30

Oscar Wehtje, Head of Product Development September 2015 LME presentation for ALFED

Oscar Wehtje, Head of Product Development September 2015

LME presentation for ALFED

1

Agenda

• Introduction to the LME

• Hedging concepts

• Warehouse reforms and pricing impacts

• New LME products and services

– Focus on the LME Premium Aluminium contracts

• Questions

• Ring tour (4:30 – 5:00 pm)

• Refreshments

2

Introduction to the LME

3

The London Metal Exchange

LME was established in 1877 in response to industrial revolution

• High metal consumption relying on imports from abroad

• The need to hedge risk of price fluctuations during long shipping voyages

• Shipping of Copper from Chile and Tin from Malaysia took three months to arrive in

London

LME was acquired by Hong Kong Exchanges and Clearing (HKEx) in December 2012

4

The London Metal Exchange New contracts have been added to the initial Copper and Tin, over the past ~100

years

1877

Copper

& Tin

1920

Lead &

Zinc

1978

Primary

Aluminium

1979

Nickel

1992

Aluminium

Alloy

2002

NASAAC

2008

Steel Billet

2010 Cobalt &

Molybdenum

2015 Aluminium

Premiums &

Ferrous suite

5

LME Volumes

LME trading volume, 2002 – 2014

• LME trading represents c. 80% of the global exchange traded base metals volume

• In 2014 a total of 177.2 million lots were traded (3.5% increase vs. 2013)

