. In our view, any hesitation on these subjects could abort the timid recovery in the economy expected for this year.

On the international scene, we highlight an escalation of protectionism, which we believe might be exacerbated by the positioning of the new US government.

We believe that Brazil has probably now passed the worst economic moment of what has been, for it, a devastating crisis, and companies like Grendene, which knew how to strengthen themselves during this period, are preparing to reap the results of a healthier economy: if these results do not appear this year, they will appear next year. This is our expectation, and we are confident.

Brazilian Footwear – Production and apparent consumption

Brasil (millions of pairs) 2011 2012 2013 2014 2015 2016 Change,

16/15

CAGR

16/11

Production 838 997 1.036 998 944 868* (8.1%) 0.7%

Imports 34 36 39 37 33 23 (30.9%) (7.5%)

Exports 113 113 123 130 124 126 1.5% 2.2%

Apparent consumption 759 920 952 905 853 765* (10.3%) 0.2%

Consumption per capita (pairs) 3.8 4.6 4.7 4.5 4.2 3.7* (11.9%) (0.5%)

Source: IBGE / Secex / Abicalçados / (*) Estimated by Grendene.

Some figures are re-presented to include effects of some updating / revision in the date sources used.

Grendene

Million of pairs 2011 2012 2013 2014 2015 2016 Change,

16/15

CAGR

16/11

Volumes 150.1 185.0 216.2 204.9 180.4 163.6 (9.3%) 1.7%

Share volume – Production 17.9% 18.6% 20.9% 20.5% 19.1% 18.8% (0.3 p.p.) (0.9 p.p.)

Domestic market 107.6 139.7 165.7 152.7 134.5 123.6 (8.1%) 2.8%

Share volume – Domestic market 14.2% 15.2% 17.4% 16.9% 15.8% 16.2% 0.4 p.p. 2.0 p.p.

Exports 42.5 45.3 50.5 52.2 45.9 40.0 (13.0%) (1.2%)

Share volume – exports 37.6% 40.0% 41.1% 40.3% 37.0% 31.7% (5.3 p.p.) (5.9 p.p.)

Source: Grendene S.A.

10 Management Report 2016

IV. Economic and financial performance

1. Gross sales revenue

The 5.7% reduction in gross revenue from 2015 to 2016 brings the CAGR down to 5.8% p.a. in 2008–16 – from 7.6% in 2008–15. This is below the lower limit of our guidance forecast rate of between 8% and 12%.

These tables show the last 6 years:

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Consolidated gross revenue 1,831.6 2,324.5 2,711.4 2,720.3 2,631.8 2,483.0 (5.7%) 6.3%

Domestic market 1,489.9 1,845.4 2,146.9 2,077.7 1,899.8 1,870.3 (1.6%) 4.7%

Exports 341.7 479.1 564.5 642.6 732.0 612.7 (16.3%) 12.4%

Exports, US$ 204.0 245.1 261.6 272.6 219.3 175.5 (20.0%) (3.0%)

Million of pairs 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Volumes 150.1 185.0 216.2 204.9 180.4 163.6 (9.3%) 1.7%

Domestic market 107.6 139.7 165.7 152.7 134.5 123.6 (8.1%) 2.8%

Exports 42.5 45.3 50.5 52.2 45.9 40.0 (13.0%) (1.2%)

R$ 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Average price 12.20 12.56 12.54 13.27 14.58 15.18 4.1% 4.5%

Domestic market 13.85 13.21 12.96 13.60 14.12 15.13 7.2% 1.8%

Exports 8.04 10.56 11.17 12.29 15.91 15.33 (3.6%) 13.8%

Exports, US$ 4.80 5.40 5.18 5.22 4.78 4.39 (8.2%) (1.8%)

1,490 1,845 2,147 2,078 1,900 1,870

342

479 565 643 732 613 1,832

2,325 2,711 2,720 2,632 2,483

2011 2012 2013 2014 2015 2016

R$

mil

lio

n

Gross sales revenue

Domestic market Exports

81% 79% 79% 76% 72% 75%

19% 21% 21% 24% 28% 25%

2011 2012 2013 2014 2015 2016

%

Domestic sales and exports as % of gross sales revenue

Domestic market Exports

11 Management Report 2016

According to figures from the Foreign Trade Ministry, the Central Bank Foreign Trade Service (Secex), and the Brazilian Footwear Manufacturers’ Association (Abicalçados), Brazilian footwear export volume (number of pairs) in 2016 was up 1.2% from 2015, export revenues in dollars were 3.9%, and average price in US$ were 2.7% higher.

Our share in total Brazilian footwear exports in 2016 was 31.8% by volume, and 17.6% by value in US$. By volume, we maintained the leadership in Brazilian footwear exports, for the 14

th year running.

107 140

166 153 134 124

43

45 51 52

46 40

150

185 216 205

180 164

2011 2012 2013 2014 2015 2016

Mil

lio

n o

f p

air

s

Volume of pairs sold

Domestic market Exports

72% 76% 77% 75% 75% 76%

28% 24% 23% 25% 25% 24%

2011 2012 2013 2014 2015 2016

%

Domestic and exports sales as % of total number of pairs sold

Domestic market Exports

13.85 13.21 12.96 13.60 14.12 15.13

8.04

10.56 11.17 12.29

15.91 15.33

12.20 12.56 12.54 13.27 14.58 15.18

2011 2012 2013 2014 2015 2016

R$

Average price

Domestic market Exports Total

12 Management Report 2016

2. Net sales revenue

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Gross sales revenue 1,831.6 2,324.5 2,711.4 2,720.3 2,631.8 2,483.0 (5.7%) 6.3%

Domestic market 1,489.9 1,845.4 2,146.9 2,077.7 1,899.8 1,870.3 (1.6%) 4.7%

Exports 341.7 479.1 564.5 642.6 732.0 612.7 (16.3%) 12.4%

Deduction from sales (350.5) (442.2) (524.1) (487.0) (429.0) (437.9) 2.1% 4.6%

Returns and taxes on sales (255.3) (328.6) (393.3) (383.0) (336.4) (346.7) 3.1% 6.3%

Discounts given to clients (95.2) (113.6) (130.8) (104.0) (92.6) (91.2) (1.6%) (0.9%)

Net sales revenue 1,481.1 1,882.3 2,187.3 2,233.3 2,202.8 2,045.1 (7.2%) 6.7%

3. Cost of goods sold

In the last five years, with all the FX volatility, increases in the minimum wage, and inflationary pressures, in Brazil our unit cost grew at the rate of 2.7% p.a., much lower than the inflation rates in the period. An element of this was the benefit of the ‘de-burdening of payroll’ put in place by the federal government starting in 2011, partially reversed in December 2015. Over the whole of this period (as a whole), total COGS grew by less than the growth in net revenue (which grew 6.7% p.a.)

Cost discipline has played a fundamental role in our results.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Cost of goods sold 840.5 1,000.2 1,193.6 1,207.4 1,134.9 1,048.6 (7.6%) 4.5%

R$ per pair 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Cost of goods sold per pair 5.60 5.40 5.52 5.89 6.29 6.41 1.9% 2.7%

1,481

1,882

2,187 2,233 2,203 2,045

2011 2012 2013 2014 2015 2016

R$

mil

lio

n

Net sales revenue

841

1,000

1,194 1,207 1,135

1,049

2011 2012 2013 2014 2015 2016

R$

mil

lio

n

COGS

13 Management Report 2016

4. Gross Profit

In spite of the reduction in 2016, our gross profit has expanded at the rate of 9.2% p.a. over the last five years.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Gross profit (Formal accounting) 640.6 882.1 993.7 1,025.9 1,067.9 996.5 (6.7%) 9.2%

Gross margin, % 43.3% 46.9% 45.4% 45.9% 48.5% 48.7% 0.2 p.p. 5.4 p.p.

(*) I.E. excluding the non-recurring effect of A3NP.

5.60 5.40 5.52 5.89

6.29 6.41

2011 2012 2013 2014 2015 2016

R$

COGS per pair

641 882

994 1,026 1,066 997

43.3% 46.9% 45.4% 45.9% 48.4% 48.7%

2011 2012 2013 2014* 2015* 2016

Gro

ss

ma

rgin

R

$ m

illi

on

Adjusted gross profit Adjusted gross margin, %

14 Management Report 2016

5. Operational expenses (SG&A)

5.1. Selling expenses Grendene’s selling expenses are predominantly in the variables freight, licensings, commissions, advertising and marketing, and over the period remained at approximately 24% of net revenue.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Selling expenses 394.5 451.0 521.2 543.7 523.7 490.6 (6.3%) 4.5%

% of net sales revenue 26.6% 24.0% 23.8% 24.3% 23.8% 24.0% 0.2 p.p. (2.6 p.p.)

(*) I.E. excluding the non-recurring effect of A3NP.

5.1.1 Advertising expenses The expense on advertising was lower than in 2015, at 6.0% of net revenue – a lower percentage than we normally invest. On the other hand, we carried out other strategic brand positioning activities and projects which, although they are not classified in the accounting as advertising expenses, are considered in our internal analysis to be marketing efforts. These activities are, principally, events held in the Melissa Galerias in São Paulo, New York and London, and regional events which, in 2016, accounted for total expenditure of R$ 9.7 mn (R$ 6.7mn in 2015). This type of expenditure was made in previous years, but not in significant amounts.

If we add these expenses (all classified as selling expenses in 2015 and 2016) to advertising expenses, the percentage of net revenue increases from 6.8% to 7.1% and 6.0% to 6.5% respectively, which we believe better represents our brand building efforts.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Advertising expenses 138.7 147.0 163.7 169.2 148.9 122.8 (17.5%) (2.4%)

% of net sales revenue 9.4% 7.8% 7.5% 7.6% 6.8% 6.0% (0.8 p.p.) (3.4 p.p.)

Strategic brand projects - - - - 6.7 9.7 44.3% -

Total 138.7 147.0 163.7 169.2 155.6 132.5 (14.8%) (0.9%)

% of net sales revenue 9.4% 7.8% 7.5% 7.6% 7.1% 6.5% (0.6 p.p) (2.9 p.p.)

395 451 521 538 518 491

26.6% 24.0% 23.8% 24.1% 23.5% 24.0%

2011 2012 2013 2014* 2015* 2016

% o

f ne

t sa

les

reve

nu

e

R$

mil

lio

n

Selling expenses % of net sales revenue

139 147 164 169 156 133

9.4% 7.8% 7.5% 7.6% 7.1%

6.5%

2011 2012 2013 2014 2015 2016

% o

f ne

t sa

les

reve

nu

e

R$ m

illi

on

Advertising expense + Strategic projects % of net sales revenue

15 Management Report 2016

5.2. General and administrative expenses (G&A)

General and administrative expenses were 4.1% lower in 2016 than 2015, and as a percentage of net revenue were 4.8% – higher than the ratio we had aimed for.

However, adjustment to exclude the effects of A3NP in consolidated results – equal to R$ 13.1mn in 2015 – gives adjusted 2015 G&A of R$ 88.6mn, or 4.0% of 2015 net revenue, i.e. in reality these expenses were 10.1% higher in 2016 than in 2015.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

G&A expenses 61.2 70.4 79.0 91.3 101.7 97.5 (4.1%) 9.8%

% of net sales revenue 4.1% 3.7% 3.6% 4.1% 4.6% 4.8% 0.2p.p. 0.7 p.p.

(*) I.E. excluding the non-recurring effect of A3NP.

6. Ebit e Ebitda

6.1. Ebit

EBIT – earnings before interests and taxes. We believe that because we have a high cash position which generates significant financial revenues, the operational profit of our activity is best characterized by Ebit.

Reconciliation: Accounting Ebit / Ebitda * / R$ mn

2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Net profit for the year 305.4 429.0 433.5 490.2 551.2 634.5 15.1% 15.7%

Non-controlling stockholders - 0.9 - (5.0) (11.9) (0.5) (95.5%) (354.8%)

Taxes on profit 34.9 65.4 68.8 39.7 43.8 34.1 (22.0%) (0.4%)

Net financial revenue (expenses) (153.0) (132.5) (103.6) (135.5) (182.4) (268.5) 47.3% 11.9%

Ebit 187.3 362.8 399.2 389.4 400.7 399.6 (0.3%) 16.4%

Depreciation and amortization 28.9 31.7 36.7 47.5 53.7 57.9 7.9% 14.9%

Ebitda 216.2 394.5 435.9 436.9 454.4 457.5 0.7% 16.2%

Ebit margin 12.6% 19.3% 18.3% 17.4% 18.2% 19.5% 1.3 p.p. 6.9 p.p.

Ebitda margin 14.6% 21.0% 19.9% 19.6% 20.6% 22.4% 1.8 p.p. 7.8 p.p.

* Figures for accounting Ebit and Ebitda are stated as per CVM instruction 527 of October 4, 2012.

61 70 79 86 89 98

4.1% 3.7% 3.6% 3.9% 4.0%

4.8%

2011 2012 2013 2014* 2015* 2016

% o

f ne

t sa

les

reve

nu

e

R$

mil

lio

n

G&A expenses % of net sales revenue

16 Management Report 2016

Reconciliation of Ebit / Ebitda

R$ million 2015 2016 Change 16/15

Net profit for the year – Recurrent 603.0 634.5 5.2%

Non-recurring effect (51.8) 0.0 -

Net profit for the year – Accounting 551.2 634.5 15.1%

Non-controlling stockholders (11.9) (0.5) (95.8%)

Taxes on profit 43.8 34.1 (22.1%)

Net financial revenue (expenses) (182.4) (268.5) 47.2%

Ebit – Accounting 400.7 399.6 (0.3%)

Non-recurring item 54.0 8.8 (83.7%)

Ebit – Recurrent 454.7 408.4 (10.2%)

Depreciation and amortization 53.7 57.9 7.8%

Ebitda – Accounting 454.4 457.5 0.7%

Ebitda – Recurrent 507.0 466.3 (8.0%)

Ebit margin – Accounting 18.2% 19.5% 1.3 p.p.

Ebit margin – Recurrent 20.7% 20.0% (0.7 p.p.)