– $14.9 trillion notional value, or

– 4 billion tonnes of metal

6

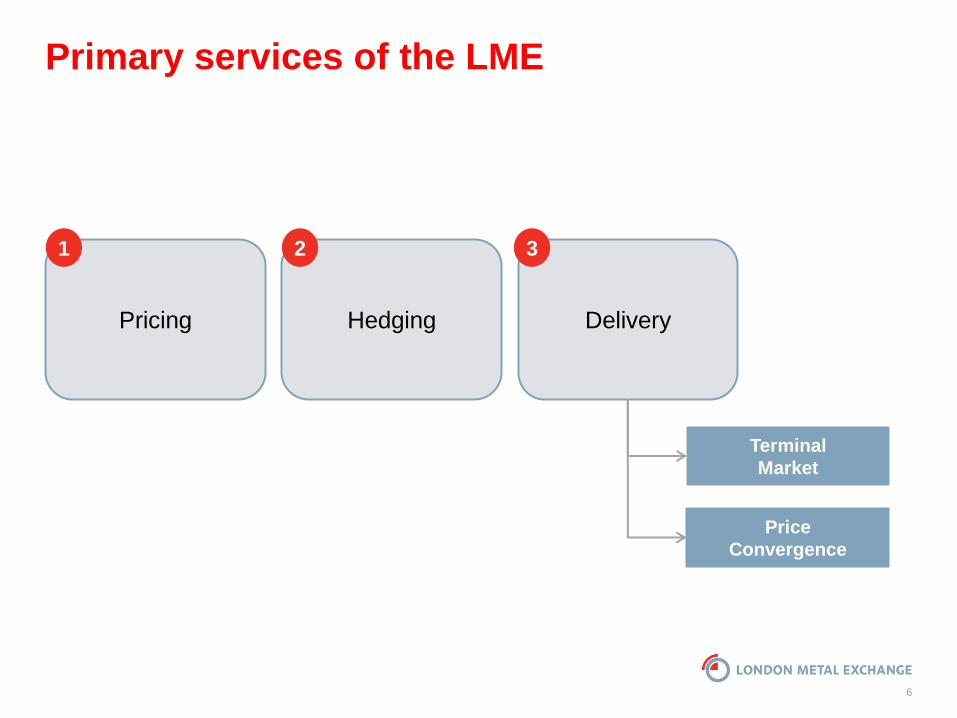

Primary services of the LME

Delivery

Terminal

Market

Price

Convergence

Hedging Pricing

1 2 3

7

Hedging concepts

8

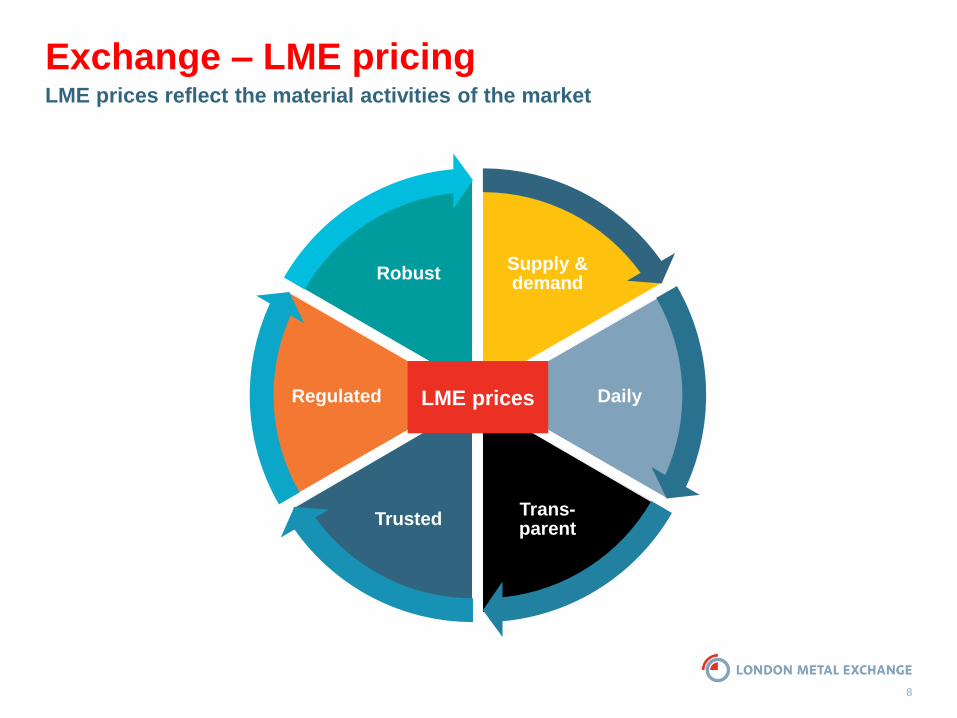

Exchange – LME pricing LME prices reflect the material activities of the market

Supply & demand

Daily

Trans-parent

Trusted

Regulated

Robust

LME prices

9

What does the LME price represent?

The LME price represents material:

• of an LME registered brand

• stored in an LME approved warehouse

• duty unpaid – no taxes / VAT etc

• buyer to pay for delivery out of warehouse

10

LME price minus discount

Low Metal Content

Smelting Concentration Mining Semi

Fabricated Products

Metal Products

The metals value chain It does not matter what stage of the metals value chain you are – the LME price is

relevant!