Ebitda margin – Accounting 20.6% 22.4% 1.8 p.p.

Ebitda margin – Recurrent 23.0% 22.8% ( 0.2 p.p.)

(*) I.E. excluding the non-recurring effect of A3NP.

6.2. Ebitda

Our business is low capital-intensive. Depreciation is around 2.5% of net revenue (2.1% in 2014, 2.4% in 2015 and 2.8% in 2016). Grendene regularly invests an amount equivalent to depreciation in any period, to keep its production capacity up to date. It also maintains positive net cash, and has no financial costs that need to be paid with funds from operations. As a result we believe that Ebit is the best indicator for operational analysis by the Company’s management.

187

363 399 400 455 408

12.6%

19.3% 18.3% 17.9%

20.7% 20.0%

2011 2012 2013 2014* 2015* 2016

EB

IT m

arg

in

R$ m

illi

on

Adjusted Ebit Adjusted Ebit margin

454.4 507.0 52.6

Ebitda, 2015

Non-recurring effect

Adjusted Ebitda, 2015

R$ m

illi

on

457.5 466.3 8.8

Ebitda, 2016

Non-recurring effect

Adjusted Ebitda, 2016

R$ m

illi

on

17 Management Report 2016

(*) I.E. excluding the non-recurring effect of A3NP.

7. Net financial revenue (expenses)

Grendene has a solid cash position, and financial revenues are an important part of its net profit. The aim of its foreign exchange transactions is hedging, mainly of receivables from exports. In these transactions Grendene is vendor of dollars, and the aim is that their net result in the long term should be very close to zero. Thus the result of Financial revenue (expenses) is basically influenced by the interest rate (Selic), and the average level of cash held by the Company.

For 2016 Grendene reports Net financial revenues, of R$ 268.5 mn, which is 47.3% more than in 2015, as follows:

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Interest received from clients 2.9 1.9 1.9 1.9 2.9 2.2 (24.2%) (5.4%)

Revenue from cash investments 128.8 93.7 81.9 100.1 168.2 207.7 23.5% 10.0%

Other financial revenues 2.6 3.5 2.2 5.2 4.1 3.3 (20.1%) 5.0%

Subtotal 134.3 99.1 86.0 107.2 175.2 213.2 21.7% 9.7%

Costs of financings (15.0) (9.2) (19.6) (21.8) (20.5) (18.3) (10.3%) 4.0%

Cofins and PIS taxes on Financial revenues - - - - (5.0) (11.0) 119.6% 0.0%

Other financial expenses (4.3) (4.2) (5.2) (5.6) (9.6) (4.9) (48.8%) 2.8%

Subtotal (19.3) (13.4) (24.8) (27.4) (35.1) (34.2) (2.3%) 12.1%

Net financial revenues (expenses) (1) 115.0 85.7 61.2 79.8 140.1 179.0 27.7% 9.3%

Revenue from FX derivatives – BM&FBovespa 3.9 14.8 18.2 16.6 66.3 49.1 (26.0%) 65.6%

Foreign exchange gains 35.5 49.7 40.2 41.9 118.8 69.7 (41.3%) 14.5%

Subtotal 39.4 64.5 58.4 58.5 185.1 118.8 (35.8%) 24.7%

Op. expenses on FX derivatives – BM&FBovespa (5.3) (11.3) (26.2) (24.0) (123.6) (11.6) (90.6%) 16.8%

Expenses of FX variation (38.2) (47.7) (28.5) (33.5) (80.3) (82.4) 2.5% 16.7%

Subtotal (43.5) (59.0) (54.7) (57.5) (203.9) (94.0) (53.9%) 16.7%

Net gain (loss) on FX variations (2) (4.1) 5.5 3.7 1.0 (18.8) 24.8 (232.0%) (243.6%)

Adjustments to present value (APV) 42.1 41.3 38.7 54.7 61.0 64.7 6.1% 9.0%

Financial result – APV (3) 42.1 41.3 38.7 54.7 61.0 64.7 6.1% 9.0%

Net financial revenues (expenses) (1) + (2) + (3) 153.0 132.5 103.6 135.5 182.3 268.5 47.3% 11.9%

In the consolidated financial statements discounts given to clients are classified as deductions from sales.

216

395 436 447 507 466

14.6%

21.0% 19.9% 20.0%

23.0% 22.8%

2011 2012 2013 2014* 2015* 2016

EB

ITD

A m

arg

in

R$

mil

lio

n

Adjusted Ebitda Adjusted Ebitda margin

18 Management Report 2016

8. Net profit for the year

In the last five years adjusted net profit (there was adjustment only in 2014 and 2015 – and none in the other years) grew at CAGR of 15.7% p.a., with increases in all margins: gross margin, operational margin, and net margin.

Net margin in 2016 was 6.0 p.p. better than in 2015 (unadjusted), and 3.6 p.p. better than in 2015 (adjusted).

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Net profit for the year, formal accounting 305.4 429.0 433.5 490.2 551.2 634.5 15.1% 15.7%

Net margin 20.6% 22.8% 19.8% 22.0% 25.0% 31.0% 6.0 p.p. 10.4 p.p.

(*) I.E. excluding the non-recurring effect of A3NP.

9. Cash generation

Net cash generated by operational activities, of R$ 566.6 mn, was used as follows: investments in fixed and intangible assets R$ 71.5 mn; payment of loans R$ 73.9 mn; financial investments R$ 103.3 mn; payment of dividends totalling R$ 313.7 mn; net loss acquiring shares for stock options R$ 4.6 mn; increase in interest in a subsidiary R$ 0.1 mn, resulting in the amount held in current account for very short-term financial investment being R$ 0.6 mn lower. The complete cash flow can be seen in the financial statements.

We generated R$ 2.1 billion, in total, from our operational activities in the last six years, confirming our excellent operational performance.

10. Net cash

The chart below shows the distribution of the cash position (cash, cash equivalents and short and long-term financial investments), loans and financings (short-term and long-term) and net cash:

305 429 434 494

603 634

20,6% 22,8%

19,8% 22,1%

27,4% 31,0%

2011 2012 2013 2014* 2015* 2016

Ne

t ma

rgin

R$

mil

lio

n

Adjusted net profit Net margin

19 Management Report 2016

11. Capex (in fixed and intangible assets)

In 2016, our main investments were in: maintenance of industrial buildings and facilities; replacement of fixed assets; and acquisition of new equipment for modernization of plant and greater efficiency of production.

We are estimating that we will invest between R$ 100 and R$ 110 mn in 2017.