Ingot

Billet Cathode

Wire

Cans

Rebar

LME price minus discount LME price

LME price plus production costs and profit

margin

11

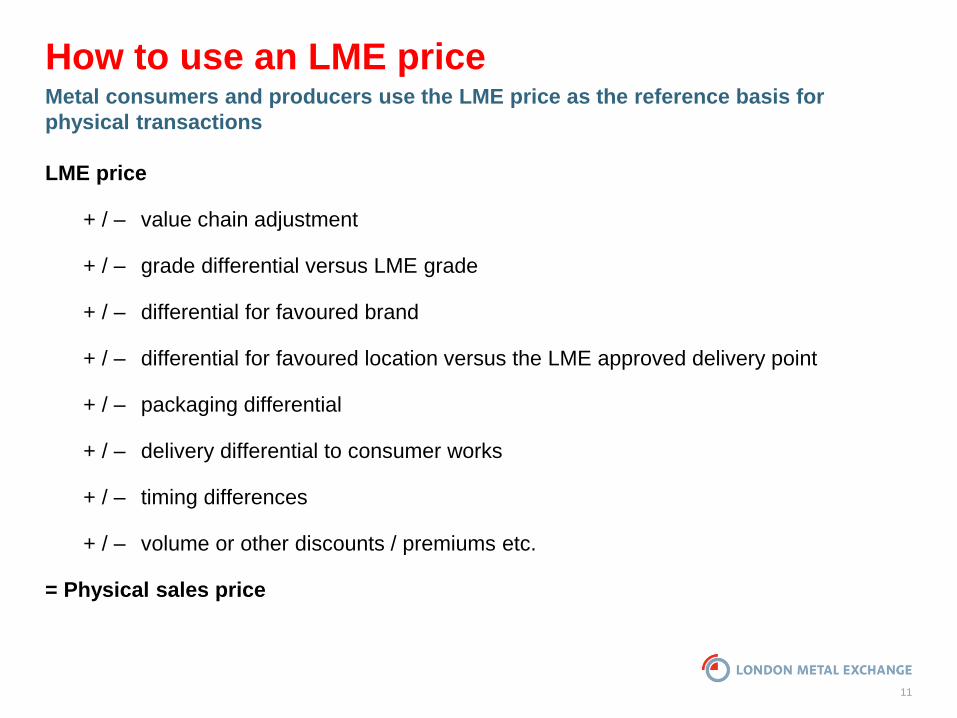

How to use an LME price

LME price

+ / – value chain adjustment

+ / – grade differential versus LME grade

+ / – differential for favoured brand

+ / – differential for favoured location versus the LME approved delivery point

+ / – packaging differential

+ / – delivery differential to consumer works

+ / – timing differences

+ / – volume or other discounts / premiums etc.

= Physical sales price

Metal consumers and producers use the LME price as the reference basis for

physical transactions

12

What stops you hedging?

Speculation Complicated Pressure off

sourcing

Liquidity Shareholder

exposure Cost

Pricing not hedging

Creating hedging

team

13

What is hedging?

• Protects against adverse price movements

– By hedging you reduce the uncertainty and your exposure to price movements

• Locks in an agreed profit margin

– The financial hedge allows the buyer/seller to lock in a certain price to be paid/received in the future

• Protects inventory value

– If hedged, any losses on the physical market (affecting the inventory value) are offset by an

increased value in the financial position

Establishing a position in a commodity futures market (LME) which is equal and

opposite to a risk on a physical market

14

Warehouse reforms

and pricing impact

15

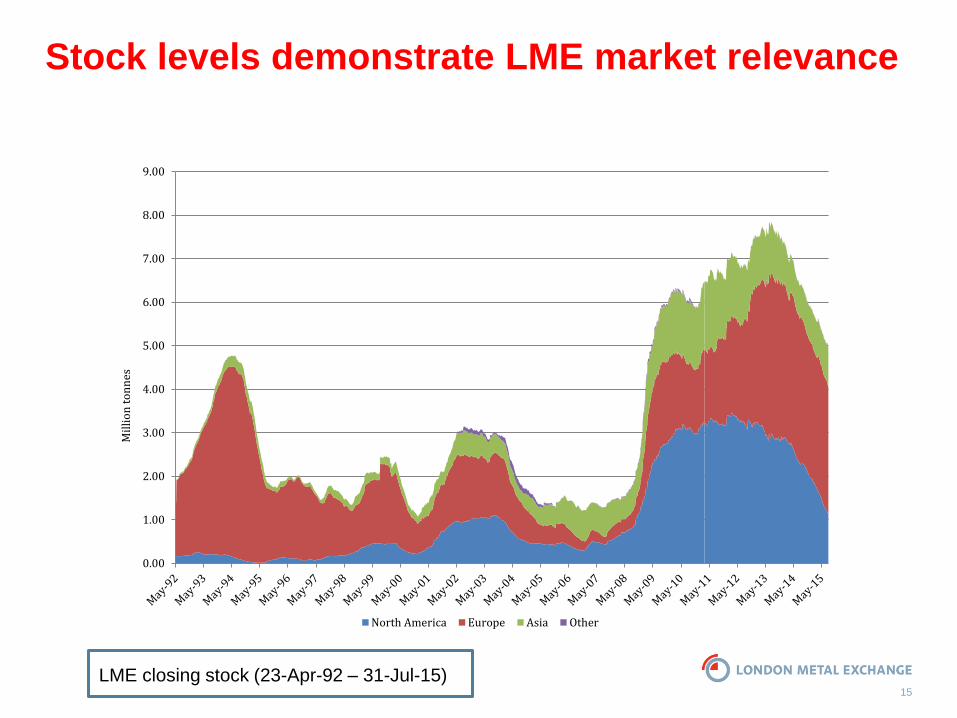

Stock levels demonstrate LME market relevance

LME closing stock (23-Apr-92 – 31-Jul-15)