R$ mn 2011 2012 2013 2014 2015 2016 Change

16/15

CAGR

16/11

Capex 39.4 63.6 154.0 119.1 73.2 71.5 (2.4%) 12.7%

916 874 734

996 1,282

1,589

(111) (138) (118) (171) (213) (125)

805 736 616 825

1,069

1,464

(400)

0

400

800

1200

1600

2000

2011 2012 2013 2014 2015 2016

R$

mil

lio

n

Cash and cash equivalents plus cash investments (ST and LT)

Loans and Financings (ST and LT)

Net cash

39

64

154

119

73 71

2011 2012 2013 2014 2015 2016

R$ m

illi

on

Capex

20 Management Report 2016

12. Independent auditors – CVM Instruction 381/03

To comply with CVM Instruction 381/2003, Grendene S.A. reports that it used the independent auditing services of PricewaterhouseCoopers – Auditores Independentes (PWC), for a special review of its quarterly information and financial statements for the business year ended December 31, 2016, for which its fees totaled R$ 444,800. In the period of that business year PricewaterhouseCoopers Contadores Públicos Ltda was, also, contracted to carry out other services relating to Bloco K and e-Social, in the amount of R$ 193,100, corresponding to 43.4% of the total of the external auditing services.

The Company’s policy in contracting any services not related to external auditing with the independent auditor is based on the principles that preserve the auditors’ independence, namely: (a) the auditor must not audit its own work; (b) the auditor must not exercise management functions in its client; and (c) the auditor must not promote the interests of its client.

The services provided by PWC related to Assurance carried out in accordance with the Brazilian Accounting Rules NBC PA 291 (R1): Independence – Other Assurance Work (Independência – Outros Trabalhos de Asseguração), as approved by Federal Accounting Council Resolution 1311/10 of December 9, 2010. They do not include the services that might compromise independence as described in that Rule.

12.1. Statement of justification in relation to independent auditors – PWC

The provision of other professional services not related to external auditing, described above, does not affect the independence nor the objectivity of the carrying out of the external auditing examinations made to Grendene S.A. and its subsidiaries. The policy of working with Grendene in the provision of services not related to external auditing is based on the principles that preserve the independence of the External Auditor, and all these principles were obeyed in the provision of the said services.

21 Management Report 2016

V. Capital markets and corporate governance

1. Capital markets

In 2016 a total of 70.8 million common shares were traded (0.86 times the total number of shares in the free float), in 336,500 trades, with total financial volume of R$ 1.2 billion. Daily averages were: 284,000 shares (0.34% of the free float); financial volume, R$ 4.9 mn; and number of trades, 1,351.

Over the 12 months of 2016, Grendene’s share (GRND3) provided investors with a gain of 10.5%, including reinvestment of dividends. The stock price varied over a range between a minimum at R$ 14.60, on January 21, 2016, and a maximum at R$ 20.41 on October 28, 2016. The Ibovespa index was 38.9% higher at the end of 2016 than at the close of December, 2016. Dividend yield, calculated on the basis of the weighted average price of the share in 2016, was 6.3% p.a. (vs. 5.2% p.a. in 2015).

This table gives number of trades, number of shares traded, financial volume, and daily average trading:

Year No. of trading

sessions

No. of trades

Number of shares

Volume R$

Price R$ Average no. of shares Average financial

volume R$

Weighted average

Close Per trade Per day Per trade Per day

2011 249 60,621 34,540,900 296,444,307 8.58 7.69 570 138,718 4,890 1,190,539

2012 246 134,570 66,297,600 772,896,090 11.66 16.49 493 269,502 5,743 3,141,854

2013 248 395,765 106,569,600 2,146,610,763 20.14 18.09 269 429,716 5,424 8,655,689

2014 248 352,905 93,691,900 1,422,422,174 15.18 15.30 265 377,790 4,031 5,735,573

2015 246 331,468 78,686,700 1,317,558,400 16.74 16.84 237 319,865 3,975 5,355,928

2016 249 336,512 70,808,700 1,214,895,573 17.16 17.58 210 284,372 3,610 4,879,099

In the period January through April 2017 Grendene will be a component of the following BM&FBovespa indices: IBRA, ICON, IDIV, IGCT, IGCX, IGNM, INDX, ITAG and SMLL.

This chart shows performance of Grendene ON shares compared to the Bovespa index (Base: Dec. 31, 2008 = 100), and daily trading volume.

On December 31, 2016 Brazilian institutional investors held 7.0% of the share capital of Grendene S.A. (25.6% of the free float); foreign investors held 16.3% (59.3% of the free float); small investors including individuals held 4.2% (15.1% of the free float); and the other 72.5% of the share capital was in the possession of the controlling stockholders and managers.