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

Mil

lio

n t

on

nes

North America Europe Asia Other

16

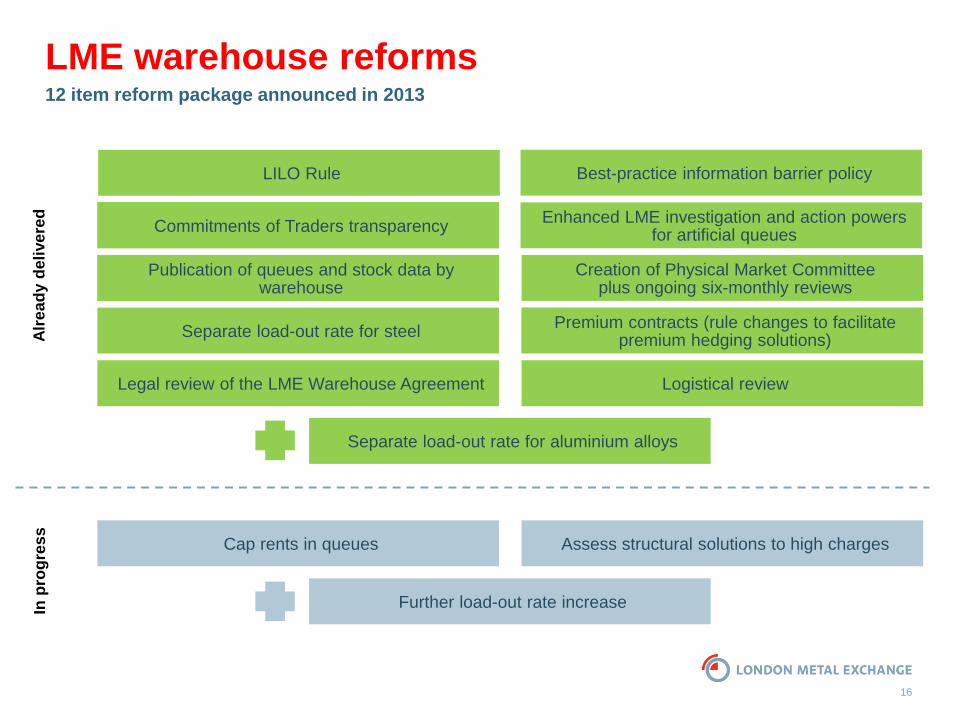

LME warehouse reforms 12 item reform package announced in 2013

Best-practice information barrier policy

Enhanced LME investigation and action powers for artificial queues

Premium contracts (rule changes to facilitate premium hedging solutions)

Separate load-out rate for steel

Legal review of the LME Warehouse Agreement Logistical review

Separate load-out rate for steel

Cap rents in queues Assess structural solutions to high charges

LILO Rule

Alr

ea

dy d

eli

ve

red

In

pro

gre

ss

Commitments of Traders transparency

Publication of queues and stock data by warehouse

Creation of Physical Market Committee plus ongoing six-monthly reviews

Enhanced LME investigation and action powers for artificial queues

Further load-out rate increase

Separate load-out rate for aluminium alloys

17

0

100

200

300

400

500

600

700

800

Waitin

g tim

e (

ca

len

da

r d

ays)

Impala Antwerp Pacorini Johor Pacorini Vlissingen Metro Detroit Pacorini New Orleans

Queue development and projected decay1 Cancellation represents the key driver of queues. Data for primary aluminium as of 31-Jul-15

Key: Consultation announcement 1-Jul-13 Decision announcement 7-Nov-13 Initial Court Judgment 27-Mar-14 Court of Appeal Judgment 7-Oct-14 Supreme Court decision 17-Dec-14

“Incumbent” queues – development driven almost exclusively by warrant cancellation, given flat load-in by

operators

“Aspirant” queues now appear to have fallen away

1Projected queue decay. For important information as to

modelling approach and assumptions, please see Notices

15/071 : A070 : W024 and 15/191 : A187 : W063.