0

100

200

300

400

500

600

700

800

-

5

10

15

20

25

30

35

40

45

50

12/31/08 12/31/09 12/31/10 12/31/11 12/31/12 12/31/13 12/31/14 12/31/15 12/31/16

Ba

sis

10

0 =

De

c. 3

1, 2

00

8

Vo

lum

e -

R$

mil

lio

n

GRND3: Comparison with Ibovespa index and daily trading volume

Daily trading volume, R$ GRND3, with reinvest. of dividends Ibovespa index

22 Management Report 2016

74.9% 74.9% 74.2% 73.6% 72.5% 72.5%

12.6% 11.2% 9.0% 7.7% 8.6% 7.0%

9.5% 10.0% 12.9% 15.2% 15.6% 16.3%

3.0% 3.9% 3.9% 3.5% 3.3% 4.2%

2011 2012 2013 2014 2015 2016

% o

f to

tal o

wn

ers

hip

Profile of stockholders

Controlling stockholders and managers Brazilian institutional investors

Non-Brazilian investors Others

23 Management Report 2016

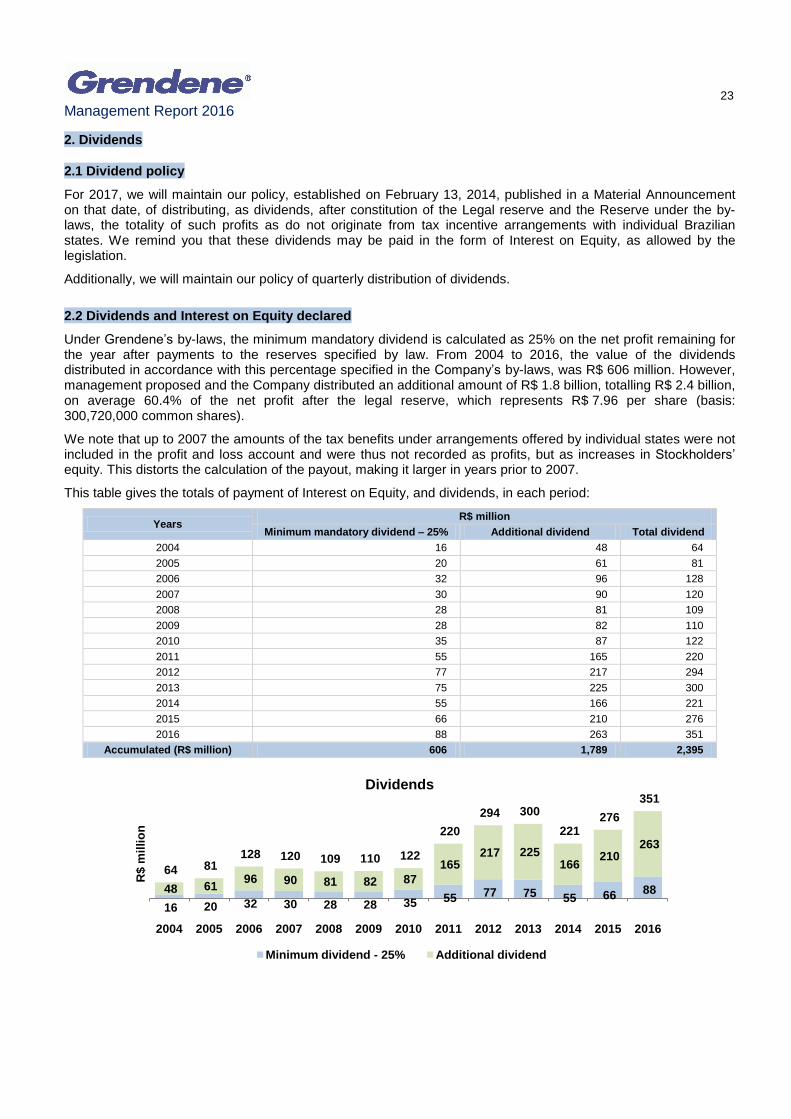

2. Dividends

2.1 Dividend policy

For 2017, we will maintain our policy, established on February 13, 2014, published in a Material Announcement on that date, of distributing, as dividends, after constitution of the Legal reserve and the Reserve under the by-laws, the totality of such profits as do not originate from tax incentive arrangements with individual Brazilian states. We remind you that these dividends may be paid in the form of Interest on Equity, as allowed by the legislation.

Additionally, we will maintain our policy of quarterly distribution of dividends.

2.2 Dividends and Interest on Equity declared

Under Grendene’s by-laws, the minimum mandatory dividend is calculated as 25% on the net profit remaining for the year after payments to the reserves specified by law. From 2004 to 2016, the value of the dividends distributed in accordance with this percentage specified in the Company’s by-laws, was R$ 606 million. However, management proposed and the Company distributed an additional amount of R$ 1.8 billion, totalling R$ 2.4 billion, on average 60.4% of the net profit after the legal reserve, which represents R$ 7.96 per share (basis: 300,720,000 common shares).

We note that up to 2007 the amounts of the tax benefits under arrangements offered by individual states were not included in the profit and loss account and were thus not recorded as profits, but as increases in Stockholders’ equity. This distorts the calculation of the payout, making it larger in years prior to 2007.

This table gives the totals of payment of Interest on Equity, and dividends, in each period:

Years R$ million

Minimum mandatory dividend – 25% Additional dividend Total dividend

2004 16 48 64

2005 20 61 81

2006 32 96 128

2007 30 90 120

2008 28 81 109

2009 28 82 110

2010 35 87 122

2011 55 165 220

2012 77 217 294

2013 75 225 300

2014 55 166 221

2015 66 210 276

2016 88 263 351

Accumulated (R$ million) 606 1,789 2,395

16 20 32 30 28 28 35 55 77 75 55 66 88 48 61 96 90 81 82 87

165 217 225

166 210

263

64 81 128 120 109 110 122

220

294 300

221 276

351

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

R$ m

illi

on

Dividends

Minimum dividend - 25% Additional dividend

24 Management Report 2016

(*) Payout: Dividend plus net Interest on Equity, divided by net profit after constitution of legal reserves.

(**) Dividend yield: Dividend per share + net Interest on Equity per share in the business year divided by weighted average price of the share in the annualized period.

Under the by-laws and the present dividend policy, and based on the amount shown below, management proposes allocation of the net profit for the 2016 business year as follows:

a) R$87,845,724.55 as minimum mandatory dividend, corresponding to 25% of the base amount for calculation of dividends, shown below; and

b) R$263,537,173.65 in dividends additional to the minimum mandatory dividend.

The sum of these amounts is a total of R$ 351,382,898.20, which after deduction of quarterly interim dividends paid, the gross amount of which totals R$ 202,789,040.29 (total of Interest on Equity, and dividends), results in a balance of R$ 148,593,857.91, which the Company will pay, subject to approval by the Annual General Meeting that approves the accounts for the business year 2016, starting on April 26, 2017 as follows:

a) R$130,000,000.00 as Interest on Equity (gross) calculated as being part of dividends (net amount R$110,500,000.00);

b) R$18,593,857.91 as complementary dividends for the 2016 business year.

The Interest on Equity, and the complementary dividends, will be payable to holders of record of the Company’s shares (GRND3) in the Company’s records on April 12, 2017 (the cut-off date).

As from this date, the credits of Interest on Equity will be credited individually to stockholders, with retention of the income tax applicable at source, in accordance with the legislation.

Thus Grendene shares (GRND3) will be traded ex-dividends and ex-Interest on Equity, on April 13, 2017 on the BM&FBovespa.

R$ 0.730 R$ 0.976 R$ 0.998

R$ 0.736 R$ 0.868

R$ 1.089

74.8% 71.1% 71.8%

46.1% 48.6% 53.1%

8.5% 8.4% 5.0% 4.8% 5.2% 6.3%

2011 2012 2013 2014 2015 2016

%

R$

pe

r s

ha

re

Dividend per share Payout (*) Dividend yield (**)

25 Management Report 2016

Basis for the distribution of dividends in 2016

Grendene S.A. (holding company) R$

Net profit for the year (2016) 634,491,601.48

( - ) Tax incentives reserve (264,614,866.54)

Basis for calculation of the Legal reserve 369,876,734.94

( - ) Constitution of Legal reserve (18,493,836.74)

Basis of calculation of the minimum mandatory dividend relating to the result of the business year 351,382,898.20

Minimum mandatory dividend – 25% 87,845,724.55

Dividend proposed in excess of the minimum mandatory dividend 263,537,173.65

Total of dividends proposed by management (Dividend + Interest on Equity) 351,382,898.20

Allocation of the proposed corporate action payments (Interest on Equity and Dividends)

Total of dividends and Interest on Equity proposed by management 351,382,898.20

( - ) Dividends and I.E. paid in advance (202,789,040.29)

( = ) Balance to be distribute for 2016 business year 148,593,857.91

Balance of dividends 18,593,857.91

Interest on Equity, gross 130,000,000.00

( - ) Income tax withheld at source (15%) 19,500,000.00

( + ) Interest on Equity, net 110,500,000.00

Corporate action payments distributed / proposed

Decision Date approved Ex-dividend

date Date of start of

payment Gross amount

R$ Gross amount per share R$

Net amount R$ Net amount per share R$

Dividend 1 Apr. 28, 2016 May 4, 2016 May 18, 2016 51,190,824.65 0.1702 51,190,824.65 0.1702

I.E. 1 Apr. 28, 2016 May 4, 2016 May 18, 2016 30,000,000.00 0.0998 25,500,000.00 0.0848

Dividend 1 Jul. 28, 2016 Aug. 3, 2016 Aug. 17, 2016 45,505,162.63 0.1513 45,505,162.63 0.1513

Dividend 1 Oct. 20, 2016 Oct. 28, 2016 Nov. 16, 2016 76,093,053.01 0.2530 76,093,053.01 0.2530

Dividend 1 Feb. 16, 2017 Apr. 13, 2017 Apr. 26, 2017 18,593,857.91 0.06182 18,593,857.91 0.06182

I.E. 1 Feb. 16, 2017 Apr. 13, 2017 Apr. 26, 2017 130,000,000.00 0.43242 110,500,000.00 0.36752

Total 351,382,898.20 1.16852 327,382,898.20 1.08862

1 Corporate action payments (Interest on Equity + Dividends) approved ad referendum the Annual General Meeting that will examine the balance sheet and financial statements for the 2016 fiscal year.