Projected data based on mid case scenario.

18

5%

10%

15%

20%

25%

Pre

miu

m %

age o

f LM

E p

rice +

pre

miu

m

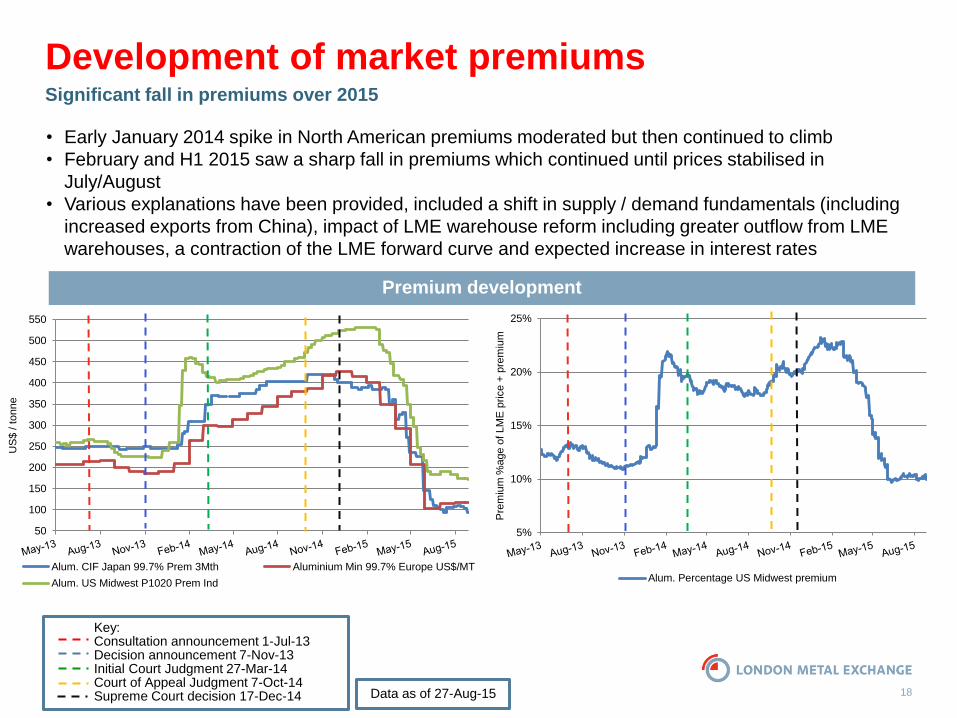

Alum. Percentage US Midwest premium

50

100

150

200

250

300

350

400

450

500

550

US

$ / tonne

Alum. CIF Japan 99.7% Prem 3Mth Aluminium Min 99.7% Europe US$/MT

Alum. US Midwest P1020 Prem Ind

Development of market premiums Significant fall in premiums over 2015

• Early January 2014 spike in North American premiums moderated but then continued to climb

• February and H1 2015 saw a sharp fall in premiums which continued until prices stabilised in

July/August

• Various explanations have been provided, included a shift in supply / demand fundamentals (including

increased exports from China), impact of LME warehouse reform including greater outflow from LME

warehouses, a contraction of the LME forward curve and expected increase in interest rates

Premium development

Data as of 27-Aug-15

Key: Consultation announcement 1-Jul-13 Decision announcement 7-Nov-13 Initial Court Judgment 27-Mar-14 Court of Appeal Judgment 7-Oct-14 Supreme Court decision 17-Dec-14