2 Amount per share subject to alteration as a result of the balance of shares in treasury on the cutoff date (April 12, 2017).

26 Management Report 2016

3. Corporate governance best practices

Seeking to keep analysts and investors informed on the performance of our business, we have permanent channels of communication, we carry out visits, we take part in conferences and we make presentations in events at various locations around the world. We also maintain a specific site for investor relations in English and Portuguese. Since 2008 we have ceased to prepare the Annual Report, providing all the information on our performance in the Report of Management and Reference Form, both being translated and posted on our site. We carry out quarterly conference calls presenting our results in Portuguese with simultaneous translation in English and we publish a press release with analysis of these results. We also present a non-deal roadshow, quarterly in Brazil and six-monthly outside Brazil, and at least two meetings with Apimec (Sao Paulo, and Rio Grande do Sul) per year.

Since April 14, 2008, as a means of aligning the interests of management with those of stockholders, we have introduced a Stock Options Plan applying to members of the Executive Board and our principal executives. Since the start of the Plan we have already made grants of 8.4 million call options (the figure is adjusted for the stock split of September 23, 2009), equivalent to 2.8% of the Company’s total shares. Of these, 16.8% remain unexercised (1.4 million shares), equivalent to 0.5% of the total shares (base date: December 31, 2016). Our shares are listed on the Novo Mercado of BM&FBovespa, since October 29, 2004. In November 2007 we adjusted our free float to 25%, in accordance with the rules established by the listing regulations of the Novo Mercado. To improve liquidity, we have contracted a market maker for our shares (GRND3) since September 2005, and in September 2009 we made a stock split of the number of shares issued from 100,000,000 to 300,000,000, aiming for better liquidity for the shares and to facilitate their purchase by small investors and consequently expand our stockholder base. On March 22, 2010 we approved an increase in share capital through issuance of 720,000 new common shares without par value, to comply with the Stock Options Plan, increasing the share capital to 300,720,000 common shares. To comply with the other exercises of options the Company acquired shares in the market, and thus stockholders were not diluted. On December 31, 2016 the shares in circulation were 27.5% of the total shares issued.

3.1 Commitment clause

The Company, its stockholders, its managers and the members of its Audit Board undertake to resolve by means of arbitration, before the Market Arbitration Chamber, all and any dispute or controversy that may arise between them, relating to our arising from, in particular, the application, validity, efficacy, interpretation, violation, or their effects, of the provisions contained in the Corporate Law, the Company’s by-laws, the rules issued by the National Monetary Council, by the Brazilian Central Bank or by the Brazilian Securities Commission, or in the other rules applicable to the functioning of the capital market in general, as well as those contained in the Listing Regulations of the Novo Mercado, the Arbitration Regulations, the Sanctions Regulations and the Novo Mercado participation agreement.

3.2 Statement by executive board

In compliance with CVM Instruction 480/09 the members of the Executive Board declare that they have discussed, reviewed and agree with the opinions expressed in the opinion of the external auditors and with the financial statements for the business year ended December 31, 2016.

27 Management Report 2016

3.3 Awards & Recognition

In 2016 Grendene was recognized and praised by various institutions for its performance in various sectors of activity.

For the second year running, Grendene won the most important seal in world design, the If Design Award. Grendene was recognized in the category Architecture and interiors, with the plan for the London Galleria Melissa.

The IF Design Award is considered to be one of the world’s important and complete design awards.

Clube Melissa, the official network of Melissa brand stores, once again received the Franchising Seal of Excellence from the Brazilian Franchising Association – for the fourth time running. The aim of the recognition – delivered in São Paulo on April 15, 2016 – is to supply the franchisor network with a broad-based satisfaction survey from the franchisees of participating brands.

On April 27, 2016, Grendene received the 2015 Champions of Innovation Award, given by Amanhã Magazine. This is the 12

th annual award, organized by the Amanhã Group in

partnership with specialized consultants Edusys and technical support from the Dom Cabral Foundation. The event recognizes the 50 companies with the most innovative and creative practices in the three states of Brazil’s South (Paraná, Santa Catarina and Rio Grande do Sul).

Grendene was award first place in the Leather and Footwear sector in Champions of Innovation, and second place in the ranking overall.

On June 23, 2016 Melissa One by One received significant awards in the 2016 Top XXI Brazil Design Awards in the categories Innovation and Professional Highlight. One of the professionals recognized was Grendene’s Design Director, Edson Matsuo. The awards aim to recognize professionals and companies and strengthen Brazilian design.

Trophy received by

Melissa One by One

Trophy received by

Design Director

Grendene was once again recognized as the best company in the textiles sector by the Melhores e Maiores publication of Exame Magazine. This recognition is based on a technical analysis of companies’ financial statements for 2015. The award event took place in São Paulo on June 29.

Companies are compared on economic/financial criteria – such as profitability, revenue growth, liquidity and wealth creation – by a team of lecturers and technical staff of Fipecafi, a foundation linked to the Economics, Management and Accounting Faculty of São Paulo University.

28 Management Report 2016

September 12, 2016: Grendene won the 2016 Valor 1000 award in the Textile, Leather and Clothing sector. This award, held at the São Paulo Grand Hyatt Hotel, recognized the best companies in 25 sectors of the economy.

September 27, 2016: Our Faça Parte Grendene program was recognized by the Brazilian Human Resources Association, Rio Grande do Sul section (ADRH-RH), with the 2016 Top Ser Humano prize. The program was created in 2012 with the aim of attracting, identifying and selecting professionals aligned with Grendene’s culture and values.

September 29, 2016: Grendene once again received the trophy for best company in the country in the textile sector, in the second annual Empresas Mais publication of the Estado de São Paulo newspaper, prepared jointly with the Management Institute Foundation (FIA). This aims to highlight Brazil’s most efficient and advanced companies, taking into account both economic success and best management practices.

November 9, 2016: Grendene was once again in the ranking of the 500 Maiores do Sul, an initiative of the Amanhã Group in partnership with PwC (PricewaterhouseCoopers). For the last 26 years this project has presented the most complete and important regional ranking in the country, identifying the 500 largest companies in the Southern Region. Classification: 9th among companies of Rio Grande do Sul and Highlight Company in the category Net revenue in companies of the Leather and Footwear sector.

December 1, 2016: Recognized as the fourth largest company in the state in the 16th

Delmiro Gouveia Awards, organized by the O Povo Communications Group and the Albanisa Sarasate Institute (IAS). Grendene has been a Highlight Winner in these awards since they were created in 2001.

December 5, 2016: Grendene was one of the Highlight Companies in the 2016 Brazil Design Award, in the communication category Environment with the Galeria Melissa London – Multi Randolph project, carried out by the Escola Britânica de Artes Criativas (British Creative Arts School – EBAC), with organization by Abedesign (Brazilian Design Companies Association).