19

Composition of premiums

PREMIUMS

Queue related

LME implementing warehouse reforms

• Queues will fall over time – might go up

first, but eventually will go down

• Queue-based premiums will fall

accordingly

Non-queue related

Outside current scope of LME prices

• Driven by market supply / demand factors

– Location

– Shape, brand, quality

– FoT charge

• Region

• FoT charge

• Queue length

LME traded Premium contracts Premium futures contracts may additionally help to manage queue-based premiums while these continue to exist

20

LME Product pipeline

21

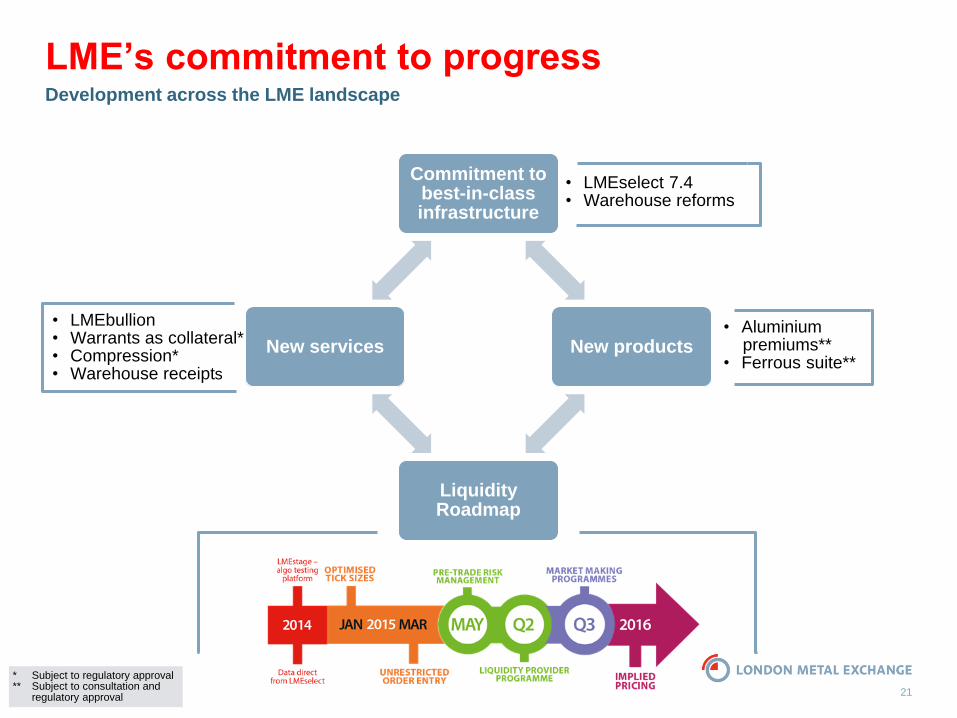

LME’s commitment to progress Development across the LME landscape

Commitment to best-in-class infrastructure

New products

Liquidity Roadmap

New services

• LMEbullion • Warrants as collateral* • Compression* • Warehouse receipts

• LMEselect 7.4 • Warehouse reforms

• Aluminium premiums** • Ferrous suite**

* Subject to regulatory approval ** Subject to consultation and regulatory approval

22

LME’s new aluminium contract suite LME’s leading global aluminium contract will be supplemented with four regional premium contracts

GLOBAL

LME ALUMINIUM

US

PREMIUM

EUROPEAN

PREMIUM

SOUTH

EAST

ASIAN

PREMIUM

EAST ASIAN

PREMIUM

LME’s new aluminium contract suite Premium contracts

Comprehensive warehouse reforms

Four regional contracts covering the key

centres of aluminium demand

1

Hedging of regional all-in price of

aluminium

2

Physical delivery of readily available metal

in Premium Warehouses

3

Launch 23 November 2015

5

NOTE: subject to regulatory approval

and rule change consultation

Monthly contract to concentrate liquidity

4

23

LME premium contract construction – illustrative Premium contract trading without diluting liquidity from the regular LME market

Note: LME premium contract indicatively assumed to trade at current surveyed US Midwest Premium level. Data as of 30 July 2015

Seller

B LME Warrant

$1,608

Current LME Aluminium Contract

$1,608 $185

LME Regional Premium Warrant

With LME Premium Contract

1 2

Buyer

A

$1,793

LME standard contract

LME premium contract

• Not in a queue • In relevant region

(e.g. Baltimore for North America)