29 Management Report 2016

VI. Social and environmental responsibility

We believe that the principal indicator of sustainability of a company is its generation of profit and financial solidity. This factor means that consumers pay for the company’s products more than the inputs extracted from nature to manufacture and distribute these products cost. Further, it ensures continuity of the company and generation of employment, and also satisfaction of the needs of millions of clients that buy and use its products.

However, we recognize that the financial statements do not always portray all the interfaces of a company with its social and environmental surroundings and these financial indicators can react slowly to problems of relationship with society or the environment. Being aware of our responsibility as a benchmark leading Company in our segment and employer of more than 20,000 employees, we have continued to improve our processes so as to reduce the consumption of inputs and raw materials, including water and all the forms of energy, and the generation of all types of waste, loss and wastage of resources that not only represent costs for the company but also exhaust the environment when consumed beyond the level of need. With these objectives, we have carried out a range of actions over the years.

Grendene’s focus in relation to sustainable development is in reduction of waste, optimization of resources (raw materials, equipment, energy and water), recyclability of products, quality of processes and man’s interaction with this context based on the triple principle: reduce, re-use, recycle. We continue to direct special attention to the consumption of water, consumption of energy, and generation of wastes in general. The actions that we take have generated not only reduction in costs and operational risks but also a lower environmental impact. This is a list of some of the reductions we have achieved, from 2015 to 2016:

water consumed per pair produced: 2%;

consumption of electricity per pair produced: 3%;

generation of wastes per pair produced: 9%.

Our principal actions with this focus in 2016 were:

Water consumption – our industrial operations are in an arid region of the country: we act to increase the availability of water, and constantly reduce the impact of our water consumption footprint.

a. At present we have one of the lowest water footprints in footwear production. b. Approximately 80% of our use of water is for human consumption. c. We have a target of re-using 100% of treated effluent by 2020 – i.e. zero disposal of effluent.

Our water consumption indicator has varied as follows:

2015 2016 Change %, 2016/2015

Water consumption (liters/pair) 1.57 1.55 (1.8%)

Water consumption (thousand m³) 259.4 252.9 (2.5%)

Energy efficiency: we are aiming for the lowest energy consumption per pair produced, and the lowest carbon emissions per pair produced.

a. Since 2012 we have invested in energy efficiency, with a range of actions from change of motors to change from traditional illumination to LEDs. With these energy efficiency actions, we have so far reduced electricity consumption per pair produced by 11.8%.

b. 85% of the electricity supplied to the manufacturing units is of renewable origin and has low or zero carbon emission equivalent.

With our actions to increase awareness; our daily indicator of energy efficiency, with targets for managers; our automation projects; and improvements in equipment, in 2016 we avoided a total volume of consumption equivalent to 1.3 million kWh, and with the fall in production, 6.5 million kWh, in the year.

Million / kWh 2015 Reduction by

efficiency Reduction in production

2016 Change %, 2016/2015

Consumption of electricity 106.8 (1.3) (6.5) 99.0 (7.3%)

30 Management Report 2016

Our wastes are 100% recyclable: the materials that comprise our footwear are 100% recyclable, each one having its own characteristic recycling features.

a. As well as our products being recyclable, they also have non-toxic characteristics and do not contain any dangerous or allergenic substances.

b. The advantage for our materials in terms of recycling is that they do not need addition of any chemical

products. In management of wastes, we recycle 92% of the material generated. Of this total, 97% is recycled as produced, and 3% undergoes some process before being re-used.

The figures for the indicator of wastes generated per pair, and total reductions, are as follows:

2015 2016 Change %, 2016/2015

Wastes (grams / pair) 10.67 8.92 (16.4%)

Reduction of wastes (thousand tons) 1.8 1.5 (18.6%)

In 2016, as a result of all the Company’s actions in caring for the environment, Grendene received Recertification by ABVTEX (the Brazilian Textile Retailers’ Association) – it was the first footwear company to receive this certification. The aim of this certificate is to enable the retail sector to certify and monitor its suppliers in relation to practices of Environmental, Social and Employment Relations responsibility.

31 Management Report 2016

VII. Human resources

The performance of our business model requires excellence in the activities of our employees. We are a company whose engine is its people who, the more they are aligned with our Values, the more then will help in achieving the targets. Our human resources management operates on the basis of this conviction.

With the mission of producing results that sustain the strategy of the business, through integrated and competitive management of people, in an environment of respect for our Values, Grendene’s HR is structured in subsystems which are strategically developed in alignment with actions to build, develop and engage teams.

Development of competencies, knowledge and skills of employees is a priority of our model for management of people. In this challenge, the leaders of the company are the principal partners of our human resources staff. This is why, since 2005, we have had the Leaders’ Academy – a program that develops leaders aligned with the business and the market, committed to distinctive results and highly motivated teams. Among the actions for which leaders are prepared are: Formal performance evaluation of teams, providing constant feedback, contributing to full growth of the individual through development plans; identification and selection of the right people for the right places; and promotion of communication at all the levels of the organization.

We also highlight the degree of our care in managing health and safety – going beyond the legal requirements, through constant investment in technologies, machinery, and technical, administrative and medical actions. We also operate awareness-raising campaigns and actions extending to the community where the company works.

The return on the investment in our people is reflected in the Company’s low turnover, and in the maintenance of its track record of good results.

Social and corporate data 2011 2012 2013 2014 2015 2016

Employees (average / year) 24,396 24,084 28,085 26,543 24,176 20,401

Hours of training (per employee) 15 20 32 50 67 79

Meals (year) 5,494,812 5,955,479 6,867,415 4,990,607 4,815,696 5,046,305

Employees with special needs (year) 1,073 1,016 1,288 1,146 1,088 971

Dental care (appointments/year) 19,656 20,485 19,875 17,818 17,555 15,391

Absenteeism 1.81% 1.73% 2.08% 2.47% 2.17% 1.88%

Turnover (month) 1.22% 2.12% 2.00% 1.66% 1.58% 1.72%

‘Basic food baskets’ distributed (units/year)* 346,858 292,398 330,814 317,514 290,269 243,229

(*) Grendene’s policy of distribution of ‘basic food baskets’ aims to reinforce the employee’s food security. It has been in place since 1990. Over time, the effort is to maintain the basket’s nutritional value offering various options of items. All the employees and interns of Grendene, without distinction, receive it after the first month of work, until they leave the Company.

32 Management Report 2016

VIII. Statement of value added

Added value, which is an indication of the wealth added to society by the Company in its economic activity, totaled R$ 1,543 billion in 2016 (R$ 1.557 billion in 2015). The complete statement is a part of the financial statements.

Added value statement

R$ ’000 2011 2012 2013 2014 2015 2016

Personnel 346,200 416,699 515,243 521,449 531,099 518,382

Taxes 218,478 250,761 271,920 240,918 240,350 254,994

Remuneration of external capital 65,787 77,518 86,700 95,615 246,601 135,728

Remuneration of own capital 305,446 429,003 433,540 490,244 539,311 633,955

Total 935,911 1,173,981 1,307,403 1,348,226 1,557,361 1,543,059

37.0% 35.5% 39.4% 38.7% 34.1% 33.6%

23.3% 21.4% 20.8% 17.9% 15.4% 16.5%

7.0% 6.6% 6.6% 7.1% 15.8% 8.8%

32.7% 36.5% 33.2% 36.4% 34.6% 41.1%

0%

25%

50%

75%

100%

2011 2012 2013 2014 2015 2016

%

Distribution of added value

Personnel Taxes Remuneration of external capital Remuneration of own capital

33 Management Report 2016

IX. Final considerations and Outlook

As we have stated, we expect 2017 to be a difficult year, with the start of a slow recovery, many uncertainties in the political field, adjustments in the domestic economy, turbulence and volatility in international markets, and a continuing context of crisis in the traditional export markets.

Although the economic outlook of Brazil is not the best it could be, we derive strong encouragement from the fact that we are in a solid position, and that when the crisis is over we will be ready to return to growth. Crises tend to eliminate the less efficient – and strengthen those that are more able. We have no doubt which group we are a member of.

For a long time we have perceived that quality design at acceptable cost is the consumption dream of the middle class. Our brands and products have stood out in these categories, and provided us with very good results.

Phrases that do justice to our design and product approach include: To deliver value to the client with low cost; – and Famous designers accessible to all income groups; ‘Affordable Luxury’ defines the value proposal that Grendene has been delivering to consumers all over the world.

In 2017 we expect to invest, in maintenance of our production capacity, an amount equivalent to annual depreciation: Between R$ 100 and R$ 110 mn. Clearly this figure is only a reference, and we will not hesitate to invest in any good opportunities, if they appear (at the moment we do not see any).

Lamentably, in our opinion, the footwear sector will continue to suffer from the economic uncertainties. In 2017 we expect a slightly increase in consumption in Brazil, in number of pairs, in the order of 0.5% to 1%, and we have no concrete expectation of returning to the record volume of pairs that we had in 2014. We expect to grow, but we are conscious of the difficulties. Whatever the market situation is, we will seek to obtain better results than those of last year – something which we have been repeatedly achieving.

The increase in margins will have to come from increase in productivity, and rationalization of costs, since increase in volumes will be unlikely. In the last six years apparent consumption of footwear in Brazil has fallen at the rate of 1.6% p.a. (CAGR), while the number of pairs sold by Grendene has increased at 3.2% p.a. (CAGR), thus a higher rate than the market, providing us with significant gains in market share in all the lines in which we operate.

In the external market our strategy of fleeing from the concept of exporting ‘commodities’ has been successful. At the same time, we will be confronting an increasingly adverse international market. We have good margins, and we expect to continue in 2017.

In the domestic market, consumers’ desire for our products has not diminished, but their purchasing power has. Hence our challenge will be to continue to meet the expectations of our consumers with products that fit their budget. We are confident that we will not disappoint them.

We have faced the scenario that presents itself in the same way as always – with determination, courage and lucidity – obtaining strong results, as is our habit. We should re-emphasize the execution of our strategy in 2017 with special attention to growth of market share and maintenance of margins, improving our communication with the market, understanding the needs of the distribution channels, innovating in products, strengthening our brands with aggressive marketing through multiple media, and seeking excellence in the operation through continuous improvements. The objective is to continually strengthen our relationship with our clients, and serve them in a way that is increasingly focused on their needs. We understand that the remuneration of stockholders depends on this.

34 Management Report 2016

Appendix I

35 Management Report 2016

OPINION OF THE AUDIT BOARD

The Audit Board of Grendene S.A., in compliance with the provisions of law and the by-laws, has examined the Report of Management and the Individual financial statements of the Company (holding company), prepared in accordance with accounting practices adopted in Brazil, and the Consolidated financial statements prepared in accordance with International Financial Reporting Standards (IFRS) issued by the International Accounting Standards Board (IASB) for the business year ended December 31, 2016, which were approved by the Company’s Board of Directors on February 16, 2017. Based on our reviews, and further considering the report of PricewaterhouseCoopers Auditores Independentes, without qualification, dated February 15, 2017, and the information and explanations received during the business year, it is the opinion of this Audit Board that the said documents are in the proper condition to be considered by the Annual General Meeting of Stockholders.

Farroupilha, February, 16, 2017.

___________________________________

João Carlos Sfreddo

Member of the Audit Board

___________________________________

Eduardo Cozza Magrisso

Member of the Audit Board

__________________________________

Herculano Aníbal Alves

Member of the Audit Board

36 Management Report 2016

Appendix II

Grendene S.A.

Parent company and consolidated financial statements for the years ended December 31, 2016 and 2015

GRENDENE S.A.

Financial statements December 31, 2016 and 2015 Index Independent auditor's report ............................................................................................................... 1 Financial statements Balance sheet .......................................................................................................................................... 6 Statement of income .............................................................................................................................. 8 Statement of comprehensive income ............................................................................................... 9 Statement of changes in equity ....................................................................................................... 10 Statement of cash flows .................................................................................................................... 11 Statement of value added ................................................................................................................. 12 Notes to the financial statements ................................................................................................... 13

1

INDEPENDENT AUDITOR'S REPORT

To the Board of Directors and Stockholders Grendene S.A. Opinion

We have audited the accompanying parent company financial statements of Grendene S.A. (the "Company" or "Parent Company"), which comprise the balance sheet as at December 31, 2016 and the statements of income, comprehensive income, changes in equity and cash flows for the year then ended, as well as the accompanying consolidated financial statements of Grendene S.A. and its subsidiaries ("Consolidated"), which comprise the consolidated balance sheet as at December 31, 2016 and the consolidated statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies. In our opinion, the financial statements referred to above present fairly, in all material respects, the financial position of Grendene S.A. and of Grendene S.A. and its subsidiaries as at December 31, 2016, and the financial performance and the cash flows for the year then ended, as well as the consolidated financial performance and the cash flows for the year then ended, in accordance with accounting practices adopted in Brazil and with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Basis for opinion

We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Parent Company and Consolidated Financial Statements section of our report. We are independent of the Company and its subsidiaries in accordance with the ethical requirements established in the Code of Professional Ethics and Professional Standards issued by the Brazilian Federal Accounting Council, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion. Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the parent company and consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Matters

Why it is a Key Audit Matter

How the matter was addressed

2

Why it is a Key Audit Matter How the matter was addressed in the audit

Government grants for investments (Notes to the financial statements 4(m) and 17)

The Company receives incentives related to the Value-added Tax on Sales and Services (ICMS), arising from the Industrial Investment Attraction Program (PROVIN) and the Program of Incentives for the Port and Industrial Activities of Ceará (PROAPI), on its activities located in the state of Ceará, as well as the Foreign Trade Incentive Program (PROCOMEX) and the Program for the Development of Bahia (PROBAHIA), on its activities located in the state of Bahia. These incentives represented a significant portion of the Company's consolidated net revenue, and its recognition is in accordance with the conditions established in the respective agreements, among which, the compliance with the specific clauses related to the considerations required and the effectiveness of the respective programs. This was an area of focus in our audit due to the significance of the tax benefit amounts when compared to the results of operations, and also the strictness necessary to comply with the requirements of each of the agreements.