• May be queued (e.g.Detroit / Vlissingen)

LME standard contract

24

Premium warehouse locations

LME premium warehouse locations in the US

Baltimore

Chicago

Los Angeles

Mobile

St Louis

Toledo

New Orleans

Detroit

Note: LME US Aluminium Premium Futures Contract covers the Midwest, Northeast and South US regions

Location without queues

Location with queues

Owensboro

25

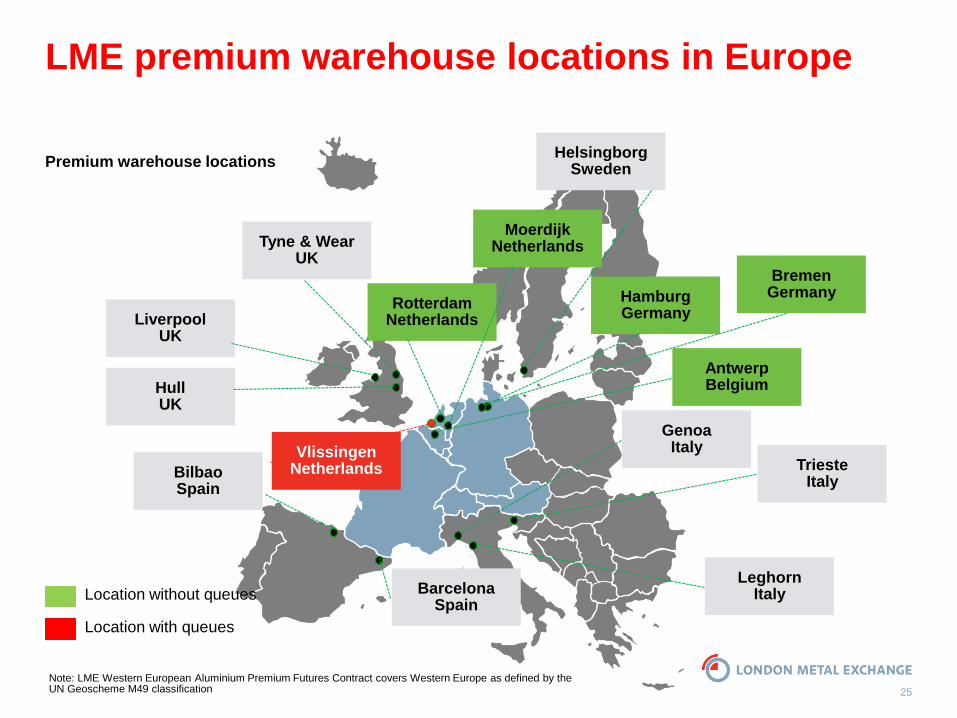

LME premium warehouse locations in Europe

Genoa Italy

Hamburg Germany

Helsingborg Sweden

Bilbao Spain

Antwerp Belgium

Barcelona Spain

Hull UK

Leghorn Italy

Liverpool UK

Rotterdam Netherlands

Trieste Italy

Tyne & Wear UK

Vlissingen Netherlands

Note: LME Western European Aluminium Premium Futures Contract covers Western Europe as defined by the UN Geoscheme M49 classification

Location without queues

Location with queues

Moerdijk Netherlands

Bremen Germany

Premium warehouse locations

26

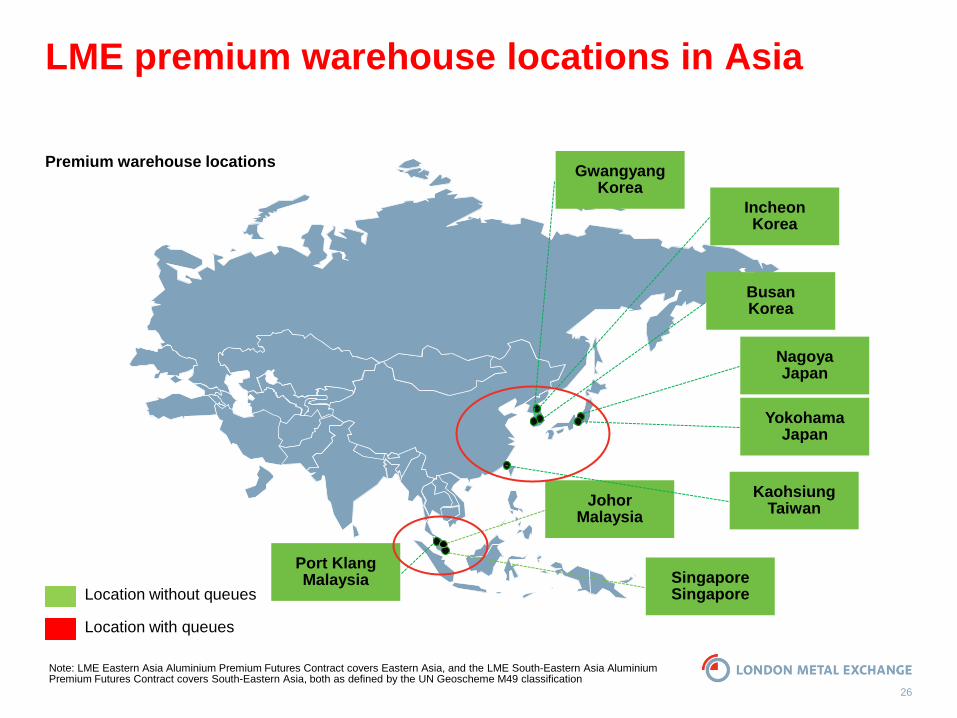

LME premium warehouse locations in Asia

Johor Malaysia

Kaohsiung Taiwan

Port Klang Malaysia Singapore

Singapore

Gwangyang Korea

Incheon Korea

Busan Korea

Location without queues

Location with queues

Note: LME Eastern Asia Aluminium Premium Futures Contract covers Eastern Asia, and the LME South-Eastern Asia Aluminium Premium Futures Contract covers South-Eastern Asia, both as defined by the UN Geoscheme M49 classification

Nagoya Japan

Yokohama Japan

Premium warehouse locations

27

Questions

28

Ring tour

29

Disclaimer

© The London Metal Exchange (the “LME”), 2015. The London Metal Exchange logo is a registered trademark of The London Metal

Exchange.

All rights reserved. All information contained within this document (the “Information”) is provided for reference purposes only. While

the LME endeavours to ensure the accuracy, reliability and completeness of the Information, neither the LME, nor any of its affiliates

makes any warranty or representation, express or implied, or accepts any responsibility or liability for, the accuracy, completeness,

reliability or suitability of the Information for any particular purpose. The LME accepts no liability whatsoever to any person for any loss

or damage arising from any inaccuracy or omission in the Information or from any consequence, decision, action or non-action based

on or in reliance upon the Information. All proposed products described in this document are subject to contract, which may or may

not be entered into, and regulatory approval, which may or may not be given. Some proposals may also be subject to consultation and

therefore may or may not be implemented or may be implemented in a modified form. Following the conclusion of a consultation,

regulatory approval may or may not be given to any proposal put forward. The terms of these proposed products, should they be

launched, may differ from the terms described in this document.

Distribution, redistribution, reproduction, modification or transmission of the Information in whole or in part, in any form or by any

means are strictly prohibited without the prior written permission of the LME.

The Information does not, and is not intended to, constitute investment advice, commentary or a recommendation to make any

investment decision. The LME is not acting for any person to whom it has provided the Information. Persons receiving the

Information are not clients of the LME and accordingly the LME is not responsible for providing any such persons with regulatory or

other protections. All persons in receipt of the Information should obtain independent investment, legal, tax and other relevant advice

before making any decisions based on the Information.

LME contracts may only be offered or sold to United States foreign futures and options customers by firms registered with the

Commodity Futures Trading Commission (CFTC), or firms who are permitted to solicit and accept money from US futures and options

customers for trading on the LME pursuant to CFTC rule 30.10.

29